Surprise crude oil production cuts from Saudi Arabia and other oil-rich countries shouldn’t produce worries of skyrocketing gas costs for U.S. drivers still smarting from last year’s pump price shocks, according to fuel industry experts.

At a time when gas prices are already increasing because of rising seasonal demand, the slashed crude oil output that Saudi Arabia announced Sunday will translate into higher prices, they say. But compared to last year — when energy markets were absorbing the initial impact of Russia’s invasion of Ukraine — the altitude on those gas price increases may not feel so steep.

On Monday, the national average for a gallon of gas was $3.50, according to AAA. That’s around 10 cents more than a month ago, but almost 70 cents less than the $4.19 average cost one year ago.

The effects of decreased oil production could translate into initial price increases of up to 15 cents per gallon, according to two different energy sector watchers.

There’s Patrick De Haan, head of petroleum analysis at GasBuddy.

At OPIS, an outlet focused on energy sector news and analytics, Chief Oil Analyst Denton Cinquegrana said he was previously expecting summer gas prices to average around $3.60.

“This move probably boosts that by about 10 – 15 cents to about $3.70-3.75/gal.” Cinquegrana told MarketWatch.

OPIS is owned by Dow Jones, which also owns MarketWatch.

It’s possible for gas price averages to hit around $3.60 in the next week or so, he said. The other 10 to 15 cents might filter into retail pump prices later this month or in early May, according to Cinquegrana.

The surprise move came from Saudi Arabia and other members of OPEC+, the Organization of the Petroleum Exporting Countries and allies, including Russia. In Saudi Arabia, officials were reportedly “irritated” by recent remarks from U.S. Energy Secretary Jennifer Granholm.

After the Biden administration tapped the country’s strategic petroleum reserve to combat last year’s high gas costs, Granholm said it will difficult to restock the reserve.

By May, more than 1 million barrels of oil a day will be slashed from output in the global energy markets. That’s in addition to OPEC+ production cuts announced last fall.

In cost breakdowns for a gallon of gas, the price of crude oil is responsible for more than half the price tag, according to the U.S. Energy Information Administration.

In Monday morning trading, the price of West Texas Intermediate crude for May delivery jumped 6% to just over $80 on the New York Mercantile Exchange.

For context, when gas prices were breaking records last year, the costs of West Texas Intermediate crude were in the triple digits. While retail prices surged in early March 2022, West Texas Intermediate crude briefly traded for more than $130 during the trading day on March 7, 2022.

The national average for a gallon of gas hit a record $5.01 in mid-June, according to AAA. In the current context, Cinquegrana doesn’t see a return to $5 gas averages, he said. Gas prices vary across the nation. California drivers are paying $4.80 on average while Mississippi drivers are paying $3.02 per gallon.

Even if price increases are not as sharp as last year, hot inflation is retreating slowly. So any extra costs are unwelcome to millions of American drivers who are living their lives and more frequently commuting to the office.

Like last year, oil prices are poised to increase, said AAA spokesman Devin Gladden.

But the economy’s background noise right now could dampen the impact as downturn worries keep sticking around, he added. Furthermore, there can be discrepancies in the announced production reductions and the amounts that are actually reduced, Gladden said.

“If recessionary concerns persist in the market, oil price increases may be limited due to the market believing lower oil demand will lead to lower prices this year,” he said.

On Monday, energy sector stocks and related exchange traded funds were climbing after the production cut news. In early afternoon trading, the Dow Jones Industrial Average DJIA, +0.81%

was up more than 200 points, or 0.7%, while the S&P 500 SPX, -0.03%

is little changed and the Nasdaq Composite COMP, -0.98%

dropped 100 points, or 0.8%.

Thenumbers: U.S. industrial production was flat in February, the Federal Reserve reported Friday.

The unchanged reading was in line with economists expectations, according to a survey by The Wall Street Journal.

Output rose a revised 0.3% in January, revised up from the initial estimate of a flat reading, but there were deep declines in November and December.

Key details: Manufacturing output downshifted to a slim 0.1% rise in February after a strong 1% gain in the prior month.

Motor vehicles and parts output fell 0.3% after a 0.6% jump in January. Excluding autos, total industrial output was unchanged.

Utilities output rose 0.5% in February. Mining output, which includes oil and natural gas, fell 0.6% after a 2% gain in the prior month.

Big picture: The softness in manufacturing is expected to continue as interest rates have moved higher. Credit conditions are expected to tighten in the wake of the worries surrounding regional banks.

Tesla Inc. late Wednesday reported mixed quarterly results, with revenue slightly below Wall Street expectations, but injected some optimism in its production outlook for 2023 and promised to rein in costs faster.

Demand is not a problem, Chief Executive Elon Musk said in a call with analysts after results. “I want to put that concern to rest,” he said, adding that January orders are stronger than ever, and demand far outstrips Tesla’s rate of production.

Petroleum is a critical input in modern economies. Besides its uses as fuel, petroleum is essential for making chemicals, plastics, other synthetic materials and asphalt. It is also used in electricity generation.

Because of this importance, it is not surprising that major oil supply disruptions in the United States have often been associated with recessions. This article explains one technique for quantifying the transmission of oil supply shocks to real economic activity, specifically employment in the manufacturing sector.

