Keith Gill better known as Roaring Kitty.Photo: STRMX (AP)

Keith Gill, the popular investor who sparked the skyrocketing of GameStop’s stock back in 2021 and appears to be back at it again, might have his E*Trade account shut down, according to a report from the Wall Street Journal Monday. The stock trading platform and its owner Morgan Stanley reportedly have concerns about possible stock manipulation, sources familiar with the matter told the Journal.

Evil’s Michael Emerson on Working Opposite a Giant, Hairy, Five-Eyed Demon

Gill, who’s known best as Roaring Kitty, began tweeting on his account on May 12 after almost three years of silence. Most of the posts consist of memes or video clips so it’s unconfirmed if Gill is the one in control of the account. His account on Reddit has also begun posting screenshots of his portfolio with E*Trade showing various bets on GameStop with a screenshot from Tuesday showing his assets valued at $289 million.

Morgan Stanley did not have a comment when asked for confirmation of the report. Gill didn’t immediately respond to a direct message sent over X.

Since the Roaring Kitty account restarted, GameStop stock has taken off, but not nearly the same as it did back in 2021. The video game retailer’s stock was trading at just over $17 on May 10 and shot up to almost $65 on May 14, two days after the May 12 post. Since then, the stock has been steadily losing value only to then jump in price again on Monday following another post from the Roaring Kitty account.

While Gill could be making hundreds of millions from his recent stock bets, it’s very unlikely we’ll see another instance of GameStop’s shares reaching $483 as it did in 2021. Back then, it was in the middle of the pandemic so people were at home paying where they could pay attention to finance moves like that and also were sitting on extra money thanks to various stimulus checks.

JetBlue Airways Corp. and Spirit Airlines Inc. said late Friday that they have appealed a court ruling that earlier this week blocked their planned merger.

JetBlue JBLU, -1.19%

and Spirit SAVE, +17.19%

announced the appeal in a terse press release that provided no more details, adding only that the process is “consistent with the requirements of the merger agreement.”

Wall Street was split on whether the airlines would be legally obliged to appeal the Tuesday ruling, which sided with the Justice Department in saying that a merger between low-cost JetBlue and ultra-low-cost Spirit would hurt competition.

Shares of Spirit rallied 12% after hours Friday, while JetBlue shares fell nearly 2%. Analysts at JP Morgan said this week that the ruling freed JetBlue from a “costly merger.”

The likelihood of Spirit attracting a new merger or takeover bid is considered low without a debt restructuring. Frontier Group Holdings Inc. ULCC, -2.13%

and JetBlue competed for Spirit in 2022, with Frontier ultimately bowing out in July of that year.

Raymond James analyst Savanthi Syth said in a note earlier Friday that it was “clear to us that Spirit is pressing JetBlue to appeal the antitrust ruling, but we continue to believe the chances of success are low.”

Syth has estimated that an appeal would take some four to five months.

Shares of Spirit have lost 67% in the past 12 months, while shares of JetBlue are down 41%. The U.S. Global Jets ETF JETS

has lost 9% in the same period. Those losses contrast with gains of 24% for the S&P 500 index SPX.

Distressed-debt giant Oaktree Capital sees big opportunities in credit unfolding over the next few years as a wall of debt comes due.

Oaktree’s incoming co-chief executives Armen Panossian, head of performing credit, and Bob O’Leary, portfolio manager for global opportunities, see a roughly $13 trillion market that will be ripe for the picking.

Within that realm is high-yield bonds, BBB-rated bonds, leveraged loans and private credit — four areas of the market that have only mushroomed from their nearly $3 trillion size right before the 2007-2008 global financial crisis.

“Clearly, the most acute area of risk right now is commercial real estate,” the co-CEOs said in a Wednesday client note. “That’s because the maturity wall is already upon us and it’s not going to abate for several years.”

More than $1 trillion of commercial real-estate loans are set to come due in 2024 and 2025, according to the Mortgage Bankers Association.

A retreat in the benchmark 10-year Treasury yield BX:TMUBMUSD10Y,

to about 4.1% on Wednesday from a 5% peak in October, has provided some relief even though many borrowers likely will still struggle to refinance.

“There’s a need for capital, especially for office properties where there are vacancies, rental growth hasn’t materialized, or the rate of borrowing has gone up materially over the last three years. This capital may or may not be readily available, and for certain types of office properties, it absolutely isn’t available,” the Oaktree team said.

With that backdrop, the firm expects to dust off its playbook from the financial crisis and acquire portfolios of commercial real-estate loans from banks, but also plans to participate in “credit-risk transfer” deals that help lenders reduce exposure.

Oaktree also sees opportunities brewing in private credit, as well as in high-yield and leveraged loans, where “several hundred” of the estimated 1,500 companies that have issued such debt are likely “to be just fine” even if defaults rise, they said.

Another area to watch will be the roughly $26 trillion Treasury market, where Oaktree has some concerns “about where the 10-year Treasury yield goes from here” — given not only the U.S. budget deficit and the deluge of supply that investors face, but also how foreign buyers, once the “largest owners in prior years, may be tapped out.”

COMP

fell Wednesday after strong retail-sales data for December pointed to a resilient U.S. economy, despite the Federal Reserve having kept its policy rate at a 22-year high since July.

TOKYO (AP) — Asian shares slid Wednesday after a decline overnight on Wall Street and disappointing China growth data, while Tokyo’s main benchmark momentarily hit another 30-year high.

Japan’s benchmark Nikkei 225 NIY00, -0.95%

reached a session high of 36,239.22, but reverted lower, last down 0.3% to 35,477. The Nikkei has been hitting new 34-year highs, or the best since February 1990 during the so-called financial bubble. Buying focused on semiconductor-related shares, and a cheap yen helped boost exporter issues.

Hong Kong’s Hang Seng HK:HSCI

tumbled 4% to 15,220.72, with losses building after data showed China hitting its economic growth target of 5.2% for 2023, surpassing government expectations, but short of the 5.3% some analysts expected. The Shanghai Composite CN:SHCOMP

shed 2% to 2,833.62.

Australia’s S&P/ASX 200 AU:ASX10000

slipped 0.2% to 7,401.30. South Korea’s Kospi KR:180721

dropped 2.4% to 2,435.90.

Investors were keeping their eyes on upcoming earnings reports, as well as potential moves by the world’s central banks, to gauge their next moves. Wall Street slipped in a lackluster return to trading following a three-day holiday weekend.

The S&P 500 SPX

fell 17.85 points, or 0.4%, to 4,765.98. The Dow Jones Industrial Average DJIA

dropped 231.86, or 0.6%, to 37,361.12, and the Nasdaq COMP

sank 28.41, or 0.2%, to 14,944.35.

Spirit Airlines SAVE, -47.09%

lost 47.1% after a U.S. judge blocked its takeover by JetBlue Airways JBLU, +4.91%

on concerns it would mean higher airfares for flyers. JetBlue rose 4.9%.

