Swiping your credit card has now become more expensive than ever, and it’s because credit card interest rates are rising crazy fast. That’s why we think you should call your credit card company and ask for a better rate — pronto.

We’re serious about this! But first, let us explain:

Your credit card’s interest rate, also known as an APR, has probably gone up just like all the other credit cards have. (Most credit cards have a variable rate.) Have you checked lately? If you have an unpaid balance, your card is probably charging you a surprising amount of interest on it right now.

Suddenly our credit cards are bleeding us dry. Here’s how fast rates are rising:

As recently as 2017, the average APR on a credit card was lower than 13%, according to the Federal Reserve. Then, from 2018 to the start of 2022, it usually hovered around 14.5%. But over the past year it started climbing with breakneck speed, and now the average APR has climbed above 19% — the highest it’s ever been.

There’s no end in sight, with plenty of financial experts predicting the average rate will rise above 20% in 2023.

You don’t have to sit still for this. Just take a little initiative and call your credit card provider.

Don’t be chicken. The phone number for customer service is right there on the back of your credit card.

You have nothing to lose!

Just Ask for a Lower Rate

Look at your latest credit card statement. Check your credit card’s interest rate. If you have more than one credit card, check all your cards. Are any of your cards charging more than 19% interest? If so, then you definitely need to negotiate that down.

If you’re unhappy with your APR, ask for it to be lowered. Do this for each of your cards.

A few things to keep in mind:

If you have a history of making your monthly payments on time, make sure to mention that.

Are you getting any offers in the mail from other credit card providers? Make sure to mention that, too. Your credit card company doesn’t want to lose your business.

Do a little homework before making that call. See if you can find a better offer for a comparable credit card — one that’s roughly similar to yours.

If you’ve had the same credit card for a long time, mention what a loyal customer you are.

The worst thing they can do is say “no.” Big deal.

How to Pay Off Credit Card Debt

It’s worth trying this because credit card debt is the most expensive kind of debt you can have. Credit cards charge you higher interest than mortgages, car loans, personal loans or lines of credit.

Most credit cards have a variable interest rate that follows what the Federal Reserve does, and the Fed keeps raising interest rates in an effort to fight runaway inflation. That’s why you can expect your credit card APR to go up, not down — at least for now.

If possible, the best thing you can do for yourself is to avoid leaving an unpaid balance on your credit card, month after month. Those interest payments add up.

Get a balance transfer credit card. If you have good to excellent credit (typically a FICO score of 670 or above) and can feasibly pay off your debt within a year, a balance transfer credit card is a solid option. Transfer the balance of a card with a high interest rate to a card that’ll charge you 0% interest for 12-18 months.

Get a debt consolidation loan. If you get a loan with a lower interest rate and pay off your credit cards, that lower rate could potentially save you thousands of dollars in interest. This is a realistic way to pay off credit card debt if you currently have little or no money to put toward it. It’s easier than you think to get a personal loan online or from your bank. If you’re a homeowner, you might think about a home equity loan.

Follow a debt repayment strategy. Two popular ways to break down debt repayments are the debt avalanche and debt snowball methods. Using the debt avalanche method, you’ll pay off your highest interest card first. With the debt snowball method, you’ll pay off the smallest balances first.

Remember, don’t get stuck in the credit card trap. Nowadays, swiping that plastic is pricier than ever.

Mike Brassfield ([email protected]) is a senior writer at The Penny Hoarder.

Opinions expressed by Entrepreneur contributors are their own.

If you need funds for your enterprise, it can be very tempting to go for the first business loan on offer. However, there are a number of things you should look for before you sign on the dotted line.

1. The right loan type

As with personal finance, there are several different forms of business loans, so you need to choose the one that best suits the needs of your enterprise.

Traditional loans: These are the business equivalent of a personal loan, which can be secured or unsecured. You’ll borrow a set amount and have a set repayment schedule with a fixed interest rate.

Line of credit: A line of credit provides you with a set funding amount but you don’t need to receive and pay interest on the full amount. You can call down funds as you need them and you’ll only pay interest on the amounts you borrow.

Equipment financing: If you need funds to purchase equipment, this type of business lending is designed to suit your needs. The piece of equipment you purchase will act as collateral for the loan, so you can usually access more flexible terms.

SBA loans: SBA or Small Business Administration loans are an option if you would struggle to qualify for a bank business loan. The lending criteria is more flexible, which could be a more agreeable choice for new enterprises.

Before you agree to a business loan offer, it is well worth assessing the other types of business lending to confirm the loan is the best fit for your enterprise.

2. Manageable loan repayments

Before you sign the loan contract, you should have an opportunity to check the details of the loan repayment requirements. You will need to think carefully about whether you can comfortably accommodate the monthly payment in your budget, not only now but throughout the lifetime of the loan.

If you have concerns that the payments may be difficult, or you may struggle to meet the payment deadlines, it is best to look for another loan product. Missed or late payments can not only create additional financial stress but can have a massive impact on your credit.

This follows on from the previous point, but you should also be fully aware of what fees you will incur with your new business loan. In addition to paying interest, you may incur origination fees, and processing fees. These will be added to your loan principal or you’ll need to pay them upfront. Ideally, your new business loan will have little or no such fees.

You also need to watch for the fees you may incur during the lifetime of the loan. For example, you don’t want to get stung with a massive late fee if there is a mix-up at the bank. It is also a good idea to look out for early repayment fees. If your business finances change and you want to clear the loan, you won’t want a loan that imposes a hefty early repayment fee.

4. A good lender reputation

Unfortunately, not every lender in the market offers the same level of service, in fact, some can be downright risky. The adage of “too good to be true” certainly applies here. So, it is vital to investigate the lender’s reputation and be on the lookout for some red flags. These include:

No verifiable credentials: If the lender does not have a professional website and does not provide details of a physical address.

Lack of fee transparency: Lenders should be very clear about their loan fee structure, so you are completely aware of how much the financing options will cost.

Pressure selling: If the sales rep is trying to pressure you to immediately accept a business loan offer without presenting you with information and the time to study it.

5. The correct loan amount

While it may be tempting to get the biggest business loan you can get approved for, this is not likely to be a good idea. Likewise, if the loan offer won’t cover your immediate funding needs, it is not the right choice.

Think carefully about what funds you need and how you’ll use them, so you can be sure to obtain a loan for the correct amount.

6. An attractive interest rate

As with any form of finance, your interest rate will determine the cost of your business loan. Lenders will use a variety of criteria to determine your risk profile and therefore your rate. However, these criteria vary from lender to lender, with some lenders being more rigid and some lenders being more flexible.

If you have a brand new enterprise, you’re not likely to get the best rates, unless you have excellent credit yourself. But, it is still important to compare rates to ensure that you’re getting the lowest possible rate for your enterprise.

However, you may be prepared to pay a slightly higher interest rate if there are minimal fees or other benefits to the loan. So, don’t look at the interest rate comparisons without some context.

While you may not need the funds urgently, you are still likely to want to implement your plans as soon as possible. So, check the funding times each lender offers for their business loans. After you submit your application and receive approval, when can you expect to receive the funds in your bank account?

Some lenders can release funds in 24 hours or only a few days, but other lenders are slower. If you will have to wait weeks or months for your funds, it is a good idea to look at alternative options.

8. Solid customer support

Finally, it is worth checking the levels of customer support offered by your potential lenders. If you have queries or questions about your loan, can you speak to the support team quickly? Some lenders have phone helplines, while others rely solely on email or chat. So, you need to be comfortable with the customer support options.

It is well worth reading some reviews of the lender to see if there are any red flags about long call wait times, slow responses to emails or other customer support issues before you become a customer.

Bottom line

Getting the right business loan for your needs requires some time to compare the different aspects and lenders. When you follow the factors above and make sure to maximize each of them, you can save money, time and financial stress.

