It’s become a common refrain among those who believe the 2023 stock-market rally seems too good to last: by almost any measure one chooses, equity valuations in the U.S. are looking stretched.

While this point is generally conceded by equity analysts, it glosses over another debate of potentially greater import. What impact, if any, do so-called fundamental factors like valuation have on stock-market performance, and could we really see them put the breaks on a momentum-driven rally?

At least for now, the answer may be that valuation is taking a back seat to hopes tied to artificial-intelligence and the strength of the U.S. economy fuel optimism that could continue to push the market higher.

“Every investors should explore fundamentals, but you have periods of momentum where fundamentals take a back seat,” said Liz Young, head of investment strategy at SoFi, during a phone interview with MarketWatch.

Valuations are looking stretched

Investors buying stocks today are paying more per unit of expected earnings than at any point since April of 2022, when interest rates were much lower than were they are now. The forward price-to-earnings ratio for the S&P 500

SPX,

-0.23%

currently stands at 19.7, according to FactSet data.

That is higher than the five-year average of 18.6, and the 10-year average of 17.4, FactSet data show.

To be sure, the P/E for S&P 500 index companies masks a remarkably wide dispersion internally. An analysis by Goldman Sachs analysts found that the so called “magnificent seven” technology stocks are currently sporting a P/E of 31, while the remaining 493 companies in the index are being valued at 17.

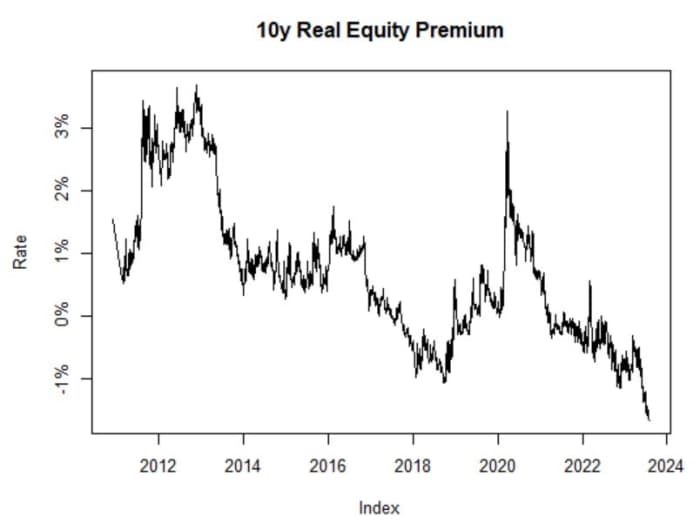

Another closely watched valuation metric that compares the value investors could reap from owning stocks with that of owning comparatively safer Treasury bonds is looking even more extreme.

The equity risk premium (ERP) has fallen to its lowest level since mid-2002, according to data analysis conducted by MarketWatch and Sierra Investment Management CIO James St. Aubin.

According to Aubin, the reason investors are willing to accept such a low equity risk premium instead of parking their money in short-term Treasury bills yielding more than 5% is that corporate earnings growth is expected to accelerate markedly starting in 2024.

In the past, investors have been willing to accept a low or even negative ERP if they believed they would be well-compensated for it by explosive earnings growth further out in the future. And the AI craze is bolstering expectations that some of the largest U.S. technology firms could reap windfall profits while boosting productivity across the U.S. economy.

“You’re willing to accept a low ERP, or in the case of the 1990s, even a negative ERP, if you think you’re going to have strong earnings growth,” St. Aubin said during a phone interview with MarketWatch.

Great expectations

Right now, Wall Street analysts expect to see earnings growth rise next year following several consecutive quarters of declines in late 2022 and the first half of 2023.

Although many S&P 500 firms have yet to report earnings for the quarter ended in June, the index is on track to see earnings shrink by more than 7% year-over-year, according to FactSet data. Assuming this comes to pass, it would mark the third straight quarter of year-over-year declines.

If earnings growth ticks higher during the second half of the year, analysts expect 2023 will ultimately yield earnings growth of roughly 1% for the calendar year.

But in 2024, analysts are already penciling in profit expansion of more than 12%, according to FactSet.

A lot of things need to go right for companies to meet this lofty benchmark, St. Aubin said. For example, companies will need to show that they can continue to raise prices even as inflation levels off, while the U.S. economy will need to avoid the recession that many economists still expect will eventually arrive.

Even if everything goes right and U.S. companies beat Wall Street’s expectations, an analysis of historical data suggests investors buying at today’s prices could experience smaller returns over the long term.

What does history tell us?

A regression analysis performed for MarketWatch by St. Aubin using data going back to 1991 found that when stocks are valued north of 20 on a forward price-to-earnings basis, annualized returns over the following decade tend to shrink to less than 5%.

Even if lofty valuations don’t put the breaks on the market rally, their influence could be felt by investors in other ways. For example, given the dispersion between valuations for the market leaders and everybody else, value-conscious investors might start to view small-cap stocks and other underappreciated cyclical sectors as a better buy.

“As valuations reach extremes in some of the sectors, I think it’s natural for people to move away from them. If investors aren’t going to rotate their money out of the equity market, maybe they move into other areas like small-caps that look more attractive,” Young said.

That is already starting to happen, to a degree. The Russell 2000

RUT,

-0.51%,

an index of small-cap stocks, has outperformed even the highflying Nasdaq Composite

COMP,

-0.35%

over the past month, rising 5% to the Nasdaq’s 3.6%, according to FactSet data. Although the Nasdaq is still sitting on a year-to-date gain of 36.5%, compared with the 12.7% for the Russell.

However, July was a good month for U.S. stocks, broadly speaking. Whether August portends the same is unclear. At least one prominent stock-market bull, Fundstrat’s Tom Lee, has advised clients to expect a shallow pullback in August. So far, the main U.S. equity indexes are starting the month in the red, with the S&P 500 and Nasdaq down 0.3% at 4,575 and 14,295 in recent trade.

See: Investors should brace for an August stock-market slump, Fundstrat’s Tom Lee warns

The Dow Jones Industrial Average, by comparison, was little-changed Tuesday afternoon in New York at 35,569.