U.S. stock indexes finished sharply higher on Thursday, the second-to-last trading session of the year, with the Nasdaq Composite jumping 2.6%, erasing losses from earlier in the week.

The three main indexes built on premarket gains after U.S. weekly jobless claims data showed the number of workers receiving benefits has climbed to the highest level since February, a tentative sign that the Federal Reserve’s interest-rate hikes might be slowing economic growth and inflation.

How stocks traded

The S&P 500 SPX, +1.75%

rose 66.06 points, or 1.8%, to end at 3,849.28.

Dow Jones Industrial Average DJIA, +1.05%

added 345.09 points, or 1.1%, finishing at 33,220.80.

Nasdaq Composite COMP, +2.59%

climbed 264.80 points, or 2.6%, to finish at 10,478.09.

On Wednesday, the Nasdaq Composite dropped 1.4% to 10,213, its lowest closing level of the year. The S&P 500 is up more than 6% from its 2022 low from mid-October, but the large-cap index remains down 19.2% year-to-date, FactSet data show.

What drove markets

The penultimate session of 2022 showed tentative signs of delivering some much needed festive cheer for the stock market as a hope for “Santa Claus rally” had earlier failed to materialize.

The jobless-claims data “points to a loosening in the labor market, which is welcome news for the Fed,” said Larry Adam, chief investment officer at Raymond James, in a tweet.

However, analysts at Citi still think the claims data indicates a still-very-tight labor markets compared to historical levels.

“While both initial and continuing claims increased this week, they remain within the levels of late 2019,” wrote Gisela Hoxha, U.S. economics research analyst at Citi. “Anecdotes of company layoffs have increased in recent months, particularly in the tech sector. While it could be hard to disentangle the seasonal effects from the announced layoffs, in our view there is no significant evidence of them showing up in the claims data yet.”

Some of those layoffs could be taking effect a couple months later as employees might be kept on payroll for some time after the announcement, which will become significant signs of weakness in the labor market in 2023, Hoxha added.

Stocks were on track to finish what’s set to be the worst year since 2008 not far from 2022 lows. The S&P 500’s 52-week closing low at 3,577.03 was hit on Oct. 12.

Still, the three indexes managed to erase losses from earlier in the week on Thursday. Nasdaq Composite was down 0.2% this week, while the S&P 500 gained 0.1% and the Dow was nearly flat as of Thursday’s close. If the S&P 500 can hold on to weekly gains through Friday, it would mark the end of a three-week losing streak that has been the index’s longest since September, FactSet data show.

Companies in focus

Tesla Inc. TSLA, +8.08%

shares finished 8.1% higher on Thursday after posting its first rise in eight sessions Wednesday. The electric-vehicle maker’s shares had declined in seven consecutive sessions, their worst losing streak since a seven-session run that ended on Sept. 15, 2018.

Southwest Airlines LUV, +3.70%

remains in focus as the airline tries to recover from logistical issues that caused thousands of flight cancellations over the past week. The stock fell 11% over the past two days, but rose 3.7% in Thursday session.

General Electric’s GE, +2.17%

spinoff of GE HealthCare Technologies will join the S&P 500 index when it begins trading as a separate public company on Jan. 4. GE HealthCare will replace Vornado Realty Trust VNO, +1.63%,

which will move to the S&P MidCap 400. Vornado will replace logistics company RXO RXO, +8.39%,

which will move to the S&P SmallCap 600. GE HealthCare — trading on a when-issued basis — rose 0.9%, while Vornado gained 1.6% and RXO jumped 8.4%.

Cal-Maine CALM, -14.50%

shares ended 14.5% lower after its quarterly earnings came in below Wall Street forecasts. Cal-Maine reported record sales for the quarter as an avian flu outbreak continued to limit the supply of eggs, driving prices sharply higher. The company also said there were no positive tests for avian flu at any of its production facilities, as of Wednesday.

U.S. stock indexes finished sharply higher on Thursday, the second-to-last trading session of the year, with the Nasdaq Composite jumping 2.6%, erasing losses from earlier in the week.

The three main indexes built on premarket gains after U.S. weekly jobless claims data showed the number of workers receiving benefits has climbed to the highest level since February, a tentative sign that the Federal Reserve’s interest-rate hikes might be slowing economic growth and inflation.

How stocks traded

The S&P 500 SPX, +1.75%

rose 66.06 points, or 1.8%, to end at 3,849.28.

Dow Jones Industrial Average DJIA, +1.05%

added 345.09 points, or 1.1%, finishing at 33,220.80.

Nasdaq Composite COMP, +2.59%

climbed 264.80 points, or 2.6%, to finish at 10,478.09.

On Wednesday, the Nasdaq Composite dropped 1.4% to 10,213, its lowest closing level of the year. The S&P 500 is up more than 6% from its 2022 low from mid-October, but the large-cap index remains down 19.2% year-to-date, FactSet data show.

What drove markets

The penultimate session of 2022 showed tentative signs of delivering some much needed festive cheer for the stock market as a hope for “Santa Claus rally” had earlier failed to materialize.

The jobless-claims data “points to a loosening in the labor market, which is welcome news for the Fed,” said Larry Adam, chief investment officer at Raymond James, in a tweet.

However, analysts at Citi still think the claims data indicates a still-very-tight labor markets compared to historical levels.

“While both initial and continuing claims increased this week, they remain within the levels of late 2019,” wrote Gisela Hoxha, U.S. economics research analyst at Citi. “Anecdotes of company layoffs have increased in recent months, particularly in the tech sector. While it could be hard to disentangle the seasonal effects from the announced layoffs, in our view there is no significant evidence of them showing up in the claims data yet.”

Some of those layoffs could be taking effect a couple months later as employees might be kept on payroll for some time after the announcement, which will become significant signs of weakness in the labor market in 2023, Hoxha added.

Stocks were on track to finish what’s set to be the worst year since 2008 not far from 2022 lows. The S&P 500’s 52-week closing low at 3,577.03 was hit on Oct. 12.

