The four allege in a lawsuit filed in the Ontario Superior Court of Justice on Monday that the investment manager for the Canada Pension Plan is breaching its duty to invest in their best interest, and subjecting their contributions to undue risk of loss by its approach. “I do not want to be suing my pension manager, but I want to retire on a stable pension into a livable future,” said 20-year-old Aliya Hirji, one of the four plaintiffs, at a news conference in Toronto.

CPP faces lawsuit on fossil fuel ties

The lawsuit, filed with the support of Ecojustice and Goldblatt Partners LLP, claims CPP Investments is drastically underestimating the financial implications of climate change, as well as worsening its harms by continuing to invest in the expansion of fossil fuel production.

Karine Peloffy, a lawyer and sustainable finance lead at Ecojustice, said the lawsuit will be a legal test on how the fund should approach climate risks, given its obligations. “It is the first time in any court anywhere that future beneficiaries will argue that one of the largest investors is breaching its duty of intergenerational equity,” Peloffy said.

CPP Investments spokesman Michel Leduc said the fund will address the matter through the courts, if necessary, but that it has a rigorous approach to integrating climate risk as one of many material factors it considers. “Our focus remains steadfast on integrating climate-related considerations into our investment activity,” he said.

CPP drops net-zero target but defends approach

The lawsuit comes after CPP Investments quietly dropped its 2050 net-zero target for carbon emissions earlier this year, but Leduc said the change in language didn’t change the fund’s focus on climate change. He said climate risks are one of many risk areas the fund has to manage as it invests to maximize long-term investment returns without undue risk.

Leduc said the fund will push back against efforts that it sees as limiting its ability to meet those obligations. “An action against CPP Investments, and our efforts to maintain the sustainability of the Canada Pension Plan, is an action against the retirement security of 22 million Canadians,” Leduc said.

Travis Olson, another one of the plaintiffs, said Monday that he doesn’t believe it is meeting those obligations when managing investments the fund will one day rely on to help pay his benefits in retirement.

“My pension manager’s practices are incompatible with an economically stable, climate-safe future that my generation is relying on,” the 22-year-old Olson said. “I’m looking forward to the day our pension manager stops betting against the world my generation will inherit, and until they do so voluntarily, we’re asking the courts to step in and protect our contributions.”

Article Continues Below Advertisement

Get free MoneySense financial tips, news & advice in your inbox.

The Canadian Press is Canada’s trusted news source and leader in providing real-time stories. We give Canadians an authentic, unbiased source, driven by truth, accuracy and timeliness.

The first can be regarded by retirees and those on the cusp of retirement as a must read: William Bengen’s A Richer Retirement, the long-awaited update of his classic book on the much-cited 4% Rule: Conserving Client Portfolios During Retirement. First published in 2006, that book was really aimed at financial advisors but became popular with the general investing public after it got extensive press exposure over the years.

The 4% Rule—which is actually closer to a 4.7% Rule depending how you interpret it—refers to the “safe” percentage of a portfolio that retirees can withdraw each year without running out of money in 30 years, net of inflation. Bengen’s term for this is “SAFEMAX.”

The new book is supposedly aimed at average investors. Still, I found it pretty technical, filled chock-a-block with charts and tables that are probably more accessible to the original audience of financial professionals. Counting some useful appendices, the book is just under 250 pages.

After wading through all Bengen’s tweaks meant to minimize the impact of inflation, bear markets, and unexpected longevity, I was left with the impression the original 4% Rule remains a pretty good initial guestimate for what retirees can safely withdraw in any given year.

Sure, 3.5% or 3% may be technically “safer,” especially if you expect to live a very long life or want to leave an estate for your heirs. I’ve even seen arguments that a 2% retirement rule may be appropriate for extremely risk-averse retirees.

On the other hand, it’s not too dangerous to withdraw 6% or 7% or more as long as stock markets and interest rates cooperate. That’s what many retirees intuitively do anyway; they reduce withdrawals in bear markets, and splurge a bit in raging bull markets.

It’s also worth noting that whether you choose 3%, 5%, or larger percentages, that guideline really just applies to your investment portfolios, whether held in tax-deferred or tax-exempt accounts or taxable ones. Most Canadian retirees can also count on the Canada Pension Plan (CPP) and Old Age Security (OAS), not to mention employer pensions. Those lacking big defined-benefit pensions but who have plenty saved in RRSPs and TFSAs can choose to pensionize or partially pensionize their nest eggs by buying annuities. (For timing, see this piece published recently on my blog.) For that concept, refer to Professor Moshe Milevsky’s excellent book, Pensionize Your Nest Egg.

Making money in any market

More controversial is Jim Cramer’s How to Make Money in Any Market. I know it’s fashionable for some mainstream financial journalists to disparage the long-time host of Mad Money and in-house stock-picking guru on Squawk on the Street. I never watch him on TV (MSNBC) but often listen to his podcasts while walking or at the gym, usually at 1.5x speed and skipping over interviews with the CEOs of more speculative stocks I have no interest in. Cramer’s critics tend to be diehard indexers who swear it’s impossible to consistently pick stocks and “beat” the market over the long run. I tend to side with them, but more on that below.

Article Continues Below Advertisement

Obviously, Cramer begs to differ, often trotting out testimonials from Nvidia millionaires who bought that spectacular artificial intelligence (AI) chip stock the moment he named his dog after it (sadly now deceased). Cramer devotes an entire chapter to that call, which he mentions every chance he gets. I did buy that stock too, although I was too late and risk-averse to bet the farm enough to change my life with it.

What his critics may not realize is that even Cramer believes in indexing at least 50% of a portfolio. In fact, he tells newcomers to stocks that their first $10,000 (US) should go in an S&P500 index fund. Hard to argue with that.

Where I part ways is his book’s recommendation of holding just five stocks for the 50% of a portfolio that is not indexed. That would mean holding around 10% of your total portfolio in each such stock, which is way more concentrated than most investors would countenance. Much of the book goes into how to choose the kind of secular growth stocks he prefers, with the help of modern AI tools like ChatGPT, Grok, and all the rest.

