Investors feeling giddy about last week’s sharp rally for stocks might want to give a listen to Tom Waits’ song, “Whistlin’ Past the Graveyard” from 1978, to sober up for the dangers that still lurk ahead.

The surge in stocks catapulted the S&P 500 index SPX, +0.92%

almost back to the 4,000 mark on Friday, also lifting it to the biggest weekly gain in roughly five months, according to Dow Jones Market Data.

“We are not convinced this is the beginning of a new bull market,” said Sam Stovall, chief investment strategist at CRFA Research. “We believe that we are headed for recession. That has not been factored into earnings estimates and, therefore, share prices.”

Stovall also said the stock market has yet to see the “traditional shakeout of confidence capitulation that we typically see that marks the end of the bear markets.”

Yet, information technology stocks in the S&P 500 jumped 10% for the week, while financials, which stand to benefit from higher interest rates, rose 5.7%, according to FactSet.

That could reflect optimism about the odds of a slower pace of Federal Reserve rate hikes in the months ahead, after sharp rate rises helped to undermine valuations and pull tech stocks dramatically lower in the past year. However, Loretta Mester, president of the Cleveland Fed, and other Fed officials since the October inflation reading on Thursday have reiterated the need to keep rates high, until 7.7% annual rate finds a clearer path to the central bank’s 2% target.

The stock-market rally also might suggest that investors view continued mayhem in the crypto sector as contained, despite bitcoin BTCUSD, +0.42%

trading near its lowest level in two years and the shocking collapse in recent days of FTX, once the world’s third-largest cryptocurrency exchange.

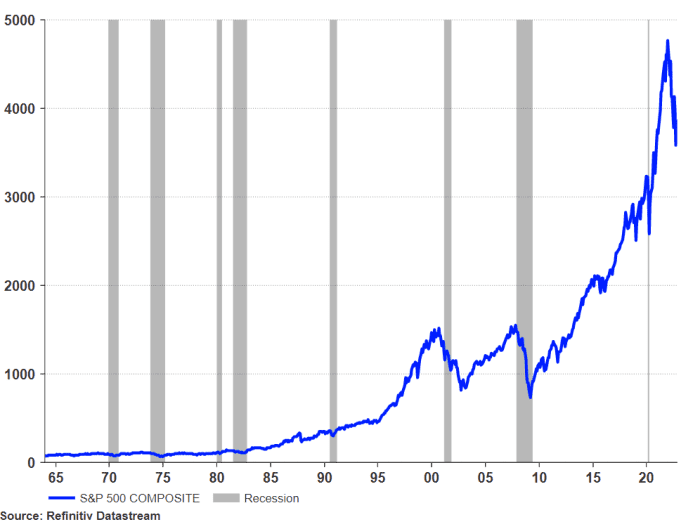

Blows to the American economy rarely have been good for stocks. A look at seven past recessions, starting in 1969, shows declines for the S&P 500 as more typical than gains, with its most violent drop occurring in the 2007-2009 recession.

The more than 37% drop of the S&P 500 from 2007 to 2009 was the worst of its kind in a recession since the late 1960s.

Refinitiv data, London Stock Exchange Group

While a looming U.S. recession isn’t a foregone conclusion, CEOs of America’s biggest banks have been warning about the risks for months. JP Morgan Chase’s Jamie Dimon said in October that a “tough recession” could drag the S&P 500 down another 20%, even though he also said consumers were doing fine, for now.

Still, the steady stream of warnings about the recession odds have left many Americans confused and wondering if one can even happen without an increase in job losses.

Big moves lately in stocks also have been hard to decode, given the economy was shocked back to life in the pandemic by trillions of dollars in fiscal stimulus and easy-money policies from the Fed that are now being reversed.

“What I think goes unnoticed, certainly by the average person, is that these moves are not normal,” said Thomas Martin, senior portfolio manager at Globalt Investments, about stock swings this week.

“It’s all about who is positioned how — and for what — and how much leverage they’re employing,” Martin told MarketWatch. “You get these outsized moves when people are offside.”

Here’s a view of the sharp trajectory upward of the S&P 500 since 2010, but also its dramatic drop this year.

Sharp rise of S&P 500 since 2010, but recent fall

Refinitiv Datastream

While Martin isn’t ruling out the potential for a seasonal “Santa Claus” rally heading into year-end, he worries about a potential leg lower for stocks next year, particularly with the Fed likely to keep interest rates high.

“Certainly what’s being priced in now is either no recession or a very, very mild recession,” he said .

However, Kristina Hooper, Invesco’s chief global market strategist, said the overarching story might be one of stocks sniffing out the first steps in a path to economic recovery, and the Fed potentially stopping its rate hikes at a lower “terminal” rate than expected.

The Fed increased its benchmark interest rate to a 3.75% to 4% range in November, the highest in 15 years, but also has signaled it could top out near 4.5% to 4.75%.

“If often happens that you can see stocks do well, in a less-than-good economic environment,” she said.

The S&P 500 rose 4.2% for the week, while the Dow Jones Industrial Average DJIA, +0.10%

gained 5.9%, posting its best weekly gain since late June, according to Dow Jones Market Data. The Nasdaq Composite Index shot up 8.1% for the week, its best weekly stretch in seven months.

In U.S. economic data, investors will get an update on household debt on Tuesday, retail sales and homebuilder data on Wednesday, followed by jobless claims and housing starts data Thursday. Friday brings existing home sales.

That means a full day of trading for stocks, which appear poised to book a robust week of gains, despite continued fears of a potential U.S. economic recession as the Federal Reserve works to tame stubbornly high costs of living.

While Friday marks the start of a three-day weekend for the bond market, Treasury yields already have climbed dramatically this year with the Fed’s sharp rate hikes. The central bank aims to temper demand for goods and services by making borrowing costs more restrictive.

Consumers may feel certain effects of inflation in their everyday lives, like when they go to the grocery store. But it can also impact our savings and investments. Here’s what to know.

The benchmark 10-year Treasury rate TMUBMUSD10Y, 3.819%

fell to about 3.8% on Thursday, but was up from a 1.3% low last December. Bond yields move in the opposite direction of prices.

The fresh rally on Wall Street followed the consumer-price index reading for October showing a 7.7% annual rate, down from a 9.1% high in June. The Dow remains down more than 8% from its January peak, the S&P 500 is 17.5% lower and the Nasdaq is 31% below its last record close, according to Dow Jones Market Data.

If the debt avalanche and snowball methods leave you feeling a bit cold when you think of all the interest you’ll end up paying, consider the debt lasso method.

Developed by David Auten and John Schneider, the Debt Lasso method involves corralling your high-interest debt into a low-interest one so you can pay down the principal balance more quickly — and for less money.

Want to learn more? Auten and Schneider told us all about the debt lasso, including who it can help the most — and who shouldn’t use it.

What Is the Debt Lasso Method?

If you’ve read about other debt payoff methods, you might be wondering if the lasso method is just a balance transfer. Auten and Schneider get that question a lot.

“The reality is that a central piece of the process is doing some sort of consolidation — whether that’s a balance transfer to a zero-interest credit card or a low-interest loan,” Auten said. “But a lot of people forget those first two pieces and the last two pieces.”

We’ll look at all the pieces, but let’s first decide if the debt lasso method can help you.

Who Should Use the Debt Lasso?

To determine if the debt lasso method is right for you, start by adding up how much you owe in credit card debt. Then compare that total debt to your annual income. If your debt is less than half of your income, the debt lasso method could work for you.

So if you have $15,000 in credit card debt and your gross income (before taxes and other deductions are taken out) is $30,000, you’re a good candidate for the debt lasso. But if you have $65,000 in credit card debt with the same salary, you may want to seek other assistance to help you pay off your credit card debt.

Pro Tip

Although it may be tempting to pay every dime toward your debt, don’t drain your emergency fund when practicing the debt lasso method.

You also might not benefit from taking up the lasso if you can realistically pay off your credit card debt in six months, since the associated fees (typically 3% to 5% of the amount being transferred) could cost you more than you’d save by taking advantage of a lower interest rate.