Still, the three indexes managed to erase losses from earlier in the week on Thursday. Nasdaq Composite was down 0.2% this week, while the S&P 500 gained 0.1% and the Dow was nearly flat as of Thursday’s close. If the S&P 500 can hold on to weekly gains through Friday, it would mark the end of a three-week losing streak that has been the index’s longest since September, FactSet data show.

Companies in focus

Tesla Inc. TSLA, +8.08%

shares finished 8.1% higher on Thursday after posting its first rise in eight sessions Wednesday. The electric-vehicle maker’s shares had declined in seven consecutive sessions, their worst losing streak since a seven-session run that ended on Sept. 15, 2018.

Southwest Airlines LUV, +3.70%

remains in focus as the airline tries to recover from logistical issues that caused thousands of flight cancellations over the past week. The stock fell 11% over the past two days, but rose 3.7% in Thursday session.

General Electric’s GE, +2.17%

spinoff of GE HealthCare Technologies will join the S&P 500 index when it begins trading as a separate public company on Jan. 4. GE HealthCare will replace Vornado Realty Trust VNO, +1.63%,

which will move to the S&P MidCap 400. Vornado will replace logistics company RXO RXO, +8.39%,

which will move to the S&P SmallCap 600. GE HealthCare — trading on a when-issued basis — rose 0.9%, while Vornado gained 1.6% and RXO jumped 8.4%.

Cal-Maine CALM, -14.50%

shares ended 14.5% lower after its quarterly earnings came in below Wall Street forecasts. Cal-Maine reported record sales for the quarter as an avian flu outbreak continued to limit the supply of eggs, driving prices sharply higher. The company also said there were no positive tests for avian flu at any of its production facilities, as of Wednesday.

Harris Kupperman, the president of Praetorian Capital, made a couple of interesting calls heading into 2022. He predicted that stocks of the giant tech-oriented companies that led the bull market would be sold off, and that oil prices would continue to rise through the end of 2022.

The first prediction came true, while the second one for oil prices fizzled. After rising to $130 in March, oil prices have fallen back to where they started the year. Then again, that second prediction still could have made you a lot of money because the share prices of oil companies kept rising anyway.

That leads to a new prediction for 2023 and a related stock screen below.

Here’s a chart showing the movement of front-month contract prices for West Texas Intermediate (WTI) crude oil CL.1, -0.62%

since the end of 2021:

FactSet

Even though Kupperman didn’t get his oil price call right, the energy sector of the S&P 500 SPX, -1.20%

was up 60% for 2022 through Dec. 27, excluding dividends. That is the only one of the 11 S&P 500 sectors to show a gain in 2022. And the energy sector is also cheapest relative to earnings expectations, with a forward price-to-earnings ratio of 9.8, compared with 16.7 for the full S&P 500.

WTI pulled back from its momentary peak at $130.50 in early March, but that didn’t reverse the long-term trend of low capital spending by oil and natural gas producers, which has given investors confidence that supplies will remain tight.

Vicki Hollub, the CEO of Occidental Petroleum Corp. OXY, -3.50%

— the best-performing S&P 500 stock of 2022 — said during a recent interview that there was “no pressure to increase production right now,” citing a $40 per barrel break-even point for oil prices.

At the end of November, these 20 oil companies stood out as reasonable plays for 2023 based on expectations for free-cash-flow generation and dividend payments.

For this next screen, we are only looking at ratings and consensus price targets among analysts polled by FactSet.

There are 23 energy stocks in the S&P 500, and you can invest in that group easily by purchasing shares of the Energy Select SPDR ETF XLE, -2.24%.

We can expand the list of large-cap names by looking at the components of the iShares Global Energy ETF IXC, -1.91%,

which holds all the energy stocks in the S&P 500 plus large players based outside the U.S.

Prices on the tables in this article are in local currencies.

IXC holds 51 stocks. To expand the list for a stock screen, we added the energy stocks in the S&P 400 Mid Cap Index MID, -1.24%

and the S&P Small Cap 600 Index SML, -1.89%

to bring the list up to 91 companies, which we then pared to 83 covered by at least five analysts polled by FactSet.

Here are the 20 companies in the list with at least 75% “buy” or equivalent ratings that have the most upside potential over the next 12 months, based on consensus price targets:

Elon Musk has been trying this week to defend Tesla’s abysmal stock performance in 2022. The electric vehicle giant has seen its stock plummet by 61% this year, making it the 11th-worst performing stock in the S&P 500 in 2022.

“As bank savings account interest rates, which are guaranteed, start to approach stock market returns, which are *not* guaranteed, people will increasingly move their money out of stocks into cash, thus causing stocks to drop,” Musk tweeted.

You might expect that Tesla’s stock drop has wiped out more investor wealth than any other stock in the world this year. But you would be wrong.

If we look at declines in market capitalization — the value of companies’ common-shares outstanding — Tesla TSLA, -1.76%

has been the fourth worst-performing stock in the benchmark S&P 500 this year, as of 1 p.m. ET on Dec. 21:

On a percentage basis, all these stocks have performed worse than the full S&P 500, which has fallen 19%, excluding dividends.

Amazon.com Inc. AMZN, +1.74%

has erased more shareholder wealth than any other publicly traded company in 2022. In total, investors in Amazon have lost $804.6 billion this year. The stock is down 48% in 2022.

Apple Inc. AAPL, -0.28%

and Microsoft Corp. MSFT, +0.23%

have also suffered larger market-cap declines than Tesla, by virtue of their sheer size.

The companies have different fiscal and annual period ends, but if we look at data for the past three reported quarters and compare to the same period a year earlier, here’s how the four stack up:

Company

Ticker

Change in sales for three quarters from year-earlier period

Change in EPS for three quarters from year-earlier period

Amazon showed a net loss of $3 billion for the first three quarters of 2022 as the company neared the end of its extraordinary multiyear effort to build out its warehouse and fulfillment infrastructure. For the first three quarters of 2021, the company booked $19 billion in profits. When announcing Amazon’s third-quarter results CEO Andy Jassy said the company was working methodically toward “a stronger cost structure for the business moving forward.”

The incredible growth of Amazon’s cloud business has stalled and disappointed the expectations the company had nurtured on Wall Street. The Amazon Web Services business is facing increasing competition from the likes of Microsoft and its customers are pulling back. Meanwhile, retail sales have also come in weak going into the Christmas and holiday season.

