Former President Donald Trump entered pleas of not guilty Thursday at an arraignment in Washington, D.C., giving his formal response to his four-count indictment over his efforts to overturn the 2020 presidential election, including his role in the Jan. 6, 2021, attack on the U.S. Capitol.

Trump, the frontrunner in polls for the 2024 Republican presidential nomination, has denied wrongdoing, and earlier Thursday he continued to criticize the legal proceedings as largely about helping President Joe Biden, a Democrat, in next year’s election.

“The Dems don’t want to run against me or they would not be doing this unprecedented weaponization of ‘Justice.’ BUT SOON, IN 2024, IT WILL BE OUR TURN,” Trump said in a post on his Truth Social platform.

In Tuesday’s 45-page indictment, Trump was hit with charges that included conspiracy to defraud the U.S. and conspiracy to obstruct an official proceeding.

The former president’s appearance in Washington is just one step in a legal battle that will likely take months or even years to play out.

Special counsel Jack Smith on Tuesday said his office “will seek a speedy trial” in the Jan. 6 case, but Trump defense attorney John Lauro has pushed back repeatedly on Smith’s statement, telling NPR on Wednesday that his side wants “a just trial, not simply a speedy trial,” and that the trial itself “could last six months or nine months or even a year.”

Trump’s legal team looks likely to make change-of-venue requests, with the former president talking up West Virginia in a Truth Social post late Wednesday. He said the Jan. 6 case “will hopefully be moved to an impartial Venue, such as the politically unbiased nearby State of West Virginia! IMPOSSIBLE to get a fair trial in Washington, D.C., which is over 95% anti-Trump.”

The next hearing in the case was reportedly scheduled for Aug. 28, which would be five days after the first GOP presidential primary debate.

Biden told CNN Thursday that he was not planning to follow Trump’s arraignment, responding with an emphatic “no” when asked about it during a bike ride in Rehoboth Beach, Del., where he is vacationing this week.

The second-quarter earnings season so far is showing that one trend that featured in the first quarter has not gone away.

“Greedflation,” or the practice of companies raising prices to protect their profit margins, is alive and well, based on the number of companies that have so far acknowledged raising prices yet again, even as inflation readings have come down and as some acknowledge that their input costs are falling.

At the same time, companies continue to emphasize on earnings calls that their customers are showing signs they are weary of higher prices and are shopping more frequently at more stores, while spending less per trip.

“Across industries, we’ve seen the same story over and over the last two years,” said Liz Zelnick, director of economic security and corporate power at Accountable.US, a liberal-leaning consumer-advocacy group.

“CEOs claim outside forces made them gouge consumers, then turn around and give themselves raises and boast of record profits and billions in new investor handouts,” she said, referring to the billions of stock buybacks and dividend payouts the same companies have made.

On a call with analysts, Chief Executive Jon Moeller signaled more price increases to come, which he attributed to the company’s innovation pipeline, which is creating must-have products.

“If you look back historically, pricing has been a positive contributor to our top-line growth for something like 48 out of the 51 last quarters and again as we strengthen our innovation program even further, that will provide opportunities to continue to benefit from modest pricing,” said Moeller, according to a FactSet transcript.

The company blew past earnings estimates with adjusted per-share earnings of $1.37, ahead of the $1.32 FactSet consensus, and sales of $20.6 billion, versus the $20 billion FactSet consensus.

Gross margin increased 380 basis points from a year ago, driven by 340 basis points of pricing benefit and 290 basis points of productivity savings.

Coca-Cola Co. KO, -0.49%

also swept past estimates and raised guidance after the drinks and snacks giant increased prices by 10%. The company’s adjusted operating margin rose to 31.6% from 30.6% a year ago.

Conagra Brands Inc. CAG, -0.75%

raised prices by up to 17%, which Chief Executive Sean Connolly described as “inflation-justified.” The parent of brands such as Birds Eye, Duncan Hines, Hunt’s, Orville Redenbacher’s and Slim Jim also reported that its customers are buying less food to stretch their budgets.

“[W]hile we did lose share in the quarter, as price gaps have stayed wider for longer than we would have liked, we are managing the business for the long term and still generated mid-single-digit top-line growth within the range of what we expected,” Chief Executive Miguel Patricio said.

The company, parent to brands including Kraft Mac and Cheese, Heinz Ketchup, Jell-O and Lunchables, indicated on the post-earnings conference call with analysts that rather than increasing discounting, or just cutting prices, it will remain focused on protecting margins, which has been allowing it to accelerate investment in the business, particularly in marketing, research and development and technology.

Besides, as Chief Financial Officer Andre Maciel said, the gaps between Kraft’s prices and those of competitors are not getting worse. “If anything, they are slightly getting better,” Maciel said, according to an AlphaSense transcript.

Considering the market-share losses and with inflation coming down, “do you think you took too much price, given you said you took price ahead of competitors, and they have not followed?” UBS analyst Cody Ross asked on the conference call.

CEO Miguel Patricio’s answer was simple: “No.”

“I mean, we had very high inflation. And we are leaders in the vast majority of categories where we play. And it’s our role as leader to try to compensate … this inflation with price increases,” Patricio said. “So I would do everything again. I mean we can always go back on price if we think we have to or when we have to. But we had to lead price increases.”

All of that leaves families to foot the bill for higher food prices, said Accountable.US’s Zelnick.

The Consumer Staples Select Sector SPDR exchange-traded fund XLP

has gained 1.2% in the year to date, while the SPDR S&P Retail ETF XRT

has gained 10.3%. The S&P 500 XRT

has gained 17%.

Once is an accident, twice is a coincidence and three times is a conspiracy.

Former President Donald Trump is accused by federal prosecutors of engaging in three major conspiracies ahead of the Jan. 6, 2021, Capitol riot to subvert the process of counting and certifying the vote before Congress in his bid to hold on to power despite having lost the 2020 election.

While spreading lies about how votes had been illegally cast, tampered with or miscounted in order to build mistrust among the public about the election’s outcome, special counsel Jack Smith says Trump and a group of six unnamed lawyers and advisers plotted to illegally meddle with the very basis of how presidential elections have been run in the U.S since its founding.

A four-count indictment unsealed in federal court in Washington on Tuesday alleges that the group worked unrelentingly to tamper with how several states counted their ballots and the process by which states sent electors to Washington to finalize their vote. The indictment also accused Trump of pressuring the Justice Department and Vice President Mike Pence to intervene even though they had no standing to do so.

“Each of theses conspiracies — which built upon the widespread mistrust the defendant was creating through pervasive and destabilizing about election fraud — targeted a bedrock function of the United States federal government: the nation’s process of collecting, counting, and certifying the results of the presidential election,” the indictment read.

Trump has dismissed the charges as being purely politicized.

“The lawlessness of these persecutions of President Trump and his supporters is reminiscent of Nazi Germany in the 1930s, the former Soviet Union, and other authoritarian, dictatorial regimes,” a statement released by his campaign read. “President Trump has always followed the law and the constitution, with advice from many highly accomplished attorneys.”

The charges allege three acts of conspiracy and one of obstructing an official proceeding. Here are the main legal arguments Smith makes against the former president:

‘We have lots of theories’

Prosecutors say that starting almost immediately after the election on Nov. 3, 2020, Trump began a campaign to get officials in key states like Arizona, Nevada, New Mexico, Pennsylvania, Michigan, Wisconsin and Georgia to overturn the election results.

Trump pressured state officials to throw the vote out based on allegations ranging from dead people voting to non-citizens casting ballots, and from voting machines being tampered to ballot-box stuffing, despite there being no evidence any of it had occurred.

“We don’t have evidence, but we have lots of theories,” one of Trump’s co-conspirators allegedly told the speaker of the house of Arizona, a Trump-backer, when asked what proof they had about electoral malfeasance.

When officials in the states refused to go along with Trump’s request to decertify the results, the president continued to publicly trumpet false claims about voter fraud and attack local officials as “terrible people” who were in on the fraud, the indictment said.

Smith said that Trump continued to make the claims despite having been told repeatedly by numerous people in multiple agencies — many of them his own supporters — that there was no truth to it and having lost case after case in court.

