Stocks closed mostly lower Friday, capping off a bruising week of losses as Treasury yields jumped and China’s mounting property woes gripped investors. The Dow Jones Industrial Average DJIA, +0.07%

rose about 27 points, or 0.1%, ending near 34,501, according to preliminary FactSet data. The S&P 500 index SPX, -0.01%

was nearly flat at 4,370 and the Nasdaq Composite Index COMP, -0.20%

shed 0.2%, despite briefly turning positive late in the session. It still was a tough week for equities, with the Dow booking a 2.2% loss, the S&P 500 index a 2.1% decline and the Nasdaq a 2.6%. The Nasdaq also posted its biggest 3-week decline since December 2022, according to Dow Jones Market Data. Yields on the 10-year Treasury rose for a 5th week in the row, with the benchmark TMUBMUSD10Y, 4.252%

rate briefly touching its highest level since November 2007, before settling back at 4.251% on Friday. China Evergrande’s EGRNF, Chapter 15 bankruptcy filing in New York late Thursday kept focus on the wobbling property market in the world’s second-largest economy. Earlier in the week, Country Garden Group missed a dollar-denominated debt payment. Next week investors will be focused on Federal Reserve Chairman Jerome Powell’s speech on Friday at the Jackson Hole economic summit for hints to whether the central bank is likely done hiking rates in this cycle. The Fed’s policy rate sits at its highest level in 22 years.

The so-called Magnificent Seven grouping of technology stocks lost some of its luster this week after four of the seven moved into correction territory, meaning their stocks have fallen at least 10% from their recent peaks.

The corporate-bond market, in contrast, seems to like all seven names.

One caveat: Tesla has no outstanding bonds. In the past, the electric-car maker issued convertible bonds, but they have all been converted into equity.

The group is credited with helping drive the stock market’s gains in the first half of the year, driven by excitement about artificial intelligence. But the rally has stalled in recent weeks as investors have fretted over the potential for U.S. interest-rate increases, surging Treasury yields and China worries, with property developer Evergrande filing for U.S. bankruptcy protection late Thursday.

On Thursday, Meta followed Apple, Microsoft and Nvidia into correction territory, as MarketWatch’s Emily Bary reported. Tesla, meanwhile, is in a bear market, meaning it’s down more than 20% from its recent peak.

The following series of charts from data-solutions provider BondCliQ Media Services show how many bonds each company has issued by maturity and how they have traded as the stocks have pulled back.

The first chart shows that Microsoft has by far the most bonds, mostly in the 30-year bucket. The software and cloud giant has more than $50 billion in long-term debt, according to its 2023 10-K filing with the Securities and Exchange Commission.

Outstanding Magnificent Seven debt by maturity bucket.

Source: BondCliQ Media Services

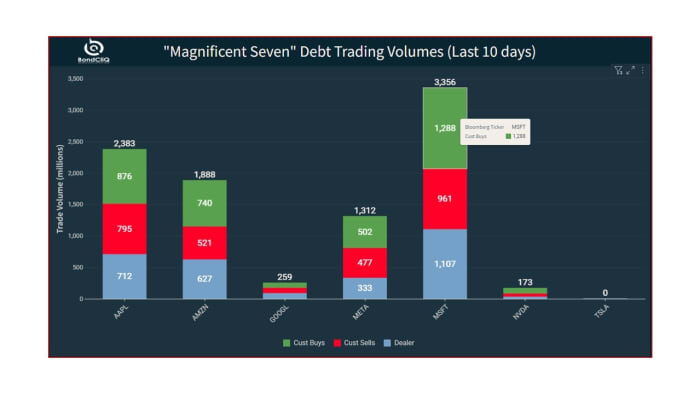

This chart shows trading volumes over the last 10 days, divided by trade type. The green shows customer buying, while the red is customer selling. The blue shows dealer-to-dealer flows. Microsoft, for example, has seen almost $1.3 billion in customer buying from dealers in the last 10 days and $960 million in customer sales to dealers.

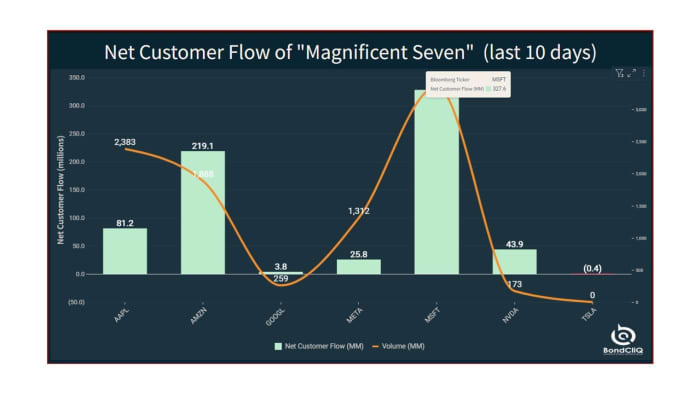

This chart shows that every name in the group has enjoyed better net buying in the last 10 days, with Microsoft leading the way.

Net customer flow of Magnificent Seven debt (last 10 days).

Source: BondCliQ Media Services

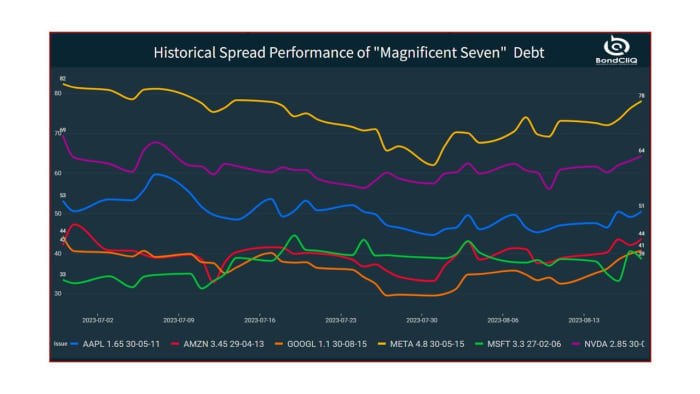

This chart shows spread performance over the last 50 days for an intermediate-term bond from each of the seven issuers. Most have tightened or remained steady over the period.

