Federal Reserve Chair Jerome Powell set a high bar for additional interest-rate hikes, economists said Sunday in their commentary on all the talk at the U.S. central bank’s summer retreat in Jackson Hole, Wyo.

Michael Feroli, chief U.S. economist for JPMorgan Chase, said that the Fed chair certainly did not give a clear signal that more tightening was coming soon. He noted that Powell stressed the Fed would “proceed carefully” and balance the risks of tightening too much or too little.

“We remain comfortable in our view that the FOMC will stay on hold for the next several meetings,” Feroli said.

The caveat to this forecast is if inflation surprises to the upside or the labor market does not continue to soften.

Ian Shepherdson, chief economist at Pantheon, said that Powell’s speech seemed hawkish to some, particularly because the Fed chair made threats to hike again.

But Shepherdson said he thought the Fed “is likely done.”

“Behind the caveats, Mr. Powell’s speech fundamentally was optimistic, though cautious,” Shepherdson said.

Boston Fed President Susan Collins also emphasized patience in an interview with MarketWatch on the sidelines of the Jackson Hole summit.

Other regional Fed officials who spoke “hinted that further action may be needed, but also observed that inflation is moving in the right direction and that the surge in yields would help cool down the economy,” said Krishna Guha, vice chairman of Evercore ISI, in a note to clients.

Traders in derivative markets expect a rate hike in November, but it is a close call, with the odds just above 50%.

The first test of the careful and patient Fed will come this coming Friday, when the government will release the August employment report.

Economists surveyed by the Wall Street Journal expect the U.S. economy added 165,000 jobs in the month. That would be the weakest job growth since December 2020.

In his speech on Friday, Powell emphasized that evidence that the labor market was not softening could “call for a monetary policy response.”

Economists at Deutsche Bank think an upside surprise in the employment data could provide enough discomfort for the Fed, and raise expectations for further tightening.

Guha of Evercore said he detected a careful effort by the officials not to surprise markets.

The exception to this rule might have been Bundesbank President Joachim Nagel, who said in a television interview that it was too early for the ECB to think about a rate-hike pause.

Barry DiRaimondo, chief of SteelWave, a West Coast property developer that in the past half-century has partnering with many of the biggest names in commercial real estate, is looking for diamonds in the rough, distressed office properties located in the American city that many have given up on.

Others may be shunning San Francisco while it’s down on its luck, but DiRaimondo sees better days ahead, despite the city’s threat of a growing deficit, its fentanyl crisis, homelessness and a reluctant return of office workers to its financial core.

“Not much is coming up right now,” DiRaimondo said of buying opportunities, while speaking from his office in the heart of San Francisco’s financial district. But he was eager to point out several nearby buildings that could be candidates to buy, at the right price.

“I think over the next 12 to 18 months, you’re going to see a tsunami,” of distressed office properties, DiRaimondo said.

Like in many big cities, a wave of office buildings bought at peak prices before the pandemic now have a pile of debt coming due, at much higher rates. But San Francisco’s financial core only recently has begun to show flickers of hope in its weak recovery post-COVID.

“Whether it’s San Francisco, Oakland or anywhere here, and your debt is rolling, you’re having a conversation with your lender,” DiRaimondo said. “There’s either a restructuring going on or a foreclosure going on.”

A number of high-profile property owners this year surrendered local properties to lenders, including Westfield’s namesake shopping center downtown and a string of well-known hotels, a blow to the city’s comeback efforts.

Still, DiRaimondo expects the bulk of property ownership transfers in this boom-and-bust cycle to take place quietly, behind the scenes, often through a building’s debt changing hands. It’s a familiar playbook for veteran real-estate developers like SteelWave and its partners, especially when San Francisco office property values tumble and new loans remains expensive and hard to come by.

“Office is a nasty word, right now. Especially tech office,” he said. “We are doing something that’s a bit different.”

Booms, busts

San Francisco’s history as a boom-and-bust town perhaps is best suited for real-estate developers able to take a bunch of lemons and make lemonade.

That has been SteelWave’s signature move in the notoriously rough-and-tumble commercial real-estate industry, through its ups and downs. It has bought over $17.5 billion in properties and developments in the past five decades, first under the Legacy Partners Commercial brand before it was renamed in 2015.

It has partnered with some of the biggest names in commercial real estate, including with Angelo Gordon & Co. in 2021 on two Silicon Valley office buildings, but also distressed debt titans that include Rialto Capital, and with Chenco, one of the largest Chinese-owned U.S. real-estate investment firms.

Its stronghold is the Bay Area and DiRaimondo is now looking to raise a $500 million fund to buy distressed buildings, including in downtown San Francisco, a place major Wall Street lenders have been backing away from for months.

“It’s hard to raise equity to buy this stuff right now,” he said, but argues his strategy, which includes expanding its reach to potential investors in the U.A.E., Israel and parts of Europe, will pan out.

SteelWave’s model of buying a property includes a final tally of costs often three to four times the initial purchase price, due to extensive overhauls.

“Typically, what we do is buy something, tear it apart, put it back together, lease it, sell it,” DiRaimondo said.

It’s niche in the distressed world that’s already produced overhauls of buildings from Seattle to Colorado to Los Angeles, places the tech industry wants to lease.

In the southern California town of Costa Mesa, that meant partnering with Invesco to turn an old newsroom and printing press for the Los Angeles Times into a creative work campus. An opinion piece in 2022 from the newspaper described the revamp as turning, “the glum newspaper architecture into something inviting.”

Forget being a ‘rent bandit’

“In New York, people rushed back and refilled the apartments, streets, and subways. Restaurants and stores flooded with customers again,” a team from Moody’s analytics wrote in a recent “tale of two cities” report. “San Francisco, on the other end, battled safety concerns, homelessness, and population exodus which existed before but only became more obvious with barren neighborhoods.”

SteelWave thinks the old days of landlords raking in top-dollar commercial rents in San Francisco, while adding little back to office buildings, are a thing of the past.

“You have to have owners who want to create cool work environments to attract people back into the city,” DiRaimondo said of downtown San Francisco’s long slog back from the brink.

That means buying properties at low prices, but also risking putting money down for major improvements. He isn’t a distressed investors looking to become a “rent bandit,” he says, because the strategy will fail to get quality tenants.

Like the Moody’s team, DiRaimondo thinks San Francisco eventually will bounce back, but he thinks not before reality hits older office properties.

Take a “commodity” building downtown, often older and midblock with generic features, that previously might have been worth $750 to $800 a square foot. It now looks worth less than $300 a square foot, he said.

The early stages of fire-sales have begun already, with the 22-story tower at 350 California, nearby to DiRaimondo’s office, reportedly fetching $200 to $225 a square foot.

“San Francisco is not dead,” DiRaimondo said. “I think there are opportunities in San Francisco.”

Barry DiRaimondo, chief of SteelWave, a West Coast property developer that in the past half-century has partnering with many of the biggest names in commercial real estate, is looking for diamonds in the rough, distressed office properties located in the American city that many have given up on.

Others may be shunning San Francisco while it’s down on its luck, but DiRaimondo sees better days ahead, despite the city’s threat of a growing deficit, its fentanyl crisis, homelessness and a reluctant return of office workers to its financial core.

“Not much is coming up right now,” DiRaimondo said of buying opportunities, while speaking from his office in the heart of San Francisco’s financial district. But he was eager to point out several nearby buildings that could be candidates to buy, at the right price.

“I think over the next 12 to 18 months, you’re going to see a tsunami,” of distressed office properties, DiRaimondo said.