“When our research and campaign team can’t back up any of the claims made by our Elite Strike Force Legal Team, you can see why we’re 0-32 on our cases,” one senior campaign advisor said, according to the indictment. “It’s tough to own any of this when it’s all just conspiracy s*** beamed down from the mothership.”

Smith argues that this effort amounted to using deceit to subvert the election’s result, which is against the law.

Phony electors

One key component of the conspiracy case against Trump revolves around efforts to create a competing slate of electors from each challenged state.

As part of the presidential electoral process, every state sends electors to Washington to deliver the vote to congress. It’s a mostly ceremonial procedure, but Trump’s legal team is accused of hatching a plot to send a second group of electors who backed Trump from several states in order to create confusion in Congress and force legislators in Washington to have to debate the election’s outcome.

No matter that the second slate of electors hadn’t been approved by officials in the states they purported to represent and were not authorized in any way, the indictment says. The effort was so patently bogus that Trump’s team even referred to the group as “phony electors” in their own correspondence, the indictment stated.

In the indictment, Smith said the effort amounted to a conspiracy to commit fraud.

‘You’re too honest’

A third leg of the conspiracy allegedly involved pressuring officials at the Justice Department and Pence to intervene in the election even though they had no standing to do so.

The indictment says Trump and his co-conspirators repeatedly communicated with then acting attorney general Jeffrey Rosen and insisted that he declare ahead of the Jan. 6 certification of the election by Congress that there had been evidence of fraud.

When Rosen said he would not do that because there was no such evidence, Trump allegedly threatened to replace him with one of the unnamed co-conspirators included in the indictment.

At one point, a deputy White House counsel told the co-conspirator that “there is no world, there is no option in which you do not leave the White House,” and warned that there would be “riots in the streets” if Trump attempted to remain in office, to which the co-conspirator allegedly said: “That’s why there is an Insurrection Act.”

For weeks ahead of the Jan. 6 certification hearing in Congress, Trump and his cohorts pressured Pence to refuse to certify the vote tally, a purely ceremonial task the vice president has presided over since the country’s founding.

Pence steadfastly refused to do so, saying his legal team had told him there was no constitutional basis for the vice president to be able to overturn an election at the last minute. In a phone call less than a week before Jan. 6, Trump allegedly berated Pence and told him, “You’re too honest.”

When a senior White House advisor told one of the unnamed co-conspirators that if Pence tried to overturn the election it would lead to violence in the streets, the co-conspirator allegedly said that there had been times in the country’s history where violence was necessary to protect the Republic, the indictment said.

In the days and hours leading up to the Jan. 6 riot, Trump posted several messages on Twitter stating that Pence had the authority to overturn the election and continuing to pressure him to do so.

Exploiting the chaos

On Jan. 6, after Pence issued a statement saying he did not have the authority to not certify the vote, protests outside Congress turned violent, with hundreds of rioters clashing with police and storming the building, delaying the proceedings.

During the standoff, some of Trump’s co-conspirators tried to reach members of Congress and the Senate to convince them to further delay the certifying process in order to buy Trump more time to convince state legislatures to nullify the already-approved votes, the indictment says.

Later that afternoon, Trump tweeted: “See, this is what happens when they try to steal an election. These people are angry. These people are really angry about it. This is what happens.”

Former President Donald Trump on Tuesday was indicted by a grand jury in Washington, D.C., in connection with the Justice Department’s probe into efforts to overturn the 2020 presidential election, including the Jan. 6, 2021, attack on the U.S. Capitol.

Special counsel Jack Smith has been examining Trump’s actions leading up to the Jan. 6 attack. On that day, a mob of Trump supporters stormed the Capitol building in an attempt to disrupt the congressional certification of the election results.

In Tuesday’s 45-page indictment, Trump was hit with four charges: conspiracy to defraud the U.S., conspiracy to obstruct an official proceeding, obstruction of and attempt to obstruct an official proceeding and conspiracy against rights.

“The attack on our nation’s capitol on Jan. 6, 2021, was an unprecedented assault on the seat of American democracy,” Smith said at a news conference.

“As described in the indictment, it was fueled by lies — lies by the defendant targeted at obstructing a bedrock function of the U.S. government, the nation’s process of collecting, counting and certifying the results of the presidential election.”

Trump is expected to be arraigned on Thursday in Washington.

“In this case, my office will seek a speedy trial so that our evidence can be tested in court and judged by a jury of citizens,” Smith also said.

The indictment said Trump had six co-conspirators, and it indicated that four of the individuals were attorneys, one was a political consultant and another was a Justice Department official.

Trump has denied wrongdoing and is the overwhelming favorite in polls for the GOP nomination for the 2024 presidential race, far ahead in a crowded field that includes Florida Gov. Ron DeSantis, former Vice President Mike Pence, former New Jersey Gov. Chris Christie and entrepreneur Vivek Ramaswamy. The former president on July 18 said he’d gotten a letter informing him he is a target of that probe. He said he anticipated being indicted.

The indictment ratchets up legal pressure for Trump as he seeks the 2024 GOP nomination and aims to challenge Democratic President Joe Biden. The former president is already facing federal charges in Florida that he mishandled classified documents after leaving the White House, and criminal charges in New York over a hush-money case. A separate election-interference investigation is underway in Georgia.

“This is nothing more than the latest corrupt chapter in the continued pathetic attempt by the Biden crime family and their weaponized Department of Justice to interfere with the 2024 presidential election, in which President Trump is the undisputed frontrunner, and leading by substantial margins,” said Trump’s 2024 campaign in a statement.

“The lawlessness of these persecutions of President Trump and his supporters is reminiscent of Nazi Germany in the 1930s, the former Soviet Union, and other authoritarian, dictatorial regimes,” the statement also said.

In addition, Trump’s campaign made an effort to raise money off the latest indictment, sending an email from the 45th president that asked supporters to “make a contribution to show that you will NEVER SURRENDER our country to tyranny as the Deep State thugs try to JAIL me for life.”

Trump’s former vice president, Mike Pence, who’s also seeking the GOP presidential nomination, said in a statement late Tuesday: “Today’s indictment serves as an important reminder: anyone who puts himself over the Constitution should never be president of the United States,” adding he will have more to day after reviewing the indictment.

An indictment does not disqualify Trump from mounting a White House campaign. The only requirements to run for president, as laid out in the Constitution, are being a natural-born citizen at least 35 years old and a resident of the U.S. for 14 years.

I’ve read your previous responses to letters on tipping, and my thoughts are simple: Tipping is dependent on the service given. I won’t tip at a deli counter, but I will tip more in a diner. I see no reason to tip a deli counter person on a regular basis. The person who rings up my groceries isn’t allowed to accept tips, and they do a lot more than put a sandwich in a bag.

As far as restaurants go, 15% is the starting point and I will go up from that as warranted. I do tend to tip a high percentage in diners. The waitstaff there are generally fabulous, deal with lower price points and a varied clientele. I feel they also suffer from customer bias where some people seem to think it’s only a diner not a fancy restaurant.

“‘Helping others is not always through money. I volunteer my time with several charities and donate blood.’”

The job is the same whether my meal is $10 or $100. I try to pay in cash to ensure the waitstaff is promptly getting their tip, and to ensure that the money does indeed go to the wait staff. Are we expected to tip on a total that includes credit-card charges? What’s more, helping others is not always through money. I volunteer my time with several charities and donate blood.

What troubles me is that throughout the New York City metro area, tipping recommendations in restaurants are based on faulty calculations. My friends and I all agree that tips are supposed to be based on the price of the meal — that is the subtotal or pre-tax figure. Restaurants frequently encourage people to tip on the final amount.

Yes, wait staff in diners work as hard as any restaurant worker, and they deserve whatever your optimum tip — 15% or 20% — and as much as you would tip in a white-tablecloth restaurant. Yes, consumers should not be expected to tip in a deli — unless you have a good relationship with the staff, and you tip occasionally for goodwill. If you choose to “skip” the charity donation in a pharmacy, that’s OK too. Yes, donations and tips are increasingly being conflated, and that’s not always a good thing. We should be comfortable with the charity and 100% sure that the donation is going to the charity in question.

