Banc of California Inc.’s proposed agreement to acquire PacWest Bancorp. helped send regional-bank stocks considerably higher on Wednesday. But even after a two-day increase of 12% for its shares, the acquiring bank remains the favorite name among analysts covering regional players in the U.S.

The merger agreement was announced after the market close on Tuesday, but the rumor mill had already sent Banc of California’s BANC, +0.62%

stock up by 11% that day. Then on Wednesday, shares of PacWest Bancorp PACW, +26.92%

shot up 27% to $9.76, which was above the estimated takeout value of $9.60 a share when the deal was announced. The merger deal, if approved by both banks’ shareholders, will also include a $400 million investment from Warburg Pincus LLC and Centerbridge Partners L.P.

A screen of regional banks by rating and stock-price target is below.

With PacWest closing above the initial per-share deal valuation, it is fair to wonder whether or not its shareholders will vote to approve the agreement. In a note to clients on Wednesday, Wedbush analyst David Chiaverini called Banc of California’s offer “fair, but not overwhelmingly attractive,” and wrote that PacWest was “a likely seller before the mini banking crisis occurred in March.”

While Chiaverini went on to predict the deal’s approval by PacWest’s shareholders, he added that he “wouldn’t be surprised if there were some dissent among a minority of shareholders [which could] possibly open the door to the potential emergence of a third-party bid.”

More broadly, Odeon Capital analyst Dick Bove wrote to clients on Wednesday that the merger deal, along with increasing involvement of private-equity firms in lending businesses, the expected enhancement of regulatory capital requirements for banks and other factors could lead to more consolidation among smaller banks.

He went on to write that we might be entering a period for the banking industry similar to the 1990s, “when rules were being changed and acquisitions were rampant,” which “created new investment opportunities.”

The SPDR S&P Regional Banking exchange-traded fund KRE, +4.74%

rose 5% on Wednesday but was still down 17% for 2023, while the SPDR S&P 500 ETF Trust SPY, +0.02%

was up 19%, both excluding dividends.

KRE holds 139 stocks, with 98 covered by at least five analysts working for brokerage firms polled by FactSet. Out of those 98 banks, 45 have majority “buy” ratings among the analysts. Among those 45, here are the 10 with the most upside potential over the next 12 months, implied by consensus price targets:

Any stock screen can only be a starting point when considering whether or not to invest. If you see any stocks of interest here, you should do your own research to form your own opinion.

One of the hottest movies of the summer is the staggeringly good biopic “Oppenheimer,” about the man who oversaw the frantic race to develop the atomic bomb during World War II.

The atom bomb dropped on Hiroshima, Japan on Aug 6, 1945 was a fission-style device. This also happens to be the same basic physics behind nuclear reactors that are in use today. It’s a reminder that technology can be, at its essence, agnostic: Whether it is used for malevolent or benevolent purposes (in nuclear fission’s instance, an instrument of death or clean, carbon-free electricity) depends upon the intent of the user.

These percentages are likely to rise as global demand for electricity — and concerns about global warming and climate change — rise. This will present opportunities for long-term oriented investors. The lion’s share of this demand — about 70%, says the Paris-based International Energy Agency (IEA), will come from India, which the United Nations says is now the world’s most populous country, China, and Southeast Asia. Put another way, “the world’s growing demand for electricity is set to accelerate, adding more than double Japan’s current electricity consumption over the next three years,” says Fatih Birol, the IEA’s executive director.

While fossil fuels remain the dominant source of electricity generation worldwide — the Central Intelligence Agency estimates that it provides about 70% of America’s electricity, 71% of India’s and 62% of China’s, for example—the IEA report says future demand will be met almost exclusively from two sources: renewables and nuclear power. “We are close to a tipping point for power sector emissions,” the IEA says. “Governments now need to enable low-emissions sources to grow even faster and drive down emissions so that the world can ensure secure electricity supplies while reaching climate goals.”

“ The Biden administration is a big booster of nuclear energy. ”

It’s helpful that the Biden administration is a big booster of nuclear energy, which the White House sees as an integral part of its broader effort to move the U.S. economy away from fossil fuels. The Department of Energy says that the country’s 93 reactors generate more than half of America’s carbon-free electricity. But price pressures from wind, solar and natural gas (which the feds call “relatively clean” even though it emits about 60% of coal’s carbon levels) have putseveral reactors out of business in recent years.

The bipartisan infrastructure bill that Biden signed into law in November 2021 includes $6 billion, spread out over several years, for the so-called Civil Nuclear Credit Program, designed to keep reactors — and the high-paying jobs that come with them — running. If a plant were to close, it would “result in an increase in air pollutants because other types of power plants with higher air pollutants typically fill the void left by nuclear facilities,” the administration says. U.S. Energy Secretary Jennifer Granholm has said the Biden administration is “using every tool available” to get the country powered by clean energy by 2035.

The private sector is beginning to stir. Last week, Maryland-based X-Energy said it would build up to 12 reactors in Central Washington state, for Energy Northwest, a public utility. These wouldn’t be the behemoth-type reactors we’re used to seeing, but “advanced small, nuclear reactors.” X-Energy, which is privately held, has also been selected by Dow DOW, -1.40%

to construct a similar facility in Texas.

Other companies are also rolling out new technology to meet demand. Nuclear fusion — a breakthrough in that it creates more energy than the Oppenheimer-era fission model and at a lower cost — is likely to be the basis for reactors in the years ahead; the Washington, D.C.-based Fusion Industry Association thinks the first fusion power plant could come online by 2030. After seven rounds of funding, one fusion company, Seattle-based Helion Energy, is currently valued at around $3.6 billion, and appears headed for a public offering.

Here too, the Biden administration is getting involved. In May, the Department of Energy announced $46 million in funding for eight other fusion companies. “We have generated energy by drawing power from the sun above us. Fusion offers the potential to create the power of the sun right here on Earth,” says Granholm.

There are several opportunities here for long-term investors. You can pick your way through any number of publicly held companies, including more traditional utilities, or spread your bet across the industry through a handful of exchange-traded funds. The largest of these is the Global X Uranium Fund URA, +0.78%,

with about $1.6 billion in assets. It’s up about 9% year-to-date. The VanEck Uranium + Nuclear Energy Fund NLR, +0.41%

is up almost 10% and sports a 1.8% dividend yield. These are respectable year-t0-date returns, even though they lag the S&P 500 SPX, +0.32%

(up close to 19%) by a wide margin.

Late on Wednesday, Tesla Inc. TSLA, -1.10%

reported that quarterly sales were up 47% from a year earlier. But the stock tumbled 10% on Thursday.