Like in many big cities, a wave of office buildings bought at peak prices before the pandemic now have a pile of debt coming due, at much higher rates. But San Francisco’s financial core only recently has begun to show flickers of hope in its weak recovery post-COVID.

“Whether it’s San Francisco, Oakland or anywhere here, and your debt is rolling, you’re having a conversation with your lender,” DiRaimondo said. “There’s either a restructuring going on or a foreclosure going on.”

A number of high-profile property owners this year surrendered local properties to lenders, including Westfield’s namesake shopping center downtown and a string of well-known hotels, a blow to the city’s comeback efforts.

Still, DiRaimondo expects the bulk of property ownership transfers in this boom-and-bust cycle to take place quietly, behind the scenes, often through a building’s debt changing hands. It’s a familiar playbook for veteran real-estate developers like SteelWave and its partners, especially when San Francisco office property values tumble and new loans remains expensive and hard to come by.

“Office is a nasty word, right now. Especially tech office,” he said. “We are doing something that’s a bit different.”

Booms, busts

San Francisco’s history as a boom-and-bust town perhaps is best suited for real-estate developers able to take a bunch of lemons and make lemonade.

That has been SteelWave’s signature move in the notoriously rough-and-tumble commercial real-estate industry, through its ups and downs. It has bought over $17.5 billion in properties and developments in the past five decades, first under the Legacy Partners Commercial brand before it was renamed in 2015.

It has partnered with some of the biggest names in commercial real estate, including with Angelo Gordon & Co. in 2021 on two Silicon Valley office buildings, but also distressed debt titans that include Rialto Capital, and with Chenco, one of the largest Chinese-owned U.S. real-estate investment firms.

Its stronghold is the Bay Area and DiRaimondo is now looking to raise a $500 million fund to buy distressed buildings, including in downtown San Francisco, a place major Wall Street lenders have been backing away from for months.

“It’s hard to raise equity to buy this stuff right now,” he said, but argues his strategy, which includes expanding its reach to potential investors in the U.A.E., Israel and parts of Europe, will pan out.

SteelWave’s model of buying a property includes a final tally of costs often three to four times the initial purchase price, due to extensive overhauls.

“Typically, what we do is buy something, tear it apart, put it back together, lease it, sell it,” DiRaimondo said.

It’s niche in the distressed world that’s already produced overhauls of buildings from Seattle to Colorado to Los Angeles, places the tech industry wants to lease.

In the southern California town of Costa Mesa, that meant partnering with Invesco to turn an old newsroom and printing press for the Los Angeles Times into a creative work campus. An opinion piece in 2022 from the newspaper described the revamp as turning, “the glum newspaper architecture into something inviting.”

Forget being a ‘rent bandit’

“In New York, people rushed back and refilled the apartments, streets, and subways. Restaurants and stores flooded with customers again,” a team from Moody’s analytics wrote in a recent “tale of two cities” report. “San Francisco, on the other end, battled safety concerns, homelessness, and population exodus which existed before but only became more obvious with barren neighborhoods.”

SteelWave thinks the old days of landlords raking in top-dollar commercial rents in San Francisco, while adding little back to office buildings, are a thing of the past.

“You have to have owners who want to create cool work environments to attract people back into the city,” DiRaimondo said of downtown San Francisco’s long slog back from the brink.

That means buying properties at low prices, but also risking putting money down for major improvements. He isn’t a distressed investors looking to become a “rent bandit,” he says, because the strategy will fail to get quality tenants.

Like the Moody’s team, DiRaimondo thinks San Francisco eventually will bounce back, but he thinks not before reality hits older office properties.

Take a “commodity” building downtown, often older and midblock with generic features, that previously might have been worth $750 to $800 a square foot. It now looks worth less than $300 a square foot, he said.

The early stages of fire-sales have begun already, with the 22-story tower at 350 California, nearby to DiRaimondo’s office, reportedly fetching $200 to $225 a square foot.

“San Francisco is not dead,” DiRaimondo said. “I think there are opportunities in San Francisco.”

The Russian ruble plunged to its lowest level against the U.S. dollar in more than 16 months on Monday, as blowback related to President Vladimir Putin’s bloody invasion of Ukraine continued to weigh on the currency.

The U.S. dollar USDRUB, +2.17%

surged to 101.74 rubles on Monday, according to FactSet data. That’s the weakest level for the Russian currency since March 28, 2022. Since the start of the year, the dollar has gained more than 38% against the ruble, making the ruble one of the worst performing major emerging-market currencies of the year compared with the greenback.

Weakness in the ruble has intensified over the past week weeks, and just a few days ago the Russian central bank announced it would halt buying of foreign currency on the open market through the end of the year. Instead, it will rely on Russia’s National Wealth Fund’s largess to supply them. The decision was enacted with the intention of “reducing volatility” in financial markets. The central bank has also said it’s launching a digital-ruble pilot program.

Economists, including Konstantin Sonin, a political economist at the University of Chicago, have blamed capital flight and falling budget revenues (due to lower oil and gas income and tax revenue) for the ruble’s troubles.

Data released by Russia’s central bank last week showed Russia’s current-account surplus has shrunk markedly during the first seven months of the year to an estimated $25.2 billion, compared with $165.4 billion during the same period in 2022. The central bank blamed the decline on a shrinking trade surplus caused by the drop in crude oil prices since the first half of 2022.

The Bank of Russia, the country’s central bank, has attempted to shore up the ruble with little benefit. Last month, the central bank hiked interest rates by 100 basis points, the first increase since before Putin ordered the invasion of neighbor Ukraine in February 2022. It hinted that more hikes were possible.

A weak ruble was one reason for the hike, as the weak currency has caused inflation to accelerate.

While the ruble remains weak, it’s still holding above its lows around 130 to the dollar seen in March 2022, weeks after the West imposed a first round of sanctions on Moscow following the invasion of Ukraine, which has morphed into a bloody stalemate with no end in sight.

The annual inflation rate rose to 4.5% in July from 3.25%, but economists at Goldman Sachs warned in a note earlier this month that inflation will likely head above the bank’s target again.

“With continuing loose fiscal policy, we expect inflation to continue to rise throughout the year to +7.0% yoy [year-over-year] in December, above the CBR’s July inflation forecast range of +5.0% – +6.5%,” said a team of economists led by Kevin Daly.

Russian officials have blamed the ruble’s latest bout of weakness on the central bank. Oreshkin Maxim, Putin’s economic aide, wrote in an editorial published in state media outlet Tass on Monday, that “loose monetary policy” was to blame for the weak ruble and urged action on that front.

“The Central Bank has all the necessary tools to normalize the situation in the near future and ensure that lending rates are reduced to sustainable levels,” he wrote.

Many economists and currency strategists expect the ruble’s slide to continue. However, a recent rebound in global crude-oil prices is leading to a modestly improved outlook.

In the U.S., West Texas Intermediate crude for September settled at $84.40 a barrel on Wednesday, its highest level of 2023, according to FactSet data. That reflects a wider trend of rising energy prices globally. However, prices remain well below the peak of roughly $130 a barrel from March 2022, when prices spiked in the immediate aftermath of the invasion.

FTX founder Sam Bankman-Fried was sent to jail Friday to await trial after a bail hearing for the fallen cryptocurrency wiz left a judge convinced that he had repeatedly tried to influence witnesses against him.