The Oil Market and the Macroeconomy

The figure below plots the dollar price of a barrel of oil in the U.S. over the past 56 years, with recession periods shaded in gray. Sharp rises in oil prices have frequently preceded recessions. For example, the recession that occurred from November 1973 to March 1975 was preceded by the 1973 oil embargo initiated by members of the Organization of Arab Petroleum Exporting Countries.

Price of Oil (U.S. Dollars Per Barrel), 1966-2022

The 1980 U.S. recession followed the 1979 oil shock, when reduced supply occurred alongside increased prices. In February 1980, the price of a barrel of oil increased by about 133% from one year earlier. More recently, some economists have argued that the doubling in oil prices between June 2007 and June 2008 intensified the 2007-09 recession, which is mainly associated with the housing downturn and financial crisis.

On the other hand, oil price increases are not always associated with economic downturns. If oil supply factors are stable, then increased oil demand—perhaps due to an improving global economy and economic outlook—can drive up oil prices. For example, the sustained period of economic growth in the U.S. and many other countries between 2002 and 2007 occurred along with sustained oil price growth.

To summarize, reductions in oil supply will increase oil prices and reduce employment and economic growth. In addition, increased economic growth will raise demand for oil and increase oil prices. Economists want to know the effect of oil supply changes on economic activity. Uncovering that effect requires the researcher to disentangle how much of a price movement is supply versus demand driven.

Uncovering the Effects of Oil Supply and Oil Demand Shocks

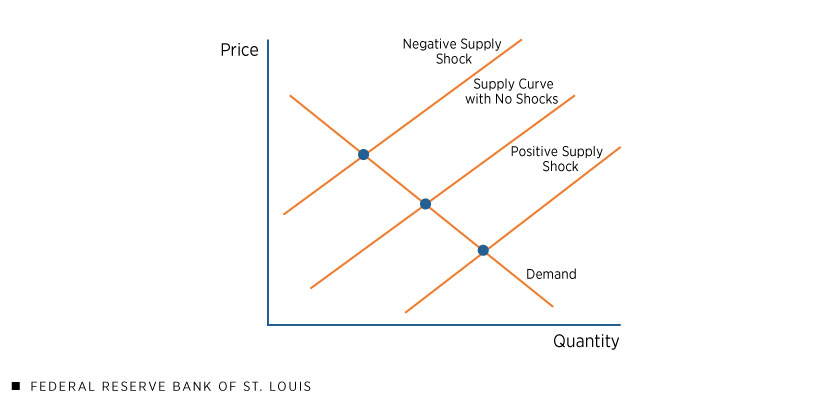

The following figure, a classic supply-demand diagram, describes the supply and demand for world oil. The horizontal axis marks quantity (e.g., millions of barrels of oil per month) and the vertical axis marks price (e.g., dollars per barrel of crude oil).

Supply and Demand for Oil

The supply curve plots the combined quantity supplied by sellers of oil at various prices. At a higher price, producers will be willing to sell more. Hence, the supply curve slopes upward. The demand curve plots the combined quantity demanded by buyers of oil at various prices. At a higher price, people and firms will try to economize on their use, and buyers will purchase less. Therefore, the demand curve slopes downward.

The market is in equilibrium when the quantity supplied equals quantity demanded. This occurs at the point where the supply curve intersects the demand curve. The market price of a barrel of oil can be read on the horizontal axis at the intersection of the two curves.

It is important to note that economists can’t directly observe the demand or supply curve in any market—oil or otherwise. That is, it is hard to tell exactly how much oil producers would supply or consumers would demand at different prices. Economists usually observe the actual quantity and price that occur in the economy and how these change over time as the unobservable demand and supply curves shift.

Using the actual price and quantity combinations observed in the economy can, however, be informative about supply and demand curves. The figure below shows three supply curves. The middle curve represents the supply curve in the absence of external shocks to the oil market; the supply curve on the right reflects conditions following a positive supply shock (such as a new discovery of oil); and the supply curve on the left reflects conditions following a negative supply shock (such as a disruption caused by civil unrest in an oil-producing country).

Supply and Demand for Oil: Supply Shocks

If an economist knows that all shocks to the oil market are supply driven (i.e., reflect movements in the supply curve), the observed equilibrium prices and quantities will trace out the demand curve as seen in the preceding figure. Likewise, if all shocks are demand driven, prices and quantities will trace out the supply curve.

Identifying Changes in the Oil Supply Curve

In the real world, both supply and demand curves move constantly and unpredictably. Unlike the very large shocks of the 1970s, economists often find it difficult to untangle which factor, or combination of factors, is moving observed prices and quantities.

In a recent article in the American Economic Review, Northwestern University economist Diego R. Känzig presented a useful way to extract supply shocks from data. Känzig explains that much of the world’s supply of oil is set by Organization of the Petroleum Exporting Countries (OPEC) members in regular meetings held by member nations. He looked at the change in oil price around tight windows before and after meetings over time.

Although demand and other supply factors may be shifting supply and demand curves most of the time, by focusing only on price changes within these small periods of time, Känzig makes a compelling case that changes in quantity and prices around these tight windows are driven by supply shocks (both positive and negative).