Tesla’s shares are still up 113% this year. The company is among a group of 13 in the S&P 500 that stand out with high growth expectations for sales, earnings and free cash flow through 2025.

But less than half of analysts polled by FactSet rate Tesla a buy. Emily Bary explains what they are worried about.

Chipotle Mexican Grill is among 14 stocks named by Michael Brush for consideration by investors looking to ride along with long-term improvement of U.S. labor productivity.

AP

The S&P 500 SPX, +0.03%

has returned 19% this year, following its 18% decline in 2022. On the same basis, with dividends reinvested, the benchmark index is still down 2% since the end of 2021.

The Dow Jones Industrial Average DJIA, +0.01%

is up 6% this year. The venerable index has trailed the S&P 500, but its closing level of 35,255.18 on Thursday was only 4% shy of its record close a 36,799.65 on Jan. 4, 2022. Joseph Adinolfi explains Dow Theory, which according to technical analysts is sending a strong bullish signal for the stock market.

Even if you have resisted the idea of a Roth IRA, you may soon be forced to have one

This year if you are age 50 or older and are already maxing-out your contribution to a 401(K), 403(B) or other qualified employer-sponsored tax-deferred retirement plan at $22,500, you can make an additional “catch up” tax deductible contribution of $7,500 for a total of $30,000. But starting in 2024, the catch up contribution will no longer be tax deductible if you earn at least $145,000 a year. You can still make the contribution with after-tax money into a Roth 401(K) account that your plan administrator may already have set up for you.

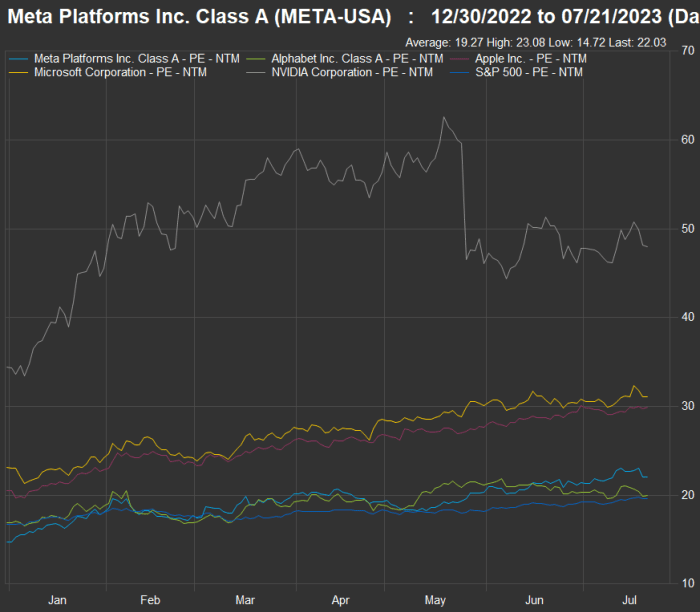

Shares of Meta Platforms Inc. and Alphabet Inc. trade only slightly higher than the S&P 500 on a forward price-to-earnings bases, while Nvidia Corp., Microsoft Corp. and Apple Inc. trade much higher.

FactSet

Leslie Albrecht looks at Meta Platforms Inc. META, -2.73%,

which is Facebook’s holding company and has a hit on its hands with the new Threads social-media platform, and Google holding company Alphabet Inc. GOOGL, +0.69%,

to consider which stock is a better buy.

In The Ratings Game column, MarketWatch reporters track analysts’ thoughts about various stocks. Here’s a sampling of this week’s coverage:

You don’t know every bad factor causing air travel to be nothing but harassment

Getting there is half the fun.

Getty Images

The U.S. flying scene — from shortages of equipment and labor (and runways) to ill-staffed air-traffic control towers — is a well-known nightmare for U.S. travelers. But there is more to the story. Jeremy Binckes looks into other factors that may surprise you and cause great inconvenience this summer.

The Federal Reserve is expected to raise interest rates again next week

The Federal Open Market Committee will meet next Tuesday and Wednesday, to be immediately followed by a policy announcement. Economists expect the central to raise the federal-funds rate by another quarter point. The question is whether or not this will end the Fed’s inflation-fighting rate cycle.

How much would you pay for 100% downside protection in the stock market?

MarketWatch illustration/iStockphoto

Over the past 30 years, the SPDR S&P 500 ETF Trust SPY,

has returned 1,650%, for an average annual return of 10%, with dividends reinvested, according to FactSet. But it hasn’t been a smooth ride. The ETF, which tracks the benchmark S&P 500, fell 18% last year and 37% during 2008, for example. And there have been even larger declines if the analysis isn’t confined to calendar years.

But can you ride through market declines? Many studies have shown that most investors who try to time the market sell after a decline has started and buy back in well after a recovery is under way, which means their long-term performance can suffer significantly.

In this week’s ETF Wrap column (and emailed newsletter), Isabel Wang describes a new buffered fund that can give you 100% downside protection over a two-year period, in return for a cap on your potential gains in the stock market. Here’s the price you would pay for the protection.

The World Cup games have started

Hannah Wilkinson scored the home team’s first goal against Norway during the first World Cup game in Auckland, New Zealand, on July 20.

Getty Images

The Women’s World Cup began Thursday with an upset victory by New Zealand over Norway.

James Rogers reports on what is expected to be a much easier environment for FIFA and corporate sponsors than that of last year’s Men’s World Cup in Qatar.

U.S. Soccer Federation President Cindy Parlow Cone participated in MarketWatch’s Best New Ideas in Money podcast and spoke about the long-term effort to achieve equal treatment for women soccer players.

More coverage of the World Cup:

Want more from MarketWatch? Sign up for this and other newsletters to get the latest news and advice on personal finance and investing.

Funds associated with Cathie Wood’s ARK Investment continued to cull shares of Coinbase Global Inc. and Tesla Inc. on Monday, according to recent trade disclosures.

The ARK Fintech Innovation ETF ARKF, +1.58%

dumped 76,788 Coinbase shares COIN, +0.23%

on the day, while the ARK Innovation ETF ARKK, +2.29%

sold 127,266 and the ARK Next Generation Internet ETF ARKW, +2.23%

sold 44,784 shares.

Coinbase represents 0.78% of the Fintech Innovation ETF, along with 0.15% of the Innovation ETF and 0.30% of the Next Generation Internet ETF. ARK disclosed the transactions and weightings in the daily trade notifications it posts to its website.

Meanwhile, the ARK Innovation ETF shed 38,329 Tesla shares TSLA, +3.20%

on Monday, while the ARK Next Generation Internet ETF sold 6,855. Those shares were worth $13.1 million based on Tesla’s Monday closing level of $290.38. Tesla represents about 0.12% of both funds as they continue to unload shares.

