State planners have approved a $53 million plan for St George’s Anglican Grammar School to move 650m from its current William Street address in the Perth CBD so it can take in more students.

Perth Local Development Assessment Panel members approved the plans from landowner the Anglican Schools Commission Inc. to turn an office building at 441 Murray Street, Perth, into the secondary college’s new home.

The typical family’s 401(k) and IRA-type accounts come to less than half that goal in the years approaching retirement age, according to the nonprofit Employee Benefit Research Institute. Total household balances in retirement accounts for those 55 to 64 years old are $413,814 on average, according to its estimates based on 2019 data, the most recent available.

The living room of Apartment 3 at No.1 St.James. Styled and completed with vintage pieces, reclaimed … [+] textiles and consciously created designs.

Mark Anthony Fox / Obbard

Preserving the historical charm of a period property is a skill which is often overlooked and one which brings depth and soul to a residential space. In the case of property investment and development company Obbard, and design expert Kate Watson-Smyth, this was a critical factor in the recent redesign of No.1 St James, a block of residential apartments owned by, and situated above, the iconic London-based wine merchants Berry Bros. & Rudd.

The exterior of the iconic No.1 St James, designed and built in 1881-2 by architect Richard Norman … [+] Shaw.

Mark Anthony Fox / Obbard

The red brick, Grade II listed building, beautifully designed with its Portland Stone details (circa. 1881) by Richard Norman Shaw, was originally built as compact apartments for country dwellers coming into the city to attend nearby clubs. The block was divided into a selection of pieds-à-terre, mostly consisting of a bedroom, sitting room and a WC with limited catering facilities. The landlords, Berry Bros. & Rudd, who have been on the site since 1698, and who originally started out as a grocers before diversifying into coffee and finally wine, decided to renovate the block two years ago after it had become outdated with previous improvements which hadn’t been sympathetic to the buildings original architecture and layout. Enlisting the help of Obbard and Watson-Smyth was the first step in the process of reviving the building while being mindful of the heritage behind it.

Now, two years on, the apartments are complete and ready for new residents to move in. And the finishing touches and historic references certainly make them a special rental investment. From reclaimed fireplaces to vintage furniture and restored artworks from the Berry Bros. & Rudd archive, the design team has paid close attention to the impact of each interior element. “The dedication to re-using furnishings in this project was a labour of love,” says Watson-Smyth. “Our design studio was constantly visiting vintage markets and auctions to find perfect pieces for each apartment.”

A cosy reading nook under the penthouse windows, complete with vintage mid-century chairs and a … [+] handmade Moroccan carpet.

Mark Anthony Fox / Obbard

Approaching interior design with this mindset can pose a variety of challenges, especially when working within strict timelines and budgets. And, as Watson-Smyth reveals, it wasn’t a simple case of placing an order for 15 identical side tables from one supplier, which meant they had to work with a range of styles and finishes across each space. “Some key pieces we sourced were snapped up before we even got a chance to put our bids in,” she laughs, “so our designs had to be a bit fluid and not everything is uniform but to us that’s what we think gives the apartments such charm.” And on visiting, the apartments’ homely, ‘lived-in’ ambience is undeniable, a result that can be difficult to achieve when redeveloping an entire block.

Where new purchases were inevitable, the team also ensured they worked with brands who work tirelessly to reduce their environmental impact. This included beds from The Cornish Bed Company, paint from Graphenstone and sofas from Love Your Home. Repurposed textiles were also utilised in a lot of the accessories within each space, thanks to a collaboration with Haines, a UK-based platform enabling the resale of dead-stock and leftover fabrics.

Striking paint colours from Graphenstone and reclaimed textiles from Haines add a beautiful … [+] sensitivity to the interiors.

Mark Anthony Fox / Obbard

Keeping it personally connected to the history behind Berry Bros. and Rudd, a variety of archive pieces have been repaired and upcycled to fit into the contemporary scheme. Notable items include a letter from The White Star Line (dated April 16th 1912) which is addressed to the company informing them of the loss of a shipment which was on the Titanic. In the bathroom of the penthouse, framed original, handwritten drinks recipes decorate the walls as well as an original hand-drawn plan of the tea clipper ship ‘Cutty Sark’ which is hanging in the first floor apartment: the inspiration behind the original ‘Cutty Sark’ whisky which was developed by Berry Bros. & Rudd in 1923. These nostalgic touches provide beautiful points of interest throughout each space, where the narrative of such a long history is given the room to live on into the future.

Framed handwritten wine recipes hang in the WC of the penthouse, another nod to the heritage behind … [+] the building itself.

Mark Anthony Fox / Obbard

“What we didn’t want was a building that felt completely disconnected,” explains Patti Patrick, Head of Design & Development for Obbard. “A lot of this project has been about reclaiming the buildings narrative that had been erased and, in working with this mindset, we want these apartments to appeal to those that respect the history of St James’s and are genuinely interested by the neighbouring St James’ Palace, and Berry Bros. & Rudd as well as a host of other iconic British institutions.” Far from being stuck in the past, the apartments boast a cohesive blend of both classic and contemporary design, a feat which has been achieved through a curated approach.

Patti Patrick – Head of Development & Design for Obbard & Kate Watson-Smyth – Design Consultant for … [+] the interior design of the redevelopment.

Mark Anthony Fox / Obbard

While the interiors speak for themselves, added services to the block also add an extra special touch. All tenants of No.1 St James will have access to a dedicated wine concierge, provided by Berry Bros. & Rudd. During store hours, residents are able to ask for advice, recommendations, as well as tastings, which means bottles can be delivered directly to their door. For wine lovers, this is an extremely attractive benefit!

Looking back at the development as a whole, Watson-Smyth reflects on the need to approach every interior design project with a conscious and responsible attitude but also allude to the fact that you need to invest time to carry out the necessary research. “Compared to five years ago there are many more eco-friendly options on the market, even when buying new,” she comments. “It’s about taking the time to research as these brands exist but perhaps aren’t the most known. What’s exciting is that there is change afoot though, specifically in an industry that has taken its time to start evolving for the better.”

Special moments are captured and the architecture has been celebrated in the redesign of No.1 St … [+] James, especially here in the Penthouse’s hidden games room where one can enjoy wine or whisky, directly from the Berry Bros. & Rudd cellar.

Mark Anthony Fox

While this project is just a snapshot of what can be achieved, especially when working at a larger scale, it is a positive step in showcasing the realm of opportunities that do exist when sustainability underpins the ethos of any design project. Paying close attention to impact does not have to mean a compromise in style, in fact it’s quite the opposite. When paying homage to history through sensitive materials and reclaimed designs, a certain depth is created which results in a striking, yet welcoming, aesthetic. For me, it is the foundation to the making of not just a house, but a home.

I recently made a panic decision to withdraw all my money from one retirement account and I am now closing on a house in February (about $200,000). I am 36 years old, married and have a 1-year-old. Half of me is regretting it, and I’m worried about next year’s taxes due to the withdrawal and the 10% penalty I paid.

I have been saving up money with my family in order to buy our first home. Recently, however, interest rates have risen, making me worry that this window to get an affordable house was closing. In a fit of panic, I withdrew all of our $26,000 saved money from my 401(k), putting it in a high-yield savings account (3.75%). We have now chosen a home and will be using around $18,000 of this money for the down payment.

I am now worried that I might have to pay income taxes and a penalty for the withdrawal itself. I am extremely anxious over this situation as I feel I have destroyed our family’s financial future and that we cannot afford to pay taxes on the money I withdrew.

My main concern or question is, is there a way to tell the IRS that this money is being used toward a house? Retroactively?

The first thing you need to do: Take a breath. Most decisions should not be made in a panic, especially when involving money.

Because you withdrew from your 401(k), yes, you will have to pay taxes and a penalty. Had it been a loan, you’d have to pay interest on what you borrowed, but it would be to your own account. Keep in mind however that loans from your employer-based retirement plans are also risky – if you were to separate from your job, for whatever reason, you’d be responsible to pay it back or it would be treated as a distribution.