Using these observations, he showed that negative news about supply coming out of these meetings increases oil prices immediately and leads to a gradual fall in oil production. Of course, these shocks are a very small fraction of the many factors moving oil prices, but their value lies in the fact that isolating them allows economists to measure the impact of a fairly pure supply shock on other variables.

The Effect of Oil Supply Shocks on Manufacturing Employment

My recent working paper with Timothy Conley of Western University and Mahdi Ebsim of New York University extends Känzig’s analysis by studying the effects of his oil price shocks on U.S. employment. We focus specifically on manufacturing employment because this sector is particularly reliant on oil. Moreover, we focus only on contractionary supply shocks and exclude expansionary shocks because research has shown that the former has a much greater effect on the macroeconomy.

In response to a 20% increase in the price of oil driven by a contractionary supply shock, we estimated that manufacturing employment fell by 1% over an 18-month horizon. Over a two-year horizon, the effect was slightly smaller, with manufacturing employment falling by 0.8%.

We view this employment effect as relatively small. One potential reason is that we estimated the response over a relatively recent period: January 1991 to January 2017. Oil has likely diminished in its importance for the U.S. economy relative to the 1970s because the U.S. has become dominated by the service sector and other sources of energy have gained prominence.

In recent weeks, Apple Inc. has accelerated plans to shift some of its production outside China, long the dominant country in the supply chain that built the world’s most valuable company, say people involved in the discussions. It is telling suppliers to plan more actively for assembling Apple products elsewhere in Asia, particularly India and Vietnam, they say, and looking to reduce dependence on Taiwanese assemblers led by Foxconn Technology Group.

Turmoil at a place called iPhone City helped propel Apple’s shift. At the giant city-within-a-city in Zhengzhou, China, as many as 300,000 workers work at a factory run by Foxconn to make iPhones and other Apple products. At one point, it alone made about 85% of the Pro lineup of iPhones, according to market-research firm Counterpoint Research.

Nvidia Corp.’s financial results had a bit of a surprise for investors, and not on the good side — product inventories doubled to a record high as the chip company gears up for a questionable holiday season.

Nvidia reported fiscal third-quarter revenue that was slightly better than analysts’ reduced expectations Wednesday, but the numbers weren’t that great. Revenue fell 17% to $5.9 billion, while earnings were cut in half thanks to a $702 million inventory charge, largely relating to slower data-center demand in China.

Gaming revenue in the quarter fell 51% to $1.57 billion. Nvidia said it is working with its retail partners to help move the currently high-channel inventories.

While the company was writing off the inventory for China, its own new product inventory was growing. Nvidia NVDA, -4.54%

reported that its overall product inventory nearly doubled to $4.45 billion in the fiscal third quarter, compared with $2.23 billion a year ago and $3.89 billion in the prior quarter. Executives cited its coming product launches, designed around its new Ada and Hopper architectures, when asked about the inventory gains.

In the semiconductor industry, high inventories can make investors nervous, especially after the industry had so many supply constraints in recent years that quickly swung to a glut of chips in 2022. With doubts about demand for gaming cards and consumers’ willingness to spend amid sky-high inflation this holiday season, having all that product on hand just amps up the nerves.

Chief Financial Officer Colette Kress told MarketWatch in a telephone interview Wednesday that the company’s high level of inventories were commensurate with its high levels of revenue.

“I do believe….it is our highest level of inventory,” she said. “They go hand in hand.” Kress said she was confident in the success of Nvidia’s upcoming product launches.

Nvidia’s revenue reached a peak in the April 2022 quarter with $8.3 billion, and in the past two quarters revenue has slowed, with gaming demand sluggish amid a transition to a new cycle, and a decline in China data-center demand due to COVID-19 lockdowns and U.S. government restrictions.

For its data-center customers, the new architectures promise major advances in computing power and artificial-intelligence features, with Nvidia planning to ship the equivalent of a supercomputer in a box with its new products over the next year. Those types of advanced products weigh on inventory totals even more, Kress said, because of the price of the total package.

“It’s about the complexity of the system we are building, that is what drives the inventory, the pieces of that together,” Kress said.

Bernstein Research analyst Stacy Rasgon believes that products based on Hopper will begin shipping over the next several quarters, “at materially higher price points.” He said in a recent note that he believes Nvidia’s numbers were likely hitting a bottom in this quarter.

“We remain positive on the Hopper ramp into next year, and believe numbers have at this point likely reached close to bottom, with new cycles brewing and an attractive secular story even without China potential,” Rasgon said in an earnings preview note Tuesday.

Nvidia Chief Executive Jensen Huang reminded investors on a conference call that the company’s inventories are “never zero,” and said everyone is enthusiastic about the upcoming launches. But it doesn’t take too long of a memory to conjure up a time when Nvidia went into a holiday with an inventory backlog that included new architecture and greatly disappointed investors: Four years ago, Huang had to cut his forecast for holiday earnings twice amid a “crypto hangover” with similar dynamics to the current moment

Investors need faith that this holiday season will not be the same, even as demand for some videogame products declines after a pandemic boom just as the market for cryptocurrency — some of which has been mined with Nvidia products — hits a rough patch. Huang said that Nvidia’s RTX 4080 and 4090 graphics cards based on the Ada Lovelace architecture had an “exceptional launch,” and sold out.

