[ad_1]

Oklo Stock Is Having Its Worst Week Since May 2024. What’s Burdening the Nuclear Start-Up.

[ad_2]

[ad_1]

While the U.S. stock market has been pricing in a “soft-landing” scenario for the economy, a blowout January jobs report, relatively strong corporate earnings, and Federal Reserve Jerome Powell’s comments during the past week could point to the possibility of “no landing,” where the economy is resilient while inflation stays on target.

Such a scenario could still be positive for U.S. stocks, as long as inflation remains steady, according to Richard Flax, chief investment officer at Moneyfarm. However, if inflation reaccelerates, the Fed may be hesitant to cut its policy interest rate much, which could spell trouble, Flax said in a call.

Investors have just gone through the busiest week so far this year for economic data and corporate earnings reports, with stocks ending at or near their record highs.

The Dow Jones Industrial Average

DJIA

finished the week with its nineth record close of 2024, according to Dow Jones Market Data. The S&P 500 index

SPX

scored its seventh record close this year on Friday, while the Nasdaq Composite

COMP

is about 2.7% lower from its peak.

The Fed kept its policy interest rate unchanged in the range of 5.25% to 5.5% at its Wednesday meeting, as expected. However, in the subsequent press conference, Fed Chair Jerome Powell threw cold water on market expectations that the central bank may start cutting its key interest rate in March, and underscored that they want “greater confidence” in disinflation.

Roger Ferguson, former Fed vice chairman, said Powell introduced “a new kind of risk, the risk of no landing.”

In that scenario, inflation will stop falling, while the economy is strong, Ferguson said in an interview with CNBC on Thursday. However, Ferguson said he doesn’t think it is the likely outcome.

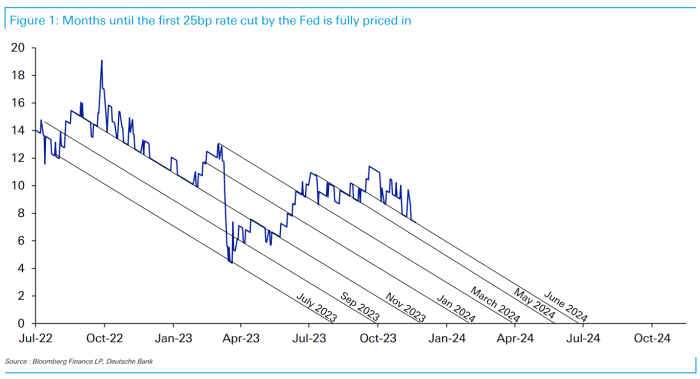

Traders were pricing in a 20.5% likelihood on Friday that the Fed will cut its interest rates in its March meeting, according to the CME FedWatch tool and that’s down from over 46% chance a week ago. The likelihood that the Fed will kick off its rate cutting program in May stood at 58.6% on Friday.

The stronger-than-expected January jobs data released on Friday further eliminates the chance of a rate cut in March, said Flax.

The U.S. economy added a whopping 353,000 new jobs in January while economists polled by The Wall Street Journal had forecast a 185,000 increase in new jobs. Hourly wages rose a sharp 0.6% in January, the biggest increase in almost two years.

The past week has also been heavy with earnings reports, as several tech giants including Microsoft

MSFT,

Apple

AAPL,

Meta

META,

and Amazon

AMZN,

reported their financial results for the fourth quarter of 2023.

Among the 220 S&P 500 companies that have reported their earnings so far, 68% have beaten estimates, with their earnings exceeding the expectation by a median of 7%, analysts at Fundstrat wrote in a Friday note.

While the reported earnings by big tech companies have been “okay,” the guidance was not, said José Torres, senior economist at Interactive Brokers.

What has been driving the tech stocks’ rally since last year was mostly the prospect of sales from artificial intelligence products, but tech companies are not able to monetize the trend yet, Torres said in a phone interview.

Adding to the headwinds is a comeback of concerns around regional banks.

On Thursday, New York Community Bancorp Inc.’s stock triggered the steepest drop in regional-bank stocks since the collapse of Silicon Valley Bank in March 2023. New York Community Bancorp on Wednesday posted a surprise loss and signaled challenges in the commercial real estate sector with troubled loans.

Meanwhile, the Fed’s bank term funding program, which was launched in March last year to bolster the capacity of the banking system, will expire on March 11.

If the Fed could start cutting its key interest rate in March, it would be “sort of like the ambulance that was going to pick regional banks up and save them,” said Torres. “Now the ambulance is coming in May at the earliest, I think that we’re in a particularly risky period from now to May,” Torres said.

Investors should go risk-off before May, according to Torres. “Last year, goods and commodities helped a lot on the disinflationary front. This year for disinflation to continue, we’re going to need services to start contributing to that. Then we’re going to need to see an increase in the unemployment rate,” Torres said.

He said he prefers U.S. Treasurys with a tenor of four years or shorter, as the long-dated ones may be susceptible to risks around the fiscal deficit and government borrowing. For stocks, he prefers the healthcare, utilities, consumer staples and energy sectors, he said.

Keith Buchanan, senior portfolio manager at Globalt Investments, is more optimistic. The slowdown in inflation and the relatively strong economic data and earnings “don’t really paint a picture for a risk-off scenario,” he said. “The setup for risk assets still leans towards the bullish expectation,” Buchanan added.

In the week ahead, investors will be watching the ISM services sector data on Monday, the U.S. trade deficit on Wednesday and weekly initial jobless benefit claims numbers on Thursday. Several Fed officials will speak as well, potentially providing more clues on the possible trajectory of rate cuts.