I understand your sense of urgency in wanting to buy a home during a more favorable market, but your time now should be spent on getting yourself financially situated and saving for the future.

“I wouldn’t advise this or done it this way, but he’s not stuck and it’s not detrimental – it’s just a tough lesson to learn,” said Jordan Benold, a certified financial planner at Benold Financial Planning.

Get very serious about your current finances and find a way to earmark a portion of your income to savings if at all possible. There are a few things you should be doing.

First, assess how much you will be paying in taxes and penalties. I’m not sure what your tax bracket is, but did this distribution push you into a higher tax bracket? You can use a calculator or talk to an accountant to see what that withdrawal will incur in taxes – then make sure you can pay it, or talk to the Internal Revenue Service about an extension. There are penalties for failing to file your taxes or pay them, and you don’t want to add that on top of your stress.

The IRS may not be able to do anything for you in terms of waiving those penalties – though it doesn’t hurt to ask, even if you have to wait on the phone for a while to talk to someone – but communication and attention to detail are key when it comes to your taxes. Getting an IRS agent on the phone and talking through your situation won’t be time wasted. There are so many rules, and an agent can help make sense of your options.

Once you get that sorted, look extremely carefully at whatever money you have coming in and what’s going out. You’re about to close on a home, and that costs money – not just the home itself, but all of the extras associated with closing. You may also need money for insurance, furniture, any repairs and so on if you haven’t factored that in yet, so fit that into your budget for when you sign the papers. Beyond that, list every expense you expect to have for the next 12 months – home insurance and taxes, a mortgage or utilities, groceries, medicine, any other nonnegotiable costs and add it all up. Don’t forget anything – ask your partner if there’s anything you may have forgotten.

Then compare it to your income. Are you under? Are you over? What changes can you make without totally draining your happiness? I always advocate for a balance…yes, in some cases you have to omit a few expenses for the time being when building up an emergency savings account or paying down debt, but don’t completely rob yourself of joy or all of your hard work may backfire. If you really need to buckle down, make a separate list of activities and entertainment you can get for free (or as close to free as possible)—walks in the park or on the beach with your partner and child, museums on free days, pot lucks and at-home movie nights with family and friends and so on.

Want more actionable tips for your retirement savings journey? Read MarketWatch’s “Retirement Hacks” column

Earmark a portion of your income to replenish your retirement savings before you try saving for any other goals. (This is separate from an emergency savings account, however – you should have one of those.) You may do that with payroll deductions in your 401(k), or also by allocating some of your savings to an IRA outside of the 401(k).

Take some time to learn the rules of your retirement plans. For example, an IRA allows an investor to take $10,000 out of the account penalty-free if it’s for a first-time home purchase (whereas a 401(k) does not have that exception). It may be too late for that, but there are other perks with various retirement accounts.

The 401(k) has a higher contribution limit and also comes with the possibility of employer matches (if your company offers it), whereas an IRA allows for penalty-free withdrawals for college. With a traditional IRA, you’d have to pay taxes on the withdrawal, whereas with a Roth IRA you’ve already paid the taxes and won’t have to pay any more for withdrawing from your contributions (you may have to pay taxes on the earnings portion, so follow distribution rules closely).

Remember – you don’t want to make distributions from your retirement savings for just anything. You can borrow money for a home or college, but you can’t borrow money for retirement, so it’s important to protect those accounts. Familiarize yourself with the pros and cons of all accounts so that you can maximize your savings and diversify your withdrawal options when you finally get to retirement.

So just buckle down, get yourself in order and think of the future. “He’s got plenty of time – 30 to 40 years to work,” Benold said. “This might be a distant memory that he hopes he can forget.”

Have a question about your own retirement savings? Email us at HelpMeRetire@marketwatch.com

Readers: Do you have suggestions for this reader? Add them in the comments below.

Strict lending rules were introduced in 2020 to tackle property developers’ unbridled borrowing.

China is planning to relax restrictions on borrowing for property developers to support the troubled sector by dialling back the “three red lines” policy, Bloomberg News has reported.

The “three red lines” policy was unveiled in August 2020 to tackle property developers’ unbridled borrowing by restricting the amount of new borrowing they can raise each year.

Beijing may allow some property firms to add more leverage by easing borrowing caps, and push back the grace period for meeting debt targets set by the policy. Regulators could also extend the deadline by at least six months, which was originally June 30, the report said citing people familiar with the matter.

Under the new proposal, China will ease restrictions on debt growth for developers depending on how many red lines they meet, easing borrowing caps to companies that meet all three thresholds, the report added.

To support the sector, policymakers have announced numerous measures in recent months including making it easier for developers to raise new funds, loan repayment extensions and more help for homebuyers. But analysts expect the recovery to be a long and bumpy one.

The “three red lines” metric put caps on debt-to-cash, debt-to-assets and debt-to-equity ratios and asked property developers to provide more details about their debts.

I’m the first of my generation to own a home and the first to earn this much annually and don’t want to mess this up. How, specifically, can a financial adviser help me?

Getty Images

Question: By the end of 2022, I will have made $350,000 before taxes as the sole breadwinner and head of household. This is a great starting point and I’m very aware how blessed we are to be in this position, but I’m always looking ahead on how to improve. I currently have $88K left in student loans (originally close to $150K) and very little credit card debt (less than $2K with more than $25K available). I have two auto loans totaling $170K for two electric vehicles at 5% interest.

I’ve recently been offered a $200K HELOC at 9%, which would help me bring down some of my monthly payments and do some small home repairs and improvements, but I want to make the right moves. And I’ve also been presented with a few long-term real estate investment opportunities that are rental properties out of state and are currently bringing it 10-12% ROI. But my biggest concern is that after taxes, 401(k) contributions, bills, savings and mortgage ($4,500), on paper I’m paycheck to paycheck. I’d like to use this HELOC to consolidate debt while also participating in some of these investment opportunities. I’m the first of my generation to own a home and the first to earn this much annually and don’t want to mess this up. How, specifically, can a financial adviser help me? (Looking for a new financial adviser too? This tool can help match you with an adviser who might meet your needs.)

Answer: You have a few questions to tackle here, so let’s go one by one. The first being the HELOC. Yes, HELOCs can be a good way to consolidate debt, but the rate you’re being offered isn’t favorable, as average HELOC rates are a little over 6%. “I would ask if 9% is the best rate you can get, because it appears a bit high,” says Chris Chen, certified financial planner at Insight Financial Strategists. What’s more, “I would like you to consider the potential impact that our Fed policy and inflation are having on interest rates, as HELOCs usually have variable interest rates and we’re in an environment with rising rates. You may start at 9% and end up significantly higher,” says Chen.

What’s more, your student loans, car loans and mortgage are all likely less than 9%, so it’s not likely that consolidation via a HELOC would save you money. “You may want to start somewhere different, like the snowball method, where you focus on one loan, usually the smallest one, and direct all of your resources to pay off that loan while maintaining payments on the others,” says Chen. This method could work to finish off your student loans and maybe one of your car loans, to start with.

Have an issue with your financial adviser or have questions about hiring a new one? Email picks@marketwatch.com.

As for those real estate investments, what do you really know about those returns? “With regards to real estate investments, I assume that the 10% to 12% ROI you speak of is the income that you would be getting from the investment. If so, that’s very high and often when you get a return that is significantly higher than the norm, there’s something else that makes the investment less desirable. Be careful,” says Chen. (Looking for a new financial adviser too? This tool can help match you with an adviser who might meet your needs.)

Certified financial planner Kaleb Paddock says you may actually want to work with a money coach before you work with a financial adviser. Whereas a financial adviser assists with developing investment strategies and long-term financial plans, a money coach offers a more educational experience and focuses on shorter term goals for money management. “A money coach will help you with paying off all of your debts, maximize your cash flow and help you create systems and processes to direct your money proactively,” says Paddock.

