FRANKFURT, Germany — The European Central Bank piled on another outsized interest rate hike aimed at squelching out-of-control inflation, increasing rates Thursday at the fastest pace in the euro currency’s history and raising questions about how far the bank intends to go with a recession looming over the economy.

The 25-member governing council raised its interest rate benchmarks by three-quarters of a percentage point at a meeting in Frankfurt, matching its record increase from last month and joining the U.S. Federal Reserve in making a series of rapid hikes to tackle soaring consumer prices.

The ECB has now raised rates for the 19-country euro area by a full 2 percentage points in just three months, distance that took 18 months to cover during its last extended hiking phase in 2005-2007 and 17 months in 1999-2000.

Central banks around the world are rapidly raising interest rates that steer the cost of credit for businesses and consumers. Their goal is to halt galloping inflation fueled by high energy prices, post-pandemic supply bottlenecks, and reviving demand for goods and services after COVID-19 restrictions eased. The Fed raised rates by three-quarters of a point for the third straight time last month.

Quarter-point increases have usually been the norm for central banks. But that was before inflation spiked to 9.9% in the eurozone, fueled by higher prices for natural gas and electricity after Russia cut off most of its gas supplies during the war in Ukraine. Inflation in the U.S. is near 40-year highs of 8.2%, fueled in part by stronger growth and more pandemic support spending than in Europe.

Inflation robs consumers of purchasing power, leading many economists to pencil in a recession for the end of this year and the beginning of next year in both the U.S. and the 19 countries that use the euro as their currency.

Markets will be watching ECB President Christine Lagarde’s news conference for clues about how far the bank intends to go.

Analysts at UniCredit said Lagarde was not likely to provide clues about the peak level of rates but “we suspect that she will drop hints pointing to an increasing likelihood that rates will have to be raised into restrictive territory, and a slower pace of hikes following today’s bold move.”

At the last meeting in September, she indicated that three-quarters of a point was not the “norm” but added that decisions are being taking on a meeting-to-meeting basis. Some analysts foresee a half-point increase at the last rate-setting meeting of the year in December and think the bank may pause after that.

The ECB foresees inflation falling to 2.3% by the end of 2024.

Higher rates can control inflation by making it more expensive to borrow, spend and invest, lowering demand for goods. But the concerted effort to raise rates has also raised concerns about their impact on growth and on markets for stocks and bonds. Years of low rates on conservative investments have pushed investors toward riskier holdings such as stocks, a process that is now going into reverse, while rising rates can lower the value of existing bond holdings.

The head of the International Monetary Fund, Kristalina Georgieva, has warned that tightening monetary policy “too much and too fast” raises the risk of prolonged recessions in many economies. The IMF forecasts that global economic growth will slow from 3.2% this year to 2.7% next year.

The ECB’s benchmark for short-term lending to banks now stands at 2%, a level last seen in March 2009.

WASHINGTON — The problems have hardly gone away. Inflation, still near a 40-year high, is punishing households. Rising interest rates have derailed the housing market and threaten to inflict broader damage. And the outlook for the world economy grows bleaker the longer that Russia’s war against Ukraine drags on.

But for now anyway, the U.S. economy has likely returned to growth after having shrunk in each of the first two quarters of 2022.

At least that’s what economists expect to see Thursday when the Commerce Department issues its first of three estimates of gross domestic product — the broadest measure of economic output — for the July-September period.

Economists surveyed by the data firm FactSet have predicted, on average, that GDP grew at a 2% annual rate in the third quarter. That would reverse annual declines of 1.6% from January through March and 0.6% from April through June.

Consecutive quarters of declining economic output are one informal definition of a recession. But most economists say they believe the economy has so far skirted a recession, noting the still-resilient job market and steady spending by consumers. Most of them have expressed concern, though, that a recession is likely next year as the Federal Reserve continues to steadily ratchet up interest rates to fight inflation.

Preston Caldwell, head of U.S. economics for the financial services firm Morningstar, notes that the economy’s contraction in the first half of the year was caused largely by factors that don’t reflect its underlying health and so “very likely did not constitute a genuine economic slowdown.” He pointed, for example, to a drop in business inventories, a cyclical event that tends to reverse itself and generally doesn’t reflect the state of the economy.

By contrast, consumer spending, fueled by a healthy job market, and stronger U.S. exports likely restored the world’s biggest economy to growth last quarter.

Thursday’s report from the government comes as Americans, worried about high prices and recession risks, are preparing to vote in midterm elections that will determine whether President Joe Biden’s Democratic Party retains control of Congress. Inflation has become a signature issue for Republican attacks on the Democrats’ stewardship of the economy.

The risk of an economic downturn next year remains elevated as the Fed keeps raising rates aggressively to try to tame stubbornly high consumer prices. The central bank has raised its benchmark short-term rate five times this year, and it’s expected to announce further hikes next week and again in December. Chair Jerome Powell has warned bluntly that taming inflation will “bring some pain’’ — namely, higher unemployment and, possibly, a recession.

Higher borrowing costs have already hammered the home market. The average rate on a 30-year fixed-rate mortgage, just 3.09% a year ago, is approaching 7%. Sales of existing homes have fallen for eight straight months. Construction of new homes is down nearly 8% from a year ago.

Still, the economy retains pockets of strength. One is the vitally important job market. Employers have added an average of 420,000 jobs a month this year, putting 2022 on track to be the second-best year for job creation (behind 2021) in Labor Department records going back to 1940. The unemployment rate was 3.5% last month, matching a half-century low.

But hiring has been decelerating. In September, the economy added 263,000 jobs — solid but the lowest total since April 2021.

International events are causing further concerns. Russia’s invasion of Ukraine has disrupted trade and raised prices of energy and food, creating a crisis for poor countries. The International Monetary Fund, citing the war, this month downgraded its outlook for the world economy in 2023.

LONDON — It took one bruising campaign defeat and six weeks of exile — but on Tuesday, Rishi Sunak will finally become U.K. prime minister.

He faces the toughest in-tray of any British leader since World War II, entering No. 10 Downing Street as the country hurtles into winter with energy bills, hospital waiting lists, borrowing costs and inflation all soaring.

The challenge has been magnified by Liz Truss’ brief crash-and-burn premiership. As a result of her now-infamous mini-budget, which was scrapped almost in its entirety after causing chaos in financial markets, the Conservatives are trailing the opposition Labour Party by over 30 percentage points in opinion polls.

On Monday, Sunak told MPs he was ready to hit the ground running as he addressed them for the first time since becoming Tory leader. Over the days and months ahead, he will need to carry out his first ministerial reshuffle without further fracturing his party; oversee the first budget since the last one wreaked havoc on the economy; and determine what support to offer voters with their energy bills past this spring.

Prime ministers tend to think of their first 100 days as a way to set the tone for their premierships. For Sunak, who has just over two years to govern before he is required to face a general election, that first impression is going to be particularly important.

October 25 — Meeting with the king and first speech outside No. 10 Downing Street

Sunak will become the prime minister Tuesday after an audience with King Charles III, where he will ask the monarch for permission to form a government.

Sunak will then address the country for the first time as prime minister from the steps outside No. 10 Downing Street at around 11.35 a.m.

To much of the British public, the former chancellor is a familiar face who announced the wildly-popular furlough scheme during the coronavirus pandemic in 2020.

His task now will be to reassure people that the government will support them during another difficult economic period — only this time he is in a much tougher position. The popularity he gained during the pandemic has waned, and he is taking over after a major government crisis — the third Tory prime minister to hold office within three months.

October 25 — First reshuffle

The first big political test for Sunak will be his Cabinet reshuffle. Tory MPs believe he will learn the lesson from Truss’ first and only one, where she divvied up roles between her allies and left almost everyone who didn’t back her out in the cold.

“I think his reshuffle will be more unifying, bringing in people from all wings and will not be as destabilizing as Liz’s,” an MP who did not back Sunak predicted.

Sunak’s leadership rival Penny Mordaunt is expected to be handed a major Cabinet position | Dan Kitwood/Getty Images

Sunak is likely to make at least his major Cabinet appointments Tuesday afternoon, so they are in place to line up alongside him on the House of Commons’ front bench when MPs grill him during so-called prime minister’s questions (PMQs) on Wednesday.

His biggest decision will be whether to keep Jeremy Hunt — who was drafted in by Truss in a last-ditch effort to save her premiership — as chancellor. He is also likely to hand a big job to his leadership rival Penny Mordaunt.