A mild stock market rally to kick off the new year will be put to the test Thursday when investors face a highly-awaited U.S. inflation reading which could well help determine the size of the Federal Reserve’s next interest-rate increase.

The December CPI reading from the Bureau of Labor Statistics, which tracks changes in the prices paid by consumers for goods and services, is expected to show a 6.5% rise from a year earlier, slowing from a 7.1% year-over-year rise seen in the previous month, according to a survey of economists by Dow Jones. The core price measure that strips out volatile food and fuel costs, is expected to rise 0.3% from November, or 5.7% year over year.

The December CPI will be particularly important for influencing the Fed’s decision in its upcoming meeting which concludes February 1, said economists at Pimco. They expect the inflation and labor market data will have moderated sufficiently will push the central bank to pause rate hikes before their May meeting.

“After hiking 50 basis points at the December meeting, we expect the Fed moves to a 25bp hiking pace in early February, and ultimately pause around 5%,” wrote Pimco’s economists Tiffany Wilding and Allison Boxer, in a Tuesday note.

However, since the Fed’s December meeting, officials have relentlessly signaled the central bank will need to raise interest rates above 5% in order to get inflation to the 2% target, with no interest rate cuts expected this year. Fed funds futures traders now see a 78% likelihood of a 25 basis point hike at its February meeting, and a 68% chance of another in March, which would bring the terminal rate to merely 4.75-5% by mid-year, according to the CME FedWatch tool.

“Inflation swaps currently see inflation falling below 2.5% by the summer of 2023, which seems hopeful,” Kramer said. “This week’s CPI reading will be essential in maintaining that view and could prove disastrous if CPI comes in hotter than expected, veering market-based inflation expectations off course.”

The stock market is looking for an “around 5%” increase in December’s core inflation, said Rhys Williams, chief strategist at Spouting Rock Asset Management. “If you get a number in the low four [percent], the stock-market rally will continue. The market is very hyper-focused on data points.”

U.S. stocks had a positive start to 2023 with hopes that cooling inflation and a potential recession may persuade the central bank to ease off the pace at which it is raising its policy interest rate.

Williams thinks inflation is coming down but it will not hit the central bank’s 2% mark by summer 2023.

“I think at some point the markets will realize, ‘oh we can’t get to 2%,” and then the markets probably do sell off on that. I think maybe in short term [the stocks go] up and then in the second quarter, they go back down as people realize that 2% is not realistic,” Williams told MarketWatch via phone.

In 2022, it seemed like every new day brought another piece of news related to student loans.

Whether it was the Biden administration’s massive forgiveness plan that was announced, then paused, then stalled in the courts or the ongoing payment pauses and rising interest rates, it was definitely a hectic year for both the industry and borrowers alike in 2022.

And guess what? Things don’t seem like they’ll slow down in 2023.

If you’re a student loan borrower, brace yourself for another year of possible highs and lows when it comes to news related to your student loans.

What You Need to Know About Student Loans for 2023

With all the changes made regarding student loans, it can be difficult for borrowers to keep up with everything they need to know. That’s what we’re here for. We’ve rounded up four things you need to know about student loans in 2023.

1. The Student Loan Forgiveness Program Hangs in the Balance

In August 2022, the Biden administration announced its unprecedented student loan forgiveness program — allowing federal student loan borrowers who make less than $125,000 per year (or $250,000 if filing jointly) to be eligible for $10,000 in loan forgiveness. It also allowed Pell Grant recipients to receive $20,000 in forgiveness.

More than 26 million forgiveness applications had been received by the U.S Department of Education — 16 million of which had been approved — when the DOE closed the application after Biden’s plan was challenged in court.

The U.S. Supreme Court will hear oral arguments related to the two ongoing cases in February. The Biden administration is confident its plan will prevail in court, but borrowers will have to wait and see if that $10,000 of sweet loan relief will find its way to them later in 2023.

2. Student Loan Payments Will Return

Because of the uncertainty around the ongoing litigation, the Biden administration announced in November that federal student loan payments would be paused again. This was the eighth extension since March 2020.

This extension will last until 60 days after the litigation is resolved, according to the U.S. Department of Education. If legal challenges are still blocking the forgiveness plan by June 30, 2023, student loan payments will resume 60 days after that.

Barring any more unforeseen delays — and with this program, you just never know — borrowers should expect to resume payments no later than late August 2023.

The payment pause covers all loans backed by the U.S. Department of Education, which includes Direct Loans, subsidized and unsubsidized loans (sometimes called Stafford loans), Parent and Graduate Plus loans and consolidation loans.

If you happen to have Federal Family Education Loans (FFEL) and Perkins loans held by the federal government, they’re covered, too. But the vast majority of those loans are commercially held, which makes them ineligible for the benefit.

3. Interest Rates Will Continue to Rise

At the end of 2022, federal student loan rates sit at 4.99%, well above the 3.73% interest rate during the 2021-2022 school year. The federal government adjusts its student loan rates every July, and they have trended higher ever since a post-pandemic drop.

The federal funds rate — which typically influences all lending interest rates, including student loans — sat at 4.33% in late December and is expected to continue rising.

4. Scammers Will Continue to Prey on Student Loan Borrowers

With the world of student loans in chaos, scammers have a perfect opportunity to take advantage of all the confusion. In the past few years, the Federal Trade Commission has returned millions of dollars to borrowers who were duped by student loan forgiveness scams.

Companies will create names that sound official, such as Student Debt Relief Group, and fake affiliation with the DOE to charge upfront and monthly fees. They say this will be credited towards the borrower’s loans, but it’s all a scam.

The FTC has become heavily involved in fighting these scammers, but they are still out there.

If you’re a borrower, be wary of any “debt relief” company that:

Asks for upfront fees. They’re illegal.

Promises immediate loan forgiveness.

Asks to provide personal information.

Pressures you to sign up for their service.

For more advice on how to spot and avoid student loan scammers in 2023, we’ve got you covered.

Robert Bruce is a senior writer for The Penny Hoarder.

The Federal Reserve is likely to raise interest rates more than the markets now expect, says Ricardo Reis, an economist at the London School of Economics.

“Markets are going to get rocked,” Reis told MarketWatch on the sidelines of the American Economic Association annual meeting in New Orleans.

“All the risks are on the upside. A rate of 5.5% is the minimum,” he added.

Last month the Fed raised the top end of its benchmark rate range to 4.5%. The central bank penciled in a 5.25% terminal rate.

Investors who trade in the fed-funds futures market now expect the Fed to stop raising when rates get to 5%.

Reis thinks the central bank will ultimately move rates higher.

The Fed is burned by failing to recognize the persistent upward move of inflation in 2021, he said.

“So I think they are biased toward over-tightening,” he said. “Either legitimately or because they are worried about fixing their past mistake, there are going to be tighter than you think.”

The economy is at a turning point and the Fed does face some “tough calls,” Reis said.

The key going forward is the path of wages.

Workers need to have their wages go up because their paychecks have not kept up with inflation.

So the Fed is going to have to gauge if the rise in wages is too much, just right or too little, he said.

If wages don’t rise much, inflation can quickly return to the Fed’s 2% target, he said.

If wages rise in line with productivity, the Fed won’t have to raise too much and inflation will come down to 2% in a few years.

This will be difficult because productivity is an economic variable that is hard to measure.

If wages spike, this would probably cause companies to continue raising prices, kicking off a wage-price spiral, Reis warned.

The Fed might overreact to the rise in wages, he said.

There is a scenario where rates go up “much more,” Reis said. But there is a range — it could be “much much more” or “much more” or “just more.”

Reis said that he was sympathetic to the idea that raising the unemployment rate to 5.5% was not a terrible outcome if it means a return to low inflation.

SPX, +2.28%

moved sharply higher Friday when the government reported relatively slow increase in wages in December. The yield on the 10-year Treasury note TMUBMUSD10Y, 3.562%

fell to 3.56%.