While having a high income is great, there’s a concept called Parkinson’s Law, which essentially states that your spending will always rise to meet your income no matter how high that income rises, explains Paddock. “Working with a money coach will help you defeat Parkinson’s Law, eliminate your debt and then enable you to supercharge your investing and life planning with a financial adviser,” says Paddock.

A financial adviser could help too, and Danielle Harrison, certified financial planner at Harrison Financial Planning, says to look for one who does comprehensive financial planning and can help you create a more holistic plan for your money. “They can assist you in the creation of both short and long-term goals and then help you by giving guidance on the financial decisions and opportunities you are presented with,” says Harrison.

A financial adviser would also help you take a long-term approach to your money and help you create a spending plan where you don’t feel like you’re living paycheck to paycheck on a $350,000 salary. “Everyone has blind spots when it comes to their finances, so finding a competent financial partner can be invaluable,” says Harrison. (Looking for a new financial adviser too? This tool can help match you with an adviser who might meet your needs.)

Have an issue with your financial adviser or have questions about hiring a new one? Email picks@marketwatch.com.

*Questions edited for brevity and clarity.

The advice, recommendations or rankings expressed in this article are those of MarketWatch Picks, and have not been reviewed or endorsed by our commercial partners.

We want to hear from readers who have stories to share about the effects of increasing costs and a changing economy. If you’d like to share your experience, write to readerstories@marketwatch.com. Please include your name and the best way to reach you. A reporter may be in touch.

For many people living in the U.S., these are tough — and confusing — times.

On Friday, the Labor Department reported 263,000 new jobs in November, while the unemployment rate held steady at 3.7%. Layoffs remain low, despite mass job cuts in the tech sector. Average hourly wages have also risen 5.1% in the past year, but still lag behind inflation for many workers. And there were 10.3 million job openings in October — slightly down from the previous month’s 10.7 million.

Some people might see the latest economic data as both challenging and confusing.

“‘It’s just mind-boggling, the disconnect that we’ve seen.’”

Given all the conflicting signals, economists say it can be difficult for consumers to know exactly how to feel about the economy right now. “It’s not new, this disparity between the actual facts on the ground about what’s going on in the economy and the sentiment,” said Heidi Shierholz, president of the Economic Policy Institute, a left-leaning think tank.

“I remember this summer it was just unambiguously the strongest jobs recovery we’ve had in decades,” she added. “There’s just absolutely zero chance that we were in a recession — not only were we not in a recession, we were in just an extraordinarily fast recovery — and the polling, a huge share of people actually thought we were in a recession. It’s just mind-boggling, the disconnect that we’ve seen.”

“Going into the pandemic, more than seven out of every 10 extremely low-income renters were already spending more than half of their income on rent. And then the pandemic hits; we saw a lot of low-wage workers lose their jobs and see an income decline,” said Andrew Aurand, vice president for research at the National Low Income Housing Coalition. “Then in 2021, we see this huge spike in prices. For a variety of reasons, they’ve struggled for a long time, and since the pandemic, it’s gotten even worse.”

But we would like your help telling an ongoing story about the American economy, centering the experiences of everyday people. Our readers know better than anyone about how today’s economic conditions have impacted their daily lives.

Income-seeking investors are looking at an opportunity to scoop up shares of real estate investment trusts. Stocks in that asset class have become more attractive as prices have fallen and cash flow is improving.

Below is a broad screen of REITs that have high dividend yields and are also expected to generate enough excess cash in 2023 to enable increases in dividend payouts.

REIT prices may turn a corner in 2023

REITs distribute most of their income to shareholders to maintain their tax-advantaged status. But the group is cyclical, with pressure on share prices when interest rates rise, as they have this year at an unprecedented scale. A slowing growth rate for the group may have also placed a drag on the stocks.

And now, with talk that the Federal Reserve may begin to temper its cycle of interest-rate increases, we may be nearing the time when REIT prices rise in anticipation of an eventual decline in interest rates. The market always looks ahead, which means long-term investors who have been waiting on the sidelines to buy higher-yielding income-oriented investments may have to make a move soon.

During an interview on Nov 28, James Bullard, president of the Federal Reserve Bank of St. Louis and a member of the Federal Open Market Committee, discussed the central bank’s cycle of interest-rate increases meant to reduce inflation.

When asked about the potential timing of the Fed’s “terminal rate” (the peak federal funds rate for this cycle), Bullard said: “Generally speaking, I have advocated that sooner is better, that you do want to get to the right level of the policy rate for the current data and the current situation.”

Fed’s Bullard says in MarketWatch interview that markets are underpricing the chance of still-higher rates

In August we published this guide to investing in REITs for income. Since the data for that article was pulled on Aug. 24, the S&P 500 SPX, -0.29%

has declined 4% (despite a 10% rally from its 2022 closing low on Oct. 12), but the benchmark index’s real estate sector has declined 13%.

REITs can be placed broadly into two categories. Mortgage REITs lend money to commercial or residential borrowers and/or invest in mortgage-backed securities, while equity REITs own property and lease it out.

The pressure on share prices can be greater for mortgage REITs, because the mortgage-lending business slows as interest rates rise. In this article we are focusing on equity REITs.

Industry numbers

The National Association of Real Estate Investment Trusts (Nareit) reported that third-quarter funds from operations (FFO) for U.S.-listed equity REITs were up 14% from a year earlier. To put that number in context, the year-over-year growth rate of quarterly FFO has been slowing — it was 35% a year ago. And the third-quarter FFO increase compares to a 23% increase in earnings per share for the S&P 500 from a year earlier, according to FactSet.

The NAREIT report breaks out numbers for 12 categories of equity REITs, and there is great variance in the growth numbers, as you can see here.

FFO is a non-GAAP measure that is commonly used to gauge REITs’ capacity for paying dividends. It adds amortization and depreciation (noncash items) back to earnings, while excluding gains on the sale of property. Adjusted funds from operations (AFFO) goes further, netting out expected capital expenditures to maintain the quality of property investments.

The slowing FFO growth numbers point to the importance of looking at REITs individually, to see if expected cash flow is sufficient to cover dividend payments.

Screen of high-yielding equity REITs

For 2022 through Nov. 28, the S&P 500 has declined 17%, while the real estate sector has fallen 27%, excluding dividends.

Over the very long term, through interest-rate cycles and the liquidity-driven bull market that ended this year, equity REITs have fared well, with an average annual return of 9.3% for 20 years, compared to an average return of 9.6% for the S&P 500, both with dividends reinvested, according to FactSet.

This performance might surprise some investors, when considering the REITs’ income focus and the S&P 500’s heavy weighting for rapidly growing technology companies.

For a broad screen of equity REITs, we began with the Russell 3000 Index RUA, -0.04%,

which represents 98% of U.S. companies by market capitalization.

We then narrowed the list to 119 equity REITs that are followed by at least five analysts covered by FactSet for which AFFO estimates are available.

If we divide the expected 2023 AFFO by the current share price, we have an estimated AFFO yield, which can be compared with the current dividend yield to see if there is expected “headroom” for dividend increases.

For example, if we look at Vornado Realty Trust VNO, +1.03%,

the current dividend yield is 8.56%. Based on the consensus 2023 AFFO estimate among analysts polled by FactSet, the expected AFFO yield is only 7.25%. This doesn’t mean that Vornado will cut its dividend and it doesn’t even mean the company won’t raise its payout next year. But it might make it less likely to do so.

Among the 119 equity REITs, 104 have expected 2023 AFFO headroom of at least 1.00%.

Here are the 20 equity REITs from our screen with the highest current dividend yields that have at least 1% expected AFFO headroom:

Click on the tickers for more about each company. You should read Tomi Kilgore’s detailed guide to the wealth of information for free on the MarketWatch quote page.

The list includes each REIT’s main property investment type. However, many REITs are highly diversified. The simplified categories on the table may not cover all of their investment properties.