Stocks of banks were mixed, meanwhile, as earnings reporting season ramps up for the final three months of 2023. Morgan Stanley MS, -4.16%

sank 4.2% after it said a legal matter and a special assessment knocked $535 million off its pretax earnings, while Goldman Sachs GS, +0.71%

edged 0.7% higher after reporting results that topped Wall Street’s forecasts.

Companies across the S&P 500 are likely to report meager growth in profits for the fourth quarter from a year earlier, if any, if Wall Street analysts’ forecasts are to be believed. Earnings have been under pressure for more than a year because of rising costs amid high inflation.

But optimism is higher for 2024, where analysts are forecasting a strong 11.8% growth in earnings per share for S&P 500 companies, according to FactSet. That, plus expectations for several cuts to interest rates by the Federal Reserve this year, have helped the S&P 500 rally to 10 winning weeks in the last 11. The index remains within 0.6% of its all-time high set two years ago.

Treasury yields BX:TMUBMUSD10Y

have already sunk on expectations for upcoming cuts to interest rates, which traders believe could begin as early as March. It’s a sharp turnaround from the past couple years, when the Federal Reserve was hiking rates drastically in hopes of getting high inflation under control.

Easier rates and yields relax the pressure on the economy and financial system, while also boosting prices for investments. And for the past six months, interest rates have been the main force moving the stock market, according to Michael Wilson, strategist at Morgan Stanley.

He sees that dynamic continuing in the near term, with the “bond market still in charge.”

For now, traders are penciling in many more cuts to rates through 2024 than the Fed itself has indicated. That raises the potential for big market swings around each speech by a Fed official or economic report.

On Wall Street, Boeing fell to one of the market’s sharper losses as worries continue about troubles for its 737 Max 9 aircraft following the recent in-flight blowout of an Alaska Air ALK, -2.13%

jet. Boeing BA, -7.89%

lost 7.9%.

In energy trading, benchmark U.S. crude CL00, -1.55%

lost 90 cents to $71.75 a barrel. Brent crude BRN00, -1.37%,

the international standard, fell 78 cents to $77.68 a barrel.

In currency trading, the U.S. dollar USDJPY, +0.44%

rose to 147.90 Japanese yen from 147.09 yen. The euro EURUSD, -0.10%

cost $1.0868, down from $1.0880.

It’s that time of year again: Leaders, business titans, philanthropists and celebs descend on the Swiss ski town of Davos to discuss the fate of the world and do deals/shots with the global elite at the annual meeting of the World Economic Forum.

This year’s theme: “Rebuilding trust.” Prescient, given the dumpster fire the world seems to be turning into lately, both literally (climate change) and figuratively (where to even begin?).

As always, the Davos great and good will be rubbing shoulders with some of the world’s absolute top-drawer dirtbags. While there’s been a distinct dearth of Russian oligarchs in attendance at the WEF since Moscow launched its full-scale invasion of Ukraine in February 2022, and Donald Trump will be tied up with the Iowa caucus, there are still plenty of would-be autocrats, dictators, thugs, extortionists, misery merchants, spoilers and political pariahs on the Davos guest list.

1. Argentine President Javier Milei

Known as the Donald Trump of Argentina — and also as “The Madman” and “The Wig” — the chainsaw-wielding Javier Milei has it all: a fanatical supporter base, background as a TV shock jock, libertarian anarcho-capitalist policies (except when it comes to abortion), and a … memorable … hairdo.

A long-time Davos devotee (he’s been attending the WEF for years), Milei’s libertarian policies have turned from kooky thought bubbles to concerning reality after he was elected president of South America’s second-largest economy, riding a wave of discontent with the political establishment (sound familiar?). The question now is how far Milei will go in delivering on his campaign promises to hack back public service and state spending, close the Argentine central bank and drop the peso.

If you do get stuck talking to Milei in the congress center or on the slopes, here are some conversation starters …

Rumor has it that Mohammed bin Salman will make his first in-person WEF appearance at this year’s event, accompanied by a giant posse of top Saudi officials.

It’s the ultimate redemption arc for the repressive authoritarian ruler of a country with an appalling human rights record — who, according to United States intelligence, personally ordered the brutal assassination of Washington Post journalist Jamal Khashoggi inside the Saudi consulate in Istanbul in 2018.

Rumor has it that Mohammed bin Salman will make his first in-person WEF appearance at this year’s event | Leon Neal/Getty Images

Perhaps MBS would still be a WEF pariah — consigned to rubbing shoulders with mere B-listers at his own Davos in the desert — if it were not for that other one-time Davos-darling-turned-persona-non-grata: Russian President Vladimir Putin. By launching his invasion of Ukraine, which killed thousands of civilians and hundreds of thousands of troops, Putin managed to push the West back into MBS’ embrace. Guess it’s all just oil under the bridge now.

Here’s a piece of free advice: Try to avoid being caught getting a signature MBS fist-bump. Unless, of course, you’re the next person on our list …

3. Jared Kushner, founder of Affinity Partners

Jared Kushner is the closest anyone on the mountain is likely to come to Trump, the former — and possibly future — billionaire baron-cum-anti-elitist president of the United States of America.

On the one hand, a chat with The Donald’s son-in-law in the days just after the Iowa caucus would probably be quite a get for the Davos devotee. On other hand … it’s Jared Kushner.

The 43-year-old, who is married to Ivanka Trump and served as a senior adviser to the former president during his time in office, leveraged his stint in the White House to build up a lucrative consulting career, focused mainly on the Middle East.

Kushner’s private equity firm, Affinity Partners, is largely funded through Gulf countries. That includes a $2 billion investment from the Saudi Public Investment Fund, led by bin Salman — which was, coincidentally, pushed through despite objections by the crown prince’s own advisers.

Kushner struck up a friendship and alliance with MBS during his father-in-law’s term in office, raising major conflict-of-interest suspicions for the Trump administration — especially when the then-U.S. president refused to condemn the Saudi leader in Jamal Khashoggi’s murder, despite the CIA concluding he was directly involved.

Running Azerbaijan is something of a family business for the Aliyevs — Ilham assumed power after the death of his father, Heydar Aliyev, an ex-Soviet KGB officer who ruled the country for decades. And the junior Aliyev changed Azerbaijan’s constitution to pave the path to power for the next generation of his family — and appointed his own wife as vice president to boot.

5. Chinese Premier Li Qiang

Li Qiang is Chinese President Xi Jinping’s ultra-loyal right-hand man, and will represent his boss and his country at the World Economic Forum this year.

Li’s claim to infamy: imposing a brutal lockdown on the entirety of Shanghai for weeks during the coronavirus pandemic, which trapped its 25 million-plus inhabitants at home while many struggled to get food, tend to their animals or seek medical help — and tanking the city’s economy in the process.