[ad_2]

Source link

[ad_1]

Investors bought up shares of Etsy Inc. on Thursday after the online crafts marketplace added to its board of directors a partner of hedge fund Elliott Investment Management L.P., which recently acquired a “sizable” stake in the company.

Etsy

ETSY,

said Marc Steinberg, who is responsible for public- and private-equity investments at Elliott, has been appointed to the board, effective Feb. 5, and will also join the board’s audit committee.

“Etsy has a highly differentiated position in the e-commerce landscape and a uniquely attractive business model, supported by a distinctive and engaged community,” Steinberg said. “We became a sizable investor in Etsy and I am joining its board because I believe there is an opportunity for significant value creation.”

Etsy’s stock shot up 8% in afternoon trading, to pare earlier gains of as much as 14.2%. The stock was headed for its best one-day gain since it climbed 9.2% on July 11.

Elliott’s stake was acquired in recent months, as the fund’s disclosure of equity holdings through the third quarter did not list Etsy shares.

“Marc’s appointment reflects our ongoing commitment to enhance the perspectives and expertise on the Etsy Board,” said Etsy Chairman Fred Wilson. “We look forward to benefiting from his voice in the boardroom as a seasoned and experienced investor as we continue our journey of creating a leading global e-commerce platform.”

Etsy now has 10 board members.

Etsy’s stock has run up 18.6% over the past three months, but has tumbled 48.5% over the past 12 months. That’s compared with the S&P 500 index’s

SPX

18.7% rally over the past year.

Read (December 2023): Etsy to cut 11% of staff as CEO says company is on ‘unsustainable trajectory’

At an investor conference in December, Chief Executive Josh Silverman said business has slowed since the post-pandemic boom, as people have “had enough of buying things” and are now spending primarily on eating out and travel. Inflation and the loss of government subsidies was also weighing on spending.

Still, Silverman said, Etsy is now about two and a half times bigger than it was before the pandemic, and the company has more active buyers than it did at the peak of the pandemic.

[ad_2]

Source link

[ad_1]

Oil futures popped higher Sunday evening, after a drone attack that killed three U.S. service members in northern Jordan, blamed by the White House on Iran-backed militants, marked a major escalation of tensions in the Middle East.

West Texas Intermediate crude for March delivery

CL00,

CLH24,

was up $1.09, or 1.4%, at $79.10 a barrel on the New York Mercantile Exchange. March Brent crude

BRN00,

BRNH24,

the global benchmark, gained $1.11, or 1.3%, to trade at $84.66 a barrel on ICE Futures Europe.

Much will ultimately depend on the U.S. response and whether Iran takes action aimed at shutting down the Strait of Hormuz, Tariq Zahir, managing member at Tyche Capital Advisors, told MarketWatch on Sunday afternoon.

“We are on the cusp of this escalating, which could seriously impact the flow of crude oil,” he said.

Three U.S. service members were killed and more than two dozen injured in a drone strike on a U.S. base in northeast Jordan, according to U.S. Central Command. They were the first U.S. fatalities in months of attacks on U.S. bases by Iran-backed militias since the start of the Israel-Hamas war in October.

President Joe Biden attributed the Sunday attack to an Iran-backed militia group and said the U.S. “will hold all those responsible to account at a time and in a manner (of) our choosing.” News reports said U.S. officials were still working to conclusively identify the precise group responsible for the attack, but have assessed that one of several Iranian-backed groups is to blame.

Some congressional Republicans called for direct retaliation on Iran.

“We must respond to these repeated attacks by Iran & its proxies by striking directly against Iranian targets & its leadership. The Biden administration’s responses thus far have only invited more attacks. It is time to act swiftly and decisively for the whole world to see,” wrote Sen. Roger Wicker of Mississippi, the senior Republican on the Senate Armed Services Committee, in a post on X.

Oil futures rallied last week to their highest since November, but with gains attributed in part to production outages in the U.S. and more upbeat expectations around economic growth.

“Crude already has the wind to its back, so this will only offer further upside,” Chris Weston, head of research at Australian brokerage Pepperstone told MarketWatch in an email.

With the U.S. election later this year, “Biden needs to strike a balance between increasing aggression that potentially puts U.S. serviceman lives in danger and could potentially raise the cost of living…while also showing a defiant stance that shows his resolve against terror,” Weston said.

Oil prices have seen short-lived rallies around developments in the Middle East since the start of the Israel-Hamas war, but have failed to build in a lasting geopolitical risk premium. West Texas Intermediate crude

CL00,

CL.1,

the U.S. benchmark, remains around $15 below its 2023 peak in the mid-$90s set in late September. Brent crude

BRN00,

the global benchmark, pushed back above $80 a barrel last week.

Attacks by Iran-backed Houthi militants on Red Sea shipping have forced a rerouting of tankers and cargo ships. For crude, that’s had implications for the physical market but hasn’t interrupted the flow of crude from the Middle East.

A move by Iran aimed at closing off the Strait of Hormuz, the world’s biggest oil-transportation chokepoint, remains a top worry.

The strait is a narrow waterway that links the Persian Gulf with the Gulf of Oman and the Arabian Sea. At its narrowest point, the waterway is only 21 miles wide, and the width of the shipping lane in either direction is just two miles, separated by a two-mile buffer zone.

Around 21 million barrels a day of crude moved through the waterway in the first half of 2023, equivalent to around a fifth of daily global consumption, according to the U.S. Energy Information Administration.

The U.S. stock market has largely looked past Middle East tensions, with the S&P 500

SPX

returning to record territory this month, while the Dow Jones Industrial Average

DJIA

has also set a series of records.

Dow futures

YM00,

were off 94 points, or 0.3% as Asian trading got under way, while S&P 500 futures

ES00,

fell 12 points, or 0.2%, and Nasdaq-100 futures

NQ00,

lost 0.3%.