Knowing what a REIT invests in is part of the research you should do on your own before buying any individual stock. For arbitrary examples, some investors may wish to steer clear of exposure to certain areas of retail or hotels, or they may favor health-care properties.

Largest REITs

Several of the REITs that passed the screen have relatively small market capitalizations. You might be curious to see how the most widely held REITs fared in the screen. So here’s another list of the 20 largest U.S. REITs among the 119 that passed the first cut, sorted by market cap as of Nov. 28:

The numbers: Construction on new houses fell 4.2% in October as high mortgage rates put off buyers and forced builders to scale back, a situation that’s likely to continue through 2023.

U.S. housing starts slowed to an annual pace of 1.43 million last month from 1.49 million in September. That figure reflects how many homes would be built in 2022 if construction took place at same rate over the entire year as it did in October.

Economists polled by MarketWatch had expected housing starts to register a rate of 1.41 million after adjusting for the typical seasonal swings in demand.

New construction hit a record 1.8 million in April before tapering off.

The number of permits, meanwhile, slipped 2.4% to a rate of 1.53 million, down sharply from a record 1.9 million last December.

Permits foreshadow how many houses are likely to be built in the months ahead, assuming a stable real estate market. But a major increase in mortgage rates this year has depressed demand and forced builders to scale back plans.

Key details: Single-family home construction fell 6.1% to an annual rate of 855,000 in October. Projects with five units or more registered a 556,000 rate, little changed from the prior month.

Housing starts are down 9% from a year ago, when mortgage rates briefly dipped below 3%.

Permits have fallen 10% from a year earlier.

Big picture: The highest mortgage rates in several decades have stifled new construction and are likely to do so through the next year or longer. The rate on a 30-year fixed mortgage recently topped 7%, more than double the rate a year ago.

While the U.S. has an acute need for more housing, fewer people can now afford to buy a home. Home prices are starting to come off record highs, but not by much.

Looking ahead: “Higher mortgage rates continue to exact a heavy toll on new construction,” said Richard Moody, chief economist of Regions Financial.

Market reaction:The Dow Jones Industrial Average DJIA, -0.18%

and S&P 500 SPX, -1.01%

fell in Thursday trades.

HIGHLAND PARK, IL – OCTOBER 21: A gate with the number 23 controls access to the home of basketball … [+] legend Michael Jordan on October 21, 2013 in Highland Park, Illinois. Twenty-three is the number Jordan wore while playing basketball for the Chicago Bulls. The home which had been offered for sale for $29 million and later dropped to $21 million is scheduled to be sold at auction on November 22. The 32,683-squre-foot home features nine bedrooms, 19 bathrooms, a 15-car attached garage and an “NBA-quality” basketball court. (Photo by Scott Olson/Getty Images)

Getty Images

The careers of most athletes are short-lived. 3.5 years is typically the average number of years WNBA players have to play at a high level. To most athletes, each day isn’t just a chance to get better on the court, but also a day to prepare for what the future may hold.

Liberian-American basketball star Matee Ajavon went on to have an illustrious start to her career by winning the Gold Medal in the Pan-American Games in Rio De Janeiro, Brazil while attending Rutgers University. Her team, led by the famous Coach C. Vivian Stringer also went to the 2007 NCAA Championship Game vs. Tennessee University only to fall short of a win.

When the Houston Comets drafted Matee Ajavon as the fifth overall pick in the 2008 WNBA Draft, she instantly knew she had been given an opportunity that most athletes only dream of throughout their lifetime. Matee was 1 of the 144 women that could actually call themselves a WNBA pro.

Her career beat the odds by lasting for a total of 10 years. Matee played with the Houston Comets (1 year), Washington Mystics (5 years), and Atlanta Dream for the last 4 years of her career. She also played in 5 different countries that included Turkey, Brazil, Israel, Poland and Romania in the off-season. Going overseas allowed some WNBA players to earn up to 10x the salary they would in the WNBA.

LOS ANGELES, CA – JULY 16: Matee Ajavon #10 of the Atlanta Dream handles the ball against the Los … [+] Angeles Sparks in WNBA game at Staples Center on July 16, 2015 in Los Angeles, California. (Photo by Leon Bennett/Getty Images)

Getty Images

In the latter stages of her career, Matee admits that she always felt the need to diversify and invest her earnings. Her search eventually led her to Real Estate Gurus; a company led by Real Estate professional Justin Giles. Giles introduced a then-retired Matee Ajavon to a whole new world by helping her build a real estate investment business.

Giles is a well-known real estate advisor and licensed real estate broker of 17+ years and has been behind the making of quite a few athlete-turned-real estate investors. He utilizes his social media platform on Instagram to educate and connect his many followers on ways to simply start investing in real estate.

His strategies, as explained in two of his books, Zero Down and Learn To Fish And Eat Forever, have also been widely received and critically acclaimed.

The number of former and current athletes investing in real estate has multiplied over time. Roger Staubach, Emmitt Smith, Magic Johnson, Shaquille O’Neal, David Robinson, Alex Rodriguez, & Martin Braithwaite immediately come to mind,

A Familiar Market

Professional athletes, especially in leagues like the NBA, WNBA, or the NFL, are traded quite often from team to team during their careers. This also means they have to purchase or rent properties from different parts of the country.

Athletes rarely have the chance to play for their home teams, which means they are likely to maintain at least two properties at any given time. One of them being their home state and the other being their current location.

While many A-list players may have people who put property deals together for them, most others have to get involved personally. In turn, this puts them squarely in the bustle of the industry. Whether knowing or unknowingly, many athletes end up as real estate investors or somewhat develop an idea or love for the industry.

Senegalese-born former Chicago Bulls star Luol Deng started a real estate symposium to educate players on the value of the sector. At the time he said, “I’ve always had a love for real estate and wanted to do something in Chicago for a long time,”

“We talk about players going broke, but we don’t talk about why that is happening,” Deng says. “The symposiums were a way to teach players about real estate and foster a better understanding of these kinds of investments.”

CHICAGO, IL – MAY 15: Luol Deng #9 of the Chicago Bulls attempts to steal the ball from LeBron … [+] James #6 of the Miami Heat in Game One of the Eastern Conference Finals during the 2011 NBA Playoffs on May 15, 2011 at the United Center in Chicago, Illinois. NOTE TO USER: User expressly acknowledges and agrees that, by downloading and or using this photograph, User is consenting to the terms and conditions of the Getty Images License Agreement (Photo by Jonathan Daniel/Getty Images)

Getty Images

A Low Entrance Bar And High Availability

Few people consider the real estate market as having a low entrance bar because of the high prices quoted for properties. Not every athlete can afford to splash $36 million on a Beverly Hills mansion like LeBron. But according to Giles, they don’t have to;

“Athletes are often looking to invest their earnings and savings into the real estate industry. So they have to learn the art of finding the best deals from anywhere in the country. At every price point, there will always be an available and lucrative property somewhere and also loans available to help anyone acquire properties.”

“Even though some pro-athletes may be familiar with buying and selling properties, they still need to learn the small details of how to actually buy and sell properties as a ‘realbusiness’. The first thing is learning how to find these deals that may not be in plain sight, next how to renovate these properties with the help of contractors, and last and definitely not least, how to turn it into healthy profits.”

The real estate market also offers many options for investment; while athletes like the NFL’s William Sweet buys and rent out their properties, others could choose to flip homes or buy and hold assets as part of their real estate portfolio.

DENVER, CO – AUGUST 29: William Sweet #75 of the Arizona Cardinals walks in the bench area during a … [+] preseason National Football League game against the Denver Broncos at Broncos Stadium at Mile High on August 29, 2019 in Denver, Colorado. (Photo by Dustin Bradford/Getty Images)

Getty Images

“There are properties that are entering foreclosure, and I teach people how to stop a foreclosure even 24 hours before the auction.” Giles explains, “There are houses owned by deceased individuals who passed on without a will. Whenever that happens, there are ways to help their heirs claim these properties and then purchase the properties from them. If you know where to look, properties are always available using these strategies”

Robbie Fowler, an ex-Liverpool Football Club and England FC star who is now estimated to be worth roughly £30 million ($34 million) also opined, “Don’t get me wrong, not everything went into property at the time. And I didn’t just invest on my own, because when I was 18, I was on next to nothing and I couldn’t afford it, regardless of what people think about football players”.