But if you fall somewhere in between, the lasso could help you pay off debt in a shorter amount of time and with less interest.

How the Debt Lasso Method Works

Developed by David Auten, left, and John Schneider, the married couple known as the Debt Free Guys, the debt lasso method involves corralling your high-interest debt into a low-interest one so you can pay down the principal balance more quickly. Photo courtesy of Studio Lemus

Ready to ride off into the debt-free sunset? Whoa there, pard’ner. Remember: You have to follow each step.

1. Commit

You cannot successfully use the debt lasso method unless you’re willing to commit.

Auten and Schneider should know: They started their own debt lasso journey with $51,000 in credit card debt. After years of poor financial choices, the couple was sitting on the floor of their basement apartment when they realized that their debt would never allow them to buy a house or enjoy life the way their friends were.

“That was our particular rock-bottom moment, realizing that here we were in this financial and literal hole,” Schneider said.

So they made a two-part commitment — which you’ll also need to do if you want to use the debt lasso method:

Stop using your credit cards. No exceptions.

Decide on an amount greater than your total minimum monthly payments that you can reliably put toward your debt every month.

Committing to the process is essential, Auten and Schneider said, as it will help you later when you may be tempted to stray off course.

2. Trim

Start with the easy wins by paying off any credit cards that have low enough balances to knock out in less than six months.

The early victory not only offers a psychological benefit but also helps your credit score.

Maintaining those credit lines will decrease your credit utilization, which accounts for approximately 30% of your credit score. And the higher your credit score, the better position you’ll be in when you’re ready to lasso.

3. Lasso

Time to saddle up.

If you have a good or excellent credit score, finding a zero-interest — aka 0% intro APR — offer where you can transfer your highest interest credit card debt should be your goal.

But if you have a less-than-stellar credit score, those offers may be tough to come by. Don’t give up.

You can still benefit from the lasso method by negotiating a lower interest rate with your current credit card company or transferring the balance to a card with a substantially lower interest rate than what you’re currently paying.

“To get you from 20% to 25% down to a 9% to 15% — that’s a great first step,” Schneider said.

And don’t limit yourself to credit card offers. Using a personal loan to pay off multiple cards has the same effect.

Compared to the average rate on credit cards, which was 18.43% as of August 2022, personal loans offered a better deal at 10.16%, according to the Federal Reserve.

Whichever offer you take, transfer or pay off as many balances as you can using your lower interest rate.

If you still have additional higher interest balances, prioritize paying off the credit card with the highest interest rate first.

Each time you pay off one credit card, put your money toward paying off the next highest balance.

Remember that you’ve committed to not using your credit cards (see Step #1). So hold onto the ones you’ve paid off. Why?

By not canceling the credit card, you’ll have more available credit, thus helping improve your credit score. And a higher credit score will help you get approved for another zero-interest credit card.

4. Automate

Automating your minimum monthly payments for all but your lassoed credit card will allow you to focus on paying off one debt at a time. But automating your payments can do even more to help.

Remember how we talked about the importance of committing because of later temptations? Here’s where that comes into play.

You may have multiple credit cards, but we’ll keep the example simple with one card: When you began your debt lasso journey, your minimum monthly payment was $80, so you committed to paying $200 on your credit card — $120 extra each month.

After you’ve paid down a portion of your balance, your credit card company tells you that your new minimum payment is only $60. Yay! But that doesn’t mean you now have $20 to spend — you should continue paying $200 each month, sending even more money toward your principal balance.

By automating your payments, you’ll be less tempted to reduce the amount when your minimum payment goes down — sort of an out-of-sight-out-of-mind mentality.

Putting all of the extra money toward your card with the highest interest rate will help you pay the least amount of interest over time. And that’s where the last step becomes crucial.

5. Monitor

Getty Images

This is no time to put your debt payment strategy out to pasture. Monitoring your accounts is an important last step, as those credit card rates can run wild if left unattended.

Before you reach the end of a zero-interest period, start looking for other offers that allow you to transfer your balance so you can avoid getting socked with the new higher interest rate on your old card.

Although opening new accounts could temporarily hurt your credit score, Auten and Schneider emphasized that the long-term benefits of paying off debt faster can help counteract that effect.

Who Should NOT Use the Debt Lasso Method — For Now

A word of warning: If you’re in an industry where you could be furloughed or laid off suddenly, you should probably hold your horses — and your cash.

“If you do get an offer and then you end up not being able to make your payments, then you could get stuck with an interest rate that’s 25 to 30%,” Auten said.

Credit card agreements often include a clause in the fine print that allows them to raise your interest rates if you miss a payment during the zero-interest offer period. Some will even sneak in the right to recoup any money you saved previously during the promotional period at the new interest rate.

The takeaway lesson: Read the fine print.

Saving your cash for now will let you build an emergency fund in case you do lose income. And if it turns out that you end up with an extra nest egg, consider it a bonus payment as you return to the debt lasso method.

Yeehaw!

Tiffany Wendeln Connors is the deputy editor at The Penny Hoarder who is fully committed to corny puns. Read her bio and other work here, then catch her on Twitter @TiffanyWendeln.

Hui Ka Yan, a member of the CPPCC National Committee and chairman of Evergrande Group, attends a press conference at the fifth session of the 12th CPPCC National Committee on March 9, 2017 in Beijing, China. (Photo by VCG/VCG via Getty Images)

VCG via Getty Images

Once China’s richest person, Hui falls out of the top 100 for the first time in 14 years.

Hui Ka Yan, the founder of real estate firm China Evergrande Group, has lost nearly all of his once massive fortune. Worth $42.5 billion and ranked the richest person in Asia at his peak in 2017, his wealth has been drastically diminished as debt woes plague the embattled developer. Yet as pressure mounts for the former tycoon to find a concrete way to repay his firm’s debts, analysts say he will certainly lose a lot more.

The 64-year-old, who dropped out of the 2022 ranks of China’s top 100 richest for the first time since his 2007 debut, now has an estimated net worth of $2.9 billion, an amount that is based entirely on the dividends he’s received over the years, though some of it has since been plowed into mansions, jets and a yacht. The number excludes Hui’s 60% stake in Evergrande, whose shares were suspended from trading in March, and still can’t meet the criteria for a resumption. Even before the suspension, the firm had lost about 95% of its peak value.

But even his personal assets are not safe from the firm’s creditors. Hui was forced to use $1 billion of his own cash to pay down Evergrande debt late last year earlier this year, and he sold earlier this year two luxury apartments at a discount–one in the city of Shenzhen and one in Guangzhou–for a combined $50 million (360 million yuan), apparently to help pay off more.

As Evergrande struggles to come up with a plan for restructuring its more than $300 billion in liabilities, which according to one person with knowledge of the matter will probably get delayed again and pushed out into 2023 due to the sheer size and complexity of the matter, more of his remaining trophy assets are likely at risk. Chen Zhiwu, a professor of finance at the University of Hong Kong, says amid China’s drastically changed political environment, the pressure is “really high, if not higher” for Hui to keep paying down corporate liabilities with his own money.

In fact, one of his three homes in Hong Kong’s prestigious The Peak neighborhood was seized by China Construction Bank (Asia) last week in November after Evergrande defaulted on a loan collateralized by the $90 million (estimated market value) property.

“Of course, he would like his personal assets and corporate assets very clearly separated, which officials aren’t willing to accept,” Chen says. “What this means is that when his company debt is in default, some of his personal fortune may have to be used to contribute to the payments to debt holders.”

The facade of 2-8a Rutland Gate, which is thought to be the most expensive home ever marketed in Britain, is recently put on sale by beleaguered billioniare Hui Ka Yan(Photo by Leon Neal/AFP via Getty Images).

AFP via Getty Images

Hui, who according to Evergrandethe company’s website is still a member of the ruling Communist Party, has pledged his two other luxury homes in the same posh Hong Kong locale as collateral for loans from Orix Asia Capital. He is also looking to sell his 45-room Knightsbridge mansion overlooking London’s Hyde Park area, two years after buying it from a Saudi prince for $232 million. And he owns private jets and a $60 million superyacht that he could be forced to sell.