I used to wonder about his show’s regular segment, Am I diversified?, where readers submit their five picks for Cramer’s consideration. I’d be surprized if there is an investor anywhere whose portfolio is that concentrated. Even Cramer’s much-cited Charitable Trust holds many more than five stocks.

Canada’s best dividend stocks

How not to invest

This leads me to the third book I ordered from Amazon, recently reviewed by Michael J. Wiener of the Michael James on Money blog: Barry Ritholtz’s book How Not to Invest. Cramer cynics might quip that would have been a better title for How to make money in any market had it not already been taken by Ritholtz; Cramer has after all famously inspired some ETF companies to provide “reverse Cramer” funds that short his major long recommendations.

Ritholtz’s book clocks in at almost 500 pages but is quite readable. It has attracted multiple testimonials ranging from William Bernstein (“Destined to become a classic.”) to DFA’s David Booth, Shark Tank’s Mark Cuban and author Morgan Housel, known through The Motley Fool, and who penned the foreword.

Ritholtz organizes his book in four parts: Bad Ideas, Bad Numbers, Bad Behavior, and Good Advice. While Cramer tempts us into individual stock-picking, Ritholtz reminds us that few can do it well; nor can most of us successfully pull off market timing. He devotes a fair bit of space to how badly some pundits’ predictions have panned out in the past. I was left with a renewed appreciation for the benefits of indexing, certainly for the core of portfolios if not for their entirety. As he puts it: “Index (mostly). Own a broad set of low-cost equity indices for the best long-term results.” He lists five advantages to indexing: lower costs and taxes, you own all the winners, better long-term performance, simplicity and less bad behaviour.

Fortunately, ordinary investors have many advantages over the pros, such as not having to benchmark against indices or worry about investors who sell a fund, the ability to keep costs low, and in theory a much longer time horizon. But the clincher is that “indexing gives you a better chance to be ‘less stupid.’”

Prerna Mathews, vice-president of ETF product strategy at Mackenzie Investments, said covered call ETFs typically invest in dividend-paying equities and further enhance income by writing call options on those holdings. A call option provides the right to purchase a security at a set price. She said covered call ETFs essentially earn option premiums in exchange for “giving up” some of the stock’s future gains beyond the set option price.

She noted covered call ETFs have flourished in the market recently, fuelled by investor enthusiasm for their higher yields. Mathews said these products can be attractive to those who prioritize income over growth and help manage market volatility.

“There’s definitely a trade-off; there’s no free lunch. The higher yield off the options premiums is coming off of the fact that you are giving up long-term return in the stock,” Mathews said. “Those options premiums, you’re getting paid out on them today, but that total return impact is usually much more significant than the yield that you’re actually generating off of them.”

Mathews said there is more onus on investors to do due diligence and not get “distracted by a flashy yield number and marketing material.”

Covered call ETFs offer income—but at a cost

Fred Masters, president of Masters Money Management Inc., said the best way to view these products is to think of them as “enhanced income products” that use options strategies to boost their yields. He said retail investors shouldn’t base their portfolios around these products, pointing to higher fees and lower overall returns. Though he said they can work as a smaller part of a larger portfolio.

Masters highlighted that management fees for these products can be “up to ten times higher” than a typical ETF in the same category.

“You can’t control outcomes in many cases when investing in equity markets, but you can control costs and keeping costs to a minimum year after year is a crucial tenet of long-term investing success,” he said. “We know these covered call ETFs are expensive and that eats into returns annually.”

Covered call ETFs can shine when markets stall but lag in rallies

Covered call ETFs can perform better under certain market conditions though, according to Nick Hearne, a financial adviser and portfolio manager at RGF Integrated Wealth Management. In a range-bound market, where stocks are moderately increasing, and in declining markets, he said covered call ETFs will often outperform traditional strategies due to the income investors receive.

Article Continues Below Advertisement

“Where they’re going to underperform is when the market increases significantly over a period of time … what they’re really doing is when they sell those call options, they’re selling their upside. That’s the downside,” Hearne said. “And over the long term, (covered call ETF investors) have less exposure to the market because they are selling part of their exposure, and so the expectation would be that a long-only or traditional strategy would outperform a covered call strategy.”

Mathews said covered call ETFs can be suited to investors prioritizing income, including people in retirement who can’t handle as much volatility in their portfolio. “Fixed income will only get you so far. In 1995, you could generate a 6% yield off of just Treasuries and investment-grade (bonds). And today, getting to that same 6% yield is so much more challenging,” she said.

However, investors choosing this path are taking on a higher level of risk through covered call exposure compared with fixed income, Mathews noted.

Despite any trade-offs, covered call ETFs have been gaining momentum in the market. Mathews said there are 17 providers that offer covered call products in Canada, with over $35 billion allocated to covered call ETFs as of September. “We continue to see very strong flows even year-to-date into these products and, unsurprisingly, with an aging demographic in Canada, we’re seeing that trend persist,” she said.

Get free MoneySense financial tips, news & advice in your inbox.

The Canadian Press is Canada’s trusted news source and leader in providing real-time stories. We give Canadians an authentic, unbiased source, driven by truth, accuracy and timeliness.

Under the transaction, Northern Superior’s shareholders will receive 0.0991 of an Iamgold share and 19 cents in cash for each common share of Northern Superior. The offer implies a total value of $2.05 per Northern Superior share, based on the closing price of the Iamgold shares on the Toronto Stock Exchange on Oct. 17. The transaction will also include a concurrent distribution to Northern Superior’s shareholders of all the shares in ONGold Resources Ltd. currently held by Northern Superior.

Under a second deal, Iamgold will acquire Mines D’Or Orbec Inc. in a stock-and-cash deal valued at $17.2 million, net of the 6.7 per cent stake it already holds in the company. Orbec shareholders will receive 6.25 cents and 0.003466 of an Iamgold share for each Orbec share they hold for a value of 12.5 cents per share.

