Stocks fell on Wednesday, a day after Fitch Ratings lowered its U.S. debt ratings to AA+ from the top AAA category, pointing to its growing debt burden and “erosion of governance” over the past two decades. The S&P 500 SPX, -1.38%

fell about 63 points, or 1.4%, ending near 4,513, booking its biggest daily percentage decline since April 25, according to preliminary Dow Jones Market Data. The Dow Jones Industrial Average DJIA, -0.98%

shed about 1%, while the Nasdaq Composite Index COMP, -2.17%

closed 2.2% lower. Stocks already had been taking a breather from their march toward record levels when Fitch on Tuesday evening made good on a threat to downgrade its U.S. debt rating a notch to AA+. Longer-dated Treasury yields rose Wednesday, with the 10-year Treasury rate TMUBMUSD10Y, 4.105%

touching 4.07%, according to FactSet. Treasurys and other haven assets are viewed as likely to benefit from a flight to safety in a scenario where investors get more jittery about the U.S. economic outlook.

As you’ve probably heard by now, Fitch Ratings late Tuesday cut the U.S. federal government’s credit rating to AA+ from AAA.

Here’s a look at what it means for investors and markets:

What’s a credit rating?

A credit rating is an independent assessment of the ability of an organization, including corporations and governments, ranging from school boards to cities, counties, states and countries, that have issued debt to meet their obligations. Fitch — alongside S&P Global and Moody’s Investors Service — is one of the world’s big three ratings firms.

The ratings firms use scales that employ letters, and in Moody’s case also include numbers, to provide a guide to creditworthiness. At the top of the list is the AAA rating from S&P and Fitch, or Aaa, in the case of Moody’s. AA+ is the second-highest rating.

Ratings that employ Cs are at the bottom of the scales, with Fitch and S&P using D ratings in cases of default or bankruptcy.

Any rating below BBB- from Fitch and S&P, or Baa from Moody’s, is considered below “investment grade.” Such debt is often termed “junk.”

Why did the U.S. rating get cut

Fitch had warned in May that a cut was possible, with the ratings firm expressing dismay over what it termed another round of “brinkmanship” around the U.S. government’s debt ceiling. The warning came amid a battle between congressional Republicans and the Biden administration over lifting or suspending the federal government’s debt ceiling.

The limit has been a frequent source of political squabbling. While the showdown was resolved with a two-year suspension of the limit, the battle underlined the high stakes. Failure to reach a deal could have led to a default. In Tuesday’s decision, Fitch said that the past two decades have seen “a steady deterioration in standards of governance” in the U.S., the debt-ceiling agreement notwithstanding.

How does the U.S. rating stack up to other countries

Fitch isn’t the first of the big three ratings firms to strip the U.S. of its AAA rating. S&P did so in 2011, amid an earlier debt-limit battle. That leaves Moody’s as the only firm to still assign the U.S. its top rating.

The pool of triple-A sovereign ratings, meanwhile, continues to dwindle. Only a handful of countries carry triple-A ratings across the board from all three ratings firms.

The cut isn’t seen having much lasting effect on investor demand for U.S. Treasurys. The market for Treasurys is the largest and most liquid debt market in the world. Despite the lack of triple-A ratings, Treasurys are viewed and treated by investors as being virtually “risk-free,” or equivalent to cash. Other types of debt are often quoted in terms of the yield premium, or spread, demanded by investors to hold them over Treasurys.

That isn’t going to change overnight. Analysts have emphasized that investors don’t buy Treasurys based on the credit rating. And any outflows from funds that are required to hold only triple-A rated bonds are expected to be limited.

“Many major Treasury holders, such as funds and index trackers, have already prepared for the move by changing mandates to specifically refer to Treasurys rather than AAA credit, and are unlikely to be forced into selling given the importance of the asset class,” said Solita Marcelli, chief investment officer for the Americas at UBS Global Wealth Management, in a Wednesday note.

How are markets reacting?

The downgrade was blamed for a weak tone across global equity markets, with U.S. stocks following suit. The Dow Jones Industrial Average DJIA

dropped around 315 points, or 0.9%, while the S&P 500 SPX

shed 1.3%. The moves come after a strong run of gains, however.

Treasury yields, which move opposite to price, were higher. The selling, however, took hold only after data from ADP that showed a stronger-than-expected rise in private-sector payrolls. Treasurys took the downgrade in stride in earlier trading, with yields moving lower.

The yield on the 10-year Treasury note BX:TMUBMUSD10Y

was up around 2 basis points near 4.02%.

Marcelli recalled that in 2011 the yield on the 10-year U.S. Treasury fell around 50 basis points, or half a percentage point, in the three days after the S&P downgrade to 2.6% on Aug. 5. Even 15 trading days later, yields were still down 40 basis points from the day of the downgrade, and around 80 basis points lower compared with where they were 15 trading days before the move.

Fitch Ratings cut its top U.S. credit rating to AA+ from AAA on Tuesday, pointing to “erosion” of governance and the nation’s expected fiscal deterioration over the next three years.

Fitch said eroding governance in the U.S. over the past two decades was among the factors for its downgrade, in a Tuesday evening statement. It also said it expected the general government deficit to climb to 6.3% of gross domestic product in 2023, from 3.7% in 2022, on weaker federal revenues, new spending initiatives and a higher interest burden.

“In Fitch’s view, there has been a steady deterioration in standards of governance over the last 20 years, including on fiscal and debt matters, notwithstanding the June bipartisan agreement to suspend the debt limit until January 2025,” Fitch said.

“The repeated debt-limit political standoffs and last-minute resolutions have eroded confidence in fiscal management. In addition, the government lacks a medium-term fiscal framework, unlike most peers, and has a complex budgeting process.”

Fitch warned in May that it might cut the U.S.’s AAA ratings as the latest debt-ceiling fight was dragging on for months without a resolution.

Borrowing costs have climbed as the Treasury Department has unleashed a flood of Treasury issuance since its June debt-ceiling deal to restock it coffers. The 1-month Treasury yield was at 5.36% on Tuesday, while auctions of other Treasury bills maturing in one year often kick off yields north of 5%.

Stocks ended trade Tuesday nearing record levels, with the Dow Jones Industrial Average DJIA, +0.20%

and S&P 500 index SPX, -0.27%

both less than 5% off their highest closing levels from early 2022.

Just a day after the Treasury Department released a $1 trillion borrowing estimate for the third quarter, questions are being raised about the extent to which foreign and domestic buyers can continue to keep up their demand for U.S. government debt.

Further details about Treasury’s financing need will be released at 8:30 a.m. on Wednesday. For now, the $1 trillion estimate, the largest ever for the July-September period, has analysts concluding that the U.S. is facing a deteriorating fiscal deficit outlook and continuing pressure to borrow.