As Evergrande’s revenues have fallen off a cliff (it only recorded $2.5 billion in contracted sales during the first eight months of the year, a plunge of around 96% from the prior year), Hui is unlikely to convince creditors that the company could ever generate enough cash flow for future repayment.

Of course, he would like his personal assets and corporate assets very clearly separated, which officials aren’t willing to accept.

Meanwhile, a nationwide mortgage boycott by angry buyers, who paid for their purchases in full but aren’t getting apartment complexes delivered on time after troubled developers such as Evergrande ran out of money, is putting pressure on the government. To quell public protests, which are rare in China, officials have agreed to issue special loans totaling $27.6 billion (200 billion yuan) to help with this type of work. Victor Shih, an associate professor of political economy at the University of California, San Diego, says banks are likely to have been told to lend to the financing arms of local governments, so that they could buy the unfinished projects from distressed real estate firms at a small discount. Evergrande said in September it had resumed working on 95% of its 706 pre-sold but undelivered construction projects.

But aside from protecting the interests of average homebuyers, few expect Beijing to reverse its course and unveil broader sector bailout measures–which are seen as crucial to restoring offshore creditor confidence. Kaven Tsang, a Hong Kong-based senior vice president at Moody’s Investors Service, says the economic pain inflicted by the real estate meltdown–including defaults, falling sales and rapidly slowing growth–are “within the [government’s] tolerance level.”

“The central government has made it clear in the past that they aren’t going to use the property sector to support the economy,” says Tsang. “We haven’t seen any changes so far.”

An Evergrande residential development under construction in Beijing, China. (Photo by Bloomberg)

Ron Thompson, a Hong Kong-based managing director at consulting firm Alvarez & Marsal Asia, says he thinks it would take at least two years for China’s housing demand to stabilize. Moody’s estimated in October that China’s property sales would continue to decline over the next 12 months, after shrinking 21% in August from the prior year, and 15.3% in September. Default risk remains high, given that the country’s developers have at least a combined $55 billion in bonds due over the next two years, but face weaker sales and limited refinancing options.

Amid this environment, bond investors mired in the restructuring of defaulted developers “aren’t expecting 100 cents on the dollar,” and are likely to demand equity and other collaterals to compensate for their rising losses, says Alvarez & Marsal Asia’s Thompson. Those who have lent specifically to Hui are increasingly taking things into their own hands, with more asset seizures and “wind-up” petitions to liquidate assets due to unpaid financial obligations, says Brock Silvers, a Hong Kong-based chief investment officer at Kaiyuan Capital, which invests in distressed assets.

Evergrande is facing a wind-up hearing in Hong Kong on Nov. 28, which was first brought in June by creditor and Samoa-based investment holding Top Shine Global Limited over $110 million in unspecified financial obligations.

Evergrande’s Hong Kong headquarters, which it acquired for $1.6 billion (HK$12.5 billion) in 2015 from Chinese Estates Holdings, controlled by Hui’s billionaire friend Joseph Lau, has also been seized by creditors and recently put on sale. The 26-story China Evergrande Centre located in Wan Chai now has an estimated value of around $1 billion, and the bidding process, concluded in late October reportedly drew interest from billionaire Li Ka-shing’s CK Asset Holdings.

Evergrande’s Hengchi 5 electric vehicle is on display at Hengchi experience center in Shanghai, China. (Photo by Wang Gang/VCG via Getty Images)

VCG via Getty Images

Hui appears to be pinning his last hope on electric cars. The Hong Kong-listed China Evergrande New Energy Vehicle Group , two thirds owned by parent Evergrande and whose trading has also been suspended since March, announced in late October that it had delivered the $24,700 Hengchi 5 electric sports utility vehicle to the first batch of 100 buyers, constituting a “major milestone” for Hengchi Auto. Parent company Evergrande also said in a July filing that it may offer equity interests in its EV unit as part of a “supplemental credit enhancement” package for restructuring offshore debt.

But Shen Meng, managing director at Beijing-based boutique investment bank Chanson & Co., says the EV deliveries offer little comfort to creditors. The beleaguered Hui, who once cherished ambitions to become the Elon Musk of China and propel Evergrande above Tesla, still has a long way to go before establishing Hengchi as a stable brand.

“The deliveries of the first batch doesn’t mean the maturing of Evergrande’s EV business, as it will take quite some effort to start bigger-scale production and delivery to the mass,” says Shen. “The EV unit is unlikely to be seen as a reliable asset, and it won’t help much with the restructuring process.”

If you’re unhappy with your partner’s spending habits, you’re not alone. One in five people in a relationship think their partner is bad with money, making them 10 times more likely to break up in the future.*

So, what’s your plan, then? Do nothing and see what happens? Or take a few steps to get on the same financial page with your partner?

While there’s no one right way for couples to handle their finances, here are some things you can do to potentially repair some damage and get on the right financial track moving forward. Together.

1. Have Open and Honest Money Talks Regularly

When it comes to a relationship’s financial success, being on the same page with your spouse is kind of a big deal. The truth is, they might not even realize they’re bad at money until you talk to them.

Scheduling regular conversations to discuss financial concerns and expectations will help you and your partner set realistic money goals while avoiding negative surprises. You might even learn that some of your own spending habits need to change.

Yes, if you both aren’t used to talking about money, this will feel a little awkward at first, but it will get easier over time. And, for the sake of your relationship’s long-term health — and maybe more importantly — your own happiness, it will be totally worth it.

2. Ask This Website to Help Pay Your Credit Card Bills This Month

Your credit card company doesn’t really care if it was you or your partner who racked up the credit card debt. It’s getting rich by ripping both of you off with high interest rates — some up to 36%. But a website called AmOne wants to help.

If you owe your credit card companies $50,000 or less, AmOne will match you with a low-interest loan you can use to pay off every single one of your balances.

The benefit? You’ll be left with one bill to pay each month. And because personal loans have lower interest rates (AmOne rates start at 2.49% APR), you’ll get out of debt that much faster. Plus: No credit card payment this month.

AmOne keeps your information confidential and secure, which is probably why after 20 years in business, it still has an A+ rating with the Better Business Bureau.

It takes two minutes to see if you qualify for up to $50,000 online. You do need to give AmOne a real phone number in order to qualify, but don’t worry — they won’t spam you or your partner with phone calls.

3. Simplify Your Budget

Want to manage your money as an actual team? Create a budget. Ew, gross. We know. But it’s important to take a good look at what you’re both spending and where you can both cut back.

If you’re not sure where to even start, we favor the 50/20/30 budgeting method for its simplicity. Here’s how it works:

50% of your income goes toward essentials.

20% goes toward financial goals.

30% goes toward personal spending.

The key is to accept you can’t create the perfect budget in an hour. You’ll have to experiment to find what works best for your relationship.

4. Raise Your Credit Score — and this Company Will Pay You up to $100

When one or both of you have damaged your credit score, it can really mess with your future financial goals — whether that’s buying a house, or taking out a loan for something else.

We all want to improve our credit score. And we’d all like to save a little more money. Good news: We found an online debit account that will pay you up to $100 every month for certain improvements you make to your credit score.**

It’s called Sesame Cash, an online bank account from Credit Sesame that comes with its own debit card. Here’s how it works: Simply add on Sesame Cash while signing up with Credit Sesame to get your free credit score and put in $25 to get started and activate your rewards. Then, put $25 toward the account each following month. This is a perfect way to set aside some money for emergencies — it’s out of sight, out of mind and will be there when you need it. It works like a prepaid debit card, but it’s so much more.

Even better, Sesame Cash will monitor your credit score and give you up to $100 when your credit score goes up.** To help you keep track, the Sesame Cash account lets you see what’s changed in your score every day, when you deposit $25 each month.***

Once the money is deposited into your Sesame Cash Account, you can spend it however you want to — after that open conversation with your partner, right? And if it’s at one of the more than 5,000 stores Sesame Cash partners with, like Burger King, Sephora or Walmart, you could earn up to 15% back instantly on your purchase.**** It’s like a gift that keeps on giving.