The numbers: The U.S. generated 223,000 new jobs in December to mark the smallest increase in two years, but the labor market still showed surprising vigor even as the economy faced rising headwinds.

SPX, -1.16%

rose in premarket trades and bond yields edged higher after the report.

Economists polled by The Wall Street Journal had forecast a smaller increase in new jobs of 200,000.

The resilient labor market is a double-edged sword for the Federal Reserve.

For one thing, a scarcity of workers has driven up wages and threatens to prolong a bout of high inflation. The Fed wants the labor market to cool off further to ease the upward pressure on prices.

Yet the strong labor market also offers the best hope for the Fed to avert a recession as it jacks up interest rates to the highest level in years. Higher rates reduce inflation by slowing the economy.

James Bullard, president of the St. Louis Federal Reserve, said on Thursday the odds of so-called soft landing have gone up in part because of the sturdy labor market. He was referring to a Goldilocks scenario in which the central bank vanquishes inflation without causing a recession.

Senior Fed officials still want to see the jobs market slacken some more, however. They are likely to keep raising rates — and keep them high — until demand for labor, goods and services ease up.

Big picture: The U.S. economy has shown more fragility, especially in segments like housing and manufacturing that are sensitive to high interest rates. Many economists predict a recession is likely this year due to the higher cost of borrowing.

The Fed, for its part, is trying to thread the needle: Bring down high inflation and keep the economy out of recession.

Whatever the outcome, one thing is virtually certain: The unemployment rate is expected to rise as U.S. growth wanes. Whether it’s enough to help the Fed achieve is far from clear.

Key details: Health care providers, hotels and restaurants accounted for most of the increase in employment last month. They added a combined 150,000-plus jobs.

Hiring was weaker in most other sectors, suggesting that the labor market is likely to soften further.

High-tech has been hit particularly hard and is experiencing a wave of layoffs.

Employment in so-called professional businesses, which includes some tech, fell by 6,000, largely reflecting fewer temps being hired. It was the only major category to post a decline.

The share of working-age people in the labor force — known as the participation rate — rose a tick to 62.3%.. A lack of people looking for work is a chief source of the labor shortage.

Hiring in November and October was little changed after government revisions. The economy added 256,000 jobs in November and 263,000 in October.

Market reaction: The Dow Jones Industrial Average DJIA and S&P 500 SPX were set to open higher in Friday trades.

Investors worry a strong labor market will push the Fed to take sterner measures to slow the economy. The slowdown in hiring and wage growth is likely to be seen in a positive light.

None of the 19 top Federal Reserve officials expect it will be appropriate to cut interest rates this year, according to the minutes of the central bank’s December policy meeting, which were released Wednesday.

Fed officials welcomed recent inflation data that showed reductions in the monthly pace of price increases but wanted to see a lot more evidence of progress to be convinced inflation was on a sustained downward path, the minutes indicated.

Investors who trade in the federal funds futures market expect the Fed to start reducing interest rates this summer.

Fed officials said that if markets start to ease financial conditions, especially if driven by a misperception of how the Fed was responding to the data, that “would complicate” the Fed effort to restore price stability.

Officials downshifted to a 50-basis-point rate increase at the Dec. 13-14 meeting, after four straight moves of 75 basis points. That puts their benchmark rate in a range between 4.25% to 4.5%. A number of Fed officials said it was important to stress that raising rates at a slower pace was not a sign of any “weakening” in the Fed’s resolve to bring inflation down to 2% or a judgement that inflation was already on a downward path.

Seventeen of 19 Fed officials said they expected rates to rise above 5% this year. Officials penciled in the high end of the interest-rate range at 5.25%, with seven officials penciling in even higher rates.

This is well above market-based measures of Fed policy-rate expectations.

Earlier on Wednesday. Minneapolis Fed President Neel Kashkari said he would like to see the Fed hike interest rates to 5.4% before pausing.

Investors see the high end of the Fed’s interest-rate range hitting 5.25% this summer and then retreating.

Fed officials said upside risks to inflation remained a “key factor” in shaping policy.

The market expects the Fed to downshift to a 25-basis-point hike at their next meeting, slated for Jan. 31- Feb.1.

Officials said they are trying to balance two risks — doing too little and adding fuel to inflation and raising rates too high and and lead to an “unnecessary reduction” in economic activity.

But before getting too far into 2023, it’s a good idea to take stock of how your finances may have changed during the last 12 months and make any needed adjustments.

Here are five areas of your finances to check on so you don’t get any unpleasant surprises this year.

5 Financial Surprises (the Bad Kind) to Avoid in 2023

Higher Interest Rates

The Federal Reserve raised interest rates seven times in 2022, and additional hikes are expected in 2023. That means carrying a credit card balance is about to become more costly. It also means you can expect a higher monthly payment if you buy a home or car in the new year.

Consider that the average 30-year mortgage rate on Dec. 20, 2022 was 6.47%, up from 3.25% at the end of 2021. On a home with a $350,000 mortgage, that translates to a monthly payment of $2,205 vs. $1,523 a year ago.

If you’ve got credit card debt (or any other debt with a variable interest rate), prioritize paying it off, as you can expect your debt to get more expensive. And if you’re buying a home or making another major purchase that requires financing, be sure to factor those higher rates into your budget. You probably can’t afford as much house as you could have a year or two ago, when interest rates were nearly zero.

Social Security Taxes

For retirees, first some good news: Social Security payments are getting their biggest cost of living increase since 1981. That raise is especially sweet because Medicare Part B premiums will drop slightly, meaning seniors can hang onto more of their Social Security checks.

The downside of fatter Social Security checks: Some recipients could end up with an unexpected tax bill. Social Security benefits are taxed at the following rates:

50% of your Social Security benefits are taxable if:

Half of your benefits + other income = $25,000 to $34,000 (singles filers) or $32,000 to $44,000 (married couples filing jointly).

85% of your Social Security benefits are taxable if:

Half of your benefits + other income = $34,000 or more (single filers) or $44,000 or more (married couples filing jointly).

If Social Security benefits are your only source of income, it’s unlikely that you’ll owe taxes. But if your higher benefit in 2023 will push your income above the thresholds listed above, start planning for your tax bill now.

Missed Student Loan Payments

If you’ve been taking advantage of student loan forbearance since March 2020 — when all payments and interest on federally held student loans were suspended — be prepared to start making payments again.

If you’re on the standard repayment plan and are unable to make the payments, apply for an income-driven repayment plan, which could substantially reduce your monthly payments when the forbearance period ends. If you’re already on an income-driven plan, update your income to modify your monthly payment.

Overdraft Fees

Overdraft fees are among the most criticized fees assessed by banks, since those who live paycheck to paycheck are the ones likely to accidentally overdraft.

The goods is that a number of institutions eliminated their overdraft fees, including Ally Bank, Alliant Credit Union and Capital One.

In 2022, Bank of America announced it’s slashing overdraft fees from $35 to $10 and intends to drop bounced check fees. Wells Fargo said that it will give customers 24 hours to make good on overdrafts, although it hasn’t budged on the $35 overdraft penalty.

What does that mean for you? If you’re banking at a place that’s socking you with fees, then maybe 2023 should be the year you find a new bank — here’s a rundown of those fee changes, plus a list of banks that don’t charge overdraft fees at all.

Widespread Uncertainty

A growing number of economists are now predicting a recession in 2023, with those polled for Bankrate’s Third-Quarter Economic Indicator pegging the odds of a recession in the next 12 to 18 months at 65%.

An emergency fund is the best way to safeguard yourself against a recession. Ideally, you’d have enough to pay for six months’ worth of necessities, but amassing this much cash can take years. Even if you’re able to stash away enough to live off of for a month or two, that will provide a valuable safety net.

Because the stock market is volatile, this is money you should keep in an FDIC-insured bank account, rather than investing it. The silver lining of those higher interest rates: Some high-yield savings accounts are now paying annual percentage yields (APYs) above 3%.