Read: Stock-market rally faces Fed, tech earnings and jobs data in make-or-break week

Away from oil, there were no signs of a significant surge in demand for instruments that traditionally serve as havens during periods of increased geopolitical tension. Futures on U.S. Treasurys

TY00,

saw a modest rise of 0.2%, while the U.S. dollar

DXY

was little changed versus major rivals and gold futures

GC00,

ticked up 0.4%.

Escalating Middle East tensions won’t go unnoticed by traders, but probably doesn’t warrant a “solid derisking,” Weston said, particularly with investors facing a barrage of major market events in the week ahead.

For U.S.-focused investors, the week ahead features a Federal Reserve policy meeting, earnings from tech industry heavyweights and a crucial December jobs report.

The Middle East situation “won’t take us too far off the rates, growth track, but we have an eye on whether this escalates,” Weston said.

—Associated Press contributed.

[ad_2]

Source link

[ad_1]

As Boeing stock enters its second week of volatile trading following the 737 MAX 9 accident, and it’s still not quite clear whether its shares have been punished enough—or if there is more pain ahead.

[ad_1]

Jan 12, 2024, 1:00 am EST

The Magnificent Seven had an extraordinary year in 2023—one that will be very difficult to repeat. And there will be a new Magnificent Seven in 2024.

Continue reading this article with a Barron’s subscription.

View Options

[ad_1]

U.S. stock indexes were edging higher on Wednesday with technology stocks looking to extend gains ahead of the December inflation report, which is expected to shed more direct light on when the Federal Reserve could dial back its two-year-long effort to tighten monetary policy and cool the economy.

On Tuesday, the Dow industrials fell 0.4%, to 37,525, while the S&P 500 declined 0.2%, to 4,757, and the Nasdaq Composite gained less than 0.1%, to 14,858.

Inflation and its impact on bond markets and the Federal Reserve’s monetary-policy trajectory are the primary focus for markets this week as investors remain on hold ahead of Thursday’s December inflation reading and high-profile corporate earnings reports on Friday, when some of the big banks will kick off the fourth-quarter 2023 earnings season.

The S&P 500 sits less than 0.7% shy of its record high of 4796.6 touched a little over two years ago, after rallying strongly in the last few months primarily on hopes that easing inflation will allow the Fed to lower interest rates sooner and faster than the markets previously anticipated.

The yield on the 10-year Treasury

BX:TMUBMUSD10Y,

the benchmark for borrowing costs, has fallen from 5% in October to 4.014% on Wednesday.

But for this bullish narrative to play out, inflation must be seen continuing to fall back to the central bank’s 2% target. That’s why great importance is therefore being placed on the consumer-price index for December, which will be published at 8:30 a.m. Eastern on Thursday.

See: These traders bet on surprise blip higher in key December inflation reading

Economists forecast that annual headline CPI inflation inched up to 3.2% last month from 3.1% in November. The core reading, which strips out more volatile items like food and energy, is expected to fall from 4% to 3.8%.

Adam Phillips, director of portfolio strategy at EP Wealth Advisors, said the CPI report may give investors enough confidence that the disinflation is likely to continue, even if the price levels are “still a very long way from anything that is considered healthy.”

However, he cautioned that the economy has “certain factors” that are beyond the Fed’s control, such as the volatility in supply chains and growing geopolitical risks, as well as a potential resurgence in inflation, he told MarketWatch via phone on Wednesday.

“[E]quities have remained broadly range-bound since just before Christmas, with little to push them in either direction,” said Jim Reid, strategist at Deutsche Bank.

“That might change soon, since we’ve got the U.S. CPI print tomorrow, and then the start of earnings season on Friday, but for now at least, there’s been few headlines for investors to latch onto, just a bit of indigestion after over exuberance before New Year left markets with a little bit of an extended hangover,” Reid added.

In U.S. economic data, the wholesale inventories declined 0.2% in November, in line with Wall Street expectations, as manufacturers continue to juggle with a fragile economy, according to the Commerce Department.

New York Fed President John Williams will speak in White Plains, N.Y., at 3:15 p.m. Eastern time.

[ad_2]

[ad_1]

Stock investors have gotten off to a wobbly start to the new year, hobbled by shifting expectations on the timing and extent of Federal Reserve interest-rate cuts in 2024.

All three major U.S. stock indexes snapped a nine-week winning streak on Friday, after unexpectedly strong December job gains prompted traders to briefly pull back on the chances of a March rate cut. The S&P 500

SPX

and Nasdaq Composite

COMP

also failed to stage a Santa Claus Rally from the five final trading days of 2023 through the first two sessions of 2024, as questions grew about the market’s multiple rate-cuts view.

It all adds up to a glimpse of what might be in store for investors in the year ahead. Already, the so-called “January effect,” or theory that stocks tend to rise by more now than any other month, could be put to the test by headwinds that include stalling progress on inflation. Inflation’s downward trend in recent months had given traders and investors hope that as many as six or seven quarter-percentage-point rate cuts from the Federal Reserve could be delivered in 2024, starting in March.

Over the first handful of days in the new year, however, reality has started to sink in. For one thing, multiple rate cuts tend to be more commonly associated with recessions and not soft landings for the economy.

Moreover, the idea that the Fed could follow through with as many rate cuts as envisioned by traders would significantly increase the probability that policymakers lose their battle against inflation, according to Mike Sanders, head of fixed income at Wisconsin-based Madison Investments, which manages $23 billion in assets. That’s because six or more rate cuts would loosen financial conditions by too much, and boost the risk of another bout of inflation that forces officials to hike again, he said.