Creating a Sesame Cash bank account is quick and secure — we’re talking bank-level encryption. And if you need to raise your credit score anyway, getting paid to do it makes the process that much sweeter.

5. Find Out If You’re Overpaying

If you or your partner are trying to be more conscious of how much you’re spending on things, wouldn’t it be nice if you got an alert when you’re shopping online at Target and are about to overpay?

Just add it to your browser for free, and before you check out, it’ll check other websites, including Walmart, eBay and others to see if your item is available for cheaper. Plus, you can get coupon codes, set up price-drop alerts and even see the item’s price history.

Let’s say you’re shopping for a new TV, and you assume you’ve found the best price. Here’s when you’ll get a pop up letting you know if that exact TV is available elsewhere for cheaper. If there are any available coupon codes, they’ll also automatically be applied to your order.

In the last year, this has saved people $160 million.

6. Save Up to $610/Year When You Use This Website To Find New Car Insurance

When you’re looking to cut spending in your relationship, every dollar counts. Did you know you can save some serious money just by switching car insurance companies?

It’s true — rates are at historic lows, and you could be paying way less for the same coverage. All you need to do is look for it.

But don’t waste your time hopping around to different insurance companies. Use a website called EverQuote to see all your options at once.

EverQuote is the largest online marketplace for insurance in the US, so you’ll get the top options from more than 175 different carriers handed right to you.

Take a couple of minutes to answer some questions about yourself and your driving record. With this information, EverQuote will be able to give you the top recommendations for car insurance. In just a few minutes, you could save up to $610 a year.

7. Cancel Your Forgotten Subscriptions

Keeping track of your household’s subscription services can feel like a game of whack-a-mole. Just when you think you’ve got a handle on them all, another random charge pops up on your bank statement.

It’s easy to let it slide — $5 here, $10 there. But it can seriously add up. Luckily, an app called Rocket Money can show you exactly where you’re wasting money on forgotten subscriptions and bills that are overcharging you. It saves the average person $720 a year.

Rocket Money helps you find and cancel things like unused streaming subscriptions and expired free trials, and they’ll also negotiate lower monthly rates with your internet company, phone company and other bills — for the same service.

Rocket Money has already saved users more than $245 million, and it uses Plaid to make sure all your sensitive information is safe. The app does all the heavy lifting. All you have to do is sign off on these money-saving changes.

It takes just a few minutes to get started and see how much you could save this year. Just register an account and link your bank account, then sit back while Rocket Money goes to work.

8. Are You an Online Shopper? Copy This Strategy To Get a $526 Refund

Chances are you do some of your shopping online. Whether it’s pet food from Walmart, toilet paper on Target or even a flight to the in-laws for Thanksgiving, you’re probably leaving money on the table.

A free website called Rakuten has the hookup with just about every online store you shop, which means it can give you a kickback every time you buy.

In fact, since Denver resident Colleen Rice started using Rakuten, it’s sent her checks in the mail totaling $526.44. For doing nothing. Seriously. Rice says she uses Rakuten for things she already has to buy, like rental cars and flights.

It takes less than 60 seconds to create a Rakuten account and start shopping. All you need is an email address, then you can immediately start shopping your go-to stores through the site.

Plus, if you use Rakuten to earn money back within the first 90 days of signing up, it’ll give you an extra $10 on the first check it sends you. Talk about money for nothing.

9. Learn How to Build Healthy Money Habits, Together

One way to be a supportive partner is to learn and improve, together.

You might not want to take a Personal Finance 101 class together, but seize the opportunity now and listen to podcasts or read books — and, ahem, more of The Penny Hoarder. Shameless plug.

**This is a limited time offer. To be eligible for cash rewards, a deposit of $25.00, every 30 days, must be made into your Sesame Cash account. Rewards earnings are available for credit score improvements of ten points or more within a 30-day reward cycle. Improvements are calculated from your baseline credit score, as determined by Credit Sesame. Please review the full program terms for more details.

***This is a limited time offer. To be eligible for daily credit score refreshes, a deposit of $25.00, every 30 days, must be made into your Sesame Cash account. Daily refreshes will appear within 24-48 hours of deposit.

****Cash back offers are powered by Empyr, Inc. Cash back requires the activation of any active offer before payment is made. Payment must be processed as a credit transaction and made before the offer expires. Offers vary by geographic location and are subject to change. Please review the full program terms for more details.

*****Capital One Shopping compensates us when you get the extension using the links provided.

SHARM EL-SHEIKH, Egypt — Climate change talks have long been stymied over demands for transfers of billions of dollars — on Monday, French President Emmanuel Macron backed a new push for the conversation to be measured in trillions.

Speaking at the COP27 climate summit in Sharm El-Sheikh, Egypt, Macron gave his support to elements of a plan outlined by Barbados’ Prime Minister Mia Mottley that seeks to overhaul the way climate finance flows to the countries that most need it.

He called for a “huge shock of concessional financing,” suspension of debt for disaster-struck countries and putting the International Monetary Fund (IMF) on notice.

It was a speech that signaled a shift in tone that developing countries have been long been pushing for.

During the first day of official speeches, leader after leader from wealthy countries highlighted the need to demonstrate “solidarity” with developing countries after a year in which calamitous disasters and a bubbling debt crisis helped reshape the often contentious conversation about climate finance.

“It’s the right thing to do,” said U.K. Prime Minister Rishi Sunak.

Money is a central focus of this year’s climate talks given the widening gap between what has been pledged and what is needed. It extends from everything from clean energy transitions to hardening countries’ defenses against climate impacts to potential payments for irreparable climate damages.

In September, Barbados issued the world’s first pandemic and natural disaster bond. “The time has come for the introduction of natural disaster-pandemic clauses in our debt instruments,” Mottley said.

“God forbid, if we are hit tomorrow, we unlock 18 percent of GDP over the next two years, because what we do is effectively put a pause on all of our debt,” she said.

Macron called for the rules of the IMF, the World Bank and other major lenders to be changed to makeclauses that halt debt repayments in the event of a disaster far more common.

“What you’re asking of us in terms of debt reimbursement and guarantees, when we are affected by a climate shock, when we are a victim of a climate accident, to some degree, there must be a suspension of those conditions,” said the French president.

Broken promises

While the need for finance to spur the transition to clean energy across the world and guard against the ravages of climate change is already stretching into trillions, the U.N. climate system remains stuck on a broken decade-old promise from rich countries. They pledged to deliver $100 billion a year in climate finance by 2020, but that’s not likely to happen until next year.

As climate impacts have grown more extreme and prolific, appeals for new and more innovative forms of finance have escalated. Ballooning debt in the wake of the pandemic has heightened those calls, with dozens of vulnerable countries threatening a debt strike in the lead-up to COP27.

Mottley has been a champion of elevating the debt crisis facing nations like her own and highlighting how it adds to climate inequities. The plan she outlined in September hinges on debt relief, increased finance, and new mechanisms for post-disaster recovery, like bonds.

The Barbados leader’s call to arms and Macron’s heavyweight backing brought a new reality and scale to the financial discussion.

Mottley has pushed for the IMF’s special drawing rights to be put toward helping climate-vulnerable nations recover and respond to climate impacts. That could be used to help unlock far more money from the private sector — $500 billion from the IMF could result in $5 trillion in investments, she said Monday.

The challenge is getting shareholders in those financial institutions to agree to reforms.

Officials in the U.S., Germany and other major economies have pushed for an overhaul of the way multilateral development banks lend to allow them to extend more climate finance. U.S. Treasury Secretary Janet Yellen has called on the World Bank to draft a roadmap by the end of the year that could then be used to drive reform efforts at other development banks.

On Monday, Macron went further, saying that by next spring, global financial institutions would need to devise ways to “come up with concrete solutions to activate these innovative financing solutions and to help us to provide access to new liquidities.”