Robin Hartill is a certified financial planner and a senior writer at The Penny Hoarder.

In the first trading day of the new year, U.S. financial markets were bogged down by the almost universal view that a recession is approaching.

A stocks rally fizzled out within the first 30 minutes of opening gains. Gold, a traditional safe haven, touched its highest level in six months, rising alongside silver and platinum. And 10- to 30-year Treasury yields, nestled in what’s known as the long end of the bond market, fell as investors jumped into government bonds — driving those yields down respectively to around 3.8% and 3.9%.

At the heart of the market moves was the strong sense that an economic downturn is all but inevitable at this point, following months of central bank interest rate hikes around the world — with the International Monetary Fund‘s chief Kristalina Georgieva warning that the economies of the U.S., European Union and China are all slowing simultaneously. Scion Asset Management founder Michael Burry said he expects another “inflation spike” after recession rocks the U.S., and former New York Fed President William Dudley said a U.S. economic downturn “is pretty likely.”

“Recession is what everyone is betting on,” said Ben Emons, senior portfolio manager and head of fixed income/macro strategy at NewEdge Wealth in New York. “And, the thinking is, therefore inflation will decelerate faster than what people anticipate and the Federal Reserve could move quicker to a rate cut. But the whole narrative of a recession is something that’s bothering the stock market and other asset classes because it will mean shrinking margins and earnings.”

Indeed, a much-hoped for rally in stocks around this time of the year, known as the “Santa Claus rally,” is failing to materialize, with just one more trading session left on Wednesday before the end of that seasonal period. The in-house research arm of BlackRock Inc., the world’s largest asset manager, described recession as “foretold” on Tuesday and said it is “tactically underweight” developed-market stocks, which are still “not pricing the recession we see ahead.” That’s the case even though global stocks ended 2022 down by 18% and bonds fell 16%, said Jean Boivin, head of the BlackRock Investment Institute, and others.

Sources: BlackRock Investment Institute, Refinitiv, Bloomberg.

“We see stock rallies built on hopes for rapid rate cuts fizzling. Why? Central banks are unlikely to come to the rescue in recessions they themselves caused to bring inflation down to policy targets. Earnings expectations are also still not fully reflecting recession, in our view. But markets are now pricing in more of the damage we see – and as this continues, it would pave the way for us to turn more positive on risk assets,” Boivin and others at BlackRock Investment Institute wrote in a note Tuesday.

“Even with a recession coming, we think we are going to be living with inflation,” they said.

Interestingly, the financial market’s focus on a 2023 recession is being accompanied by the view that such a downturn will help cure inflation, allowing central banks to end, slow, or even reverse their monetary policy-tightening campaigns. That view was buttressed by Tuesday’s release of inflation data out of Germany, which showed that the annual rate from the consumer price index fell by more than expected in December to a four-month low. Back in the U.S., fed funds futures traders priced in a greater likelihood of a smaller-than-usual, 25-basis point rate hike by the Federal Reserve in February.

As of Tuesday afternoon, all three major U.S. stock indexes DJIASPX were down, led by a 1.3% drop in the Nasdaq Composite.

Meanwhile, a rally in Treasurys moderated relative to earlier in the day. The 10-year Treasury yield TMUBMUSD10Y, 3.785%,

a benchmark for borrowing costs, dropped back to levels last seen around Dec. 23-26, a period when conditions were “totally illiquid and no one was trading,” said Emons of NewEdge Wealth.

It was 2017, the year before they got married, when Ali and Josh Lupo took a serious look at their finances — and realized they owed more than $100,000 in student loans.

Courtesy of The FI Couple

Despite working long, hard hours in human services, the couple was still living paycheck-to-paycheck, unsure how they’d afford a wedding or pay off their staggering debt.

“So we started having that conversation of: ‘Is this what we want to do for the next 30 to 40 years, or do we want to start learning how to live differently?’ And that was where our mindset around money really started to evolve,” Josh tells Entrepreneur.

The Lupos began tracking their expenses and saw they spent most of their income on rent and car payments, followed by food and dining out. Their first plan of attack? Implementing a strict budget: No date nights, no Netflix subscription, etc.

But the extreme approach burned the couple out quickly, so they went back to the drawing board. They needed to find a creative way to reduce their largest expense: housing.

Self-education led them to a solution (Ali emphasizes how many online resources, podcasts and books on financial freedom exist). If the Lupos purchased a multi-family home with a low down payment, they could dramatically decrease their monthly payments by renting out the other unit.

So that’s exactly what they did.

In the years since then, the Lupos have continued their journey to financial independence. They manage numerous streams of active and passive income, including their work as personal-finance content creators running the educational platform “The FI Couple.”

If you’re ready to get your finances on track in 2023, read on for the Lupos’ step-by-step strategy.

Define what success looks like for you

The first step is the foundation for all the rest: Figure out your unique definition of success.

The couple suggests considering what your ideal day and life look like. In other words, be clear about how financial freedom will allow you to do more of the things that make you happy.

“Our life was ‘easier’ when our heads were in the sand, ignoring everything about our finances,” Ali says. “Our lives are more complicated and harder now because we’re more in tune with all of the responsibilities that come with this. But to have the power and autonomy over our time is worth all of it, so [you have to be] clear with your why.”

Build a community that can help you stay the course

The road to financial freedom can be a difficult one, but it’s even harder for those going it alone.

Finding a community geared towards financial wellness can make all the difference, according to the Lupos.

“Unfortunately, being financially savvy is not the norm,” Josh says, “and pursuing financial independence can get lonely because a lot of people aren’t necessarily living the same lifestyle. So whether it’s in person or online, having that community of like-minded people can be really inspiring.”

Know your numbers: income, expenses, assets and debts

Another critical move?Get thoroughly acquainted with the reality of your financial picture.

As of September 2022, consumer debt in the U.S. was at $16.5 trillion, according to Bankrate. But many Americans are unaware of how much they actually owe: A 2019 survey from U.S. News found that one in five Americans doesn’t know if they have credit card debt.

The Lupos stress the value of familiarizing yourself with all of your numbers.

“So literally outlining and understanding your income, expenses, assets and debts,” Ali explains, “and having a crystal clear understanding of your financial situation.”

Figure out how to lower expenses and increase your income

Next up, consider how you might save and earn more money — “the two biggest levers a person can pull,” Josh notes.

The couple acknowledges that increasing your income significantly can seem challenging at first, but the key is to get creative.

“We decided to focus on how we could radically lower our expenses to increase our savings,” Josh says, “and doing so helped us pay off all the debt and buy real estate.”

“If you’re able to increase your income and reduce your expenses, you’ll have more of a gap in between,” Ali adds, “and what you do with that gap is the key to becoming financially independent.”

Never underestimate your earning potential either.

“Coming from backgrounds in social work and human services that are historically lower-income opportunities, for a long time we identified ourselves as people [whose] value was a little bit lower and [thought] earning more just simply wasn’t in the cards,” Josh says. “In hindsight though, [the key is] getting around the right people and understanding different opportunity vehicles.”

Consider which strategy makes the most sense for your lifestyle

It’s not enough to brainstorm a solution and go all in — part of the secret is choosing an approach that aligns with your values and priorities.

As fundamental as real estate investment has been to the Lupos’ success, the couple recognizes that it’s not for everyone.

“The goal of financial independence is to have enough assets to pay for your overall cost of living,” Ali says. “So you have to [ask], What strategy makes sense for me? Do I want to invest in stocks? Do I want to invest in real estate? Do I want to be a business owner?“

“We talk to people all the time,” she continues. “They say, ‘I want to buy real estate.’ But then we talk to them, and I’m like, ‘It doesn’t really sound like you want real estate. Because real estate’s not that passive — and it’s a little more hands-on.’ You really have to think about which investing strategy makes sense for [your] life.”

Real estate isn’t always “passive”

Then again, neither are 40-50 hour weeks at a job

At least with real estate “hard” weeks are still only 2-3 hours of work

Maybe the most important thing to keep in mind, though? Don’t forget to enjoy the journey to financial freedom.