And your main point: Yes, tipping on the subtotal before tax and before credit-card charges is absolutely fair, although a lot of people — especially when calculating the tip among friends — tip on the after-tax total. Why? Perhaps we don’t want to be seen splitting hairs over the tax among friends and/or in front of a service worker who has given us exemplary service. Calculating tips is often done under pressure, and no one likes to be seen as a cheapskate. I almost always tip on the total amount, knowing that the sales tax is included, primarily because I figure that extra $1 or more is going to the person who served my table.

My colleague, MarketWatch news editor Nicole Pesce, put together a guide for how much you should tip everyone, and who you should NOT tip. She also cited three reasons why tipping has become such a note of contention, and why it appears we are tipping more: people tipped staff more during the pandemic (they were, after all, putting their health and lives at risk with their jobs); 40-year high inflation over the last 12 months has increased the cost of everything and, as such our tips rose in tandem with prices; and, finally, digital tipping appears to be ubiquitous, and people have been suffering from tipping fatigue.

“‘You’re not the only one: Americans are souring on tipping.’”

You’re not the only one with tipping fatigue, though: Americans are generally souring on tipping. A large majority (66%) of U.S. adults have a negative view about tipping, according to a poll released by the personal-finance site Bankrate last month. The bottom line: consumers feel they are being forced to compensate employees for low pay (41%) and they don’t appreciate all that digital guilt tipping (32%) and, as a result, they believe that tipping culture has gotten out of control (30%). Respondents also said they were confused about how much to tip (15%), but a small minority (a paltry 16%) said they would be willing to pay higher prices in lieu of tipping.

People appear to be less generous with their tipping amounts, and they also appear to be tipping less often. What’s perhaps most surprising from Bankrate’s research is that only 65% of diners actually tip when they eat out (that’s down from 73% last year). After restaurants, people are most likely to tip barbers/hairdressers (53% of those polled) and food-delivery workers (50%). From thereon, only a minority of people say they tip taxi or rideshare drivers (New York City cabs, which give tipping options upon payment, may be an outlier here), hotel housekeepers, baristas and food-delivery workers.

It’s important that we have this conversation about tipping because expectations and digital tipping methods are evolving all the time. On the one hand, people are facing higher prices and they are understandably feeling under pressure to tip. On the other hand, this conversation naturally overlaps with the working conditions and pay of service workers. Americans are tipping less than they did during the worst days of the pandemic. Service workers — along with medical personnel, bus and train drivers and first responders — were among the heroes of the pandemic. That is something I hope we never forget.

“The person who rings up my groceries isn’t allowed to accept tips, and they do a lot more than put a sandwich in a bag,” the letter writer says.

I went for dinner with six friends last weekend, and we each ordered entrees and desserts, and some side orders. One of our group only eats gluten-free food, so he ordered two starters. We split the bill, and it worked out at $36 each. But our gluten-free friend cried foul, and asked for a separate check to pay $22 for his gluten-free dish. I was outraged — and almost felt physically sick. I kicked my husband under the table, and said under my breath, “Can you believe that?’

Can you believe it? Do you think he should have just paid the $35 instead of asking for a separate check? Adding insult to injury, he left the waiter a $10 tip. Why not just pay $35 like everyone else? I told my husband I was never going for dinner with him again. Don’t you think he should have just paid $35 like everyone else? It was a big crowd. If everyone did that, you’d need a forensic accountant to figure out how many breadsticks someone ate.

We otherwise had a nice evening, and it was a bring-your-own-bottle restaurant. I work as a teacher and my husband works in tech. We own a home together and have three kids. Our gluten-free friend is a freelance consultant, and is divorced with two kids. He had a very privileged upbringing. I worked hard for everything I have. I’m not saying any of us are rich, but when we go out to eat, we like to share and share alike, and split the bill down the middle.

When did eating out become so full of these cringeworthy moments?

Equal Bill Splitter

Dear Equal,

I’m sorry to say that the most cringeworthy moment here happened when you kicked your husband under the table. I’m not a big fan of under-table communication in a group, and while we could debate the pros and cons of asking for a separate check for a $13 difference, I don’t think there’s much of a gray area when it comes to calling someone out at the dinner table, especially when your eye-rolling and disapproval could be picked up by the other guests.

As far as your friend is concerned, $13 is a lot of money to pay when you did not eat all the food that was ordered by the table. Maybe it doesn’t seem like it to you or anyone reading this column, but your friend is divorced with two kids, and works as a freelancer — so let’s assume his income is not always stable. Could he have just split it down the middle and paid $35 and another 15% or 20% for a tip? Sure. But he has good financial boundaries. I applaud him.

The real issue here may go back to your respective upbringings, and could explain your dramatic — and I would argue disproportionate reaction — to your friend asking for a separate $22 check. You’ve worked hard, and maybe your friend had an easier start in life, but that doesn’t mean he’s not entitled to pay for what he ate, and watch every dollar. Divorce is like a recession. You can end up struggling to get back on your financial feet for years.

Perhaps your friend had always intended to pay $22 for his gluten-free dish, and tip the server 50%, or perhaps he has a well-trained side eye and caught your reaction to his paying for his own order, and he decided to pay closer to what everyone else had paid. But ordering separate checks, I suspect, will become more common as prices continue to rise, even at a slower pace, and people feel uncertain about spending money in restaurants.

You believe in equality of bill splitting. I suggest you apply that equality to all dinner guests, regardless of upbringing and dietary restrictions, and allow them to make their own choices about what they pay for at dinner. People often have problems — financial or otherwise — that we are not aware of, so try to leave space for that. And if your friend did see your eye-rolling and under-the-table antics? I’d like to think he made space for your behavior too.

Readers write to me with all sorts of dilemmas.

By emailing your questions, you agree to have them published anonymously on MarketWatch. By submitting your story to Dow Jones & Co., the publisher of MarketWatch, you understand and agree that we may use your story, or versions of it, in all media and platforms, including via third parties.

The Moneyist regrets he cannot reply to questions individually.

Food prices grew at a slower pace in June, but economists remain concerned that prices will reach a level where consumers will make dramatic changes in their behavior.

Food prices rose 3% in June compared to a year ago, according to the latest data from the Bureau of Labor Statistics. After a year of price hikes, consumers continued to see food prices rise, but at a slower rate.

Grocery prices were 5.7% higher in June compared to a year ago, and dining out was 7.7% more expensive. That’s significantly lower than the 13.5% peak inflation for grocery prices last August and the 8.8% peak inflation for dining out.

“Overall, there continues to be a similar narrative of extended upward pressure on food prices as we try to discern whether this stress has led to a tipping point where consumers are struggling to buy the foods that they want,” said Jayson Lusk, the head and distinguished professor of Agricultural Economics at Purdue University.

Reported food insecurity across households of different income levels reached 17% in June, the highest level since March 2022, according to the monthly Consumer Food Insights Report from Purdue University. Although it didn’t deviate too much from the normal range — food insecurity hovered at 14% two months ago — Lusk said the increase is concerning given the amount of pressure on more financially vulnerable consumers.

“Reported food insecurity across households of different income levels reached 17% in June, the highest level since March 2022, according to Purdue University. ”

The pandemic-era expansion of the Supplemental Nutrition Assistance Program ended in March, meaning SNAP recipients are now receiving $90 less on average every month, according to the Center on Budget and Policy Priorities, a progressive policy think tank based in Washington, D.C.

The recent rise in food insecurity could be a lag from households adjusting to the policy change, Lusk said. On average, consumers are spending about $120 per week on groceries and $70 per week on dining out or takeout, the report found.

Middle-income households earning $50,000 to $100,000 a year and low-income households earning less than $50,000 a year cut weekly spending on groceries and dining out by about $10 a week, Purdue found. The average weekly grocery expenditure for low-income households was $103 in June; for middle-income households, it was $118. Households earning more than $100,000 a year spent $141 a week on groceries in June.

Around 47% of low-income households — those earning less than $50,000 a year — said they relied on SNAP benefits in May, up from roughly 40% in February, according to a recent Morning Consult report.