U.S. District Judge Lewis A. Kaplan ordered Bankman-Fried’s bail revoked after prosecutors said he’d tried to harass a key witness in his fraud case last month when he showed a journalist her private writings and in January when he reached out to the general counsel for FTX with an encrypted communication.

His lawyers insisted he shouldn’t be jailed for trying to protect his reputation against a barrage of unfavorable news stories.

Kaplan said he had concluded there was probable cause to believe Bankman-Fried had tried to “tamper with witnesses at least twice” since his December arrest.

A defense lawyer said an appeal of the incarceration order would be filed and asked for an immediate stay of the order.

The 31-year-old has been under house arrest at his parents’ home in Palo Alto, California, since his December extradition from the Bahamas on charges that he defrauded investors in his businesses and illegally diverted millions of dollars’ worth of cryptocurrency from customers using his FTX exchange.

Bankman-Fried’s $250 million bail package severely restricts his internet and phone usage.

Two weeks ago, prosecutors surprised Bankman-Fried’s attorneys by demanding his incarceration, saying he violated those rules by giving The New York Times the private writings of Caroline Ellison, his former girlfriend and the ex-CEO of Alameda Research, a cryptocurrency trading hedge fund that was one of his businesses.

Prosecutors maintained he was trying to sully her reputation and influence prospective jurors who might be summoned for his October trial.

Ellison pleaded guilty in December to criminal charges carrying a potential penalty of 110 years in prison. She has agreed to testify against Bankman-Fried as part of a deal that could lead to a more lenient sentence.

Bankman-Fried’s lawyers argued he probably failed in a quest to defend his reputation because the article cast Ellison in a sympathetic light. They also said prosecutors exaggerated the role Bankman-Fried had in the article.

They said prosecutors were trying to get their client locked up by offering evidence consisting of “innuendo, speculation, and scant facts.”

Since prosecutors made their detention request, Kaplan has imposed a gag order barring public comments by people participating in the trial, including Bankman-Fried.

David McCraw, a lawyer for the Times, had written to the judge, noting the First Amendment implications of any blanket gag order, as well as public interest in Ellison and her cryptocurrency trading firm.

Ellison confessed to a central role in a scheme defrauding investors of billions of dollars that went undetected, McGraw said.

“It is not surprising that the public wants to know more about who she is and what she did and that news organizations would seek to provide to the public timely, pertinent, and fairly reported information about her, as The Times did in its story,” McGraw said.

A worsening U.S. fiscal situation caught stock and bond investors off guard in the past week and now a round of approaching government auctions is about to provide a crucial test for Treasurys.

The question in the days ahead is whether risks to the demand for U.S. government debt are growing. If so, that could put upward pressure on Treasury yields, which would undermine the performance of stocks. However, if investors end up caring less about the fiscal situation than they do about the possibility of slowing economic growth and decelerating inflation, government debt’s safe-haven appeal could be reinforced, putting a limit on how high yields might go.

Concern about the deteriorating fiscal outlook was a factor behind the past week’s rise in long-term Treasury yields. Ten- BX:TMUBMUSD10Y

and 30-year yields BX:TMUBMUSD30Y

respectively jumped to 4.188% and 4.304% on Thursday, the highest levels since early November, as investors sold off long-term government debt — which took the shine off U.S. stocks. By Friday, though, a moderating pace of U.S. job creation for July sent yields into reverse, giving equities a temporary lift during the final trading session of the week.

At issue is the extent to which potential buyers of Treasurys may be deterred by Fitch Ratings’ Aug. 1 decision to cut the U.S. government’s top AAA rating, at a time when the government is about to unleash what Barclays rates strategists describe as a “tsunami” of supply. A total of $103 billion in 3-, 10-and 30-year Treasurys come up for sale between Tuesday and Thursday. In addition, a spate of Treasury bills are scheduled to be auctioned starting on Monday.

Gene Tannuzzo, global head of fixed income at Boston-based Columbia Threadneedle Investments, said that while he and his team still have room to add T-bills to the government money-market funds they oversee during the week ahead, they haven’t made up their minds about whether to buy more longer-dated maturities for their bond funds.

“While we are comfortable that the Fed is at or near the end of its rate hikes, there are a lot more questions about the durability of the economic recovery, the degree that inflation will remain low, and the risk premium that needs to be put in at the long end,” Tannuzzo said via phone.

Treasury’s $1 trillion third-quarter borrowing plans, along with some technical issues and the Bank of Japan’s decision to switch to a more flexible yield-curve control approach, might reduce demand for U.S. government debt, he said. Columbia Threadneedle managed $617 billion as of June.

“One can’t ignore the risk of an unruly rise in yields, but our view is that this is a low risk and what the Treasury auctions may produce instead is ‘indigestion,’ driven by poor technicals and low liquidity, Fitch’s downgrade, and the Bank of Japan action — and by the end of August, we should be past much of this,” he told MarketWatch.

Risks to the demand for Treasurys may become obvious soon, given Tuesday-Thursday’s $103 billion in total sales of 3-, 10- and 30-year securities, according to analyst John Canavan of U.K.-based Oxford Economics. The main “question mark” for the market’s ability to absorb the increased Treasury issuance will be whether or not domestic investment funds continue to show interest, Canavan wrote in a note distributed on Friday.

Source: Oxford Economics.

“ ‘My suspicion is that with higher rates comes equally solid demand’ at upcoming auctions.”

— John Flahive, head of fixed income at BNY Mellon Wealth Management

Market players have had little difficulty absorbing Treasury coupon issuances in recent years because of flight-to-safety trades made after the U.S. onset of the Covid-19 pandemic in 2020. Now, however, increased auction sizes are being accompanied by still-elevated inflation, better-than-expected economic growth, and the possibility of more rate hikes by the Federal Reserve — which is likely to complicate the market’s ability to absorb the increased supply “without hiccups,” Canavan said.

On the flip side of the debate is John Flahive, head of fixed income at BNY Mellon Wealth Management in Boston, which managed $286 billion in assets as of June. He said equity markets will continue to be much more focused on economic developments and earnings. And as long as the latter of the two remains robust, stocks “can grind higher in a low-volatility environment,” Flahive said via phone.

Saying he does not expect his team to be a major participant in the Treasury auctions, Flahive said that the bond market’s reaction in the past week was “a little overdone” and “we always felt that there was a limited to how much yields could go up to reflect more government debt.”

“My suspicion is that with higher rates comes equally solid demand” at upcoming auctions, he said. “I’m still optimistic about rates going back down over time as the result of a slowing economy and decelerating inflation. We continue to like the bond market and see a better-than-even chance that yields go down as the economy continues to weaken in the quarters ahead.”

Friday’s reaction to July’s official jobs report, which showed the U.S. added a modest 187,000 new jobs, provided a breather from the past week’s run-up in Treasury yields.

On Friday, the 30-year Treasury yield fell 9 basis points to 4.214%, yet still ended with its biggest weekly gain since early February. The 10-year rate, which dropped 12.8 basis points to 4.06%, finished with a third straight week of advances.

Stocks fell Friday, leaving major indexes with weekly declines. The Dow Jones Industrial Average DJIA

posted a 1.1% weekly fall, while the S&P 500 SPX

shed 2.3% and the Nasdaq Composite COMP

retreated 2.9%. The soft start to August comes after a run of sharp gains for equities. The S&P 500 remains up 16.6% for the year to date.

The economic calendar for the week ahead includes U.S. inflation updates.