He paid tribute to Mottley’s “force of character” and said the two leaders — one who commands an economy 600 times larger than the other — had agreed to form a group of “wise minds” to develop suggestions for the overhaul of the international financial system.

But one Mottley suggestion that Macron swerved was her call for fossil fuel companies to pay a levy on their profits into a fund for disaster-hit countries.

“How do companies make $200 billion in profits in the last three months and not expect to contribute at least 10 cents on every dollar of profit to a loss and damage fund?” she asked.

Mounting medical bills can wreck your financial life. They can damage your credit score, make it difficult to pay other bills and demolish your emergency savings fund.

But the rising cost of health care and a lack of adequate insurance makes it difficult for many people to escape medical bills.

Fortunately, there are steps you can take both before and after seeking health care to help lower or even eliminate your medical debt.

So What Happens When You Don’t Pay Medical Bills?

You might not want to deal with that bill — but avoiding your medical debts can have serious financial consequences.

Specifically, this is what can happen if you don’t pay medical bills:

Additional reminders and phone calls from the hospital or doctor’s office

Late fee charges

Forwarding the debt to a collections agency

Increasing letters and phone calls from the agency

Legal action, such as wage garnishment

If a medical bill isn’t paid after a certain period of time, it can be turned over to a debt collection agency.

So long as a medical bill is yours, it’s accurate and you owe the money, then debt collectors can contact you to try to collect it, according to the Consumer Financial Protection Bureau.

Letting your medical bills linger in collections is a bad idea. Debt collectors can actually sue you to recover the money.

If they win the lawsuit, the debt collector can garnish wages from your bank account or place a lien on your home.

To avoid having your bill sent to collections, call the hospital or doctor’s office billing department and work with them to create a payment plan you can afford — then stick to it.

How Unpaid Medical Bills Impact Your Credit Score

Unpaid medical bills won’t hurt your credit score right away. But if you ignore them long enough, your credit score will suffer.

First, your medical provider will need to send the bill to a collection agency. That could take anywhere from one to six months. Then, the collection agency must try to collect on the debt for a full year before it appears on your credit reports.

If the agency reports the unpaid medical debt to credit reporting agencies, it will appear on your credit reports under payment history, which makes up about 35% of your credit scores.

The exact impact depends on your credit situation, but even someone with a good credit score could see a drop of as much as 50 to 100 points, though the effect will lessen over time

An unpaid medical bill in the payment history section of your report can cause your credit score to drop by as much as 50 to 100 points. Unpaid medical debts can linger on your credit report for up to seven years.

Your credit score impacts many things in your life. A bad credit score can keep you from opening a new credit card or skyrocket your interest rate on a new loan.

So Why Wouldn’t You Pay Your Medical Bills?

Well, some of us can’t afford unexpected medical bills.

More than 100 million people in the U.S. live with medical debt, according to a recent joint research project from NPR and the Kaiser Health Network released in July 2022.

The poll found that more than half of U.S. adults say they’ve gone into debt because of medical or dental bills in the past five years.

Medical debt isn’t just a problem for the uninsured or underinsured. It can also come from billing issues, like out-of-network doctors, hospitals or ambulance rides people thought were in-network.

The Consumer Financial Protection Bureau aired its concerns about the use of medical collections — a main point being that many consumers are unaware their medical debt even exists, unlike unpaid utility and phone bills.

The agency found that 58% of bills in collections and on people’s credit records are medical bills.

Here Are 6 Ways to Tackle Your Unpaid Medical Bills

The best advice, as with almost any financial matter, is to stay proactive.

“First, get a detailed, itemized statement to see if you even owe it and that it’s accurate,” said Pat Palmer, Medical Billing Advocates of America founder and CEO.

If you have health insurance coverage, make sure the claim was correctly submitted to your health insurance company and they paid their share.

Check your itemized billing statement for duplicate items, services you didn’t receive and charges that your health insurance company should have picked up.

Call the hospital billing department or your provider’s office manager with questions or if something doesn’t look right. Remember: You have the right to demand to know what you’re paying for.

You can also ask the provider not to send the bill to collections until you can make a payment. This isn’t guaranteed to work, but still worth trying.

2. Try to Negotiate Your Bill

If you find you do owe the bill, try calling and negotiating with your medical provider.

You might be able to negotiate your medical bill to a smaller amount or set up a repayment schedule, Palmer said.

Start the negotiation process with the medical provider — the hospital or doctor’s office where you got care. Medical providers may ask for proof of income or other financial statements.

Negotiating your medical bill can help get part of the unpaid debt forgiven. Or you might be able to work out a lower payment or a no-interest payment plan.

If the provider can’t or won’t negotiate and the bill is in collections, then ask the bill collector if you can settle for a lesser amount.

Providers and debt collectors are often willing to negotiate because they rather get some money from you than nothing at all.

If you’re successful, get details about the payment plan and the new amount you owe in writing. This way you have a record of your agreement with the provider or debt collection company.

3. Ask About Financial Assistance Programs

Owe a big hospital bill? Call the hospital’s billing department and see if they offer financial assistance for unpaid medical bills.

If you make less than the federal poverty income level, you could qualify for the hospital’s charity care program, which covers the medical expenses of patients with low incomes.

Even if you make two to three times the federal poverty level, you’re still likely to qualify for a discount on your bill.

Just make sure to speak with the billing department within 90 days of getting the bill.

4. Know Your Rights and Advocate for Yourself

Consumers are enjoying more protections from the credit-damaging consequences of medical debt than they used to.

In 2022, the three major credit reporting agencies — Equifax, Experian and TransUnion — announced that paid medical bills will no longer be included on credit reports issued by those companies.

In the past, a medical bill that went to collections could linger on your credit report for years — even after you paid it off.

Another change in 2022: Medical bills only show up on your credit report if they go unpaid for at least 12 months. (It used to be six months).

And starting in March 2023, the three major credit bureaus will not include information on medical bills in collection for amounts of $500 or less on consumer credit reports.

Here are two rights you have, according to the Consumer Financial Protection Bureau:

Medical debt collectors can’t engage in aggressive collection tactics, like calling you around the clock, harassing you or contacting you through social media pretending to be someone else. You have the right to tell collections agencies to stop contacting you. Learn about your rights in the debt collection process and how to file a complaint.

Debt collectors can’t report a medical bill to the three credit bureaus without trying to collect the debt from you first. Here’s how to dispute an error on your credit report.

In August 2022, VantageScore announced all paid and unpaid medical debt — regardless of how much is owed or how long the debt has been in collections — will be excluded from 3.0 or 4.0 score calculations by mid-October 2022.

Finally, The No Surprises Act protects you from receiving surprise bills from out-of-network providers you didn’t choose in a medical emergency. This rule went into effect January 2022.

Dealing with debt collectors? Knowing these five things can reduce your stress and save you time.

5. Get Outside Help

Medical bill advocate organizations can help negotiate bills on your behalf. They can also detect billing errors the average patient might miss.

Medical bill advocates come at a cost, though. They often charge by the hour (think $100 an hour or more), or they take a percentage of the amount they’re able to get reduced from the bill (usually 25% to 35%).

Opinions expressed by Entrepreneur contributors are their own.

“You can’t take it with you” — how often have you heard that?

It’s an oft-abused phrase employed, usually within the context of a person amassing wealth or assets beyond their needs. What it speaks to is intent, and that’s what building multi-generational wealth is all about: growing your assets to pass them on to future generations.

We’re not just talking about money and other valuable items, though. There’s far more to it than that.

Right now, in the West and throughout the world, we’re experiencing deep financial uncertainty. Especially since the crash of 2008, we’ve been on an increasingly fast treadmill of debt.

Most Millennials and Generation Z in America identified home ownership as the prime marker for success. Increasingly, though, they are being priced out of the housing market altogether. Two-thirds of non-homeowners cited affordability as why they didn’t own their own home.