Minutes of the Fed’s Dec. 12-13 meeting show that policymakers were uncertain about their forecasts for rate cuts this year and failed to rule out the possibility of further rate hikes. Nonetheless, fed funds futures traders continued to cling to expectations for a big decline in borrowing costs, with the greatest likelihood now coalescing around five or six quarter-point rate cuts that total 125 or 150 basis points of easing by year-end. That’s roughly twice as much as what policymakers penciled in last month, when they voted to keep interest rates at a 22-year high of 5.25% to 5.5%.

Uncertainty over the path of U.S. interest rates could leave investors flat-footed once again, and damp the optimism that sent all three major stock indexes in 2023 to their best annual performances of the prior two to three years. In November, analysts at Deutsche Bank AG

DB,

counted seven times since 2021 in which markets expected the Fed to make a dovish pivot, only to be wrong.

Financial markets have been operating with “sky-high expectations” for 2024 rate cuts, but the only way to substantiate six cuts this year is with an “abrupt and sharp downturn in the economy,” said Todd Thompson, managing director and portfolio co-manager at Reams Asset Management in Indianapolis, which oversees $27 billion.

Heading into 2024, euphoria over the prospect of lower borrowing costs produced what Thompson calls “an alarming, everything rally,” which he says leaves equities and high-yield corporate debt vulnerable to pullbacks between now and the next six months. Beyond that period, however, “the trend is likely to be lower rates as the economy finally succumbs to tightening conditions at the same time inflation continues to recede.”

The coming week brings the next major U.S. inflation update, with December’s consumer price index report released on Thursday. The annual headline rate of inflation from CPI has slowed to 3.1% in November from a peak of 9.1% in June 2022. In addition, the core rate from the Fed’s favorite inflation gauge, known as the PCE, has eased to 3.2% year-on-year in November from a 4.2% annual rate in July.

The Fed needs to keep interest rates higher because of all the uncertainty around inflation’s most likely path forward, and the U.S. labor market “won’t degrade fast enough in the first quarter to justify a first rate cut in March,” according to Sanders of Madison Investments.

Rate-cut expectations are “going to be the issue for 2024, and a lot of it is going to be revolving around inflation getting back to that 2% target,” Sanders said via phone. “We think somewhere between 75 and 125 basis points of rate cuts make sense, and that the first move is more of a June-type of event. We don’t think it makes sense to have a March rate cut unless the labor market falls off a cliff.”

History shows that Treasury yields tend to fall in the months leading up to the first rate cut of a Fed easing cycle. However, that isn’t happening right now. Yields on government debt have been on an upward trend since the end of December, with 2-

BX:TMUBMUSD02Y,

10-

BX:TMUBMUSD10Y,

and 30-year yields

BX:TMUBMUSD30Y

ending Friday at their highest levels in more than two to three weeks.

See also: What history says about stocks and the bond market ahead of a first Fed rate cut

While financial markets generally tend to be efficient processors of information, they “haven’t been very accurate in terms of pricing in rate cuts” this time, said Lawrence Gillum, the Charlotte, North Carolina-based chief fixed-income strategist for broker-dealer for LPL Financial. He said the big risk for 2024 is if financial conditions ease too much and the Fed declares victory on inflation too soon, which could reignite price pressures in a manner reminiscent of the 1970s period under former Fed Chairman Arthur Burns.

“We think rate-cut expectations have gone too far too fast, and that the backup in yields we are seeing right now is the market acknowledging that maybe rate cuts are not going to be as aggressive as what was priced in,” Gillum said via phone.

December’s CPI report on Thursday is the data highlight of the week ahead.

On Monday, consumer-credit data for November is set to be released, followed the next day by trade-deficit figures for the same month.

Wednesday brings the wholesale-inventories report for November and remarks by New York Fed President John Williams.

Initial weekly jobless claims are released on Thursday. On Friday, the producer price index for December comes out.

[ad_2]

[ad_1]

Shares of Apple Inc. are starting 2024 with a selloff, after Barclays analyst Tim Long said it was “time for a breather,” citing weak hardware sales as iPhone 15 demand disappoints.

“We are still picking up weakness on iPhone volumes and mix, as well as a lack of bounce-back in Macs, iPads and wearables,” Long wrote in a note to clients. “The biggest takeaway from the latest checks is incrementally worse [iPhone] 15 data points out of China, together with developed markets remaining soft.”

He cut his rating on the stock

AAPL,

to underweight from neutral, and trimmed his price target to $160 from $161. The new target implies about 17% downside from Friday’s closing price of $192.53.

The stock slumped 1.8% in premarket trading Tuesday, putting it on track to open at a seven-week low.

Long said iPhone 15 sales have been “lackluster” and believes Phone 16 sales will be the same, as he expects other hardware categories to remain weak. He said it’s time for investors to take a “breather” on the stock, as he doesn’t think it can keep rallying in the face of downbeat demand data, like it did in 2023.

“We expect reversion after a year when most quarters were missed and the stock outperformed,” Long wrote.

He expects Apple to report “in-line” fiscal first-quarter results, which runs through December, but he trimmed his second-quarter to further below consensus expectations.

He now expects earnings per share and revenue for the quarter through March to be down in the low-single-digit percentage range, while the FactSet consensus calls for EPS to be up 2.6% at $1.57 and revenue to rise 1.1% to $95.8 billion.

Apple’s stock surged 48.2% in 2023, or almost double the S&P 500 index’s

SPX

gain of 24.2%, even as revenue for each quarter of fiscal 2023 through September was below that of a year ago.

Long is now one of just four of the 44 analysts surveyed by FactSet who are bearish on Apple’s stock, while 27 (61%) are bullish and 13 are neutral. His $160 price target is 19.2% below the average target of $197.92.