Amazon’s stock has declined 22% since it closed at $110.96 on Oct. 27, right before it disappointed investors not only with its third-quarter results, but with its outlook: It expects to break even during the holiday quarter. Analysts polled by FactSet had previously expected a profit of more than $5 billion.

Tesla stands in contrast to Amazon, as you can see on the table above. Its sales grew by 58% during the first three quarters of 2022 from the year-earlier period and its earnings per share rose nearly threefold.

This has been a year of significant declines for shares of giant tech-oriented companies, especially those that had traded at lofty price-to-earnings valuations — that group includes Amazon and Tesla. In fact, these companies have given up all their pandemic era gains int he stock market.

But with Tesla’s results so outstanding through the first three quarters of 2022, it raises the question: How much of the drop in the electric car makers share price was tied to Musk’s actions as CEO of Twitter, which he acquired on Oct. 27 after a monthslong saga? And how much of a relief rally, if any, might there be for Tesla if Musk, as expected, steps down as Twitter CEO?

How about some bottom-feeding?

Here’s the same list of 10 stocks in the S&P 500 that have seen the largest declines in market cap this year, with a summary of analysts’ ratings, consensus price targets and declines in their forward price-to-earnings ratios:

Investors love dividend stocks but there are different ways to look at them, including various “quality” approaches. Today we are focusing on high yields.

A high dividend yield can be a warning that investors have lost confidence in a company’s ability to maintain its dividend payout. But there are always exceptions, some of which can be brought about by market events — some investors remain skeptical of energy stocks, for example, after so much pain before this year’s outstanding performance for the sector.

Below is a screen of stocks that have high dividend yields and are favored by analysts. The screen has no financial quality filters.

For investors who are interested in dividend stocks but wish to focus on quality and total returns, this recent look at the S&P Dividend Aristocrats (companies that have raised dividends consistently for many years) might be of interest. For those looking for income but also worried about dividend cuts, here is a list of stocks with dividend yields of at least 5% whose payouts are expected to be well-covered by free cash flow in 2023.

Removing the filters for a high-yield dividend-stock screen

For a broad screen of stocks with high dividend yields that are favored by analysts, we began with the S&P Composite 1500 Index SP1500, +1.42%,

which is made up of the S&P 500 SPX, +1.42%,

the S&P 400 Mid Cap Index MID, +1.48%,

and the S&P 600 Small Cap Index SML, +1.49%.

The S&P indexes exclude energy partnerships, so we added the 15 stocks held by the Alerian MLP ETF AMLP, +1.81%

to the list. Energy partnerships tend to have high distribution yields, in part because they pass most earnings through to investors. But they also can make tax preparation more complicated. They can also be volatile as oil CL00, +2.96%

CL00 and natural-gas NG00, +1.58%

prices swing.

The S&P indexes also exclude business development companies, or BDCs, so we expanded our initial screen to include the 24 stocks held by the VanEck BDC income ETF BIZD, +0.76%.

BDCs are specialized leveraged lenders that make loans with high interest rates, mainly to middle-market companies. They often take equity stakes in the companies they lend to, for a venture-capital-type of investment style. The BDC space features several stocks with very high dividend yields, but is also known for volatility.

You have been warned — this particular stock screen focuses only on high yields and favorable ratings among analysts working for brokerage firms. There is no look back at dividend cuts and no cash-flow analysis as featured in other dividend-stock articles. If you see anything of interest resulting from the screen, you need to do your own research to consider whether or not a long-term commitment to one or more of these companies is worth the risk as you seek high income.

The screen

Starting with the S&P Composite 1500 and the components of AMLP and BIZD, there are 68 stocks with dividend yields of at least 8%, according to data provided by FactSet.

Among the 68 companies, 55 made the first screen, because they are covered by at least five analysts polled by FactSet.

Among the 55 companies, 11 have “buy” or equivalent ratings among at least 70% of analysts.

Here they are, ranked by upside potential implied by analysts’ consensus price targets:

Following a sharp and sustained rise in interest rates, U.S. stocks have taken a broad beating this year.

But 2023 may bring very different circumstances.

Below are lists of analysts’ favorite stocks among the benchmark S&P 500 SPX,

the S&P 400 Mid Cap Index MID

and the S&P Small Cap 600 Index SML

that are expected to rise the most over the next year. Those lists are followed by a summary of opinions of all 30 stocks in the Dow Jones Industrial Average DJIA.

Stocks rallied on Dec. 13 when the November CPI report showed a much slower inflation pace than economists had expected. Investors were also anticipating the Federal Open Market Committee’s next monetary policy announcement on Dec. 14. The consensus among economists polled by FactSet is for the Federal Reserve to raise the federal funds rate by 0.50% to a target range of 4.50% to 4.75%.

A 0.50% increase would be a slowdown from the four previous increases of 0.75%. The rate began 2022 in a range of zero to 0.25%, where it had sat since March 2020.

A pivot for the Fed Reserve and the possibility that the federal funds rate will reach its “terminal” rate (the highest for this cycle) in the near term could set the stage for a broad rally for stocks in 2023.

Wall Street’s large-cap favorites

Among the S&P 500, 92 stocks are rated “buy” or the equivalent by at least 75% of analysts working for brokerage firms. That number itself is interesting — at the end of 2021, 93 of the S&P 500 had this distinction. Meanwhile, the S&P 500 has declined 16% in 2022, with all sectors down except for energy, which has risen 53%, and the utilities sector, which his risen 1% (both excluding dividends).

Here are the 20 stocks in the S&P 500 with at least 75% “buy” or equivalent ratings that analysts expect to rise the most over the next year, based on consensus price targets:

Most of the companies on the S&P 500 list expected to soar in 2023 have seen large declines in 2022. But the company at the top of the list, EQT Corp. EQT,

is an exception. The stock has risen 69% in 2022 and is expected to add another 62% over the next 12 months. Analysts expect the company’s earnings per share to double during 2023 (in part from its expected acquisition of THQ), after nearly a four-fold EPS increase in 2022.