At stake for the broader fixed-income market is whether the presence of large ongoing auctions over the coming quarter and beyond will lead to a prolonged period where demand from potential buyers might begin to dry up, Treasury yields edge higher, and the government-debt market returns to some form of illiquidity.

“You can make the argument that since 2020, with the onset of Covid, that Treasury issuances have been met with reasonably good demand,” said Thomas Simons, an economist at Jefferies JEF, -1.75%.

“But as we go forward and further away from that period of time, it’s hard to see where that same flow of dollars can come from. We may be looking at recent history and drawing too much of a conclusion that this borrowing need will be easily met.”

Simons said in a phone interview Tuesday that “the risk is that you don’t get continued demand from foreign or domestic buyers of fixed income.” The result could be “six to nine months where the market is fatigued by bigger auction sizes, Treasurys become more and more difficult to trade, there’s a grind higher in yields, and there may be issues with liquidity where markets may not be so deep.” Still, he expects such a period, if there is one, to be less acute than what was seen in the 2013 taper tantrum or last year’s volatility in the U.K. bond market.

On Monday, the Treasury revealed a $1.007 trillion third-quarter borrowing estimate that was $274 billion higher than what it had expected in May. The estimate — which Simons calls “eye-popping” — assumes an end-of-September cash balance of $650 billion, and has gone up partly because of projections for lower receipts and higher outlays, according to Treasury officials.

Monday’s estimate is the largest ever for the third quarter, though not relative to other parts of the year. In May 2020, a few months after the onset of the COVID-19 pandemic in the U.S., Treasury gave an almost $3 trillion borrowing estimate for the April-June quarter of that year.

For the upcoming fourth quarter, Treasury is now expecting to borrow $852 billion in privately-held net marketable debt, assuming an end-of-December cash balance of $750 billion. According to strategist Jay Barry and others at JPMorgan Chase & Co. JPM, -1.05%,

the third- and fourth-quarter estimates “suggest that, at face value, Treasury continues to expect a wider budget deficit” for the 2023 fiscal year.

As of Tuesday, investors appeared to be less focused on the Treasury’s borrowing needs than on signs of continued strength in the U.S. labor market, which raises the prospect of higher-for-longer interest rates. One- TMUBMUSD01Y, 5.400%

through 30-year Treasury yields TMUBMUSD30Y, 4.100%

were all higher as data showed demand for workers is still strong. Meanwhile, all three major U.S. stock indexes DJIA, +0.05%

COMP, -0.41%

were mostly lower in morning trading.

According to Simons, who the most likely buyers will be at Treasury’s upcoming auctions will depend on where the department decides to focus its issuances. If the focus is on bills, then money-market mutual funds could “move some cash over,” he said. And if it’s on long-duration coupons, it would be “real money” players such as insurers, pension funds, hedge funds and bond funds — though much will rely on inflows from clients “before demand would pick up.”

The bond market is expressing confidence in company cash flows, flashing a sign of support for the stock market’s rally, according to DataTrek Research.

“U.S. corporate bond spreads continue to tighten and are now essentially the same as 2017–2019,” said Nicholas Colas, co-founder of DataTrek Research, in a note emailed Monday. “That is a green light for further stock market gains.”

Declining corporate bond spreads over comparable Treaurys signal rising confidence in future cash flows and earnings, said Colas. Both investment-grade and high-yield bonds have broadly seen their spreads tighten over the past few weeks to average levels seen in 2017–2019, when conditions in the economy were generally good, his note shows.

Investment-grade spreads averaged 1.19 percentage points over Treasurys over that stretch, while junk bonds averaged 3.82 percentage points, according to Colas’s research.

“This was a period of generally good economic conditions and just one hiccup in capital markets, namely when the Fed briefly overreached on rate policy in late 2018,” he said.

This year, investment-grade bond spreads have recently declined to around 1.22 percentage points and those for high-yield debt have narrowed to 3.78%, the DataTrek note said.

“Corporate bond markets continue to mirror equity market confidence” in stable and strengthening company cash flows, Colas said. “This is not only supporting the ongoing rally in large caps, but also helping small caps outperform in July.”

The Russell 2000 index RUT, +1.09%,

which tracks small-cap stocks in the U.S., has climbed 4.9% so far this month, exceeding the S&P 500’s 3% gains over the same period, according to FactSet data. The Russell 2000 has been trailing the S&P 500 in 2023, though, with 12.5% gains so far this year.

Earlier this month, Bespoke Investment Group also pointed to high-yield bonds as the latest indicator confirming the equity market’s rally. The S&P 500, a gauge of U.S. large-cap stocks, has jumped 19.3% this year through Friday.

Citigroup analysts said in a research note on Friday that they raised their 2023 target for the S&P 500 by 600 points to 4,600, while revising up their mid-2024 target to 5,000, from 4,400.

The popular stock-market index SPX, +0.15%

closed Friday at 4,582.23.

The S&P 500 index is on the verge of a fifth straight monthly gain in July. It’s a reality that few on Wall Street expected just eight months ago.

As a result, it seems that one by one, equity analysts at the big banks are issuing mea culpas or tweaking their S&P 500 targets.

With so many reconsidering their assumptions about markets and the economy, one analyst who has been bullish for months sees an opportunity to reflect on what Wall Street got wrong in 2023 — and by doing so, pinpoint potential existential threats to the rally that may lie ahead.

Jawad Mian, a longtime financial markets professional and the founder of Stray Reflections, said professional investors and economists generally underestimated just how resilient U.S. corporations, and U.S. consumers, and the broader U.S. economy would be to higher interest rates. At the same time, they failed to fully appreciate inflation’s ability to boost corporate profits over the long term.

So far, stocks have proved resilient to higher bond yields in 2023, but that doesn’t mean they always will be. Mian believes that rising real yields could eventually push past a “tipping point” that would send U.S. equity valuations sharply lower.

“I think what’s happening is we are collectively discovering how high interest rates can go before the economy breaks,” he said.

“I think the 10-year yield is heading toward 5%. But the nuanced take here is the path higher is not troublesome…however, at some point, we’ll reach a level that’s too much,” Mian added during a phone interview with MarketWatch.

The yield on the 10-year Treasury note TMUBMUSD10Y, 3.962%

stood at 3.955% on Friday.

Past the point of no return

The Federal Reserve pushed its policy interest-rate to its highest level in 22 years earlier this week, and further hikes certainly could push long-dated bond yields higher, Mian said. But the blow that drives markets over the cliff could easily come from somewhere else as well.

For example: Foreign investors, particularly those in Japan, could choose to dump U.S. Treasurys now that they’re being enticed by more attractive yields back home.