For low-income households, rising food insecurity is often coupled with juggling bills such as utilities and rent, which has also led to rising eviction rates in recent months, according to Propel, an app that aims to help low-income Americans improve their financial health. Propel surveys SNAP users on insecurity around food, finance and their housing situation.

Nearly half of the survey respondents said they cannot afford the food they want. “We were unable to pay bills because we had to buy food. We’re about to lose our home,” a South Carolina user named Anna told the Propel survey.

The share of surveyed households that paid their utilities late rose 11% from May to June, and only 27% of respondents paid their utility bills on time and in full, according to Propel’s June survey.

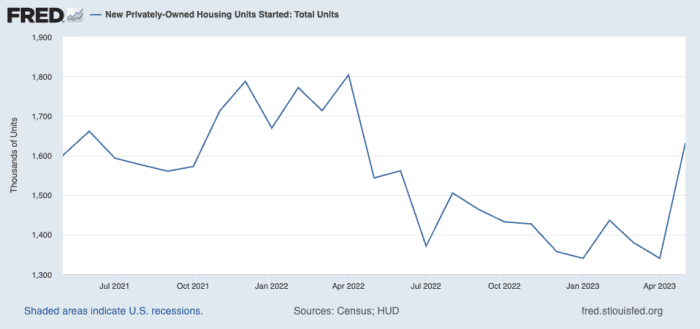

The housing market may feel out of whack to home buyers coping with fast-rising home prices and 7% mortgage rates. But like it or not, the housing market is in the pink of health.

Several economic indicators that measure housing activity — from home prices to sentiment surveys — show that home builders and sellers (the few that are out there) are finding strong demand from home buyers.

News of the housing market’s relative health may be welcome to some — like real-estate agents and investors — but it’s becoming a concern for economists. The more buoyant the housing market, economists say, the more likely the U.S. Federal Reserve will unveil another interest-rate hike, which further heightens the risk of a recession.

“‘The housing market has started to recover, and this is a problem for the Fed because more demand for housing will boost home prices and rents.’”

— Torsten Slok, chief economist at Apollo

“The housing market has started to recover, and this is a problem for the Fed because more demand for housing will boost home prices and rents,” Torsten Slok, chief economist at Apollo, wrote in a note in May. And housing is a big part of how the government measures inflation, he added. This will make it more difficult to reduce inflation from 5% to the Fed’s 2% inflation target, he said.

If the Fed launches another rate hike, it would push mortgage rates, which are already in the 7% range, to go even higher.

“The housing market is in a very — if fragile — recovery,” Mike Simonsen, founder and president of real-estate analytics firm Altos Research, told MarketWatch.

“There appears to be more demand than available supply for homes, especially in the real-estate market,” he explained, which is keeping home prices high, but that doesn’t mean demand could evaporate if the current situation changes. Recall when rates doubled from pandemic-era lows in 2021 to 7% last year, which zapped home-buying momentum.

House hunters have adjusted their expectations. But if rates were to jump from 7% today to even higher levels, “I would not be at all surprised if homebuyers stopped abruptly again,” Simonsen said, stating his thesis for the fragility of the sector. Americans broadly expect rates to go over 8%, according to a March survey by the New York Federal Reserve.

MarketWatch looked at three housing-market indicators — and the picture looks rosier than ever:

Active listings are down — blame interest rates

Redfin’s deputy chief economist, Taylor Marr, said his go-to indicator was active listings.

Active listings are down this spring, compared to the previous year, according to the company’s data. At the end of June, the number of homes listed for sale on the market was down 8.1% over the prior year.

“It really captures that supply is pulling back significantly relative to demand,” Marr said.

Redfin data says that active listings of homes are down.

As a result, the housing market is seeing an excess of demand and not enough supply, which has led to a resurgence of bidding wars in some parts of the U.S.

While this metric is showing signs of the housing market returning to life and heating up amid a shortage of houses for sale, Marr said he’s not yet ready to call it a recovery. “It’s hard to declare completely the bottom of the housing market,” he said.

Still battle-scarred by the housing crash of the Great Recession, Marr said economists “might be hesitant” to say that the housing market is in recovery mode. “We still have a lot of uncertainty with the economy ahead,” he added. “If the economy really takes a turn three or four months from now for whatever reason, it could certainly bring the housing market back lower than it was even last November,” he added.

The price gap between new and existing homes

With a major shortage of resale homes, new-home sales have been taking off.

Home builders, understandably, are thrilled about the inventory shortage.

The National Association of Home Builders measures builders’ sentiment in a monthly index, and that indicator has been very cheery of late. In June, the index turned positive for the first time in nearly a year. Builders were scaling back price reductions; they were happy about current sales conditions as well as sales over the next six months, the NAHB said.

“A bottom is forming for single-family home building as builder sentiment continues to gradually rise from the beginning of the year,” said Rob Dietz, chief economist of the NAHB.

One of the major U.S. home builders, Lennar, also offered some commentary on its second-quarter earnings call last month. The company’s executive chairman, Stuart Miller, said that “the market and the economy will remain constructive for home builders as pent-up demand continues to come to market and consume affordable offerings.”

Miller also doesn’t expect the supply issue to be fixed anytime soon: “We believe that the supply constraint will continue to limit available inventory and maintain supply-demand balance,” he said on the call. “The core elements of the supply shortage will not resolve in the near term as the almost 15-year production deficit will take years to resolve.”

Home-builder confidence, as a result, is signaling high optimism about the future of the housing market, and a return to normalcy.

Builders have ramped up building new single-family and multi-family homes.

Ali Wolf, chief economist at Zonda, looks at how prices of new homes trend relative to resale homes as a key indicator of the health of the housing market. Her conclusion? Housing industry professionals involved in the construction and sale of new homes are out of a recession, given the robust demand.

In fact, demand has been so strong that new homes — generally considered to be more expensive than resales — have become more affordable in home buyers’ eyes given the competition in the existing home space.

Typically, new homes are 20% more expensive than resales, Wolf said. And today? That spread has fallen to 4%.

So what’s going on? Builders are not necessarily slashing prices. Instead, existing home prices have risen as homeowners are reluctant to sell.

That’s a good deal for buyers. New homes, Wolf said, are traditionally considered a “luxury good.” They’re brand new, and buyers can often customize them. They also require less maintenance than older homes.

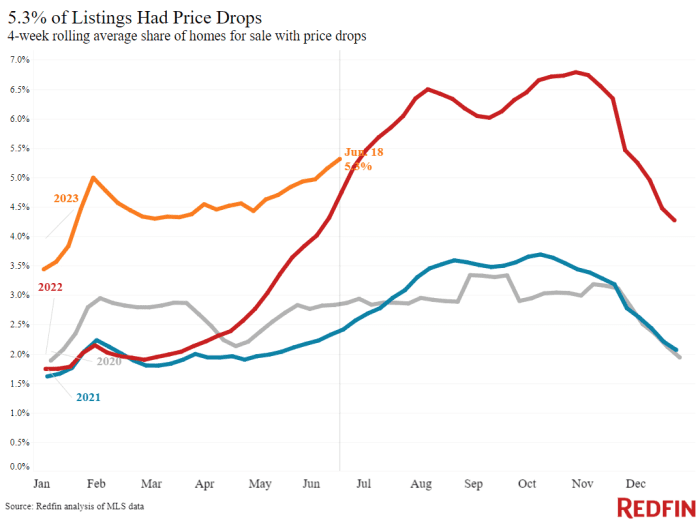

Sellers are holding out on cutting prices

Simonsen, who leads Altos Research, said price cuts were his go-to indicator to gauge the health of the real-estate market. Specifically, price cuts formed a proxy for demand, he explained.

“When the houses are on the market, if there are no buyers for the current houses that are listed, people start taking price cuts,” Simonsen said.

And to be clear, price cuts jumped last year, when rates jumped, he added.

But that dynamic has since changed, as seen in the chart below. “There are currently fewer price reductions now than in 2018 or 2019,” Simonsen said.

Data from Redfin says that homeowners aren’t cutting prices on their homes when selling, possibly due to strong interest from buyers.

And for those of you holding out for home prices to crash? Keep waiting, Simonsen said.