Li’s also the guy selling (and whitewashing) China’s Uyghur policy in the Islamic world. In case you need a refresher, China has detained Uyghurs, who are mostly Muslim, in internment camps in the northwest region of Xinjiang, where there have been allegations of torture, slavery, forced sterilization, sexual abuse and brainwashing. China’s actions have been branded genocide by the U.S. State Department, and as potential crimes against humanity by the United Nations.

Li Qiang will represent his boss and his country at the World Economic Forum this year | Johannes Simon/Getty Images

Nicknamed “the Napoleon of Africa” in a nod to his campaign to seize power in 1994, Paul Kagame has ruled over the land of a thousand hills since. He’s often praised for overseeing what is probably the greatest development success story of modern Africa; he’s also a dictator.

Forced from office in 2018 by mass protests following the murder of investigative journalist Ján Kuciak and his fiancée Martina Kušnírová, Fico rose from the political ashes to become Slovakian prime minister for the fourth time late last year. His Smer party ran a Putin-friendly campaign, pledging to end all military support for Ukraine.

Slovakian courts are still working through multiple organized crime cases stemming from the last time Smer was in power, involving oligarchs alleged to have profited from state contracts; former top police brass and senior military intelligence officers; and parliamentarians from all three parties in Fico’s new coalition government.

8. President of Hungary Katalin Novák

Katalin Novák, elected Hungarian president in 2022, must’ve pulled the short straw: she’s been sent to Davos to fly the flag for the EU’s pariah state. Luckily, the 46-year-old is used to being the odd one out at a shindig: She’s both the first woman and the youngest-ever Hungarian president.

It’s her thoughts on the gender pay gap, though, that ought to get attention at the famously male-dominated World Economic Forum: In an infamous video posted back in late 2020, Novák told the sisterhood: “Do not believe that women have to constantly compete with men. Do not believe that every waking moment of our lives must be spent with comparing ourselves to men, and that we should work in at least the same position, for at least the same pay they do.” That’s us told.

9. Cambodian Prime Minister Hun Manet

You may be surprised to see Hun Manet on this list: The new, Western-educated Cambodian prime minister has been touted in some circles as a potential modernizer and reformer.

But Hun Manet is less a breath of fresh air and a lot more continuation of the same stale story. Having inherited his position from his father, the longtime autocrat Hun Sen, Hun Manet has shown no signs of wanting to reform or modernize Cambodia. While some say it’s too early to tell where he’ll land (given his dad’s still on the scene, along with his Communist loyalists), the fact is: Many hallmarks of autocracy are still present in Cambodia. Repression of the opposition? Check. Dodgy “elections”? Check. Widespread graft and clientelism? Check and check.

10. Qatar Prime Minister Mohammed bin Abdulrahman bin Jassim al-Thani

How has a small kingdom of 2.6 million inhabitants in the Persian Gulf managed to play a starring role in so many explosive scandals?

Mohammed bin Abdulrahman bin Jassim al-Thani is the prime minister of Qatar, a country that’s played a starring role in many explosive scandals | Chris J. Ratcliffe/AFP via Getty Images

You’d think that sort of record would see Mohammed bin Abdulrahman bin Jassim al-Thani shunned by the world’s top brass. Nah! Just this month, U.S. Secretary of State Antony Blinken met with the Qatari leader and told him the U.S. was “deeply grateful for your ongoing leadership in this effort, for the tireless work which you undertook and that continues, to try to free the remaining hostages.”

See you on the slopes, Mohammed!

11. Polish President Andrzej Duda

When you compare Polish President Andrzej Duda to some of the others on this list, he doesn’t seem to measure up. He’s not a dictator running a violent petro-state, hasn’t invaded any neighbors or even wielded a chainsaw on stage.

But Duda is yesterday’s man. As the last one standing from Poland’s nationalist Law and Justice party that was swept out of office last year, Duda’s holding on for dear life to his own relevance, doing his best to act as a spoiler against the Donald Tusk-led government by wielding his veto powers and harboring convicted lawmakers. All of which is to say: When you catch up with President Duda at Davos, don’t assume he’s speaking for Poland.

12. Amin Nasser, CEO of Aramco

The Saudi Arabian state oil and gas company is Aramco — the world’s biggest energy firm — and Amin Nasser is its boss. If you read Aramco’s press releases, you’d be forgiven for assuming it is also the world’s biggest champion of the green energy transition. Spoiler alert: It’s far from it.

Exhibit A: Aramco is reportedly a top corporate polluter, with environment nongovernmental organization ClientEarth reporting that it accounts for more than 4 percent of the globe’s greenhouse gas emissions since 1965. Exhibit B: Bloomberg reported in 2021 that it understated its carbon footprint by as much as 50 percent.

Nasser, meanwhile, has criticized the idea that climate action should mean countries “either shut down or slow down big time” their fossil fuel production. Say that to Al Gore’s face!

This article has been updated to reflect the fact Shou Zi Chew is no longer going to attend the World Economic Forum.

Dionisios Sturis, Peter Snowdon, Suzanne Lynch and Paul de Villepin contributed reporting.