Investors received a small taste of what this might look like on Thursday afternoon when a headline about the Bank of Japan’s plans to loosen its grip on its government bond market sent the yield on the 30-year Treasury bond TMUBMUSD30Y, 4.021%

north of 4%, sparking a selloff in stocks that led to the Dow Jones Industrial Average snapping a 13-day winning streak.

Yields on the 10-year Japanese government bond hit their highest levels since 2014 on Friday after the BOJ confirmed those reports during its July policy meeting.

While it’s important for investors to monitor bond-market threats like this, yields don’t exist in a vacuum. Corporate earnings are another important piece of the puzzle.

Higher yields make bonds more attractive to investors, helping to dim the appeal of stocks, but they also increase borrowing costs for corporations, potentially cutting into profits and pushing companies to lay off employees or enact other belt-tightening measures.

The more pressure companies face from rising borrowing costs, they more likely they’ll need to take more cost-cutting measures like laying off employees.

“Generally speaking, if yields move higher that should put downward pressure on multiples. That’s a risk to the stock market for sure,” said James St. Aubin, chief investment officer for Sierra Investment Management, during a phone interview with MarketWatch.

For now at least, it looks like stocks could continue to ride this wave of momentum higher, even if valuations are looking somewhat stretched relative to recent history already, St. Aubin said. For this to continue though, corporate earnings will need to keep pace with increasingly optimistic expectations.

Already, stock valuations are looking lofty based on the price-to-earnings ratio, one of Wall Street’s favorite metrics for determining how expensive or cheap the market looks.

The forward 12-month price-to-earnings ratio for the S&P 500 index currently stands at 19.4. That’s already higher than the five-year average of 18.6, and the 10-year average of 17.4, according to FactSet data.

Right now, investors are willing to tolerate this because they expect corporate profits to grow substantially in the years ahead, even though profits are expected to contract by 7% in the quarter ended in June, bringing the stretch of negative earnings growth to a third straight quarter.

But in 2024, year-over-year earnings growth is expected to swell to 12.6%. If companies meet, or surpass, these expectations, stocks will likely hold on to their gains, if not continue to climb, St. Aubin said.

However, should earnings growth disappoint, a painful market reckoning might follow.

Since the start of 2023, U.S. stocks have nearly erased all of their losses from 2022, which was the worst year for stock-market performance since 2008, while bonds saw their biggest declines in decades as yields soared driven by inflation and the Federal Reserve’s aggressive interest-rate hikes. Since Jan. 1, the S&P 500 SPX, +0.99%

has risen 19.3% to 4,582.23, according to FactSet.

The Nasdaq Composite COMP, +1.90%

has risen 36.8% to 14,316, while the Dow Jones Industrial Average DJIA, +0.50%

is up 7%.

Worries about a possible policy tweak by the Bank of Japan threw a wet blanket on a stretched U.S. stock-market rally Thursday, with the Dow Jones Industrial Average snapping its longest winning streak since 1987 after the 10-year Treasury yield surged back above the 4% level.

The Japanese yen also strengthened after a news report said policy makers on Friday would discuss a possible tweak to the Bank of Japan’s so-called yield-curve control policy that would loosen the cap on long-dated government bond yields.

Nikkei, without citing sources, reported that BOJ officials would talk about the matter at Friday’s policy meeting and that the potential change would allow the yield on the 10-year Japanese government bond TMBMKJP-10Y, 0.440%

to trade above its cap of 0.5% “to some degree.”

‘Ultimate fear’

Why is that a negative for U.S. Treasurys and, in turn, U.S. stocks?

The “ultimate fear” is that Japanese investors, who have vast holdings of U.S. fixed income, including Treasury notes and other securities, “begin to see a higher level of yields in their own backyard,” Torsten Slok, chief economist at Apollo Global Management, told MarketWatch in a phone interview. That could prompt heavy liquidation of those U.S. positions as investors repatriate holdings to reinvest the proceeds at home.

That dynamic explains the knee-jerk reaction that saw the 10-year U.S. Treasury yield TMUBMUSD10Y, 4.004%

surge more than 16 basis points to end above 4%, he said. Yields rise as debt prices fall.

The surge in yields, in turn, saw stocks give up early gains, with U.S. indexes ending lower across the board.

What is yield curve control?

The Bank of Japan began implementing yield curve control, or YCC, in 2016, a policy that aims to keep government bond yields low while ensuring an upward-sloping yield curve. Under YCC, the BOJ buys whatever amount of JGBs is necessary to ensure the 10-year yield remains below 0.5%.

Nikkei said a possible tweak would allow gradual increases in the yield above 0.5%, but would clamp down on any sudden spikes, allowing the BOJ to rein in fluctuations driven by speculators.

Global market participants are sensitive to changes in YCC. The BOJ sent shock waves through markets in December when it lifted the cap from 0.25% to 0.5%. Investors were rattled by the prospect of the Bank of Japan giving up its role as the remaining low-rate anchor among major central banks.

BOJ Gov. Kazuo Ueda in May said the bank would start shrinking its balance sheet and end its yield-curve control policy if a 2% inflation looks achievable and sustainable after many years of undershooting.

Yen rallies

The yield on the 10-year JGB has traded above 0.4%, but remained below the 0.5% cap. Continued interest rate rises by the Federal Reserve and other major central banks in the past year have raised worries that the 10-year JGB yield could test the limit, Nikkei reported. Those rate hikes, meanwhile, have added pressure to the yen, whose weakness is seen contributing to inflation pressures.

The yen USDJPY, -0.02%

strengthened following the report. The U.S. dollar was off 0.5% versus the currency, fetching 139.48 yen.

The Dow Jones Industrial Average DJIA, -0.67%

ended the day down nearly 240 points, or 0.7%, snapping a 13-day winning streak, while the S&P 500 SPX, -0.64%

declined 0.6% and the Nasdaq Composite COMP, -0.55%

lost 0.5%.

Japanese stocks have solidly outpaced strong gains for U.S. equities in 2023, with the Nikkei 225 NIK, +0.68%

up 26% so far this year versus an 18.7% rise for the S&P 500.

Investors are waiting to see what the Bank of Japan actually has to say.

While the Nikkei report helped “exaggerate” a selloff in Treasurys, the market may be inoculated against bigger swings after the BOJ’s December adjustment to the rate band, said Ian Lyngen and Benjamin Jeffery, rates strategists at BMO Capital Markets, in a note.

The analysts said they expect that “the magnitude of the follow through repricing in U.S. rates will be comparatively more contained than would otherwise be expected.”

More recently, the weak yen has raised the cost of hedging long Treasury positions for Japanese investors. So a stronger yen resulting from a shift toward tighter policy would help make hedging costs for owning Treasurys less onerous for Japanese investors as well, Lyngen and Jeffery wrote, “which over the longer term may begin to make Treasurys more attractive to Japanese buyers and add to the list of sources for duration demand.”