Close Sunak allies who are likely to get promotions include Mel Stride, the current chairman of the Treasury select committee, Craig Williams, Claire Coutinho and Laura Trott. Tory big beast Michael Gove could see a return to Cabinet.

October 26 — First PMQs

Sunak will go head-to-head as prime minister with Keir Starmer, the Labour leader, for the first time on Wednesday.

Unlike his predecessor, Sunak won’t have much to worry about from his own side — Tory MPs have largely rowed behind him since he became their leader on Monday, with many expressing relief that the perpetual state of crisis of the Truss government has ended.

But MPs will want him to demonstrate that he can land blows against Starmer at a time when Labour is streets ahead in the polls. Sunak told Tory MPs on Tuesday that their party faced an “existential threat” as a result of its low poll ratings.

October 28 — Deadline to form a government in Belfast

If a power-sharing arrangement is not in place at Stormont by Friday, a fresh set of elections to the Northern Irish assembly will have to be triggered.

Calling these elections — the second set in seven months — could be one of the Sunak government’s first acts and an indication of successive Tory prime ministers’ failure to deal with the political crisis in Northern Ireland.

The Democratic Unionist Party issued a fresh warning on Monday night that it would not participate in the assembly unless Sunak takes action on the post-Brexit Northern Ireland protocol agreed with the EU.

October 31 — First budget

The next budget was penciled in for October 31 by Kwasi Kwarteng, the Truss-era chancellor who wanted to use it to reassure financial markets still reeling from his last one.

The timing of the budget — widely derided by Tory MPs because of the optics of holding it on Halloween — was intended to give the Bank of England time to react before its own key meeting on November 3, where it will set interest rate levels for the weeks ahead.

In its biggest test so far, Sunak’s government will have to decide whether to stick with that date; what actions to take to reassure the markets; and how to fill the enormous hole in the U.K. public finances.

Carl Emmerson, deputy director of the Institute for Fiscal Studies, said: “If his chancellor is Jeremy Hunt and Sunak is comfortable with the way things are proceeding for next Monday, then going ahead has lots of advantages.

“You get the announcement out before the Bank of England makes its next inflation figure, and you get the Office for Budgetary Responsibility forecasts out there, which helps show the markets you are serious about them.

“The case for changing that date is much stronger if Sunak says, ‘Actually, I want to do something different to what Jeremy Hunt has been planning, and I need more time,’” Emmerson added.

November 3 — Bank of England rates meeting

The Bank of England’s monetary policy committee is expected to raise interest rates at its meeting on November 3, triggering a fresh hike in people’s mortgages.

This is the point when many people will realize for the first time that they will have to make much larger mortgage repayments once their current fixed-rate deals come to an end.

Sunak made combating inflation and keeping mortgages low a central theme of his leadership campaign over the summer. Reacting to the rates decision and ensuring the government works closely with the Bank of England to combat inflation will be a key test of his premiership.

November 6 — COP27 summit in Egypt

Sunak made a point of telling Tory MPs on Tuesday that he is committed to the U.K.’s goal of achieving net-zero carbon emissions by 2050.

The question now is whether he attends the COP27 climate summit in Sharm El Sheikh, Egypt. Truss reportedly planned to go, despite her skepticism of aspects of the net-zero agenda.

If Sunak does go to Egypt, it could be his first foreign trip in office (unless he decides to make a quick visit to Ukraine beforehand) and his first opportunity to present himself on the world stage.

November 8 — Boundary changes

The Boundary Commission for England will publish its new constituency map on November 8.

At this point, some Tory MPs will know with near certainty that their constituencies are being carved up between neighboring areas, with some forced to jostle with colleagues over who will get to stand where.

It will be a political headache for Sunak to deal with, and any MPs whose safe seats become marginal will sense their political careers coming to an end — and will have less of an incentive to support him in key votes in the months ahead.

November 13 — G20 meeting in Indonesia

The next big foreign trip coming down the track is the G20 summit in Bali, Indonesia.

The meeting will be an opportunity for Western powers to present a united front against Russia following its invasion of Ukraine and against China’s increased aggression toward Taiwan, but also to hold talks behind closed doors. There have been reports that both China’s Xi Jinping and Russian Vladimir Putin will attend.

Sophia Gaston, the head of foreign policy at the Policy Exchange think tank, said this was shaping up to be “one of the most extraordinary summits of modern history, with a violent war raging in Ukraine and the leading protagonist, Vladimir Putin, on the guest list alongside other autocratic leaders and outraged democratic allies.”

“As well as promoting free trade and the rules-based international order, Sunak would likely see the G20 as an opportunity to build support for his proposed ‘NATO-style’ technology alliance,” Gaston said. “He may well also debut a new U.K. message on the net-zero transition.”

Late November or early December — Chester by-election

Labour whips are preparing to trigger a by-election in the city of Chester in late November or December.

The by-election is taking place because the city’s MP Christian Matheson resigned after a parliamentary watchdog recommended he be suspended for sexual misconduct.

Matheson sits on a 6,164-vote majority, and the seat has traditionally been a swing seat flipping between the Tories and Labour. It was Conservative up until 2010.

Based on current polling figures, Labour should win a significantly larger majority than it currently has, though by-elections do suffer from small turnouts and so unexpected results are not uncommon. A dramatic Tory defeat would set alarm bells ringing in the party.

Another by-election could be triggered in the coming months if, as expected, Boris Johnson elevates his ally and MP Nadine Dorries to the House of Lords in his resignation honors. That would likely be the first by-election in a Tory-held seat fought with Sunak as party leader.

December 31 — U.K. deadline for joining trans-Pacific trade bloc

The U.K. government has said it hopes to conclude negotiations on joining the CPTPP — a trade agreement signed by 11 countries including Australia and New Zealand — by the end of the year.

Securing this deal was one of Truss’ priorities. For Sunak it would represent both a concrete foreign policy achievement and an indication that the U.K. is successfully building closer diplomatic ties with countries in the Indo-Pacific after Brexit.

Talks around the partnership have thrown up some diplomatic obstacles, with China reacting angrily to U.K. trade officials meeting Taiwanese counterparts. Both China and Taiwan have applied to join the CPTPP.

There have been suggestions that the evidence against him is so damning that Johnson could face temporary suspension from parliament or even be kicked out as an MP. The inquiry may have formed part of Johnson’s decision not to stand for the Tory leadership contest.

If the privileges committee says Johnson should be sanctioned once it concludes its inquiry, Sunak will have to judge his response and decide whether to whip Tory MPs to back its recommendations even if that provokes Johnson’s ire. There is also the risk that Sunak himself will be dragged into the probe, given he too was fined over the Partygate scandal.

Among other things, the probe will examine the impact of the economic policies that Sunak designed as chancellor during the pandemic, putting his decisions under scrutiny.

His “Eat Out to Help Out” scheme — which encouraged people to dine in restaurants during the post-lockdown summer of 2020 — could become a focus, with critics claiming it drove up coronavirus-related infections and deaths.

February — Energy support nears its end

By the time Sunak’s first 100 days are up, there will be pressure on the government to explain how it will support people with their energy bills past the spring if wholesale gas prices haven’t drastically fallen. Hunt has already rolled back the Truss government’s two-year guarantee and instead capped people’s energy bills at an average of £2,500 for just six months. That policy ends in April.

The Institute for Fiscal Studies’ Emmerson said: “We’ve got a big generous offer from the government through this winter — although prices are still a lot higher than they were last year, they will be nowhere near as high as they would have otherwise been.

“The prime minister and chancellor will spend a lot of time thinking about how they replace that scheme. In some ways, it’s very similar to the kind of furlough scheme that Sunak had during the pandemic — very generous, big scheme with lots of crude edges to it,” he said.

“It’s understandable wanting to get in place quickly to support people, but how do you get out of it? Do it too quickly and that’s too much pain for too many people — keep it in place for too long, and that’s very expensive to the government.”

It’s just one of so many enormous decisions the new PM faces in his first 100 days.

Foreign investors spooked by the outcome of the Communist Party’s leadership reshuffle dumped Chinese equities and the yuan despite the release of stronger-than-expected GDP data. They’re worried that Xi’s tightening grip on power will lead to the continuation of Beijing’s existing policies and further dent the economy.

Hong Kong’s benchmark Hang Seng

(HSI) Index plunged 6.4% on Monday, marking its biggest daily drop since November 2008. The index closed at its lowest level since April 2009.