On Monday, June consumer-credit data is set to be released. Tuesday brings the NFIB’s small business optimism index, plus data on the U.S. trade balance and wholesale inventories. Then on Thursday, weekly initial jobless claims and the July consumer-price index are released. That’s followed on Friday by the producer-price index for last month and an August consumer-sentiment reading.

Meanwhile, portfolio manager and fixed-income analyst John Luke Tyner at Alabama-based Aptus Capital Advisors, which manages roughly $5 billion in assets, said he plans to follow the Treasury auctions, but doesn’t usually participate in them.

“One of the biggest trends we’ve seen is the continued increase in the issuance amounts from Treasury. Whatever we are budgeting for is never enough, which justifies the Fitch downgrade,” Tyner said via phone. “It’s tough to say people aren’t going to buy U.S. debt, but you’ve got to entice them to buy duration and take the risk.

“The U.S. is not an emerging market, but ultimately we are going to see the market rate that participants require be higher, with a notable uptick in term premia,” he said. “What we could see in the face of all this issuance is a grind up in yields on an auction-by-auction basis. If I look at the technicals, a 4.9%-5% yield on the 10-year note seems in the cards,” and “it will be difficult for stocks to hold or expand from full valuations as rates run up.”

Stocks have surged this year without really anything going right, besides the rolling out of error-prone artificial intellligence chatbots. Interest rates have surged to a 22-year high, earnings are down from last year, and pandemic-era savings are being drawn down if not entirely exhausted.

Strategists at Bank of America led by Michael Hartnett have an interesting theory.

“Asset price overshoots [are] the new normal,” they say.

Consider:

Oil CL00, -0.37%

went from -$37 in April 2020 to $123 in March 2022, then down to $67 the following 12 months.

Bitcoin BTCUSD, +0.32%

went from $5,000 in January 2020 to $68,000 in November 2021, down to $16,000 a year later, and up to $29,000 now.

The S&P 500 went from 3300 to 2200 to 4800 to 3500 to 4600 thus far in 2020s.

“AI is simply the new overshoot,” they say.

The S&P 500 SPX, +0.67%

has gained 18% this year as the Nasdaq Composite COMP, +1.53%

has rallied by 34%.

Hartnett and team noted that real retail sales — that is, adjusted for inflation — fell at a 1.6% year-over-year clip, which has coincided with recessions since 1967. Real retail sales falls in excess of 3% are associated with hard recessions.

Historically, a 2-3 point rise in the savings rate also is recessionary, and already it’s risen from 3% to 4.6%. The unemployment rate so far hasn’t risen, though a 0.5 point to 1 point rise in the jobless rate also is typically recessionary.

“It would be so ‘2020s’ for the economy to hit a brick wall just as everyone punts ‘soft landing’ into 2024,” they say.

They like emerging market/commodities as summer upside plays and credit and tech as autumn downside plays.

Worries about a possible policy tweak by the Bank of Japan threw a wet blanket on a stretched U.S. stock-market rally Thursday, with the Dow Jones Industrial Average snapping its longest winning streak since 1987 after the 10-year Treasury yield surged back above the 4% level.

The Japanese yen also strengthened after a news report said policy makers on Friday would discuss a possible tweak to the Bank of Japan’s so-called yield-curve control policy that would loosen the cap on long-dated government bond yields.

Nikkei, without citing sources, reported that BOJ officials would talk about the matter at Friday’s policy meeting and that the potential change would allow the yield on the 10-year Japanese government bond TMBMKJP-10Y, 0.440%

to trade above its cap of 0.5% “to some degree.”

‘Ultimate fear’

Why is that a negative for U.S. Treasurys and, in turn, U.S. stocks?

The “ultimate fear” is that Japanese investors, who have vast holdings of U.S. fixed income, including Treasury notes and other securities, “begin to see a higher level of yields in their own backyard,” Torsten Slok, chief economist at Apollo Global Management, told MarketWatch in a phone interview. That could prompt heavy liquidation of those U.S. positions as investors repatriate holdings to reinvest the proceeds at home.

That dynamic explains the knee-jerk reaction that saw the 10-year U.S. Treasury yield TMUBMUSD10Y, 4.004%

surge more than 16 basis points to end above 4%, he said. Yields rise as debt prices fall.

The surge in yields, in turn, saw stocks give up early gains, with U.S. indexes ending lower across the board.

What is yield curve control?

The Bank of Japan began implementing yield curve control, or YCC, in 2016, a policy that aims to keep government bond yields low while ensuring an upward-sloping yield curve. Under YCC, the BOJ buys whatever amount of JGBs is necessary to ensure the 10-year yield remains below 0.5%.

Nikkei said a possible tweak would allow gradual increases in the yield above 0.5%, but would clamp down on any sudden spikes, allowing the BOJ to rein in fluctuations driven by speculators.

Global market participants are sensitive to changes in YCC. The BOJ sent shock waves through markets in December when it lifted the cap from 0.25% to 0.5%. Investors were rattled by the prospect of the Bank of Japan giving up its role as the remaining low-rate anchor among major central banks.

BOJ Gov. Kazuo Ueda in May said the bank would start shrinking its balance sheet and end its yield-curve control policy if a 2% inflation looks achievable and sustainable after many years of undershooting.

Yen rallies

The yield on the 10-year JGB has traded above 0.4%, but remained below the 0.5% cap. Continued interest rate rises by the Federal Reserve and other major central banks in the past year have raised worries that the 10-year JGB yield could test the limit, Nikkei reported. Those rate hikes, meanwhile, have added pressure to the yen, whose weakness is seen contributing to inflation pressures.

The yen USDJPY, -0.02%

strengthened following the report. The U.S. dollar was off 0.5% versus the currency, fetching 139.48 yen.

The Dow Jones Industrial Average DJIA, -0.67%

ended the day down nearly 240 points, or 0.7%, snapping a 13-day winning streak, while the S&P 500 SPX, -0.64%

declined 0.6% and the Nasdaq Composite COMP, -0.55%

lost 0.5%.

Japanese stocks have solidly outpaced strong gains for U.S. equities in 2023, with the Nikkei 225 NIK, +0.68%

up 26% so far this year versus an 18.7% rise for the S&P 500.

Investors are waiting to see what the Bank of Japan actually has to say.

While the Nikkei report helped “exaggerate” a selloff in Treasurys, the market may be inoculated against bigger swings after the BOJ’s December adjustment to the rate band, said Ian Lyngen and Benjamin Jeffery, rates strategists at BMO Capital Markets, in a note.

The analysts said they expect that “the magnitude of the follow through repricing in U.S. rates will be comparatively more contained than would otherwise be expected.”

More recently, the weak yen has raised the cost of hedging long Treasury positions for Japanese investors. So a stronger yen resulting from a shift toward tighter policy would help make hedging costs for owning Treasurys less onerous for Japanese investors as well, Lyngen and Jeffery wrote, “which over the longer term may begin to make Treasurys more attractive to Japanese buyers and add to the list of sources for duration demand.”

That could make U.S. debt more attractive to new Japanese buyers, Slok agreed.

But that’s oveshadowed by the near-term worry, Slok said, that existing Japanese investors will be inclined to sell Treasurys. Flow data will be very much in focus if the Bank of Japan follows through on the apparent trial balloon floated in the Nikkei report.

Investors will be watching, he said, to see “if the train is leaving the station.”

BlackRock, the world’s largest asset manager, has filed an application for a spot bitcoin exchange-traded fund.

There are currently no such products in the U.S. The SEC approved several bitcoin BTCUSD futures-based ETFs in the past, but has yet to greenlight anything that is backed by bitcoin itself.