That could make U.S. debt more attractive to new Japanese buyers, Slok agreed.

But that’s oveshadowed by the near-term worry, Slok said, that existing Japanese investors will be inclined to sell Treasurys. Flow data will be very much in focus if the Bank of Japan follows through on the apparent trial balloon floated in the Nikkei report.

Investors will be watching, he said, to see “if the train is leaving the station.”

Former Federal Reserve Vice Chair Richard Clarida on Thursday said he thinks another interest-rate hike this year would be a wise move by the U.S. central bank.

In an interview on Bloomberg, Clarida said the biggest risk for the Fed is to declare “mission accomplished” too early and having to restart rate hikes next year.

“So if I were there, it would skew me to getting in that additional hike this year, and I think some members of the Fed will see it that way,” Clarida said.

Fed Chair Jerome Powell said Wednesday that the Fed will decide what to do about interest rates on a “meeting-by-meeting” basis.

Read: Fed no longer foresees a U.S. recession, highlights from Powell presser

The Fed is forecasting that the unemployment rate will rise to 4.5% by the end of 2024 from 3.6% in June.

That is still a forecast for recession because under the Sahm rule, created by former top Fed staffer Claudia Sahm, the start of a recession is signaled when the three-month moving average on the unemployment rate rises by 0.5 percentage points or more from its low during the past year.

But Clarida said the Fed faces an alternative scenario where inflation picks up again early next year after slowing later this year.

“If the Fed finds itself in March of 2024 with an unemployment rate of 4% and and inflation rate of 4% with some of that temporary good news [on inflation] behind them, they’re in a very tough spot,” he said.

“I do think that’s a risk. It’s not the base case,” he said.

The Dow Industrial Average DJIA, -0.61%

was trading slightly lower on Thursday after 13 straight sessions in the green.

The yield on the 10-year Treasury yield TMUBMUSD10Y, 4.016%

has risen to 3.97%, the highest level in two weeks.

U.S. stocks closed higher, with the Dow posting its longest win streak in over six years, according to Dow Jones Market Data. The Dow Jones Industrial Average DJIA, +0.52%

gained about 184 points, or 0.5%, ending near 35,411, according to preliminary FactSet data. With 11 straight sessions of gains, it was the blue-chip gauge’s longest streak of win since Feb. 27, 2017, according to Dow Jones Market Data. The S&P 500 index SPX, +0.40%

advanced 0.4%, with the energy sector leading the way higher, and the Nasdaq Composite Index COMP, +0.19%

ended up 0.2%. Stocks have been charging higher in 2023 despite the dramatic pace of rate hikes from the Federal Reserve since last year. Focus is on Wednesday’s Fed rate decision, with U.S. central bankers expected to raise rates by another 25 basis points to a 5.25%-5.5% range, potentially marking the last in this cycle as its inflation fight appears to be pay off. Energy prices rose Monday, with U.S. West Texas Intermediate crude for September CL00, +0.13%

delivery ending at $78.74 a barrel, the highest for a front-month contract in three months, according to Dow Jones Market Data.

Late on Wednesday, Tesla Inc. TSLA, -1.10%

reported that quarterly sales were up 47% from a year earlier. But the stock tumbled 10% on Thursday.

Tesla’s shares are still up 113% this year. The company is among a group of 13 in the S&P 500 that stand out with high growth expectations for sales, earnings and free cash flow through 2025.

But less than half of analysts polled by FactSet rate Tesla a buy. Emily Bary explains what they are worried about.

Chipotle Mexican Grill is among 14 stocks named by Michael Brush for consideration by investors looking to ride along with long-term improvement of U.S. labor productivity.

AP

The S&P 500 SPX, +0.03%

has returned 19% this year, following its 18% decline in 2022. On the same basis, with dividends reinvested, the benchmark index is still down 2% since the end of 2021.

The Dow Jones Industrial Average DJIA, +0.01%

is up 6% this year. The venerable index has trailed the S&P 500, but its closing level of 35,255.18 on Thursday was only 4% shy of its record close a 36,799.65 on Jan. 4, 2022. Joseph Adinolfi explains Dow Theory, which according to technical analysts is sending a strong bullish signal for the stock market.

Even if you have resisted the idea of a Roth IRA, you may soon be forced to have one

This year if you are age 50 or older and are already maxing-out your contribution to a 401(K), 403(B) or other qualified employer-sponsored tax-deferred retirement plan at $22,500, you can make an additional “catch up” tax deductible contribution of $7,500 for a total of $30,000. But starting in 2024, the catch up contribution will no longer be tax deductible if you earn at least $145,000 a year. You can still make the contribution with after-tax money into a Roth 401(K) account that your plan administrator may already have set up for you.

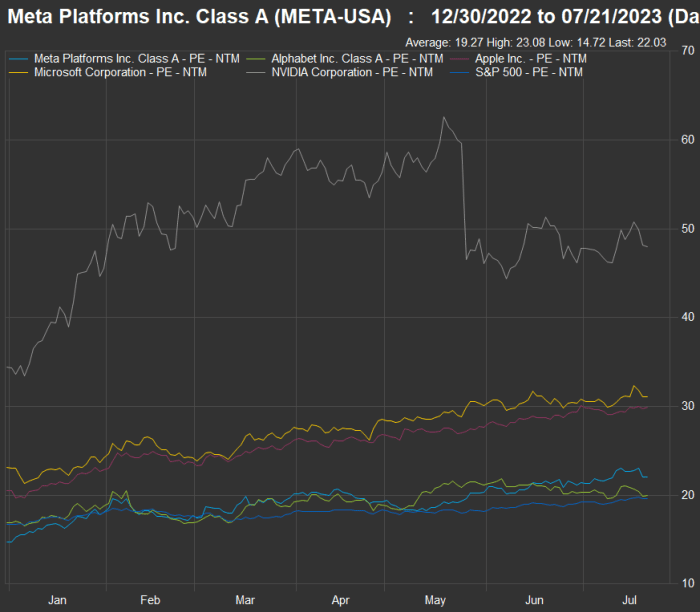

Shares of Meta Platforms Inc. and Alphabet Inc. trade only slightly higher than the S&P 500 on a forward price-to-earnings bases, while Nvidia Corp., Microsoft Corp. and Apple Inc. trade much higher.

FactSet

Leslie Albrecht looks at Meta Platforms Inc. META, -2.73%,

which is Facebook’s holding company and has a hit on its hands with the new Threads social-media platform, and Google holding company Alphabet Inc. GOOGL, +0.69%,

to consider which stock is a better buy.

In The Ratings Game column, MarketWatch reporters track analysts’ thoughts about various stocks. Here’s a sampling of this week’s coverage:

You don’t know every bad factor causing air travel to be nothing but harassment

Getting there is half the fun.