Shares of Amazon.com Inc. AMZN

are expected to soar 50% over the next year, following a decline of 46% so far in 2022. If the shares were to rise 50% from here to the price target of $136.02, they would still be 18% below their closing price of 166.72 at the end of 2021.

You can see the earnings estimates and more for any stock in this article by clicking on its ticker.

Click here for Tomi Kilgore’s detailed guide to the wealth of information available for free on the MarketWatch quote page.

Mid-cap stocks expected to rise the most

The lists of favored stocks are limited to those covered by at least five analysts polled by FactSet.

Among components of the S&P 400 Mid Cap Index, there are 84 stocks with at least 75% “buy” ratings. Here at the 20 expected to rise the most over the next year:

Among companies in the S&P Small Cap 600 Index, 91 are rated “buy” or the equivalent by at least 75% of analysts. Here are the 20 with the highest 12-month upside potential indicated by consensus price targets:

What worked well during the years-long bull market through 2021 — a focus on growth, regardless of price — has ground to a halt this year. The rebirth of the value style of investing — and modest valuations overall — has taken hold.

The approach taken by the Invesco S&P 500 GARP ETF has paid off through both bull and bear markets.

Let’s begin with a 10-year chart comparing total returns with dividends reinvested for the Invesco S&P 500 GARP ETF SPGP, +0.67%

and the SPDR S&P 500 ETF Trust SPY, +0.78%,

which tracks the benchmark S&P 500:

FactSet

So far this year, SPGP is down 12%, while SPY is down 16%. But the long-term chart shows significant and consistent outperformance for SPGP, even during the bull market.

The S&P 500 GARP Index

GARP stands for “growth at a reasonable price.” SPGP tracks the S&P 500 GARP Index, which is reconstituted and rebalanced twice a year, on the third Fridays of June and December. The next change occurs Dec. 16.

S&P Dow Jones Indices assigns a growth score to each component of the S&P 500 by averaging the three-year compound annual growth rate (CAGR) for earnings and sales per share.

The top 150 components of the S&P 500 by growth score are eligible for inclusion in the GARP index. Those 150 are ranked by “quality/value composite score,” which is the average of these three ratios:

Financial leverage — total debt to book value.

Return on equity — trailing 12 months’ earnings per share divided by book value per share.

Earnings-to-price — 12 months’ earnings per share divided by the share price.

The top 75 of the 150 by QV rankings are then included in the GARP index and weighted by the growth score, with portfolio weightings ranging from 0.5% to 5%.

There is a weighting limitation of 40% to any one of the 11 S&P sectors.

Addressing concentration risk

The benchmark S&P 500 Index SPX, +0.75%

is weighted by market capitalization, which means it is more heavily concentrated than you might expect — success is rewarded, with rising stocks more heavily weighted over time.

That can backfire during a bear market, with Amazon.com Inc. AMZN, +2.14%

down 47% and Tesla Inc. TSLA, -0.34%

down 51% this year, to name two prominent examples.

Looking at the SPDR S&P 500 ETF Trust SPY, +0.78%,

which is the first and largest exchange traded fund and tracks the benchmark index by holding all of its components, six companies (Apple Inc. AAPL, +1.21%,

Microsoft Corp. MSFT, +1.24%,

Amazon, both common share classes of Alphabet Inc. GOOGL, -1.30%

That percentage has come down this year, but a lot of risk remains concentrated in a handful of companies. (Apple alone makes up 6.4% of the SPY portfolio. Tesla is now the ninth-largest holding, making up 1.4% of the portfolio.)

One way to address high concentration in an index fund is to use an equal-weighted approach, which Mark Hulbert recently discussed.

For the Invesco S&P 500 GARP ETF, the underlying index’s selection methodology has resulted in much less portfolio concentration than we see in SPY, with the top five holdings making up 10.9% of the portfolio.

NEW YORK — Donald Trump’s company was convicted of tax fraud on Tuesday in a case brought by the Manhattan District Attorney, a significant repudiation of financial practices at the former president’s business.

A jury found two corporate entities at the Trump Organization guilty on all 17 counts, including conspiracy charges and falsifying business records.

The verdict came on the second day of deliberations following a trial in which the Trump Organization was accused of being complicit in a scheme by top executives to avoid paying personal income taxes on job perks such as rent-free apartments and luxury cars.

The conviction is a validation for New York prosecutors, who have spent three years investigating the former president and his businesses, though the penalties aren’t expected to be severe enough to jeopardize the future of Trump’s company.

As punishment, the Trump Organization could be fined up to $1.6 million — a relatively small amount for a company of its size, though the conviction might make some of its future deals more complicated.

Trump, who recently announced he was running for president again, has said the case against his company was part of a politically motivated “witch hunt” waged against him by vindictive Democrats.

Trump himself was not on trial but prosecutors alleged he “knew exactly what was going on” with the scheme, though he and the company’s lawyers have denied that.

The case against the company was built largely around testimony from the Trump Organization’s former finance chief, Allen Weisselberg, who previously pleaded guilty to charges that he manipulated the company’s books and his own compensation package to illegally reduce his taxes.

Weisselberg testified in exchange for a promised five-month jail sentence.

To convict the Trump Organization, prosecutors had to convince jurors that Weisselberg or his subordinate, Senior Vice President and Controller Jeffrey McConney, were “high managerial” agents acting on the company’s behalf and that the company also benefited from his scheme.

Trump Organization lawyers repeated the mantra “Weisselberg did it for Weisselberg” throughout the monthlong trial. They contended the executive had gone rogue and betrayed the company’s trust. No one in the Trump family or the company was to blame, they argued.

Though he testified as a prosecution witness, Weisselberg also attempted to take responsibility on the witness stand, saying nobody in the Trump family knew what he was doing.

“It was my own personal greed that led to this,” an emotional Weisselberg testified.

Weisselberg, who pleaded guilty to dodging taxes on $1.7 million in fringe benefits, testified that he and McConney conspired to hide that extra compensation from his income by deducting their cost from his pre-tax salary and issuing falsified W-2 forms.