Nvidia shares gained more than 2% in after-hours trading Wednesday, suggesting that some are betting that this time will be different. That enthusiasm needs to translate into revenue for Nvidia so that this big gain in inventories does not end up being part of another write-down at some point in the future.

Vicki Hollub’s Occidental Petroleum controls the biggest piece of the most important area for oil production in the United States. Not so long ago, an oilman in a position like that—and it would’ve been a man, before Hollub came along—would have gone for broke, turning up production to its physical limits.

Not Hollub. Occidental produces on average the equivalent of about 1.15 million barrels of oil a day, and that’s more than enough to turn a profit. The company can make money as long as oil prices are above $40 a barrel. They’ve been above $80 for almost all of this year, as the war in Ukraine takes a toll on global markets and the Saudi-led oil cartel OPEC now slashes production.

“We don’t feel like we’re in a national crisis right now,” Hollub told MarketWatch in an interview. And that means Hollub can keep executing on her plans: making shareholders happy by paying down debt and buying back shares. “When you have such a low break-even, to me there’s no pressure to increase production right now, when we have these other two ways that we can increase shareholder value,” Hollub said.

That market-focused logic puts her at odds with President Biden, who is acting like there is a national energy crisis ongoingprecisely because of what oil CEOs like Hollub are doing. The size of oil companies’ profits is outrageous, Biden said Monday. They’re raking in cash not because of innovation or investment but as a windfall from the war in Ukraine, Biden said. “Rather than increasing their investments in America or giving American consumers a break, their excess profits are going back to their shareholders and to buying back their stock, so the executive pay is — are going to skyrocket,” Biden said. He has ordered releases from the Strategic Petroleum Reserve to keep down gas prices and asked Congress to tax oil-company profits.

But Hollub is single-mindedly focused on seizing the moment to improve the company’s financial position. Occidental still has significant debt left over from a challenging acquisition Hollub spearheaded before the pandemic. In the second quarter alone, the company used its windfall to repay $4.8 billion in debt. If Biden called, she’d listen, but she hasn’t spoken to him one-on-one. Hollub said she’d spoken to the administration through Energy Secretary Jennifer Granholm. (“She doesn’t know the industry very well right now, but it’s because she hasn’t been in her job very long,” Hollub said.) The White House and the Department of Energy did not return requests for comment.

Hollub says she’s just following the market. “If demand goes down, we reduce production, if it goes up, we increase.” Oil prices have fluctuated rapidly over the year, and with a recession widely anticipated in the near future, demand could drop, Hollub said. Biden’s releases of oil from the SPR, she added, may have reduced gasoline prices, but at a cost to national security. “The SPR should be reserved for emergency situations, and you never know when those might come,” Hollub said.

Hollub’s message may not be politically convenient, but it’s exactly what her shareholders want to hear. Occidental OXY, -2.29%

is America’s hottest stock and has returned 150% this year, making it the top-performing company in the S&P 500 SPX, -0.65%.

Investors who bought shares of Occidental in January and held them through today would have more than doubled their money, even as the broader market has crashed. Warren Buffett’s Berkshire Hathaway has gone on a buying spree this year, and now owns more than 20% of Occidental’s shares. How Hollub got here constitutes America’s greatest corporate saga in recent years, from her 2019 debt-fueled decision to buy bigger rival Anadarko Petroleum over the vocal objections of activist investor Carl Icahn, to the pandemic-induced collapse in oil prices that almost bankrupted Occidental, and Buffett’s extension, removal, and re-extension of support.

With Occidental now on solid financial footing, Hollub is continuing to leave a mark on the oil industry and the world, landing her on the MarketWatch 50 list of the most influential people in markets. Hollub’s tangles with the wise men of Wall Street have left her savvier about how to manage her business. Stung by previous boom-and-bust cycles, Hollub has helped lead America’s oil frackers away from being “swing producers” that could counter the war-driven increase in energy prices, as she paid down debt and returned cash to shareholders through dividends and stock buybacks instead of plowing some of that money into shale oil fields. She is also pushing investment into Occidental’s massive new carbon-capture effort.

More than anything, Hollub is focused on guys like Bill Smead, founder of Smead Capital Management, who is a long-term investor in Occidental and a Hollub fan. “She’s somebody that we have a great deal of respect for and appreciate all the money she’s making us,” he said.

With that kind of backing, Hollub is planning to put Occidental in the driver’s seat of the massive national economic transition induced by climate change. She is positioning Occidental to be the company of the energy transition, one geared not to the free-for-all economy of the last century or some carbonless vision of the next, but the oil company for right now. She might even stop drilling new oil wells entirely.

“Now we feel like we control our own destiny,” Hollub said.

For the chief executive of a company that’s having a banner year on Wall Street while investors choke down generational losses, Hollub seems to constantly be on the alert for threats. Talking through the company’s prospects, she repeats a certain phrase: “I know that this will ultimately get me in trouble, but…”

Trouble? Hollub and Occidental have known their share.