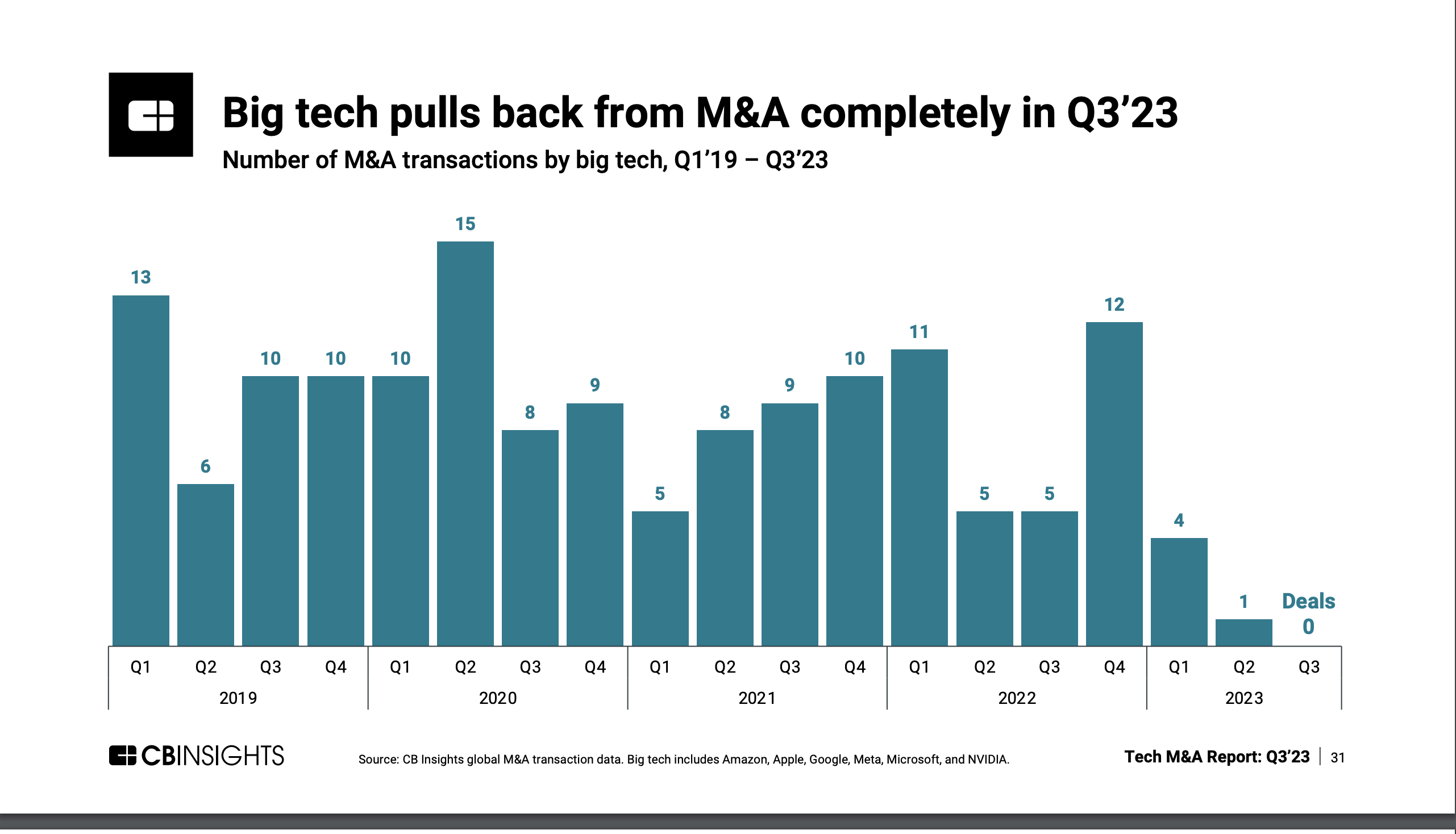

It’s that time of year when we look back at the year’s biggest tech M&A deals. Typically by this time, the usual acquisitive suspects like Microsoft, Salesforce, Adobe, SAP Oracle and Cisco have taken at least a few big swings. But this year, only Cisco took a big bite, ultimately announcing 11 total deals.

SAP made a couple smaller deals, but Microsoft, Salesforce, Adobe and Oracle mostly stayed on the sidelines this year. The $61 billion Broadcom-VMware deal announced in May 2022 finally closed last month, and Adobe and Figma agreed to end their $20 billion deal this month, which has been stuck in regulatory limbo since it was announced in September 2022.

It’s not our imagination that there are fewer deals from the biggest players. CB Insights reported zero deals in Q3 this year from Big Tech. Compare that with 2019, when there were 10 such deals in Q3, or with 2020, when there were eight.

Image Credits: CB Insights

Perhaps the high cost of borrowing put a damper on the deals we saw in 2023. Long gone are the days of 2020 when the top deals totaled $165 billion. This year it was just $67.7 billion, the lowest total we’ve seen since 2019’s all-time low of $40 billion, the second year we compiled these top deal lists.

It’s worth noting that a good number of the deals this year involved private equity firms either buying companies or selling them off at a nice profit.

Maybe the smaller deals involving AI mattered more, like Atlassian buying Loom for $975 million; Salesforce acquiring Airkit.ai for an undisclosed amount, one of only two small acquisitions this year; or Snowflake nabbing AI search company Neeva, also for an undisclosed amount.

Regardless, here’s what the top 10 enterprise deals looked like this year from cheapest to most costly:

Alteryx, an Irvine, California-based software company developing data science and analytics products, today announced that it’s agreed to be acquired by private equity firms Clearlake Capital Group and Insight Partners in a deal worth $4.4 billion.

Clearlake and Insight reportedly beat out Symphony Technology Group, another private equity firm, which Reuters reported several days ago had been vying for Alteryx.

The Clearlake-Insight deal, which includes debt, values Alteryx’s equity at around $3.46 billion, reports Reuters — a 29.1% premium over the company’s closing share price on Friday. It’s expected to close in the first half of 2024 subject to customary closing conditions and approvals.

The immediate impact on Alteryx’s ~2,900 employees isn’t clear.

“In addition to delivering significant and certain cash value to our stockholders, this transaction will provide increased working capital and industry expertise — and the flexibility as a private company,” Alteryx CEO Mark Anderson said in a statement. “Over the past several years, we’ve executed a comprehensive transformation strategy to enhance our go-to-market capabilities and establish a strong cloud and AI innovation roadmap. We’re excited to partner with Clearlake and Insight for the next stage of Alteryx’s journey.”

SRC, the predecessor to Alteryx, was co-founded in 1997 by Dean Stoecker, Olivia Duane Adams and Ned Harding and initially focused on creating data engines for demographic-based mapping and reporting. In 2006, SRC released the software app Alteryx as a platform for building analytical processes and services. By 2011, SRC had changed its name to Alteryx, which by then had become its core product.

After raising tens of millions of dollars from VC firms including Toba Capital, Insight, Sapphire Ventures, ICONIQ Capital and Meritech Capital Partners, Alteryx went public on the NYSE in 2017.

More recently, Alteryx transitioned to a subscription-focused business model — and greatly expanded its AI-powered feature offerings — as part of a strategy to tap into growing demand for data analytics services. According to the analyst firm Research and Markets, the big data analytics market could be worth $105.08 billion by 2027, up from $37.34 billion in 2018.

Alteryx now counts more than 8,300 companies as its customers, including Coca-Cola, Vodafone, Walmart and Ford. In its coverage of the deal today, SiliconAngle notes that Alteryx generated $232 million in sales last fiscal quarter, up 8% from the same time a year ago, and that its annualized recurring revenue grew nearly three times as fast in the same time frame, jumping roughly 21% to $914 million.

“When we founded Alteryx in 1997, we did so with a vision for the future of data science and analytics. Today, Alteryx stands out as an industry leader with a differentiated platform that scales data democratization in a governed manner,” Stoecker said. “Our agreement with Clearlake and Insight validates the strength of our business and the value of Alteryx’s capabilities and innovation.”

Private-equity funds aimed at wealthy individuals continue to draw in fresh capital as the universe of alternative investments grows beyond its roots serving endowments, pension funds and other institutions, according to industry data.

Registered funds that take investments from individuals and smaller institutions rose by about $125 billion in 2022 from the previous year to total assets under management (AUM) of $425 billion, according to data from private-equity investor and data provider Hamilton Lane Inc. HLNE.