During his closing argument, prosecutor Joshua Steinglass attempted to refute the claim that Trump knew nothing about the scheme. He showed jurors a lease Trump signed for Weisselberg’s company-paid apartment and a memo Trump initialed authorizing a pay cut for another executive who got perks.

“Mr. Trump is explicitly sanctioning tax fraud,” Steinglass argued.

The verdict doesn’t end Trump’s battle with Manhattan District Attorney Alvin Bragg, a Democrat who took office in January.

Bragg has said that a related investigation of Trump that began under his predecessor, District Attorney Cyrus Vance Jr., is “active and ongoing.”

In that wide-ranging probe, investigators have examined whether Trump misled banks and others about the value of his real estate holdings, golf courses and other assets — allegations at the heart of New York Attorney General Letitia James’ pending lawsuit against the former president and his company.

The district attorney’s office has also investigated whether any state laws were broken when Trump’s allies made payments to two women who claimed to have had sexual affairs with the Republican years ago.

Near the end of his tenure last year, Vance directed deputies to present evidence to a grand jury for a possible indictment of Trump. After taking office, though, Bragg let that grand jury disband so he could give the case a fresh look.

On Monday, he confirmed that a new lead prosecutor had been brought on to handle that investigation, signaling again that it was still active.

The S&P 500 and Nasdaq Composite indexes recorded their worst day in almost a month on Monday,after a hotter-than-expected U.S. services-sector reading fueled concerns that the Federal Reserve may need to be even more aggressive in its inflation battle.

How stocks traded

The Dow Jones Industrial Average DJIA, -0.26%

finished down 482.78 points, or 1.4%, at 33,947.10.

The S&P 500 SPX, -1.79%

ended 72.86 points lower, or 1.8%, at 3,998.84.

The Nasdaq Composite COMP, -11.01% closed down 221.56 points, or 1.9%, at 11,239.94.

Those were the largest declines for the S&P 500 and Nasdaq Composite since Nov. 9, according to Dow Jones Market Data.

Strong wage growth numbers released Friday were followed up on Monday by a robust reading for the U.S. services sector — both of which helped to stoke fears that the Fed’s interest-rate hikes, along with the central bank’s modest balance-sheet unwind, haven’t had much of an impact on the tight labor market.

“If nothing else, the ISM services report is being interpreted as very strong, and thus the economy is overheating and that means more Fed tightening,” said Will Compernolle, a senior economist at FHN Financial in New York. “Consumer resilience has proven to be more intense than I would have expected. In the two most interest-rate sensitive sectors — housing and autos — tightening has channeled into markets in meaningful ways.”

But there has been so much pent-up demand, that higher interest rates haven’t been cooling overall spending as much as the Fed would like because companies are still having to fill a backlog of orders, he said via phone.

In other economic data, the final November S&P Global U.S. services PMI edged up to 46.2 from 46.1, but remained in contractionary territory.

November jobs data released on Friday showed average hourly wages grew over the past year by more than 5% as of November, beating economists’ expectations and stoking concerns that robust wage growth would continue to fuel inflation, market strategists said.

Worries about a more-aggressive Fed also helped to drive Treasury yields higher, adding to the pressure on stocks. The yield on the 10-year note rose 9.6 basis points to 3.6% on Monday. Treasury yields move inversely to prices, and yields had fallen sharply over the past month, driven by shifting expectations about the pace of Fed rate hikes.

Monday’s ISM services figure “surprised to the upside, suggesting that the economy is still running above its long-run sustainable path and that the Fed is going to have to slow the economy more than expected in 2023,” Bill Adams, the Dallas-based chief economist for Comerica Inc. CMA, said via phone.

Meanwhile, oil futures ended lower on Monday, a day after Sunday’s decision by OPEC and its allies to keep production quotas unchanged.

Falling equity prices helped drive the CBOE Volatility Index VIX, +8.87%,

also known as the VIX, back above 20 on Monday. The volatility gauge had fallen sharply in recent weeks as stocks rallied, potentially signaling complacency that could ultimately hurt stocks, said Jonathan Krinsky, chief market technician at BTIG, in a note to clients.

GameStop Corp.‘s Class A shares GME, -7.12%

ended down by 7.1% ahead of the company’s third-quarter results, which are set to be released after the market closes on Wednesday. Analysts are looking for a narrowing loss from the videogame retailer.

Shares of U.S. airlines and aircraft makers traded higher on Monday, bucking the broader trend in stocks. Boeing Co. BA, +1.22%

and United Airlines Holdings Inc. UAL, +2.60%

were among the best performers in the S&P 500, finishing up by 1.2% and 2.6%, respectively.

Salesforce Inc. performed better than expected in the third quarter, but executives issued a fourth-quarter forecast that fell short of expectations on Wednesday and revealed that co-Chief Executive Bret Taylor is leaving the company.

Salesforce CRM, +5.65%

shares fell about 7% after hours, after rising about 5.5% in the regular session to close at $159.97, their fifth gain in the past six sessions.

The cloud-software company said in a news release that founder, co-CEO and Chairman Marc Benioff will resume the sole CEO role on Jan. 31. Taylor is the second executive to be elevated to co-CEO with Benioff, only to leave with Benioff still in charge. Keith Block stepped down in February 2020 after just 18 months in the position, and Taylor lasted exactly a year in the co-CEO position after being promoted Nov. 30 of last year.

“I am grateful for six fantastic years at Salesforce,” Taylor, who was also vice chairman, said in a statement. “Marc was my mentor well before I joined Salesforce and the opportunity to partner with him to lead the most important software company in the world is career-defining. After a lot of reflection, I’ve decided to return to my entrepreneurial roots.”

On the company’s earnings call, Benioff said “we’re still in a little bit of shock and extremely sad” about Taylor’s exit, but did not answer an analyst’s question about whether he would fill the co-CEO position.

At least one analyst said he didn’t see the departure coming: “Given that Mr. Taylor was assumed to be the ‘heir apparent’ at CRM, this does bring up a lot of questions in terms of the management team and frankly offsets some of the positive narrative around margins heading into [calendar year 2023],” wrote Kirk Materne, analyst for Evercore ISI, in a note Wednesday.