The drama surrounding Occidental’s 2019 acquisition of Anadarko would make for a good boardroom thriller—or at least a lively business-school case study. Anadarko had big assets in the crucial Permian Basin region of Texas and New Mexico, where horizontal drilling in shale rock had reinvigorated an aging oil field into the nation’s biggest production zone.

Hollub and her team made an offer to buy Anadarko after months of research. She thought she had a deal locked, only to hear on the radio that Anadarko had announced plans to combine with Chevron. She nearly drove off the road, Texas Monthly recounts.

Hollub turned to Buffett for help. He agreed to what was effectively a $10 billion loan at 8% interest, in the form of preferred shares, along with warrants that allow Berkshire Hathaway, Buffett’s company, to buy more common stock. That got Hollub what she wanted, but many on Wall Street hated it. “The Buffett deal was like taking candy from a baby and amazingly she even thanked him publicly for it!” Icahn wrote in a letter to his fellow shareholders. Icahn had bought a slug of Occidental’s shares and, in the ensuing months, the billionaire investor led a shareholder campaign against Hollub, insisting that she needed stronger board oversight. Icahn allies were made Occidental directors.

In 2020, as COVID-19 flattened the global economy, deeply indebted Occidental was forced to cut its dividend for the first time in decades. Buffett sold his stock. At Icahn’s urging, the company issued 113 million warrants to its shareholders, allowing them to buy shares at $22, at a time when the stock was trading at $17. Gary Hu, one of the Icahn directors on Occidental’s board, pointed to those warrants as evidence of their success. “Our involvement in Occidental represented activism at its finest,” said Hu.

Hollub flatly disagrees. Icahn saw an opportunity to make an easy profit in derailing the Anadarko deal, Hollub said. “And what he expected is that we would lose and he would benefit from that. Since that didn’t happen, he managed to maneuver his way onto the board.” Icahn’s representatives on the board came to Hollub with a number of plans, including the warrants. She felt that one wouldn’t do any harm. “So that’s what we agreed to, but yeah, the other 10 or so weird things, we didn’t do.”

““She’s somebody that we have a great deal of respect for and appreciate all the money she’s making us.””

— Bill Smead, founder of Smead Capital Management

Former Occidental CEO Stephen Chazen returned to chair the board at Icahn’s insistence. Icahn and Occidental ultimately reached a settlement. His board members left, and the activist sold his common shares earlier this year. Chazen passed away in September. The experience embittered both sides, but there is one point of agreement: Hollub will do as she sees fit. “We were clearly wrong about the board’s ability to restrain Vicki’s ambitions,” Hu said.

Icahn made a $1.5 billion profit. At a MarketWatch event in September, Icahn said he still holds the warrants. But he hasn’t let go of the issues that motivated him to push into Occidental in the first place, though he insists he has no problem with Hollub personally. He likened her to a kid who got lucky gambling in Vegas. “The system allowed her to do it. And she’s just one small example of what is wrong with corporate governance.”

But as Icahn has himself shown, the system of corporate money in America is malleable. Its players can learn the rules of the game and adapt. Quarter after quarter since the dark days of the pandemic, Hollub turned up on corporate earnings calls pledging to keep cash flows strong, to invest in the highest-returning assets, and not to fall into the trap of overinvesting in debt-fueled or expensive production capacity, as so many failed shale producers have done in the past. She’s driven the company’s debt from nearly $40 billion following the Anadarko acquisition to less than $20 billion today. She increased the company’s dividend earlier this year. Along the way she transformed from market pariah to textbook CEO.

Hollub and other CEOs who run America’s biggest shale-oil producers have learned from the industry’s past mistakes. After proving a decade ago they could successfully extract shale oil, many U.S. oil producers were cheered on by growth and momentum stock investors as they borrowed billions to ramp up production, only to have those same investors abandon them after Saudi Arabia induced a plunge in oil prices. In the years that followed, U.S. shale-oil producers cultivated a new set of more value-oriented shareholders by promising they would share in profits through dividends and stock buybacks. Hollub and many of those other CEOs are not interested in chasing unrestrained growth again.

The world’s most famous value investor is now also on board. For Buffett, an earnings call Hollub led in February was the turning point. “I read every word, and said this is exactly what I would be doing. She’s running the company the right way,” Buffett told CNBC. Berkshire Hathaway BRK.A, +0.15%

started buying Occidental stock soon after. In August, federal regulators gave Buffett’s company permission to buy up to half of the company. (Asked for comment, a representative of Berkshire Hathaway asked for questions by email but did not respond to them.)

The markets are rife with speculation that Buffett will go all the way and purchase the entire company, though neither Hollub nor Berkshire have said as much. Hollub said simply that Buffett is bullish on oil, so she expects him to invest for the long haul. A Buffett buyout wouldn’t necessarily be a win for the investors who’ve hung on as Occidental’s stock price has recovered. “I’d probably make more money if he doesn’t buy it,” said Smead.

Warren Buffett is back to betting on Hollub and bought 20% of Occidental’s stock this year.

Johannes Eisele/Agence France-Presse/Getty Images

Where Hollub might cause real trouble is in the fight to keep carbon dioxide out of the earth’s atmosphere. That’s not because she’s a climate-denier. Far from it. Like many of her fellow oil-and-gas CEOs in recent years, Hollub has come to see climate change not as a threat to the business, but as an opportunity to be managed.