Even with U.S. stocks in a new bull market, investors aren’t showing many signs of backing away from money-market funds and other cash-like investments offering yields of about 5%, the highest in about 15 years.

Money-market funds hit a record of $5.9 trillion in assets as of Tuesday, signaling a continuing drain out of bank deposits into higher-yielding “cash-like” investments, according to Peter Crane, president and publisher of Crane Data.

It is the notion that the Federal Reserve could deliver a hawkish jolt to markets even if it refrains from raising rates when its two-day policy meeting ends on Wednesday.

There are concerns that such an outcome could spark a turnaround in U.S. stocks, especially if an uncomfortably strong reading on May inflation — due this coming Tuesday just as the Fed’s policy meeting is slated to begin — pushes the central bank toward something even more extreme, like delivering a rate increase on Wednesday despite intimating that it plans to abstain.

On the other hand, signs that the economy has weakened and inflation has continued to fade would help the Fed to justify skipping a rate increase in June — as several senior officials have suggested it will — while signaling that a potential hike at its following meeting in July could be the final increase for the cycle.

“Softening U.S. data should support calls that a June skip could eventually turn into a July pause. Next week, most of the data is expected to remain weak or little changed: retail sales could be flat m/m, the Fed regional surveys should remain in negative territory, and consumer sentiment will waver,” said Craig Erlam, senior market analyst at OANDA, in emailed commentary.

Wednesday’s meeting comes at a critical time for the market. U.S. stocks have powered ahead for more than six months, with the S&P 500 SPX, +0.11%

having risen more than 20% off its Oct. 12 closing low, according to FactSet. Just this past week, the index exited bear-market territory for the first time in a year.

The index is up 12% so far in 2023, reversing some of its 19.4% decline from 2022, its biggest calendar-year drop since 2008, according to Dow Jones Market Data.

So far this year, highflying tech stocks have helped to paper over weakness in other areas of the market. This has started to change over the past two weeks, as small-cap and value-stocks have lurched suddenly higher, but there are fears that the Fed could hurt the most interest-rate sensitive technology names if Chairman Jerome Powell hints at rates rising higher than investors presently anticipate.

The so-called “Megacap eight” stocks — a group that includes both classes of Alphabet Inc. stock GOOG, +0.16%

GOOGL, +0.07%,

Microsoft Corp. MSFT, +0.47%,

Tesla Inc. TSLA, +4.06%,

Microsoft Corp. MSFT, +0.47%,

Netflix Inc. NFLX, +2.60%,

Nvidia Corp. NVDA, +0.68%,

Meta Platforms Inc. META, +0.14%

— have driven nearly all of the S&P 500’s gains this year, according to Ed Yardeni, president of Yardeni Research, who included his analysis in a note to clients.

But since the beginning of June, the Russell 2000 RUT, -0.80%,

a gauge of small-cap stocks in the U.S., has risen more than 6.6%, according to FactSet data. The Russell 1000 Value Index RLV, -0.15%

has also gained nearly 3.7% in that time. During this period, both have outperformed the tech-heavy Nasdaq Composite COMP, +0.16%,

although the Nasdaq remains the market leader, having risen 26.7% since Jan. 1.

Concerns about the Fed’s plans intensified this week after the Bank of Canada delivered a surprise interest-rate hike, ending a four-month pause. The BOC’s decision followed a similar move by the Reserve Bank of Australia, and partly as a result, U.S. Treasury yields rose and tech-heavy stocks tumbled, with the Nasdaq logging its biggest drop since April 25, according to FactSet.

While small-caps held up amid the chaos, the reaction stoked fears that something similar might be in store for markets when the Fed delivers its latest decision on interest rates Wednesday.

Consequences of a ‘hawkish pause’

Stocks could be in for more turbulence if the Fed signals it plans to follow the BOC and RBA with a hawkish surprise of its own. And it wouldn’t necessarily need to hike rates to pull this off, market strategists said.

Emerging signs of complacency in the market could complicate its reaction. That the Cboe Volatility Index has fallen back below 15 VIX, +1.32%

for the first time since before the arrival of COVID-19 is one such sign that investors aren’t worried enough about a potential selloff, said Miller Tabak + Co.’s Chief Market Strategist Matt Maley.

Another analyst likened the potential fallout from a hawkish Fed to the bad old days of 2022.

“If the Fed signals that rates will be going up again, the market playbook could read more like 2022 than what we have seen so far in 2023,” said Will Rhind, the founder and CEO of GraniteShares, during a phone interview with MarketWatch.

Perhaps the biggest wild card is Tuesday’s inflation report. If the numbers come in hot, Powell and his peers could face pressure to hike rates without priming the market first.

For this reason, Rhind believes investors are underestimating the likelihood of a hike next week, even as Fed funds futures currently see a roughly 70% probability that the central bank will stand pat, according to the CME’s FedWatch tool.

And Rhind isn’t the only one. Leslie Falconio, chief investment officer at UBS Global Wealth Management, says the Tuesday inflation report could be a make-or-break moment for markets, summing up fears expressed elsewhere on Wall Street in a recent note to clients.

“We believe another rate increase is on the table, and that the CPI release on 13 June, a day before the Fed decision, will be decisive. In our view, another hike won’t have a material impact on the pace of economic growth,” Falconio said.

What should investors watch out for?

Assuming the Fed does forego a hike in June, there are a few key tells that investors should watch for to determine whether a “hawkish pause” is under way.

Perhaps the most important will be how the Fed handles changes to its closely watched “dot plot.” A modestly higher median dot would send an unmistakable signal to the market that the Fed will continue with its campaign of tightening monetary policy, perhaps to the detriment of the market, said Patrick Saner, head of macro strategy at the Swiss Re Institute.

“If the Fed skips but wanted to avoid the impression of the hiking cycle being done, it would need to include a revision of the dot plot. They could justify that with a more resilient GDP forecast and a higher inflation outlook. So I think it is the dots and then the statement that will be in focus,” Saner said during a phone interview with MarketWatch.

Beyond that, whatever the Fed does or says will likely be viewed through the lens of economic data that is due out next week. In addition to the Tuesday inflation report, a report on May retail sales is due out Thursday, and a on consumer sentiment from the University of Michigan will land on Friday. All these data points could influence investors’ impressions of the state of the U.S. economy, and their expectations for how the Fed will behave as a result.

Lawmakers and the White House appear set to avert a calamitous U.S. government default, but stock-market investors need to be aware that what comes next could still make for a bumpy ride.

“Some time in the next several days, markets will trade their last bit of angst over raising the debt ceiling for what was always going to be the real problem — handling the massive fundraise by Treasury,” said Steven Blitz, chief U.S. economist at TS Lombard, in a Wednesday note warning of a “potent liquidity squeeze” ahead.

Welcome back to Distributed Ledger. This is Frances Yue, reporter at MarketWatch.

Fears are brewing in financial markets that the U.S. lawmakers won’t be able to reach an agreement to raise the country’s debt limit by X date, or the date that the U.S. government is unable to meet its debt obligations.

Analysts at JPMorgan Chase & Co. JPM, +0.94%

on Wednesday said they see the odds of debt ceiling negotiators failing to reach a deal by early June at “around 25% and rising.”

Concerns around a technical default of U.S. government debt have contributed to volatility acrossfinancialmarkets, sending Treasury bills maturing in the first eight days of June above 6%. Yields on such bills briefly topped 7% on Thursday.

As investors search for havens from such tumult, gold and bitcoin are often cited as potential refuges.