The Chinese yuan weakened sharply, hitting a fresh 14-year low against the US dollar on the onshore market. On the offshore market, where it can trade more freely, the currency tumbled 0.8%, hovering near its weakest level on record, even as the Chinese economy grew 3.9% in the third quarter from a year ago, according to the National Bureau of Statistics. Economists polled by Reuters had expected growth of 3.4%.

The sharp sell-off came one day after the ruling Communist Party unveiled its new leadership for the next five years. In addition to securing an unprecedented third term as party chief, Xi packed his new leadership team with staunch loyalists.

A number of senior officials who have backed market reforms and opening up the economy were missing from the new top team, stirring concerns about the future direction of the country and its relations with the United States. Those pushed aside included Premier Li Keqiang, Vice Premier Liu He, and central bank governor Yi Gang.

“It appears that the leadership reshuffle spooked foreign investors to offload their Chinese investment, sparking heavy sell-offs in Hong Kong-listed Chinese equities,” said Ken Cheung, chief Asian forex strategist at Mizuho bank.

The GDP data marked a pick-up from the 0.4% increase in the second quarter, when China’s economy was battered by widespread Covid lockdowns. Shanghai, the nation’s financial center and a key global trade hub, was shut down for two months in April and May. But the growth rate was still below the annual official target that the government set earlier this year.

“The outlook remains gloomy,” said Julian Evans-Pritchard, senior China economist for Capital Economics, in a research report on Monday.

“There is no prospect of China lifting its zero-Covid policy in the near future, and we don’t expect any meaningful relaxation before 2024,” he added.

Coupled with a further weakening in the global economy and a persistent slump in China’s real estate, all the headwinds will continue to pressure the Chinese economy, he said.

Evans-Pritchard expected China’s official GDP to grow by only 2.5% this year and by 3.5% in 2023.

Monday’s GDP data were initially scheduled for release on October 18 during the Chinese Communist Party’s congress, but were postponed without explanation.

The possibility that policies such as zero-Covid, which has resulted in sweeping lockdowns to contain the virus, and “Common Prosperity” — Xi’s bid to redistribute wealth — could be escalated was causing concern, Cheung said.

“With the Politburo Standing Committee composed of President Xi’s close allies, market participants read the implications as President Xi’s power consolidation and the policy continuation,” he added.

Mitul Kotecha, head of emerging markets strategy at TD Securities, also pointed out that the disappearance of pro-reform officials from the new leadership bodes ill for the future of China’s private sector.

“The departure of perceived pro-stimulus officials and reformers from the Politburo Standing Committee and replacement with allies of Xi, suggests that ‘Common Prosperity’ will be the overriding push of officials,” Kotecha said.

Under the banner of the “Common Prosperity” campaign, Beijing launched a sweeping crackdown on the country’s private enterprise, which shook almost every industry to its core.

“The [market] reaction in our view is consistent with the reduced prospects of significant stimulus or changes to zero-Covid policy. Overall, prospects of a re-acceleration of growth are limited,” Kotecha said.

On the tightly controlled domestic market in China, the benchmark Shanghai Composite Index dropped 2%. The tech-heavy Shenzhen Component Index lost 2.1%.

The Hang Seng Tech Index, which tracks the 30 largest technology firms listed in Hong Kong, plunged 9.7%.

Shares of Alibaba

(BABA) and Tencent

(TCEHY) — the crown jewels of China’s technology sector — both plummeted more than 11%, wiping a combined $54 billion off their stock market value.

The sell-off spilled over into the United States as well. Shares of Alibaba and several other leading Chinese stocks trading in New York, such as EV companies Nio

(NIO) and Xpeng, Alibaba rivals JD.com

(JD) and Pinduoduo

(PDD) and search engine Baidu

(BIDU), were all down sharply Thursday afternoon.

Some investors are on edge that the Federal Reserve may be overtightening monetary policy in its bid to tame hot inflation, as markets look ahead to a reading this coming week from the Fed’s preferred gauge of the cost of living in the U.S.

“Fed officials have been scrambling to scare investors almost every day recently in speeches declaring that they will continue to raise the federal funds rate,” the central bank’s benchmark interest rate, “until inflation breaks,” said Yardeni Research in a note Friday. The note suggests they went “trick-or-treating” before Halloween as they’ve now entered their “blackout period” ending the day after the conclusion of their November 1-2 policy meeting.

“The mounting fear is that something else will break along the way, like the entire U.S. Treasury bond market,” Yardeni said.

Treasury yields have recently soared as the Fed lifts its benchmark interest rate, pressuring the stock market. On Friday, their rapid ascent paused, as investors digested reports suggesting the Fed may debate slightly slowing aggressive rate hikes late this year.

Stocks jumped sharply Friday while the market weighed what was seen as a potential start of a shift in Fed policy, even as the central bank appeared set to continue a path of large rate increases this year to curb soaring inflation.

The stock market’s reaction to The Wall Street Journal’s report that the central bank appears set to raise the fed funds rate by three-quarters of a percentage point next month – and that Fed officials may debate whether to hike by a half percentage point in December — seemed overly enthusiastic to Anthony Saglimbene, chief market strategist at Ameriprise Financial.

“It’s wishful thinking” that the Fed is heading toward a pause in rate hikes, as they’ll probably leave future rate hikes “on the table,” he said in a phone interview.

“I think they painted themselves into a corner when they left interest rates at zero all last year” while buying bonds under so-called quantitative easing, said Saglimbene. As long as high inflation remains sticky, the Fed will probably keep raising rates while recognizing those hikes operate with a lag — and could do “more damage than they want to” in trying to cool the economy.

“Something in the economy may break in the process,” he said. “That’s the risk that we find ourselves in.”

‘Debacle’

Higher interest rates mean it costs more for companies and consumers to borrow, slowing economic growth amid heightened fears the U.S. faces a potential recession next year, according to Saglimbene. Unemployment may rise as a result of the Fed’s aggressive rate hikes, he said, while “dislocations in currency and bond markets” could emerge.

U.S. investors have seen such financial-market cracks abroad.

The Bank of England recently made a surprise intervention in the U.K. bond market after yields on its government debt spiked and the British pound sank amid concerns over a tax cut plan that surfaced as Britain’s central bank was tightening monetary policy to curb high inflation. Prime minister Liz Truss stepped down in the wake of the chaos, just weeks after taking the top job, saying she would leave as soon as the Conservative party holds a contest to replace her.

“The experiment’s over, if you will,” said JJ Kinahan, chief executive officer of IG Group North America, the parent of online brokerage tastyworks, in a phone interview. “So now we’re going to get a different leader,” he said. “Normally, you wouldn’t be happy about that, but since the day she came, her policies have been pretty poorly received.”

Meanwhile, the U.S. Treasury market is “fragile” and “vulnerable to shock,” strategists at Bank of America warned in a BofA Global Research report dated Oct. 20. They expressed concern that the Treasury market “may be one shock away from market functioning challenges,” pointing to deteriorated liquidity amid weak demand and “elevated investor risk aversion.”

“The fear is that a debacle like the recent one in the U.K. bond market could happen in the U.S.,” Yardeni said, in its note Friday.

“While anything seems possible these days, especially scary scenarios, we would like to point out that even as the Fed is withdrawing liquidity” by raising the fed funds rate and continuing quantitative tightening, the U.S. is a safe haven amid challenging times globally, the firm said. In other words, the notion that “there is no alternative country” in which to invest other than the U.S., may provide liquidity to the domestic bond market, according to its note.

YARDENI RESEARCH NOTE DATED OCT. 21, 2022

“I just don’t think this economy works” if the yield on the 10-year Treasury TMUBMUSD10Y, 4.228%

note starts to approach anywhere close to 5%, said Rhys Williams, chief strategist at Spouting Rock Asset Management, by phone.

Ten-year Treasury yields dipped slightly more than one basis point to 4.212% on Friday, after climbing Thursday to their highest rate since June 17, 2008 based on 3 p.m. Eastern time levels, according to Dow Jones Market Data.

Williams said he worries that rising financing rates in the housing and auto markets will pinch consumers, leading to slower sales in those markets.

“The market has more or less priced in a mild recession,” said Williams. If the Fed were to keep tightening, “without paying any attention to what’s going on in the real world” while being “maniacally focused on unemployment rates,” there’d be “a very big recession,” he said.