“When we first started out, it felt like a chore,” Ali says. “Through the process, we’ve learned that the journey to financial independence is more important than the destination and that it’s really important that whatever you do to get there is sustainable and you don’t sacrifice the quality of your life to achieve [your] goal. Because then once you get to the goal, what life do you have?”

This is an opinion editorial by Mickey Koss, a West Point graduate with a degree in economics. He spent four years in the infantry before transitioning to the Finance Corps.

“First they ignore you, then they laugh at you, then they fight you, then you win”

At the time of this writing, the U.S. Senate had just introduced the Digital Asset Anti-Money Laundering Act of 2022. The bill contains many threatening aspects, such as KYC laws for self-custody wallets and money-transmitter licensing requirements.

This bill also comes on the heels of the European Central Bank’s (ECB) recent revelation that Bitcoin is on an “artificially induced last gasp before the road to irrelevance.” About a week later, an official from the bank announced it was considering a Bitcoin and crypto ban in order to mitigate environmental damage.

The below is a thread by Level39 depicting testimony from the recent Senate Banking Committee hearing.

I think this is just the beginning of the “then they fight you stage” and it will only get worse in 2023. Stay vigilant this year. While a ban and much of the regulations would be comically impossible to actually enforce, they would serve as a significant speed bump to widespread adoption. I would keep an ear to the ground (and probably to Bitcoin Twitter) to stay abreast of situations that could be influenced by a sea of calls to your governmentally-elected representatives, just like what happened with the infrastructure bill in 2021.

The Debt Spiral… Spirals

Luckily, I think more and more people will begin to wake up from the matrix and realize just how bad the situation really is. The fact is, it’s getting pretty hard to obscure at this point.

The above chart is essentially my new favorite picture. When people ask me about Bitcoin lately, all I do is show them this graph and they pretty quickly understand the magnitude of money creation during the 2020 COVID-19 era. What they don’t quite understand, just yet, is that it is going to continue, and probably at increasing rates and intervals.

The U.S. federal government is already projected to run a $1 trillion deficit in 2023 (that’s 12 zeroes, folks). Even if the U.S. government shut down the entire military and eliminated the Department of Defense’s projected $800 billion budget, the budget would still be projected to be operating in the red for 2023. The real kicker in this is that the deficit is likely to be much higher, meaning that more debt will have to be issued, and that would be in a period of increasing interest rates due to Federal Reserve tightening.

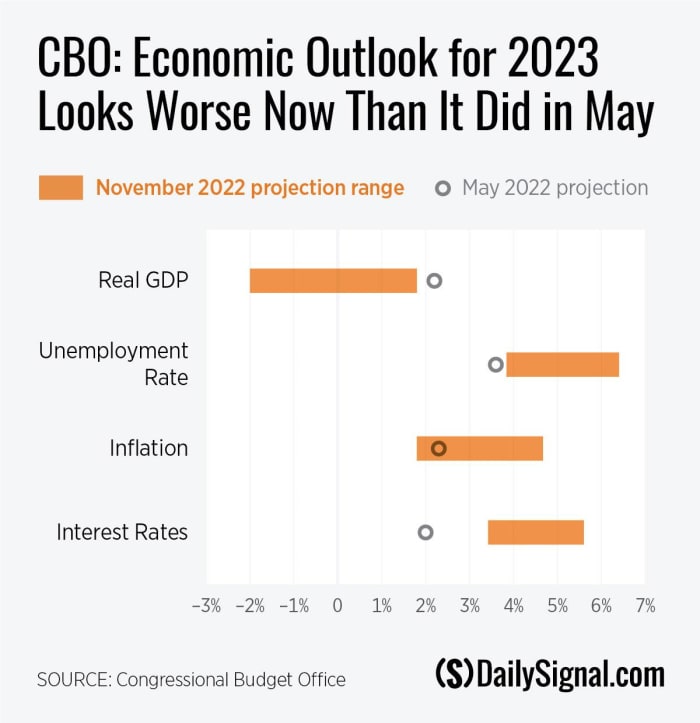

The Congressional Budget Office is projecting that negative growth in GDP is about as likely as lower-than-expected positive growth. Couple that with an expected increase in unemployment, and you get yourself a fiscal double whammy. First, unemployment and negative GDP growth imply less tax receipts to the federal government, meaning a potentially bigger deficit, i.e., more debt. You add in the fact that the debt is being issued at a significantly higher rate, and you’ve got yourself the ingredients for an accelerating debt spiral.

Even if everything goes completely to plan, a trillion-dollar deficit is certainly nothing to celebrate. I think the numbers speak for themselves. People I work with and am friends with are really starting to notice and get worried; people who have never previously given a lick of interest to economics before.

And when all of the proverbial stuff hits the spinning thing, you can bet that the Fed steps right in with more money printing. Adding a trillion or so dollars to the debt at 5% interest? I don’t think it’s gonna happen. I’m betting interest rates won’t be much higher for much longer. Quantitative easing three is dead. Long live quantitative easing infinity.

Coincidentally, as I write this article, I received the above article in an email from the Bitcoin Layer. Looks like they agree with me. Rate hikes can’t hike much more than they’ve already hiked. They’re basically off of the trail.

Bitcoin Reignites The Pioneer Spirit

Once upon a time, in a place called America, people used to take responsibility for their actions, traveling off to seek adventure and opportunity in the West. The Oklahoma Sooners’ namesake hails from the Oklahoma Land Rush of 1889, where nearly 50,000 Americans lined up on the edge of the “Unassigned Lands” to race to claim their stakes in the undeveloped wildlands that became Oklahoma.

Much like homesteading in the 19th century, Bitcoin is both a team sport and a race. It’s a race in the sense that if you do not take responsibility to claim your stake in cyberspace before someone else, you may have missed an opportunity of a lifetime. It’s a team sport in the sense that successfully adopting Bitcoin into your life will likely require a degree of help from others.

How many BTC Sessions videos did you watch before setting up your first hardware wallet? How long after that did you actually send any UTXOs to your self-custody address? How long did it take before you even knew what a UTXO is?

Bitcoin is the new frontier, the digitalization of the Unassigned Lands in the old American West. The journey is fraught with dangers and pitfalls, but the payoff is an opportunity that we will likely never see again during our lifetimes. Everyone gets bitcoin at the price that they deserve, yes, but that doesn’t mean you can’t help them accelerate the learning process.

Let’s make 2023 the year we drained the exchanges; auditing them for paper bitcoin through sheer blunt force trauma. I challenge you to try and embody the homesteading pioneer spirit to help make this happen; to help your friends and family understand this phenomenon and opportunity. To help them take self custody and preserve their wealth in a self-sovereign way. Help lead the horse to water, so to speak. You can’t save everybody, but you can at least try to help them see what’s coming, and stake their claim in the new Wild West in cyberspace.

This is a guest post by Mickey Koss. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

If there’s a silver lining to the current economic situation that features soaring inflation and falling stocks, it’s that savers can get more for their money.

Even after just a few months of rising interest rates, you can find online savings accounts yielding more than 3%. But that might not be good enough anymore.

“Rather than being grateful for yield, that’s going to change quickly into turning your nose up at yield,” says Matt McKay, a certified financial planner and partner at Briaud Financial Advisors in College Station, Texas.

The Federal Reserve continued to raise rates through the end of 2022, and yields on savings products are now high enough that they look like a safe haven compared with a stock market that’s in the red this year.

And that means certificates of deposits, or CDs, are back in the conversation — even if that comes with caveats.

Advisers still favor Treasury bills and notes and Series I savings bonds for getting the best combination of low risk and high yield, but some are looking more seriously at CDs now. And for the everyday investor doing it on their own, CDs offer an additional boost beyond a savings account without much effort.

“It’s good for anyone if they have cash sitting around, if you can pick up something — CDs, T-bills, whatever — it’s good to get something,” says McKay.