There are, of course, several factors that have gone into this situation. It boils down to a total lack of focus on building generational wealth. Now we could lay that at the feet of consumerism; far too much emphasis on instant gratification, not enough on the journey of life and deferred gratification for greater future reward.

Certainly, that’s true to an extent. We buy on credit now more than ever (I’ll get to why that’s bad…but not why you think, shortly). We seek shortcuts and outcomes rather than journeys and experiences. But as with everything in life: the answer lies in more than one factor.

Right now, we’re experiencing the perfect storm of destabilizing geopolitics, recessions, war and cultural norms that don’t favor multi-generational wealth.

We’ve cultivated this sense of wealth being about what you can demonstrate to others. It’s all about “flex” culture (as the kids say). But this belies the true nature of what it means to be wealthy.

What is wealth?

I’m not going to say something as predictable or demonstrably untrue as: “wealth has nothing to do with money.” That kind of platitudinal soundbite is also part of the problem. We’re not holding ourselves accountable for what we say publicly. Money is absolutely a component of wealth, there’s no doubt. But it also doesn’t paint the complete picture.

A “wealth” of something simply means that you have an abundant supply of it. For example, you can have a wealth of knowledge. It comes down to how resourced you are as a person and how valuable you can be as an individual to the broader community.

We’ve done ourselves a cultural disservice in emphasizing money. Not that this is some kind of anti-capitalist rant! I’m a serial entrepreneur, after all. We do, however, need to steer the conversation towards other forms of wealth to heal the current pain we find ourselves in.

For multi-generational wealth, we must take a more holistic approach to life

Millions of dollars in the bank won’t serve you if you have to sacrifice your mental well-being and time with your family (or a family, for that matter) to achieve it. My vision of multi-generational wealth is not about one generation falling on their proverbial sword to bring it about.

My approach is about breaking these “molds” into which we constantly try to force ourselves. I want us to ditch the ‘cookie-cutter’ approach altogether and really examine what we have to offer future generations beyond just accrued capital.

Thanks to inflation, the money that you leave behind for your kids will be eroded by the sands of time anyway.

Our education systems throughout the west offer pitifully little education when it comes to money management. We need to start teaching our kids how to handle money properly if we want to build generational wealth.

That starts with understanding how to use debt properly!

We’re used to buying things on credit, usually having been fed the ridiculous line about how it frees up your capital to earn money. Given the rates that most retailers and third-party lenders charge, that’s total garbage.

You find me a savings account or investment portfolio that will give you the level of return that will match or exceed what they’re charging!

That said: we also need to avoid the trap of thinking that debt is inherently evil. It’s not. It just depends on how you use it.

Consumer debt (i.e., buying consumables with debt) is a terrible idea because you’re servicing debt on something that is losing value. Hence why you can leverage your capacity to service debt, for example, to become a lender yourself essentially. That’s how a lot of other successful entrepreneurs and I make a lot of money.

From an entrepreneurial perspective, educating your kids about how debt works is a massive leap toward building generational wealth.

This means educating yourself — no bad thing. I would encourage you to break the old habits and stigmas around debt for your own sake. Learn to identify the difference between consumer debt and the debt you can leverage.

The most important advice I can offer to you as an entrepreneur that will help you build multi-generational wealth is to…

Find your ‘why’!

“He who has a why to live for can bear almost any how” — Friedrich Nietzsche

This is always the first port of call for anyone I coach in business. It’s the single most important thing to teach your kids if you want them to build on your legacy.

You must understand what’s driving you and why. That takes serious introspection and hard work. You will need to weed out all the programmings you’ve been fed since you were a kid that is keeping you motivated by the desires of others.

We think that so much of what drives us comes from us. More often than not, however, we’re being driven by what someone else expects of us. When we don’t confront this proactively, it leads to mid-life crises.

The stark realization that we have less time left than we’ve had throws into sharp relief all of the things we’ve valued and how little we actually did for ourselves!

Don’t let that be the legacy you leave.

Get your head around the life that you want to lead. Be an example to future generations and build your resources (money, knowledge, health, energy, etc…) to be of maximal service.

Being of service to others ultimately builds true wealth, after all.

You probably know that paying down debt is good for your credit score. But there’s a persistent myth about credit card balances and credit scores. Some people say that carrying a small balance from month to month somehow helps your credit score.

The idea that carrying a balance helps your credit score is totally false. Read on to learn the facts about how your balance affects your credit score.

How Your Credit Card Balance Affects Your Credit Score

There are five things that determine your credit score. These credit score factors break down as follows:

Payment history (35%)

Credit utilization (30%)

Average age of credit (15%)

Credit mix (10%)

Hard inquiries and new credit (10%)

As you can see, your credit utilization, or the percentage of open credit that you’re using, accounts for 30% of your credit score. The rule of thumb is that you don’t want your credit utilization ratio to climb higher than 30%. If you can get it to 0%, that’s ideal.

Here’s where it gets a bit tricky. If you’re regularly using credit, a balance will probably show up on your credit report. That’s because you don’t control when your credit card company reports activity to the bureaus.

For example, suppose you have a $5,000 limit and a zero balance. Then you make a $100 purchase. If your creditor then reports to the bureau, you’ll have a 2% credit utilization ratio ($100/$5,000 = 2%), even if the bill hasn’t come due yet.

Having a credit utilization ratio above 0% isn’t necessarily something to worry about, though. According to Experian, consumers with a perfect 850 FICO score have an average credit utilization of 5.8%.

That doesn’t mean the average person with a perfect score is carrying a 5.8% balance from month to month. When your creditor reports to the bureaus, they’re simply providing a snapshot of your account at that given moment. Even if you pay off your balance in full each month, it’s likely that your account will show that you’re using up part of your open credit.

If your credit utilization ratio is 0% because you never use your credit cards, your score could suffer. When you’re not making regular credit purchases and you don’t have outstanding loans, you aren’t generating activity that’s reported to the credit bureaus. That’s harmful because payment history is even more important than your credit utilization.

Moreover, your credit card company could cancel your card due to inactivity. That hurts your score in two ways: Your credit utilization could increase because the amount of open credit you have will drop. If the card was also one of your older accounts, it will also lower your average length of credit.

Should You Carry a Credit Card Balance?

There’s no benefit to your credit score when you don’t pay off your balance in full. You’ll also pay unnecessary interest, unless you’re taking advantage of a temporary interest-free window.

That said, you shouldn’t worry about a balance showing up on your credit report. As long as your balances — both overall and on each individual card — stay below 30%, you’ll be able to build good credit.

Make every payment on time. The No. 1 habit of people with exceptional credit scores is that they never miss payments. One late payment will stay on your credit report for seven years.

Always keep your utilization below 10%. Most members of the 800 club pay off their balances in full each month, but many say they never let their balances climb above 10%.

Keep your oldest card open. As you build good credit, you typically qualify for better credit card rewards. But people with top-notch credit keep those old cards open and use them for a small monthly purchase. Credit scoring models favor customers who have long-term relationships with their cards.

Finally, don’t worry too much about small fluctuations in your credit score. Your score can vary from month to month based on the balance you have at the time your creditor reports to the bureaus. Fluctuations are completely normal. Focus on making on-time payments and keeping your balances low, and you’ll build a healthy credit score.

Robin Hartill is a certified financial planner and a senior writer at The Penny Hoarder. She writes the Dear Penny personal finance advice column. Send your tricky money questions to [email protected]or chat with her in The Penny Hoarder Community.

If you’re planning a trip out of the U.S., you’ve probably started to worry about how you’re going to pay for things once you get there.

To avoid running around with a pocket full of cash — a situation we DON’T recommend — a no foreign transaction fee credit card might be your solution.

No foreign transaction fees means you can pay for things without being dinged for the privilege of using a foreign bank.

However, most credit cards do charge foreign transaction fees, so we’ve gathered a list of the best no foreign transaction fee credit cards on the market to meet your traveling needs.