Getty Images

The U.S. flying scene — from shortages of equipment and labor (and runways) to ill-staffed air-traffic control towers — is a well-known nightmare for U.S. travelers. But there is more to the story. Jeremy Binckes looks into other factors that may surprise you and cause great inconvenience this summer.

The Federal Reserve is expected to raise interest rates again next week

The Federal Open Market Committee will meet next Tuesday and Wednesday, to be immediately followed by a policy announcement. Economists expect the central to raise the federal-funds rate by another quarter point. The question is whether or not this will end the Fed’s inflation-fighting rate cycle.

How much would you pay for 100% downside protection in the stock market?

MarketWatch illustration/iStockphoto

Over the past 30 years, the SPDR S&P 500 ETF Trust SPY,

has returned 1,650%, for an average annual return of 10%, with dividends reinvested, according to FactSet. But it hasn’t been a smooth ride. The ETF, which tracks the benchmark S&P 500, fell 18% last year and 37% during 2008, for example. And there have been even larger declines if the analysis isn’t confined to calendar years.

But can you ride through market declines? Many studies have shown that most investors who try to time the market sell after a decline has started and buy back in well after a recovery is under way, which means their long-term performance can suffer significantly.

In this week’s ETF Wrap column (and emailed newsletter), Isabel Wang describes a new buffered fund that can give you 100% downside protection over a two-year period, in return for a cap on your potential gains in the stock market. Here’s the price you would pay for the protection.

The World Cup games have started

Hannah Wilkinson scored the home team’s first goal against Norway during the first World Cup game in Auckland, New Zealand, on July 20.

Getty Images

The Women’s World Cup began Thursday with an upset victory by New Zealand over Norway.

James Rogers reports on what is expected to be a much easier environment for FIFA and corporate sponsors than that of last year’s Men’s World Cup in Qatar.

U.S. Soccer Federation President Cindy Parlow Cone participated in MarketWatch’s Best New Ideas in Money podcast and spoke about the long-term effort to achieve equal treatment for women soccer players.

More coverage of the World Cup:

Want more from MarketWatch? Sign up for this and other newsletters to get the latest news and advice on personal finance and investing.

Within one month Santosh Kol, an aspirant for government jobs in India, lost in betting apps the entire 40,000 rupees ($489) that his father had sent him in March to pay for his tuition.

Kol’s father, a construction labourer in Sidhi district in the central Indian state of Madhya Pradesh, had borrowed the money from the community leaders in his village to pay for the coaching classes where his son was enrolled to prepare for national competitive exams for government jobs. Kol, 25, said that one of his friends suggested he bet on these apps, which offer the opportunity to earn large sums of money. Initially, he won a few thousand rupees but then became greedy and lost everything.

Kol’s name has been changed to protect his identity.

Kol, who lives in a one-room apartment with books scattered everywhere and a small kitchen in one corner, told Al Jazeera that he was hoping to win money from his betting and return it to the village elders.

He said, “My family is extremely poor. They somehow managed to gather this much money for my fees. I thought I would win money in this app and return his money. However, when I invested my money in these apps, I lost it. Now, I am getting suicidal thoughts” because he is worried about how he will return the money, he said.

Kol is not the only one who is addicted to these apps.

Prateek Kumar, a 16-year-old teen from the same area and an ardent cricket fan has developed a habit of betting on fantasy gaming apps.

His father Lalji Dwivedi is a small farmer and earns about 6,000 to 7,000 rupees ($73 to $85) a month. He told Al Jazeera that his son is hooked on cricket and watches all the matches of the Indian Premier League (IPL), cricket’s most lucrative domestic tournament and which counts some of these gaming apps as its sponsors. Dwivedi blames the ads for luring his son into the gaming world.

“He got influenced by an advertisement during the breaks, and he started using fantasy gaming apps to bet every day,” Dwivedi said. “Now, before each match, he asks me to give him money to bet on these apps. When I refuse to give him money, he gets upset.”

Fantasy gaming apps have exploded in popularity in India in recent years [Anil Kumar Tiwari/Al Jazeera]

In recent years, fantasy gaming apps have exploded in popularity in India, with millions of users joining platforms such as Dream11, My11Circle and MPL, among others. These apps offer users the chance to create virtual teams of real-life athletes and compete against others based on the performance of these athletes, with the chance to win cash prizes or other rewards.

However, the lack of regulatory authority and the massive advertising campaigns by these platforms have led to concerns about the addictive nature of these apps and the potential harm they can cause to users, particularly children and vulnerable individuals.

Prateek’s favourite apps are Dream11 and My11Circle, his father said. They require a user to be 18 years old to be able to play, but that hasn’t deterred Prateek who used his father’s ID to sign up on both apps.

Al Jazeera’s emails to Dream11, My11Circle and the industry body the Federation of Indian Fantasy Sports, went unanswered.

Dwivedi told Al Jazeera that initially, Prateek used to bet between 50 to 100 rupees ($0.60 to $1.20). However, now he creates two to three teams and ends up losing an average of 300 to 400 rupees ($3.70 to $4.90) – money from the family’s savings and from his mother’s earnings as an agricultural labourer – on most days.

“I don’t earn enough money to feed my family. If my son keeps losing this much money, I don’t know how we will manage to survive,” said Dwivedi, adding that he has tried to deny his son the money but as the teen gets agitated, he gives in to his demands.

He added, “I am deeply concerned about my son’s behaviour, which has left me feeling anxious and helpless.”

Massive advertising by fantasy apps

Fantasy gaming apps were the top advertisers on television during IPL-16, which ended in late May, with 18 percent of the advertising share, up from 15 percent in the previous IPL, according to a TAM advertising report.

The apps use famous cricket players including Saurav Ganguly, Virat Kohli, Shubman Gill, Hardik Pandya, as well popular actors like Aamir Khan, R Madhavan, Sharman Joshi and others to endorse them.

As per a report by consultancy RedSeer, the income of fantasy gaming platforms increased by 24 percent during the IPL cricket matches from 2022 to 2023, reaching over 28 billion rupees ($341m). Around 61 million users took part in fantasy gaming activities, nearly 65 percent of who came from small towns.

These gaming apps require an entry fee to participate, and there is a risk of losing money if the team underperforms. Dream11, the largest fantasy sports platform in India, boasts over 180 million users. MPL claims to have 90 million users, and My11Circle claims to have 40 million users.

Santosh Kol planning his fantasy team as he bets money [Anil Kumar Tiwari/Al Jazeera]

The great debate: Game of skill or chance?

Shashank Tiwari, a lawyer at Jabalpur High Court, said that in India, the law for controlling fantasy gaming apps is mainly based on the Public Gambling Act of 1867. This law forbids all types of gambling in the country, except for certain games that involve skill, including bridge and chess. He added that ads for these apps can be misleading because they show people winning a lot of money, but in reality, most players only win a small amount.