“I know some people don’t want oil to be produced for very long, but it’s going to be,” Hollub said. For that to change, people have to start using less oil. “It’s not that the more supply we generate, then the more that people are gonna use. It’s all driven by demand,” she said. And even with an electric vehicle in every driveway, we’d still need to extract oil to produce plastics and to create airplane fuel, among other projects that fall under the category of hard-to-abate emissions.

Hollub’s plan for Occidental is to wrap the company around that lingering stream of demand for hydrocarbons. She says Occidental is now in the business of carbon management, a euphemism that glides over the messiness of the climate transition and companies’ role in it. Companies need to show anxious shareholders that they’re serious about reducing their carbon emissions, but they also need to keep operating in an economy that is still seriously short on meaningful alternatives to fossil fuels. Occidental is here to help, spurred along by a series of state and federal incentives that the company lobbied for over years, culminating in the passage this year of the Inflation Reduction Act.

Climate advocates have for years tried to make the use of fossil fuels reflect their full cost on the environment. That has put them deeply at odds with oil-and-gas executives like Hollub, who opposes carbon taxes. It’s also left U.S. climate policy stalled as the planet warms. But the IRA tries something else. “I do not see the IRA as a handout to the energy industry,” said Sasha Mackler, executive director of the energy program at the Bipartisan Policy Center, a D.C. think tank. Rather than making dirty energy more expensive, the IRA tries to make clean energy cheaper, Mackler said. And that’s something Hollub can get on board with. She’s selling the idea that a barrel of oil can be clean.

Getting to a net-zero barrel of oil, as Hollub calls it, involves literally rerouting the route carbon dioxide takes through the world. For companies like Occidental, CO2 isn’t just a planet-destroying waste product. It’s a critical input to the process of oil production. Engineers can use CO2 to essentially juice aging oil wells by pumping it underground to displace hydrocarbons. The process is called enhanced oil recovery, or EOR. Occidental is the industry leader, producing the equivalent of 130,000 barrels per day of EOR oil and gas as of 2020. And that oil can, in theory, be less impactful on the climate. “We have it documented that it takes more CO2 injected into the reservoir than what the incremental barrels from that CO2 that are produced will emit when they’re used,” she said.

The trick is where that injected CO2 comes from. The Permian is crisscrossed with thousands of miles of pipelines that bring CO2 to oil fields from as far away as Colorado. At the moment, the vast majority comes from naturally occurring reservoirs or as a byproduct of the production of methane. One of the strangest ironies of modern oil production is that companies like Occidental don’t actually have enough CO2. “There’s two billion barrels of resources remaining to be developed in our conventional reservoirs using CO2,” Hollub said.

So she and her team went out looking for more. Eventually they hit on the idea that’s encapsulated in the IRA. Instead of pulling CO2 out of the ground only to put it back, Occidental could divert some of the CO2 that’s being produced by so-called industrial sources, companies that would otherwise be dumping it into the atmosphere because, of course, there’s no business reason not to.

Finding companies that wanted to do the right thing with their waste CO2 turned out to be harder than Hollub thought. “We knocked on the doors of a lot of emitters,” Hollub said. They found one taker—a Texas ethanol producer that was willing to try a pilot. It was a decent start but not enough to unlock all those buried barrels.

That may soon change, driven by the IRA. The law puts new financial incentives behind those conversations Occidental was having with CO2 emitters. The IRA significantly beefed up the so-called 45Q tax incentive for companies to put CO2 permanently in the ground. Occidental can get $60 a ton in tax credits if the CO2 is stored in the process of pumping more oil for EOR, or $85 if the company just buries it.

There’s also a higher tier of incentives if companies obtain that CO2 using an experimental technology called direct air capture. Occidental is spending $1 billion to build what would be the world’s largest direct-air-capture facility in Texas, which you can loosely think of as a giant fan to suck ambient CO2 directly out of the atmosphere. Hollub plans to build as many as 70 by 2035.

The problem some see with this plan, and with Hollub and others’ efforts to shape legislation around it, is it tightens the economy’s dependence on fossil fuels rather than loosening it. Americans will now effectively pay Occidental to pursue more enhanced oil recovery. Those net-zero barrels of oil—should they materialize—might be better in climate terms than a traditional barrel. But that’s not the only alternative. Dollar for dollar, public money would be better spent on solar energy and other low-carbon options than on EOR, said Kurt House, who knows as much because he’s tried it. House got a Ph.D. at Harvard in the science of carbon capture and storage more than a decade ago and co-founded a company to put the idea into practice. “It is bad, bad economics,” he said. “If you pay people a million dollars a ton of CO2 sequestering, they will sequester a lot of CO2. But it’ll cost us. It’ll make solving global warming much, much, much, much, much more expensive.”