The Best Credit Cards with No Foreign Transaction Fees

Chase Sapphire Preferred Credit Card: Best Overall

Capital One Venture X Credit Card: Best Premium Travel Cards

American Express Gold Credit Card: Best for Foodies

Discover it Cashback Credit Card: Best for No Annual Fee

Capital One QuickSilver Credit Cash Rewards: Best for Simple Cash Back

United Explorer Credit Card: Best Airline Credit Card

Ink Business Preferred Credit Card: Best for Business Travelers

Bank of America Travel Rewards Card for Students: Best for Students

Petal 1 “No Annual Fee” Credit Card: Best for Bad Credit

Chase Sapphire Preferred Credit Card

Best Overall

Key Features

60K sign-up bonus points

$50 annual hotel credit

The Chase Sapphire Preferred credit card is our overall winner for the best no foreign transaction fee credit card because it has good reward rates, a lucrative sign up bonus, and lots of peace of mind travel perks to keep you protected while you travel.

Chase Sapphire Preferred Credit Card

Annual Cost

$95

Regular APR

18.24-25.24% variable APR

Reward Rate

1 – 5 points per $1

Credit Score

Good to excellent credit (670 and higher)

More Information about Chase Sapphire Preferred Credit Card

The Chase Sapphire Preferred credit card offers a whopping 5x points on travel purchased through Chase Ultimate Rewards. You then get 2x points on all other travel purchases, 3x points on online grocery purchases, dining purchases, and streaming services, and 1x points on all other purchases. Plus, for a limited time, you’ll get 5x points on Lyft (until March 31, 2025).

When you’re ready to cash in your points, you can log on to the Chase Ultimate Rewards portal or transfer your points at a 1:1 ratio to any of Chase’s 11 airline partners or 3 hotel partners. However, you’ll get more value booking travel on the Chase Ultimate Rewards website because your points are worth 25% more when you book through Chase.

This 25% value addition also amplifies your sign up bonus. When you sign up, you’ll receive 60,000 bonus points after you spend $4,000 in the first three months. With the 25% increase, these points are worth approximately $750 when redeemed for travel purchased through Chase Ultimate Rewards.

Chase also rewards you for booking hotels through their website with their annual hotel credit. You can receive up to $50 in statement credits each year if you purchase hotels through Ultimate Rewards.

As if all that wasn’t enough, to top it off you’ll get 10% of your total points back each anniversary as a reward for keeping your credit card account open.

The Chase Sapphire Preferred card of course has no foreign transaction fee for international purchases, but it doesn’t offer any Global Entry reimbursement or airport lounge access which is a bummer.

However, you do get Auto Rental Collision Damage Waiver, Trip Cancellation/Trip Interruption Insurance, travel and emergency assistance services, extended warranty protection, and purchase protection–some nice perks if you’re using this card for an oversea adventure but you want to keep it from becoming too adventurous.

Capital One Venture X Credit Card

Best Premium Travel Card

Key Features

75,000 bonus miles with eligible purchases

10,000 anniversary miles bonus

The Capital One Venture X credit card offers lots of premium perks and credits that help make up for the hefty annual cost.

Capital One Venture X Credit Card

Annual Cost

$395

Regular APR

19.99% – 26.99% variable APR

Reward Rate

2 – 10 points per $1

Credit Score

Excellent (750 and above)

More Information about Capital One Venture X Credit Card

The Capital One Venture X credit card claims to be an elevated rewards card and, for the most part, it delivers.

First off, you get 75,000 bonus miles when you spend $4,000 on purchases within the first 3 months of the account opening.

This large sign up bonus isn’t the end of Capital One’s bonus points, with 10,000 points each account anniversary year. Plus, they’ll reimburse up to $300 in travel when booked through Capital One Travel.

When booking travel, you can feel secure you’re always getting Capital One’s best prices with their free price drop protection and free 24 hour price match.

These perks start to make the hefty $395 annual fee feel much more manageable.

When it comes to earning points, you’ll get 10x points for hotels and rental cars booked through Capital One Travel and 5x points for flights when they are also booked through Capital One Travel. All other purchases get 2x points for every dollar spent.

You also get access to the Capital One Lounges and their partner lounge network. You can get you and 2 guests into the lounge each visit. While the partner lounge network is pretty vast, there is only one actual Capital One Lounge located in Dallas/Fort Worth International Airport, with two being built in the Denver and Dulles airports.

Capital One adds TSA Precheck or Global Entry reimbursement to their no foreign transaction fees and travel perks. You also get peace of mind with cell phone protection, primary auto insurance, and travel accident insurance.

American Express Gold Credit Card

Best for Foodies

Key Features

90K membership rewards points

$120 dining credit

This card is almost a no-brainer for foodies for whom travel is incomplete without the local dining experience. While the annual fee is a little high, the 4x returns on restaurants worldwide and $120 dining credit make the American Express Gold Card a tasty choice for international dining enthusiasts.

American Express Gold Credit Card

Annual Cost

$250

Regular APR

18.99% – 25.99% variable APR

Reward Rate

1 – 4 points per $1

Credit Score

Good to excellent credit (670 and higher)

More Information about American Express Gold Credit Card

In many ways, the American Express Gold Card is an international foodie’s dream. With the combination of no foreign transaction fees and 4x points for restaurants worldwide, this card rewards you for sampling the newest international cuisine.

You also receive 4x points on US supermarket purchases (up to $25,000 annually), 3x points on flights booked with airlines or at amextravel.com, and 1x points on all other purchases.

American Express Gold Card also offers a $120 dining credit. Basically, you earn $10 in statement credit monthly when you use your card to pay at select restaurants. Enrollment is required, but it’s like free food money.

Speaking of free money, the Gold Card also offers $120 Uber cash credit. All you have to do is add the card to your Uber account and you’ll get $10 of Uber Cash each month to spend on Uber eats or Uber rides in the US.

You also can get 60,000 membership rewards points in a sign up bonus after you spend $4,000 in the first 6 months.

These points can be transferred to American Express’ 17 airline partners and 3 hotel partners. Most of the transfers are 1:1, but know that you will be charged $0.00006 per point with a maximum fee of $99 when you send them to US airlines.

While these perks are great, the annual fee is higher than most other similar credit cards. If you’re raking in points, it can still definitely be worth it, but it’s worth checking that you’ll be spending enough in those categories.

Discover it Cashback Credit Card

Best for No Annual Fee

Key Features

5% cash back in rotating categories

0% introductory APR

The Discover it Cashback card offers good rewards rates to earn cash rewards. You do have to activate rotating bonus categories each quarter, but with no annual fee, the Discover it Cashback is still a solid no foreign transaction fee choice.

More Information about Discover it Cashback Credit Card

The Discover it Cashback card offers 5% cash back on rotating bonus categories that change quarterly. You have to activate these categories because you aren’t signed up for the bonus automatically, but we think the 5% return makes a little work worth it.

The rotating categories are:

January through March – 5% back on grocery stores (excluding Walmart, Target, and warehouse stores) and fitness clubs or gym memberships

April through June – 5% on gas stations and Target

July through September – 5% on restaurants and Paypal

October through December – 5% on Amazon.com and digital wallet purchases

You have to log onto your account to activate the bonus category each quarter. Also, each category has a $1,500 maximum rewards return. All other purchases receive 1%.

While getting your extra 5% cash back bonus category is a little complicated, getting your rewards into your pocket couldn’t be easier. With Discover, your cash rewards can be deposited directly to your bank account, applied as a statement credit, or sent to Amazon.com or Paypal.

As icing on the cake, you’ll also get Discover’s Unlimited Cashback Match where they’ll give you a dollar-for-dollar match of your cashback earned automatically at the end of your first year.

While there are no specific travel rewards with this card (Discover does have a travel specific card, but the reward rate of this card is better), it does have awesome customer service that’s available to help you 24/7.

One of people’s main concerns with Discover is that it’s not as widely accepted. Within the US, this is no longer true with Discover being accepted 99% of the time. Outside of the US, however, Discover’s coverage is more limited in Africa, the Middle East, and Eastern Europe, which is why we couldn’t give it 5 stars.