“I invested with partners. It was all through the advice I was given, not because I knew anything or wanted to know it, it was totally by accident”.

He continued, “When you’re 18, I think it is probably the last thing on your mind. You’re obviously signing new contracts and you want to go out, you probably want a new car, and you’ll get all the things that you haven’t had”.

BRISBANE, AUSTRALIA – MARCH 04: Roar coach Robbie Fowler poses during an International Champions Cup … [+] media opportunity, ahead of matches between Crystal Palace FC, West Ham United FC and the Brisbane Roar at Suncorp Stadium on March 04, 2020 in Brisbane, Australia. (Photo by Jono Searle/Getty Images)

Getty Images

“But then all of a sudden, there comes a time when you think: Uh, I need to pull the reins in a little bit here and maybe look after my life after football. When I was 18, that was far from my mind, but over the years, it does materialise that way”.

Passive Income

Every investor’s dream is to have a portfolio that yields more passive income than active income. Athletes and celebrities often invest in stocks and bonds to get passive income, but the fluctuating markets have dissuaded many of them and made real estate investing a bit more attractive. This desire for passive income has led several pro athletes to invest in real estate investment trusts (REITs). While REITs are often considered safe, they are also more of a long-term strategy.

“After the housing crash of 2008, I found myself in so much debt. But somehow, I decided to stick with real estate, and over time I have devised investment strategies that make investing in real estate virtually recession-proof.” Giles believes that there is no such thing as a bad property market.

Justin Giles – The Celebrity-Athlete’s Pathway; Why Professional Athletes Are Investing Heavily Into … [+] Real Estate

REG

If the storied investment successes of NBA greats like Shaquille O’Neal and Magic Johnson are anything to go by, pro athletes will be investing in real estate for quite some time.

Investors cheered when a report last week showed the economy expanded in the third quarter after back-to-back contractions.

But it’s too early to get excited, because the Federal Reserve hasn’t given any sign yet that it is about to stop raising interest rates at the fastest pace in decades.

Below is a list of dividend stocks that have had low price volatility over the past 12 months, culled from three large exchange traded funds that screen for high yields and quality in different ways.

In a year when the S&P 500 SPX, -0.40%

is down 18%, the three ETFs have widely outperformed, with the best of the group falling only 1%.

That said, last week was a very good one for U.S. stocks, with the S&P 500 returning 4% and the Dow Jones Industrial Average DJIA, -0.32%

having its best October ever.

This week, investors’ eyes turn back to the Federal Reserve. Following a two-day policy meeting, the Federal Open Market Committee is expected to make its fourth consecutive increase of 0.75% to the federal funds rate on Wednesday.

The inverted yield curve, with yields on two-year U.S. Treasury notes TMUBMUSD02Y, 4.540%

exceeding yields on 10-year notes TMUBMUSD10Y, 4.064%,

indicates investors in the bond market expect a recession. Meanwhile, this has been a difficult earnings season for many companies and analysts have reacted by lowering their earnings estimates.

The weighted rolling consensus 12-month earning estimate for the S&P 500, based on estimates of analysts polled by FactSet, has declined 2% over the past month to $230.60. In a healthy economy, investors expect this number to rise every quarter, at least slightly.

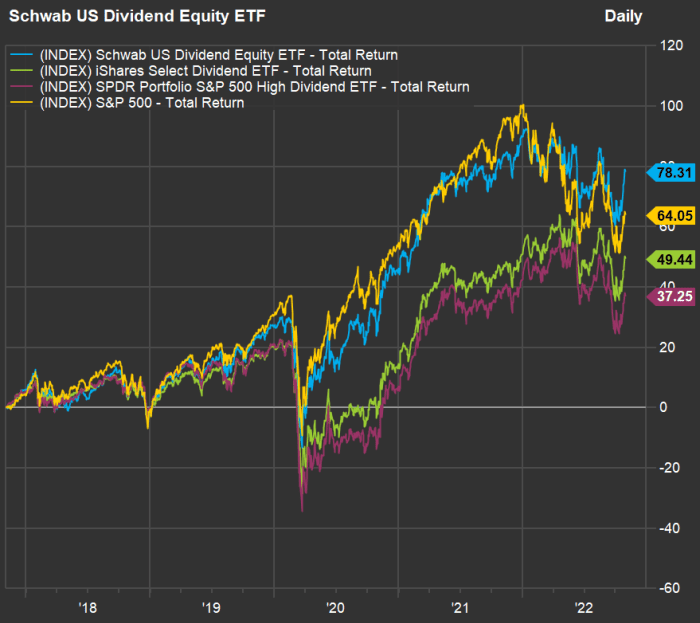

Low-volatility stocks are working in 2022

Take a look at this chart, showing year-to-date total returns for the three ETFs against the S&P 500 through October:

FactSet

The three dividend-stock ETFs take different approaches:

The $40.6 billion Schwab U.S. Dividend Equity ETF SCHD, +0.15%

tracks the Dow Jones U.S. Dividend 100 Indexed quarterly. This approach incorporates 10-year screens for cash flow, debt, return on equity and dividend growth for quality and safety. It excludes real estate investment trusts (REITs). The ETF’s 30-day SEC yield was 3.79% as of Sept. 30.

The iShares Select Dividend ETF DVY, +0.45%

has $21.7 billion in assets. It tracks the Dow Jones U.S. Select Dividend Index, which is weighted by dividend yield and “skews toward smaller firms paying consistent dividends,” according to FactSet. It holds about 100 stocks, includes REITs and looks back five years for dividend growth and payout ratios. The ETF’s 30-day yield was 4.07% as of Sept. 30.

The SPDR Portfolio S&P 500 High Dividend ETF SPYD, +0.60%

has $7.8 billion in assets and holds 80 stocks, taking an equal-weighted approach to investing in the top-yielding stocks among the S&P 500. It’s 30-day yield was 4.07% as of Sept. 30.

All three ETFs have fared well this year relative to the S&P 500. The funds’ beta — a measure of price volatility against that of the S&P 500 (in this case) — have ranged this year from 0.75 to 0.76, according to FactSet. A beta of 1 would indicate volatility matching that of the index, while a beta above 1 would indicate higher volatility.

Now look at this five-year total return chart showing the three ETFs against the S&P 500 over the past five years:

FactSet

The Schwab U.S. Dividend Equity ETF ranks highest for five-year total return with dividends reinvested — it is the only one of the three to beat the index for this period.

Screening for the least volatile dividend stocks

Together, the three ETFs hold 194 stocks. Here are the 20 with the lowest 12-month beta. The list is sorted by beta, ascending, and dividend yields range from 2.45% to 8.13%:

Any list of stocks will have its dogs, but 16 of these 20 have outperformed the S&P 500 so far in 2022, and 14 have had positive total returns.

You can click on the tickers for more about each company. Click here for Tomi Kilgore’s detailed guide to the wealth of information available free on the MarketWatch quote page.

Billionaire Wu Yajun has stepped down as Longfor chairman. (Photo by May Tse/South China Morning Post via Getty Images)

South China Morning Post via Getty Images

Wu Yajun, the billionaire cofounder of real estate developer Longfor Properties, has stepped down as chair of the company amid an industry-wide crisis that is showing little sign of abating.

Shares of the Hong Kong-listed Longfor tumbled as much as 38% on Monday after the 58-year-old tycoon announced her decision late Friday night. Due to age and health reasons, Wu has resigned as executive director and chairperson of the board, but will continue to advise the company on its strategic development, Longfor wrote in a filing to the Hong Kong Stock Exchange.