[ad_2]

[ad_1]

U.S. stocks capped off a wild 2023 with a two-month sprint that has carried the Dow to record highs and the S&P 500 index to within a whisker of a similar milestone.

But after such a powerful advance, some portfolio managers and strategists are concerned that the market could suffer its own post-New Year’s Eve hangover once the calendar turns to January 2024.

Instead of providing a tailwind for the market, several who spoke with MarketWatch worried that the “January effect” might work in reverse as investors scramble to lock in gains after the S&P 500 rose 24% in 2023, according to FactSet data.

“Any time you have a big burst like that, I think you’re vulnerable to some profit-taking,” said James St. Aubin, chief investment strategist at Sierra Investment Management, during an interview with MarketWatch. “It wouldn’t surprise anybody to see the market cool off a bit after a strong run.”

From high valuations, to bullish sentiment indicators, to economic data, to geopolitics and beyond, here are a few things that could trip up the market in January.

A technical gauge that’s widely followed by Wall Street portfolio managers and technical analysts has been screaming that U.S. stocks are overbought for a month.

The 14-day relative strength index on the S&P 500, a momentum indicator that’s supposed to help put the magnitude of the index’s latest moves into context, climbed as high as 82.4 on Dec. 19, its highest since 2020, according to FactSet data.

Although the RSI has since pulled back, it continues to hover around 70, seen by analysts as the threshold for when something can be considered “overbought.”

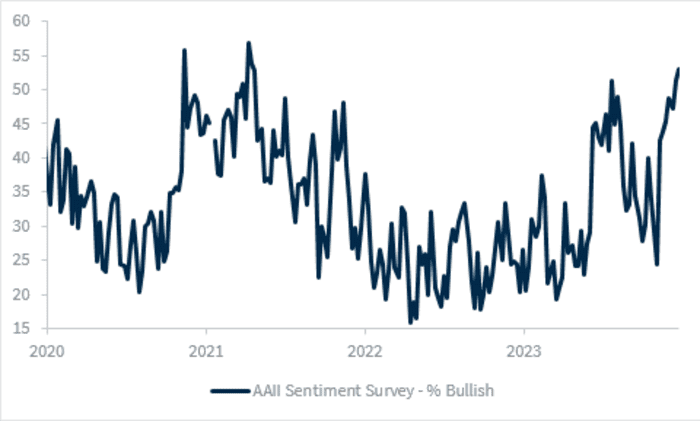

In the span of just two months, investors have gone from incredibly bearish to incredibly bullish, according to the American Association of Individual Investors’ weekly sentiment survey.

That should give investors pause, since the gauge is seen as a reliable counter-indicator. When sentiment becomes stretched in either direction, it can signal that the market is about to turn. Investors say that is what happened back in July, and also in October after the S&P 500 touched its 2022 bear-market nadir.

According to the AAII survey published ahead of the Christmas holiday, nearly 53% of respondents said they were bullish, the highest since April 2021. That number came down a bit this week, but it remains high relative to levels from October.

Wall Street’s favorite “fear gauge” is giving the all-clear. To some, that’s reason enough to worry.

The Cboe Volatility Index

VIX,

better known as the Vix, measures implied volatility, or how volatile traders’ expect the S&P 500 to be over the coming month based on trading activity in options contracts tied to the index.

In December, the Vix dropped below 12 for the first time since before the advent of the COVID-19 pandemic.

Nancy Tengler, CEO and CIO of Laffer Tengler Investments, said in emailed commentary that she is keeping a close eye on the Vix. Once volatility starts to climb, investors should consider taking some chips off the table.

Some investors are already anxious about the next U.S. inflation report, due Jan. 11.

The Cleveland Fed’s inflation nowcast has core CPI rising more than 0.3% in December. If this proves accurate, it would be the hottest inflation reading since May.

And even if core inflation comes in slightly cooler, stocks might not greet it with the same enthusiasm they have shown in the past.

“U.S. CPI for December will hopefully continue to show a disinflationary trend, although the question is: can we keep rallying on this same dynamic?” said Larry Adam, chief investment officer at Raymond James, in emailed comments.

For three straight quarters beginning with the final three months of 2022, the largest U.S. companies saw their earnings shrink on a year-over-year basis.

This “earnings recession” finally came to an end in the third quarter, but the conundrum that investors now face is whether companies can manage to satisfy Wall Street’s lofty expectations for 2024.

The artificial-intelligence software boom and the fact that the U.S. economy avoided a recession in 2023 has helped boost analysts’ confidence about earnings, strategists said.

According to the bottom-up consensus estimate from FactSet, analysts expect S&P 500 aggregate earnings to increase by 11.7% for the calendar year 2024.

“Markets have been baking in this 11.7% earnings growth figure for a while now. That’s a lot of optimism,” Goldman said during an interview with MarketWatch.

To be sure, this list is hardly comprehensive.

Politics and geopolitics also came up a lot in discussions with analysts. Investing professionals cited Taiwan’s upcoming presidential election, another looming federal debt-ceiling showdown in the U.S., the beginning of the 2024 Republican presidential primaries, the ongoing conflicts in Gaza and Ukraine, and more as potential threats to market calm.

Some expressed concern that the Treasury could spark a selloff in bonds and stocks with its next quarterly refunding announcement in early 2024.

But in the view of Cetera’s Goldman, a dynamic that Wall Street traders call it “buy the rumor, sell the news” could represent a bigger threat.

The thinking works like this: investors have already front-run aggressive Federal Reserve interest rate cuts. So, if the Fed delivers, the rush to take profits could drive stocks lower instead of propelling the main U.S. indexes to new highs. Put another way, many strategists believe investors have already priced in pretty aggressive Fed rate cuts.

So unless the central bank finds a way to deliver something even greater than what Wall Street is expecting, the main U.S. equity indexes could struggle to continue their advance.