RedBird IMI has agreed a loan package with the Barclay family that would let it take control of the Telegraph newspaper and Spectator magazine, a prospect that’s sparked concern among Conservative lawmakers because of the fund’s ties to Abu Dhabi.

The media investment vehicle, which is a joint venture between RedBird Capital Partners and the United Arab Emirates-based International Media Investments, said in a statement Monday that it had agreed to lend the Barclay family £600 million ($750 million), secured against the politically influential titles.

“Under the terms of this agreement, RedBird IMI has an option to convert the loan secured against the Telegraph and Spectator into equity, and intends to exercise this option at an early opportunity,” the investment vehicle said in a statement.

Lloyds Banking Group Plc seized the Telegraph titles along with the Spectator magazine from the Barclay family in June to claw back debts, removing Barclay family members from their director positions and placing the businesses in receivership. The RedBird IMI loan will help the Barclay family to pay off the debt owed to Lloyds.

Separately, IMI will lend a further £600 million secured against other Barclay family businesses and commercial interests. IMI is a private investment vehicle for Sheikh Mansour Bin Zayed Al Nahyan, according to a spokesman for RedBird IMI, whose statement emphasized IMI’s involvement would be passive.

“Following transfer of ownership, RedBird Capital alone will take over management and operational responsibility for the titles under the leadership of RedBird IMI Chief Executive Jeff Zucker,” the statement said, referring to the former president of CNN. “International Media Investments will be a passive investor only.”

Still, RedBird IMI’s statement will likely heighten concern among Conservative lawmakers, who are pushing the UK government to scrutinize the UAE’s involvement. Lawmakers have described any possible influence of the UAE royal family over the Telegraph as “a risk to our national security,” citing its record on press freedom and position on Israel.

The prospect of foreign influence on the title has already raised concerns among senior ministers including Kemi Badenoch and Tom Tugendhat, Bloomberg News reported Saturday.

“Any transfer of ownership will of course be subject to regulatory review,” RedBird IMI said in its statement, which pledged to maintain the existing editorial team of the publications. “We will continue to cooperate fully with the government and the regulator.”

Even before that, UK Culture Secretary Luzy Frazer could issue a so-called Public Interest Intervention Notice. That would launch a study of the deal by British regulators. She could also freeze the transaction while that happens, if she chooses. The antitrust watchdog – the CMA – and media regulator Ofcom will report findings on antitrust and media issues respectively, to inform Frazer’s final decision, which could see her clear the deal, block it, or impose conditions.

Subscribe to the new Fortune CEO Weekly Europe newsletter to get corner office insights on the biggest business stories in Europe. Sign up before it launches Nov. 29.

Carnage in the bond market in September could tee up an opportunity for investors to earn big returns on U.S. government debt in a year.

Owners of 10-year Treasury BX:TMUBMUSD10Y

notes at recent yields of around 4.5% could reap up to 20% in total returns in a year if the U.S. economy stumbles into a recession, according to UBS Global Wealth Management.

The key would be for U.S. debt to rally significantly as investors scramble for safety in the roughly $25 trillion treasury market.

“U.S. yields remain well above long-term equilibrium levels, providing scope for them to fall as the macroeconomic outlook becomes more supportive for bonds,” a team led by Solita Marcelli, chief investment officer Americas at UBS Global Wealth Management, wrote in a Friday client note.

Their base-case call is for the 10-year Treasury yield to fall to 3.5% in 12 months, with it easing back to 4% in an upside scenario for growth, and for the economy’s benchmark rate to tumble as low as 2.75% in a downside scenario of a U.S. recession.

“That would translate into total returns over the period of 14% in our base case, 10% in our upside economic scenario, and 20% in our downside scenario.”

A rally in Treasury debt could help boost funds that track the Treasury market and the broader U.S. bond sector. The popular iShares 20+ Year Treasury Bond ETF TLT

was down 10.9% on the year through Friday, while the iShares Core U.S. Aggregate Bond ETF AGG

was 3% lower, according to FactSet.

A tug of war has been developing in the Treasury market, with fear gripping investors this week as bond yields spike in the wake of signals last week from the Federal Reserve that interest rates may need to stay higher for longer than many on Wall Street anticipated.

Much hinges on how painful things get if rates stay high, which would ratchet up borrowing costs for households, companies and the U.S. government as the Fed works to get falling inflation down to its 2% target.

Hedge-fund billionaire Bill Ackman this week said he thinks Treasury yields are going higher in a hurry, as part of his bet that the 30-year Treasury yield BX:TMUBMUSD30Y

has more room to climb.

The 10-year Treasury edged lower to 4.572% on Friday, after adding almost 50 basis points in September, which helped the stock market reclaim some lost ground in a dismal month, while the 30-year Treasury yield pulled back to 4.709%, according to FactSet.

The Dow Jones Industrial Average DJIA

posted a 3.5% decline in September, its biggest monthly loss since February, the S&P 500 index SPX

fell 4.8% and the Nasdaq Composite Index COMP

shed 5.8% for the month.

Shares of investment giant Blackstone Inc. and vacation-home rental platform Airbnb Inc. rallied after hours on Friday after both won the nod to join the S&P 500 index SPX

later this month.

The announcement, from S&P Dow Jones Indices, said that the change would take hold before the start of trading on Monday, Sept. 18. The move, among others announced Friday, will “ensure each index is more representative of its market-capitalization range,” according to a release.

Airbnb ABNB, +0.87%

currently has a market value of $83.98 billion, and its shares are up 64.7% so far this year. Blackstone BX, -1.77%,

currently worth $129.29 billion, has seen its stock rise 43.6% year-to-date.

Shares of Airbnb and Blackstone were up 5.7% and 4.8%, respectively, after hours on Friday.

Blackstone and Airbnb will replace Lincoln National Corp. LNC, +2.14%

and Newell Brands Inc. NWL, +1.23%

in the index, S&P Dow Jones Indices said on Friday. In the process, Lincoln and Newell will join the S&P SmallCap 600.

“We’ve established an unparalleled global platform of leading business lines, offering over 70 distinct investment strategies,” Chief Executive Stephen Schwarzman told analysts. “We believe our clients view us as the gold standard in alternative asset management.”

Meanwhile, Airbnb last month said that travelers were seeking longer stays and bigger properties in pricier areas, as the rebound in travel endures despite a tidal wave of inflation last year. The company’s second-quarter results and third-quarter sales forecast topped Wall Street’s estimates.

Meanwhile, S&P 500 member Deere & Co. DE, +1.94%

will replace Walgreens Boots Alliance Inc. WBA, -7.43%

in the S&P 100, S&P Dow Jones Indices said on Friday. That change also takes hold on Sept. 18. S&P Dow Jones Indices said Walgreens “is no longer representative of the megacap market space” but will stay in the S&P 500.

Shares of Deere fell 0.2% after hours. Walgreens stock was up 0.4%.