She has handed the reins over to 40-year-old Chen Xuping, who has been with the company since 2008 and first worked as a construction manager before being promoted through the ranks. But the mogul, whose wealth plunged $1 billion to $6.1 billion in a single day, isn’t giving investors much to cheer.

“Longfor is experiencing management changes when the industry is undergoing a lot of difficulties,” says Kenny Ng, a Hong Kong-based securities strategist at Everbright Securities. “Investors are worried about how it would cope with the challenges.”

The company, for its part, said in a separate Friday filing that the role changes were results of its corporate governance strategy and focuses on nurturing senior managers through “culture and mechanism.” It disclosed in the same filing that contracted sales stood at 59.8 billion yuan ($8.2 billion) in the third quarter of this year, representing a mere 0.8% growth from the same period a year ago.

China’s real estate industry, meanwhile, is still mired in a deep crisis. Home prices have sank for a 13th straight month in September, as Beijing’s campaign to reduce financial leverage causes a wave of defaults, and buyer confidence remains weak in a slumping economy.

Longfor is considered to be on stronger footing than its debt-laden peers such as the now defaulted China Evergrande Group, thanks to Wu’s emphasis on financial discipline and relative prudence when it comes to borrowing. The company said in the aforementioned filing that it had no debt due this year, and its financial position “remains healthy and stable.” It was allowed in August to sell $219 million worth of yuan-denominated bonds that are guaranteed by the state, as Beijing sought to boost market sentiment towards healthier developers.

Still, the company’s shares have lost 70% of value year to date, underscoring investors’ pessimism toward the real estate sector. To prevent the current crisis from spiraling out of control, officials have also announced a series of easing policies including tax exemptions and lowering mortgage rates. But Fitch Ratings said in an October 24 report that the moves are “selective and modest in scale,” and unlikely to boost housing demand.

The whipsaw action wasn’t limited to stocks, and was described by Rick Rieder, the chief investment officer for global fixed income at BlackRock, as “one of the craziest days” of his career.

The bond market’s warning

Some investors who focus on stocks might not realize that the bond market is much larger, and that its movements can cause government and central-bank policies to shift. Larry McDonald, founder of The Bear Traps Report and author of “A Colossal Failure of Common Sense,” which described the 2008 failure of Lehman Brothers, explained just how bad the action was in the U.K. bond market over the past few weeks, when 30-year government bonds issued in December traded as low as 24 cents on the dollar. He also predicted what will happen if the Federal Reserve continues on its current course of interest-rate increases.

Michael Brush argues the Federal Reserve is moving too quickly to raise interest rates and cool the U.S. economy. He expects a rapid decline in inflation and a new bull market for stocks. In a column, he shares five sentiment indicators that suggest it is time to buy stocks — especially this group of companies.

Time for a refreshing COLA if you are on Social Security

Getty Images

The Social Security Administration has announced that its cost-of-living adjustment (COLA) for 2023 will be 8.7%, the largest increase in four decades. There is more to the story, including tax implications and changes to Medicare, as Jessica Hall and Alessandra Malito explain.

Freddie Mac said interest rates on 30-year mortgage loans averaged 6.92% on Oct. 13, up from 3.05% a year earlier. Mortgage Daily said rates had hit 7.10% — the highest in 20 years — and economists are warning these levels could be a “new normal.”

A homeowner locked-in with a low interest rate on their mortgage loan will be reluctant to sell. And some would-be buyers may now be priced out of the market because of much higher loan payments. Here’s what economists expect for home prices in 2023.

This is why Florida’s insurance market is such a mess

Florida insurers are not only suffering from storm-damage payouts.

Joe Raedle/Getty Images

Hurricanes are nothing new to Floridians, but insurers in the state are losing money even though premiums have doubled over the past five years. Shahid S. Hamid, the director of the Laboratory for Insurance at Florida International University, explains why the Florida insurance market is so distorted.

Here’s a travel option you may never have heard of — home swapping

Villefranche-sur-mer on the French Riviera.

istock

Home swapping can give you an opportunity to live as a local in a faraway place while spending much less than you would as a tourist. Here’s how it works.

Want more from MarketWatch? Sign up for this and other newsletters, and get the latest news, personal finance and investing advice.

Rent growth is beginning to cool. But it’s descending from a heck of a peak.

Rental prices climbed 7.2% between September 2021 to September of this year, the largest annual increase since 1982, according to consumer price data released Thursday. Overall, shelter costs were also among the most significant drivers in rising consumer prices, along with the cost of food and medical care, the Labor Department said.

Still, it’s not all bad news for tenants. A new report from Realtor.com out Thursday found that nationwide, median rental prices in 50 large metros grew at their slowest annual pace in 16 months in September — at 7.8%. That marked the second consecutive month of single-digit year-over-year growth for 0-2 bedroom properties, and it meant that median asking rents fell by $12 in a month, Realtor.com said.

Housing inflation in the Consumer Price Index lags trends in the rental market, though, meaning the slowdown in rent growth might not register in the data for a while.

While median rental prices are still nearly 23% higher than they were two years ago, they’re no longer climbing at breakneck speeds with no end in sight. These days, economists say, that counts as a silver lining.

“After more than a year of double-digit yearly rent gains and nearly as many months of record-high rents, it’s especially important to see consistency before we confirm a major shift like the recent rental market cool-down,” Realtor.com Chief Economist Danielle Hale said in a statement. “But September data provides that evidence, as national rents continued to pull back from their latest all-time high registered just two months ago.”

“This return of more seasonal norms indicates that rental markets are charting a path back toward a more typical balance between supply and demand, compared to the previous year,” Hale added. “We expect rent growth to keep slowing in the months ahead, partly driven by the impact of inflation on renters’ budgets.”

(Realtor.com is operated by News Corp NWSA, +1.64%

subsidiary Move Inc., and MarketWatch is a unit of Dow Jones, which is also a subsidiary of News Corp.)

A Redfin RDFN, -3.55%

report out Thursday, meanwhile, said rents grew 9% year-over-year in September — the slowest pace since August 2021. Rents were still way up year-over-year in cities like Oklahoma City (24.1%), Pittsburgh (20%), and Indianapolis (17.9%.)

This week Freddie Mac said the average interest rate on a 30-year mortgage loan in the U.S. had climbed to 6.70% from 6.29% the week before and 6.02% two weeks ago. The average rate a year ago was 3.01%.

Would-be sellers who have low-rate mortgage loans are reluctant if it means they need to take out a new loan to fund their next home. Would-be buyers are forced out of the market, as the monthly principal and interest payment for a new 30-year loan, based on Freddie Mac’s figures, has increased 53% from a year ago.

Home-sale contracts are being canceled at a record pace in some areas.

The dollar has strengthened as the Federal Reserve has taken the lead among central banks in raising interest rates. This is reverberating across the world, making it more costly for countries to make interest payments on dollar-denominated debt and increasing the cost of any commodity traded in dollars.

The rising dollar lowers prices on imported goods for Americans and can also lower their international travel costs. But Michael Wilson, Morgan Stanley’s chief equity strategist, warns that earnings for the S&P 500 SPX, -1.51%

would decline as a direct result of the strong dollar and called the current foreign-exchange backdrop an “untenable situation” for the stock market.

This is what happens when bearish sentiment runs high

Michael Brush interviews David Baron, co-manager of the Baron Focused Growth Fund BFGFX, -0.76%,

who describes opportunities cropping up as institutional investors dump stocks. He also explains his winning long-term strategy, which has included a very long-term investment in Tesla Inc. TSLA, -1.10%.

When interest rates rise, bond prices fall. But it also means that if you have money to put to work, bond yields have become much more attractive.

Khuram Chaudhry, a European equity quantitative strategist at JPMorgan in London, makes the case for buying bonds now.

What about preferred stocks?

Getty Images/iStockphoto

Preferred stocks feature stated dividend yields and prices that move the same way bond prices do. That means prices for many issues are now heavily discounted to face value and that current yields are much higher than they were at the end of 2021. Here’s an in-depth guide on how to research preferred stocks and make your own selections.