Remember CDs?

If you’re under 50, you might never have invested in a CD and have no memory of how investors used to build ladders of different maturities as a cornerstone of their portfolio.

“With younger clients, nobody ever talks about CDs — never, never, never,” says Dennis Nolte, a certified financial planner and financial consultant at Seacoast Investment Services in Orlando, Fla.

For some, however, CDs never went out of style. These promissory notes from banks, which have been around in the U.S. since the 1800s, come in maturities generally from three months to five years, in exchange for interest at maturity.

You’re locked into the time period or face surrender charges that vary, unless you choose a more flexible, lower-interest option. The laddering strategy consists of buying CDs at different maturities and then reinvesting as they each come due.

Over the past few years, CDs haven’t been worth it for most savers, who could get as much from a high-yield savings account without restrictions. The average five-year CD would have nabbed you nearly 12% in 1984, but now the average five-year rate is just 0.74%, according to Bankrate.com. Back in 1984, CDs were nearly 50% of deposits at FDIC-insured banks, with $1.24 trillion held in the first quarter of that year. In 2022, there’s nearly the same dollar amount, which amounts to just 6.3% of deposits.

With rates rising, you can find better-than-average deals, closing in on 4% at some banks or brokerages. Many have a $1,000 minimum purchase, but you can find fractional offers for as little as $100.

CDs versus Treasurys and I-bonds

Treasury bills and notes come in roughly the same maturities as CDs, and are yielding slightly more currently. They also have no state tax burden on gains.

You can buy directly at TreasuryDirect.gov, with a $100 minimum, but to sell, you have to transfer holdings to a brokerage. Or you can buy and sell through a brokerage, but your minimums may be $1,000.

For I-bonds, you can only buy directly at TreasuryDirect.gov, with a minimum of $25 and a maximum of $10,000 per person a year, with gifts allowed to others up to $10,000 per recipient. I-bonds are indexed for inflation, with rates that reset every six months, and today are yielding 6.89% through April 2023. The biggest caveat is that you are locked into one year, and then face a surrender penalty of three months of interest if you cash out before five years.

A strategy for today’s rising rates

If you are chasing yield and have money you don’t need for a year, then I-bonds are the place for the first $10,000.

“It makes sense to max out I-bonds before investing in CDs,” says Ken Tumin, founder of DepositAcccounts.com.

Just make sure you’re motivated enough to navigate a still-wonky website and keep track of the investment on your own, because it won’t align with any of your other accounts. McKay had a client who was eager to jump into I-bonds, and he was mad at first that McKay hadn’t recommended it. “But then he called to complain, saying this is terrible, it’s so difficult,” he says.

If you have funds beyond that for savings, consider Treasury bills or notes because the rates are higher, says Tumin. Then consider CDs. That’s what Nolte is doing with some clients, particularly older ones who have past experience with them.

“Why not get something guaranteed? It’s maybe not keeping pace with inflation, but you’re not losing principal,” says Nolte.

CD rates move more slowly than other products, so even after the next rate hike, this strategy would still apply. But already Tumin sees investors ready to lock into long-term CDs, anticipating a recession and a drop in interest rates. If rates subsequently fall, and CDs lag, they would eventually end up with a price advantage over Treasury investments. Then people like McKay will be advising clients to buy in earnest.

“That’s when CDs become most attractive — as soon as rates peak or there are cuts [in rates],” says McKay.

Got a question about the mechanics of investing, how it fits into your overall financial plan and what strategies can help you make the most out of your money? You can write me at beth.pinsker@marketwatch.com.

We know how incredibly easy it is to rack up credit card debt.

More than 50% of Americans carry a credit card balance, with 30% carrying more than $1,000 of debt or more month to month, 15% carrying $5,000 or more and 6% carrying $10,000 or more, according to a recent GOBankingRates survey. The ongoing pandemic and rising inflation have made it even harder for Americans to avoid going into credit card debt, with 45% increasing their overall debt since the start of the pandemic.

But here’s the tricky thing about credit cards: They only benefit you when you’re building credit and receiving perks — but not when you’re paying interest. If you’re paying a lot of interest on your balances, credit card companies are making money off of you.

Your cards are using you, not the other way around.

With average APRs (annual percentage rates) on new credit cards north of 16%, according to LendingTree, paying them off is a smart move. You can do it. And it’ll be worth it.

Tina Russell/The Penny Hoarder

5 Ways to Eliminate Credit Card Debt

Before you start your journey to becoming debt free, try to stop using your credit cards altogether until you can use them without putting yourself in financial risk. Though the specifics will vary based on your situation, we only recommend using credit cards if:

You don’t have any debt outside of a mortgage or student loans. (Mortgages and student loan debt are almost impossible to avoid nowadays.)

You have an emergency fund with three to six months of expenses saved. This is how much money you’d need to survive during that time period, assuming you have no income reaching your bank account.

You can pay off your credit card debt in full every month — not just minimum payments.

However you do it, make paying off your credit cards — and learning to use them responsibly — a high priority.

First, determine how much credit card debt you have. You can do this using a tool like Credit Sesame, a free credit monitoring service.

Then choose your weapons! We’ll go over five different methods, from debt consolidation loans to repayment strategies to settlement, for paying off your credit card debt.

1. The Debt Avalanche Method

Instead of looking at your debt in its entirety, we recommend approaching it bit by bit. By breaking your debt down into manageable chunks, you’ll experience quicker wins and stay motivated.

Using the debt avalanche method, you’ll order your credit card debts from the highest interest rate to the lowest. You’ll make the minimum payment on each of your credit card accounts, and any extra income you have will go toward the highest-interest card.

Eventually, that card will be paid off, and you won’t have to worry about that monthly payment anymore. Then, you’ll attack the debt with the next-highest interest rate, and so on, until all your cards are paid off.

2. The Debt Snowball Method

With the debt snowball method, you’ll order your debts from the lowest balance to highest, regardless of the interest rates on the cards. You’ll make the minimum payment on each of your credit card balances, and any extra income will go to the credit card with the smallest balance.

Starting with the smallest balance allows you to experience wins faster than you would with the avalanche. This method is ideal for people who are motivated by quick wins, but it has a downside: Those who choose it could end up paying more interest over the long term.

Here’s an example of how each method would work if you’re paying off four credit cards of varying balances and interest rates.

$654 with 0% interest

$5,054 with 15% interest

$2,541 with 23% interest

$945 with 17% interest

If you followed the avalanche method, you’d pay off card No. 3 first, followed by No. 4, No. 2 and No. 1. If you followed the snowball method, you’d pay off card No. 1 first, followed by No. 4, No. 3 and No. 2.

Choosing the right method comes down to deciding whether you’d rather get quick results or save money on interest. We encourage you to check a debt calculator yourself, so you can calculate what each method would cost you.

3. The Balance Transfer

If you have good to excellent credit (typically a FICO score of 670 or above) and can feasibly pay off your debt within a year, a balance-transfer credit card is a great option. Balance-transfer credit cards can save you money on interest charges by letting you transfer the balance of a card with a high interest rate to a card with 0% interest.

Most of these cards offer 0% interest for 12 to 18 months with no annual fee. They generally have a 3% to 5% balance-transfer fee, but you can easily find balance transfer cards with no fee. Higher credit scores help borrowers to qualify for a credit card with better terms.

Think a balance transfer card is the right move for your finances? We’ve put together a list of the best balance transfer cards currently available.

4. Take out a Loan

You might look at getting a loan to consolidate and refinance your debts.

If you get a loan with a lower interest rate and pay off your credit cards, that lower rate could potentially save you thousands of dollars in interest.

This is a realistic way to pay off credit card debt if you currently have little or no money to put toward it.

Let’s look at two options for debt consolidation here: A personal loan or a home equity loan.