Salesforce reported that third-quarter net income fell to $210 million, or 21 cents a share, compared with $468 million, or 47 cents a share, in the year-ago period. Adjusted for stock-based compensation and other costs, earnings were $1.40 a share. Revenue rose to $7.84 billion from $6.86 billion in the year-ago quarter.

“We remain positive on the long-term outlook for Salesforce as front-office applications leader,” Michael Turits, analyst for KeyBanc Capital Markets, wrote ahead of the company’s earnings report. “That said, we remain cautious regarding the near-term outlook given ongoing recession concerns, slowing cloud spend, and weaker conversations we had with a few Salesforce channels this quarter.”

Those concerns sprung up in the company’s forecast, as Salesforce executives’ guidance fell $900 million short of expectations. They expect fourth-quarter earnings of 23 cents to 25 cents a share on revenue in the range of $7.932 billion to $8.032 billion, and adjusted earnings of $1.35 to $1.37 a share. Analysts had forecast adjusted earnings of $1.44 a share on revenue of $8.94 billion.

Chief Financial Officer Amy Weaver said on the earnings call that along with the “unpredictable” macroeconomic environment and some slowing in customer spending, the strong dollar had an impact on the company’s showing. “Foreign exchange continued to be a headwind for our results,” she said.

Still, Weaver said the company remains committed to a goal of operating margins of 25% or above; in the third quarter it was at 22.7%, which she said was a record high. Among the things the company is doing, she said, is taking a measured approach to hiring. Earlier this month, the company confirmed hundreds of layoffs, though it did not address them during the call.

In response to an analyst’s question about employees working from home and the company’s real-estate footprint, Benioff said the San Francisco-based company will have more employees in the office while maintaining the flexibility of remote work. “We’re never going back to how it was, we all know that,” he said. Meanwhile, Weaver said the company is “looking at every aspect of our real estate .”

Shares of Salesforce have declined about 37% this year. The Dow Jones Industrial Average DJIA, +2.18%,

whose 30 components include Salesforce, has fallen about 5% year to date, while the S&P 500 index SPX, +3.09%

is down almost 15% this year.

Income-seeking investors are looking at an opportunity to scoop up shares of real estate investment trusts. Stocks in that asset class have become more attractive as prices have fallen and cash flow is improving.

Below is a broad screen of REITs that have high dividend yields and are also expected to generate enough excess cash in 2023 to enable increases in dividend payouts.

REIT prices may turn a corner in 2023

REITs distribute most of their income to shareholders to maintain their tax-advantaged status. But the group is cyclical, with pressure on share prices when interest rates rise, as they have this year at an unprecedented scale. A slowing growth rate for the group may have also placed a drag on the stocks.

And now, with talk that the Federal Reserve may begin to temper its cycle of interest-rate increases, we may be nearing the time when REIT prices rise in anticipation of an eventual decline in interest rates. The market always looks ahead, which means long-term investors who have been waiting on the sidelines to buy higher-yielding income-oriented investments may have to make a move soon.

During an interview on Nov 28, James Bullard, president of the Federal Reserve Bank of St. Louis and a member of the Federal Open Market Committee, discussed the central bank’s cycle of interest-rate increases meant to reduce inflation.

When asked about the potential timing of the Fed’s “terminal rate” (the peak federal funds rate for this cycle), Bullard said: “Generally speaking, I have advocated that sooner is better, that you do want to get to the right level of the policy rate for the current data and the current situation.”

Fed’s Bullard says in MarketWatch interview that markets are underpricing the chance of still-higher rates

In August we published this guide to investing in REITs for income. Since the data for that article was pulled on Aug. 24, the S&P 500 SPX, -0.29%

has declined 4% (despite a 10% rally from its 2022 closing low on Oct. 12), but the benchmark index’s real estate sector has declined 13%.

REITs can be placed broadly into two categories. Mortgage REITs lend money to commercial or residential borrowers and/or invest in mortgage-backed securities, while equity REITs own property and lease it out.

The pressure on share prices can be greater for mortgage REITs, because the mortgage-lending business slows as interest rates rise. In this article we are focusing on equity REITs.

Industry numbers

The National Association of Real Estate Investment Trusts (Nareit) reported that third-quarter funds from operations (FFO) for U.S.-listed equity REITs were up 14% from a year earlier. To put that number in context, the year-over-year growth rate of quarterly FFO has been slowing — it was 35% a year ago. And the third-quarter FFO increase compares to a 23% increase in earnings per share for the S&P 500 from a year earlier, according to FactSet.

The NAREIT report breaks out numbers for 12 categories of equity REITs, and there is great variance in the growth numbers, as you can see here.

FFO is a non-GAAP measure that is commonly used to gauge REITs’ capacity for paying dividends. It adds amortization and depreciation (noncash items) back to earnings, while excluding gains on the sale of property. Adjusted funds from operations (AFFO) goes further, netting out expected capital expenditures to maintain the quality of property investments.

The slowing FFO growth numbers point to the importance of looking at REITs individually, to see if expected cash flow is sufficient to cover dividend payments.

Screen of high-yielding equity REITs

For 2022 through Nov. 28, the S&P 500 has declined 17%, while the real estate sector has fallen 27%, excluding dividends.

Over the very long term, through interest-rate cycles and the liquidity-driven bull market that ended this year, equity REITs have fared well, with an average annual return of 9.3% for 20 years, compared to an average return of 9.6% for the S&P 500, both with dividends reinvested, according to FactSet.

This performance might surprise some investors, when considering the REITs’ income focus and the S&P 500’s heavy weighting for rapidly growing technology companies.

For a broad screen of equity REITs, we began with the Russell 3000 Index RUA, -0.04%,

which represents 98% of U.S. companies by market capitalization.

We then narrowed the list to 119 equity REITs that are followed by at least five analysts covered by FactSet for which AFFO estimates are available.

If we divide the expected 2023 AFFO by the current share price, we have an estimated AFFO yield, which can be compared with the current dividend yield to see if there is expected “headroom” for dividend increases.