Investors are anticipating that the Fed’s path of unusually large rate hikes this year will eventually lead to a softer labor market, dampening demand in the economy under its effort to curb soaring inflation. But the labor market has so far remained strong, with an historically low unemployment rate of 3.5%.

George Catrambone, head of Americas trading at DWS Group, said in a phone interview that he’s “fairly worried” about the Fed potentially overtightening monetary policy, or raising rates too much too fast.

The central bank “has told us that they are data dependent,” he said, but expressed concerns it’s relying on data that’s “backward-looking by at least a month,” he said.

The unemployment rate, for example, is a lagging economic indicator. The shelter component of the consumer-price index, a measure of U.S. inflation, is “sticky, but also particularly lagging,” said Catrambone.

At the end of this upcoming week, investors will get a reading from the personal-consumption-expenditures-price index, the Fed’s preferred inflation gauge, for September. The so-called PCE data will be released before the U.S. stock market opens on Oct. 28.

Meanwhile, corporate earnings results, which have started being reported for the third quarter, are also “backward-looking,” said Catrambone. And the U.S. dollar, which has soared as the Fed raises rates, is creating “headwinds” for U.S. companies with multinational businesses.

“Because of the lag that the Fed is operating under, you’re not going to know until it’s too late that you’ve gone too far,” said Catrambone. “This is what happens when you’re moving with such speed but also such size, he said, referencing the central bank’s string of large rate hikes in 2022.

“It’s a lot easier to tiptoe around when you’re raising rates at 25 basis points at a time,” said Catrambone.

‘Tightrope’

In the U.S., the Fed is on a “tightrope” as it risks over tightening monetary policy, according to IG’s Kinahan. “We haven’t seen the full effect of what the Fed has done,” he said.

While the labor market appears strong for now, the Fed is tightening into a slowing economy. For example, existing home sales have fallen as mortgage rates climb, while the Institute for Supply Management’s manufacturing survey, a barometer of American factories, fell to a 28-month low of 50.9% in September.

Also, trouble in financial markets may show up unexpectedly as a ripple effect of the Fed’s monetary tightening, warned Spouting Rock’s Williams. “Anytime the Fed raises rates this quickly, that’s when the water goes out and you find out who’s got the bathing suit” — or not, he said.

“You just don’t know who is overlevered,” he said, raising concern over the potential for illiquidity blowups. “You only know that when you get that margin call.”

U.S. stocks ended sharply higher Friday, with the S&P 500 SPX, +2.37%,

Dow Jones Industrial Average DJIA, +2.47%

and Nasdaq Composite each scoring their biggest weekly percentage gains since June, according to Dow Jones Market Data.

Still, U.S. equities are in a bear market.

“We’ve been advising our advisors and clients to remain cautious through the rest of this year,” leaning on quality assets while staying focused on the U.S. and considering defensive areas such as healthcare that can help mitigate risk, said Ameriprise’s Saglimbene. “I think volatility is going to be high.”

NEW YORK — Wall Street capped a volatile run for stocks with a broad rally Friday, contributing to sizable weekly gains for major indexes.

The S&P 500 rose 2.4% and notched its biggest weekly gain since June. The Dow Jones Industrial Average rose 2.5% and the Nasdaq composite ended 2.3% higher.

More than 90% of the stocks in the benchmark S&P 500 index rose. Technology stocks, retailers and health care companies powered a big share of the rally. Oracle rose 5%, Home Depot added 2.3% and Pfizer rose 4.8%.

Social media companies fell broadly after Snapchat’s parent company issued a weak forecast and the Washington Post reported that Elon Musk plans to slash about three-quarters of the payroll at Twitter after he buys the company. Snap slumped 28.1% and Twitter shed 4.9%.

Markets have been unsettled in recent days, as stocks lurched from sharp gains early in the week to losses later in the week. The market appeared headed for another sell-off early Friday, then reversed course amid fresh signals from the Federal Reserve that it may consider easing up on its aggressive pace of interest rate hikes as it tries to bring down inflation.

“The hope is that they at least slow down,” Jay Hatfield, CEO of Infrastructure Capital Advisors.

The Fed is expected to raise interest rates another three-quarters of a percentage point at its upcoming meeting in November. Markets have been unsettled partly because investors have been hoping that any sign of inflation easing or economic growth slowing could signal that the Fed will ease up on its rate increases, which have yet to show any signs of significantly impacting inflation.

Mary Daly, president of the Federal Reserve Bank of San Francisco, said Friday that she’s thinking about the dangers of raising interest rates too high and doing too much damage to the economy.

While the Fed likely isn’t yet ready to start dialing down the size of its rate hikes, she said, “I think the time is now to start talking about stepping down. The time is now to start planning for stepping down.”

If the Fed does come out of its meeting next month with a fourth straight increase of 0.75 percentage points to its key overnight interest rate, as most investors expect, she said: “I would really recommend people don’t take that away as: It’s 75 forever.”

A 0.75 point jump is triple the size of the Fed’s usual move, and the Fed risks creating a recession if it moves too high or too quickly.

Daly’s comments helped push down investors’ expectations for how high the Fed will hike rates through the end of the year. Traders are now pricing in just a 45% chance that the Fed will hike rates by 0.75 percentage points next month and again by the same amount in December.

Just a day ago, they were much more confident about that, pricing in a 75% probability. Instead, traders increasingly see the Fed dialing down to a more modest increase of 0.50 percentage points in December, according to CME Group.

Daly was speaking at meeting of the University of California-Berkeley’s Fisher Center for Real Estate & Urban Economics’ Policy Advisory Board.

Central banks around the world have mostly been raising interest rates to fight inflation and much of the focus has been on the Fed. It has raised its key interest rate to a range of 3% to 3.25%. A little more than six months ago, that rate was near zero.

Even if the Fed does dial down the size of its increases soon, officials at the central bank have also been adamant that they plan to leave rates alone at that high level for a while to continue to slow the economy in hopes of forcing down high inflation.

“The concern is still that bond yields are heading higher and the Fed is not signaling a pivot,” said Ross Mayfield, investment strategist at Baird. “Until there is a meaningful pivot driven by a drop in inflation, it’s a huge headwind to the market.”

Treasury yields, which hit multiyear highs this week on expectations of more Fed rate hikes, eased Friday. The yield on the 10-year Treasury note, which affects mortgage rates, slipped to 4.22% from 4.24% late Thursday. The yield on the two-year Treasury, which tends to track investors’ expectations for Federal Reserve action on interest rates, fell to 4.49% from 4.61%.

Stocks got a boost from the pullback in yields. The S&P 500 rose 86.97 points to 3,752.75. The index posted a 4.7% gain for the week.

The Dow climbed 748.97 points to close at 31,082.56, and the Nasdaq added 244.87 points to 10,859.72.

Small company stocks also gained ground. The Russell 2000 index rose 37.85 points, or 2.2%, to finish at 1,742.24.

Investors have shifted their focus, for now, to the latest round of corporate earnings as they look for more clues about how hot inflation and rising interest rates are shaping the economy. Reports from airlines, banks, railroad operators and others have so far provided mixed financial results and forecasts.

American Express fell 1.7% after setting aside hundreds of millions of dollars to cover potential losses as the economy continues to deteriorate. Railroad CSX rose 1.7% after reporting solid financial results.

A version of this story first appeared in CNN Business’ Before the Bell newsletter. Not a subscriber? You can sign up right here. You can listen to an audio version of the newsletter by clicking the same link.

London CNN Business

—

Twelve days from now, the Federal Reserve will meet again, and expectations for the central bank’s next moves are firming up. The consensus among investors: Persistently hot inflation means the Fed will need to continue with its string of aggressive interest rate hikes, which is unprecedented in the modern era.

What’s happening: Markets see a 99% probability that rates will rise by another three-quarters of a percentage point, reaching a range of 3.75% to 4%.

A hike of that magnitude is now “a given,” Quincy Krosby, chief global strategist for LPL Financial, told clients on Wednesday. “Concern is now focused on December, and whether the Fed is prepared to transition to smaller rate hikes.”

That’s up from a 60% probability one month ago. So what changed?

Inflation, mainly. The US Consumer Price Index rose 8.2% in the year to September after rising 8.3% annually in August. While CPI peaked at 9.1% in June, that reading was still uncomfortably elevated and higher than economists had expected.