ARK scooped up 455 shares of Meta Platforms Inc. META, +0.57%

within its Next Generation Internet ETF and bought up 3,729 shares within the ARK Innovation ETF. That amounted to $1.3 million worth of stock based on Meta’s $310.62 Monday close.

Two ARK funds bought a combined $790 million in Robinhood Markets Inc.’s stock HOOD, +0.89%,

with the fintech fund scooping up 25,641 shares and the Next Generation Internet ETF buying 37,630 shares. ARK added 4,608 shares of SoFi Technologies Inc. SOFI, +4.41%

to the fintech fund, worth $43,683 based on Monday’s close.

ARK was also active in shares of Twilio Inc. TWLO, -0.63%,

buying 15,702 within the Fintech Innovation ETF, 133,499 within the Innovation ETF and 22,748 within the Next Generation Internet ETF. That amounted to $11.4 million in Twilio’s stock based on Monday’s $66.47 closing price.

These reports, excerpted and edited by Barron’s, were issued recently by investment and research firms. The reports are a sampling of analysts’ thinking; they should not be considered the views or recommendations of Barron’s. Some of the reports’ issuers have provided, or hope to provide, investment-banking or other services to the companies being analyzed.

Would Twitter have been better off to remain a public company rather than be taken private by Elon Musk?

We’ll never know for sure, of course. But it’s hard to imagine that it would have performed any worse. Twitter as a private company is hemorrhaging advertisers, and according to a recent Fidelity analysis its market value is down nearly two-thirds from the $44 billion Musk paid for it.

Grading Twitter’s performance as a private company is more than an idle armchair exercise. It goes to the heart of an age-old debate over whether companies can be more profitably managed when private rather than public. The private equity (PE) industry not surprisingly claims that its approach is superior, and much of Wall Street agrees since many PE firms have produced impressive long-term returns.

The industry’s claims are not devoid of dissenters. Consider a recent study from Verdad Capital entitled “Private Equity Operational Improvements.” It was conducted by Minje Kwun of Dartmouth College and Lila Alloula of Yale University.

In order to overcome the otherwise insuperable obstacle of being unable to measure how private companies are performing, the researchers focused on a subset of leveraged buyouts (LBOs) from 1996 to 2021 in which the private equity firms issued public debt. In order to sell debt to the public, of course, the PE firms had to issue financial statements publicly, and that enabled the researchers to analyze the LBOs’ performance after going private, relative to public companies in the same industry sector.

Kwun and Alloula focused on six indicators of financial performance: Revenue growth, EBITDA margin, capital expenditures as a percentage of sales, and the ratios of gross profit to total assets, EBITDA to total assets, and debt to EBITDA. (EBITDA, of course, refers to Earnings Before Interest, Taxes, Depreciation and Amortization.)

Relative to public companies in the same sector over the three years after going private, LBOs on average did not show any operational improvement along these six dimensions. The researchers conclude: “The [private equity] industry mythology of savvy and efficient operators streamlining operations and directing strategy to increase growth just isn’t supported by data.”

Their results are consistent with those of a near-decade ago study by Jonathan Cohn and Lillian Mills of the University of Texas and Erin Towery of the University of Georgia. They used a different technique to access the otherwise inaccessible financial data of newly-private companies: Their tax returns. The professors focused on the operating performance of a sample of companies that had gone private between 1995 and 2007, comparing them to otherwise-similar companies that remained public. On average over the three years after going private, the researchers found, the private companies performed no better than the public ones.

The source of PE’s industry high returns

What, then, is the source of the increased return that the private equity industry often produces? The answer appears to be increased leverage. Leverage increases returns on the upside, even if it magnifies losses on the downside. Leverage has worked to the PE industry’s advantage over the last several decades since public markets have on balance have risen significantly.

Notice that increasing leverage requires no particular management expertise or shrewd strategic planning. In principle it’s no more difficult than you or me purchasing stock on margin.

These studies are not the final word on the subject. Some other studies, using alternate methodologies, have found some operational improvement at companies after being taken private. If different methodologies can reach such different conclusions, however, that would suggest that the benefits of going private are not as obvious and overwhelming as the private equity industry would have us believe.

At a minimum, Kwun and Alloula argue, we should be skeptical “of any claims of operational improvements being a major contributor to PE’s performance relative to public markets.”

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at mark@hulbertratings.com

It hasn’t served a vital economic function since the government stopped treating it as money back in 1971. Actually, you could argue it stopped being necessary long before that.

Yes, some people prefer it in jewelry. It is used in some technological equipment, and sometimes, still, in dentistry. But so what? According to authoritative data from the World Gold Council, even all those uses only account for about half of the world’s supply each year. Logically, this should mean that there is a gigantic glut of gold and that its price would be in free fall.

But it isn’t. Gold is beating U.S. stocks and bonds this month. And this isn’t even a rarity. I’ve run some numbers and have found a couple of things that could be very important to retirees, and for all of us suckers saving for retirement.

Even though, according to traditional financial theory, they really make no sense at all.

The first thing is that over the past century including some gold in your portfolio alongside stocks and bonds has genuinely added value. It has produced higher average returns, less volatility and fewer of those disastrous “lost decades” where your portfolio ended up whistling Dixie.

The second thing is that this peculiarity has been showing no signs of letting up in recent years or decades — even though, if anything, gold makes even less sense today than it used to.

Let me explain.

As usual, I’ve tapped the excellent database maintained by the NYU Stern School of Business, which tracks asset values going back to 1928.

Over that period, a conventional so-called balanced portfolio invested 60% in the S&P 500 SPY, -0.06%

index of large-company stocks and 40% in U.S. 10-year Treasury bonds TMUBMUSD10Y, 3.832%

has generated an average return of 4.9% a year in “real” terms, meaning above inflation.

A portfolio that’s 60% invested in the S&P 500, 30% in the bonds and 10% in gold GC00, -0.26%

earned a slightly higher average, 5.1% a year in real terms. But the volatility was lower: The portfolio that included the gold had a lower standard deviation of returns, and a much higher “median” return, meaning the middlemost return if you ranked all the years from best to worst. The portfolio including gold beat the traditional one by five full percentage points in total over the typical 10-year period, and failed to keep up with inflation for 10 years on only five occasions — half as often as the portfolio consisting exclusively of stocks and bonds.

Nor is this just about olden times. The portfolio including 10% gold has beaten the traditional 60/40 by an average of 0.4 percentage point a year since President Richard Nixon finally killed the gold standard in 1971. And it has beaten the traditional portfolio by the same amount, an average of four-tenths of a percentage point, so far this millennium. (The 60/40 portfolio has done better if you start measuring only in 1980, as that ignores the golden 1970s but includes the long bear market for gold of the 1980s and 1990s.)