Teck Resources ‘very pleased’ with progress of talks with regulators on Anglo deal

Teck Resources (TSX:TECK.B)

Numbers for its third quarter of 2025.

Profit: $281 million (up from loss of $748 million a year ago)

Revenue: $3.39 billion (up from $2.86 billion in same quarter last year)

The head of Teck Resources (TSX:TECK.B) says he’s happy with the way talks with government officials are going as the company seeks Ottawa’s approval for its proposed merger with U.K. mining giant Anglo American—even as the industry minister signalled last month she wanted more from the companies.

“Conversations are ongoing, and they’re productive and we’re very pleased in the way that they’re unfolding at the moment,” chief executive Jonathan Price told a conference call to discuss the company’s latest results Wednesday.

Teck announced a deal last month to merge with Anglo American to form the Anglo Teck group; however, the deal requires approval under the Investment Canada Act, which can be used to block deals deemed against the national interest.

“We are engaging on an ongoing and collaborative basis with the Canadian government here,” Price said.

“Those discussions have been frequent and productive.” He said he believes the company has put forward a strong and comprehensive package of commitments to Canada, a key element of which is the plan to move the headquarters of Anglo to Vancouver.

The companies have said the combination would create a $70-billion copper mining powerhouse with headquarters and top executives based in Vancouver. They have pitched it as a “merger of equals” even though Anglo American is worth more than double Teck. Shareholders vote on the deal in December, while Price said the company will be completing all of its filings related to antitrust and competition with regulators globally.

Article Continues Below Advertisement

Industry Minister Mélanie Joly has said Ottawa wants to see longer-term commitments to Canada if Teck is allowed to merge with Anglo American. Teck and Anglo American have committed about $4.5 billion in spending in Canada over five years as part of the deal. However, a significant portion of that has already been announced by Teck, including the mine life extension of its Highland Valley copper mine.

Price’s comments came as the company reported a profit from continuing operations attributable to shareholders amounted to $281 million or 57 cents per diluted share for its third quarter. The result compared with a loss of $748 million or $1.45 per diluted share in the same quarter last year. On an adjusted basis, Teck says it earned 76 cents per diluted share from continuing operations in its latest quarter, up from an adjusted profit of 60 cents per diluted share a year earlier. Revenue totalled $3.39 billion, up from $2.86 billion in the same quarter last year.

In reporting its third-quarter results, Teck said production at Quebrada Blanca in Chile continues to be constrained by the pace of development of a tailings management facility, requiring downtime in the concentrator.

Mullen Group Q3 profit down from year ago as acquisitions boost revenue

Mullen Group Ltd. (TSX:MTL)

Numbers for its third quarter of 2025.

Profit: $33.2 million (down from $38.3 million a year ago)

Revenue: $561.8 million (up from $532 million in same quarter last year)

Mullen Group Ltd. (TSX:MTL) reported its third-quarter profit fell compared with a year ago as acquisitions helped boost its revenue.

The trucking and logistics company says it earned $33.2 million or 36 cents per diluted share for the quarter ended Sept. 30. The result compared with a profit of $38.3 million or 41 cents per diluted share a year earlier.

Revenue for the quarter totalled $561.8 million, up from $532.0 million in the same quarter last year. The increase was helped by the acquisition of Cole International Inc. and Pacific Northwest Moving (Yukon) Ltd.

On an adjusted basis, Mullen Group says it earned 38 cents per share in its latest quarter, down from an adjusted profit of 41 cents per share a year earlier.

Wealthsimple says assets top $100 billion under administration

Wealthsimple Inc. says its assets under administration have reached $100 billion as the company tweaks its offerings. The privately-held financial platform has seen its assets roughly double from a year ago, while in 2023 it had set a target of 2028 to reach the $100 billion mark.

Images of people lining up at gold dealers around the world have become common again, and Canada is no exception. As early as September 2023, Global News reported a “gold rush” at Costco, where one-ounce gold bars were selling out within hours of being listed online.

But before giving in to the fear of missing out, it may be worth considering some alternatives to physical gold. Investment case aside, there are several practical reasons why owning bullion directly may not be the best approach for many investors.

The case against bullion

This isn’t an argument against owning gold directly. I have a few Gold Maple Leaf coins myself and there’s something almost primal about holding them. The weight, the shine—it taps into an ancient fascination with the metal that no security can replicate.

But objectively, buying and storing physical bullion has never been the most seamless or efficient way to gain gold exposure.

The first issue is the bid-ask spread. When you buy from a dealer, you’re not transacting at the spot price you see quoted online. Dealers make their money on the spread between what they sell at and what they’ll buy back for. As of October 17, for example, Vancouver Bullion & Currency Exchange (VBCE) listed one-ounce Gold Maple Leaf coins as follows:

VBCE Buy: $5,893 CAD

VBCE Sell: $6,068 CAD

That’s a spread of $175, or about 3%. In other words, gold prices have to rise by at least that much just for you to break even.

Then there’s the matter of security. I keep mine in a heavy-duty, bolted-down, fireproof safe that wasn’t cheap. Hiding it under a mattress or burying it in the backyard isn’t advisable.

If you decide to store it at the bank, you’ll pay annual fees for a safety deposit box and, more importantly, reintroduce counterparty risk. The whole point of owning gold is to remove intermediaries, but as soon as it’s sitting in a bank vault, it’s no longer fully in your control.

Article Continues Below Advertisement

If your top priority is to physically hold your wealth, to have it in your possession, then by all means, buy bullion. There’s nothing wrong with that. Just know it’s not as easy as clicking “buy” on a screen. You have to find a reputable dealer, pay a premium, arrange secure storage, and handle logistics that digital gold holders never have to think about. And since gold produces no income, every expense—from dealer spreads to storage—comes directly out of your total return.