The 6.6% annual uptick in shelter costs was of particular concern. It takes longer for housing expenses to come back down than some other categories, since renters tend to sign leases for 12-month periods. The monthly rise in core services costs (excluding energy) was the largest gain in three decades.

The data underscored the need for the Federal Reserve to stay tough — while a strong jobs report for September will deliver confidence the central bank can do so without causing undue harm to the US economy.

Fed officials have said as much. In an interview with Reuters on Friday, St. Louis Fed President James Bullard said inflation had become “pernicious,” which means that “frontloading” larger rate hikes is logical.

The market impact: The S&P 500 kicked off the week with a 3.8% rally before dropping 0.7% on Wednesday. It’s still plodding along in a bear market, about 23% below its January peak. So long as the Fed signals its intention to keep the pressure on, boosting the odds of a US recession, volatility is expected to persist.

Even relatively solid corporate earnings may not be sufficient to change the direction.

“So far, the results are decent, but they’re being compared to consensus estimates that have been persistently lowered since early summer,” noted strategists at Charles Schwab.

Tesla

(TSLA) posted a solid quarter of earnings and record revenue, but now says it will likely fall short of its target for a 50% growth in the number of cars it sells this year.

Quick rewind: As recently as July, the company said it was still aiming for a target of 50% growth from the 936,000 cars it delivered in 2021.

But with two quarters of disappointing deliveries caused by supply chain issues and Covid-related shutdowns in China, that goal has looked increasingly out of reach, my CNN Business colleague Chris Isidore reports.

CEO Elon Musk said that the electric carmaker is not struggling with demand.

“We expect to sell every car that we make, for as far in the future as we can see,” he said on a call with analysts on Wednesday.

Instead, the company said it would “just” miss its target due to complications with delivery of cars from its factories to customers at the end of the year.

Shares are down 5% in premarket trading on Thursday. They’ve dropped 37% year-to-date, compared to a 22.5% fall in the S&P 500.

“This quarter was not roses and rainbows,” said Dan Ives, tech analyst for Wedbush Securities. “Competition is increasing. There are some logistical challenges.”

America’s business leaders are becoming more pessimistic. The Conference Board recently reported a slide in its CEO confidence index, which it said had hit levels not seen “since the depths of the Great Recession.”

Of the 136 CEOs who were surveyed, 98% said they were preparing for a US recession over the next 12 to 18 months — and 99% said they were bracing for a recession in Europe.

Notably, the business community is not being quiet about its concerns.

Amazon founder Jeff Bezos tweeted Tuesday that “the probabilities in this economy tell you to batten down the hatches.”

He was responding to a clip of an interview with Goldman Sachs CEO David Solomon, who told CNBC that “it’s a time to be cautious.”

“You have to expect that there’s more volatility on the horizon now,” Solomon said. “That doesn’t mean for sure that we have a really difficult economic scenario. But on the distribution of outcomes, there’s a good chance that we have a recession in the United States.”

American Airlines

(AAL), AT&T

(T), Dow, Nucor

(NUE) and Quest Diagnostics

(DGX) report results before US markets open. CSX

(CSX), Snap

(SNAP) and Whirlpool

(WHR) follow after the close.

Also today:

Initial US jobless claims for last week post at 8:30 a.m. ET.

Existing home sales for September follow at 10 a.m. ET.

Coming tomorrow: Earnings from American Express and Verizon.

This may surprise you: Wall Street analysts expect earnings for the S&P 500 to increase 8% during 2023, despite all the buzz about a possible recession as the Federal Reserve tightens monetary policy to quell inflation.

Ken Laudan, a portfolio manager at Kornitzer Capital Management in Mission, Kan., isn’t buying it. He expects an “earnings recession” for the S&P 500 SPX, +2.78%

— that is, a decline in profits of around 10%. But he also expects that decline to set up a bottom for the stock market.

Laudan’s predictions for the S&P 500 ‘earnings recession’ and bottom

Laudan, who manages the $83 million Buffalo Large Cap Fund BUFEX, -2.86%

and co-manages the $905 million Buffalo Discovery Fund BUFTX, -2.82%,

said during an interview: “It is not unusual to see a 20% hit [to earnings] in a modest recession. Margins have peaked.”

The consensus among analysts polled by FactSet is for weighted aggregate earnings for the S&P 500 to total $238.23 a share in 2023, which would be an 8% increase from the current 2022 EPS estimate of $220.63.

Laudan said his base case for 2023 is for earnings of about $195 to $200 a share and for that decline in earnings (about 9% to 12% from the current consensus estimate for 2022) to be “coupled with an economic recession of some sort.”

He expects the Wall Street estimates to come down, and said that “once Street estimates get to $205 or $210, I think stocks will take off.”

He went further, saying “things get really interesting at 3200 or 3300 on the S&P.” The S&P 500 closed at 3583.07 on Oct. 14, a decline of 24.8% for 2022, excluding dividends.

Laudan said the Buffalo Large Cap Fund was about 7% in cash, as he was keeping some powder dry for stock purchases at lower prices, adding that he has been “fairly defensive” since October 2021 and was continuing to focus on “steady dividend-paying companies with strong balance sheets.”

Leaders for the stock market’s recovery

After the market hits bottom, Laudan expects a recovery for stocks to begin next year, as “valuations will discount and respond more quickly than the earnings will.”

He expects “long-duration technology growth stocks” to lead the rally, because “they got hit first.” When asked if Nvidia Corp. NVDA, +6.14%

and Advanced Micro Devices Inc. AMD, +3.69%

were good examples, in light of the broad decline for semiconductor stocks and because both are held by the Buffalo Large Cap Fund, Laudan said: “They led us down and they will bounce first.”

Laudan said his “largest tech holding” is ASML Holding N.V. ASML, +3.79%,

which provides equipment and systems used to fabricate computer chips.

Among the largest tech-oriented companies, the Buffalo Large Cap fund also holds shares of Apple Inc. AAPL, +3.09%,

Microsoft Corp. MSFT, +3.88%,

Amazon.com Inc. AMZN, +6.63%

and Alphabet Inc. GOOG, +3.91%

Laudan also said he had been “overweight’ in UnitedHealth Group Inc. UNH, +1.77%,

Danaher Corp. DHR, +2.64%

and Linde PLC LIN, +2.25%

recently and had taken advantage of the decline in Adobe Inc.’s ADBE, +2.32%

price following the announcement of its $20 billion acquisition of Figma, by scooping up more shares.

Summarizing the declines

To illustrate what a brutal year it has been for semiconductor stocks, the iShares Semiconductor ETF SOXX, +2.12%,

which tracks the PHLX Semiconductor Index SOX, +2.29%

of 30 U.S.-listed chip makers and related equipment manufacturers, has dropped 44% this year. Then again, SOXX had risen 38% over the past three years and 81% for five years, underlining the importance of long-term thinking for stock investors, even during this terrible bear market for this particular tech space.

Here’s a summary of changes in stock prices (again, excluding dividends) and forward price-to-forward-earnings valuations during 2022 through Oct. 14 for every stock mentioned in this article. The stocks are sorted alphabetically:

You can click on the tickers for more about each company. Click here for Tomi Kilgore’s detailed guide to the wealth of information available free on the MarketWatch quote page.

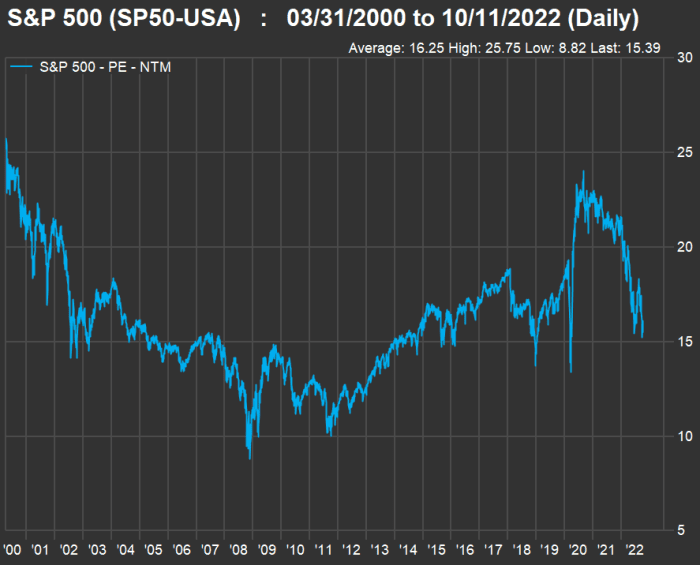

The forward P/E ratio for the S&P 500 declined to 16.9 as of the close on Oct. 14 from 24.5 at the end of 2021, while the forward P/E for SOXX declined to 13.2 from 27.1.