And gold has added value in five of the last seven years (while in the other two it was effectively a tie).

It’s not so much that gold is a great long-term investment on its own. It’s that gold has seemed to shine when others, specifically stocks and bonds, have failed. And it still does. It held up during the crash of 1929-32. But it also held up during the crash in 2002. And in 2008. And 2020.

A financial expert told me this was “hindsight bias.” But so is most financial analysis.

When your financial adviser tells you what you might reasonably expect from large stocks, small stocks, international stocks, real estate and so forth in the decades ahead, he or she is basing that on history. (In some cases this has been downright hilarious, as when advisers said you should still expect “average” historical returns of 5% a year from Treasurys, even when they had only a 2% yield.)

I’m danged if I know why. But so far this year, once again, you’ve been better off in a portfolio of 60% stocks, 30% bonds and 10% gold than in just 60% stocks and 40% bonds. Make of it what you will.

At a time when many investors seem euphoric, others are warning that stock valuations have once again turned frothy. It may pay to take a look back at valuation and performance and consider your own risk tolerance.

A value-based approach that offers lower volatility and good long-term returns can be expected to be less flashy than one focused on the hottest technology stocks. But depending on how much it bothers you when the stock market gyrates, it may be a better way for you to invest. Lower volatility might help you to avoid the type of emotional reaction that can lead to selling into a declining market or attempting to time the market, both of which tend to be losing strategies.

Aaron Dunn is a co-head of the value equity team at Eaton Vance, which is based in Boston and is a unit of Morgan Stanley. During an interview, he explained how he and Brad Galko, who co-heads the team, select stocks for the Eaton Vance Focused Value Opportunities Fund. The fund’s performance benchmark is the Russell 1000 Value Index RLV, +1.08%.

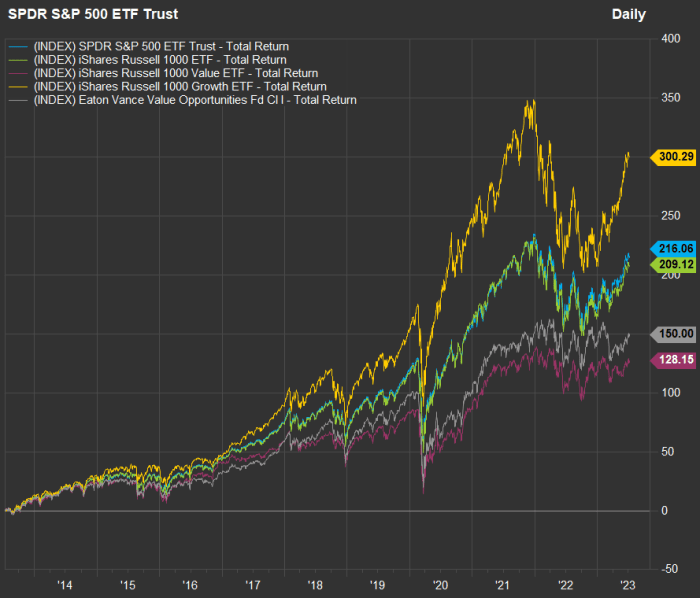

First, let’s take a broad look at how aggregate forward price-to-earnings ratios have moved for exchange-traded funds tracking several broad indexes over the past 10 years:

FactSet

The valuations are lower than their 2020 peaks. But for all but one, the valuations still appear to be high when compared with their 10-year averages:

All of the listed ETFs listed here are trading well above their 10-year average P/E valuations except the iShares Russell 1000 Value ETF, which is only slightly higher. These numbers back the notion that the broad market is expensive and that a value approach may be more reasonable. It is also worth keeping in mind that during 2022, when the SPDR S&P 500 ETF Trust SPY, +0.64%

declined 18.2% and the iShares Russell 1000 ETF IWB, +0.80%

fell 19.2%, the iShares Russell 1000 Value ETF IWD, +1.07%

pulled back 7.7% and the Eaton Vance Focused Value Opportunity Fund’s Class I shares were down only 3.3%, all with dividends reinvested.

If we look at 10-year total returns, the nonvalue indexes, so heavily weighted to the largest technology-oriented companies, have been excellent performers for investors who could remain committed through thick and thin:

For five and 10 years, the growth-oriented approaches have shined. But for three years, which includes the 2022 disruption, the Eaton Vance Value Opportunities Fund has fared best, even outperforming its benchmark.

A selective approach to value

The Eaton Vance Focused Value Opportunity Fund’s Class I EIFVX, +0.92%

shares are rated four stars (out of five) within Morningstar’s Large Value fund category. The fund’s Class A EAFVX, +0.93%

shares are rated three stars. The difference is that the Class I shares, which are typically distributed through investment advisers, have annual expenses of 0.74% of assets under management, while the Class A shares have an expense ratio of 0.99%. You can purchase Class I shares directly through brokerage platforms for a $50 fee.

Dunn said that when selecting stocks for the fund, he and Galko take a bottom-up approach to identify quality companies. The want to see high returns on invested capital (ROIC) over the long term, as well as a “good competitive position” for a company and a strong management team.

They also prefer companies with low debt. “We do not want to buy overlevered companies and be in a situation where we are diluting through equity raises and putting capital at risk,” he said.

Dunn added that he and Galko look closely at free cash flow generation. A company’s free cash flow is its remaining cash flow after capital expenditures. This is money that can be used to fund expansion, acquisitions, dividend increases or share buybacks, or for other corporate purposes.

“Philosophically, what this results in is that we hold up well in markets such as last year’s. And we find upside in stocks trading below intrinsic value,” he said.

“We focus on finding ideas where there is a good skew for upside relative to downside,” he added.

According to Morningstar, the fund’s active share when compared with IWD is high, at 91.45%. Active share is a measure of how much an actively managed fund differs in investment exposure from its benchmark index. If you are paying more for active management than you would to invest in an index fund, active share is something to consider. If it is low, you might be overpaying for a “closet indexer.” You can read about how Morningstar assesses active shares here.

The fund is concentrated, typically holding between 25 and 45 companies.

According to Morningstar’s most recent data, these were the fund’s top 10 holdings (out of 28 stocks) as of May 31:

There is no forward price-to-earnings ratio for Micron Technology Inc. MU, +1.79%,

because the company’s combined EPS for the next 12 months are expected to be negative.

Micron is a company in transition, caught up in diplomatic conflict between the U.S. and China, whose government directed some manufacturers in May to stop purchasing memory chips made by the company. Then again, in June, Micron highlighted its “commitment to China” when announcing a new investment in its plant in Xi’an.