But Hollub isn’t likely to change course. “I would say to those who don’t like what we’re doing, who do they want to do this? Tell me who have they gotten to, that will commit to take CO2 out of the atmosphere?” she said. “This climate transition cannot happen as fast as some people want it to happen because the world can’t afford it,” Hollub said. “We’re looking at, you know, $100 to $200 trillion for this climate transition. We cannot spend that kind of money to make this transition happen without help from diverting some of the CO2 to enhanced oil recovery, which enables then the technology to be developed and to be built at a faster pace.” And in the meantime, Occidental can sell carbon offsets to companies like United Airlines, which is supporting the direct-air-capture facility.

Those companies can choose whether they want the CO2 Occidental is capturing to be buried, full stop, or used for more oil production. But it’s clear Hollub thinks EOR is a big part of the future for Occidental. She has often said that the last barrel of oil should come from EOR. “I think there could be a world where we do stop drilling new wells,” she said. “To increase recovery from the remaining conventional reservoirs is something that’s kind of like a best kept secret for the United States. Nobody very much realizes that, but that is there. And that gives us that longevity beyond what some people are forecasting,” Hollub said.

Hollub is well-aware of her critics. Perhaps that’s why she keeps looking around for signs of trouble. But even if it finds her, she doesn’t plan to change much. “I have no regrets,” she said.

U.S. stock indexes ended modestly lower on Wednesday, despite briefly turning positive in the final hour of trading, while data showed steady growth in private-sector jobs and in the service sector, indicating more scope for the Federal Reserve to continue to raise interest rates.

How stocks traded?

The Dow Jones Industrial Average DJIA, +0.03%

lost 42.45 points, or 0.1%, to finish at 30,273.87

The S&P 500 SPX, +0.21%

was off 7.65 points, or 0.2%, ending at 3,783.28

The Nasdaq Composite COMP, +18.82%

shed 27.77 points, or 0.2%, to end at 11,148.64

On Tuesday, the Dow jumped 825 points, or 2.8%, while the S&P 500 increased 3.1% and the Nasdaq Composite rallied 3.3%.

What drove markets?

Wall Street stocks finished in the red after three main indexes bounced back from earlier losses in the final hour of trade, following a strong September private employment report in the morning.

Data released Wednesday showed that private-sector payrolls rose by 208,000 in September, indicating steady growth and supporting the view that the Fed has enough scope to keep raising interest rates. Economists surveyed by The Wall Street Journal had expected a rise of 200,000.

The report came two days before the closely watched nonfarm payrolls data issued by the Bureau of Labor Statistics. Investors are eying on it for important guidance on the Fed’s policy stance in the November meeting.

Friday’s employment report is expected to show the economy added 275,000 jobs in September, compared with 315,000 new positions added in August, according to a survey polled by Dow Jones.

“That certainly could move the needle,” said Kristina Hooper, chief global market strategist at Invesco. “Again, it doesn’t mean that it actually is going to change the market, but it could be the catalyst for short term rally if we get a disappointing jobs report.”

“But keep in mind, that’s just the anticipation of a Fed pivot based on data. But that does not ensure a Fed pivot. And so it could be one of those short-term rallies like the one we saw earlier this week,” Hooper said.

In other data Wednesday, an ISM barometer of U.S. business conditions in the service sector dipped to 56.7% in September but still showed steady growth and rising employment in a sign the economy is still expanding.

The U.S. trade deficit in August fell to $67.4 billion, the lowest level since mid 2021, paving the way for a resumption of growth in gross domestic product in the third quarter.

The S&P 500 had just enjoyed its largest two day percentage gain since April 2020 on Monday and Tuesday, and the best start to a quarter since 1938, according to Dow Jones Market data.

The bounce followed three quarters of declines, the worst such run since 2008, during which time the S&P 500 fell 24.8% to a near two-year trough as investors worried that the Federal Reserve’s interest rate hikes to crush inflation would harm the economy.

Brian Mulberry, client portfolio manager at Zacks Investment Management, believes the volatility in the stocks will continue because markets are getting a very “consistent message” from the Fed.

“Given what has happened over the last five trading sessions alone, we would be basically telling our clients to tighten your seatbelt a little bit because it’s definitely going to continue to be a bumpy ride,” Mulberry told MarketWatch in a phone interview on Wednesday. “If we get a ‘Goldilocks’ (jobs) report, that would mean decent economic activity is going on. That’s good for earnings overall in the market, but it’s not growing to a point where interest rates would have to be ratcheted up another 125 basis points by the end of the year.”

One major reason behind the rise early this week was the view that the Fed would pivot away from its aggressive monetary tightening.

Johanna Chua, chief Asia economist at Citi, said that though U.S economic growth remained in better shape than other countries and Fed officials continued to sound hawkish, the market risked being wrongfooted by any signs that interest rates could soon peak.

“Even as the overall fundamental setup has not changed… trimming of bearish risk/bearish rates/bullish USD positions has driven a sharp reversal,” Chua said.

Mary Daly, president of the Federal Reserve Bank of San Francisco said Wednesday that the Federal Reserve needs to keep raising its benchmark interest rate in order to cool inflation that hit a 40-year high earlier this year and has shown little signs of cooling. Atlanta Fed President Raphael Bostic will speak at 4 p.m. Eastern.

CLX22,

rose $1.24, or 1.4%, to settle at $87.76 a barrel on the New York Mercantile Exchange.