Historical spread performance of Magnificent Seven debt.

Apple’s stock entered correction Wednesday upon falling more than 10% from its July 31 peak of $196.45. The company sells mainly discretionary products, and right now “consumers are still being pinched” and thinking more carefully about where they spend their money, according to Matt Stucky, senior portfolio manager for equities at Northwestern Mutual Wealth Management.

There is room for a continued selloff in U.S. Treasurys which has already pushed 10- and 30-year yields to their highest levels since 2007 and 2011, according to researchers at Barclays.Though the recent selloff took a breather on Friday, the steady drive higher in long-dated yields which unfolded this week left observers warning that the era of low rates may be firmly behind the U.S. as a new normal appears to take shape in the bond market. Long-term rates yields are just beginning to enter ranges that have been historically consistent with where they traded during the early 2000s.Read: Why Treasury yields keep rising,…

While negative returns might stir bad memories of last year’s shocking losses for bonds, stocks and nearly everything else, investors holding Treasury debt issued at 2023’s higher yields might want to sit back and take stock.

“This is the top thing we hear,” said Ryan Murphy, director of fixed-income business development at Capital Group, of evaporating returns in what’s been a tough August. “You saw the worst bond market in 40 years last year. Investors, they are tired, and feel beaten up.”

Murphy’s message to clients is this: “In bonds, you earn the money over time.” And those dwindling bond returns since January? “Approach it with a deep breath, and know this is going to work out in the end.”

Capital Group’s laid-back style and lack of “a star CEO” earned it recognition by Institutional Investor in March as “a new bond leader” without a king, in large part because it attracted $100 billion in funds over the past five years, or twice the total of its peers.

Recent volatility in interest rates again zapped yearly gains in many bond funds, as Fed officials continued to warn that a roaring labor market and robust spending could keep inflation from receding to the central bank’s 2% annual target.

The spike in long-term bond yields makes older, lower-yielding securities look comparatively less attractive. That’s reflected in the yearly return on a key Bloomberg U.S. government bond and note index, which turned negative for the first time since March (see chart), when several regional banks failed, stoking fears of a broader banking crisis.

Returns on U.S. government bonds turn negative for the year.

FactSet

However, a look back at August 2022 shows the 10-year Treasury yield starting around 2.6%, according to FactSet.

By contrast, Treasury bill yields BX:TMUBMUSD06M

neared 5.5% on Thursday, or “north of anything we’ve seen over the past 15 years,” Murphy said. And for investors looking to lock in longer-term yields, the 10-year Treasury rate BX:TMUBMUSD10Y

touched 4.307% on Thursday, its highest level since November 2007, according to Dow Jones Market Data.

“It’s becoming more expensive for the government and companies to finance debt because of the rapid climb in rates,” Murphy said of the drag of higher long-term interest rates.

On the flip side, it’s also been one of the best stretches for lenders and bond investors in terms of getting paid to act as creditors since the 2007-2008 global financial crisis, but without a U.S. recession — or at least not yet.

What’s also different from last year is that the Fed already jacked up interest rates to a 22-year high of 5.25%-5.5% in July, and has signaled it’s likely nearly finished with hikes in this cycle.

Record cash on the sidelines

Murphy pointed to a mountain of cash on the sidelines, in the form of assets in money-market funds, as another potential stabilizer for markets.

Assets in money-market funds hit a record $5.57 trillion for the week ending Wednesday, according to data from the Investment Company Institute.

“What’s really interesting is that there’s been two bursts of investors going into money-market funds. There was a big shift right at the onset of COVID, and another burst over the past 12-18 months since the beginning of the rate-hiking cycle,” Murphy said.

Looking back to 2008, he pointed to a similar buildup in money-market assets, and a roughly $1.1 trillion wall of cash subsequently leaving the sector, as financial assets began to recover in the wake of the financial crisis.

“What we did see, while not all of it, was a healthy amount went back into fixed-income in the following years,” Murphy said.

Stocks closed lower Thursday and were headed for another week of losses, with the Dow Jones Industrial Average DJIA

2.3% lower on the week so far, the S&P 500 index SPX

down 2.1% and the Nasdaq Composite Index off 2.4%, according to FactSet.

U.S. stocks posted back-to-back losses Wednesday after Federal Reserve minutes of its July meetings showed concerns about inflation revving back up. The Dow Jones Industrial Average DJIA fell about 180 points, or 0.5%, ending near 34,765, according to preliminary FactSet data. The S&P 500 index SPX gave up 0.8% and the Nasdaq Composite Index COMP closed 1.2% lower. All three benchmarks booked back-to-back loses, while the S&P 500 ending at its lowest level in more than a month. Minutes of the Fed’s July 25-26 meeting said “most participants continue to see significant upside risks to inflation, which could require further…

U.S. stocks closed sharply lower Tuesday as investors monitored signs of China’s darkening economic backdrop and gauged if a robust U.S. consumer could spell more Federal Reserve rate hikes. The Dow Jones Industrial Average DJIA fell about 360 points, or 1%, to about 34,946, according to preliminary FactSet data. The S&P 500 index SPX dropped 1.2% to about 4,437, its lowest close since mid-July, according to FactSet. The Nasdaq Composite Index COMP ended 1.1% lower. Chinese retail sales and industrial production in the world’s second biggest economy grew less than expected in July. Its growing property woes also contributed…

Hawaiian Electric Industries Inc.’s stock added to losses Tuesday, tumbling 26% after S&P Global Ratings downgraded its rating on the utility company to junk.