Still, gold futures have been retreating since the most-active contract reached its second-highest settlement on record on May 4.

Bitcoin, which rallied almost 60% so far this year, have also posted lackluster performance for the past few weeks, down 5.8% over the past month.

Are gold and bitcoin effective hedges against a technical default of U.S. government debt? Why are we not seeing a rally as the X date approaches? I caught up with several analysts to ask their views.

Find me on Twitter at @FrancesYue_ to share any thoughts on crypto, gold, or this newsletter.

Is gold the haven?

FactSet

“Generally speaking, gold thrives when there are periods of uncertainty,” said Rhona O’Connell, analyst at StoneX Group. “But if you take that uncertainty too far, then we get to stages where people are sitting on their hands and not really doing very much and that’s what’s happened here.”

Gold futures for June delivery GC00, +0.09% GCM23, +0.09%

on Thursday declined by $20.90, or 1.1%, to $1,943.70 per ounce on Comex, with prices for the most-active contract posting their lowest finish since March 21, according to FactSet data.

As gold futures price retreat to below $2,000, “I suppose it’s arguable that the bulls might be a bit disappointed,” said O’Connell. But there’s “bound to be a retreat” with gold’s price premium building over the past few weeks, according to O’Connell.

“The fact that gold hasn’t managed to climb any higher given the potential seriousness of the economic consequences should no agreement be reached before the June deadline reflects a prevailing view that ultimately the markets believe some middle ground can be found in time,” Rupert Rowling, analyst at Kinesis Money, wrote in a recent note.

Still, gold’s price stays elevated at levels that were not seen many times in history.

What about bitcoin?

Considering the rally bitcoin had so far this year, it’s “not crazy to see a little bit of pullback, according to Steven Lubka, a managing director at Swan Bitcoin.

Bitcoin gained almost 60% so far this year while still down over 60% from its all-time high in 2021.

Still, if the U.S. ends up defaulting on its debt, and “everyone freaks out, bitcoin could do very well in that scenario,” Lubka said, citing bitcoin’s limited supply, decentralized and non-sovereign properties.

However, not everyone agrees. There is not enough evidence to support the claim that bitcoin could serve as a hedge against the debt ceiling tumult, according to Lapo Guadagnuolo, director at S&P Global Ratings.

“We can’t make that argument because we don’t see that in the data,” Guadagnuolo said.

A rising dollar

The recent strength of the U.S. dollar have also weighed on bitcoin and gold.

On Thursday, the ICE U.S. Dollar Index DXY, -0.02%,

which measures the currency’s strength against a basket of six major rivals, climbed above 104 to its highest level since March 17, according to Dow Jones market data.

Although a technical default of U.S. government debt could hurt the dollar’s reputation in the long term, it might have little bearing on the immediate reaction, which would resemble a knee-jerk move higher, as my colleague Joseph Adinolfi elaborated here.

As gold is mostly denominated in U.S. dollar and bitcoin’s main trading pairs are dollar-denominated stablecoins, a strong dollar could weigh on both assets.

Still, the debt ceiling debacle in the long term could strengthen the narrative around bitcoin and gold, as “the governance of the worlds fiat system comes into question,” according to Greg Magadini, director of derivatives at Amberdata.

Crypto in a snap

Bitcoin lost 2.8% in the past week and was trading at around $26,360 on Thursday, according to CoinDesk data. Ether declined 0.9% in the same period to around $1,805

When the U.S. debt-ceiling fight finally is resolved, the Treasury is expected to unleash a flood of bill issuance to help refill its coffers run low by the protracted standoff in Washington, D.C., over the government’s borrowing limit.

Treasury bills are debt issued by the U.S. government that mature in four to 52 weeks. New bill issuance could reach about $1.4 trillion through the end of 2023, with roughly $1 trillion flooding the market before the end of August, according to an estimate from BofA Global strategists.

They expect the deluge through August to be about five times the supply of an average three-month stretch in years before the pandemic.

“The good news is that we have a high degree of confidence around who is going to buy it,” said Mark Cabana, rates strategist at BofA Global, in a phone interview with MarketWatch. “The bad news is that it’s not going to be at current levels. Things have to cheapen.”

Cabana sees a key buyer of bill supply unleashed by a debt-ceiling deal in money-market funds, which have climbed to nearly $5.4 trillion in assets managed since the regional banking crisis erupted in March (see chart).

So people who yanked billions of dollars in deposits from banks after the collapse of Silicon Valley Bank in March and parked them in money-market funds could end up playing an encore performance in this year’s debt-ceiling drama.

Money-market funds swell since March, topping $5 trillion in assets

Money-market funds have been the main reason why at least $2 trillion consistently sits overnight at the Federal Reserve’s reverse repo facility. The program was last offering a roughly 5% rate, a level Cabana said new Treasury bills might need to exceed by about 10-20 basis points.

“It’s an unintended consequence of a debt-ceiling deal getting done,” said George Catrambone, head of fixed income Americas at DWS Group, about market expectations for heavy short-term Treasury bill issuance, but he also expects money-market funds, foreign buyers and other institutions auctions to continue as buyers in the market.

“There’s always buyers. It’s a question of price.”

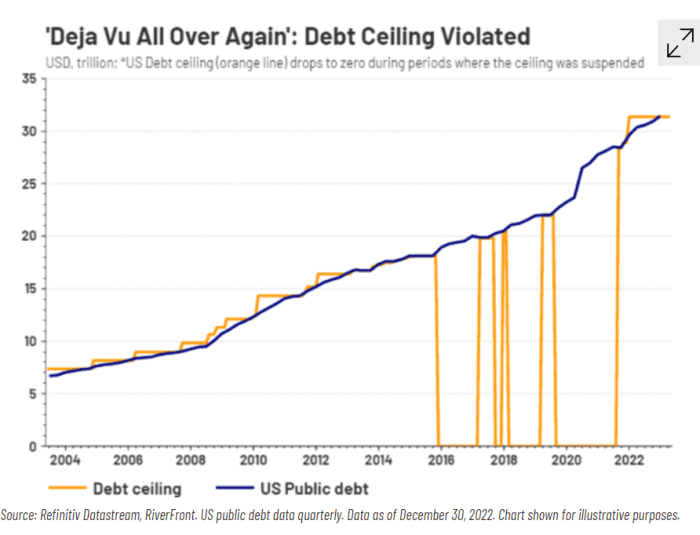

Congress has struck deals each time U.S. public debt has exceeded its debt ceiling in the past, including by suspending it eight times since 2016 (see chart).

In the past when the U.S. debt-limit has been violated, Congress extended or suspended it

Refinitive, RiverFront

That doesn’t mean financial markets have been sitting by idly. The 1-month Treasury yield TMUBMUSD01M, 5.616%

rose to 5.6% on Wednesday, while the 3-month yield TMUBMUSD03M, 5.350%

was 5.3%, according to FactSet. Bill maturing around the “X-date,” which could come as soon as June 1, have even higher yields.

“Those are obviously pretty heady yields,” Catrambone said. “But it also exemplifies the market having to price in potential market disruptions in the month of June,” even though his team, like many in financial markets, expect that eventually “cooler heads will prevail” in Washington as the debt-ceiling standoff heads down to the wire.

Stocks were lower Wednesday, with the Dow Jones Industrial Average DJIA, -0.75%

off almost 300 points, or 0.9%, on pace for a fourth day in a row of losses, according to FactSet. The S&P 500 index SPX, -0.83%

was off 0.9% and the Nasdaq Composite Index was down 0.9%.