Nikkhhil Jethwa, a technology expert and a lawyer, said that if we consider a game as a game of skill, then we must comprehend that the app algorithm controls the entire game, which is synchronised in such a way that the company generates more profit than the players. If a game is classified as a skill game, it should include analytics, statistics, or data studies. Assumption-based decisions cannot be considered skilful.

In India, games requiring a substantial amount of skill can be played for money without being classified as gambling. However, the absence of a standardised set of laws across all states has resulted in difficulties in regulating fantasy gaming apps in the country. For now, certain states have legalised and regulated online gaming, whereas a handful of others have completely prohibited it.

‘Need Uniform law’

Last year in January, Madhya Pradesh – Santosh Kol and Prateek Kumar’s home state – said it would bring in a new law to regulate online gaming. Home Affairs Minister Narottam Mishra made the announcement after an 11-year-old boy died allegedly by suicide. The boy, according to local media reports, was addicted to online gaming apps and had spent 6,000 rupees ($73) on them without his parents’ knowledge. In December, the state set up a task force to study the technical, legal and other aspects of banning online gambling. It is yet to submit its report.

While Indian law has some provisions – such as the Juvenile Justice Act of 2015, to protect, care for and help rehabilitate children who need it, and the Information Technology Rules of 2021, which require intermediaries to make sure that minors are kept safe from harmful content – these laws are “insufficient in effectively addressing the extensive psychological repercussions, especially the detrimental effects on minors”, lawyer Tiwari said. Instead of piecemeal measures, “a uniform national law to regulate these apps could help to create clarity and consistency in the legal landscape”, he added.

Lalji Dwivedi (left) is worried that his son Prateek Kumar (right) is addicted to these gaming apps [Anil Kumar Tiwari/Al Jazeera]

Surge in addiction treatment seekers

In 2014, the National Institute of Mental Health and Neuro-Sciences (NIMHANS) in Bengaluru, India, started the Service for Healthy Use of Technology, or SHUT Clinic. It is India’s first clinic that deals exclusively with mental health problems related to technology use. At the time, the clinic used to get about three to four patients with gaming addictions per week. That number has now shot up to about 20 to 22 individuals seeking help per week, Dr Manoj Sharma, professor of clinical psychology and head of the SHUT Clinic, told Al Jazeera.

According to Dr Sharma, some students are treating these apps as the equivalent of their education, which, he said, is “a worrying trend”. They believe that if they continue to use these apps, they will earn a significant amount of money and recover their losses. This kind of thinking can lead to addiction to these gaming apps, he said.

Most addicted individuals do not acknowledge that they have developed an obsession with these apps, he added. Many parents bring their children to the clinic for treatment, but it takes a considerable amount of time for the children to admit that they are addicted to such apps.

According to Jethwa, fantasy games should not involve money. Instead, the winner should be awarded points so that only individuals with a genuine interest in gaming will participate.

Dr Sharma suggested that instead of focusing on imposing stricter laws, it is crucial to establish forums in smaller cities to create public health awareness about the mental health issues caused by these apps.

High tax

The Indian government declared on July 11 that it will impose a 28 percent tax on online gaming, which analysts expect will be collected from customers who will now have to pay higher fees.

Anirudh Tagat, a research author at the Department of Economics at Monk Prayogshala, a nonprofit research organisation, said the government is treating online games similar to cigarettes and alcohol, hoping that the high taxes will make people not want to play them.

Tagat said, “The government wants to make it more expensive to play these games so that people will stop playing them. But I don’t think people will actually stop playing just because of the high taxes.”

He added, “These apps use different strategies to get people to play and spend money on them. Even if they have to pay a lot of taxes, these apps will still continue to be popular in the long run.”

U.S. stocks finished at new highs for the year on Monday to kick off a busy week for corporate earnings, with the Nasdaq leading the way up. The Dow Jones Industrial Average DJIA, +0.22%

rose about 76 points, or 0.2%, ending near 34,585, based on preliminary FactSet data. The S&P 500 index SPX, +0.39%

gained 0.4% and the Nasdaq Composite Index COMP, +0.93%

closed up 0.9%. That was the Dow’s sixth straight day of wins and marked the highest close since April 2022 for all three major stock indexes, according to Dow Jones Market Data. Equities have rallied as the U.S. economy remains resilient in the face of sharply higher interest rates, keeping investors hopeful about a soft landing, instead of a recession. Treasury Secretary Janet Yellen said on Monday that she doesn’t anticipate a U.S. recession, in an interview with Bloomberg television. After several big banks reported on Friday, second-quarter earnings results continue with Tesla, TSLA, +3.20%

Morgan Stanley MS, +0.69%,

Goldman Sachs GS, +0.31%,

Netflix NFLX, +1.84%

and more on deck.

The numbers: Commercial and industrial loans — a key economic driver — held roughly steady in the week ending July 5, the Federal Reserve said Friday. Loans rose $200 million to $2.754 trillion, the central bank said.

Bank lending has been slowly decelerating, falling for three straight months. C&I loans hit a peak of $2.82 trillion in mid-March, right before the collapse of Silicon Valley Bank.

Uncredited

Key details: Total bank deposits rose by $24.9 million to $17.367 trillion in the same week. Deposits have been shrinking slowly. They peaked at $18. 21 billion in mid-April.

Big picture: In the wake of the collapse of Silicon Valley Bank in March, economists have been watching the data carefully for signs of a credit crunch, as banks have weak balance sheets as a result of the Fed’s swift increases in interest rates since March 2022.

San Francisco Fed President Mary Daly said Monday she hadn’t seen credit tightening that is in excess of normal.

“I do think, from research literature, that this takes a while to show itself, and so I think we are still looking into the fall before we would have a declarative statement to make about the extent of credit tightening and the impact on the economy,” Daly said.

The numbers: The University of Michigan’s gauge of consumer sentiment rose to a preliminary July reading of 72.6 from a June reading of 64.4. It is the largest gain since December 2005. Sentiment is at its highest level since September 2021.

Economists polled by the Wall Street Journal had expected a June reading of 65.5.

However, Americans’ expectations for overall inflation over the next year rose to 3.4% in July from 3.3% in the prior month. Expectations for inflation over the next 5 years ticked up to 3.1% from 3% in June.

Key details: According to the UMich report, a gauge of consumers’ views on current conditions jumped to 77.5 in July from 69 in the prior month, while a barometer of their expectations rose to 69.4 from 61.5.

Big picture: Sentiment is improving as gasoline prices have held steady this summer. Low unemployment is also playing a role.