“There’s nothing in the data that shows prices crash,” he said. Even if a recession hits at the end of the year, which results in more job layoffs, demand for home-buying falling, and an increase in foreclosures and distress, that’s still a few years from now, he added.

“There’s no signal of home prices crashing anywhere,” Simonsen added.

The Supreme Court knocked down the Biden administration’s plan to cancel up to $20,000 in student debt for a wide swath of borrowers, the court announced Friday.

The decision means that the White House won’t move forward with the plan for now, though it’s possible officials could try to launch a new version of the debt-forgiveness initiative using a different legal authority. Roughly 26 million borrowers applied for or were automatically eligible for debt relief under the Biden administration’s plan, which canceled up to $10,000 in student debt for borrowers earning less than $125,000 and up to $20,000 in federal loans for borrowers who met that criteria and also used a Pell grant in college.

Americans owe $1.7 trillion of student loans and the White House had estimated that more than 40 million borrowers would benefit from the initiative. But almost as soon as the Biden administration announced the debt-forgiveness plan last year, opponents looked for ways to challenge it legally. Ultimately, two cases made it to the high court.

In one case, two student-loan borrowers sued over the debt-relief plan in part because the Department of Education didn’t submit it for public comment. That, they said, resulted in an initiative that arbitrarily left out or limited the amount of relief available to some student loan borrowers, like themselves. The suit filed by the borrowers was backed by the Job Creators Network, a conservative advocacy organization co-founded by Bernard Marcus, the co-founder of Home Depot, who also supported former President Donald Trump.

Six Republican-led states brought the other case on the basis that canceling debt could harm their state coffers.

The court considered two issues in these cases. The first is whether the plaintiffs had standing, or the ability to bring a lawsuit because they’ve been directly harmed by the policy. The second is whether the Biden administration overstepped in its executive authority when issuing the policy. In order for the justices to reach the second issue, or the merits of the case, they had to find that the plaintiffs had standing to sue.

Legal experts, including some who believed the Biden administration didn’t have the authority to authorize the debt-relief plan, were skeptical of the notion that the parties bringing the cases had standing to sue. During oral arguments in February, the court’s three liberal justices also questioned whether the parties who challenged debt forgiveness were actually injured by the policy.

In addition, one of the members of the court’s conservative wing, Justice Amy Coney Barrett, asked pointed questions about the six states’ argument that they had standing to sue in part because the debt-relief plan would injure the state of Missouri. That claim surrounded the Missouri Higher Education Loan Authority, or MOHELA, a state-affiliated organization that services federal student loans. The states had argued if MOHELA lost accounts due to the debt-relief plan, its revenue would decline and that loss would hurt Missouri because of MOHELA’s ties to the state.

Despite these questions, Barrett agreed with the court’s five other conservative judges and found that the states have standing to sue. The three liberal justices dissented.

“MOHELA is, by law and function, an instrumentality of Missouri,” Chief Justice John Roberts wrote in the majority opinion. “It was created by the State, is supervised by the State, and serves a public function. The harm to MOHELA in the performance of its public function is necessarily a direct injury to Missouri itself.”

The court’s decision in the states’ suit allowed the justices to get to the merits of the case. The parties challenging the debt-relief plan argued that the Department of Education went beyond the authority Congress delegated it in discharging student debt. Solicitor General Elizabeth Prelogar argued to the justices that in canceling student debt, the Secretary of Education acted “within the heartland” of the authority Congress provided to him under the HEROES Act, a 2003 law that aims to ensure student-loan borrowers aren’t left worse off by a national emergency.

The court’s conservative majority sided with the states, with a 6-3 decision, striking down the debt-relief plan in its current form.

“The HEROES Act allows the Secretary to ‘waive or modify’ existing statutory or regulatory provisions applicable to financial assistance programs under the Education Act, but does not allow the Secretary to rewrite that statute to the extent of canceling $430 billion of student loan principal,” Roberts wrote.

In the months leading up to the court’s decision, White House officials said there was no backup plan for if the Supreme Court knocked down the debt-forgiveness initiative. Advocates and activists have said that student-loan repayments shouldn’t resume until the Biden administration fulfills its promise to cancel some student debt.

The bill President Joe Biden signed in June to raise the nation’s debt limit requires that the Department of Education end the pause on federal student loan, interest payments and collections 60 days after June 30, 2023. Interest on federal student loans will resume starting September 1 and payments will start to come due in October, according to the Department’s website.

Advocates and activists have said for years that the Higher Education Act provides the Secretary of Education with the authority to discharge student loans. In ruling that the HEROES Act didn’t authorize the Biden administration’s debt-relief plan, the court left the option open for the Biden administration to create a loan-forgiveness program authorized under the HEA.

The court’s decision marks the latest development in a more-than-decade-long push to get the government to cancel student debt en masse. The idea, which has its origins in the Occupy Wall Street movement, made it to the presidential campaign stage during the 2020 cycle and was adopted by the White House last year.

Proponents of student debt cancellation and the Biden administration, have expressed concern that without some kind of relief a large swath of borrowers could slip into delinquency and default with the return of student loan payments later this year.

Rite Aid Corp. said Thursday that its fiscal first-quarter pharmacy sales got a boost from a new class of drug.

Pharmacy sales, which rose 3.4% from a year ago, were boosted by higher sales of Ozempic and other GLP-1 receptor agonists, which are used to treat Type 2 diabetes and obesity.

The higher sales did not translate into profit, however.

“As the cost of these drugs is also high, the impact of the increase in volume of these drugs on our gross profit dollars is minimal,” Rite Aid Chief Financial Officer Matthew Schroeder told analysts on the company’s earnings call, according to a FactSet transcript.

Still, the company RAD, +2.96%

cheered investors by raising its full-year revenue guidance due to the sales bump from Ozempic and other high-dollar GLP-1 drugs. It now expects revenue of $22.6 billion to $23 billion, ahead of the FactSet consensus of $22.3 billion.

Ozempic, Wegovy and Rybelsus, which are made by Novo Nordisk NOVO.B, +0.17%

NOVO.B, +0.17%,

and Mounjaro, which is made by Eli Lilly & Co. LLY, +1.34%,

have become so popular in the U.S. that supplies have at times run short and the U.S. Food and Drug Administration has been forced to warn patients against using knockoff versions.

The drugs are administered by injection and mimic the effects of GLP-1, a gut hormone that can help control blood-sugar levels and reduce appetite. GLP stands for glucagon-like peptide.

Ozempic, Rybelsus and Mounjaro have been approved by the Food and Drug Administration for treatment of Type 2 diabetes, while Wegovy is approved for people with obesity and for certain people with excess weight combined with weight-related medical problems.

Last year, more than 5 million prescriptions for Ozempic, Mounjaro, Rybelsus or Wegovy were written for weight management, up from 230,000 in 2019, according to data and analytics firm Komodo Health.

Obesity drugs could be a $54 billion market by 2030, up from $2.4 billion in 2022, Morgan Stanley said in a report last year. Reports of people who take GLP-1 drugs seeing improvements in addictive behaviors such as smoking and drinking have lately amplified interest in the medications.

Drug companies, including Lilly and Pfizer Inc. PFE, -0.32%,

are now working to develop treatments in the form of pills that could be more convenient alternatives to the injectables.

A recent article in The Wall Street Journal describes how many baby boomers remain attached to stocks, even in retirement. Adults age 65 and up are the only group of Americans to see stock ownership rates rise since before the 2008 financial crisis, according to the article. Whether because of sentimental attachment, fear of missing out, or tax aversion, older Americans often overweight their portfolios to stocks, which could put their retirement goals in jeopardy. So for this week’s Barron’s Advisor Big Q column, we asked financial advisors: “How do you persuade baby boomer clients who own too much stock to reallocate?”

Less than 48 hours before being found dead in prison, Jeffrey Epstein met with his lawyers to sign a new version of his last will and testament.

The disgraced financier had been under psychological observation from a previous episode in which he was found hanging in his prison cell, but the provocative step of signing a new will went unnoticed by prison officials until after Epstein’s death.

That lapse was one of many missteps and missed opportunities to stop Epstein from killing himself sometime in the early morning hours of Aug. 10, 2019, contained in an official report released Tuesday by the Department of Justice’s internal, investigative watchdog.