The whipsaw action wasn’t limited to stocks, and was described by Rick Rieder, the chief investment officer for global fixed income at BlackRock, as “one of the craziest days” of his career.

The bond market’s warning

Some investors who focus on stocks might not realize that the bond market is much larger, and that its movements can cause government and central-bank policies to shift. Larry McDonald, founder of The Bear Traps Report and author of “A Colossal Failure of Common Sense,” which described the 2008 failure of Lehman Brothers, explained just how bad the action was in the U.K. bond market over the past few weeks, when 30-year government bonds issued in December traded as low as 24 cents on the dollar. He also predicted what will happen if the Federal Reserve continues on its current course of interest-rate increases.

Michael Brush argues the Federal Reserve is moving too quickly to raise interest rates and cool the U.S. economy. He expects a rapid decline in inflation and a new bull market for stocks. In a column, he shares five sentiment indicators that suggest it is time to buy stocks — especially this group of companies.

Time for a refreshing COLA if you are on Social Security

Getty Images

The Social Security Administration has announced that its cost-of-living adjustment (COLA) for 2023 will be 8.7%, the largest increase in four decades. There is more to the story, including tax implications and changes to Medicare, as Jessica Hall and Alessandra Malito explain.

Freddie Mac said interest rates on 30-year mortgage loans averaged 6.92% on Oct. 13, up from 3.05% a year earlier. Mortgage Daily said rates had hit 7.10% — the highest in 20 years — and economists are warning these levels could be a “new normal.”

A homeowner locked-in with a low interest rate on their mortgage loan will be reluctant to sell. And some would-be buyers may now be priced out of the market because of much higher loan payments. Here’s what economists expect for home prices in 2023.

This is why Florida’s insurance market is such a mess

Florida insurers are not only suffering from storm-damage payouts.

Joe Raedle/Getty Images

Hurricanes are nothing new to Floridians, but insurers in the state are losing money even though premiums have doubled over the past five years. Shahid S. Hamid, the director of the Laboratory for Insurance at Florida International University, explains why the Florida insurance market is so distorted.

Here’s a travel option you may never have heard of — home swapping

Villefranche-sur-mer on the French Riviera.

istock

Home swapping can give you an opportunity to live as a local in a faraway place while spending much less than you would as a tourist. Here’s how it works.

Want more from MarketWatch? Sign up for this and other newsletters, and get the latest news, personal finance and investing advice.

BEIJING — European stocks and Wall Street futures gained Thursday while Asian markets fell ahead of U.S. inflation data that investors worry will reinforce Federal Reserve plans for more aggressive interest rate hikes.

London and Frankfurt advanced. Shanghai, Tokyo and Hong Kong declined. Oil prices advanced.

Wall Street’s benchmark S&P 500 ended lower Wednesday after inflation in producer prices edged down but still was near a multi-decade high.

The more closely watched consumer price index was due out later Thursday.

“A hawkish reaction to the data could add more pressure to stocks,” Anderson Alves of ActivTrades said in a report.

The Fed and other central banks in Europe and Asia have raised rates by unusually big margins to cool inflation that is at multi-decade highs, but traders are afraid they might tip the global economy into recession.

In early trading, the FTSE 100 in London gained 0.2% to 6,840.35. The DAX in Frankfurt rose 0.8% to 12,272.20 and the CAC 40 in Paris added 0.5% to 5,845.55.

On Wall Street, futures for the benchmark S&P 500 index and the Dow Jones Industrial Average were up 0.5%.

On Wednesday, the S&P 500 gave up 0.3% for its sixth daily decline and the Dow slide 0.1% after a report showed producer price inflation is very hot.

Prices rose 8.5% in September, down from March’s peak of 11.7%. But prices gained 0.4% compared with August following two months of declines.

Consumer inflation on Thursday and retail sales data Friday could give a clearer picture of where prices are hottest and how consumers are reacting.

Minutes from the Fed’s last meeting, released Wednesday, underscored the central bank’s commitment to taming “unacceptably high” inflation.

The S&P 500 is down 25% so far this year and close to a two-year low.

In Asia, the Shanghai Composite Index lost 0.1% to 3,016.35 and the Nikkei 225 in Tokyo sank 0.6% to 26,237.42. Hong Kong’s Hang Seng tumbled 1.9% to 16,389.11, its lowest close in more than 11 years.

The Kospi in Seoul fell 1.8% to 2,162.87 while Sydney’s S&P-ASX 200 gained less than 0.1% to 6,642.60.

India’s Sensex lost 0.7% to 57,205.89. New Zealand’s benchmark lost 0.5% and Southeast Asian markets also declined.

In energy markets, benchmark U.S. crude gained 19 cents to $87.64 per barrel in electronic trading on the New York Mercantile Exchange. Brent crude, the price basis for international oil trading, added 31 cents to $92.67 per barrel in London.

The dollar strengthened to 146.74 after hitting a 24-year high of 145.85 on Wednesday.

The dollar’s exchange rate has been rising against other currencies due to the Fed’s rate hikes and recession fears. The yen’s weakness has prompted expectations Japan’s central bank might intervene for a second time to prop up the exchange rate following an intervention in September.

As Britain’s central bank boss, tasked with managing inflation and setting interest rates, Andrew Bailey likes targets. Now he is one.

Markets are dumping U.K. assets amid chaotic policymaking from Liz Truss’ new government — but Bailey’s rocky stewardship of the Bank of England is getting a growing share of the blame. His harshest critics include some of Truss’ most senior Conservative Party colleagues.

At stake are home loans for 2 million households coming due for renewal amid cripplingly high interest rates in the next two years and the viability of pension funds managing more than £1 trillion worth of assets. Failure to quell a “fire sale” of U.K. bonds and currency risks a financial meltdown that could spread far beyond British shores.

The current bond market pressure began after U.K. Chancellor Kwasi Kwarteng announced a vast package of unfunded tax cuts, stoking investors’ fears about the long-term sustainability of the government’s debt.

The dramatic selloff of government bonds sparked a panic at U.K. pension funds, which couldn’t handle the price falls, and has huge knock-on impacts for mortgage rates and borrowing costs.

The political fallout has so far landed on Truss’ government’s shoulders — prompting U-turns on key policies as opinion polls showed cratering support.

Yet before the U.K.’s self-inflicted turmoil, Bailey was feeling political pressure over the central bank’s handling of double-digit inflation and the rising cost of living that comes with it.

While No. 10 refuses to be drawn on the Bank’s decisions, Business Secretary Jacob Rees-Mogg suggested a failure to raise interest rates quickly was at the root of the turmoil in financial markets.

He dismissed it as “commentary” to draw a direct link between the government’s mini-budget and concerns over the U.K.’s financial stability that led to emergency intervention from the Bank, adding that pension funds’ “high-risk” activities had played a role.

“It could just as easily be the fact that the day before, the Bank of England did not raise interest rates by as much as the Federal Reserve did,” he told the BBC’s Today program.

In another apparent swipe at the Bank, Rees-Mogg added: “The pound and other currencies have been falling against the dollar because interest rates in the U.S. have been rising faster than they have in other markets.”

In the immediate aftermath of Kwarteng’s disastrous mini-budget, the Bank seemed to be in command of the situation when it stepped in to calm the pension fund crisis and refused to be pushed into an early interest rate rise by markets. But two further interventions this week and confusion over stark comments from Bailey himself risk undermining that impression.

The governor on Tuesday issued a rare ultimatum to beleaguered pension funds struggling to meet cash calls in the government bond market. “You’ve got three days left now. You’ve got to get this done,” he warned at an event in Washington.

The bank has effectively bailed out pension funds since the U.K. government’s mini-budget roiled the markets. The bond-buying intervention is intended to offer temporary relief and give the affected funds time to raise enough cash to handle historic surges in yields.

Bailey’s message appeared to be aimed at upping the pressure on funds to sell assets in time rather than expecting an extension beyond Friday’s deadline. “We will be out by the end of this week,” he said.

Yet the remarks seemed to backfire instantly, sparking a sharp fall in the pound, although it has since recovered.