A consortium of groups representing the private funds industry filed a lawsuit against the Securities and Exchange Commission Friday in an attempt to block new rules that would require private equity and hedge funds to disclose quarterly performance, fees and expenses.

The rules, adopted last week, would also ban so-called side letters, or agreements between a fund and specific investors that give them preferential treatment, unless those arrangements are made available to all investors.

“The Private Fund Adviser rule will harm investors, fund managers, and markets by increasing costs, undermining competition, and reducing investment opportunities for pensions, foundations, and endowments,” he added.

The MFA was joined by several other industry groups in filing the lawsuit, including the National Association of Private Fund Managers, National Venture Capital Association, American Investment Council, Alternative Investment Management Association and the Loan Syndications & Trading Association.

An SEC spokesperson told MarketWatch that “the Commission undertakes rulemaking consistent with its authorities and laws governing the administrative process, and we will vigorously defend the challenged rule in court.”

SEC Chair Gary Gensler argued in recent speeches and statements that the new rules are necessary to protect investors, including the pension funds and endowments that have increasingly turned to alternative investments in recent years to boost returns.

He said in a May speech that private funds are of growing importance to the U.S. economy, noting that advisers report that they now manage $25 trillion in assets — up from $1 trillion in 1998 — surpassing the size of the U.S. banking sector.

“The private fund industry plays an important role in each sector of the capital markets,” he said.

“It also plays an important role for investors, such as retirement funds and endowments,” he added. “Standing behind those entities are a diverse array of teachers, firefighters, municipal workers, students, and professors.”

The U.S. Labor Day holiday will mark another milestone in the marathon to bring workers back to the office, but it won’t be a quick fix for landlords, according to Thomas LaSalvia, head of commercial real estate economics at Moody’s Analytics.

“A lot of companies are saying that after Labor Day, ‘We expect more out of you,” LaSalvia said, referring to days in the office. Still, office attendance, he argues, likely only stages a fuller comeback if a job or promotion is on the line.

That could prove difficult, with Friday’s U.S. jobs report for August expected to show U.S. unemployment at a scant 3.5%, near the lowest levels since the late 1960s, even if hiring has been slowing. The labor market, so far, appears unfazed by the Federal Reserve’s benchmark rate reaching a 22-year high.

It has been a different story for landlords facing a roughly 19% vacancy rate nationally and piles of debt coming due, especially for owners of older Class B and C office buildings with a bleak outlook or properties in cities with wobbling business centers.

As with shopping malls, LaSalvia said it’s largely a problem of oversupply, with many office properties at risk of becoming obsolete as tenants flock to better buildings and locations staging a rebirth. The trend can be traced in leasing data since 2021, with Class A properties in central business districts (blue line) showing a big advantage over less desirable buildings in the heart of cities (orange line).

Return to office isn’t going to save the entire office property market

Moody’s Analytics

“Little by little, we are finding the office isn’t dead,” LaSalvia said, but he also sees more promise in neighborhoods with a new purpose, those catering to hybrid work and communities that bring people together.

Another way to look at the trend is through rents. Manhattan’s Penn Station submarket, with its estimated $13 billion overhaul and neighboring Hudson Yards development, has seen asking rents jump 32% to $74.87 a square foot in the second quarter since the fourth quarter of 2019, according to Moody’s Analytics. That compares with a 2% bump in asking rents in downtown New York City to $61.39 a square foot for the same period.

The push for a return to the office also doesn’t mean a repeat of prepandemic ways. Goldman Sachs analysts estimate that part-time remote work in the U.S. has stabilized around 20%-25%, in a late August report, but that’s still up from 2.6% before the 2020 lockdowns.

Furthermore, the persistence of remote work will likely add another 171 million square feet of vacant U.S. office space through 2029, a period that also will see tenants’ long-term leases expire and many companies opting for less space. The additional vacancies would roughly translate to 57% of Los Angeles roughly 300 million square feet of office space sitting empty.

“The fundamental reason why we had offices in the first place have not completely disintegrated,” LaSalvia said. “But for some of those Class B and C offices, the writing was on the wall before the pandemic.”

U.S. stocks were mixed Thursday, but headed for losses in a tough August for stocks, with the S&P 500 index SPX

off about 1.5% for the month, the Dow Jones Industrial Average DJIA

2.1% lower and the Nasdaq Composite COMP

down 2% in August, according to FactSet.

Stocks closed mostly lower Friday, capping off a bruising week of losses as Treasury yields jumped and China’s mounting property woes gripped investors. The Dow Jones Industrial Average DJIA, +0.07%

rose about 27 points, or 0.1%, ending near 34,501, according to preliminary FactSet data. The S&P 500 index SPX, -0.01%

was nearly flat at 4,370 and the Nasdaq Composite Index COMP, -0.20%

shed 0.2%, despite briefly turning positive late in the session. It still was a tough week for equities, with the Dow booking a 2.2% loss, the S&P 500 index a 2.1% decline and the Nasdaq a 2.6%. The Nasdaq also posted its biggest 3-week decline since December 2022, according to Dow Jones Market Data. Yields on the 10-year Treasury rose for a 5th week in the row, with the benchmark TMUBMUSD10Y, 4.252%

rate briefly touching its highest level since November 2007, before settling back at 4.251% on Friday. China Evergrande’s EGRNF, Chapter 15 bankruptcy filing in New York late Thursday kept focus on the wobbling property market in the world’s second-largest economy. Earlier in the week, Country Garden Group missed a dollar-denominated debt payment. Next week investors will be focused on Federal Reserve Chairman Jerome Powell’s speech on Friday at the Jackson Hole economic summit for hints to whether the central bank is likely done hiking rates in this cycle. The Fed’s policy rate sits at its highest level in 22 years.

Opinions expressed by Entrepreneur contributors are their own.

Many founders looking to sell their businesses consider offers from private equity firms, which typically buy out most of an owner’s stake while giving them a piece of the restructured organization, incentivizing them to fully participate in its transition and scale. These founders are in a unique position to help maximize the future value of their companies by supporting a critical aspect of their evolutions that most private equity firms don’t sufficiently prioritize.

Private equity firms are highly focused on the financial and operational aspects of businesses’ potential, yet only a select few dedicate real, expert attention to the cultures of newly acquired portfolio companies. This can add risk to the strategies designed to grow organizations, as workplace cultures can serve to drive or impede companies’ success, depending on their nuances, and will take form regardless of what actions leaders take. They either develop organically without intention or alignment to strategy or are purposely shaped for organizations’ ultimate benefit.

This offers founders the opportunity to step into the role of culture advocate and champion, helping retain core aspects of their original cultures while sunsetting those that need to evolve. Founders who truly engage fully and openly in this process can help shape a culture 2.0 that honors the history and legacy of their organizations, maintaining the best of what they built, while serving strategic needs as the businesses grow.