The report stands by the initial determination that Epstein’s death was the result of suicide as there were no signs of foul play or that anyone had been anywhere near his cell after he was last seen alive by prison guards the night before.

But the report also lays out in detail Epstein’s final days, including a number of curious steps he took in that time and a series of serious protocol breaches made by prison staff that would contribute to him being left unwatched long enough to kill himself.

Epstein was arrested on July 6 of that year on federal sex-trafficking charges. He was ordered held without bail and eventually placed in the special housing unit of the Manhattan Correctional Center in New York while he awaited trial. There, inmates were kept in their cells for 23 hours a day, although Epstein spent much of his time meeting with his attorneys, the report said.

From the beginning, Epstein had a cellmate. On the night of July 23, the cellmate began banging on the cell door and screaming for the guards. When officers arrived, they found Epstein hanging from the bunk bed ladder with an orange piece of cloth wrapped around his neck.

The officers pulled Epstein down and managed to resuscitate him. When he later came to, he initially said he thought his cellmate had tried to kill him, but later said he could not recall what had happened. An investigation could not definitively conclude what had happened, the DOJ report said.

Following the episode, Epstein was placed on suicide watch — in which he was continuously monitored by staff. When prison psychologists later determined that Epstein was no longer a risk to himself, they downgraded his status to “psychological observation,” meaning he could be returned to a cell and not be kept under continual watch.

Curiously, Epstein said he wanted his original cellmate back. When prison officials said they weren’t sure that was such a good idea, Epstein replied: “Yeah, but I don’t understand, you know, we were bunkies, everything was cool,” the report quoted him as saying.

On July 30, prison staff were informed that Epstein needed to be assigned an “appropriate cellmate,” and he was housed with another inmate in a cell just 15 feet away from the guard station. That inmate later reported that Epstein was allowed to sleep on a mattress on the floor and was given an extra blanket, in violation of prison rules.

On August 8, Epstein signed the new will. The following morning, Epstein’s cellmate was transferred out of the prison, leaving Epstein alone.

Later that day, more than 2,000 pages of documents were publicly released as part of court proceedings against Epstein’s long-time companion, Ghislaine Maxwell. The documents included extensive information that was damaging to Epstein.

Maxwell was found guilty in 2021 of conspiring with Epstein to sexually abuse minors and sentenced to 20 years in prison.

That evening, after meeting with his lawyers, Epstein was allowed to place an unmonitored phone call. The report said that while Epstein claimed he was calling his mother, he actually phoned “someone with whom he allegedly has a personal relationship,” the report stated.

Epstein was last seen alive in his cell at 10:40 p.m. and was discovered dead by prison staff at 6:30 a.m. the following morning. He was once again found hanging from the upper bunk with a cord tied around his neck.

According to the report, prison officials discovered extra sheets and bedding in the cell. An investigation revealed that the prison guards on duty that night, failed to conduct rounds of the cell block and check on Epstein every 30 minutes like they were supposed to, meaning Epstein was unwatched for nearly eight hours.

The guards were later charged with falsifying records to show that they had done the required rounds while they were actually sleeping and surfing the internet. The two guards later reached deferred prosecution agreements with the federal prosecutors, in which charges against them were dropped after they performed community service and kept out of trouble for six months.

Some of the prison cameras in the cell block also had been malfunctioning for weeks so that while they provided a live feed of the area, they failed to record. A nearby camera that was fully operational showed no one entering the area after the guards last locked Epstein in his cell at 10:40 p.m. the night before he was found dead, the report said.

An autopsy showed no signs of foul play or that Epstein had struggled with anyone prior to his death. Officials say they believe he had hanged himself.

Home-equity lines of credit (HELOCs) and second-lien mortgages have been staging a notable comeback as U.S. homeowners look for liquidity and ways to monetize the pandemic surge in home prices, according to BofA Global.

It used to be that borrowers sitting on an estimated $33 trillion pile of equity built up in their homes could simply refinance and pull out cash, until the Federal Reserve’s rapid rate hikes began squelching the option.

Now, with mortgage rates above 6%, and the Fed penciling in two more rate hikes in 2023, cash-strapped homeowners have been seeking out alternatives to extract cash from their properties.

While cash-out refinances tumbled 83% in the fourth quarter of 2022 from a year before, HELOCs rose 7% and home-equity loans grew 31%, according to the latest TransUnion data.

“Borrower demand remains high, particularly given household budgets have been pressured by rising food and energy costs,” a BofA Global credit strategy team led by Pratik Gupta’s, wrote in a weekly client note.

Risky loans to subprime borrowers and home equity products helped precipitate the 2007-2008 global financial crisis and the era’s wave of devastating home foreclosures.

At the time, households had more than $1.2 trillion of home equity revolving and available credit (see chart), whereas the figure was closer to $900 billion in the first quarter of this year.

Home equity products are making a big comeback as households seek liquidity

BofA Global, New York Fed Consumer Credit Panel/Equifax

The pandemic saw home prices surge, giving a big boost to home equity levels. The Urban Institute pegged home equity in the U.S. at $33 trillion as of May, up from a post-2008 peak of about $15 trillion.

BofA analysts argued this time home equity products look different, with roughly $17 trillion of tappable equity across 117 million U.S. homeowners, and most borrowers having high credit scores and low rates.

“The vast majority of that — $14 trillion — is from the cohort of homeowners who own their homes free & clear,” Gupta’s team wrote.

Another $1.6 trillion of equity could be available from Freddie Mac and Fannie Mae borrowers, according to his team, which pegged an estimated 94% of all outstanding U.S. first-lien home mortgages now below 4% rates.

Major banks own the bulk of home equity balances (see chart), led by Bank of America Corp. BAC, +1.23%,

PNC Bank PNC, +0.57%,

Wells Fargo, WFC, -0.05%,

JPMorgan Chase JPM, +0.24%

and Citizens CFG, +0.35%,

according to the team, which notes several other major banks appear to have hit pause on their programs.

A smaller portion of HELOCs and second-lien mortgages have been securitized, or packaged up and sold as bond deals, while nonbank lenders have been offering the products as well.

Stocks closed lower Monday, taking a pause from a recent rally, as investors monitored weekend tumult in Russia. The Dow Jones Industrial Average DJIA, -0.04%

was less than 0.1% lower, while the S&P 500 index SPX, -0.45%

was off 0.5% and the Nasdaq Composite COMP, -1.16%

fell 1.2%, according to FactSet.

That’s a notion that has long fueled hope for many of the more than 40% of Americans who are considered obese — and fueled criticism by those who advocate for wider weight acceptance. Soon, it may be a reality.

High-dose oral versions of the medication in the weight-loss drug Wegovy may work as well as the popular injections when it comes to paring pounds and improving health, according to final results of two studies released Sunday night. The potent tablets also appear to work for people with diabetes, who notoriously struggle to lose weight.

Drugmaker Novo Nordisk NOVO.B, +0.22%

plans to ask the U.S. Food and Drug Administration to approve the pills later this year.

“If you ask people a random question, ‘Would you rather take a pill or an injection?’ People overwhelmingly prefer a pill,” said Dr. Daniel Bessesen, chief of endocrinology at Denver Health, who treats patients with obesity but was not involved in the new research.

That’s assuming, Bessesen said, that both ways to take the medications are equally effective, available and affordable. “Those are the most important factors for people,” he said.

There have been other weight-loss pills on the market, but none that achieve the substantial reductions seen with injected drugs like Wegovy. People with obesity will be “thrilled” to have an oral option that’s as effective, said Dr. Katherine Saunders, clinical professor of medicine at Weill Cornell Health and co-founder of Intellihealth, a weight-loss center.

Novo Nordisk already sells Rybelsus, which is approved to treat diabetes and is an oral version of semaglutide, the same medication used in the diabetes drug Ozempic and Wegovy. It comes in doses up to 14 milligrams.

But results of two gold-standard trials released at the American Diabetes Association’s annual meeting looked at how doses of oral semaglutide as high as 25 milligrams and 50 milligrams worked to reduce weight and improve blood sugar and other health markers.