What are they saying? “The good news is that sentiment has roughly retraced half of its fall from pre-pandemic levels. For most Americans, a modest gain in income is expected. Still, durable goods buying conditions remain far off their recent levels. The rise in confidence seems restrained, and clouds concern about the forecasted economic downturn which continues to linger,” said Scott Murray, economist at Nationwide, in a note to clients.

Federal Reserve Board Gov. Christopher Waller said Thursday he was not swayed by June’s benign consumer inflation data, and said he wants the central bank to go ahead with two more 25-basis-point rate hikes this year.

“I see two more 25-basis-point hikes in the target range over the four remaining meetings this year as necessary to keep inflation moving toward our target,” Waller said in a speech to bond-market experts, known as The Money Marketeers of New York University.

That would bring the Fed’s benchmark rate to a range of 5.5%-5.75%.

Waller said that, while the cooling of CPI data for June was welcome news, “one data points does not make a trend.”

“The report warmed my heart, but I have got to think with my head,” Waller said.

He noted that inflation slowed in the summer of 2021 before rocketing higher.

In his remarks, Waller said he is now more confident that the contagion from the collapse of Silicon Valley Bank in March will not create a significant problem for the economy.

“I see no reason why the first of those two hikes should not occur at our meeting later this month,” he said.

Traders in derivative markets have priced in high odds of a rate hike after the Fed’s meeting in two weeks. But traders have been skeptical the Fed will follow through with a second hike, even before the soft CPI data.

Waller said the timing of the second hike depends on the data.

“If inflation does not continue to show progress and there are no suggestions of a significant slowdown in economic activity, then a second 25-basis-point hike should come sooner rather than later, but that decision is for the future,” he said.

During a question-and-answer session, Waller stressed that September was a “live meeting,” meaning the Fed could hike rates at that time.

Some economists had thought the Fed was moving to an “every-other-meeting” pace of hikes, but Waller said he did not favor such mechanical moves, and that data should be the deciding factor.

Some Fed officials want the central bank to hold rates steady in July, and perhaps through the end of the year, thinking the economy is going to be hit by “lagged” effects from past rate hikes.

Waller said he believes the bulk of the effects from last year’s tightening have passed through the economy already.

“Pausing rates now, because you are waiting for long and variable lags to arrive, may leave you standing on the platform waiting for a train that has already left the station,” he said.

The yield on the 10-year Treasury note TMUBMUSD10Y, 3.786%

has fallen to 3.77% this week after a lower-than-expected gain in jobs in the June report and the cooling of inflation. The yield had hit a recent high of 4.07% ahead of those softer reports.

Stocks rose for a fourth day in a row on Thursday, a day ahead of second-quarter earnings from America’s biggest lenders. The Dow Jones Industrial Average DJIA, +0.14%

rose about 46 points, or 0.1%, ending near 34,394, according to preliminary data from FactSet. But the S&P 500 index SPX, +0.85%

gained 0.9% to end at 4,509, clearing the 4,500 mark for the first time since April 5, 2022 when it ended at 4,545.86, according to Dow Jones Market Data. The Nasdaq Composite Index COMP, +1.58%

scored another blockbuster day, up 1.6%. Investors have been optimistic as inflation pressures ease and as perhaps the best-telegraphed U.S. economic recession in recent history has yet to materialize. The S&P 500 and Nasdaq have been charging higher on buzz about AI technology, with much of this year’s stock-market gains fueled by a small group of stocks. The risk-on tone ahead of earnings from JPMorgan Chase and Co., JPM, +0.49%

Wells Fargo WFC, +1.04%

and Citigroup C, +0.63%,

had the U.S. dollar DXY, -0.74%

earlier on pace to end at its lowest level since early April 2022. Treasury yields also continued to fall, with the 10-year TMUBMUSD10Y, 3.768%

rate back down to 3.759%, after topping 4% in recent weeks. The six biggest banks are expected to issue a deluge of fresh debt after earnings, despite the Federal Reserve having sharply increased rates and borrowing costs for businesses and households to tame inflation.

Markets seem to be embracing the notion of a soft landing for the U.S. economy despite inflation remaining above the Federal Reserve’s 2% target.

“Soft landings are not impossible, but they’re pretty improbable,” said Bob Elliott, co-founder, chief executive officer and chief investment officer at Unlimited Funds, in a phone interview. “They’re particularly challenging in an environment where the labor market is tight,” he said, and yet “many investors are sort of enamored with this idea that we could get a soft landing.”

The U.S. stock market was rising Wednesday after fresh data showed inflation rose in June slightly less than expected. Meanwhile, the unemployment rate remains low in the U.S., with wage growth helping to fuel consumer spending in an economy that grew at a revised 2% annualized pace in the first quarter.

“There’s a race going on between the Fed slowing the economy down, and then on the other side, inflation becoming entrenched,” said Elliott. In that race, the Fed has been “one or two steps behind,” he said, ahead of Wednesday’s inflation reading.

The consumer-price index showed U.S. inflation rose 0.2% in June for a year-over-year rate of 3%, according to a report Wednesday from the Bureau of Labor Statistics. Core CPI, which excludes energy and food prices, increased 0.2% last month for a year-over-year rate of 4.8%. The Bureau of Labor Statistics said core inflation’s rise in June marked the smallest monthly increase since August 2021.

“The Fed will see the June CPI report as progress, but they are still very likely to raise the target rate a quarter percent at their decision in July,” Bill Adams, chief economist for Comerica Bank, said in emailed comments Wednesday. “The Fed would rather overtighten and slow the economy more than necessary than under-tighten and risk inflation accelerating when the economy regains momentum.”

Many investors have been expecting the Fed to hike its benchmark interest rate by a quarter percentage point at its policy meeting later this month, which would bring it to a targeted range of 5.25% to 5.5%. Federal-funds futures on Wednesday pointed to a 92.4% probability of such a rate hike and a slightly more than 80% chance of the Fed then pausing at its next meeting in September, according to CME FedWatch Tool, at last check.

After the expected increase in July, traders in the fed-funds-futures market were on Wednesday largely expecting the Fed to hold rates steady for the rest of the year.

“The bulls get their wish – CPI print came in better than expectations,” said Rhys Williams, chief strategist at Spouting Rock Asset Management, in emailed comments Wednesday. “We think the danger now is that the Federal Reserve does one too many rate increases and the soft landing turns into something harder.”

In Elliott’s view, both the stock and bond markets lately appeared to be embracing the idea of a soft landing for the economy.

The yield on the two-year Treasury note, which recently has been trading below the Fed’s benchmark rate, tumbled after the CPI report was released Wednesday. Two-year yields TMUBMUSD02Y, 4.758%

were down about 16 basis points around midday Wednesday at 4.73%, according to FactSet data.