If your main reason for owning gold is to diversify a portfolio or participate in its price rally—rather than to establish self-custodied reserves as a last-ditch store of value—it’s worth considering other vehicles. Exchange-traded funds (ETFs), closed-end funds (CEFs), and gold mining equities can all provide exposure without the friction, cost, and security headaches of physical bullion.

Gold ETFs

Gold exchange-traded funds (ETFs) are open-ended funds that correspond directly to custodied, audited reserves of gold. They benefit from the same in-kind creation and redemption structure used by all ETFs, meaning authorized participants can exchange shares for physical gold (and vice versa).

This arbitrage mechanism helps keep the ETF’s market price closely aligned with its net asset value (NAV), reducing the risk of persistent premiums or discounts.

There are plenty of choices from Canadian issuers. The main things to focus on are low management expense ratios (MERs) and tight bid-ask spreads, since both affect total return over time. A good example is the BMO Gold Bullion ETF (ZGLD),which carries a competitive 0.23% MER and holds unencumbered, 400-ounce gold bars in a local BMO vault that’s regularly audited.

For investors looking for a low-cost, liquid way to track gold’s spot price, ETFs like this tend to be the most straightforward and accessible route.

Gold CEFs

Before ETFs dominated the market, closed-end funds were the go-to security for gold exposure. Unlike ETFs, they don’t create or redeem shares on demand.

A CEF is issued with a fixed number of shares at its IPO, and afterward, trading takes place only among investors in the open market. Because of that, supply and demand can cause the market price to deviate from NAV, leading to either a discount or premium.

The Cenovus offer values MEG at $8.6 billion, including assumed debt, and is made up of half cash and half stock. MEG shareholders are set to vote on the proposal on Oct. 22.

Cenovus and MEG have neighbouring oilsands properties at Christina Lake, south of Fort McMurray, Alta.

U.S. fuel distributor Sunoco LP’s proposed takeover of Calgary-based fuel retailer and refiner Parkland Corp. (TSX:PKI) has cleared a key regulatory milestone with Ottawa’s approval under the Investment Canada Act. The transaction is expected to close in the fourth quarter of this year, subject to remaining regulatory approvals and the satisfaction or waiver of customary closing conditions, Parkland said in a release Tuesday. A review under the Investment Canada Act considers whether foreign investments would be a net benefit to the country or cause potential harm to national security.

The Parkland-Sunoco deal was announced at a time of fraught Canada-U.S. relations and amped-up resource nationalism amid the onslaught of U.S. President Donald Trump’s tariffs. Earlier this year, Ottawa recently updated national security guidelines under the act to account for potential harms to Canada’s economic security. The government said it will consider the size of the Canadian business, its place in the innovation ecosystem and the impact on Canadian supply chains.

Parkland and Sunoco announced the friendly cash-and-stock deal valued at US$9.1 billion including assumed debt in May following a bitter proxy battle with investors in the Canadian company unhappy with its performance and strategy.

Parkland owns the Ultramar, Chevron and Pioneer gas station chains as well as several other brands in 26 countries. Sunoco outlets that had long operated in Canada were rebranded in 2009 under the Petro-Canada banner. Parkland also runs a refinery in Burnaby, B.C., which supplies nearly one-third of the region’s domestically supplied gasoline and jet fuel.

The deal cleared a key U.S. antitrust hurdle last month when the waiting period under the Hart-Scott-Rodino Act expired. Shareholders approved the takeover in June.

Cineplex selling Cineplex Digital Media to U.S. company Creative Realities for $70M

Cineplex Inc. (TSX:CGX) has signed a deal to sell its Cineplex Digital Media subsidiary to Creative Realities Inc., a U.S.-based digital signage company, for $70 million. CDM offers digital signage for a wide range businesses including retailers and banks as well as digital menu boards for restaurants.

Article Continues Below Advertisement

As part of the deal, Cineplex has signed a long-term agreement to continue as CDM’s exclusive advertising sales agent for CDM operated digital-out-of-home networks across Canada.

Cineplex chief executive Ellis Jacob says the sale will provide the company with meaningful capital to continue to deliver value for shareholders. Cineplex says proceeds of the sale will be used to strengthen its balance sheet and provide cash for share buybacks, debt reduction, and general corporate purposes.

The deal is expected to close in the coming weeks, subject to regulatory approvals and other customary closing conditions.

The Canadian Press is Canada’s trusted news source and leader in providing real-time stories. We give Canadians an authentic, unbiased source, driven by truth, accuracy and timeliness.

Cineplex says box office revenue for the third quarter totalled $159.5 million, down from $174.9 million a year earlier.

Cineplex chief executive Ellis Jacob says outside a tough comparative last August, with the release of Deadpool & Wolverine, the third-quarter box office performed well compared with a year ago. He added that the success of Taylor Swift, The Official Release Party of A Showgirl last weekend marked a dynamic start to the fourth quarter.

Cineplex has 171 movie theatres and entertainment venues across Canada.

Aritzia’s Q2 profit surge driven by U.S. customer growth, operational changes: CEO

Artizia Inc. (TSX:ATZ)

Numbers for its second quarter of 2025:

Profit: $66.3 million (up from $18.2 million a year ago)

Sales: $812.1 million (up from $615.7 million)

Aritzia Inc. said strength in its U.S. business and moves to avoid higher shipping fees boosted its latest quarterly results. “We’ve seen outstanding new customer growth in the United States, where our base of loyal clients expands quarter after quarter. We’re also super pleased with our second-quarter results in Canada,” Aritzia CEO Jennifer Wong told analysts on a call Thursday.

The Vancouver-based clothing retailer reported $66.3 million in net income during its second quarter, up from $18.2 million during the same period last year. Its net revenue rose by almost a third to $812.1 million, from $615.7 million during the same period a year earlier.

The company said its U.S. net revenue rose more than 40 per cent to $486.1 million, accounting for just under 60 per cent of its total revenue. Wong also noted the company launched a new international e-commerce platform in August, which she said was fuelling higher revenue growth. “Its performance in the first six weeks has meaningfully exceeded our expectations, and we’re confident we’ll hit our target to triple sales within two years or less,” she said.