Cash balances at the Treasury Department have since dwindled to less than $100 billion, according to economists at Jefferies. Barclays strategists estimate its cash balance may fall below $50 billion between June 5-15.

“Basically, we are just draining our cash account to fund operations while we wait to figure out the debt ceiling,” said Lindsay Rosner, senior portfolio manager at PGIM Fixed Income.

But when the battle over the debt limit ends in a resolution, she expects longer-dated Treasury yields to increase, as haven buying on fears of potentially a full U.S. government default and a credit rating downgrade will have been taken off the table.

“The Armageddon, whatever small probability people were pricing in of catastrophe, remove that,” she said. “And that means the worst economic outcome has been removed.”

That’s also a reason why Rosner has been avoiding ultrashort Treasurys in the eye of the debt-ceiling fight in favor of 2, 3 or 4-year bonds offering some of the highest yields in years.

“We’re being afforded good yield, good spread, a couple of years out the curve,” she said. “Play that game.”

Continued uncertainty about whether a debt-ceiling resolution can come together fast enough to avoid a government default pushed yields on Treasury bills maturing between early and mid-June toward 6% on Tuesday.

The yield on Treasury bills maturing on June 6 touched that level before slipping slightly to 5.997% Tuesday afternoon, according to Bloomberg data. Meanwhile, the rate on T-bills maturing on June 8 was at 5.905%.

In addition, the one-year T-bill issued in June 2022 and which matures on June 15 was yielding 6.141%, though analysts said that was likely being impacted by a government auction on Tuesday. That 6.141% yield was the highest of any government obligation maturing within two weeks after the so-called X-date of June 1 — when Treasury Secretary Janet Yellen said the government might be unable to pay all its bills if no action is taken on the debt ceiling.

The Treasury bill market is where debt-ceiling angst has played out the most and Tuesday brought wild trading as investors questioned whether the government will be forced to miss payments after June 1. At the moment, the T-bill market is in a state of dislocation — one in which yields ranged from as little as 2.924% on the government obligation maturing on May 30 to as high as 6.141% on the 1-year bill maturing in three weeks.

The higher the yield on a Treasury obligation, the more investors are demanding to be compensated for the risk of holding that bill. Yields also rise when investors are selling off or staying away from the underlying maturity. Tuesday’s moves suggest that investors and traders are factoring in at least some risk that the government could cross the X-date without a debt-ceiling resolution.

Right now, the market regards bills maturing between June 6 and June 15 as “the most at risk for a delayed payment and no one wants to own” them, said Lawrence Gillum, the Charlotte, N.C.-based chief fixed income strategist at LPL Financial.

“Ultimately, markets expect something to get done, but money managers who have to own those T-bills are not taking any chances,” he said via phone.

For much of Tuesday, the broader financial market appeared to be relatively confident that a debt-ceiling agreement could be reached by June 1, a day after President Joe Biden and House Speaker Kevin McCarthy each described talks as “productive” on Monday. Then came word of McCarthy telling House Republicans on Tuesday that negotiators were nowhere near a deal yet, with Bloomberg citing Republican Representative Ralph Norman and another unidentified person in the room.

COMP, -1.26%

finished lower, while Treasury yields beyond the 2-year rate slipped toward the end of Tuesday’s New York trading session — a sign of fading optimism in the outlook for the U.S. economy.

One of the financial market’s favorite indicators of impending U.S. recessions — the difference between the 2- and 10-year Treasury yields — has been persistently inverted since July 5, 2022. That’s the longest such streak since May 1980, and yet no recession has been declared so far by the only arbiters who matter, those at the National Bureau of Economic Research.

On Tuesday, fed funds futures traders priced in a 28.1% chance of another quarter-point rate hike by the central bank in June, which would take the main policy rate target to between 5.25%-5.5%. They also factored in a slight 5.6% likelihood of another similar-size rate hike in July.

Gillum and Greg Faranello, head of U.S. rates at AmeriVet Securities in New York, said they see a small chance of no debt-ceiling agreement by June 1. Under such a scenario, the Treasury market would fall into “disarray,” with T-bill yields spiking in a manner reminiscent of last year’s crisis of confidence in the U.K. bond market, they said. It would also make it harder for the Fed to hike rates on June 14, and likely lead to a flight-to-quality trade in longer-term Treasurys as equities sell off.

As of Tuesday, the T-bill market was “definitely showing some signs of stress, there’s no question about it,” Faranello said via phone. Meanwhile, “the economy is doing better than the narrative of recession,” even after the recent turmoil in regional banks, and a move toward 4% in the 10-year rate this year “can’t be ruled out.” However, that could change quickly based on the outcome of the debt-ceiling debate.

Getting something done on the debt ceiling by June 1 “is going to be a challenge,” Faranello said. The risk of default “is small but not a zero-percent probability,” as is the prospect of chaos if negotiators come too close to the wire and create a period of confusion in the Treasury market.

“At a minimum, there would be pretty severe economic damage” from a default or any confusion, it “could be chaotic,” and “you would see that impact on risk assets,” he said.

When it comes to investing, some people don’t think in terms of thousands of dollars, tens of thousands, or even millions.

They think in hundreds of millions, or even billions. They have so much money they actually set up a private company, known as a “family office,” to manage all the loot.

Popular crypto exchange Coinbase COIN, -7.27%

late Monday asked a federal court to force the U.S. Securities and Exchange Commission to respond yes or no to its petition from July 2022 to make formal rules around digital-asset regulation.

Coinbase’s petition requested that the “Commission propose and adopt rules to govern the regulation of securities that are offered and traded via digitally native methods, including potential rules to identify which digital assets are securities.”

In March, Coinbase was hit with a Wells notice from the SEC, identifying potential violations of securities laws that might spur it to take legal action. The notice came after nine months of back-and-forth between the SEC and Coinbase, CEO Brian Armstrong said in March.

Coinbase was expected to respond to the notice by the end of April, but Monday’s filing reveals that Coinbase believes the SEC’s approach doesn’t provide enough regulatory guidance for crypto companies in the U.S. to operate.

“The SEC at a minimum must set forth how those inapt and inapposite requirements are to be adapted to digital assets. But the SEC has refused to do even that,” the filing says. “It has not conducted any rulemaking to provide the regulatory clarity and process that companies need to determine which digital asset products and services to register and how to make the registration that the SEC now demands.”

Coinbase shares slid more than 7% on Monday but are up 55% year to date. Still, the stock is down nearly 60% over the past 12 months. In comparison, the S&P 500 SPX, +0.09%

is up nearly 8% in 2023 and has declined almost 4% over the past year.

U.S. stocks just touched their highest levels in two months. Yet, signs of a looming selloff are piling up, according to Jonathan Krinsky, chief technical strategist at BTIG.

The S&P 500 SPX, +0.33%

and Russell 3000 RUA, +0.40%

are both trading just shy of their highs from mid-February, but market breadth hasn’t recovered, as index gains over the past month have largely relied on megacap names like Microsoft Corp. MSFT, +0.93%

and Apple Inc. AAPL, +0.01%

helping to offset weakness in other areas of the market.

As of Friday, only 45% of Russell 3000 stocks were trading above their 200-day moving averages, according to data cited by Krinsky. By comparison, when the broad-market gauge was trading at its highest level of 2023 back in February, 70% of the individual stocks included in the index were trading above their 200-day moving average. Technical analysts use moving averages as a gauge of a stock or index’s momentum.

