It’s crunch time. President Joe Biden and the House Republicans have just days to act to prevent the country from defaulting on its debt. In January, the U.S. hit its debt limit of $31.4 trillion, which means the federal government can’t rack up any more tabs (or borrow more money) — so paying the bills on time just got more complicated.

How will the debt ceiling deadline affect you? It’s a loaded question, so let’s pull back the layers. Here’s what to know.

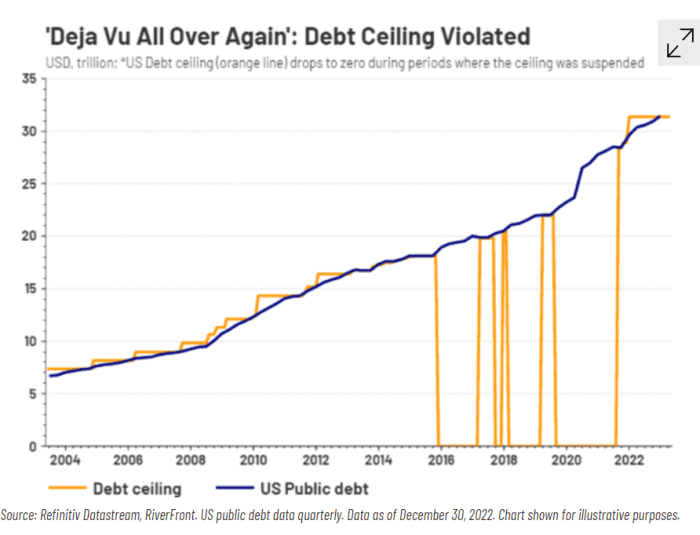

What is the debt ceiling?

The debt ceiling was created by Congress in 1917 and limits how much the U.S. can borrow to fund legal obligations set by lawmakers in the past (social security, tax refunds, military salaries, interest payments on outstanding debt, medicare benefits, and more). In other words, it caps how much debt the U.S. can incur. The current debt ceiling is $31.4 trillion.

What does hitting the debt ceiling mean?

Hitting the debt ceiling limit wouldn’t be a hot topic if the country’s revenue exceeded its costs (the government receives money primarily from individual and corporate taxes but also has other sources such as leases of government-owned buildings and land, sale of natural resources, and admission to national parks).

However, the U.S. hasn’t been in the green since 2001, meaning that for over 20 years, the government has had to borrow money to fund operations. Now that the U.S. has hit its debt limit, there are two options: raise or suspend the limit so the government can pay its bills on time or face a default.

Raising the debt ceiling would be just what it sounds like (bumping up the limit that the U.S. can borrow). Suspending the debt ceiling means that the Treasury can temporarily override the ceiling and borrow more beyond the current limit. If the U.S. were to default, the country wouldn’t be able to pay its bills on time, and the economic impact would likely be felt immediately.

Related: Fannie Mae Says a ‘Modest Recession’ Is ‘Expected’ in Second Half of the Year

When is the deadline to raise or suspend the debt ceiling?

In a letter sent to House Speaker Kevin McCarthy on Monday, Treasury Secretary Janet Yellen warned that it is “highly likely” that the Treasury will be unable to fulfill its financial obligations if Congress does not raise or suspend the debt ceiling as soon as June 1.

“I continue to urge Congress to protect the full faith and credit of the United States by acting as soon as possible,” she wrote.

What would happen if the U.S. defaults?

In March, Moody Analytics chief economist Mark Zandi warned that if the U.S. defaults, it would be “catastrophic” and Americans would likely pay for the default “for generations.”

For example, government workers and businesses with government contracts might not get paid on time, and social security payments could stop. In a broader sense, it would also trigger “a loss of consumer and business confidence,” said Brookings Institution analysts Wendy Edelberg and Louise Sheiner.

Would a default cause a recession?

The default would essentially spark a nationwide economic collapse and induce an “immediate, sharp recession,” the Council of Economic Advisors warned in early May.

Harry Mamaysky, professor of professional practice at Columbia Business School, told Entrepreneur that the government has “lots of obligations to lots of people.”

“At some point, when there’s not enough money, they have to begin to prioritize who to pay first,” Mamaysky said. “Someone is not going to get paid the money that they’re owed on time, and that’s going to be disruptive.”

Related: Bank Failures and Inflation Making You Sweat? Here Are 3 Marketing Moves to Make Your Business Recession-Proof.