“Markets are already buying the rumor that we’re going to have a better 2024, that the Fed is going to cut rates, that breadth is going to widen,” Goldman said.

“Maybe we’re already seeing that priced in.”

[ad_2]

[ad_1]

Updated Dec 27, 2023, 7:34 am EST / Original Dec 27, 2023, 4:26 am EST

Stock futures traded slightly lower Wednesday after the S&P 500 finished higher Tuesday and just 0.45% below its record close of 4,796.56 hit Jan. 3, 2022. The broad market index has risen 24% this year and has gained 4.5% this month as traders bet the Federal Reserve will begin cutting interest rates as soon as March.

Continue reading this article with a Barron’s subscription.

[ad_2]

[ad_1]

U.S. stocks closed higher Tuesday, building on a streak of eight straight weekly gains as the final, holiday-shortened week of 2023 got under way.

On Friday, stocks finished a choppy pre-holiday trading session mostly higher, with the S&P 500, Dow and Nasdaq each scoring an eighth straight weekly gain. The S&P 500 finished 0.9% away from its record close of 4,796.56, set on Jan. 3, 2022.

Read:…

Already a subscriber?

Log In

[ad_2]

[ad_1]

Shares of Manchester United Ltd. MANU climbed 4.7% in premarket trades Tuesday after British billionaire Sir Jim Ratcliffe clinched his 25% minority stake in the iconic English soccer club. Manchester United announced the agreement on Christmas Eve, with Ratcliffe acquiring 25% of the Class B shares held by the American Glazer family, which owns the club, and up to 25% of Class A shares. The Glazers and Class A shareholders will receive the same price of $33 a share. The deal values the club at $5.4 billion, falling below initial hopes of $6 billion, according to Bloomberg. Ratcliffe will also provide an additional $300…

Already a subscriber?

Log In

[ad_2]

[ad_1]

2023 will go down in history for the start of a new bull market, albeit a strange one.

Despite some year-end catch-up by the rest of the S&P 500 index, megacap technology stocks, characterized by the so-called Magnificent Seven, have dominated gains for the large-cap benchmark SPX, which is up 23.8% for the year through Friday’s close.

That’s…

Already a subscriber?

Log In

[ad_2]

[ad_1]

Almost as predictable as the big jolly man himself, many on Wall Street are eagerly waiting for the so-called Santa Claus rally to further fuel stock-market gains that have already put investors in a holiday mood.

As defined by the Stock Trader’s Almanac, the Santa Claus rally refers to the stock market’s tendency to rise during the last five trading days of the current calendar year and the first two trading sessions of the new year. Friday marks the start of the period, which will run through Wednesday, January 3 this time around.

If recent history holds, then stocks are set to have a good run in the next six trading days as Santa Claus tends to come to Wall Street almost every year. Since 1950, the Santa rally has boosted the S&P 500

SPX

by an average of 1.3% over the seven trading-day range. The benchmark large-cap index closed higher 78% of the Santa Claus trading window in the past 75 years, and gained during that time for the past seven years, according to Dow Jones Market Data.

This time, though, the stock market has already been in a party mood even ahead of Christmas, with some market watchers, including Yardeni Research’s Ed Yardeni thinking the Santa rally has come “ahead of schedule.”

U.S. stocks are sitting on hefty gains at the close of a rollercoaster year. The S&P 500 jumped 4.3% in December, just 0.7% shy of its record set nearly two years ago amid growing optimism that the Federal Reserve may begin cutting interest rates as early as the first half of 2024, a fervor that policymakers attempted to rein in since last week’s FOMC meeting.

Opinion: Santa Claus is coming to town and bringing presents for your stock portfolio

But a relentless rally in the run-up to the official Santa rally indicates some of Santa’s largesse may have already been delivered, said Pete A. Biebel, senior vice president and senior investment strategist at Benjamin F. Edwards.

“I do think that the market is a little bit extended, so our expectations for this traditional Santa rally period should be dialed back a bit,” Biebel told MarketWatch on Friday.

Biebel points to the midweek dip on Wednesday which made the Dow Jones Industrial Average

DJIA

down 475.92 points, or 1.3%, for its biggest one-day percentage decline since October. The blue-chip index ended a streak of five straight record finishes as a strong year-end rally briefly lost momentum, according to Dow Jones Market Data.

While there wasn’t any clear fundamental trigger for the selloff, some Wall Street analysts think a surge in trading of zero-day to expiry options (0DTE) should be blamed for the pullback. Others said the derivatives that have exploded in popularity this year were just one piece of the puzzle, as overbought technical conditions and low year-end trading volumes also were cited as likely factors.

The “air pocket” for stocks on Wednesday was an omen or a red flag that the markets have that potential for steep drawdowns, Biebel said. “It doesn’t mean it has to happen, but it’s a warning that the market is not as rosy as it seems — there is potential trouble below the surface.”

See: Chasing the Santa rally? Look out below!

However, some analysts suggest investors not to bet against the seasonal momentum, especially during the bull market with a strong uptrend which took the three indexes off their October lows, said Adam Turnquist, chief technical strategist at LPL Financial.

“Stocks are overbought, but the market can stay overbought for longer than most people expect, especially at this stage of a bull market,” Turnquist told MarketWatch via phone.

Meanwhile, stock-market returns during this time frame have historically correlated closely to returns in January and the subsequent year. Since 1950, the S&P 500 has generated an average forward annual return of 10.4% when Santa comes to town. That is well above the return when Santa doesn’t show up, which is only around 4%, according to data compiled by LPL Financial.

“There’s the potential [for a Santa rally] but we’ll likely see a little bit of a hangover as well as a reset in January or February from these overbought conditions,” he added.