S&P Global Ratings cut its rating on the company HE to BB- and placed it on CreditWatch negative, meaning the rating agency could downgrade it again in the near term.

Investors were jolted by a stronger-than-expected retail sales report on Tuesday, which underscores the dual-edged sword now facing markets.

July’s 0.7% surge in retail sales is helping to bolster the view that a resilient U.S. economy can avoid a recession, despite more than a year of rate hikes by the Federal Reserve. However, the data also serves as another piece of information that some policy makers can use to support even more hikes in the final four months of this year, and left the benchmark 10-year Treasury yield…

The numbers: Builder confidence waned in August as the 30-year mortgage rate surged, dampening U.S. home-buying interest.

Despite a persistent shortage of homes on the market for resale, builders have lost confidence in the late summer amid declining customer traffic from higher mortgage rates, as well as challenges in the construction process.

U.S. stocks closed higher on Monday, with the Dow flipping positive near the closing bell, as technology stocks bounced back. The Dow Jones Industrial Average DJIA rose about 26 points, or 0.1%, ending near 35,308, according to preliminary FactSet data. The S&P 500 index SPX scored a 0.6% gain and the Nasdaq Composite Index COMP closed up 1.1%, booking its best daily percentage climb since July 28, according to FactSet data. The S&P 500’s information technology sector outperformed with a 1.9% gain, while the communication services segment rose 1%. The rally saw shares of Meta Platforms META, Apple Inc. AAPL, Alphabet…

Barry DiRaimondo, chief of SteelWave, a West Coast property developer that in the past half-century has partnering with many of the biggest names in commercial real estate, is looking for diamonds in the rough, distressed office properties located in the American city that many have given up on.

Others may be shunning San Francisco while it’s down on its luck, but DiRaimondo sees better days ahead, despite the city’s threat of a growing deficit, its fentanyl crisis, homelessness and a reluctant return of office workers to its financial core.

“Not much is coming up right now,” DiRaimondo said of buying opportunities, while speaking from his office in the heart of San Francisco’s financial district. But he was eager to point out several nearby buildings that could be candidates to buy, at the right price.

“I think over the next 12 to 18 months, you’re going to see a tsunami,” of distressed office properties, DiRaimondo said.

Like in many big cities, a wave of office buildings bought at peak prices before the pandemic now have a pile of debt coming due, at much higher rates. But San Francisco’s financial core only recently has begun to show flickers of hope in its weak recovery post-COVID.

“Whether it’s San Francisco, Oakland or anywhere here, and your debt is rolling, you’re having a conversation with your lender,” DiRaimondo said. “There’s either a restructuring going on or a foreclosure going on.”

A number of high-profile property owners this year surrendered local properties to lenders, including Westfield’s namesake shopping center downtown and a string of well-known hotels, a blow to the city’s comeback efforts.

Still, DiRaimondo expects the bulk of property ownership transfers in this boom-and-bust cycle to take place quietly, behind the scenes, often through a building’s debt changing hands. It’s a familiar playbook for veteran real-estate developers like SteelWave and its partners, especially when San Francisco office property values tumble and new loans remains expensive and hard to come by.

“Office is a nasty word, right now. Especially tech office,” he said. “We are doing something that’s a bit different.”

Booms, busts

San Francisco’s history as a boom-and-bust town perhaps is best suited for real-estate developers able to take a bunch of lemons and make lemonade.

That has been SteelWave’s signature move in the notoriously rough-and-tumble commercial real-estate industry, through its ups and downs. It has bought over $17.5 billion in properties and developments in the past five decades, first under the Legacy Partners Commercial brand before it was renamed in 2015.

It has partnered with some of the biggest names in commercial real estate, including with Angelo Gordon & Co. in 2021 on two Silicon Valley office buildings, but also distressed debt titans that include Rialto Capital, and with Chenco, one of the largest Chinese-owned U.S. real-estate investment firms.

Its stronghold is the Bay Area and DiRaimondo is now looking to raise a $500 million fund to buy distressed buildings, including in downtown San Francisco, a place major Wall Street lenders have been backing away from for months.

“It’s hard to raise equity to buy this stuff right now,” he said, but argues his strategy, which includes expanding its reach to potential investors in the U.A.E., Israel and parts of Europe, will pan out.

SteelWave’s model of buying a property includes a final tally of costs often three to four times the initial purchase price, due to extensive overhauls.

“Typically, what we do is buy something, tear it apart, put it back together, lease it, sell it,” DiRaimondo said.

It’s niche in the distressed world that’s already produced overhauls of buildings from Seattle to Colorado to Los Angeles, places the tech industry wants to lease.

In the southern California town of Costa Mesa, that meant partnering with Invesco to turn an old newsroom and printing press for the Los Angeles Times into a creative work campus. An opinion piece in 2022 from the newspaper described the revamp as turning, “the glum newspaper architecture into something inviting.”

Forget being a ‘rent bandit’

“In New York, people rushed back and refilled the apartments, streets, and subways. Restaurants and stores flooded with customers again,” a team from Moody’s analytics wrote in a recent “tale of two cities” report. “San Francisco, on the other end, battled safety concerns, homelessness, and population exodus which existed before but only became more obvious with barren neighborhoods.”

SteelWave thinks the old days of landlords raking in top-dollar commercial rents in San Francisco, while adding little back to office buildings, are a thing of the past.

“You have to have owners who want to create cool work environments to attract people back into the city,” DiRaimondo said of downtown San Francisco’s long slog back from the brink.

That means buying properties at low prices, but also risking putting money down for major improvements. He isn’t a distressed investors looking to become a “rent bandit,” he says, because the strategy will fail to get quality tenants.

Like the Moody’s team, DiRaimondo thinks San Francisco eventually will bounce back, but he thinks not before reality hits older office properties.

Take a “commodity” building downtown, often older and midblock with generic features, that previously might have been worth $750 to $800 a square foot. It now looks worth less than $300 a square foot, he said.