In August, the U.S. ended what’s known as the de minimis exemption, which had allowed packages worth $800 or less to ship south of the border without duties. “Previously, under the de minimis exemption, we utilized our existing supply chain network in Canada to fulfil a portion of U.S. e-commerce orders. However, the removal of the de-minimis exemption in August required an operational pivot,” Wong said.

She said the company relocated all U.S. order fulfilment to its Ohio distribution centre, which was expanded last year to more than double its previous size. Wong said the company hired additional staff at the facility.

Article Continues Below Advertisement

“Despite headwinds from the elimination of the de minimis and higher reciprocal tariff rates on Vietnam and Cambodia, our proactive mitigation strategies and strong revenue growth have positioned us very well,” she said. “As a result, our margin outlook for fiscal 2026 is unchanged at 15.5 to 16.5 per cent. We’re leveraging our agile global supply chain to minimize tariff exposure where possible.”

Todd Ingledew, Aritzia’s chief financial officer, said that due to the retailer’s year-to-date performance and improved expectations for the second half of the year, it is raising its net revenue forecast for the full fiscal year to between $3.3 billion and $3.5 billion. In its first-quarter report in January, Aritizia had predicted net revenue of $3.1 billion to $3.25 billion.

For the second quarter, Aritzia’s net income per diluted share came in at 56 cents compared to 16 cents per diluted share a year earlier. On an adjusted basis, Aritzia’s net income amounted to $69.8 million, rising from $24.5 million during the second quarter of last year.

U.S. government to take 10-per-cent stake in Canadian mining company Trilogy Metals

Vancouver-based Trilogy Metals Inc. (TSX:TMQ) says the U.S. government will take a 10% stake in the mineral exploration company, which has mining interests in Alaska that Washington wants to see developed. The U.S. government is spending US$35.6 million on the stake, and has options to increase it further in the future. The transaction remains subject to regulatory and other approvals.

The announcement comes as U.S. President Donald Trump signed an executive order that directs a road to be built in Alaska allowing access to the Ambler mining district, an area rich in copper where Trilogy Metals has an interest through a joint venture. The long-debated Ambler Road project was approved in the first Trump administration, but was later blocked by the Biden administration after an analysis determined the project would threaten caribou and other wildlife and harm Indigenous peoples that rely on hunting and fishing.

“This proposed partnership with the U.S. Government represents a significant milestone for Trilogy Metals and for the development of a secure, domestic supply of critical minerals for America in Alaska,” Trilogy Metals CEO Tony Giardini said in a news release. The partnership interest underscores the strategic importance of Trilogy’s Upper Kobuk Mineral Projects in supporting U.S. energy, technology, and national security priorities, he said.

U.S. Secretary of the Interior Doug Burgum said the investment will help secure critical mineral supplies.

“They’re (Trilogy Metals) one of the companies that has mining claims in this area that is a remote wilderness right now, and again making that investment so we can make sure that we’re securing these critical mineral supplies and that ownership in that company will benefit the American people,” he said.

TRACK THE TROPICS WITH FIRST WARNING. METEOROLOGIST ERIC BURROUGHS. WE HAVE BEEN SO FORTUNATE SO FAR THIS HURRICANE SEASON. KNOCK ON WOOD, THAT PERSISTS. I MEAN, ALL OF THE HURRICANES HAVE STAYED AWAY FROM THE UNITED STATES. WE STILL HAVE ABOUT A MONTH AND A HALF TO GO FOR HURRICANE SEASON. SO LET’S MONITOR AND SEE HOW THIS PLAYS OUT. THE GOOD NEWS DOES NOT LOOK LIKE JERRY WILL BE A LANDFALL FOR US. IT’S UNDERGOING SOME SIGNIFICANT WIND SHEAR, BUT AS THE HURRICANE HUNTERS HAVE BEEN INVESTIGATING, THEY HAVE FOUND IT GRADUALLY INTENSIFYING. WINDS ARE NOW AT 65 MILES AN HOUR. SO JERRY CONTINUES TO DEVELOP. WE THINK IT BECOMES A CATEGORY ONE HURRICANE AS IT LIFTS TO THE NORTH AND EVENTUALLY MAKES A HARD RIGHT TURN. IT GETS CLOSE ENOUGH TO THE LEEWARD ISLANDS AND WINDWARD ISLANDS, THOUGH, THAT THEY DO HAVE TROPICAL STORM WATCHES POSTED, SO IT IS EXPECTED TO STAY NORTH OF THEM. BUT SOME OF THOSE SQUALLY CONDITIONS MAY MOVE IN. SO IF YOU’VE GOT FRIENDS OR FAMILY THAT LIVE OUT THERE, JUST KEEP THAT IN MIND. ELSEWHERE, WE ARE WATCHING. THIS IS EXTRATROPICAL. INVEST 96. JUST SOMETHING INTERESTING TO LOOK AT. HAS A LOW END 10% CHANCE OF

The National Hurricane Center is monitoring Tropical Storm Jerry. Bookmark this page for the latest maps and spaghetti models for Jerry. Hurricane season 2025The Atlantic hurricane season runs from June 1 through Nov. 30. Stay with WESH 2 online and on-air for the most accurate Central Florida weather forecast.>> More: 2025 Hurricane Survival GuideThe First Warning Weather team includes First Warning Chief Meteorologist Tony Mainolfi, Eric Burris, Marquise Meda and Cam Tran.>> 2025 hurricane season | WESH long-range forecast>> Download Very Local | Stream Central Florida news and weather from WESH 2

The National Hurricane Center is monitoring Tropical Storm Jerry.

Bookmark this page for the latest maps and spaghetti models for Jerry.

Hurricane season 2025

The Atlantic hurricane season runs from June 1 through Nov. 30. Stay with WESH 2 online and on-air for the most accurate Central Florida weather forecast.