Dunn said downside for Micron’s stock was “mitigated” because of the company’s relatively low debt. He also said that as companies continue to adopt more cloud services and deploy artificial-intelligence technology, demand for memory chips will increase.

While there is no current forward P/E for Micron, the stock always trades at low valuations relative to most other large tech companies. Dunn touted Micron’s strong cash flow and said the stock was “underappreciated” and remained “an interesting play on cloud and AI.”

While it is not among the top 10 holdings listed above, Dunn highlighted Dollar Tree Inc. DLTR, +1.80%

as an example of the type of value stock he favors. The company “was not well run” following its acquisition of Family Dollar in 2015. But he has been impressed with its more recent turnaround efforts, including improvements in how products are shipped to stores, better efficiency and “a lot of work going on with culture, how they operate, how they treat employees [and] adding some shelf space to move more product.”

It is interesting to see NextEra Energy Inc. NEE, +0.67%

among the fund’s largest holdings. This has been quite a strong grower over the past 10 years, with a total return of 346% as the owner of Florida Power & Light has grown along with its customer base and has become a leader in the build-out of solar-power generation.

Dunn said the company is “still growing in the mid-single digits. For a utility company, that is a strong profile.”

When discussing Alphabet Inc. GOOGL, +0.59%,

the fund’s largest holding as of May 31, Dunn said that “it is really an advertising business with other businesses around it” and that its P/E valuation was “not extremely taxing.” He said Alphabet had been “less aggressive with cost cutting” than other technology giants and added that the company’s “targeted search” through Google and other properties, such as YouTube, “probably provides a better return on investment than broadcast advertising, and that really is the key.”

If you’re a retiree and you’re trying to square the circle of rising costs, longer lifespans, more expensive medical care and turbulent markets, don’t be afraid to run the numbers on your biggest investment.

That would be your home — if you own it.

U.S. house prices are now so high that it is almost impossible for seniors not to ask themselves the obvious question: “Should we cash in, invest the money, and rent?”

Right now the average U.S. house price is nearly $360,000. That’s about a third higher than just a few years ago, before the COVID-19 pandemic. The lockdowns, the panic, the stimulus checks and 2.5% mortgage rates have all passed into history. But the sky-high prices remain — for now.

After several years of double-digit percentage increases, apartment-rent growth is falling for only the second time since the 2008 financial crisis. WSJ’s Will Parker joins host J.R. Whalen to discuss.

There is a similar story for seniors. Federal data show that the average U.S. house price is now nearly 17 times the average annual Social Security benefit — an even higher ratio than it was in August 2008, just before Lehman Brothers collapsed. At that juncture, the average house price was 15 times higher.

U.S. National Home Price Index vs. average rent of primary residence in U.S. city, according to the U.S. Bureau of Labor Statistics. Indexed: January 1987=100.

S&P/Case-Shiller

Our simple chart, above, compares average U.S. home prices with average U.S. rents, going back to 1987. (The chart simply shows the ratio, indexed to 100.) The bottom line? House prices are very high at the moment compared with rents — again, prices are about where they were in 2006-07.

And the two must run in tandem over the long term, because the economic value of owning a house is not having to pay rent to live there.

If there are times when, in general, it makes more financial sense for seniors to rent than to own, this has to be one of those.

Seniors who own their own homes may think high interest rates on new mortgages don’t affect them. They most likely either already have a mortgage at a lower, older rate or they’ve paid off their home loan. But if you want to sell, you’ll almost certainly be selling to someone who needs a mortgage.

If borrowing costs drive down real-estate prices, seniors who hold off on selling may miss out on gains they may never see again. After the last housing peak, in 2006, it took a full decade for prices to recover fully. Those who sold when the going was good had the chance to buy lifetime annuities at excellent rates or to invest in stocks and bonds that overall rose about 80% over the same period.

Incidentally, there is also an exchange-traded fund that invests in residential REITs, Armada’s Residential REIT ETF HAUS, -0.53%,

though in addition to single-family homes and apartment-complex operators, about 25% of the fund is invested in companies involved in manufactured-home parks and senior-living facilities.

For each person, the math will be different, and there are a number of questions you need to ask. Where do you want to live? How much would you get if you sold your house? How much would you pay in taxes? How much would it cost to rent the right place? Do you want to leave a property to your heirs? And what would be the costs of moving — both financial and emotional?

The conventional wisdom is that you should own your home in retirement.

“I would advise any and all retirees against renting if at all possible,” says Malcolm Ethridge, a financial planner at CIC Wealth in Rockville, Md. “You need your costs to be as fixed as possible during retirement, to match your income being fixed as well. If you choose to rent, you’re leaving it up to your landlord to determine whether and by how much your No. 1 expense will increase each year. And that makes it very tough to determine how much you are able to allocate toward everything else in your budget for the month.”

A key point here, from federal data, is that nationwide rents have risen year after year, almost without a break, at least since the early 1980s. They even rose during the global financial crisis, with just one 12-month period where they fell — and then by only 0.1%.

“My general advice for clients is that owning a home with no mortgage in retirement is the best scenario, as housing is typically the highest cost we pay monthly,” says Adam Wojtkowski, an adviser at Copper Beech Wealth Management in Mansfield, Mass. “It’s not always the case that it works out this way, but if you can enter retirement with no mortgage, it makes it a lot easier for everything to fall into place, so to speak, when it comes to retirement-income planning.”

“Renting comes with a lot of risk,” says Brian Schmehil, a planner with the Mather Group in Chicago. “If you rent, you are subject to the whims of your landlord, and a high inflationary environment could put pressure on your finances as you get older.”

But it’s not always that simple.

“With housing costs as high as they are now though, renting may be a viable solution, at least for the moment,” says Wojtkowski. “We don’t know what the housing-market trends will be going forward, but if someone is waiting for a housing-market crash before they move, they could very likely be waiting for a long time. We just don’t know.”

“Any decision comes with pros and cons,” says Schmehil. “Selling when your home values are historically high and renting allows you to capture the equity in your home, which is usually a retiree’s largest or second-largest financial asset. These extra funds allow you to spend more money on yourself in retirement without having to worry about doing a reverse mortgage or selling later in retirement, when it may be harder for you to do so.”

Renting also allows you to be more flexible about where you live, for example nearer your children or grandchildren, he adds.

And as any experienced property owner knows, renting also brings another benefit: You no longer have to do as much work around the house.

“Renting is great in that you don’t need to maintain a residence,” says Ann Covington Alsina, a financial planner running her own firm in Annapolis, Md. “If the dishwasher breaks or the roof leaks, the landlord is responsible.”

Wojtkowski agrees, noting that many people no longer want to spend time mowing the lawn or shoveling snow in retirement. “Ultimately, one of the things that I’ve seen most retirees most concerned with is eliminating the general upkeep [and] maintenance of homeownership in retirement,” he says.