The early stages of fire-sales have begun already, with the 22-story tower at 350 California, nearby to DiRaimondo’s office, reportedly fetching $200 to $225 a square foot.

“San Francisco is not dead,” DiRaimondo said. “I think there are opportunities in San Francisco.”

Barry DiRaimondo, chief of SteelWave, a West Coast property developer that in the past half-century has partnering with many of the biggest names in commercial real estate, is looking for diamonds in the rough, distressed office properties located in the American city that many have given up on.

Others may be shunning San Francisco while it’s down on its luck, but DiRaimondo sees better days ahead, despite the city’s threat of a growing deficit, its fentanyl crisis, homelessness and a reluctant return of office workers to its financial core.

“Not much is coming up right now,” DiRaimondo said of buying opportunities, while speaking from his office in the heart of San Francisco’s financial district. But he was eager to point out several nearby buildings that could be candidates to buy, at the right price.

“I think over the next 12 to 18 months, you’re going to see a tsunami,” of distressed office properties, DiRaimondo said.

Like in many big cities, a wave of office buildings bought at peak prices before the pandemic now have a pile of debt coming due, at much higher rates. But San Francisco’s financial core only recently has begun to show flickers of hope in its weak recovery post-COVID.

“Whether it’s San Francisco, Oakland or anywhere here, and your debt is rolling, you’re having a conversation with your lender,” DiRaimondo said. “There’s either a restructuring going on or a foreclosure going on.”

A number of high-profile property owners this year surrendered local properties to lenders, including Westfield’s namesake shopping center downtown and a string of well-known hotels, a blow to the city’s comeback efforts.

Still, DiRaimondo expects the bulk of property ownership transfers in this boom-and-bust cycle to take place quietly, behind the scenes, often through a building’s debt changing hands. It’s a familiar playbook for veteran real-estate developers like SteelWave and its partners, especially when San Francisco office property values tumble and new loans remains expensive and hard to come by.

“Office is a nasty word, right now. Especially tech office,” he said. “We are doing something that’s a bit different.”

Booms, busts

San Francisco’s history as a boom-and-bust town perhaps is best suited for real-estate developers able to take a bunch of lemons and make lemonade.

That has been SteelWave’s signature move in the notoriously rough-and-tumble commercial real-estate industry, through its ups and downs. It has bought over $17.5 billion in properties and developments in the past five decades, first under the Legacy Partners Commercial brand before it was renamed in 2015.

It has partnered with some of the biggest names in commercial real estate, including with Angelo Gordon & Co. in 2021 on two Silicon Valley office buildings, but also distressed debt titans that include Rialto Capital, and with Chenco, one of the largest Chinese-owned U.S. real-estate investment firms.

Its stronghold is the Bay Area and DiRaimondo is now looking to raise a $500 million fund to buy distressed buildings, including in downtown San Francisco, a place major Wall Street lenders have been backing away from for months.

“It’s hard to raise equity to buy this stuff right now,” he said, but argues his strategy, which includes expanding its reach to potential investors in the U.A.E., Israel and parts of Europe, will pan out.

SteelWave’s model of buying a property includes a final tally of costs often three to four times the initial purchase price, due to extensive overhauls.

“Typically, what we do is buy something, tear it apart, put it back together, lease it, sell it,” DiRaimondo said.

It’s niche in the distressed world that’s already produced overhauls of buildings from Seattle to Colorado to Los Angeles, places the tech industry wants to lease.

In the southern California town of Costa Mesa, that meant partnering with Invesco to turn an old newsroom and printing press for the Los Angeles Times into a creative work campus. An opinion piece in 2022 from the newspaper described the revamp as turning, “the glum newspaper architecture into something inviting.”

Forget being a ‘rent bandit’

“In New York, people rushed back and refilled the apartments, streets, and subways. Restaurants and stores flooded with customers again,” a team from Moody’s analytics wrote in a recent “tale of two cities” report. “San Francisco, on the other end, battled safety concerns, homelessness, and population exodus which existed before but only became more obvious with barren neighborhoods.”

SteelWave thinks the old days of landlords raking in top-dollar commercial rents in San Francisco, while adding little back to office buildings, are a thing of the past.

“You have to have owners who want to create cool work environments to attract people back into the city,” DiRaimondo said of downtown San Francisco’s long slog back from the brink.

That means buying properties at low prices, but also risking putting money down for major improvements. He isn’t a distressed investors looking to become a “rent bandit,” he says, because the strategy will fail to get quality tenants.

Like the Moody’s team, DiRaimondo thinks San Francisco eventually will bounce back, but he thinks not before reality hits older office properties.

Take a “commodity” building downtown, often older and midblock with generic features, that previously might have been worth $750 to $800 a square foot. It now looks worth less than $300 a square foot, he said.

The early stages of fire-sales have begun already, with the 22-story tower at 350 California, nearby to DiRaimondo’s office, reportedly fetching $200 to $225 a square foot.

“San Francisco is not dead,” DiRaimondo said. “I think there are opportunities in San Francisco.”

For the last 18 months, all you’ve heard from the markets is that the U.S. economy is three months away from a recession. Now, the popular analysis is that that inflation is on a smooth glidepath down and the economy will never have a downturn again.

Worries about a recession have evaporated, and all the talk is about a “soft landing,” with the Federal Reserve not having to hike interest rates more than once more, at most.

But behind the scenes, in some economic circles, there is growing concern about another risk for the economy, dubbed a “no landing” scenario.

What does “no landing” mean? Essentially it’s marked by economic growth that’s too strong to allow inflation to fall all the way to 2%, where the Federal Reserve aims for it to be, and therefore an economy that will need more Fed rate hikes, according to Chris Low, chief economist at FHN Financial.

So instead of the U.S. central bank starting to cut rates early next year, there may be more rate hikes in store.

“There is still considerable work to do before the inflation beast is fully tamed,” Low said.