Maple Leaf Foods is keeping a 16 per cent stake in Canada Packers and the two companies have entered into an evergreen supply agreement. It will also be an anchor customer for Canada Packers which will supply pork for its prepared meats business.

Michael McCain, executive chair at both companies, says Maple Leaf Foods and Canada Packers are moving forward as independent entities, each with a clear investment profile and experienced teams. He says the McCain family and McCain Capital Inc. are fully committed to the future of both companies.

TMX Group acquires U.S.-based data and analytics provider Verity

TMX Group (TSX:X) says it has acquired Verity, an investment research management system, data, and analytics provider. Financial terms of the agreement were not immediately available.

Verity has two core products. VerityRMS is a research management system, while VerityData offers enhanced data sets and insights primarily focused on public equity filings.

TMX Datalinx president Michelle Tran says the addition of Verity strengthens the company’s ability to serve a growing global client base.

TMX Group is the operator of the Toronto Stock Exchange and other markets.

MEG Energy says Glass Lewis recommends shareholders back Cenovus offer

MEG Energy Corp. (TSX:MEG) says a second major independent proxy advisory firm has recommended its shareholders back a takeover offer for the company by Cenovus Energy Inc. (TSX:CVE). The company says Glass, Lewis & Co. has issued a report recommending shareholders vote for the cash-and-stock offer by Cenovus over a rival all-stock offer by Strathcona Resources Ltd.

The report comes after proxy advisory firm Institutional Shareholder Services Inc. said last week that MEG shareholders should support the Cenovus bid.

Article Continues Below Advertisement

The Cenovus offer must be approved by a two-thirds majority vote by MEG shareholders, expected to be held on Oct. 9. Strathcona (TSX:SCR) has said it intends to vote its 14.2 per cent interest in MEG against the deal.

Cenovus and MEG have side-by-side oilsands properties at Christina Lake, south of Fort McMurray, Alta., while Strathcona also has operations in the region.

Stella-Jones signs deal to buy Brooks Manufacturing for US$140 million

Utility pole company Stella-Jones Inc. (TSX:SJ) has signed a deal to buy U.S.-based Brooks Manufacturing Co. for US$140 million.

Brooks is a maker of treated wood distribution crossarms and transmission framing components. It was founded in 1915 and operates a facility in Bellingham, Wash.

Stella-Jones chief executive Eric Vachon called the acquisition a natural fit. “The addition of Brooks bolsters Stella-Jones’ suite of solutions, enhancing its ability to meet the growing demand of utilities and unlock new growth opportunities,” Vachon said in a statement Tuesday. “The acquisition reflects our strategic focus and aligns with our vision to make Stella-Jones a partner of choice to our infrastructure customers.”

Brooks’ sales for 2024 totalled about US$84 million.

RBC Capital Markets analyst James McGarragle called the deal a “strategically positive move.” “It creates a valuable growth platform for Stella-Jones by diversifying its product offering and leveraging Brooks’ established brand and customer relationships,” McGarragle wrote in a note to clients. “Furthermore, the acquisition aligns with Stella-Jones’ long-term strategic objectives to expand beyond traditional product categories and accelerate growth in the infrastructure segment, positioning the company to capitalize on ongoing investments in utility modernization.”

The deal is subject to closing conditions, including U.S. regulatory approval, and is expected to occur by the end of the year. The deal for Brooks follows the acquisition by Stella-Jones of Locweld Inc., a designer and manufacturer of lattice transmission towers and steel poles, earlier this year.

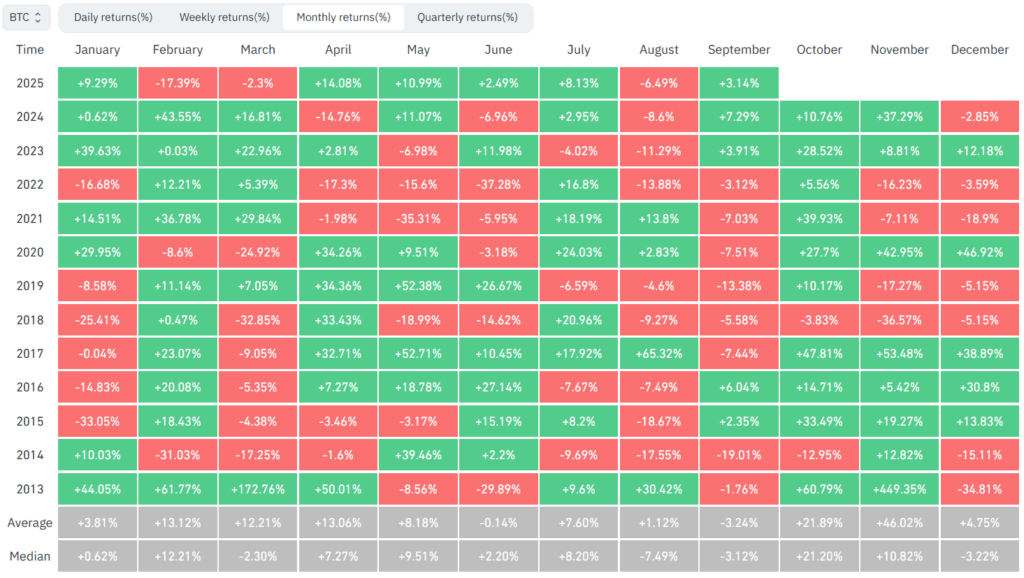

August and September haven’t been great months for crypto investors, but that’s not necessarily a bad thing because markets need a healthy breather every now and then. Bitcoin (BTC), the largest cryptocurrency based on market capitalization, was down about 6.5% in August, and so far in September has regained only about 3.14% of that drop.

A quick look at the BTC price chart below shows that the price of BTC has hovered around the $110,000 mark (all figures in US dollars unless otherwise specified)—plus or minus 10% since May 2025. This is a consolidation, which indicates that for the time being, neither the bulls nor the bears are obvious winners.