Stanley Druckenmiller predicted a “hard landing” in 2023 for the U.S. economy while speaking at CNBC’s Delivering Alpha Investor Summit on Sept. 28.

Bloomberg

Stanley Druckenmiller predicted a U.S. recession in 2023 as a result of monetary policy tightening by the Federal Reserve. That may not be much of a stretch, considering that the U.S. economy contracted during the first half of 2022, according to revised GDP figures from the Bureau of Economic Analysis.

After the new U.K. government of Prime Minister Liz Truss announced a massive tax cut along with a new spending program to help counter rising fuel costs and new borrowing, the pound hit a new low against the dollar on Sept. 26 as investors and money managers panicked and sold-off U.K. government bonds. Steve Goldstein explains how and why the Bank of England came tot the rescue.

After Tesla CEO Elon Musk said the upcoming Cybertruck would be sufficiently waterproof to “serve briefly as a boat,” the San Francisco Bay Ferry offered this advice to patrons.

Want more from MarketWatch? Sign up for this and other newsletters, and get the latest news, personal finance and investing advice.

The numbers: Mortgage rates continue to march towards 7%, continuing to pressure potential homeowners looking to buy a home.

The 30-year fixed-rate mortgage averaged 6.7% as of Sept. 29, according to data released by Freddie Mac FMCC, +0.75%

on Thursday.

Mortgage rates are up as the Federal Reserve pushed key interest rates up to deal with the worst inflation the country has seen in 40 years.

That’s up 41 basis points from the previous week — one basis point is equal to one hundredth of a percentage point, or 1% of 1%.

The rise in rates is bad news for prospective buyers, as it potentially adds hundreds of dollars to their mortgage payments.

Mortgage rates are now at highs last seen since mid-2007. To put the latest rate in perspective: A year ago, the 30-year was at 3.01%.

“Mortgage rates are now at highs last seen since mid-2007. To put the latest rate in perspective: A year ago, the 30-year was at 3.01%.”

Bloomberg’s chief economist Michael McDonough said a $2,500 monthly mortgage payment — with 20% down — would have gotten a buyer a $758,000 home last year.

This year? You’d get a lot less house — with $2,500 per month, you’d only be able to afford a $476,000 home, he wrote on Twitter TWTR, -1.12%.

The median price of an existing home in the U.S. was $389,500 in August, down from $403,800 the previous month, the National Association of Realtors said.

The average rate on the 15-year mortgage also rose over the past week to 5.96%. The adjustable-rate mortgage averaged 5.3%, up from the prior week.

“The uncertainty and volatility in financial markets is heavily impacting mortgage rates,” Sam Khater, chief economist at Freddie Mac, said in a statement.

Khater added that Freddie Mac’s survey of lenders revealed a large dispersion in rates, so home buyers should shop around with lenders to find a good quote.

Mortgage applications also fell in the latest week, as cautious buyers continue to pull back as rates march towards 7%.

The yield on the 10-year Treasury note TMUBMUSD10Y, 3.784%

rose slightly above 3.8% in morning trading on Thursday.

Got thoughts on the housing market? Write to MarketWatch reporter Aarthi Swaminathan at aarthi@marketwatch.com

Hi everyone! And a happy new year! I hope this finds you and yours well. I wanted to reach out today to provide an update on where we stand with our plans for APA!’s campuses, land, and facilities.

As a reminder, your voices were heard in November as you helped us get the APA! Resolution passed with Austin City Council. In that resolution, the city council directed us to work with the City of Austin staff to determine an intake percentage number based on those animals at risk of euthanasia. We continue those discussions with the city and will have an update to share with you in February.

While we remain hopeful that we will finally reach a new agreement with city animal services and sign a long term lease to keep a small portion of our operations on our Town Lake Animal Center (TLAC) campus as soon as possible, we are excited to be exploring our expansion regardless of the TLAC outcome.

The APA! Board of Directors and some other amazing volunteers have been utilizing their connections to help us find Austin properties to purchase and expand our footprint. Right now there are a couple of potential properties we are looking at and because the property is, of course, at a premium in Austin, we are looking at properties with existing buildings we could adjust to fit our programs and services – and also properties with mostly open land. Based on what we find and can afford, the APA! leadership team is working on different solutions with a group of architects to puzzle together which programs and services would fit where and how best to maximize each scenario of property combinations for lifesaving.

What this means for APA! team members and supporters is that change – but exciting change – is on the horizon very soon. By this time next year, we could potentially have 4 locations, including TLAC and Tarrytown! With this expanding footprint we are making sure that each potential place provides a drastic improvement to what we have now. We know that a shelter needs to serve the purposes it should – not mass housing in uncomfortable kennels but getting each animal who needs us most the care, support and rehabilitation they need to get them ready for a home (whether it be foster or adoptive home) and out of kennel as quickly as possible!

We will continue to keep you informed of our property progress and your support we’ll need during this exciting time. Thank you as always for being part of this amazing lifesaving community for people and pets.

There are only seven days until the final October City Council meeting agenda must be posted.

That means we have seven days to make it clear to the city council members that No Kill in Austin is important and deserves their urgent attention.

There are many layers to this problem, but right now one of the most important things that you, as a supporter of the animals who need us to save their lives, can know is that we simply need a relationship with the city that makes sense.

APA! has kept Austin No Kill by taking animals off the city’s kill list every single day for 10 years now. We will continue to do that. We will not agree to continue serving as Austin Animal Center’s overflow partner. It doesn’t make sense to our mission as a nonprofit organization or the pets that never get a chance to leave a shelter alive.

It is no longer fair to serve as an overflow partner for Austin Animal Center anymore for two main reasons:

First, the rebuildable land leased to APA! by the City of Austin has been dramatically reduced to just one fourth of what we were promised in the Lamar Beach Master Plan. This is not reflected anywhere in the negotiations with city staff or in our actual license agreement. It is as if it doesn’t matter. But it does matter to us because, once we sign an agreement, we cannot use the property in the future the way we have been for the last 10 years. This means we can not build anything new on this property that will even come close to matching our current capacity. It is unreasonable to expect APA! to provide the same level of services to the City when the property we have been given in exchange for those services has been so significantly reduced.

Second, the City of Austin Animal Center has received over $10,000,000 more dollars per year than they had when Austin first became a No Kill city. Our mission is to eliminate the killing of pets in shelters and as long as an animal is at risk in Austin, we will save it. It is not reasonable to ALSO ask APA! to provide free services to Austin Animal Center that they’ve been funded to provide to Austin people and animals.

We believe that APA’s support of the City of Austin, in keeping Austin No Kill and driving the city to be progressive and sustainable, is worth the land we are being given. City Council will have to decide if they agree. Please contact your council member’s office today with an email and follow-up call if you agree. It is so important that the council offices hear your voice before they make the final determination.

As the second installment in a short series of letters meant to inform you of APA!’s relationship with the City of Austin, we wanted to bring you up to speed on the Town Lake Animal Center (TLAC) property and how it impacts the renegotiation of our license agreement to operate APA!.

Built in the 1950s, the TLAC facility was a huge improvement over what existed before, which was a structure somewhere in Austin that held all the animals in a massive concrete pen without adequate food and water until they were all shot, in front of an audience, when their time was up. The beginning of sheltering in Austin, as in the entire United States, was rooted in the fear of a nationwide pandemic of Rabies.

Austin American Statesman, 1951Austin American Statesman, 1956, laying the pad for the original Ringworm facility and the original Building C

As such, from 1950 all the way until 2008, the intention of housing the animals was never to save them all or any percent close to that. The original purpose of this facility, in fact, was to continue ridding Austin of dogs and cats who didn’t have owners with the means to reclaim them. TLAC and the structures that still stand today serve as an important reminder for all of us of a past that we never want to go back to.