U.K. government borrowing costs also increased again on Wednesday, with the yield on 30-year gilts moving above 5 percent — the level that first sparked the bank’s intervention — before dropping back after the Bank used its firepower to buy £4.4 billion of gilts.

Financial market experts think the governor’s comments were a mistake that will force the bank into following the government’s recent U-turns.

Mike Howell of CrossBorder Capital described Bailey’s words as the “shortest suicide note in history,” and said the governor will have to change course.

“Andrew Bailey’s insistence that emergency support will end on Friday is an unsustainable position that we expect to be reversed quickly,” said Oxford Economics chief economist Innes McFee.

If the Bank loses credibility, its ability to rescue the economy from market disruption will be severely hampered. Increasingly costly interventions will yield ever more limited results if investors lose faith in the U.K.’s most important financial institution.

Before Bailey’s comments on Tuesday, one markets strategist said the Bank could “test the water” by stopping the program on Friday and then restarting if necessary — but that would be risky because it’s unclear how much yields would have to rise before triggering the same problems at pension funds.

“While a very able central banker, he has spent most of his career outside the BoE’s monetary policy and markets areas,” said EFG Bank chief economist Stefan Gerlach, previously a central banker himself.

“He is not the best fit for the job, given the nature of the problems the Bank is facing now. His communications missteps over the last year were damaging,” he said, pointing to Bailey’s confusing guidance on interest rates. “It’s like the fire brigade saying ‘you have to have your fire before Friday because then we are heading home.’”

This article is part of POLITICO Pro

The one-stop-shop solution for policy professionals fusing the depth of POLITICO journalism with the power of technology

Calling inflation “unacceptably high,” Federal Reserve leaders saw their strategy of fighting price pressures aggressively as less risky to the economy than doing too little, minutes of the bank’s last meeting show.

The Fed approved another jumbo-size increase in U.S. interest rates at its Sept. 21-22 meeting. It also signaled plans for another pair of big increases before year-end in a surprise to Wall Street DJIA, -0.10%.

The minutes of the Fed’s meeting underscore that top officials were disappointed and worried about persistently high inflation.

“A sizable portion of the economic activity has yet to display much response,” the Fed minutes said. “Inflation had not yet responded appreciably to a policy tightening.”

While some senior Fed officials also worried the bank could go too far and damage the economy, the majority appeared to believe it was vital for the central bank to squelch inflation, even if that meant keeping rates high for a prolonged period.

“Many participants emphasized that the cost of taking too little action to bring down inflation likely outweighed the cost of taking too much action,” the minutes said.

The Fed predicts the economy will eventually slow as rates rise, but it noted the labor market remains extremely tight.

Fed officials also expressed concern that oil prices could rise again, supply chains would not heal as quickly as expected and that rising wages could exacerbate inflation.

“Inflation was declining more slowly than [Fed officials] had been anticipating,” the minutes said.

The internal Fed debate has also playing out publicly since the last meeting.

Some senior officials such as Atlanta Federal Reserve President Raphael Bostic hope the bank will make enough progress in its fight against inflation to “pause” rate hikes at the end of this year.

Fed critics contend the bank is going to go too far and could plunge the economy into a second recession in four years. A pause would allow the Fed to see how much its prior rate hikes have succeeded in lowering the rate of inflation, they say.

Failing to do so, they contend, would make it even harder to get prices back under control if Americans come to view high inflation as the norm. That would do even more damage to the economy in the long run.

Jennifer Lee, senior economist at BMO Capital Market, downplayed the debate and said the Fed in unified on its next few steps.

“The Federal Reserve is pretty much in sync and is not going to be easing anytime soon,” she said.

Since March the Fed has lifted a key short-term interest rate from near zero to an upper end of 3.25%. And the central bank has telegraphed plans to raise the so-called fed funds rate to as high as 4.75% by next year.

Rising U.S. interest rates has done little so far to douse inflation.

The rate of inflation, using the Fed’s preferred PCE price index, rose at a yearly rate of 6.2% as of August. That’s a long way off from the Fed’s forecast for inflation to fall to 2.8% in 2023 and 2.3% by 2024.

The higher cost of borrowing has only chilled a few parts of the economy, most notably housing.

The rate on a 30-year mortgage has surged above 7% to a 16-year high from less than 3% one year ago. The result has been a slowdown in home buying and construction and softer sales of home furnishings.

Most consumer and business loans are influenced by the fed funds rate.

Jerome Powell and other members of the Federal Reserve are obsessed with choking off inflation once and for all, even if the Fed’s series of aggressive rate hikes slow the economy to a crawl. That could be bad news for consumers, investors and Corporate America.

What’s more, many market experts and economists note that the rate of inflation, while still uncomfortably high, is falling and should continue to decline – but there is a noted lag effect. Fed vice chair Lael Brainard admitted as much in a speech Monday, saying that “policy actions to date will have their full effect on activity in coming quarters.”

Still, the Fed isn’t done raising rates. Investors are pricing in the strong probability of a fourth consecutive three-quarters of a percentage point hike at the Fed’s next meeting on November 2. And the chances of a fifth straight hike of that magnitude at the Fed’s December 14 meeting are also on the rise.

It seems that Powell wants to atone for his mistake of repeatedly calling inflation “transitory” for much of last year. So the Fed is going to keep raising rates to prove that it is taking inflation seriously, even if that leads to a bigger pullback in stocks…and tipping the economy into a recession.

Needless to say, that’s a problem. Especially since the Fed has two mandates: price stability and maximum employment. That means the jobs market might get hit due to the Fed’s laser-like focus on inflation.

“My concern is that the Fed is tightening so quickly and so significantly without knowing what it means for the economy,” said Brian Levitt, global market strategist with Invesco.

Keep in mind that the Fed’s series of rate hikes are unprecedented in the “modern” era of central banking, i.e. after Alan Greenspan became Fed chair in 1987 and the Fed became far more transparent.

The Fed was far more opaque before Greenspan, and the market didn’t pick apart every speech, policy move and economic forecast the way Wall Street does now. Inflation in the 1970s and early 1980s was also a much different animal, due largely to an oil price shock that lasted years because of a supply shortage.

The current inflation crisis stems from more temporary (we won’t say transitory) supply chain issues tied to the pandemic as well as the rapid reopening of the global economy following a brief recession.

“We’re more cautious because the Fed is tightening into a weakening economy,” said Keith Lerner, co-chief investment officer and chief market strategist with Truist Advisory Services. “These supersized hikes are the most aggressive in decades. But the Fed has scar tissue from inflation.”

Unless pricing pressures pick up again, it appears the year-over-year increase for the consumer price index (CPI) peaked at 9% in June. That’s a big move from about 2.3% in February 2020 just before the pandemic shutdown. But 9% is still a far cry from the CPI high during the Volcker years of 14.6% in early 1980.

And with consumer and wholesale prices already edging lower, some experts worry that the continued uber-hawkish stance by the Fed will do more harm than good for the economy.

“The speed at which the Fed is increasing rates will certainly have some unintended consequences,” said Michael Weisz, president of Yieldstreet, an investment firm that specializes in so-called alternative assets such as real estate, private equity, venture capital and art.

Weisz said the surge in interest rates could lead to a “consumer credit crunch being more pronounced,” in which loans beyond mortgages might become more expensive and harder to get.

Rate hikes raise the costs for companies to pay down their debt, increasing the possibility of corporate bankruptcies and defaults on commercial loans. It may even potentially lead to stagflation…the double whopper of stagnant growth and continued inflation. In other words, prices may remain high and the job market will probably be worse.

“The Fed runs a real risk of over-tightening, as the impacts of the restrictive policy may not flow through inflation and unemployment data until it’s too late,” Weisz added.

As long as inflation remains the bigger issue for the economy, the Fed is going to focus more on getting prices under control. After all, the unemployment rate is at 3.5%, a half-century low.

“The Fed has made it clear their number one priority right now is price stability,” said Dustin Thackeray, chief investment officer of Crewe Advisors. “Until the Fed sees sustained evidence their monetary policy is having a material impact on…the job market, they will maintain their persistent efforts in reining in inflationary pressures.”

U.S. stock indexes edged higher on Wednesday, while hotter-than-expected producer price inflation data deepened concerns that the Federal Reserve may continue its aggressive interest rate hikes.

