Contract semiconductor manufacturer GlobalFoundries (NYSE: GFS) is the fourth largest producer of computer chips producing 7% of the world’s supply. This pales compared to the 53% market share controlled by Taiwan Semiconductor Manufacturing Company (NYSE: TSM). It’s ironic that GlobalFoundries was a divestiture of one of Taiwan Semi’s largest contract manufacturing clients, Advanced Micro Devices (NYSE: AMD).

AMD had decided in 2008 to go fabless and outsource its capital-intensive chip production rather than continue losing money producing them in-house. This asset-light model worked out great for AMD and Taiwan Semi. GlobalFoundries was left on its own to turn around a money-bleeding operation into a profitable business firing on all cylinders with top and bottom line metrics.

MarketBeat.com – MarketBeat

It Pays to Be Made in the U.S.A.

Being a domestic chip maker has its perks these days as the U.S. makes an aggressive attempt to bolster its production of semiconductors to reduce its reliance on foreign producers. The CHIPS Act of 2021 provides nearly $280 billion in funding which includes $52 billion in manufacturing and research grants and a 25% investment tax credit (ITC) to make chips in the U.S.

GlobalFoundries is based in Malta, New York, and has operations in the U.S., Singapore, and the European Union. It has received $30 million in funding in Vermont and received approval to become its own utility enabling it to buy electricity on the cheap. Rival domestic chip maker Intel (NASDAQ: INTC) is also a key benefactor of the CHIPS Act.

The World’s Fourth Largest Chipmaker

GlobalFoundries supplies chips used in smart mobile devices, computing, automotive, communications, infrastructure, datacenter, aerospace and defense, and the internet of things (IoT). It’s long-term agreements (LTAs) have grown to 38 customers totaling nearly $27 billion in revenues. Committed prepays rose 6% to $3.8 billion.

It shares many customers with Taiwan Semi. It extended its production contract with Qualcomm (NASDAQ: QCOM). AMD is still a customer of GlobalFoundries but transferred production of 7 nanometer (nm) core dies to Taiwan Semiconductor. This was due to GlobalFoundries terminating its outfitting for 7 nm production to the prohibitive costs involved in 2018. GlobalFoundries was added to the Philadelphia Stock Exchange Semiconductor index (SOX) on Sept. 19, 2022.

Record Top and Bottom Line Growth

On Nov. 8, 2022, GlobalFoundries released its fiscal third-quarter 2022 results for the quarter ending September 2022. The Company reported an earnings-per-share (EPS) profit of $0.67 excluding non-recurring items versus consensus analyst estimates for a profit of $0.62, a $0.06 beat.

Revenues rose 22% year-over-year (YoY) to $2.07 billion beating analyst estimates for $2.05 billion. The Company achieved record gross margins of 29.4% and adjusted gross margins of 29.9%.

The Company recorded record net income of $336 million and an adjusted EBITDA of $793 million. GlobalFoundries ended the quarter with cash and cash equivalents of $3.5 billion.

CEO Thomas Caufield commented, “300mm-equivalent wafer shipments of 637 thousand was a record for GF, an increase of 5% year-over-year. Our revenue grew 22% year-over-year, and we delivered record gross, operating, and net profits, making significant progress toward our long-term financial model. We remain on track to deliver a strong year of growth and profitability.”

Raising Guidance

GlobalFoundries upped their Q4 2022 guidance for EPS to come in between $1.14 to $1.44 versus $1.00 consensus analyst estimates. Revenues are expected between $2.05 billion to $2.10 billion versus $2.08 billion consensus analyst estimates.

Geopolitical Risk-Free

Unlike Taiwan Semi, GlobalFoundries faces no geopolitical risk. Taiwan Semi is in a territorial dispute with China which always carries the risk of a potential invasion. South Korea’s Samsung (OTCMKTS: SSNLF) faces the constant threat of an invasion by North Korea. Furthermore, GlobalFoundries is expected to be a pure play benefactor of the CHIPS Act and also the European Chips Act, which seeks to bolster the production of semiconductors in Europe from 10% to 20% by 2030 investing up to 43 billion euros in funding.