Capital One QuickSilver Cash Reward

Best for Simple Cash Back

Key Features

$200 new card member offer

No annual fee

With no annual fee, the Capital One QuickSilver Cash Rewards card’s flat rate of 1.5% cash back on everything makes it an easy card to feel comfortable with. It’s simple; you don’t have to activate bonus categories or watch that you’re purchasing the right things. You just spend and earn.

More Information about Capital One QuickSilver Cash Rewards Credit Card

The Capital One QuickSilver Cash Rewards card is a no fuss credit card that offers a decent return on all purchases. This simplicity does cost you a little in reward returns, but you can get 5% back on hotels and rental cars booked through Capital One Travel.

We love the low intro APR with 0% for 15 months on purchases and balance transfers, then 17.99% to 27.99 % after that. Plus, they also currently offer a $200 cash bonus if you spend $500 on purchases in the first three months.

Because Mastercard is the credit card issuer, the Capital One QuickSilver is accepted pretty widely internationally, so the no foreign transaction fees will come in handy.

Besides that, they offer $0 fraud liability, 24 hour travel assistance services, extended warranty, and travel accident insurance.

It might not be the way to earn rewards quickly, but the Capital One QuickSilver is a good option for simple earning and easy foreign spending.

United Explorer Credit Card

Best Airline Credit Card

Key Features

50K sign-up bonus miles

$0 fee for the first year, then $95

The United Explorer Card is one of our favorite airline cards with a $0 introductory fee, good reward returns, and some airport perks not offered by other mid-tier cards. If you fly with United, this card offers some really good perks for not that much out-of-pocket and is probably a good choice for your no foreign transaction fees card.

United Explorer Credit Card

Annual Cost

$0 introductory annual fee then $95

Regular APR

18.74-25.74% variable APR

Reward Rate

1 -2 miles per $1

Credit Score

Good to excellent credit (670 and higher)

More Information about United Explorer Credit Card

The United Explorer Card offers 2 miles for every dollar spent at United Airlines, restaurants, and hotels. All other purchases earn you 1 mile per dollar.

You can also currently earn 50,000 miles in a sign up bonus when you spend $3,000 in the first 3 months. Plus, you can claim a $0 introductory rate for the annual fee, making the card an easy financial decision.

While traveling with the United Explorer Card, you get no forieign transaction fees, priority boarding, and a free checked bag for you and a friend.

You can also get a $100 TSA PreCheck, Global Entry, or NEXUS fee credit and two one-time passes to the United Club airport lounge. It’s not a yearly membership, but for the annual fee, it’s a nice perk.

As you earn points, you can achieve United’s Premier Status which gives you preferred seating, upgrades, waived fees and access to Saver Award flights–flights offered at a lower miles rate.

The key value to an airline credit card is that it matches where you fly. Check out our 5 best airline credit cards to find the airline card that matches your flight pattern.

Ink Business Preferred Credit Card

Best for Business Travel

Key Features

100K bonus points

Chase Ultimate Rewards

Offered by Chase, the Ink Business Preferred credit card is a good choice for most business owners. It earns you 3x points back on common business expenses and 25% more value when you redeem points through Chase Ultimate Rewards.

Ink Business Preferred Credit Card

Annual Cost

$95

Regular APR

18.99% – 23.99 % variable APR

Reward Rate

1 – 3x points per $1

Credit Score

Good to excellent credit (670 and higher)

More Information about Ink Business Preferred Credit Card

One of the biggest draws to the Ink Business Preferred card is the huge sign up bonus. You’re rewarded 100,000 bonus points after you spend $15,000 on purchases in the first 3 months of opening your account. That’s about $1,000 in cash or $1,250 in travel points on Chase Ultimate Rewards.

Off the bat, that’s a great start for a business card.

You can also earn points on your business spending, earning 3 points for every dollar spent (up to $150,000 each year) on common business expense like:

Shipping

Advertising purchases with social media sites and search engines

Internet, cable, phone purchases

Business travel

Everything else earns 1 point per dollar, but these common business spending returns will probably more than compensate for the $95 annual fee.

Like other cards offered by Chase, you get 25% more value with your points when you redeem them for travel through Chase Ultimate Rewards or you can transfer them to Chase’s airline or hotel partners on a 1:1 basis.

Other business perks with the Ink Business Preferred card include free employee cards, 24/7 access to quarterly reports, fraud protection, trip cancellation insurance, and more. We especially like the cell phone protection plan which will give you up to $1,000 per claim for you and any of your employees listed on your bill.

Petal 1 “No Annual Fee” Credit Card

Best for Bad Credit

Key Features

No Annual Fee

Starter credit limits

Petal 1 “No Annual Fee” Visa Credit Card is for borrowers with bad or no credit history that struggle to qualify for other credit cards. The card offers cash back at select merchants and a potentially high credit limit.

Petal 1 “No Annual Fee” Credit Card

Annual Cost

$0

Regular APR

22.99% to 32.49% Variable APR

Reward Rate

2% – 10% cash back

Credit Score

Poor to no credit history (300 and higher)

More Information about Petal 1 “No Annual Fee” Visa Credit Card

If you’re looking at this list and worried that you won’t qualify for any of the cards above, the Petal 1 “No Annual Fee” Visa Credit Card might be the right choice for you. It’s an unsecured card that offers no annual fee and no foreign transaction fees.

With this card, credit limits start around $300 but can go as high as $5,000. You can qualify for a credit increase each 6 months by making qualifying on-time payments and keeping your credit score within a specific, personalized range. Many “bad credit” cards have much lower credit limits, so we love the possibility of such a high limit.

As expected, this card has a high APR that can really hurt you if you carry a balance. However, many similar credit cards charge an annual fee, so the fact that this one doesn’t and you can still receive cashback at select merchants is a nice feature.

What is a Foreign Transaction Fee?

A foreign transaction fee is a fee that credit card holders pay for transactions that pass through a foreign bank. While we mostly think of foreign transaction fees applying when you visit a foreign country, they are also assessed when you purchase something from a foreign merchant or in a foreign currency online.

A credit card’s foreign transaction fee is normally somewhere between 1% to 3% of the transaction. While this fee technically includes an issuer fee and a network fee, it is shown as one composite percentage to help you understand how much each transaction will cost you. Legally, this percentage must be communicated to the consumer, so you should be able to find it on your card membership agreement.

How much are Foreign Transaction Fees?

Foreign transaction fees normally range from 1% to 3% per transaction. Credit card companies are required to publish these fees, but make sure to read the fine print.

For example, some cards also have a minimum charge amount. This means for each foreign transaction you will be charged the greater of the percentage of the purchase or a set dollar amount (typically $1) — that makes your $2 water bottle purchases significantly more expensive.

Foreign Transaction Fee Comparison

Issuer

Foreign Transaction Fee

American Express

2.7%

Bank of America

3%

Barclays

3%

Capital One*

None

Chase

3%

Citi

3%

Discover*

None

US Bank

Up to 3%

Wells Fargo

3%

*Capital One and Discover do not charge foreign transaction fees on any of their cards

What to Look for in a No Foreign Transaction Fees Credit Card?

What makes a good no foreign transaction fee card looks pretty similar to a normal credit card — namely: APR, annual fees vs. rewards, and sign-up bonuses — but unlike a normal credit card, we also pay attention to the offered travel benefits.

APR

In an ideal world, you’ll never need to worry about your credit card’s APR. But, in case you end up not being able to pay your balance off in full each month, we think it’s important to understand what you might be charged in interest.

You’ll want to pick a card with a low APR, just in case you ever end up carrying a balance. We especially love the cards that offer a 0% APR as an introductory offer.

Annual Fee vs. Rewards

In essence, you want to make sure that this card isn’t costing you more than the service it’s providing you. While some cards offer $0 annual fees, the more expensive cards tend to offer more rewards — just make sure you’ll be able to take advantage of them.

One thing you might check is that your spending habits line up with the card’s reward system. It won’t benefit you at all that your card offers 8% on Lyft if you never rideshare.