How are stock-index futures trading

The Dow Jones Industrial Average DJIA, +0.50%

was up 120 points, or 0.4% to around 29,355

The S&P 500 SPX, +0.35%

gained 5.3 points, or 0.2% to about 3,594

The Nasdaq Composite COMP, -6.31%

traded 5.1 points, or 0.1% higher to 10,430

On Tuesday, the Dow Jones Industrial Average rose 36 points, or 0.12%, to 29239, the S&P 500 declined 24 points, or 0.65%, to 3589, and the Nasdaq Composite dropped 116 points, or 1.1%, to 10426. The S&P 500 closed down 1,177 points, or 24.7% for the year to date.

What’s driving markets

The 12-month rate of producer price inflation slowed to to 8.5% from 8.7% while the annual core rate, excluding food and energy, was unchanged at 5.6%, but the monthly rate rose 0.4% in September, above forecast, and the monthly core PPI was also up 0.4% in September.

Such data has worsened fears that to curb inflation, the Fed will continue its aggressive rate hikes, which may steer the U.S. economy into a recession.

“We believe the odds of a recession in 2023 are now better than 50%,” Greg Bassuk, chief executive at AXS Investments, wrote in a Wednesday note. “Last week’s market turbulence saw volatility at levels we have not seen since July, and we believe investors should brace for ongoing market volatility and uncertainty throughout Q4, in concert with another likely Fed interest rate hike to the tune of 0.75% in November,” according to Bassuk.

The 10-year Treasury yield BX:TMUBMUSD10Y, which started the year around 1.65% was trading at 3.931% on Wednesday, off 1.3 basis points, after the producer price inflation data.

Traders are also awaiting U.S. September consumer prices data on Thursday due at 8:30 am Eastern Time.

“Inflation has proven to be difficult to forecast and given the negative ‘shock’ from the August CPI, it would be difficult for any investor to have conviction going into this report,” according to Tom Lee, head of research at Fundstrat.

“For us, analyzing the month over month numbers is much more important than looking at the headline,” Zachary Hill, head of portfolio management at Horizon Investments, said in an interview.

“The way we’ve been thinking about it, the last three months annualized [inflation] gives you a kind of a decent idea of where the shorter term trends are around inflation,” Hill said. “We think that’s what the Fed is going to be looking at to see progress towards their 2% goal. And unfortunately, based on various measures, we’re nowhere near that today.”

Investors have become increasingly concerned of late that severe stresses in the financial system may emerge as central banks switch from the era of zero or negative interest rates to sharply higher borrowing costs as they try to tackle inflation at multi-decade highs.

“[G]lobal financial conditions have tightened as central banks continue to raise interest rates. Our latest Global Financial Stability Report shows that financial stability risks have increased since our last report, with the balance of risks tilted to the downside,” said the International Monetary Fund in a report released on Tuesday.

“The mood of global investors was gloomy enough and hardly needed yesterday’s reminder from the IMF that the risks to financial stability have increased,” Ian Williams, strategist at Peel Hunt, noted. “Its report highlighted specifically (if obviously) the threats from persistent inflation, China’s slowdown and the war in Ukraine. The highlighted ‘disorderly repricing of risk’ is arguably already underway.”

The Fed may offer its view on the topic as a number of officials are due to give comments on Wednesday. Minneapolis Fed President Neel Kashkari said the Fed is “dead serious” about getting inflation down. Fed vice chair Michael Barr will speak at 1:45 p.m. The minutes of the Fed’s previous monetary policy setting meeting will be released at 2 p.m. ET and Fed governor Michelle Bowman will deliver comments at 6.30 pm.

PHG, -11.33%

plunged 12% after the Dutch tech company issued its second profit warning this year, forewarning that supply chain problems will impact sales and third-quarter profits.

Intel Corp. INTC, +1.50%

may fire thousands of workers by the end of the month, around the same time the chip manufacturer reports quarterly results amid a tough year for semiconductor makers, Bloomberg reported late Tuesday. The company’s shares rose 1% Wednesday.

Shares of PepsiCo Inc. climbed 4.6% Wednesday, after the beverage and snack giant reported third-quarter profit and revenue that rose above expectations and raised its full-year outlook, as higher prices helped offset some volume weakness.

South Korea’s central bank went for a second outsized rate increase in three months in response to the aggressive U.S. monetary policy tightening and high inflation at home.

The Bank of Korea raised its benchmark seven-day repurchase rate by 50 basis points to 3.00% on Wednesday. The bank’s latest move followed its quarter-percentage-point rate rise in August after its first-ever half-percentage-point increase in July.

Twenty-two of 25 analysts surveyed by The Wall Street Journal had expected the bank to resume the outsized rate increase, citing its pressing need to respond to the Fed’s faster-than-expected pace of rate increases and still high inflation at home.

Korean policy makers have been concerned about the won’s steep decline against the greenback, as the Fed lifted federal funds rates by 75 bps at each of its past three meetings and could make another big such rate increase in November. The weaker won could risk a flight of foreign capital from the country.

South Korea’s headline inflation softened for a second consecutive month to 5.6% in September but remained well above the BOK’s 2% annual target.

BOK officials expect inflation to remain above 5% in the near term.

NEW YORK — Stocks shook off an early stumble and rose broadly on Wall Street in afternoon trading Tuesday as investors wait for updates on inflation and corporate earnings this week.

The S&P 500 rose 0.4% as of 1:44 p.m. Eastern, on pace to snap a four-day losing streak. The benchmark index fell as a much as 1.2% earlier after a dour forecast from the International Monetary Fund stoked recession fears.

The Dow Jones Industrial Average rose 348 points, or 1.2%, to 29,551 and the Nasdaq was 0.1% higher.

Health care companies and retailers made some of the strongest gains. Johnson & Johnson rose 2% and Walmart rose 3.2%.

Technology stocks remained the weakest area of the market. Chipmakers continued slipping in the wake of the U.S. government’s decision to tighten export controls on semiconductors and chip manufacturing equipment to China. Qualcomm fell 3.3%.

Markets in Europe and Asia slipped.

Uber fell 8.2% and Lyft slumped 9.8% following a proposal by the U.S. government that could give contract workers at ride-hailing and other gig economy companies full status as employees.

U.S. crude oil prices fell 1.9%.

Bond yields were mixed. The yield on the 10-year Treasury, which influences mortgage rates, edged higher to 3.89% from 3.88% late Friday. The yield on the 2-year Treasury, which follows Federal Reserve action, held steady at 4.30%. Bond markets were closed on Monday for a holiday.

Recession fears have been weighing heavily on markets as stubbornly hot inflation burns businesses and consumers. U.S. stocks are coming off of four straight losses. Economic growth has been slowing as consumers temper spending and the central banks globally raise interest rates.

Wall Street is closely watching the Fed as it continues to aggressively raise its benchmark interest rate to make borrowing more expensive and slow economic growth. The goal is to cool inflation, but the strategy carries the risk of slowing the economy too much and pushing it into a recession.

The International Monetary Fund on Tuesday cut its forecast for global economic growth in 2023 to 2.7%, down from the 2.9% it had estimated in July. The cut comes as Europe faces a particularly high risk of a recession with energy costs soaring amid Russia’s invasion of Ukraine.

Investors have a busy week ahead of economic and corporate earnings reports that could provide a clearer picture of inflation’s impact, while also raising questions about whether the Fed should continue with its aggressive rate hikes.

Investors still expect the Fed to raise its overnight rate by three-quarters of a percentage point next month. It would be the fourth such increase, which is triple the usual amount, and bring the rate up to a range of 3.75% to 4%. It started the year at virtually zero.

The Fed will release minutes from its last meeting on Wednesday, possibly giving Wall Street more insight into its views on inflation and next steps. The government will also release its report on wholesale prices, which will help provide more details on how inflation is hitting businesses.

The closely watched report on consumer prices will be released on Thursday and a report on retail sales is due Friday.

The latest round of corporate earnings will ramp up this week with reports from PepsiCo, Delta Air Lines and Domino’s Pizza. Banks, including Citigroup and JPMorgan Chase, will also report results.

Don’t assume the worst is over, says investor Larry McDonald.

There’s talk of a policy pivot by the Federal Reserve as interest rates rise quickly and stocks keep falling. Both may continue.

McDonald, founder of The Bear Traps Report and author of “A Colossal Failure of Common Sense,” which described the 2008 failure of Lehman Brothers, expects more turmoil in the bond market, in part, because “there is $50 trillion more in world debt today than there was in 2018.” And that will hurt equities.