Former Fed Vice Chair Richard Clarida described the risk in crystal-clear terms. “If the Fed finds itself in March 2024 with an unemployment rate of 4% and an inflation rate of 4% with some of that temporary good news behind them, they are in a very tough spot,” Clarida said in a recent interview with Bloomberg News.

“It is a risk. It is not the base case. But if I was still there [at the Fed], I would be assessing it,” he added.

So why does this matter? Why would the Fed be in such a tough spot? Two words: presidential election.

A Fed that is dedicated to bringing inflation down might have to slam the brakes on the economy forcefully to get the job done. That gets tough during an election year, especially one that already seems poised to be filled with acrimony.

“The Fed does not play politics with monetary policy. The FOMC will do what is right for the economy, election year or not. Nevertheless, FOMC participants are already sensitive to triggering a recession. Doing it in an overt way when Congress, a third of the Senate, and the White House are up for grabs would be reckless,” Low said.

Andrew Levin, professor of economics at Dartmouth College and a former top Fed staffer, said “raising interest rates sharply in the midst of an election cycle could be a delicate matter. Even the vaunted inflation fighter, Paul Volcker [the Fed’s chairman from 1979 to 1987], decided to ease off the brakes midway through the 1980 presidential campaign.”

Ray Fair, a Yale economics professor, thinks that, whether or not the Fed successfully lowers consumer-price inflation to the vicinity of 2% will be what really matters for the 2024 presidential election. If inflation does not go gently and the Fed is still fighting next year, it would likely be negative for President Joe Biden and the Democratic Party, he said.

To avoid hiking rates next year, the Fed, in Low’s view, will raise interest rates to 6% by the end of this year. That is an out-of-consensus call. Financial markets think the Fed is done hiking with its benchmark policy interest rate in a range of 5.25% to 5.5%.

Many economist and the financial markets are talking more about prospective Fed rate cuts in early 2024 than any more hikes.

Asked during a recent radio interview if he thought a “no landing” scenario was taking shape, Philadelphia Fed President Patrick Harker replied: “I don’t think so.”

Harker said the economy was likely on track to return to the low-interest-rate and low-inflation environment of 2012-19.

“I think about this a lot, and I asked myself what’s different fundamentally about the U.S. economy now then the way it was before the pandemic,” Harker said. He concluded that there wasn’t much difference.

The big trend Harker mentioned was demographics, with baby boomers still moving in large numbers into retirement. “I don’t think we have to stay in a high-inflation regime. I think we can get back to where we were,” he said.

Steve Blitz, chief U.S. economist at research firm GlobalData.TSLombard, said he puts the probability of a “no landing” scenario at about 35%.

Blitz added it was a common mistake for economists, policy makers, traders and journalists “to presume that the expansion to come is going to look like the expansion that was.”

“At least in the United States, that was never the case,” he added.

Blitz said that if the U.S. economy were growing at a rate below 2% with an inflation rate higher than 3%, the Fed would have to raise the policy rate to about 6.5%. But if the economy is humming along with 3% growth and inflation over 3%, that would be a trickier spot. “Does the Fed really want to slow that down?” he asked.

The range of possible outcomes for the economy remains wide. Some economists still believe that a recession early next is the most likely outcome.

Other economists, like Michelle Meyer, chief U.S. economist at Mastercard, think the economy will continue to grow, with inflation coming down. Meyer described that outcome as “a soft landing with bumps.”

Stephen Stanley, chief economist at Santander U.S., said he thinks the U.S. economy will “muddle through” next year with subpar growth in the range of 1% for several quarters and inflation slowing gradually.

“Obviously, that optimism melts away if we’re back to readings of 0.4% and 0.5% on core CPI in three months or six months,” Stanley said.

The thing that will make companies lower prices is if consumers stop complaining about paying more for the things they need and want, and actually start refusing to buy them.

As the U.S. corporate earnings-reporting season progresses, with earnings from major retailers Walmart Inc. WMT, +0.59%,

Target Corp. TGT, +0.10%

and Home Depot Inc. HD, +0.52%

on tap next week, investors can get a ground-floor view of how consumer demand may have been hurt, or not, by higher prices, and what the companies plan to do, or not do, about it.

This dynamic of how consumers adjust their spending habits when prices change is referred to by economists as the price elasticity of demand.

“ For companies to cut prices, ‘you have to have the consumer go on strike, and they’re not there yet.’”

— Jamie Cox, Harris Financial Group

Those who trust companies will choose to ratchet down prices on their own, or at least not raise them because the rise in input costs has been slowing, haven’t been listening to what the many companies have told analysts on their post-earnings-report conference calls.

Kraft Heinz Co. KHC, +0.47%

acknowledged after its second-quarter report that its relatively higher prices have hurt demand, but not by enough for the food and condiments company to consider cutting prices.

Colgate-Palmolive Co. CL, +0.81%

said it will continue to raise prices, even as inflation slows and selling volume declines, as the consumer-products company continues to be laser focused on boosting margins and profits.

And while PepsiCo Inc. PEP, +0.16%

was worried that elasticities would increase, given how its lower-income customers were being particularly pressured by inflation, the beverage and snack giant reported strong results as it witnessed “better elasticities” in most of the markets in which it operated.

“Obviously, there is still carryover pricing, and I don’t think we’ll do anything different than our normal cycles on pricing in the balance of the year,” PepsiCo Chief Financial Officer Hugh Johnston told analysts, according to an AlphaSense transcript.

Basically, as MarketWatch has reported, so-called greedflation is alive and well.

Jamie Cox, managing partner for Harris Financial Group, said as long as the job market stays strong, as it is now, corporate greed will continue to pay off.

“If something is more expensive, and you have a job, you’ll complain about it, but you won’t substitute it for something cheaper,” Cox said. For companies to cut prices, “you have to have the consumer go on strike, and they’re not there yet,” Cox added.