Source: Google Finance as of Sept. 25, 2025

August and September are typically down months for BTC

Although months of flat trading can be frustrating for investors, it’s not unheard of and there’s historical precedent for August and September typically being bad for BTC.

Of the thirteen instances since 2013—because that’s when we have reliable public data on BTC price movements from—August has been red nine times (including 2025) and September has been red eight times until 2024. On average, BTC’s August return over the years has been 1.12% and September’s has been -3.24%. On average, BTC’s best months have been October (up 21.89%) and November (up 46.02%).

The following table lays out BTC’s monthly return through the years. See the bottom two rows for average (and median) returns in each calendar month.

Nobody can predict the market accurately based on such historical data, so what can crypto investors learn from this? If you’re bullish on BTC, ethereum (ETH), and other cryptocurrencies, it usually pays to remain invested—especially through October and November—despite the historical bearishness of August and September.

Article Continues Below Advertisement

The best crypto platforms and apps

We’ve ranked the best crypto exchanges in Canada.

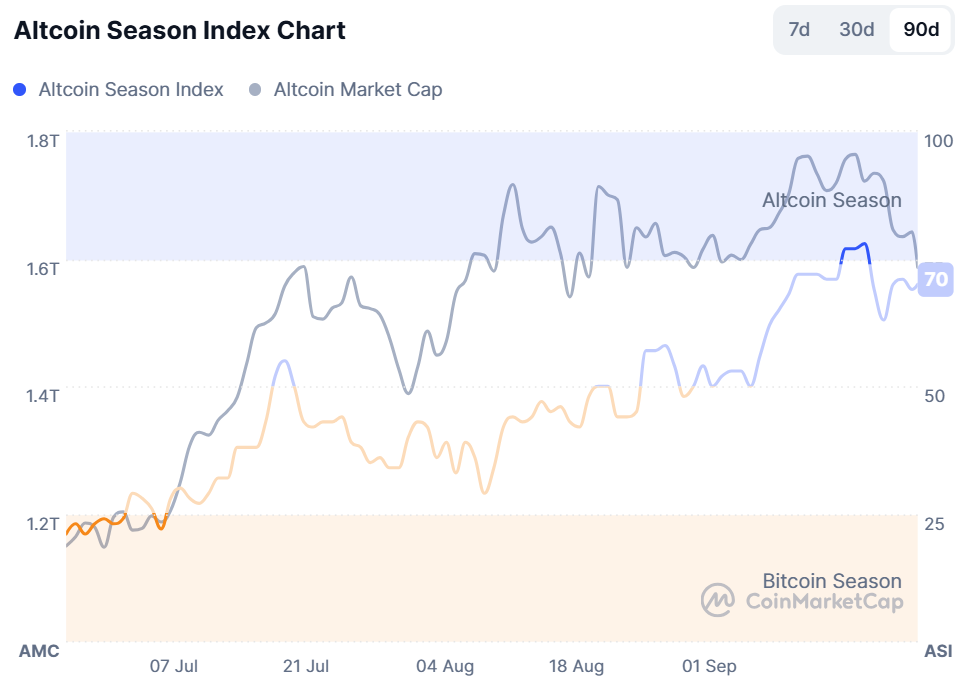

Is altcoin season over?

Altcoin season refers to the phase of the crypto market in which alternative coins (those other than BTC) outperform BTC itself in price appreciation. Typically, altcoin season appears at the end of a bull market cycle—the phase we’re probably in right now. I’ve written about altcoin season in an earlier edition of this column a few months ago, when I flagged the possibility of ETH and other cryptocurrencies outperforming BTC in the second half of 2025.

As the chart below shows, we’re in altcoin season based on the CMC Altcoin Season Index. This index tracks the performance of altcoins relative to BTC over 90 days and assigns a score of 0 to 100, with a score over 70 indicating the outperformance of altcoins relative to BTC.

The race for altcoin ETFs in the US is on. While altcoin ETFs are already available to Canadian investors, we’re about to see a rush of new altcoin ETFs being launched in the US in the coming months.

Recently, on Sept. 25, 2025, the Hashdex Nasdaq Crypto Index ETF announced that they’ll expand their crypto ETF holdings to include XRP, SOL, and Stellar (XLM). The inclusion of these altcoins will create the first truly multi-crypto ETF in the US. This is a sign of things to come.

While 2024 was the year for BTC ETFs, 2025 is the year for ETH and other altcoin ETFs. We could see a slew of altcoin ETFs being launched in the US as a result of the streamlining of listing rules by the US Securities and Exchange Commission (SEC). As reported by Reuters, these streamlined SEC listing rules (applicable to crypto ETFs), would reduce the approximate listing time from about 240 days to just 70 days.

Canadian investors searching for a multi-crypto ETF with exposure to BTC and altcoins can consider these two ETFs—both of which trade on the Toronto Stock Exchange (TSX).

ETF name

Ticker symbol

Exchange

Currency options

Portfolio

Net assets

MER

Evolve Cryptocurrencies ETF

ETC

Toronto Stock Exchange (TSX)

CAD and USD

BTC (74.1%)ETH (14.6%)XRP (7%)SOL (4.2%)

$84.31 million (CAD)

MERs of underlying funds applicable*

CI Galaxy Multi-Crypto Navigator ETF

CMCX

Toronto Stock Exchange (TSX)

CAD and USD

ETH (35.6%)SOL (23.5%)BTC (10.5)Cash and equivalents (30.3%)

$5.54 million (CAD)

1.04%

*ETC has four underlying ETFs as its holdings. While ETC itself has a 0.0% management fee (MER), the underlying ETFs held by ETC will incur management fees and other costs. As of September 2025, three of the four underlying ETFs have a MER of 0.75%, while the fourth has a MER of 0.0% until Dec 31, 2025, post which its MER will be 1%.