A 16-month study of about 1,600 people who were overweight or obese and already being treated for Type 2 diabetes found the high-dose daily pills lowered blood sugar significantly better than the standard dose of Rybelsus. From a baseline weight of 212 pounds, the higher doses also resulted in weight loss of between 15 and 20 pounds, compared to about 10 pounds on the lower dose.

Another 16-month study of more than 660 adults who had obesity or were overweight with at least one related disease — but not diabetes — found the 50-milligram daily pill helped people lose an average of about 15% of their body weight, or about 35 pounds, versus about 6 pounds with a dummy pill, or placebo.

That’s “notably consistent” with the weight loss spurred by weekly shots of the highest dose of Wegovy, the study authors said.

But there were side effects. About 80% of participants receiving any size dose of oral semaglutide experienced things like mild to moderate intestinal problems, such as nausea, constipation and diarrhea.

In the 50-milligram obesity trial, there was evidence of higher rates of benign tumors in people who took the drug versus a placebo. In addition, about 13% of those who took the drug had “altered skin sensation” such as tingling or extra sensitivity.

Medical experts predict the pills will be popular, especially among people who want to lose weight but are fearful of needles. Plus, tablets would be more portable than injection pens and they don’t have to be stored in the refrigerator.

But the pills aren’t necessarily a better option for the hundreds of thousands of people already taking injectable versions such as Ozempic or Wegovy, said Dr. Fatima Cody Stanford, an obesity medicine expert at Massachusetts General Hospital.

“I don’t find significant hesitancy surrounding receiving an injection,” she said. “A lot of people like the ease of taking a medication once a week.”

In addition, she said, some patients may actually prefer shots to the new pills, which have to be taken 30 minutes before eating or drinking in the morning.

Paul Morer, 56, who works for a New Jersey hospital system, lost 85 pounds using Wegovy and hopes to lose 30 more. He said he would probably stick with the weekly injections, even if pills were available.

“I do it on Saturday morning. It’s part of my routine,” he said. “I don’t even feel the needle. It’s a non-issue.”

Some critics also worry that a pill will also put pressure on people who are obese to use it, fueling social stigma against people who can’t — or don’t want to — lose weight, said Tigress Osborn, chair of the National Association to Advance Fat Acceptance.

“There is no escape from the narrative that your body is wrong and it should change,” Osborn said.

Still, Novo Nordisk is banking on the popularity of a higher-dose pill to treat both diabetes and obesity. Sales of Rybelsus reached about $1.63 billion last year, more than double the 2021 figure.

Other companies are working on oral versions of drugs that work as well as Eli Lilly and Co.’s LLY, +0.25%

Mounjaro — an injectable diabetes drug expected to be approved for weight-loss soon. Lilly researchers reported promising mid-stage trial results for an oral pill called orforglipron to treat patients who are obese or overweight with and without diabetes.

Pfizer PFE, -1.11%,

too, has released mid-stage results for dangulgipron, an oral drug for diabetes taken twice daily with food.

Novo Nordisk officials said it’s too early to say what the cost of the firm’s high-dose oral pills would be or how the company plans to guarantee adequate manufacturing capacity to meet to demand. Despite surging popularity, injectable doses of Wegovy will be in short supply until at least September, company officials said.

Signing up for Amazon Prime is as easy as 1-2-3. Canceling it, not so much.

For years, up until this past April, the online retail giant made customers trying to quit its signature service navigate an odyssey through a labyrinthine system called the “Iliad Flow” named after the epically long and complex masterwork by the Greek poet Homer.

According to a civil lawsuit filed Wednesday by the Federal Trade Commission, Amazon customers were required to make their way through a four-page, six-click, 15-option process to stop paying for the service. One wrong click, and they were sent back to the beginning, the lawsuit said.

The FTC noted that Amazon AMZN, +3.69%

maintained the multistep process even though new subscribers in the U.S. to $14.99-a-month or $139-a-year Prime accounts needed only one or two clicks. And even though subscribers could sign up on a multitude of devices, they could only cancel using their desktop computer or mobile phone or by calling customer service.

The FTC suit also accused Amazon of manipulating millions of customers into inadvertently signing up for Prime and then hitting them with automatic renewals without warning.

Amazon has dismissed the charges as misguided, adding that the lawsuit is legally and factually inaccurate. It has vowed to fight the FTC.

The FTC said in court papers that Amazon created the complex “Iliad Flow” exit strategy in 2016 and kept it in place until April of this year, when it caught wind that the agency was preparing to file a lawsuit about the practice.

During that time frame, Amazon quadrupled the number of global Prime subscribers from around 50 million to more than 200 million. The program brings around $25 billion into Amazon’s coffers every year.

The suit described an allegedly maddening process for a customer to actually cancel a subscription.

To start, a subscriber first had to find the “Iliad Flow,” which was not made easy, the FTC suit said. A customer had to select the “accounts and list” dropdown menu, navigate to the third column and then select the eleventh option there: Prime Membership.

That would bring the customer to the Prime Central page. There, one would have to click the “manage membership” button to trigger options that finally included an “end membership” button. But that was only the beginning.

Only after clicking “end membership” would the customer enter the “Iliad Flow” process. From there, a customer would need to navigate three more pages, each with a multitude of options, to finally complete canceling the subscription.

This is one of several web pages a Prime customer would need to navigate in order to cancel the service, the FTC said.

Federal Trade Commission

On the first page, customers were forced to “take a look back at [their] journey with Prime” — a kind of greatest-hits reel of Prime services used over the years. The page was also loaded with marketing material for a multitude of Prime services, with links reading: “Start shopping today’s deals!” and “You can start watching videos by clicking here!” or “Start listening now!”

One wrong click would knock the subscriber out of the “Iliad Flow.”

If the subscriber managed to navigate to the bottom of the page, he or she would finally find a “continue to cancel” button. That would take them to Page 2.

According to the FTC, that page would present the customer with a number of discount options, such as switching from monthly to annual payments, or taking advantage of student discounts or discounts for people on government assistance. The page also included warning icons and links stating: “Items tied to your Prime membership will be affected if you cancel your membership,” and “By canceling, you will no longer be eligible for your unclaimed Prime exclusive offers.”

Clicking on any of those would take the subscriber out of the “Iliad Flow.”

At the bottom of that page was another “continue to cancel” button, which would take the user to Page 3.

If you managed to get to this page, you were only six options away from actually being able to quit Amazon’s Prime service, the FTC suit said.

Federal Trade Commission

On this final page, a customer was presented with five options, only the last of which — “end now” — would actually allow the subscription to be canceled. The other options included pausing the subscription or canceling its auto-renewal function. Pressing any of the four other choices would bring the user out of the “Iliad Flow.” They would have to start over if they wanted to continue.

Only after successfully navigating this maze of web pages would the customer be allowed to actually cancel the service.

The suit said this process caused cancellations to drop significantly.

A nascent category of mental health treatments is getting a major cash infusion.

Blake Mycoskie, founder of the canvas-footwear phenomenon TOMS Shoes, has committed to giving $100 million to support psychedelic research and access, Mycoskie told MarketWatch in an exclusive interview. The money will help fund academic institutions investigating psychedelics’ potential to treat anxiety, depression, post-traumatic stress disorder and other mental-health issues, as well as nonprofits helping to connect patients in need with psychedelic treatments.

Traditional psychedelics include hallucinogens like LSD and psilocybin, or “magic” mushrooms–recently legalized in Oregon and Colorado. Other drugs that can alter mood and perception–such as ketamine and MDMA, also known as ecstasy–aren’t classical psychedelics but are broadly included in the research and policy discussions generating a surge of interest in this class of treatments. The U.S. Food and Drug Administration, for example, has granted psilocybin and MDMA “breakthrough therapy” status, a designation designed to expedite development and review of drugs for serious conditions, and could approve MDMA for treatment of PTSD as soon as next year.

Given the rapid developments in the field, ”we really need to get this right, and we really need to have these foundations and nonprofits funded properly,” therapists trained, and clinics open and running smoothly, Mycoskie said. “I felt a real sense of urgency,” he said, and asked his wealth manager, “what’s the most that I can give?”