“ ‘At some point, people are going to say, “All right — enough.” ’ ”

— Paul Nolte, Murphy & Sylvest Wealth Management

The reason elasticity is so important in the current environment is that, as long as consumers continue to pay the higher prices companies are charging, inflation will remain stubbornly high, making it, in turn, more likely that the Federal Reserve will continue to raise interest rates or, at the very least, not lower them.

But the longer interest rates stay high enough to crimp economic growth, the more likely the stock market will reverse lower as recession fears rise.

“At some point, people are going to say, ‘All right — enough,’ ” said Paul Nolte, senior wealth manager and market strategist at Murphy & Sylvest Wealth Management. “But we just haven’t seen that yet.”

What is elasticity?

Economists use the term “price elasticity of demand” to refer to the way in which consumers adjust their spending habits when prices change.

“Elasticity tries to measure how much more producers will want to produce if prices rise, and how much more consumers will want to buy if prices fall,” explained Bill Adams, chief economist at Comerica.

Elasticity often depends on the type of product a company sells.

For example, consumer-discretionary-goods companies that sell products and services that people want will often experience greater price elasticity than consumer-staples companies that sell things that people need, such as groceries and prescription drugs.

But even for needs, consumers often still have a choice, as less expensive generic, or private-label, alternatives may be available.

Andre Schulten, chief financial officer of consumer-staples maker Procter & Gamble Co. PG, +0.58%,

which recently beat earnings expectations as it continued to raise prices, telling analysts that, while there was “some trading into private label,” the overall market share of private-label products was unchanged for the year.

As Harris Financial’s Cox said, consumers may be complaining about higher prices, but they aren’t yet desperate enough to stop buying.

The Federal Reserve’s latest Beige Book economic survey stated that business contacts in some districts had observed a “reluctance” to raise prices as consumers appeared to have grown more sensitive to prices, but other districts reported “solid demand” allowed companies to maintain prices and profitability.

That’s likely why companies and analysts have become less concerned about price elasticity. Based on a FactSet analysis, mentions of the word “elasticity” in press releases and conference calls of S&P 500 companies SPX

increased as inflation and interest rates started surging in early 2022 through the end of the year.

Mentions of the word elasticity in earnings press releases and conference-call transcripts of S&P 500 companies.

FactSet

As the chart shows, “elasticity” popped up in more than 55% of earnings releases and conference calls in mid-2022, but with the second-quarter 2023 earnings-reporting season more than half over, mentions had dropped to about 20%.

Perhaps that will pick up, as retailers, especially those catering to lower-income customers — recall the PepsiCo comment — assess the demand impact of continued price increases.

Meanwhile, the branded-foods company Conagra Brands Inc. CAG, +0.71%,

whose wide-ranging food brands including Birds Eye, Duncan Hines, Hunt’s, Orville Redenbacher’s and Slim Jim, were starting to see the emergence of a different dynamic.

Chief Executive Sean Connolly said consumers were shifting behavior in some categories as prices remained high. Rather than trade down to lower-priced alternatives, he noticed some consumers buying fewer items overall, “more of a hunkering down than a trading down.”

That’s exactly the kind of consumer behavior that is needed, if companies are to stop feeding into the greedflation phenomenon and to start pulling back on prices.

The numbers: The University of Michigan’s gauge of consumer sentiment inched down to a preliminary August reading of 71.2 after hitting a 22-month high of 71.6 in the prior month.

Economists polled by the Wall Street Journal had expected sentiment to inch up to a 71.7 reading in August.

Another key part of the report is the U. of M. measure of inflation expectations.

According to the report, Americans’ expectations for overall inflation over the next year slipped to 3.3% in August from 3.4% in the prior month, while expectations for inflation over the next 5 years inched down to 2.9% from 3%.

Key details: According to the Michigan report, a gauge of U.S. consumers’ views on current conditions rose to to 77.4 in August from 76.6 in the prior month, while a barometer of their future expectations fell to 67.3 from 68.3.

Big picture: Sentiment has been boosted by waning recession fears and disinflation in grocery store prices.

What the University of Michigan said: “Consumer sentiment was essentially unchanged from July, with small offsetting increases and decreases within the index. In general, consumers perceived few material differences in the economic environment from last month, but they saw substantial improvements relative to just three months ago,” said Joanne Hsu, the director of University of Michigan consumer surveys.

SPX

were mixed in early trading Friday while the yield on the 10-year Treasury note BX:TMUBMUSD10Y

rose to 4.12%, the highest level since the spike last week after Fitch Ratings downgraded the U.S. credit rating.

The numbers: The U.S. producer price index rose 0.3% in July, the Labor Department said Friday, up from a revised flat reading in June and the largest gain since January.

Economists polled by The Wall Street Journal had forecast a 0.2% advance.

The core producer price index, which excludes volatile food, energy prices, and trade services rose 0.2 in July, up from a 0.1% gain in the prior month. This is the largest increase since February.

Key details: Over the past year, headline producer price inflation was running at a 0.8% rate in July, up from 0.2% in the prior month.

Core prices are up 2.7% from a year earlier, matching the gain in June. Core PPI prices were running at a 5.8% rate in July 2022.

A big part of the increase in producer prices was in the services sector.

The cost of services rose 0.5% last month, up from a 0.1% drop in June. This is the largest increase in a year. The increase was led by a 7.6% gain for portfolio management.

The cost of goods rose 0.1% in July after a flat reading in the prior month.

Energy prices were flat in July, down sharply from a 0.7% gain in the prior month.

Wholesale food prices jumped 0.5% after a 0.2% fall in the prior month.

Further back on the production line, prices for intermediate goods fell 0.6%, the sixth straight monthly decline.

Big picture: Price pressures have been diminishing at the producer level much faster than at the consumer level. Economists are watching the inflation data closely to see if the July interest rate hike by the Federal Reserve was the last hike of the cycle.