However, the short-term ramifications of default could be nowhere near as damaging as the long-term implications–what Mamaysky calls a “reputational issue” that could call into question the U.S.’s credibility as a smart country to do business with.

“That’s the biggest risk to me—it isn’t what happens this year or next year, but will the world perceive in five to 10 years the U.S. to be the best country in the world to conduct business?” he said. “It’s not imminent, but if Congress doesn’t watch it, they’re going to erode confidence.”

On Wednesday, top credit rating agency Finch placed the U.S.’s current “AAA” rating under “rating watch negative,” which means the country’s perfect score might be at risk for a downgrade.

“The Rating Watch Negative reflects increased political partisanship that is hindering reaching a resolution to raise or suspend the debt limit despite the fast-approaching x date (when the U.S. Treasury exhausts its cash position and capacity for extraordinary measures without incurring new debt),” the company said in a statement.

How will a default affect small businesses?

A recent report by Goldman Sachs found that 65% of small business owners would be “negatively impacted” if the U.S. defaults on its debt. Furthermore, 90% said it was “very important” that the government avoid defaulting.

If the U.S. defaults, businesses with government contracts may not see payments, and shops that have customers who rely on food stamps or social security to pay for necessities may see a drop in spending.

“If you’re a social security recipient and you owe rent, you may not have the money to pay rent,” Mamaysky added. “And if the landlord owes the utility bill on their building, they may not be able to pay the utility bill because they didn’t get the rent.”

Related: 7 Savings Strategies for Small Businesses in Uncertain Economic Climates

What’s more, a 2011 Federal Reserve of New York report said small businesses were hit the hardest during the 2008-2009 recession.

According to the report, banks become “more selective and risk-averse” when granting loans in a recession, making it more difficult for individuals to get a small business loan.

“Small firms, which rely more on external financing and tend to be riskier, are more likely to be affected by a credit crunch,” researchers wrote.

How many times has the debt ceiling been raised or modified?

Despite the current pressure to raise or suspend the debt ceiling, it’s a relatively routine practice for the U.S. government. Since 1960, Congress has acted 78 times to raise, temporarily extend, or revise the definition of the debt limit to avoid a default—49 times under Republican presidents and 29 times under Democratic presidents, according to the Treasury, adding that “Congressional leaders in both parties have recognized that this is necessary.”

The most recent increase was in 2021 when the debt ceiling was raised by $2.5 trillion.

What’s the hold-up to raise or suspend the debt ceiling?

McCarthy and the Biden administration are negotiating a deal to avoid a federal default. However, the two have differing stances: McCarthy and House Republicans are pushing for $3.6 trillion in cuts and limits to future spending for certain programs (which are not specified in the bill) in exchange for raising the debt ceiling, while the Biden administration is focused on raising the limit and paying bills on time before it agrees to any cuts.

On Thursday, the House is set to vote on a deal and then recess while negotiators continue to work on an agreement.

“Following [Thursday’s] votes, if some new agreement is reached between President Biden and Speaker McCarthy, members will receive 24 hours’ notice in the event we need to return to Washington for any additional votes, either over the weekend or next week,” House Majority Leader Steve Scalise said, per CNN.

What is the 14th Amendment, and what does it have to do with the debt ceiling?

The 14th Amendment covers equal protection and other rights such as citizenship, state taxation, and what Congress can regulate. The fourth section of the Amendment, which covers public debt, states that the “validity of the public debt of the United States … shall not be questioned.”

Given that the U.S. has hit its debt ceiling and may not be able to pay its bills, there is an argument that, by invoking the 14th Amendment, Biden has the legal authority to bypass Congress (which approves any action to raise or suspend the debt ceiling) and essentially continue to issue more debt through the Treasury and ignore the debt limit.

Biden has been supportive but cautious about invoking the 14th Amendment as a solution.

“The question is, could it be done and invoked in time that it would not be appealed, and as a consequence past the date in question and still default on the debt? That is a question that I think is unresolved,” Biden told reporters on Sunday, per The Wall Street Journal.

Some experts have said that the move would be unconstitutional.

“The Biden administration even flirting with these ideas really suggests that the administration’s fidelity to the Constitution is questionable or opportunistic,” Philip Wallach, a senior fellow at the center-right think tank American Enterprise Institute, told the Wall Street Journal.

Others have been slightly more straightforward on their opinion of the idea, Yellen saying it could provoke a “constitutional crisis,” and Representative Chip Roy saying if Biden took the 14th Amendment route, the House Republicans would “blow crap up.”