Several planners — including Covington Alsina and Wojtkowski — note that one alternative to selling and renting is simply downsizing. This can free up capital, especially when home prices are high, like now, without leaving you exposed to rising rents.

Many baby boomers have been doing exactly that.

Meanwhile, I am reminded of my late friend Vincent Nobile, who — after a long and fruitful life owning homes and raising a family — found himself widowed and alone in his 80s. He rented a small cottage on a New England sound and said how glad he was that he never had to worry about maintaining the roof or the appliances, or fixing the plumbing or the heating, or any one of a thousand other irritations. Or paying property taxes — which go down even more rarely than rents.

When the regular drives to Boston got too onerous, he moved into the city and rented there. And he was glad to do it. The money he had made was all in investments — a lot less hassle both for him and his heirs.

I once asked him if he would prefer to own his own home. He shook his head and laughed.

Shares of electric vehicle makers got a broad boost Monday, after upbeat delivery and production data from a host of companies, including industry leader Tesla Inc. and those based in China.

The Global X Autonomous and Electric Vehicles exchange-traded fund DRIV, +1.08%

jumped as much as 1.7% intraday, before paring gains to close up 1.1%. It has climbed 5.7% amid a five-day win streak. The ETF outperformed the broader stock market by a wide margin, as the S&P 500 index SPX, +0.12%

inched up 0.1% and the Nasdaq Composite COMP, +0.21%

edged up 0.2%.

The ETF’s most-active component was Tesla’s stock TSLA, +6.90%,

which climbed 6.9% to $279.82, the highest close since Sept. 28, 2022. It has run up 16.1% amid a five-day win streak.

The rally comes after Tesla revealed over the weekend a blowout deliveries report, in which the EV leader said it delivered a record 466,000 vehicles in the most recent quarter, well above expectations of 449,000.

The ETF’s second-most active member was Rivian Automotive Inc.’s stock RIVN, +17.41%,

which shot up 17.4% to its highest close since Feb. 17, and rocketed 45.4% amid a five-day win streak.

Nio Inc.’s U.S.-listed stock NIO, +3.51%

rallied 3.5% to $10.03, the first close above the $10 mark since March 31, after the Shanghai-based EV maker reported June deliveries that jumped 74% from May, but were down 17.4% from a year ago.

Among its China-based peers, the U.S.-listed shares of Xpeng Inc. XPEV, +4.17%

advanced 4.2% to the highest close since Sept. 26, 2022, of Li Auto Inc. LI, +3.42%

hiked up 3.4% to the highest close since July 21, 2022 and of Boyd Co. Ltd. BYDDY, +3.07%

rose 3.1%.

Elsewhere, Lucid Group Inc. shares LCID, +7.26%

charged 7.3% higher to a record sixth-straight gain and the highest close since May 31, as the EV sector’s rally helped offset an effective downgrade at Citi Research.

In an interview on YouTube channel “Financial Journey,” as disclosed on Friday, Mullen Chief Executive Officer David Michery said he doesn’t believe the stock’s price reflects the true value of the company.

He said he expects manufacturing of the Mullen One class 1 last-mile delivery cargo vans to begin in August with “sellable” vehicles available in September.

For the Mullen Three class 3 trucks, with a gross vehicle Weight Rating (GVWR) of 11,000 pounds, Michery said manufacturing will start “right around the corner” in July, with sellable vehicles in August and September.

A nascent category of mental health treatments is getting a major cash infusion.

Blake Mycoskie, founder of the canvas-footwear phenomenon TOMS Shoes, has committed to giving $100 million to support psychedelic research and access, Mycoskie told MarketWatch in an exclusive interview. The money will help fund academic institutions investigating psychedelics’ potential to treat anxiety, depression, post-traumatic stress disorder and other mental-health issues, as well as nonprofits helping to connect patients in need with psychedelic treatments.

Traditional psychedelics include hallucinogens like LSD and psilocybin, or “magic” mushrooms–recently legalized in Oregon and Colorado. Other drugs that can alter mood and perception–such as ketamine and MDMA, also known as ecstasy–aren’t classical psychedelics but are broadly included in the research and policy discussions generating a surge of interest in this class of treatments. The U.S. Food and Drug Administration, for example, has granted psilocybin and MDMA “breakthrough therapy” status, a designation designed to expedite development and review of drugs for serious conditions, and could approve MDMA for treatment of PTSD as soon as next year.

Given the rapid developments in the field, ”we really need to get this right, and we really need to have these foundations and nonprofits funded properly,” therapists trained, and clinics open and running smoothly, Mycoskie said. “I felt a real sense of urgency,” he said, and asked his wealth manager, “what’s the most that I can give?”

The $100 million answer to that question amounts to about a quarter of Mycoskie’s net worth and marks a major milestone in psychedelics’ delicate image transformation. Shedding some of their dangerous-party-drug reputation, psychedelics are gaining attention from top pharmacologists, the scientific community, biotech companies and investors who see them as a critical part of the solution to America’s mental health crisis.

Cracked open

Mycoskie, 46, said his interest in psychedelics dates back to 2017, when a friend returning from a trip to Central America described his incredible experience with ayahuasca, a plant-based psychedelic brewed into a tea. As an entrepreneur under intense pressure to perform, Mycoskie said, he decided to try it for himself. The experience “cracked me open, and it connected me more to my faith in God, made me feel that we were all connected and everything was fine and perfect,” he said. “I came back just feeling like, wow, that was more powerful than any therapy I’d ever done.” He later tried MDMA-assisted therapy, he said, which also helped him process issues that traditional talk therapy had left unresolved.

Realizing how many people could benefit from similar treatments, Mycoskie started giving money to academic groups and the Multidisciplinary Association for Psychedelic Studies, or MAPS, a nonprofit organization. He also got involved in last year’s Colorado ballot initiative, which legalized psilocybin and several other psychedelic substances, including ibogaine, which has shown potential to treat substance-use disorders. Mycoskie has already given about $10 million to psychedelic research and access, he said, and plans to give about $5 million annually for 18 more years.

Mycoskie was a bit squeamish at first, he acknowledges, about publicly backing research on drugs that are largely illegal. “Am I going to get held up at TSA every time I go through the airport?” he remembers thinking. The U.S. Drug Enforcement Administration categorizes LSD and MDMA alongside heroin as “schedule one” drugs, defined as “drugs with no currently accepted medical use and a high potential for abuse.” But with growing public awareness and acceptance of the drugs’ potential as mental-health treatments, he said, he felt emboldened to make a big public commitment, and “the research has caught up,” he said. “It’s important that people like myself put their name out there and their money out there to show that this really is a path forward,” he said.