Austin American Statesman, 1977, when TLAC was occupied by the Humane Society

In 2007, the city made the decision to vacate TLAC and embarked on hiring an architect to build a new shelter in East Austin. There was a lot of controversy over the planned move because it would involve removing lost and homeless animals from downtown Austin. The concerns were threefold:

A lack of visibility would lead to more deaths (now substantiated by the commercial market). Then mayor, Lee Leffingwell, compromised, promising the citizens of Austin there would always be an adoption center at TLAC, even after the move.

The new shelter had fewer kennels than TLAC. Staff asserted that more animals could be co-housed at the new shelter so it actually served the same number of pets. Unfortunately, at the time, almost all big dogs were being killed so co-housing was only intended for little dogs.

The addition at the new site of a huge incinerator so the pets who were killed would no longer have to be sent to the city dump in large truck fulls. Luckily, this was struck from the final plans because it was a big expense for a practice that was going to stop.

In the end, the new shelter was approved and slated to open in mid 2011 with the understanding that the old TLAC facility, already in disrepair, would be demolished.

By 2008, APA! started rescue work and began pulling animals from the TLAC euthanasia list so that we could make a measurable impact on the live release rate in the City of Austin. Our goal was to make Austin a No Kill City as fast as humanly possible. At this time, the city was at only a 45% live release rate with 10,000 to 14,000 animals dying every year. APA! volunteers showed up every day to see the animals listed to be killed by 11:30am the following morning, and pull as many as we could into foster homes.

By 2010, when Austin had a 72% live release rate (largely up because of APA!), the city council, championed by Mike Martinez and Laura Morrison and at the recommendation of the Animal Advisory Commission, voted to formally make Austin a No Kill City with a goal of a 90% live release. In the No Kill Implementation Plan that was passed with this vote, a section included keeping open an adoption center at TLAC, specifically by using the Davenport Building (TLAC’s main admin building), after the city shelter moved to its new location. Of course, we already had our eye on using TLAC as our future facility though we heard from Council offices we had a 0% chance of getting it.

By 2011, the year of the city shelter move, APA! helped the city achieve an 89% live release rate. And now we were openly advocating for taking over the old shelter (TLAC) so that we could continue to help Austin and have a building for our organization.

Surprisingly, APA! had to overcome massive obstacles to be able to occupy TLAC, even though it was empty and even though we were the driver of No Kill. The city had plans to tear it down, due to the dilapidated conditions that existed well before we started rescue. The city couldn’t sell it or use it to build anything other than a park or animal shelter since it is dedicated park land with a grandfather clause for animals. At the time, we had a rocky relationship with the city shelter staff due to the nature of how we supported them, by pulling animals off the euthanasia list rather than taking animals they wanted us to take who may or may not ever have been in danger of euthanasia. Although we were awarded the temporary use of TLAC, that relationship made it very hard to keep Lamar Beach for animals, even after we moved in.

In 2017, city council voted, this time championed by council members Kathie Tovo, Leslie Pool, Alison Alter, Steve Adler, Greg Casar to allow APA! to rebuild at TLAC and stay for 75 years, basing future plans on a document called the Lamar Beach Master Plan, that showed the general space we would occupy and what our buildings might look like.

Essentially, in Phase II of the master plan, with an unknown timeline, Cesar Chavez would be moved away from the lake and cross right through our current footprint. To accommodate that, APA! needed to move back towards the YMCA and the railroad track. In that vote, the council directed city staff to “negotiate and execute” the 75 year agreement over the next four years.

You might be thinking, who would want to build when we are sandwiched between Cesar Chavez and the railroad tracks? We would! We had looked for other property throughout Austin but faced neighborhood overlays that have a blanket clause requiring kennels to be voted on by the neighborhood. That was a painful and exhausting process and it was clear the only neighborhood in Austin that wanted us was the one right around TLAC. With the neighborhood restrictions throughout the City of Austin, we faced finding a property outside the city limits which would eliminate visibility of our important work. At the time, we abandoned the idea of an alternate location.

We began these negotiations, sure about our ability to rebuild based on the Master Plan, and expected to get to the 75 year contract signing quickly. However, as soon as the surveyors and architects got busy, it was made clear to us that land issues would halt immediate plans to fundraise and improve the shelter facilities at TLAC. These issues are detailed below:

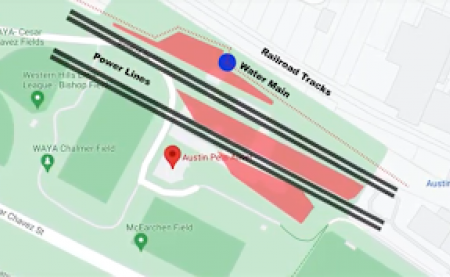

The power lines over us are the heaviest duty type of transmission power line there is, meaning they cannot be buried. We worked hard with Austin Energy and there is no way around them. Nothing can be built on 30 feet of either side of them. We have TWO sets that run from one side to the other, eliminating over 120 feet of buildable space in a longitudinal section.

We have broached the subject of heavy renovations under the power lines since the power lines were raised after our buildings were built, but Austin Energy has assured us that any site plan request that comes through for renovation will be denied because they believe it is in our best interest to get out from under the lines.

There is a 72” water main that runs from the railroad tracks down to Cesar Chavez that cannot be built over and cannot be moved.

The railroad hill is partially owned by the railroad company and would cost $1M to purchase each of two small chunks that would be technically on our property.

The floodplain is outside the land we would be building on but it prevents us from moving our footprint anywhere else on the land and going through the process of demanding that the master plan be reviewed again.

The property known to us as the “Y Field” in the northeast corner behind us, is where we would be pushed to and it is currently owned by YMCA. In order for us to gain formal access to it, the Y and the city have to finish the agreement that requires the city to build a parking garage on Y property, closer to Cesar Chavez. The status of this is unclear, holding up our ability to formally attain the Y field that would be needed for us to build on.

There are many heritage trees on the property that we do not want to harm and that would be quite expensive to move.

After years of discussion with many city departments that control the entities above, it is clear that whatever space we have left at TLAC will likely be a fourth to a third of the size of the footprint we use today.

As a result, we believe we have no choice but to purchase another property, hopefully for use in addition to TLAC, in order to serve our full mission. This will prove difficult because of the neighborhood restrictions that exist in seemingly every neighborhood within the city limits. We are currently pursuing all leads on land within 30 minutes of downtown Austin for what we hope is ultimately a satellite facility.

So what does that have to do with the negotiation of our license agreement? It means that after years of discussion with many city departments, we have come to learn whatever space we have left at TLAC will likely be just a quarter to third of the footprint we use today. We are bitterly disappointed with this outcome and believe we have no choice but to add a second site because the city cannot fulfill all of our land needs as we once thought. The bottom line is the millions of dollars our non-profit organization provides in lifesaving services to the City of Austin annually, and will spend building at the site, far exceeds the value of having free land to build upon.

I want to be clear, we still want to rebuild whatever we can at TLAC because we believe the extra cost to us is worth it for our mission and for Austin. We know it is necessary for pets to be front and center in our city and if we leave, TLAC will never be used to help animals again. We know our city believes in No Kill as one of its core community principles. Our vision for the future of this land is to use it to show the world that No Kill is a crown jewel of Austin. It should serve as a Phoenix, rising from the ashes of the 500,000 pets that needlessly lost their lives at this site over the last 70 years, and be a sign that history will never repeat itself on Austin’s watch again.

We will continue to keep you updated on these matters and hope you, as one of our valued supporters, will help advocate for keeping the TLAC property for the animals after this short letter series ends. We will continue to look for new property regardless of what happens at TLAC and appreciate the leads our supporters send us. If you think you might have a land lead to send our way, you can find details of what we are looking for here.

As always, we are grateful for the support you have shown to APA! staff and to the pets that are counting on us. If our history has taught us anything, it’s that Austin believes in the value that animals bring to all of our lives and expects us to do everything we can to save them. Thank you for joining us and committing so much to this mission.

Thank you,

Ellen Jefferson, DVM President and CEO Austin Pets Alive!/American Pets Alive!