[ad_1]

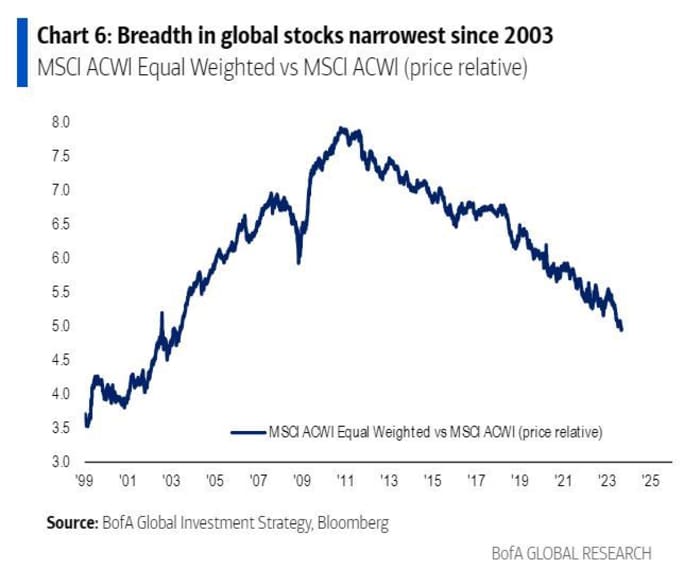

U.S. stocks have risen sharply in 2023, with a small number of technology companies driving an ever-increasing share of the stock-market gains.

While the 11.7% year-to-date gains for the large-cap benchmark S&P 500 index

SPX

show 2023 has been a “good year” for stocks, that hardly tells the whole story, said Jonathan Krinsky, the technical strategist at BTIG.

The U.S. stock market has seen the median return for shares in the S&P 500 index rise merely 1.1% in 2023, which is “a different planet” compared with their median gain of 16.2% in 2014, when the benchmark index recorded a yearly advance of 11.4%, Krinsky said in a Sunday note (see chart below).

SOURCE: BTIG ANALYSIS, BLOOMBERG

The Russell 3000

RUA

— a barometer that represents approximately 98% of the American equities — had a median return of negative 2.2% this year, but the index has gained 11.3% year to date, wrote Krinsky, citing BTIG and Bloomberg data. In 2014, the median return for the Russell 3000 was 6.9%, and it recorded a yearly gain of 10.4%.

Meanwhile, the median year-to-date return for stocks in the S&P 1500, which includes all shares in the S&P 500, S&P 400

MID

and S&P 600

SML

and covers approximately 90% of U.S. stocks, rose a merely 0.1% versus the index’s 11.2% advance this year, said Krinsky. The S&P 1500 recorded a median return of 8.8% in 2014 and was up 10.9%.

So far in 2023, investors have struggled to brush off a rise in Treasury yields primarily triggered by the Federal Reserve bumping up interest rates and the risk of recession, with hope that the stock-market rally hasn’t run out of steam yet.

However, the S&P 500 and the Nasdaq Composite

COMP

Friday locked in their worst month of the year, down 4.9% and 5.8%, respectively, according to FactSet data.

Treasury yields continued to rise on Monday with the yield on the 2-year

BX:TMUBMUSD02Y

up 6.4 basis points to 5.110%, while the yield on the 10-year Treasury

BX:TMUBMUSD10Y

jumped 11 basis points to 4.682%. The 10-year rate ended at its highest level since Oct. 12, 2007, according to Dow Jones Market Data.

As a result, investors were hoping October and the last quarter of 2023 could bring some relief to the scorching summer selloff they had to endure in markets. Historically, the fourth quarter has been the best quarter for the U.S. stock market, with the S&P 500 index up nearly 80% dating back to 1950 and gaining more than 4% on average, according to data compiled by Carson Group.

“It seems to us that a rally [in the fourth quarter] is the consensus view based on the fact that seasonals tend to work that way,” Krinsky said. “While October is a strong month on ‘average’, it has been down ten of the last 30 years, with eight of those years losing 1.77% or more.”

In other words, when October is good it tends to be really good, but when it’s bad it tends to be quite bad, Krinsky added.

U.S. stocks finished mostly higher on Monday with the Dow Jones Industrial Average

DJIA

down 0.2%, while the S&P 500 ended flat and the Nasdaq edged up 0.7%, according to FactSet data.

[ad_2]