Time will tell if investors receive the seasonal presents that history promises in 2023, or if an overly extended rally will let the Grinch steal Christmas. After all, Santa rally is more of a “curiosity” than a phenomenon, said Biebel.

U.S. stocks were edging higher on Friday, with three major indexes on pace for their eighth consecutive positive week. The Dow Jones Industrial Average has risen 0.4%, while the S&P 500 was up 0.9% and the Nasdaq Composite

COMP

has jumped 1.3% this week, according to FactSet data.

[ad_2]

[ad_1]

Speculation that the 60-40 portfolio may have outlived its usefulness has been rife on Wall Street after two years of lackluster performance.

But as the yield on the 10-year Treasury note

BX:TMUBMUSD10Y

hovers around 4%, some strategists say the case for allocating a healthy portion of one’s portfolio to bonds hasn’t been this compelling in a long time.

And with the Federal Reserve penciling three interest-rate cuts next year, investors who seize the opportunity to buy more bonds at current levels could reap rewards for years to come, as waning inflation helps to normalize the relationship between stocks and bonds, restoring bonds’ status as a helpful portfolio hedge during tumultuous times, market strategists and portfolio managers told MarketWatch.

Add to this is the notion that equity valuations are looking stretched after a stock-market rebound that took many on Wall Street by surprise, and the case for diversification grows even stronger, according to Michael Lebowitz, a portfolio manager at RIA Advisors, who told MarketWatch he has recently increased his allocation to bonds.

“The biggest difference between 2024 and years past is you can earn 4% on a Treasury bond, which isn’t that far off from the projected return in U.S. stocks right now,” Lebowitz said. “We’re adding bonds to our portfolio because we think yields are going to continue to come down over the next three to six months.”

Since modern portfolio theory was first developed in the early 1950s, the 60-40 portfolio has been a staple of financial advisers’ advice to their clients.

The notion that investors should favor diversified portfolios of stocks and bonds is based on a simple principle: bonds’ steady cash flows and tendency to appreciate when stocks are sliding makes them a useful offset for short-term losses in an equity portfolio, helping to mitigate the risks for investors saving for retirement.

However, market performance since the financial crisis has slowly undermined this notion. The bond-buying programs launched by the Fed and other central banks following the 2008 financial crisis caused bond prices to appreciate, while driving yields to rock-bottom levels, muting total returns relative to stocks.

At the same time, the flood of easy money helped drive a decadelong equity bull market that began in 2009 and didn’t end until the advent of COVID-19 in early 2020, FactSet data show.

More recently, bonds failed to offset losses in stocks in 2022. And in 2023, U.S. equity benchmarks such as the S&P 500

SPX

have still outperformed U.S. bond-market benchmarks, despite bonds offering their most attractive yields in years, according to Dow Jones Market Data.

The Bloomberg U.S. Aggregate Total Return Index

AGG

has returned 4.6% year-to-date, according to Dow Jones data, compared with a more than 25% return for the S&P 500 when dividends are included.

But this could be about to change, according to analysts at Deutsche Bank. The team found that, going back decades, the relationship between stocks and bonds has tended to normalize once inflation has slowed to an annual rate of 3% based on the CPI Index.

The CPI Index for November had core inflation running at 4% year over year, a level it has been stuck at for the past several months. The Fed’s projections have inflation continuing to wane in 2024.

Staff economists at the central bank expect the core PCE Price Index, which the Fed prefers to the CPI gauge, to slow to 2.4% by the end of next year. If that comes to pass, investors should see the inverse relationship between stocks and bonds return, according to Lebowitz and others.

The dismal performance of 60-40 portfolios over the past two years has inspired a wave of Wall Street think pieces questioning whether it still makes sense for contemporary investors.

A team of academics led by Aizhan Anarkulova at Emory University in November presented findings showing that over a lifetime, investors would have reaped higher returns via a portfolio consisting of 100% exposure to stocks, split between foreign and domestic markets.

But fixed-income strategists at Deutsche and Goldman Sachs Group, as well as others on Wall Street, say investors wouldn’t be well-served by excluding bonds from their portfolio, particularly with yields at current levels.

Rob Haworth, senior investment strategy director at U.S. Bank’s wealth-management business, says investors now have an opportunity to lock in attractive returns for decades to come, ensuring that the bonds in their portfolios will, at the very least, deliver a steady stream of income that would reduce any losses in stocks or declines in bond prices.

There is, however, one catch: with the Fed expected to cut interest rates, that window could quickly close.

“The problem is, for investors in cash, the Fed’s just told you that is not going to last. I think that means it is time to start thinking about your long-term plan,” Haworth said.

Read: Fed could be the Grinch who ‘stole’ cash earning 5%. What a Powell pivot means for investors.

[ad_2]

[ad_1]

U.S. stock indexes were higher on Wednesday as Wall Street tried to build on their year-end rally with a fresh record in sight for the S&P 500 index.

On Tuesday, the Dow booked a fifth straight record close, while the S&P 500 rose and the Nasdaq extended its winning streak to a ninth day.

U.S. stocks were edging higher on Wednesday with the S&P 500 less than 1% shy of the all-time closing high of 4796.56 it recorded at the start of January 2022, while the Dow industrials and Nasdaq were struggling to extend their nine consecutive daily gains.

The Wall Street large-cap benchmark S&P 500 has jumped 24.3% this year, partially powered by hopes that the U.S. economy has not been too badly damaged by the Federal Reserve’s ratcheting up of interest rates to cool inflation.

The latest leg of the rally reflects hopes that with inflation back down to 3.1%, the central bank will begin quickly trimming borrowing costs next year. Not even an concerted effort by Fed officials to counter the market’s rate-cut optimism has damped trader’s ardor.