Mycoskie’s $100 million commitment “is the biggest that we’ve ever seen in the psychedelics space,” said Joe Green, president of the Psychedelic Science Funders Collaborative, a nonprofit supporting philanthropy in the field, and a MAPS board member. Now that research has made great strides to support use of the medicines as mental-health treatments, that money can help ensure that “these actually come to the world in a safe and beneficial way,” Green said. With certain treatments legalized in Oregon and Colorado, for example, “the system requires licensed guides, facilitators, licensed service centers,” he said. “It’s not like cannabis medical–you won’t be able to take the mushrooms outside the service center.”

Psychedelic therapeutics market could be worth more than $8.3 billion by 2028

Mycoskie plans to publicize his pledge at the Multidisciplinary Association for Psychedelic Studies’ psychedelic science conference–billed as “the largest psychedelic conference in history”–this week in Denver. On the agenda: Sessions ranging from state policy and regulatory considerations to clinical trials of psilocybin- and MDMA-assisted therapy and “sex and psychedelics: weaving altered states for healing and pleasure.”

The news comes as lawmakers on both sides of the aisle are pushing for new funding for research into the use of psychedelics to treat PTSD in military service members as part of the fiscal year 2024 National Defense Authorization Act, which the House Armed Services Committee will consider Wednesday.

Already, public companies like Atai Life Sciences ATAI, -6.91%,

Compass Pathways CMPS, -3.37%

and Cybin CYBN, +6.81%

are developing therapies based on psychedelic substances. The psychedelic therapeutics market could be worth more than $8.3 billion by 2028, according to InsightAce Analytic. Even the federal government is throwing money at this niche, funding efforts to develop psychedelic mental-health treatments without the hallucinogenic side effects.

More than one in five U.S. adults live with a mental illness, according to the National Institute of Mental Health, and less than half of the roughly 58 million adults with any mental illness are receiving treatment. Suicide rates, which have been on a long upward trajectory, declined briefly between 2018 and 2020 before returning to peak levels in 2021, according to the Centers for Disease Control and Prevention. Nine out of 10 U.S. adults believe the country is suffering a mental health crisis, according to a survey last year by CNN and KFF, a health policy nonprofit. And commonly prescribed antidepressants, such as selective serotonin reuptake inhibitors (SSRIs) don’t work well for many patients.

Nushama, a New York City wellness center offering ketamine-based therapy.

Courtesy of Nushama and Costas Picadas

Mental illness “is truly an epidemic, and we are losing the fight,” said Dylan Beynon, CEO and founder of Mindbloom, which offers a telehealth ketamine treatment program. While there are some existing solutions that are helping to bend the curve, he said, more research and educational support for providers and patients is needed, he said.

Indeed, some substantial hurdles still separate psychedelic mental-health treatments from many of the patients they might benefit, including a lack of insurance coverage for the currently legal treatments and debate over how to administer them safely. In the case of ketamine, for example, which is FDA-approved as an anesthetic and used off-label as a mental-health treatment, some providers favor in-person guided sessions while others, like Beynon, advocate for telehealth prescribing–a model that boomed during the pandemic.

Some experts have lately warned that the practice of psychedelic medicine may be getting ahead of the science. Given the growing public and commercial interest, “there is the risk that use of psychedelics for purported clinical goals may outpace evidence-based research and regulatory approval,” the American Psychiatric Association said last year in a position statement on psychedelic and “empathogenic” agents–a category that includes MDMA.

Mycoskie has also made some investments in the psychedelics space, although he said profits aren’t his motivation. He has invested in Mind Medicine Inc. MNMD, -0.50%,

which says it is developing “psychedelic inspired medicines” that aim to treat the underlying causes of distress in the brain. And Mycoskie helped fund a public benefit corporation linked with MAPS, which is taking MDMA through the FDA approval process–an investment that will pay dividends when the treatment is commercialized, he said.

Providers currently offering ketamine treatments say they’re eager to expand into MDMA and other therapies in the category as soon as they’re legal. Mindbloom, for example, currently offers a ketamine treatment program that’s available through telehealth in several dozen states and aims to start offering MDMA-assisted therapy late next year after FDA approval is finalized, Beynon said. Psilocybin-assisted therapy could come a couple of years after that, he said.

Nushama, a New York City psychedelic wellness center that offers ketamine-based therapy, delivered through in-person IV infusions, also hopes to expand into MDMA when it’s approved, said co-founder Jay Godfrey.

Treatment without the trip

Still on the horizon: New treatments that could produce psychedelic medicines’ mental-health benefits without the trip. University of North Carolina School of Medicine pharmacology professor Dr. Bryan Roth is leading an effort to create new medications for depression, anxiety and substance abuse that work similarly to psychedelics but without the hallucinogenic, disorienting side effects. His effort is backed by a $27-million grant from the Defense Advanced Research Projects Agency. Such treatments, Roth said, could help the many patients for whom such psychedelic effects are unappealing or ill-advised–such as military service members. “You would never want to give psilocybin or ketamine to somebody who has a gun,” Roth said.

Having worked with Vietnam veterans suffering from PTSD while training as a psychiatrist earlier in his career, Roth said, he’s keenly aware of the need for safe and effective treatments. “There was nothing we could give them for their symptoms,” he said. “The most we could do was give them medications to stop their ability to have dreams, so they wouldn’t have nightmares. That was basically it.”

“Undoing 52 years of propaganda is a heavy lift,” said Nushama co-founder Jay Godfrey.

Costas Picadas

Roth’s team has already developed compounds that have shown antidepressant effects without psychedelic side effects in mice, he said. The team is now working to find a clinical candidate suitable for testing in humans, he said.

Treatments that can help “break bad emotional or psychological patterns without scary, high-friction psychedelic experiences would be a great thing for patients, providers and the healthcare system,” said Mindbloom’s Beynon.

Much more remains to be done to reduce the stigma associated with psychedelics, experts say. It has been 52 years since President Richard Nixon declared drug abuse “public enemy number one,” and billions of dollars have been spent since then telling people that “these medicines are dangerous, that they’re addictive, and that they’ll fry your brains,” Godfrey said. “Undoing 52 years of propaganda is a heavy lift, but one thing I’m optimistic about is that the outcomes are starting to speak for themselves.”

This copy is for your personal, non-commercial use only. To order presentation-ready copies for distribution to your colleagues, clients or customers visit http://www.djreprints.com.

BlackRock, the world’s largest asset manager, has filed an application for a spot bitcoin exchange-traded fund.

There are currently no such products in the U.S. The SEC approved several bitcoin BTCUSD futures-based ETFs in the past, but has yet to greenlight anything that is backed by bitcoin itself.