The $100 million answer to that question amounts to about a quarter of Mycoskie’s net worth and marks a major milestone in psychedelics’ delicate image transformation. Shedding some of their dangerous-party-drug reputation, psychedelics are gaining attention from top pharmacologists, the scientific community, biotech companies and investors who see them as a critical part of the solution to America’s mental health crisis.

Cracked open

Mycoskie, 46, said his interest in psychedelics dates back to 2017, when a friend returning from a trip to Central America described his incredible experience with ayahuasca, a plant-based psychedelic brewed into a tea. As an entrepreneur under intense pressure to perform, Mycoskie said, he decided to try it for himself. The experience “cracked me open, and it connected me more to my faith in God, made me feel that we were all connected and everything was fine and perfect,” he said. “I came back just feeling like, wow, that was more powerful than any therapy I’d ever done.” He later tried MDMA-assisted therapy, he said, which also helped him process issues that traditional talk therapy had left unresolved.

Realizing how many people could benefit from similar treatments, Mycoskie started giving money to academic groups and the Multidisciplinary Association for Psychedelic Studies, or MAPS, a nonprofit organization. He also got involved in last year’s Colorado ballot initiative, which legalized psilocybin and several other psychedelic substances, including ibogaine, which has shown potential to treat substance-use disorders. Mycoskie has already given about $10 million to psychedelic research and access, he said, and plans to give about $5 million annually for 18 more years.

Mycoskie was a bit squeamish at first, he acknowledges, about publicly backing research on drugs that are largely illegal. “Am I going to get held up at TSA every time I go through the airport?” he remembers thinking. The U.S. Drug Enforcement Administration categorizes LSD and MDMA alongside heroin as “schedule one” drugs, defined as “drugs with no currently accepted medical use and a high potential for abuse.” But with growing public awareness and acceptance of the drugs’ potential as mental-health treatments, he said, he felt emboldened to make a big public commitment, and “the research has caught up,” he said. “It’s important that people like myself put their name out there and their money out there to show that this really is a path forward,” he said.

Mycoskie’s $100 million commitment “is the biggest that we’ve ever seen in the psychedelics space,” said Joe Green, president of the Psychedelic Science Funders Collaborative, a nonprofit supporting philanthropy in the field, and a MAPS board member. Now that research has made great strides to support use of the medicines as mental-health treatments, that money can help ensure that “these actually come to the world in a safe and beneficial way,” Green said. With certain treatments legalized in Oregon and Colorado, for example, “the system requires licensed guides, facilitators, licensed service centers,” he said. “It’s not like cannabis medical–you won’t be able to take the mushrooms outside the service center.”

Psychedelic therapeutics market could be worth more than $8.3 billion by 2028

Mycoskie plans to publicize his pledge at the Multidisciplinary Association for Psychedelic Studies’ psychedelic science conference–billed as “the largest psychedelic conference in history”–this week in Denver. On the agenda: Sessions ranging from state policy and regulatory considerations to clinical trials of psilocybin- and MDMA-assisted therapy and “sex and psychedelics: weaving altered states for healing and pleasure.”

The news comes as lawmakers on both sides of the aisle are pushing for new funding for research into the use of psychedelics to treat PTSD in military service members as part of the fiscal year 2024 National Defense Authorization Act, which the House Armed Services Committee will consider Wednesday.

Already, public companies like Atai Life Sciences ATAI, -6.91%,

Compass Pathways CMPS, -3.37%

and Cybin CYBN, +6.81%

are developing therapies based on psychedelic substances. The psychedelic therapeutics market could be worth more than $8.3 billion by 2028, according to InsightAce Analytic. Even the federal government is throwing money at this niche, funding efforts to develop psychedelic mental-health treatments without the hallucinogenic side effects.

More than one in five U.S. adults live with a mental illness, according to the National Institute of Mental Health, and less than half of the roughly 58 million adults with any mental illness are receiving treatment. Suicide rates, which have been on a long upward trajectory, declined briefly between 2018 and 2020 before returning to peak levels in 2021, according to the Centers for Disease Control and Prevention. Nine out of 10 U.S. adults believe the country is suffering a mental health crisis, according to a survey last year by CNN and KFF, a health policy nonprofit. And commonly prescribed antidepressants, such as selective serotonin reuptake inhibitors (SSRIs) don’t work well for many patients.

Nushama, a New York City wellness center offering ketamine-based therapy.

Courtesy of Nushama and Costas Picadas

Mental illness “is truly an epidemic, and we are losing the fight,” said Dylan Beynon, CEO and founder of Mindbloom, which offers a telehealth ketamine treatment program. While there are some existing solutions that are helping to bend the curve, he said, more research and educational support for providers and patients is needed, he said.

Indeed, some substantial hurdles still separate psychedelic mental-health treatments from many of the patients they might benefit, including a lack of insurance coverage for the currently legal treatments and debate over how to administer them safely. In the case of ketamine, for example, which is FDA-approved as an anesthetic and used off-label as a mental-health treatment, some providers favor in-person guided sessions while others, like Beynon, advocate for telehealth prescribing–a model that boomed during the pandemic.

Some experts have lately warned that the practice of psychedelic medicine may be getting ahead of the science. Given the growing public and commercial interest, “there is the risk that use of psychedelics for purported clinical goals may outpace evidence-based research and regulatory approval,” the American Psychiatric Association said last year in a position statement on psychedelic and “empathogenic” agents–a category that includes MDMA.

Mycoskie has also made some investments in the psychedelics space, although he said profits aren’t his motivation. He has invested in Mind Medicine Inc. MNMD, -0.50%,

which says it is developing “psychedelic inspired medicines” that aim to treat the underlying causes of distress in the brain. And Mycoskie helped fund a public benefit corporation linked with MAPS, which is taking MDMA through the FDA approval process–an investment that will pay dividends when the treatment is commercialized, he said.

Providers currently offering ketamine treatments say they’re eager to expand into MDMA and other therapies in the category as soon as they’re legal. Mindbloom, for example, currently offers a ketamine treatment program that’s available through telehealth in several dozen states and aims to start offering MDMA-assisted therapy late next year after FDA approval is finalized, Beynon said. Psilocybin-assisted therapy could come a couple of years after that, he said.

Nushama, a New York City psychedelic wellness center that offers ketamine-based therapy, delivered through in-person IV infusions, also hopes to expand into MDMA when it’s approved, said co-founder Jay Godfrey.

Treatment without the trip

Still on the horizon: New treatments that could produce psychedelic medicines’ mental-health benefits without the trip. University of North Carolina School of Medicine pharmacology professor Dr. Bryan Roth is leading an effort to create new medications for depression, anxiety and substance abuse that work similarly to psychedelics but without the hallucinogenic, disorienting side effects. His effort is backed by a $27-million grant from the Defense Advanced Research Projects Agency. Such treatments, Roth said, could help the many patients for whom such psychedelic effects are unappealing or ill-advised–such as military service members. “You would never want to give psilocybin or ketamine to somebody who has a gun,” Roth said.

Having worked with Vietnam veterans suffering from PTSD while training as a psychiatrist earlier in his career, Roth said, he’s keenly aware of the need for safe and effective treatments. “There was nothing we could give them for their symptoms,” he said. “The most we could do was give them medications to stop their ability to have dreams, so they wouldn’t have nightmares. That was basically it.”

“Undoing 52 years of propaganda is a heavy lift,” said Nushama co-founder Jay Godfrey.

Costas Picadas

Roth’s team has already developed compounds that have shown antidepressant effects without psychedelic side effects in mice, he said. The team is now working to find a clinical candidate suitable for testing in humans, he said.

Treatments that can help “break bad emotional or psychological patterns without scary, high-friction psychedelic experiences would be a great thing for patients, providers and the healthcare system,” said Mindbloom’s Beynon.

Much more remains to be done to reduce the stigma associated with psychedelics, experts say. It has been 52 years since President Richard Nixon declared drug abuse “public enemy number one,” and billions of dollars have been spent since then telling people that “these medicines are dangerous, that they’re addictive, and that they’ll fry your brains,” Godfrey said. “Undoing 52 years of propaganda is a heavy lift, but one thing I’m optimistic about is that the outcomes are starting to speak for themselves.”