For example, if we look at Vornado Realty Trust VNO, +1.03%,

the current dividend yield is 8.56%. Based on the consensus 2023 AFFO estimate among analysts polled by FactSet, the expected AFFO yield is only 7.25%. This doesn’t mean that Vornado will cut its dividend and it doesn’t even mean the company won’t raise its payout next year. But it might make it less likely to do so.

Among the 119 equity REITs, 104 have expected 2023 AFFO headroom of at least 1.00%.

Here are the 20 equity REITs from our screen with the highest current dividend yields that have at least 1% expected AFFO headroom:

Click on the tickers for more about each company. You should read Tomi Kilgore’s detailed guide to the wealth of information for free on the MarketWatch quote page.

The list includes each REIT’s main property investment type. However, many REITs are highly diversified. The simplified categories on the table may not cover all of their investment properties.

Knowing what a REIT invests in is part of the research you should do on your own before buying any individual stock. For arbitrary examples, some investors may wish to steer clear of exposure to certain areas of retail or hotels, or they may favor health-care properties.

Largest REITs

Several of the REITs that passed the screen have relatively small market capitalizations. You might be curious to see how the most widely held REITs fared in the screen. So here’s another list of the 20 largest U.S. REITs among the 119 that passed the first cut, sorted by market cap as of Nov. 28:

The numbers: Construction on new houses fell 4.2% in October as high mortgage rates put off buyers and forced builders to scale back, a situation that’s likely to continue through 2023.

U.S. housing starts slowed to an annual pace of 1.43 million last month from 1.49 million in September. That figure reflects how many homes would be built in 2022 if construction took place at same rate over the entire year as it did in October.

Economists polled by MarketWatch had expected housing starts to register a rate of 1.41 million after adjusting for the typical seasonal swings in demand.

New construction hit a record 1.8 million in April before tapering off.

The number of permits, meanwhile, slipped 2.4% to a rate of 1.53 million, down sharply from a record 1.9 million last December.

Permits foreshadow how many houses are likely to be built in the months ahead, assuming a stable real estate market. But a major increase in mortgage rates this year has depressed demand and forced builders to scale back plans.

Key details: Single-family home construction fell 6.1% to an annual rate of 855,000 in October. Projects with five units or more registered a 556,000 rate, little changed from the prior month.

Housing starts are down 9% from a year ago, when mortgage rates briefly dipped below 3%.

Permits have fallen 10% from a year earlier.

Big picture: The highest mortgage rates in several decades have stifled new construction and are likely to do so through the next year or longer. The rate on a 30-year fixed mortgage recently topped 7%, more than double the rate a year ago.

While the U.S. has an acute need for more housing, fewer people can now afford to buy a home. Home prices are starting to come off record highs, but not by much.

Looking ahead: “Higher mortgage rates continue to exact a heavy toll on new construction,” said Richard Moody, chief economist of Regions Financial.

Market reaction:The Dow Jones Industrial Average DJIA, -0.18%

and S&P 500 SPX, -1.01%

fell in Thursday trades.

Investors cheered when a report last week showed the economy expanded in the third quarter after back-to-back contractions.

But it’s too early to get excited, because the Federal Reserve hasn’t given any sign yet that it is about to stop raising interest rates at the fastest pace in decades.

Below is a list of dividend stocks that have had low price volatility over the past 12 months, culled from three large exchange traded funds that screen for high yields and quality in different ways.

In a year when the S&P 500 SPX, -0.40%

is down 18%, the three ETFs have widely outperformed, with the best of the group falling only 1%.

That said, last week was a very good one for U.S. stocks, with the S&P 500 returning 4% and the Dow Jones Industrial Average DJIA, -0.32%

having its best October ever.

This week, investors’ eyes turn back to the Federal Reserve. Following a two-day policy meeting, the Federal Open Market Committee is expected to make its fourth consecutive increase of 0.75% to the federal funds rate on Wednesday.

The inverted yield curve, with yields on two-year U.S. Treasury notes TMUBMUSD02Y, 4.540%

exceeding yields on 10-year notes TMUBMUSD10Y, 4.064%,

indicates investors in the bond market expect a recession. Meanwhile, this has been a difficult earnings season for many companies and analysts have reacted by lowering their earnings estimates.

The weighted rolling consensus 12-month earning estimate for the S&P 500, based on estimates of analysts polled by FactSet, has declined 2% over the past month to $230.60. In a healthy economy, investors expect this number to rise every quarter, at least slightly.

Low-volatility stocks are working in 2022

Take a look at this chart, showing year-to-date total returns for the three ETFs against the S&P 500 through October:

FactSet

The three dividend-stock ETFs take different approaches:

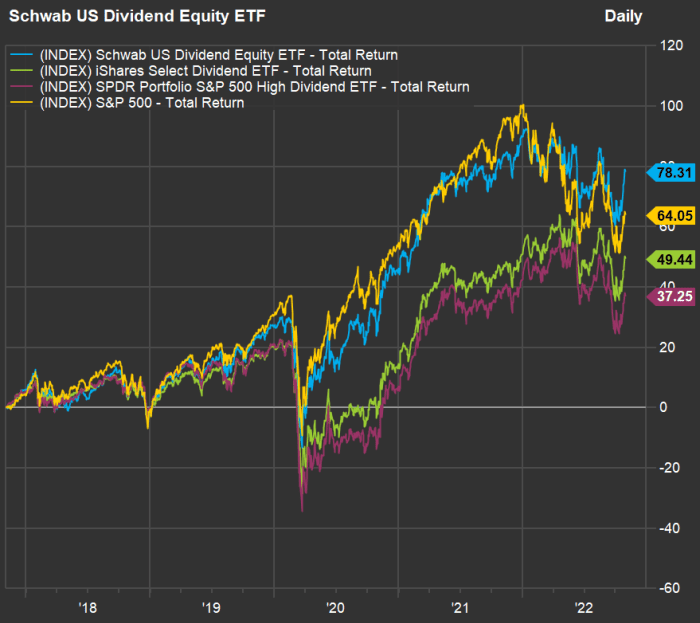

The $40.6 billion Schwab U.S. Dividend Equity ETF SCHD, +0.15%

tracks the Dow Jones U.S. Dividend 100 Indexed quarterly. This approach incorporates 10-year screens for cash flow, debt, return on equity and dividend growth for quality and safety. It excludes real estate investment trusts (REITs). The ETF’s 30-day SEC yield was 3.79% as of Sept. 30.