Even with U.S. stocks in a new bull market, investors aren’t showing many signs of backing away from money-market funds and other cash-like investments offering yields of about 5%, the highest in about 15 years.

Money-market funds hit a record of $5.9 trillion in assets as of Tuesday, signaling a continuing drain out of bank deposits into higher-yielding “cash-like” investments, according to Peter Crane, president and publisher of Crane Data.

If there were no tax cheats in America, there would be no Social Security crisis. Benefits could be paid, and payroll taxes kept the same, for the next 75 years.

That’s not me talking. That’s math. It comes from the number crunchers at the Social Security Administration and the Internal Revenue Service.

And it explains why those of us who support Social Security should be pounding the table in outrage over one clause of the Biden-McCarthy debt ceiling deal: The part where the president has to retreat from his crackdown on tax cheats just so McCarthy and the House Republicans would agree to prevent America defaulting on its debts.

It’s just two years since the administration got into law an extra $80 billion for the IRS to beef up enforcement. That was supposed to include hiring an estimated 87,000 IRS agents.

OK, so nobody likes paying taxes and nobody likes the IRS. Cue the inevitable critiques of an IRS tax “army,” and so on. But this isn’t about whether taxes should be higher or lower. It’s about whether everyone should pay the taxes that they owe.

After all, if we’re going to cut taxes, shouldn’t they apply to those of us who obey the laws as well as those who don’t? Or do we just support the “Tax Cuts for Criminals” Act?

Why would any voter rally around a platform of “I stand with tax cheats?”

If this seems abstract, consider the context and how it affects you and your retirement — and the retirements of everyone you know.

Social Security is now running at an $80 billion annual deficit. That’s the amount benefits are expected to exceed payroll taxes this year. (So say the Social Security Administration’s trustees.)

Next year, that deficit is expected to top $150 billion. By 2026, we’re looking at $200 billion and rising. The trust fund will run out of cash by 2034, and without extra payroll taxes will have to slash benefits by a fifth or more.

Over the next 75 years, says the Congressional Budget Office, the entire funding gap for the program will average about 1.7% of gross domestic product per year.

Meanwhile, how much are tax cheats stealing from the rest of us? A multiple of that.

But it still worked out at around 12% of all the taxes people were supposed to pay (including payroll taxes). And around 2.3% of GDP.

Over the next 10 years, based on similar ratios to GDP, that would come to another $3.3 billion.

Sure, Social Security’s trust fund is theoretically separate from the rest of Uncle Sam’s finances. But that’s an accounting issue: A distinction without a difference.

Some people want to cut benefits. Others want to raise the retirement age, which also means cutting benefits. Others want to raise taxes on benefits — which also means cutting benefits. Others want to hike payroll taxes, either on all of us or (initially) only on very high earners.

But if investing some of the trust fund in stocks is a no-brainer, so, too, is insisting everyone obey the law and pay the taxes they actually owe each year. I mean, shouldn’t we do that before we think about raising taxes even further on those who abide by the law?

How could anyone object? Any party that believes in law and order would support enforcing, er, law and order on tax evasion. And any party of fiscal conservatism would support measures, like tax enforcement, to narrow the deficit.

And, actually, any party that truly supported lower taxes for all would be tough on tax evasion: It is precisely this $500 billion in evasion by a small, scofflaw minority that forces the rest of us to pay more. We have, quite literally, a tax on obeying the law.

“‘Icahn’s favorite Wall Street saying: “If you want a friend, get a dog.” Over his storied career, Icahn has made many enemies. I don’t know that he has any real friends. He could use one here.’”

— Bill Ackman, Pershing Square Capital Management

That was billionaire hedge-fund manager Bill Ackman, founder and chief executive of Pershing Square Capital Management, resurrecting his longstanding feud with billionaire activist investor Carl Icahn in a tweet Wednesday.

Ackman was referencing the fallout from the recent report by short-selling firm Hindenburg Research that accused Icahn’s publicly traded investment vehicle, Icahn Enterprise Partners LP IEP, -13.83%,

of inflating asset values and causing his company to trade at a large premium. The report from May 2 has cost IEP about $10.9 billion in lost market cap, after the stock tumbled another 21% on Thursday.

Ackman said he is neither long or short IEP but merely “watching from a distance.”

But he seemed to agree with Hindenburg’s founder and CEO, Nate Anderson, who questioned margin loans extended to Icahn using his roughly 85% stake in IEP as collateral. Icahn has not disclosed the terms of those loans although he recently told the Financial Times that he used the money to make additional investments outside of his publicly traded vehicle.

“Over the years I have made a great deal of money with money,” he was quoted as having said. “I like to have a war chest, and doing that gave me more of a war chest.”

Ackman said the margin lender or lenders “must be extremely concerned with the situation,” particularly after IEP has disclosed a federal investigation of its business and corporate governance.

For his part, Icahn has called Hindenburg’s analysis “misleading and self-serving” and said it was designed solely to hurt long-term IEP shareholders.

Ackman compared the situation to that of failed investment fund Archegos, “where the swap counterparties were comforted by each having relatively smaller exposures to the situation.”

“The problem is that multiple lenders make for a more chaotic situation. All it takes is for one lender to break ranks and liquidate shares or attempt to hedge, before the house comes falling down. Here, the patsy is the last lender to liquidate.”

Ackman also expressed his surprise that Icahn has not disclosed the margin-loan terms, or even said who provided them. “My understanding of 13D SEC rules is that they require disclosure of sources of financing and even copies of financing agreements, although many investors ignore these requirements.”

Ackman also questioned how IEP’s large dividend yield is feasible, as it’s not supported by operating cash flows.

“The yield is generated by returning capital to outside shareholders, which is in turn funded by the company selling stock to investors,” said Ackman.

Icahn’s problem now is that his system has been outed by the short seller, Ackman wrote.

“Transparency is not the friend of $IEP having caused a more than 50% decline in the shares, which has caused Icahn to post more shares, now more than 65% of his holdings,” he said in the tweet.

The bad blood between Icahn and Ackman goes back to a business dispute the two had over a 2003 deal involving Hallwood Realty. The litigation between them went on for years.

But their animosity for one another hit a crescendo in 2013, when Bill Ackman publicly waged a $1 billion short-selling campaign against Herbalife. Sensing weakness, Icahn took a long position in Herbalife’s stock HLF, -5.21%

and helped deal Ackman significant losses on his bet over time.

The two claimed they had made up in 2014, sharing a stage at a conference broadcast by CNBC.

Ackman had previously had taken a soft shot at Icahn over the Hindenburg report, saying there was a “karmic quality” to it. But now their battle of Wall Street titans appears to be back in full force.