This dismissal of less-dovish Fedspeak has left some observers bemused.

“Investors are dreaming of aggressive rate cuts in an environment of strong economic growth, and that is not the right recipe for easing inflation and keeping it sufficiently low,” Ipek Ozkardeskaya, senior analyst at Swissquote Bank. “The robust economic data and high earnings expectations are not compatible with a dovish Fed,” she said.

See: Why the 60-40 portfolio is poised to make a comeback in 2024

Perhaps the current bullishness is also reflective of seasonal trends, with optimism about a festive bounce underpinning stocks. The “Santa Claus Rally” period stretches from the last five trading days of the year and first two trading days of the new year, according to the Stock Trader’s Almanac.

Since 1950, the S&P 500 has averaged a gain of 1.32% and closed higher 78.1% of the time over that period, according to Dow Jones Market Data.

In U.S. economic data, existing-home sales rose 0.8% in November to 3.82 million, the National Association of Realtors said on Wednesday. Sales of previously owned homes unexpectedly inched up last month, snapping a five-month slump as easing mortgage rates encouraged some U.S. homebuyers.

Meanwhile, U.S. consumer confidence index rose to 110 in December, up from a downwardly revised 101 in the previous month, the Conference Board said Wednesday.

“The consumer is feeling pretty well as rates move lower, employers add to their payroll, and income expectations improve,” said Jeffrey J. Roach, chief economist at LPL Financial. “So far, investors have a green light as they merge into the new year.”

That said, investors will continue seeking guidance from more economic data due later this week that may provide more clarity on the Fed’s interest-rate path in 2024. A revision of third-quarter GDP print is expected on Thursday morning, followed by Friday’s personal consumption expenditure (PCE) inflation report — the Fed’s preferred inflation gauge.

[ad_2]

[ad_1]

Dec 19, 2023, 4:31 am EST

Stock futures traded flat Tuesday, a day after the S&P 500 finished up 0.5% and moved closer to its all-time. The broad market index stands just 1.2% below its record of 4,796.56 reached in early January 2022.

Continue reading this article with a Barron’s subscription.

[ad_2]

[ad_1]

Wall Street seems to agree that U.S. stocks will climb to fresh record highs in 2024. But the most important question for investors may still be the direction and speed of interest-rate moves.

Rate-sensitive groups of stocks with lackluster fundamentals, such as financials, utilities, staples, “may be able to outperform, at least early in the year,” if one expects interest rates “to come down quickly and permanently,” said Nicholas Colas, co-founder of DataTrek Research.

But if “one expects a bumpier ride on the rate front,” then stronger groups, like technology and tech-adjacent sectors “should do better,” Colas said in a Monday client note.

The S&P 500’s utilities, consumer staples and energy sectors have been the worst performing parts of the large-cap benchmark index so far in 2023, according to FactSet data.

With an over 10% year-to-date decline, the S&P 500’s utilities sector

XX:SP500.55

has significantly underperformed the broader index’s

SPX

23.6% advance.

The S&P 500’s best performing information technology sector

XX:SP500.45

was up 56.5% for the same period. But its consumer staples

XX:SP500.30

and energy

XX:SP500.10

sectors have slumped by 2.6% and 4.1% so far this year, respectively, according to FactSet data.

Utilities and consumer staples are usually considered defensive investment sectors, or “bond proxies,” because they can help investors minimize stock-market losses in any economic downturn. Companies in these sectors usually provide electricity, water and gas, or they sell products and services that consumers regularly purchase, regardless of economic conditions.

However, utilities and consumer staples stocks were under a lot of pressure this year. A relentless climb in U.S. Treasury yields in October made defensive stocks less attractive compared with government-issued bonds, or money-market funds offering 5%, especially as the economy remained strong, pushing recession expectations out further.

Colas expects “weaker groups” to catch a stronger tailwind if rates continue to decline.

See: Markets are declaring victory over inflation for Powell, and that has some economists worried

The yield on the 10-year Treasury

BX:TMUBMUSD10Y

last week booked its biggest weekly decline in a year after the Federal Reserve signaled a pivot to rate cuts in 2024, which helped the S&P 500 score its longest weekly winning streak since 2017.

The S&P 500’s utilities and consumer staples sectors rose 0.9% and 1.6% last week, respectively, compared with the information technology sector’s 2.5% advance and communication services sector’s

XX:SP500.50

0.1% decline, according to FactSet data.

Earnings growth expectations for each S&P 500 sector in 2024 are indicated below. Sectors to the left of the dotted black line are expected to show better bottom-line results than the S&P 500 as a whole, while those to the right are expected to show weaker earnings growth.

Wall Street expects next year to see 11.5% growth in S&P 500 earnings-per-share (EPS), to $244, and 5.5% revenue growth, according to FactSet data.

However, there is a wide dispersion across S&P 500 sectors. The range goes from 2% revenue and 3% earnings growth for the energy sector, to 9% revenue and 17% earnings growth for the information technology sector, according to data compiled by DataTrek Research.

“Playing fundamentally weaker sectors therefore assumes even more good news on the rate front,” Colas said, adding that it still is riskier than sticking with “tried and true groups” like technology.

Moreover, sectors such as utilities, financials and consumer staples are not expected to show 10% earnings growth next year, while health care and big tech-dominated groups like communication services, technology and consumer discretionary, are expected to show much better than average revenue and earnings growth in 2024, said Colas, citing FactSet data.

U.S. stocks closed higher on Monday, with the Dow Jones Industrial Average

DJIA

building on its all-time high set last week. The S&P 500 gained 0.5% and the Dow Industrials closed fractionally higher. The Nasdaq Composite

COMP

finished up 0.6%, according to FactSet data.

[ad_2]