“As the Fed has moved interest rates to very restrictive levels thus far, and probably will execute another hike or possibly two from here, we think that patience should be a real virtue in their overall disposition toward ongoing monetary policy,” said Rick Rieder, BlackRock’s CIO of global fixed income and head of the firm’s global allocation investment team, in emailed comments Wednesday. “Today’s CPI report for June displayed notable moderation, which is good news for policy makers, markets and households overall.”

U.S. stocks were up Wednesday afternoon, with the S&P 500 SPX, +0.83%

gaining 0.7% while the Dow Jones Industrial Average DJIA, +0.39%

rose 0.4% and the Nasdaq Composite COMP, +1.15%

advanced 0.9%, according to FactSet data, at last check. The stock-market’s fear gauge, the Cboe Volatility index VIX, -7.28%,

was down more than 7% at 13.8 around midday Wednesday.

Fed-funds futures traders continue to price in a better-than-90% probability the Federal Reserve will lift the benchmark interest rate by 25 basis points to a range of 5.25% to 5.5% later this month, while expectations for another quarter-point move in either September or November faded somewhat after a weaker-than-expected rise in June nonfarm payrolls. Fed-funds futures reflect a 92.4% probability of a quarter-point hike on July 26, according to the CME FedWatch tool, little changed from Thursday. The probability of the fed-funds rate rising to 5.5% to 5.75% at the Fed’s September policy meeting fell back to 22.8% Friday morning from 27.5%. For November, the probability was 36.5% versus 40.2% on Thursday.

It didn’t land with the same kind of political explosion as Dobbs. But the Supreme Court’s decision last year in West Virginia v. Environmental Protection Agency was every bit as outrageous: The six-member conservative majority, in handcuffing the EPA’s regulatory authority, had “declared war on governing,” as my colleague Cristian Farias put it at the time—and underscored, for Doug Lindner, the desperate need for judicial reform.

“We decided that that was a step too far,” says Lindner, senior director of judiciary and democracy at the League of Conservation Voters, the influential environmental advocacy group. The Court, he tells me, was “serving the interests of the polluters,” and had not only shifted too far to the right—it had become too powerful.

Lindner is hardly alone in that sentiment; he’s part of a growing recognition on the left that progress in the policy arena could be entirely undermined by an activist, right-wing court that has come to seem less like a judicial body and more like an unelected “superlegislature,” as Democratic representative Ritchie Torresput it last week. That’s why a diverse coalition of advocacy organizations—including the League of Conservation Voters—has banded together recently to form United for Democracy, which hopes to move the needle on Supreme Court reform. Stasha Rhodes, the director of the campaign, acknowledges that “it’s not an easy fight.” The Supreme Court is “broken,” she says, and Democrats can’t fix it right now without the support of the very Republicans who helped break it. But Rhodes tells me that she remains “hopeful that the momentum will turn into something.”

“Issue groups that may have been hesitant to weigh in on the Supreme Court before now understand that they don’t have a choice, because the Supreme Court impacts all of our issues, from pollution and the water we drink to safety in our communities to our most personal health care decisions,” Rhodes says of the effort, which has so far sought to build public pressure on lawmakers to act. “As we start to increase the drumbeat on this issue, and include more people outside of Washington in the conversation, I think we feel really good about our ability to move Congress in a way that they start to take action.”

The campaign—which launched in mid-June, before the conservative majority further undermined the Environmental Protection Agency; struck down Joe Biden’s student loan forgiveness plan and affirmative action in college admissions; and effectively authorized discrimination against LGBTQ+ Americans—includes a number of progressive heavy hitters, including NARAL Pro-Choice America and the Service Employees International Union, one of the largest and most influential unions in the country. The hope, for Rhodes and the groups involved, is that there will be strength in numbers—that these disparate organizations will be able to highlight, for Democratic- and Republican-leaning voters alike, the Court’s “willingness to break those traditional norms, showing that they’re too powerful, too political, and unfit to meet today’s challenges,” Rhodes explains.

“We’re not going to stand by as corrupt justices repeal our fundamental rights,” echoes SEIU president Mary Kay Henry, “while acting like the rules don’t apply to them.”

That could add to the already growing momentum around Supreme Court reform that has built up in the wake of devastating decisions like Dobbs and the conflict of interest scandals that have erupted around Clarence Thomas and Samuel Alito, two stalwarts of the right-wing supermajority. The question now is: How can the campaign best channel that momentum? And will it be enough to actually effect change?

Legal fights have always been instrumental to movements for labor, abortion, gun control, civil rights, and beyond. But Dobbs—which overturned half a century of precedent last year in ending the federal right to an abortion—threw the Supreme Court’s outsize role in those battles into stark relief. It’s as if “there’s this one massive national veto pen, basically, in the Supreme Court, that can change or dictate our rights on a whim,” says Angela Vasquez-Giroux, vice president of communications and research at NARAL Pro-Choice America.

So far, several proposals have gained traction on the left—from adding seats to the bench to imposing stricter, more common-sense ethics and transparency rules—to avoid further politicizing the scandal-plagued court. Even Nancy Pelosi—the former House Speaker who’s often at loggerheads with her progressive flank—has recently come out in favor of term-limiting justices.

But those reforms have hit a brick wall in Washington: Chief Justice John Roberts and his colleagues have brushed off concerns about ethics scandals and partisan rulings; Republicans have accused Democrats of mounting political attacks on the conservative majority; and President Joe Biden has so far refused to embrace major reform, even as he correctly laments that the Roberts court is “not a normal court.”

Still, popular outrage and growing activism around reform over the past year do seem to be having an impact, at least on the Democratic lawmakers who have become more assertive in their calls for Supreme Court overhauls. Meanwhile, some of the most influential issue groups in the country—including Planned Parenthood, which endorsed Supreme Court expansion, term limits, and ethics reform in May—are adding even more fuel to the fire.

Twitter content

This content can also be viewed on the site it originates from.

To be sure, the path forward for reform is very rocky. Public trust in the Supreme Court has been at a historiclow, and that has so far seemed to have little effect on the conservative justices and their Republican defenders, who have made change all but impossible in the current Congress.

Any substantive action, then, will likely depend on Democrats winning back the House, expanding their majority in the Senate, and retaining the presidency in 2024. That’s not impossible: The GOP already suffered the public’s outrage at the Court last cycle, and could pay the price again next fall. But unless and until that happens, the hope for reform will continue to butt up against the reality of a divided Washington. “I wish that Supreme Court ethics weren’t a partisan issue,” Lindner says. “Ethics never should be a partisan issue. But then again, neither should clean air, clean water, or voting rights be partisan issues, and yet here we are.”

There was support from an unspecified number of Federal Reserve officials for an interest rate hike at the central bank’s policy meeting in June, according to a summary of the discussions released Wednesday.

“Some participants indicated that they favored raising the target range for the federal funds rate 25 basis points at this meeting or they could have supported such a proposal,” the minutes of the June 13-14 meeting said.