Personal Loan

Online marketplaces will allow you to prequalify for a personal loan without doing a hard inquiry of your credit, so if you want to shop around, head there first. Shopping for personal loans online does not affect credit scores.

A personal debt consolidation loan is a good idea if you have decent credit and can manage the repayment plan that accompanies the loan. Whereas credit cards offer revolving credit, meaning you can continue to borrow and just make minimum payments, a debt consolidation loan will have a predetermined repayment plan with a set schedule of payments.

A debt consolidation loan is similar to a balance transfer credit card, as you are consolidating all of your debt into one place. The personal loan route is more attractive, however, because rates are typically lower for debt consolidation loans.

A good resource for finding personal loans here is Fiona, a search engine for financial services, which can help match you with the right personal loan to meet your needs. It searches the top online lenders to match you with a personalized loan offer in less than a minute.

Home Equity Loan

If you own a home with equity, you have three ways to borrow money against the value of your home: a home equity loan, home equity line of credit or a cash-out refinance.

With a home equity loan, the lender gives you your money all at once, and you repay it at a fixed interest rate over a set period of time.

With a home equity line of credit, you’re given a limit to borrow. Within that limit, you can take as little or as much as you need whenever you want.

With a cash-out refinance, you refinance your first mortgage with a mortgage that’s slightly more money than your current one, and pocket the difference.

For homeowners, these options will most likely offer the lowest interest rates. But they’re also the riskiest, because your home is the collateral — something you own that your lender can take if you don’t pay off the loan.

5. Debt Settlement

The world of debt collections and creditors can be confusing, intimidating and sometimes even illegal. There’s a common misconception, for example, that someone can take your house or you can go to jail for not making your credit card payments. But credit card debt is unsecured debt, meaning no one can put you in jail or take your house if you don’t pay it.

If you’re being harassed by creditors or have circumstances that make your debt repayment confusing, don’t give up before finding out your options for assistance.

Debt Management Program

With a debt management program, a credit counseling company will handle your consolidation in hopes of getting you a better interest rate and lower fees. You’ll be assigned a counselor, who will set up a repayment and education plan for you. This program is specifically for unsecured debt, like credit cards and medical bills.

A debt management program pays your creditors for you to ensure you stay current on your debt payments. Your credit score may even improve during the program. But if you miss a monthly payment, you can be dropped, and you’ll lose all the benefits you gained.

Debt management plans usually don’t reduce your debt, but they may reduce your interest rates by as much as half or extend your payment timeline to make paying your debt more manageable.

Credit Card Debt Settlement

If you’re in more than just a temporary season of financial instability, and you can’t see yourself affording the amount of credit card debt you owe, debt settlement is an option, though we regard it as a last resort.

Debt settlement reduces the amount of debt you owe, but it will significantly lower your credit score and negatively impact your credit report.

The process isn’t as simple as debt consolidation. You have to convince every creditor that if they don’t settle with you, they probably won’t get anything at all. So, of course, during that time you won’t be making any payments — while interest and late fees accrue.

You can do this on your own, but most people seek the help of a debt settlement company.

Like a debt management program, a debt settlement firm will negotiate debts on your behalf, and the company will make lump-sum payments to creditors while you make monthly payments to the debt settlement company.

Pro Tip

Be careful when seeking help with debt settlement. While some companies are legitimately there to assist you, others take your money and do very little to help your situation.

While you’re paying the debt settlement company, you’ll still be delinquent with any creditors the company hasn’t yet negotiated with, meaning you’ll still get calls from those creditors.

And there’s no guarantee the company will be successful. If it isn’t successful in negotiating, you’ll still be responsible for the full debt amount, plus any extra interest that accrued.

If the company is successful, you’ll have to pay the settlement amount in full. Then in April, you’ll owe taxes on the amount forgiven.

The settlement company will also charge you up to 25% in fees on top of the settlement.

How one Penny Hoarder paid off $12,000 in debt in just 12 weeks. She shares her top tips so you can get out of debt too.

Bankruptcy

Bankruptcy is another last resort. The two major types for individuals are Chapter 7 and Chapter 13.

Chapter 7 bankruptcy allows you to completely discharge all your debts except student loans in four to six months by liquidating your assets. A trustee gathers and sells all of your nonexempt assets to pay off your debt. Those assets can include property that’s not your primary residence, a vehicle with equity, investments or valuable collections.

Those who earn a high income or have significant assets typically choose Chapter 13, which allows you to keep certain assets while still repaying some of the debts. It’s a long, arduous process that doesn’t guarantee to resolve your debt. It can be reversed if your income increases, and it wrecks your credit.

Both bankruptcy options have negative long-term ramifications on your credit. But if you’re out of options, bankruptcy gives you a chance to get your debt under control and get creditors and debt collectors off your back.

Getty Images

How to Pay off Credit Card Debt Fast

If you want to become debt free quickly, here are some ways to pay off credit cards fast:

Up Your Monthly Payments

Make two payments per month instead of one. Most credit card companies use an average daily balance to compute interest charges. Instead of making monthly payments of $400 toward a balance, make two payments of $200, one at the middle of the month and one at the end. You’ll lower the average daily balance so you’ll pay less interest. Some credit card users even advocate for paying off credit card balances every week; a weekly reminder in your calendar is all it takes.

Try to Get a Lower Rate

Ask your credit card companies for lower interest rates. It’s worth trying at least once for each credit card you have. Research competitor cards similar to yours for which you qualify and that offer better rates — then share those with your credit card company to see if they’ll match it.

Knocking four interest percentage points off a $10,000 balance, for example, can save you hundreds of dollars in interest annually. Add those savings to your debt repayment budget!

Get the Debt Reduced

Sometimes you can convince a credit card company to forgive your debt — or at least part of it. After all, these companies want to retain you as a customer, so they may be more open to negotiation than you might think. If you’re in serious financial trouble, explain the situation to the card issuer. Offer to pay a portion of the balance owed as payment in full.

For most of us, though, there’s no quick answer.

How Much Will Paying Off Credit Cards Raise Your Score?

You might be asking yourself, “How much will my credit score go up if I pay off my credit cards?” It turns out that credit card usage has a huge impact on credit scores.

If you spend too much of your overall limit or miss payments, you’ll hurt your score. If you keep your balances low and regularly make your minimum monthly payment on time, your score will increase over time.

Just because you have available credit doesn’t mean you should max out your credit cards. Your credit utilization, which tells the credit bureaus how much of your available credit you’re using, shows whether you are sensible with your borrowing.

Keeping your credit utilization at or under 30% is ideal. That means on a credit card with a $10,000 limit, you wouldn’t want your balance to exceed $3,000.

Credit utilization accounts for a whopping 30% of your score. Other factors affecting your score include payment history (35%), credit history length (15%), credit mix (10%) and new credit (10%).

Looking for ways to increase your score outside of paying down your credit card debt? Penny Hoarder senior editor Robin Hartill shares 10 moves you can make in 2023 to improve your credit.

Credit card issuers make it so easy to get in the habit of overspending. The introductory APR offers, new credit card sign-up bonuses and cash back offers are designed to get us using cards more frequently and thinking less about what items cost.

So if you ever want to be debt-free, you need to change the way you use credit cards.

Former Freelance Editor Janet Keeler, freelancer Tim Moore, former Staff Writer Jen Smith and Senior Writer Mike Brassfield contributed to this post.

My brother owes me over $6,000, and he is taking forever to pay it off. He owes money to banks as well. Would it be better to ruin our relationship and take him to court or just forgive the debt?

It’s a lot of money, and he has owed it to me for quite a number of years now. Do you have any other suggestions of how to recoup that money?

-Irritated

Dear Irritated,

Let’s put aside the relationship for a second. Do you think your brother has $6,000 sitting around somewhere and is refusing to pay you? Or is it likelier that he’s flat broke and you’re just one of the many people he owes?

Many people believe the myth that successfully suing someone means you’ll actually get money. That’s simply not true. Even if you have solid proof your brother owes you (which often isn’t the case with family and friends) and you win a court judgment, that judgment is worthless when the person you’ve sued is broke.