What are they saying? “In short, PPI surprised to the upside in July. While we do not expect further rate hikes this year, if inflation surprises to the upside and the labor market and growth do not slow, another increase in interest rates cannot be ruled out in 2023,” said Rubeela Farooqi, chief U.S. economist at High Frequency Economics.

A worsening U.S. fiscal situation caught stock and bond investors off guard in the past week and now a round of approaching government auctions is about to provide a crucial test for Treasurys.

The question in the days ahead is whether risks to the demand for U.S. government debt are growing. If so, that could put upward pressure on Treasury yields, which would undermine the performance of stocks. However, if investors end up caring less about the fiscal situation than they do about the possibility of slowing economic growth and decelerating inflation, government debt’s safe-haven appeal could be reinforced, putting a limit on how high yields might go.

Concern about the deteriorating fiscal outlook was a factor behind the past week’s rise in long-term Treasury yields. Ten- BX:TMUBMUSD10Y

and 30-year yields BX:TMUBMUSD30Y

respectively jumped to 4.188% and 4.304% on Thursday, the highest levels since early November, as investors sold off long-term government debt — which took the shine off U.S. stocks. By Friday, though, a moderating pace of U.S. job creation for July sent yields into reverse, giving equities a temporary lift during the final trading session of the week.

At issue is the extent to which potential buyers of Treasurys may be deterred by Fitch Ratings’ Aug. 1 decision to cut the U.S. government’s top AAA rating, at a time when the government is about to unleash what Barclays rates strategists describe as a “tsunami” of supply. A total of $103 billion in 3-, 10-and 30-year Treasurys come up for sale between Tuesday and Thursday. In addition, a spate of Treasury bills are scheduled to be auctioned starting on Monday.

Gene Tannuzzo, global head of fixed income at Boston-based Columbia Threadneedle Investments, said that while he and his team still have room to add T-bills to the government money-market funds they oversee during the week ahead, they haven’t made up their minds about whether to buy more longer-dated maturities for their bond funds.

“While we are comfortable that the Fed is at or near the end of its rate hikes, there are a lot more questions about the durability of the economic recovery, the degree that inflation will remain low, and the risk premium that needs to be put in at the long end,” Tannuzzo said via phone.

Treasury’s $1 trillion third-quarter borrowing plans, along with some technical issues and the Bank of Japan’s decision to switch to a more flexible yield-curve control approach, might reduce demand for U.S. government debt, he said. Columbia Threadneedle managed $617 billion as of June.

“One can’t ignore the risk of an unruly rise in yields, but our view is that this is a low risk and what the Treasury auctions may produce instead is ‘indigestion,’ driven by poor technicals and low liquidity, Fitch’s downgrade, and the Bank of Japan action — and by the end of August, we should be past much of this,” he told MarketWatch.

Risks to the demand for Treasurys may become obvious soon, given Tuesday-Thursday’s $103 billion in total sales of 3-, 10- and 30-year securities, according to analyst John Canavan of U.K.-based Oxford Economics. The main “question mark” for the market’s ability to absorb the increased Treasury issuance will be whether or not domestic investment funds continue to show interest, Canavan wrote in a note distributed on Friday.

Source: Oxford Economics.

“ ‘My suspicion is that with higher rates comes equally solid demand’ at upcoming auctions.”

— John Flahive, head of fixed income at BNY Mellon Wealth Management

Market players have had little difficulty absorbing Treasury coupon issuances in recent years because of flight-to-safety trades made after the U.S. onset of the Covid-19 pandemic in 2020. Now, however, increased auction sizes are being accompanied by still-elevated inflation, better-than-expected economic growth, and the possibility of more rate hikes by the Federal Reserve — which is likely to complicate the market’s ability to absorb the increased supply “without hiccups,” Canavan said.

On the flip side of the debate is John Flahive, head of fixed income at BNY Mellon Wealth Management in Boston, which managed $286 billion in assets as of June. He said equity markets will continue to be much more focused on economic developments and earnings. And as long as the latter of the two remains robust, stocks “can grind higher in a low-volatility environment,” Flahive said via phone.

Saying he does not expect his team to be a major participant in the Treasury auctions, Flahive said that the bond market’s reaction in the past week was “a little overdone” and “we always felt that there was a limited to how much yields could go up to reflect more government debt.”

“My suspicion is that with higher rates comes equally solid demand” at upcoming auctions, he said. “I’m still optimistic about rates going back down over time as the result of a slowing economy and decelerating inflation. We continue to like the bond market and see a better-than-even chance that yields go down as the economy continues to weaken in the quarters ahead.”

Friday’s reaction to July’s official jobs report, which showed the U.S. added a modest 187,000 new jobs, provided a breather from the past week’s run-up in Treasury yields.

On Friday, the 30-year Treasury yield fell 9 basis points to 4.214%, yet still ended with its biggest weekly gain since early February. The 10-year rate, which dropped 12.8 basis points to 4.06%, finished with a third straight week of advances.

Stocks fell Friday, leaving major indexes with weekly declines. The Dow Jones Industrial Average DJIA

posted a 1.1% weekly fall, while the S&P 500 SPX

shed 2.3% and the Nasdaq Composite COMP

retreated 2.9%. The soft start to August comes after a run of sharp gains for equities. The S&P 500 remains up 16.6% for the year to date.

The economic calendar for the week ahead includes U.S. inflation updates.

On Monday, June consumer-credit data is set to be released. Tuesday brings the NFIB’s small business optimism index, plus data on the U.S. trade balance and wholesale inventories. Then on Thursday, weekly initial jobless claims and the July consumer-price index are released. That’s followed on Friday by the producer-price index for last month and an August consumer-sentiment reading.

Meanwhile, portfolio manager and fixed-income analyst John Luke Tyner at Alabama-based Aptus Capital Advisors, which manages roughly $5 billion in assets, said he plans to follow the Treasury auctions, but doesn’t usually participate in them.