The S&P 500’s energy sector SP500.10, -0.07%

rose 2.1% following the news, up 12.6% over the last three trading days. According to Dow Jones Market Data, it was the best three-day percentage gain since November 2020 when it gained 16.1%. Shares of Schlumberger SLB, +0.77%

gained 6.3% at the close, while Exxon Mobil XOM, +1.32%

shares advanced 4%.

Companies in focus

Shares of Helen of Troy Ltd. HELE, -2.75%

finished 3.4% higher Wednesday, after the consumer products company, with brands including OXO, Hydro Flask and Braun, reported fiscal second-quarter earnings that beat expectations but cut its full-year outlook, as rising inflation has prompted consumers to change their spending patterns.

Shares of Monopar Therapeutics Inc. MNPR, +6.36%

gained 1.8% after the company said it completed enrollment in a Phase 2b clinical trial evaluating its experimental therapy aimed at preventing severe oral mucositis in patients undergoing chemoradiotherapy for oropharyngeal cancer.

Shares of Eiger BioPharmaceuticals Inc. EIGR, +0.85%

tumbled 5% after the company said it will not pursue emergency authorization of its experimental treatment for mild and moderate COVID-19 infections.

Shares of Lamb Weston Holdings Inc. LW, +2.45%

ended 4.2% higher Wednesday, after the potato supplier reported fiscal first-quarter profit that beat expectations, higher prices helped offset a volume decline.

Shares of Nike Inc. plunged as much as 10% after hours Thursday, after the athletic-gear giant’s executives said price-cutting efforts to flush off-season clothing from warehouses in North America would dent gross margins for the rest of its fiscal year and warned of a big potential hit from the stronger dollar.

Management also said they expected their rivals to keep cutting prices through at least the end of the calendar year, as they try to clear their own stockpiles. But the Nike executives said inventory levels in North America likely “peaked” in its first quarter, which ended on Aug. 31, and expected levels to even out — with newer, seasonally-aligned, in-demand product — in the months ahead as it prepares for the holiday rush.

“We’re taking decisive action to clear excess inventory, focusing on specific pockets of seasonally late product, predominantly in apparel,” Chief Financial Officer Matthew Friend said on Nike’s earnings call.

He added that he expected the moves to have a “transitory impact” on gross margins for the year.

The lopsided inventory levels, which grew 44% during Nike’s third quarter, followed factory closures last year in Asia, where most of its footwear is made, that led to late product deliveries, Friend said.

But those late deliveries are now getting mixed in with holiday-season deliveries that are set to arrive earlier than planned. The earlier arrivals, executives said, were a function of earlier ordering — due to the shipping delays that have characterized the past year —and then a sudden, more recent improvement in those shipping times.

And as the U.S. dollar strengthens, Friend said he expected the full-year negative impact of foreign exchange on reported sales and earnings before interest and taxes to be $4 billion and $900 million, respectively.

Still, executives said inventory management in China was “ahead of plan” as it recalibrates supply and navigates COVID-19 related restrictions there. And they said that consumer demand was still strong, despite rising prices. Friend and CEO John Donahoe both repeated that Nike remained customers’ “No. 1 cool” and “No. 1 favorite” brand.

Donahoe said shoes like the Air Max Scorpion — which offered the “most air ever, in terms of pound per square inch” — reflected Nike’s commitment to innovation. The company’s Travis Scott and LeBron 20 sneakers also remained popular, executives said. The back-to-school season, and demand for its Jordan and Converse sneakers, were also solid.

As for fiscal first-quarter financials, Nike reported net income of $1.5 billion, or 93 cents a share, compared with $1.9 billion, or $1.16 a share, in the year-earlier period. Sales came in at $12.7 billion, compared with $12.2 billion a year ago.

Analysts polled by FactSet expected earnings of 92 cents a share on sales of $12.28 billion. Shares of Nike NKE, -3.41%

were last down 9.3% after hours, but fell more than 10% at one point after the close.

Prior to the report, analysts following Nike had zeroed in on the impact of the stronger U.S. dollar, the impact of China’s COVID lockdowns, as well as the effects from bigger discounts to sell shoes and other gear that sat around for too long due to backups in the company’s supply chain. The back-to-school season, and competition with the likes of Adidas AG ADDYY, -5.21%

were also points of focus for Wall Street.

Gross margins fell to 44.3% from 46.5% during the quarter. Nike executives said the decrease “was primarily driven by North America, which took measures to liquidate excess inventory through Nike Direct markdowns and wholesale marketplace actions.”

Inventory for Nike stood at $9.7 billion, a 44% increase from the year-earlier period, due to what executives described as “ongoing supply-chain volatility, partially offset by strong consumer demand during the quarter.”

Nike, in June, said it expected “higher promotional activity” in the first quarter, as it tries to sell seasonal items that arrived late, following the factory closures last year in Asia. However, for the full year ahead, management at that time said it was planning for “mid-single-digit price increases.”

Executives also said then that they were planning to expand sales that go directly to consumers, via its own stores and online. The company over the years has been trying to rely less on retail chains like Foot Locker Inc. FL, -6.36%

for sales.

Shares of Nike have fallen 43% so far this year. By comparison, the S&P 500 index SPX, -2.11%

is down around 24% over that time.