A unique and singular role in cultural transitions

Founders across industries — from healthcare services to tech — are known for pouring their hearts and souls into their businesses, all but ensuring the cultures that develop are intertwined with their values, workstyles and preferences. As such, they can have an incredibly strong influence on the design of a refreshed culture that encourages the ideal combination of behaviors that will drive future value creation — from how decisions are made to openness toward new ways of working to how leaders share information.

Of course, founders can also struggle with the idea that the companies they built tirelessly will undergo cultural changes — reflecting the years and often decades they’ve invested in creating positive and productive workplaces. Feelings of defensiveness and distrust are incredibly common, especially for those in service-minded, mission-driven sectors, like healthcare, who rely on a professional vocabulary distant and apart from the world of private equity.

Founders should seek to identify these feelings and recognize what’s driving them, ultimately getting to a place of understanding that the culture that got them “here” won’t take them “there.” Getting “there” will necessitate an intentionally designed culture 2.0. Their participation in the development of such cultures, and openness to new leadership adding their fingerprints to what they’ve created, will best ensure that organizations maintain their “secret sauce” while embarking on their next chapters.

A growing number of top-performing private equity firms are achieving success by supporting the development of strong, healthy workplaces, especially in mission-driven organizations. Increasingly, the savviest of these investors recognize the value of cultural evolution within their portfolio as a driver of growth, although most will admit it’s not their particular area of expertise.

This leaves an opening for founders to advocate for the intentional development of refreshed cultures that accelerate organizations’ journeys to growth and greater profitability while keeping their missions intact. Those who choose to be proactive in this area will overwhelmingly find willing and collaborative partners, as most private equity firms understand the importance of including founders in future-looking conversations. If anything, private equity firms are now so aware of the dangers of imposing their own top-down ethos that they often downplay the risk of inaction with regard to culture.

Of course, founders can only advance these efforts to a point, as their enduring success and bottom-line impacts require more than just an individual proponent. They’ll need buy-in at the board level to greenlight the in-depth, expert work required to maximize results, including analyzing and mapping out the existing and desired future culture, designing and implementing work streams that facilitate a transition from one culture to another and “pulling” new cultural elements through every facet of the company until they become wholly engrained.

The savviest founders are taking an even more proactive and novel approach toward maximizing their workplace cultures. Before putting their businesses up for sale, they’re utilizing third-party experts to independently assess and quantify the value of the people-centric elements of their businesses, including both the cultural strengths they’ve cultivated and also their existing leadership. Not only do these investments significantly reduce the efforts required to intentionally transition cultures after a transaction, but they also increase the value of the companies and boost what buyers are willing to pay for them, shedding light on what has traditionally been an unknown.

These methods and tools are new but catching on, especially as more and more private equity firms, and founders alike, recognize how culture can serve as a barrier or a springboard toward a smooth and profitable exit.

GGV Capital, a prominent Silicon Valley venture capital firm, has become the latest big investor to break up its US and China operations into separate companies as tensions between the two countries over tech and geopolitics continue to rise.

The firm announced Thursday that it would divide its business into two “completely independent” firms with separate new brands, which have not been revealed.

According to the company, one side will concentrate on North America, Latin America, Europe, Israel and cross-border US-India deals, led by teams in California and New York by managing partners Glenn Solomon, Hans Tung, Jeff Richards and Oren Yunger.

The other side will focus on China, Southeast Asia and South Asia, run from its headquarters in Singapore, by managing partners Jenny Lee and Jixun Foo.

GGV’s existing Chinese yuan-denominated funds “will continue to be managed independently” under its Chinese brand, Jiyuan Capital, it said.

In a statement, the firm attributed the decision to the fact that “over the last decade, the investment landscape has shifted significantly, and the operating environment has become highly complex.”

“Against these new realities, GGV is also evolving,” it added, without elaborating further.

The transition is expected to be completed by the end of the first quarter of next year.

GGV Capital has approximately $9.2 billion in assets under management. The firm is known for backing tech companies around the world, such as Alibaba (BABA), Airbnb (ABNB), Slack, TikTok owner ByteDance and Chinese ride-hailing provider Didi.

The move comes as US-China tensions continue to affect how businesses operate across the world’s top two economies.

Last month, the Biden administration announced it would restrict investments by US venture capital and private equity firms, as well as joint ventures, in Chinese artificial intelligence, quantum computing and semiconductors.

The executive order will exacerbate a slump in deals between the United States and China, and deliver a “major blow” to Chinese startups, analysts and investors previously told CNN.

Asked whether theUS order or wider geopolitical tensions had factored into its decision, GGV Capital declined to comment.

The firm has recently come under greater scrutiny from US lawmakers.

In July, a US House committee said it had sent letters to four investment firms, including GGV, “expressing serious concern and demanding information about the firms’ investments” in artificial intelligence, chips and quantum computing companies in China.

One investment named was a GGV deal with Megvii, an AI developer. The company is best known for its facial recognition software, and has long been accused of human rights violations against Uyghurs and other members of Muslim minority groups in China’s Xinjiang region.

Megvii was added to a US trade blacklist in 2019 over the issue and previously told CNN that there were “no grounds” for that decision.

The ongoing pressure has already led other firms to separate their US and Chinese businesses this year.

In June, top global venture capital firm Sequoia announced a similar decision to cordon off its operations into three entities that cover Europe and the United States; China; and India and Southeast Asia. Its China business will be run independently under its Chinese name, Hongshan.

Leaders of the Silicon Valley firm said at the time that it had “become increasingly complex to run a decentralized global investment business.”

In August, Dentons, a leading law firm, also said its China unit would become a standalone legal entity, in response to new Chinese regulations related to data privacy, cybersecurity and capital control.

Elon Musk’s biotechnology startup Neuralink raised $280 million in a fundraising round, the company announced Monday via X, the Musk-owned social media platform formerly known as Twitter.

The Series D round was led by Founders Fund, a San Francisco-based VC firm established by Peter Thiel, the controversial billionaire who was also a cofounder at PayPal.

“We’re extremely excited about this next chapter at Neuralink,” the company wrote.

The brain chip startup wants to use implants to connect your brain to a computer, a goal Musk has been working on for five years. The company so far has only tested on animals and faced scrutiny after a monkey died in project testing in 2022 as part of efforts to get the animal to play Pong, a computer game.

Macaque monkeys have been used in testing by Neuralink as the company has been developing Bluetooth-enabled implantable chips — inserted into the monkey’s brains — that the company says can communicate with computers via a small receiver.

The funding news comes months after Musk announced the company was moving towards human trials. The billionaire said at a December recruiting event that Neuralink has submitted “most” of its paperwork to the US Food and Drug Administration and could begin testing on humans within six months.

But employees have said the company is rushing to market, resulting in careless animal deaths and a federal investigation, according to a December report by Reuters.