BTIG

Lackluster breath is looking like more of an issue analysts say, especially now that the Nasdaq’s outperformance appears to be fading after leading markets higher since the start of the year.

Over the last two weeks, the Dow Jones Industrial Average DJIA, +0.30%

has outperformed the Nasdaq Composite COMP, +0.28%

by the widest margin since the two-week period ending Dec 30, according to FactSet data.

Krinsky cited exchange-traded funds that feature megacap technology names, including the iShares Expanded Tech-Software ETF IGV, +0.45%,

the Communications Services Select Sector SPDR Fund ETF XLC, -0.57%

and Consumer Discretionary Select Sector SPDR Fund ETF XLY, +0.71%,

as examples of emerging weakness in this critical sector of the market. Meanwhile, regional bank stocks, small-cap stocks and shares of retailers, all of which have lagged behind the market this year, look weak.

Krinsky summed up this dynamic thus: “The weak parts of the market remain weak, while the strong parts now appear vulnerable,” the BTIG analyst said in a Sunday note to clients.

Furthermore, “[i]n absolute and relative terms, the tech sector looks like a poor risk/reward to us here,” Krinsky added.

Low implied volatility is another issue for markets, Krinsky said. That can mean investors have gotten too complacent and markets may be heading for a selloff, analysts say.

The Cboe Volatility Index VIX, -0.41%,

otherwise known as Wall Street’s “fear gauge,” finished Friday at its lowest end-of-day level since Jan. 4, according to Dow Jones Market Data. The Cboe S&P 500 9-Day Volatility Index, which tracks implied volatility over a shorter time horizon, has also fallen to January lows, FactSet data show.

Such low levels mean volatility could be poised to “mean revert,” Krinsky said, which may portend a selloff in the months ahead for the S&P 500, the most liquid and most closely watched gauge of U.S. stock-market performance.

Implied volatility gauges measure activity in option contracts linked to the S&P 500 to gauge how volatile traders expect markets to be over the coming days and weeks. Typically, implied volatility advances when U.S. stocks are falling.

The greenback has shown some signs of life in recent sessions, although the U.S. dollar remains well below the multi decade highs it reached back in September. That the buck bounced off its February lows late last week suggests that momentum could be skewed toward the upside for the dollar, Krinsky said, which could create more problems for stocks given the dollar’s tendency to weigh on markets during 2022.

The ICE U.S. Dollar Index DXY, -0.43%,

a gauge of the dollar’s strength measured against a basket of rivals, was up 0.7% in recent trade at 102.22.

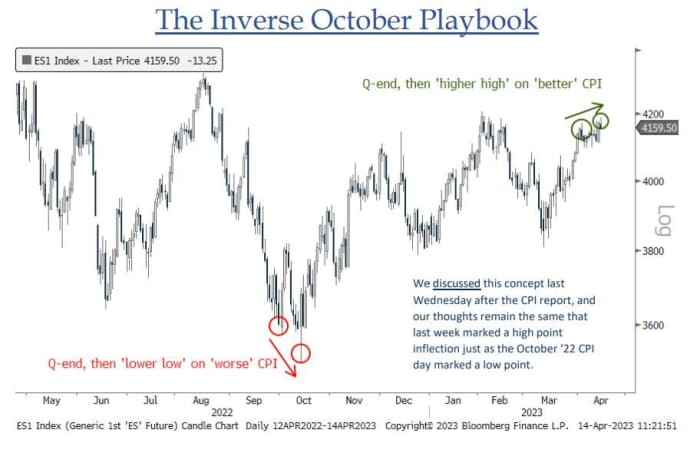

All of these factors support the notion that stocks could be headed for what Krinsky called the “reverse October playbook.”

BTIG

Just as the S&P 500 bottomed following the hotter-than-expected September report on consumer-price inflation, the market’s monthslong rebound rally may have peaked following last week’s CPI report for March, which showed consumer prices rose a scant 0.1% last month, less than the 0.2% increase that had been forecast by economists polled by MarketWatch.

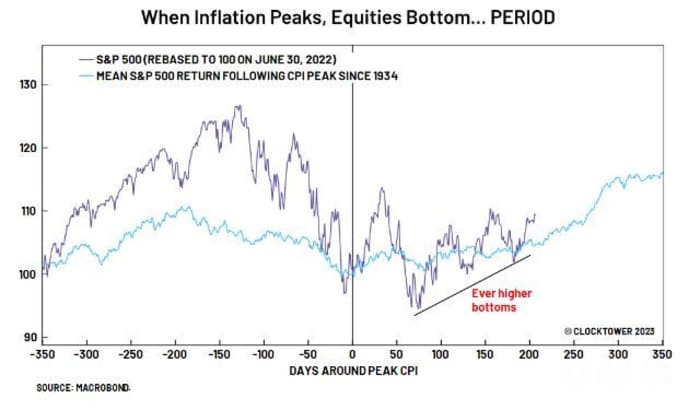

Not everybody agrees with this assessment. Marko Papic, chief strategist at Clocktower Group, cited market data going back to 1934 to show that U.S. stocks tend to rally after inflation peaks. Consumer-price inflation reached its highest level in more than four decades when the CPI headline number showed prices up 9.1% year-over-year in June.

CLOCKTOWER GROUP

U.S. stocks look set to decline for a second day in a row on Monday, with the S&P 500 off 0.3% at 4,126, while the Nasdaq Composite was down by 0.4% at 12,070, and the Dow Jones Industrial Average traded marginally lower at 33,881.

This copy is for your personal, non-commercial use only. To order presentation-ready copies for distribution to your colleagues, clients or customers visit http://www.djreprints.com.

Bitcoin rallied Monday to its highest level in 10 months, as some industry proponents touted the asset as a potential “safe haven,” like gold, as recession fears return to the forefront, and after fears rose last month about potential instability in the banking system.

The world’s largest cryptocurrency topped $30,000 Monday night for the first since June 10, 2022, according to Dow Jones Market Data, peaking at $30,321 before pulling back. Bitcoin BTCUSD, +3.20%

has surged 81% year to date, though is still down over 57% from an all-time high in November 2021. Ethereum ETHUSD, +1.68%

also rallied Monday, and was closing in on the $2,000 level for the first time since last August.

“With the bank crisis, I think that the leading feature of bitcoin has changed from speculative tech to safety. A lot more like gold,” said David Tawil, president and co-founder at ProChain Capital. Some investors may have started to view the asset as a haven from the banking turmoil and a recession, instead of a speculative asset, Tawil said.

Still, bitcoin has been often trading in tandem with other risky assets, such as stocks, for the past few years.

“I also believe there will be an influx of liquidity from Asia, especially Asian tech companies who had accounts with Silicon Valley Bank who are now looking for places to put their money,” according to Stefan Rust, founder of Truflation.

The rally on Monday may be partially driven by “the growing influence on the crypto market led by Hong Kong,” while U.S. regulators increase their oversight over the industry, according to Rachel Lin, co-founder and chief-executive at Synfutures.

Hong Kong Financial Secretary Paul Chan said Sunday in a blog post that while crypto markets have been highly volatile, it’s the “right time” to push the adoption of Web3, or the so-called third generation of the internet, in the region.

Bitcoin had been attempting to break the $30,000 level, a psychological level, for three weeks, Rust noted.

Stocks were mixed Monday, with the Dow Jones Industrial Average DJIA, +0.30%

up 0.3% and the S&P 500 SPX, +0.10%

up 0.1%, while the Nasdaq Composite COMP, -0.03%

dipped 0.1%.