“One of the biggest trends we’ve seen is the continued increase in the issuance amounts from Treasury. Whatever we are budgeting for is never enough, which justifies the Fitch downgrade,” Tyner said via phone. “It’s tough to say people aren’t going to buy U.S. debt, but you’ve got to entice them to buy duration and take the risk.

“The U.S. is not an emerging market, but ultimately we are going to see the market rate that participants require be higher, with a notable uptick in term premia,” he said. “What we could see in the face of all this issuance is a grind up in yields on an auction-by-auction basis. If I look at the technicals, a 4.9%-5% yield on the 10-year note seems in the cards,” and “it will be difficult for stocks to hold or expand from full valuations as rates run up.”

US. stocks closed lower Friday, capping off a volatile week that finished with losses after Fitch took away its top AAA ratings for the U.S. and government bond yields embarked on a wild ride. The Dow Jones Industrial Average DJIA, -0.43%

fell about 150 points, or 0.4% on Friday, ending near 35,065, according to preliminary FactSet data. The S&P 500 index SPX, -0.53%

shed 0.5% and the Nasdaq Composite Index closed 0.4% lower. For the week, the Dow posted a 1.1% decline, the S&P 500 a 2.3% drop and the Nasdaq shed 2.9% since Monday, according to FactSet. Investors were focused on July jobs data released on Friday for clues to the health of the economy and potential next moves by the Federal Reserve on rates. The 10-year Treasury yield TMUBMUSD10Y, 4.045%

swung almost 13 basis points lower on Friday to 4.06%, after briefly climbing to about 4.2% earlier in the week, according to FactSet data.

Icahn Enterprises Inc.’s bonds saw better buying on Friday, after Carl Icahn’s investing arm announced it was halving its quarterly distribution, a move that disappointed unit holders but is positive for its bonds.

Bondholders are typically focused on making sure a company can make its interest payments and repay the principal when a bond matures.

The company said it would now make a distribution of $1, down from $2 previously. The news came as the company posted a surprise loss for the second quarter and a $1 billion decline in revenue.

Icahn placed the blame for the fund’s poor performance on Hindenburg Research, the short seller that published a report about IEP on May 2, accusing it of overstating asset values. Hindenburg also revealed that Icahn himself had borrowed from the company, among other issues.

The stock promptly tumbled and was last down 24%, putting it on track for its biggest one-day selloff since it went public 36 years ago. The next biggest drop was 20.0% on May 2, when the Hindenburg Research report was released.

As the chart below from data-as-a-service provider BondCliQ Media Services shows buyers emerging after 8:00 a.m. Eastern, immediately after the news was announced. By midmorning, some sellers had emerged.

Icahn Enterprises net customer flow (intraday). Source: BondCliQ Media Services

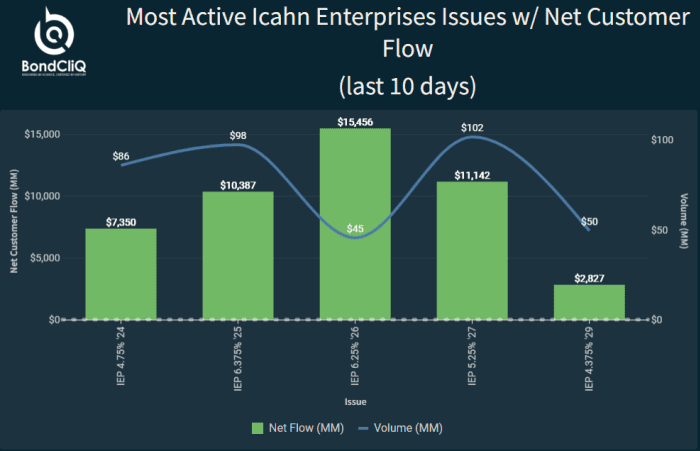

The following table shows there was net buying over the last 10 days, focused on the 6.35% notes that mature in 2026.

Most active Icahn Enterprises issues with net customer flow (last 10 days). Source: BondCliQ Media Services

In a letter to unit holders accompanying the results, Icahn acknowledged missteps in the past several years as the company has shifted away from its core activist strategy and shorted far more than was necessary.

“While we made money on the long side through our activism efforts, our returns have been overwhelmed by our overly bearish view of the market and related oversized short (hedge) positions,” Icahn wrote. “Over the past six months, we have significantly reduced our hedges. Going forward, we intend to stick to our knitting and focus on our activist strategy while remaining appropriately hedged.”

Activism is the best investment paradigm because “there is no accountability in Corporate America,” he wrote.

With many exceptions, “most CEOs are incapable of creating great businesses (or even improving them) and the desire to empire build is rampant. “

Many are not the best person for the job or even the most talented individual in the organization, he continued. Far too often, they have climbed through the ranks by being agreeable and presenting no threat to their superiors.

“Those CEOs are generally too busy playing at the proverbial country club to realize what improvements can be made or what hidden jewels can be unlocked,” he said.

CEOs are hard to unseat, as they can pack a board with loyal cronies and use company funds to defend against an activist campaign by hiring expensive legal and financial experts, further depleting the coffers.

Icahn has himself waged endless activist campaigns against companies and their management teams, and most recently succeeded in his effort to shake up management at gene sequencing test maker Illumina Inc. ILMN, +1.85%, as the Associated Press reported.

Past activist campaigns by Icahn’s company have generated billions of dollars for shareholders and helped boards and CEOs capture untapped value, Icahn has argued, citing Reynolds, Netflix NFLX, +0.66%,

Forest Labs, Apple AAPL, -3.72%,

CVR Energy CVI, -0.40%,

Herbalife HLF, -0.32%

eBay EBAY, -0.73%,

Tropicana, Cheniere LNG, +0.27%

and Occidental OXY, +3.14%

as examples.