Before Neuralink’s brain implants are mass-produced and hit the broader market, they’ll need regulatory approval. The FDA put out a paper in 2021 mapping out the agency’s initial thoughts on brain-computer interface devices, noting the field is “progressing rapidly.”

A tweet by Neuralink Monday announced they were hiring and invited those interested to “join in on engineering challenges to restore vision and mobility.”

Banc of California Inc.’s proposed agreement to acquire PacWest Bancorp. helped send regional-bank stocks considerably higher on Wednesday. But even after a two-day increase of 12% for its shares, the acquiring bank remains the favorite name among analysts covering regional players in the U.S.

The merger agreement was announced after the market close on Tuesday, but the rumor mill had already sent Banc of California’s BANC, +0.62%

stock up by 11% that day. Then on Wednesday, shares of PacWest Bancorp PACW, +26.92%

shot up 27% to $9.76, which was above the estimated takeout value of $9.60 a share when the deal was announced. The merger deal, if approved by both banks’ shareholders, will also include a $400 million investment from Warburg Pincus LLC and Centerbridge Partners L.P.

A screen of regional banks by rating and stock-price target is below.

With PacWest closing above the initial per-share deal valuation, it is fair to wonder whether or not its shareholders will vote to approve the agreement. In a note to clients on Wednesday, Wedbush analyst David Chiaverini called Banc of California’s offer “fair, but not overwhelmingly attractive,” and wrote that PacWest was “a likely seller before the mini banking crisis occurred in March.”

While Chiaverini went on to predict the deal’s approval by PacWest’s shareholders, he added that he “wouldn’t be surprised if there were some dissent among a minority of shareholders [which could] possibly open the door to the potential emergence of a third-party bid.”

More broadly, Odeon Capital analyst Dick Bove wrote to clients on Wednesday that the merger deal, along with increasing involvement of private-equity firms in lending businesses, the expected enhancement of regulatory capital requirements for banks and other factors could lead to more consolidation among smaller banks.

He went on to write that we might be entering a period for the banking industry similar to the 1990s, “when rules were being changed and acquisitions were rampant,” which “created new investment opportunities.”

The SPDR S&P Regional Banking exchange-traded fund KRE, +4.74%

rose 5% on Wednesday but was still down 17% for 2023, while the SPDR S&P 500 ETF Trust SPY, +0.02%

was up 19%, both excluding dividends.

KRE holds 139 stocks, with 98 covered by at least five analysts working for brokerage firms polled by FactSet. Out of those 98 banks, 45 have majority “buy” ratings among the analysts. Among those 45, here are the 10 with the most upside potential over the next 12 months, implied by consensus price targets:

Any stock screen can only be a starting point when considering whether or not to invest. If you see any stocks of interest here, you should do your own research to form your own opinion.

U.S. stocks finished at new highs for the year on Monday to kick off a busy week for corporate earnings, with the Nasdaq leading the way up. The Dow Jones Industrial Average DJIA, +0.22%

rose about 76 points, or 0.2%, ending near 34,585, based on preliminary FactSet data. The S&P 500 index SPX, +0.39%

gained 0.4% and the Nasdaq Composite Index COMP, +0.93%

closed up 0.9%. That was the Dow’s sixth straight day of wins and marked the highest close since April 2022 for all three major stock indexes, according to Dow Jones Market Data. Equities have rallied as the U.S. economy remains resilient in the face of sharply higher interest rates, keeping investors hopeful about a soft landing, instead of a recession. Treasury Secretary Janet Yellen said on Monday that she doesn’t anticipate a U.S. recession, in an interview with Bloomberg television. After several big banks reported on Friday, second-quarter earnings results continue with Tesla, TSLA, +3.20%

Morgan Stanley MS, +0.69%,

Goldman Sachs GS, +0.31%,

Netflix NFLX, +1.84%

and more on deck.

Would Twitter have been better off to remain a public company rather than be taken private by Elon Musk?

We’ll never know for sure, of course. But it’s hard to imagine that it would have performed any worse. Twitter as a private company is hemorrhaging advertisers, and according to a recent Fidelity analysis its market value is down nearly two-thirds from the $44 billion Musk paid for it.

Grading Twitter’s performance as a private company is more than an idle armchair exercise. It goes to the heart of an age-old debate over whether companies can be more profitably managed when private rather than public. The private equity (PE) industry not surprisingly claims that its approach is superior, and much of Wall Street agrees since many PE firms have produced impressive long-term returns.

The industry’s claims are not devoid of dissenters. Consider a recent study from Verdad Capital entitled “Private Equity Operational Improvements.” It was conducted by Minje Kwun of Dartmouth College and Lila Alloula of Yale University.

In order to overcome the otherwise insuperable obstacle of being unable to measure how private companies are performing, the researchers focused on a subset of leveraged buyouts (LBOs) from 1996 to 2021 in which the private equity firms issued public debt. In order to sell debt to the public, of course, the PE firms had to issue financial statements publicly, and that enabled the researchers to analyze the LBOs’ performance after going private, relative to public companies in the same industry sector.

Kwun and Alloula focused on six indicators of financial performance: Revenue growth, EBITDA margin, capital expenditures as a percentage of sales, and the ratios of gross profit to total assets, EBITDA to total assets, and debt to EBITDA. (EBITDA, of course, refers to Earnings Before Interest, Taxes, Depreciation and Amortization.)

Relative to public companies in the same sector over the three years after going private, LBOs on average did not show any operational improvement along these six dimensions. The researchers conclude: “The [private equity] industry mythology of savvy and efficient operators streamlining operations and directing strategy to increase growth just isn’t supported by data.”

Their results are consistent with those of a near-decade ago study by Jonathan Cohn and Lillian Mills of the University of Texas and Erin Towery of the University of Georgia. They used a different technique to access the otherwise inaccessible financial data of newly-private companies: Their tax returns. The professors focused on the operating performance of a sample of companies that had gone private between 1995 and 2007, comparing them to otherwise-similar companies that remained public. On average over the three years after going private, the researchers found, the private companies performed no better than the public ones.

The source of PE’s industry high returns

What, then, is the source of the increased return that the private equity industry often produces? The answer appears to be increased leverage. Leverage increases returns on the upside, even if it magnifies losses on the downside. Leverage has worked to the PE industry’s advantage over the last several decades since public markets have on balance have risen significantly.

Notice that increasing leverage requires no particular management expertise or shrewd strategic planning. In principle it’s no more difficult than you or me purchasing stock on margin.

These studies are not the final word on the subject. Some other studies, using alternate methodologies, have found some operational improvement at companies after being taken private. If different methodologies can reach such different conclusions, however, that would suggest that the benefits of going private are not as obvious and overwhelming as the private equity industry would have us believe.

At a minimum, Kwun and Alloula argue, we should be skeptical “of any claims of operational improvements being a major contributor to PE’s performance relative to public markets.”

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at mark@hulbertratings.com