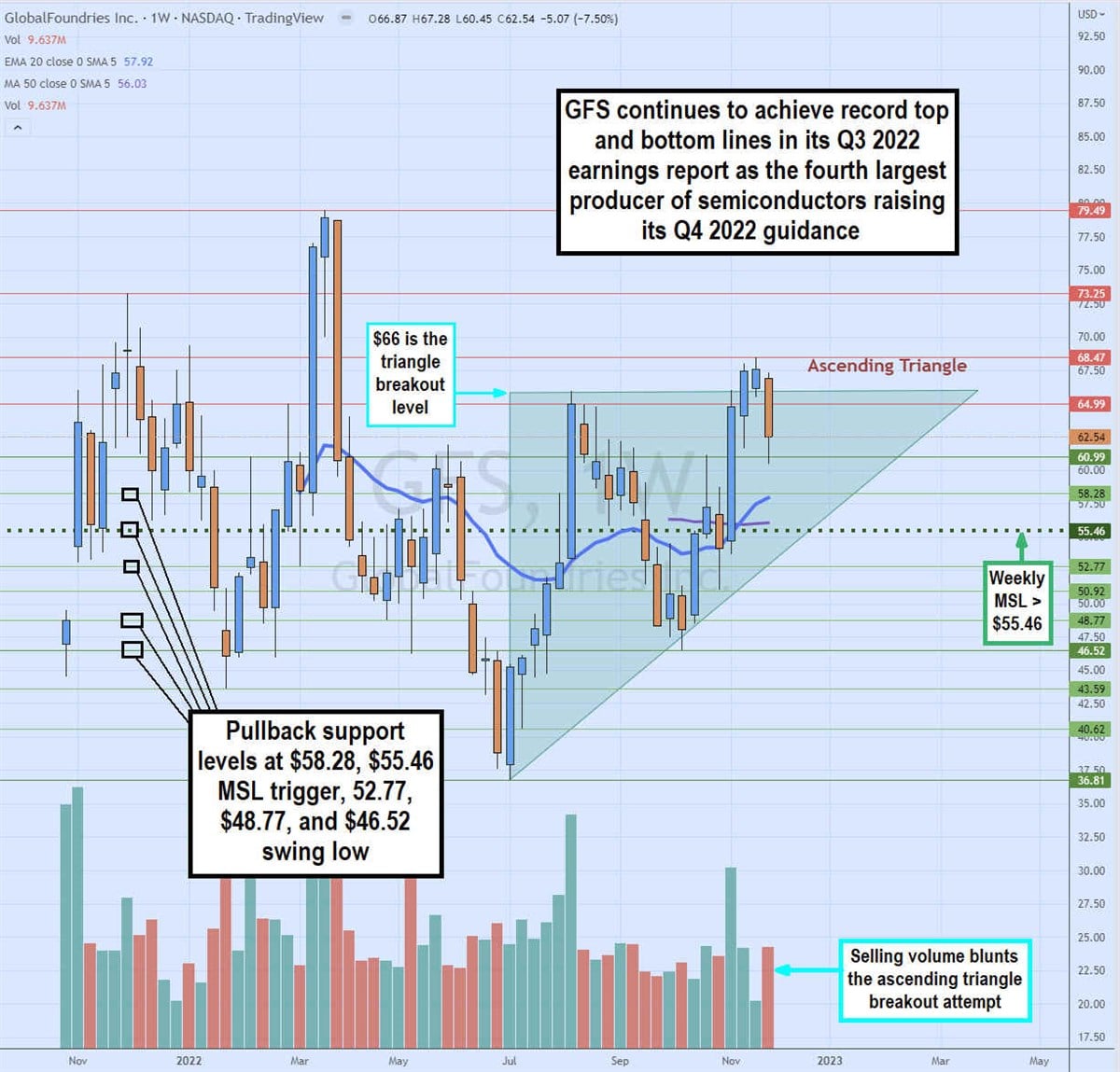

Weekly Ascending Triangle Attempt

The weekly candlestick chart on GFS shows the swing low being made at $36.81 on July 5, 2022. Shares proceeded to surge in the following five consecutive weeks to peak at $65.96 before falling to a recent swing low of $46.52 on Oct. 10, 2022.

Shares triggered the weekly MSL buy signal on the breakout through $55.46 causing the weekly 20-period exponential moving average (EMA) to cross up through the weekly 50-period MA forming a breakout and uptrend with $57.92 and $56.03 as supports, respectively.

The surge on heavy volume was able to break out through the $66 upper trendline resistance on the ascending triangle pattern but peaked out at $68.47 before falling sharply back under the triangle breakout line in the sand at $66. The selling volume doubled the previous buying volume bar as shares dipped back to the $60.99 support level.

Pullback supports sit at the $58.28 weekly 20-period EMA, $55.46 weekly MSL trigger, $52.77, $48.77, and the $46.52 recent swing low level.

Jea Yu

Source link