Got a Burning Money Question?

Get practical advice for your money challenges from Robin Hartill, a Certified Financial Planner and the voice of Dear Penny.

DISCLAIMER: Select questions will appear in The Penny Hoarder’s “Dear Penny” column. We are unable to answer every letter. We reserve the right to edit and publish your questions. But don’t worry — your identity will remain anonymous. Dear Penny columns are for general informational purposes only, but we promise to provide sound advice based on our own research and insights.

Robin Harthill

Thank You for your question!

Your willingness to share your story might help others facing similar challenges.

While we can’t publish every question we receive, we appreciate you sharing your question with us.

The Penny Hoarder’s Robin Hartill is a Certified Financial Planner and the voice of Dear Penny.

You could ask for a court order to garnish his bank account, but that won’t do you any good if there’s no money in there. Plus, if he owes banks money for things like negative balances and overdraft fees, he might not even have a bank account.

Maybe you could get a wage garnishment order if your brother is employed. But federal law generally limits that amount to 25% of someone’s disposable income, so if your brother doesn’t make a lot, this may not yield much. Also keep in mind that some types of income, like Social Security, are off-limits from creditor claims.

In many states, $6,000 is within the threshold for small claims court, so you probably wouldn’t have to pay much in court costs. But also consider the value of your time. You could end up wasting many hours and still walk away with nothing — while still destroying the relationship with your brother in the process.

Think about how likely it is that your brother can afford to repay you. Does he spend money on vacations, hobbies and going out to eat? If so, go ahead and sue your brother. Give him a final warning or two first. Maybe try sending him a demand letter via certified mail stating your intent to sue if he doesn’t pay up. In this scenario, I wouldn’t be so worried about creating a rift.

Someone who deliberately stiffs you out of $6,000 clearly doesn’t value the relationship.

But if you think your brother is struggling, have a talk with him and ask him to be realistic. Does he ever see himself getting caught up enough to repay you? I’m sure you’ve probably had this conversation far too many times to count by now. But maybe if you offer some flexible solutions, you can recoup at least some of that money.

Could he afford payments of $50 or $100 a month? If he has a bank account and he agrees to this, ask him to set up automatic transfers.

You may also borrow a move from professional debt collectors and offer to forgive some of the debt he owes in exchange for a lump sum. Since he owes you $6,000, you could tell him that if he can pay $3,000, you’ll forgive the other half. When you’re talking about a debt that’s been lingering for several years, collecting anything is better than nothing.

I’d also let him know that suing him is something you’ve considered. Tell him that’s a route you really don’t want to go because you care about the relationship — but also that when you lent him the $6,000, you really believed he’d repay you.

The important thing here is to be realistic. If you don’t believe your brother will ever have the funds to repay you, I think forgiving this debt is the best option. This is as much for you as for your brother.

When you’re holding onto the hope that something will happen, you wind up frustrated every time it doesn’t. Sometimes the best thing you can do is move on. Plus, accepting the fact that you’re never getting that $6,000 back helps you plan your own finances better.

Of course, forgiving isn’t forgetting. Don’t ever lend your brother money again. And if you ever lend money to someone in the future, do it with the assumption that you won’t be repaid.

Robin Hartill is a certified financial planner and a senior writer at The Penny Hoarder. Send your tricky money questions to [email protected].

The news is abuzz with rumors of the next recession coming in 2023 or 2024. But for most Americans, all of that triggers a sudden panic and a desperate need to look at one’s bank account.

What is a recession, what does it mean, and how can you prepare yourself and your family’s finances for one? This article will answer each of these questions and more. By the end, you’ll know what to expect and how to prepare for a recession.

What is a recession?

According to economists working for the National Bureau of Economic Research, a recession is a prolonged period of economic downturn or declining economic activity.

It affects a nation’s or the world’s entire economy and lasts for a few months or more. In some ways, the best way to understand the recession is to compare it to “regular” or positive economic activity and GDP.

GDP (gross domestic product) is essentially the combined value of the goods and services made by an economy, like the American economy. The country’s GDP grows a bit each day/week/month in a standard economy.

When a recession kicks in, there is no economic expansion. Instead, the GDP is negative — the value of goods and services in the economy decreases — for more than two quarters or approximately six months. People stop spending as much money when this happens because the dollar’s value decreases.

This decrease in consumer demand triggers a decline in industrial production, exacerbating the spiral effect and making a recession last longer. A significant decline in the business cycle, characterized by many consecutive quarters of lower consumer spending, may lead to job losses or a high unemployment rate.

Several past recessions have stalled economic growth and led to the depletion of the Federal Reserve or the “Fed.”

These include the recession leading into World War II, the Great Recession financial crisis, which occurred in 2008 from speculation on real estate, and the most recent recession brought on by the Covid-19 pandemic and the necessary cutback/slowdown on retail sales in the U.S. economy.

Signs of a recession

Aside from this recession indicator, some typical economic indicators also have other signs and symptoms to pay attention to.

These signs include:

More layoffs than average, a tighter labor market.

A general, widespread decline in stock market stock prices.

As for GDP? According to some sources, the American GDP was -1.6% in the first quarter of 2022 and -0.9% in the second quarter of 2022. Technically, this means there is currently a recession, regardless of what people say.

Note that a recession differs from a depression, which is much more severe. In a depression, the economy tanks significantly, and many more people may lose their jobs and money.

In contrast, a recession is usually relatively short-lived. Some people may not feel a recession’s impact, depending on how much money they have saved up and their financial situation before the recession occurs.

In any case, a recession is never good news, which could signify that you must prepare accordingly.

How to prepare for a recession

Fortunately, there are multiple ways in which you can prepare for a recession. Good recession prep can keep your finances secure until the recession recedes, allowing you to maintain your investments, keep your savings account intact and provide your family with peace of mind.

Knock out as much debt as possible (and avoid new debt)

Your priority should be to get rid of as much debt in your name as possible. You should already be trying to clear debt aggressively. The longer you leave it hanging around, the worse your credit will be and the more interest fees you’ll pay over time — it’s lost funds.

As you put more of your money toward knocking out your debt, prioritize high-interest debt, such as credit cards and loans with high-interest rates. When you get rid of as much debt as possible, you set yourself up for financial success during the potentially turbulent economic times ahead.

Avoid taking out any unnecessary loans or opening up new credit accounts during this timeframe. If you avoid further debt, you’ll have more money to spend on savings or necessities, which may be necessary soon.

Speaking of saving, you should continue to save aggressively or even save more money than you were previously.

You might not get an unexpected promotion or pay raise during the recession. Even worse, your job could be at risk if you recently joined a company or are at the beginning of your professional career.

In these cases and others, your income streams could dry up unexpectedly. If you save aggressively before that happens, you’ll be well-positioned to get back on your feet and weather this economic storm until clear skies return.

Try to save as aggressively as possible and put that money into a secure savings account. That way, you’ll earn interest on those savings and avoid accidentally spending the money.

Diversify investments

Plunging numbers and red lines on charts are not reasons to withdraw all of your investments or blow up your portfolio if you’re invested in the stock market. You should keep your money in the market; after all, the stock market will eventually rebound just like it always does.

Instead of panicking, diversify your investments by distributing your money into different stocks, funds, and other securities and assets. When you diversify your portfolio further, you protect it from economic damage, even from recessions.

Plus, if you diversify your investments instead of withdrawing from the market, you’ll prevent yourself from losing money in the short term.

Every time a recession occurs, some Americans invested in the market sell all of their securities, which only lowers prices for those securities. Then they regret this panicked decision as the market inevitably rebounds, with many stocks achieving higher prices than they reached previously.

Bottom line: keep your investments in the market and keep your eye on the prize, particularly for long-term gains. A recession will eventually pass. Your current positions may be unattainable the next time you have money to invest in the market.