The iShares Select Dividend ETF DVY, +0.45%

has $21.7 billion in assets. It tracks the Dow Jones U.S. Select Dividend Index, which is weighted by dividend yield and “skews toward smaller firms paying consistent dividends,” according to FactSet. It holds about 100 stocks, includes REITs and looks back five years for dividend growth and payout ratios. The ETF’s 30-day yield was 4.07% as of Sept. 30.

The SPDR Portfolio S&P 500 High Dividend ETF SPYD, +0.60%

has $7.8 billion in assets and holds 80 stocks, taking an equal-weighted approach to investing in the top-yielding stocks among the S&P 500. It’s 30-day yield was 4.07% as of Sept. 30.

All three ETFs have fared well this year relative to the S&P 500. The funds’ beta — a measure of price volatility against that of the S&P 500 (in this case) — have ranged this year from 0.75 to 0.76, according to FactSet. A beta of 1 would indicate volatility matching that of the index, while a beta above 1 would indicate higher volatility.

Now look at this five-year total return chart showing the three ETFs against the S&P 500 over the past five years:

FactSet

The Schwab U.S. Dividend Equity ETF ranks highest for five-year total return with dividends reinvested — it is the only one of the three to beat the index for this period.

Screening for the least volatile dividend stocks

Together, the three ETFs hold 194 stocks. Here are the 20 with the lowest 12-month beta. The list is sorted by beta, ascending, and dividend yields range from 2.45% to 8.13%:

Any list of stocks will have its dogs, but 16 of these 20 have outperformed the S&P 500 so far in 2022, and 14 have had positive total returns.

You can click on the tickers for more about each company. Click here for Tomi Kilgore’s detailed guide to the wealth of information available free on the MarketWatch quote page.

(BEP), Cameco agreed to buy Westinghouse Electric, a servicer to nuclear power plants, for $7.88 billion, including debt. Cameco will own 49% of the joint venture once the deal is completed.

When the stock market has jumped two days in a row, as it has now, it is easy to become complacent.

But the Federal Reserve isn’t finished raising interest rates, and recession talk abounds. Stock investors aren’t out of the woods yet. That can make dividend stocks attractive if the yields are high and the companies produce more cash flow than they need to cover the payouts.

Below is a list of 21 stocks drawn from the S&P Composite 1500 Index SP1500, +3.12%

that appear to fit the bill. The S&P Composite 1500 is made up of the S&P 500 SPX, +3.06%,

the S&P 400 Mid Cap Index MID, +3.18%

and the S&P Small Cap 600 Index SML, +3.80%.

The purpose of the list is to provide a starting point for further research. These stocks may be appropriate for you if you are looking for income, but you should do your own assessment to form your own opinion about a company’s ability to remain competitive over the next decade.

Cash flow is key

One way to measure a company’s ability to pay dividends is to look at its free cash flow yield. Free cash flow is remaining cash flow after planned capital expenditures. This money can be used to pay for dividends, buy back shares (which can raise earnings and cash flow per share), or fund acquisitions, organic expansion or for other corporate purposes.

If we divide a company’s estimated annual free cash flow per share by its current share price, we have its estimated free cash flow yield. If we compare the free cash flow yield to the current dividend yield, we may see “headroom” for cash to be deployed in ways that can benefit shareholders.

For this screen, we began with the S&P Composite 1500, then narrowed the list as follows:

Dividend yield of at least 5.00%.

Consensus free cash flow estimate available for calendar 2023, among at least five analysts polled by FactSet. We used calendar-year estimates, even though fiscal years for many companies don’t match the calendar.

Estimated 2023 free cash flow yield of at least double the current dividend yield.

For real-estate investment trusts, dividend-paying ability is measured by funds from operations (FFO), a non-GAAP figure that adds depreciation and amortization back to earnings. Adjusted funds from operations (AFFO) takes this a step further, subtracting cash expected to be used to maintain properties. So for the two REITs on the list, the FCF yield column makes use of AFFO.

For many companies in the financial sector, especially banks and insurers, free cash flow figures aren’t available, so the screen made use of earnings-per-share estimates. These are generally considered to run close to actual cash flow for these heavily regulated industries.

Here are the 21 companies that passed the screen, with dividend yields of at least 5% and estimated 2023 FCF yields at least twice the current payout. They are sorted by dividend yield:

Any stock screen has its limitations. If you are interested in stocks listed here, it is best to do your own research, and it is easy to get started by clicking the tickers in the table for more information about each company. Click here for Tomi Kilgore’s detailed guide to the wealth of information for free on the MarketWatch quote page.

For the “estimated FCF yields,” consensus free cash flow estimates for calendar 2023 were used for all companies except the following:

For the REITs, (Uniti Group Inc. UNIT, +7.36%

and Macerich Co. MAC, +8.18%

), consensus AFFO estimates were used.

Consensus EPS estimates were used for Prudential Financial Inc. PRU, +5.66%,

Invesco Ltd. IVZ, +6.76%

and Franklin Resources Inc. BEN, +4.37%.

Stocks declined again on Friday, closing out September with large losses across the board as the rally from the June lows partway through August faded into memory.

The S&P 500 SPX, -1.51%

fell 1.5% on Friday. The benchmark index slumped 9.3% for September, leading to a 2022 loss of 24.8%. The Dow Jones Industrial Average DJIA, -1.71%

gave up 1.7% on Friday, for a September decline of 8.8%. The Dow has now fallen 20.9% for 2022. The Nasdaq Composite Index COMP, -1.51%

pulled back 1.5% on Friday for a September drop of 10.5% and a year-to-date plunge of 32.4%. (All price changes in this article exclude dividends.)

Below is a list of stocks in the S&P 500 that fell the most during September.

Nike Inc. NKE, -12.81%

was down 13% on Friday for a September decline of 22%, after the company warned that discounting to clear inventory would continue to affect its earnings performance. Here’s how analysts reacted.