Source: Data for each ETF was gathered from the ETFs’ respective websites as of Sept. 25, 2025

Crypto price swings are common

Cryptocurrencies including BTC, ETH, XRP, SOL, XLM, and others are speculative and remain highly volatile assets subject to significant price swings. Even stablecoins, which are seemingly “safe,” may be risky if not adequately backed by real-world assets.

Of course, those with guaranteed-for-life, taxpayer-backed, defined benefit pension plans may well be in an enviable position. I often wonder why the usual media financial profiles of senior couples even bother when their subjects both enjoy such pensions.

Sadly, most of us are not in such a fortunate position. We may have cobbled together a couple of small private-sector pensions over the years, but for the most part what wealth we have is in RRSPs/RRIFs, TFSAs and non-registered savings, which rise and fall with financial markets. From what I see at the new Retirement Club (which I wrote about in this space this past summer) most of those in the so-called retirement risk zone realize they are in effect their own pension managers, which means paying close attention to the markets.

Retirement Club co-founder Dale Roberts posted a typically anxious commentary on a recent The Globe and Mail column by Dr. Norman Rothery, CFA. Rothery, a celebrated value-stock picker who runs the StingyInvestor.com site, suggested the current environment of Trump-inspired tariffs and global trade wars is causing plenty of anxiety for this group. In the link, summarized as “With today’s market, investors close to retirement face precarious times,” Rothery said investors on the cusp of retirement are “facing peril from a combination of the unusually lofty U.S. stock market and political uncertainty that’s disrupting world trade.”

U.S. stocks trading at worrying levels

The U.S. stock market is “trading at worrying levels,” based on several value factors, Rothery said: the S&P 500 Index is “trading at a cyclically adjusted price-to-earnings ratio near 39—above its peak of 33 in 1929 and approaching its top of 44 in late 1999, based on monthly data. Similarly the index’s price-to-sales ratio is approaching its 1999 high. A broader composite measure that includes many different market factors indicates that the U.S. market’s valuation is at record levels.”

Rothery concluded it’s “likely that the U.S. stock market will generate unusually poor average real returns over the next decade or so.”Unfortunately,the U.S. now represents about 65% of the world’s stock market by market capitalization based on its weight in the MSCI All-Country World Index at the end of August. So if the U.S. market flops, “It’ll likely take the rest of the world with it— at least temporarily,” Rothery cautioned.

This could affect recent retirees just beginning to draw down portfolios, due to “sequence-of-returns risk.” That means those in the retirement risk zone who suffer early losses could eventually be in danger of outliving their savings. Rothery also references the famous 4% rule of financial planner and author William Bengen: the theory that investors in a 55/40/5 stocks/bonds/cash portfolio should be able to sustain retirement savings for 30 years provided the annual “SafeMax” withdrawal not exceed 4% a year after adjusting for inflation. Bengen has just released a new book titled A Richer Retirement: Supercharging the 4% Rule to Spend More and Enjoy More, which this column may review next month.

Can defensive funds reduce the risk?

At the Retirement Club, members anxiously posed questions in the site’s chat room about whether they should be moving to cash and bonds, gold, or other alternatives to U.S. stocks. To this, Roberts—who also runs his own Cutthecrapinvesting blog—warned against getting too defensive but agreed that a move to a 70% fixed income/30% stocks allocation might work for some nervous early retirees. Personally, he has trimmed back his U.S. growth stock exposure and added to defensive exchange-traded fund (ETF) sectors like consumer staples, health care, and utilities. He also mentioned a U.S. equity ETF trading in Canadian dollars: iShares Core MSCI US Quality Dividend ETF (XDU.T)

Advisor and certified financial planner John De Goey, of Toronto-based Designed Wealth Management, took a similarly cautious stance in his recent (Sept 12) speech at the MoneyShow in Toronto, archived here on YouTube. Titled “Bullshift and Misguided beliefs,” the talk expanded on De Goey’s usual themes of advisor bullishness and complacent investors, also articulated in his 2023 book, Bullshift. De Goey suggests many advisors believe their own bullish messages, often to the detriment of the performance of their own investment portfolios.

Article Continues Below Advertisement

In the talk, De Goey said the U.S. economy is getting dangerous for investors. “A whole series of economic indicators are flashing red… Despite that a lot of Canadian investors are piling into the U.S. market.” U.S. stocks now account for more two thirds of the global stock market and many Canadians are overweight U.S. stocks, De Goey said, referencing the same elevated CAPE ratio that Rothery cited.

But the “real pain of the tariffs that was expected in April is now just around the corner, as stockpiled inventories get used up.” Trump’s 2025 tariffs are a case of “déjà vu all over again,” De Goey said, comparing them to the protectionist Smoot-Hawley tariffs of 1930, which ushered in the Great Depression. The U.S. now has its most corrupt administration in history, he said, so “expect chaos.” But investors are being “gaslit” by the financial industry. “There’s clear evidence mutual fund registrants are prone to herding/collective stupidity… and it seems the industry is the culprit because who else could it be?” In short, he believes optimism is good for business in the financial industry.

Peter Grandich, a veteran U.S. investor and author, is also bearish about U.S. stocks. His 2011 autobiography was titled Confessions of a Former Wall Street Whiz Kid. Having experienced three major financial panics in his 41-year career (1987, 2000 and 2008), he recently told clients he believes “we’re on the threshold of economical, social, and political crisis, which I believe can make those other three look like a walk in the park in comparison.” His personal asset allocation consists of only cash, T-bills, and three speculative junior resource stocks. “I certainly am not suggesting others consider such a portfolio, but I do believe capital preservation must overwhelm capital appreciation positions. Because corporate bond yields are now so close to Treasury bond yields, I don’t wish to own any. I suspect such a view is rarer than finding a needle in a haystack, but I never have been more adamant in needing to personally be a live chicken versus a dead duck.” (In September, Grandich interviewed me on his podcast.)

But first, a global “melt-up”?

Not everyone is so bearish. One newsletter I subscribe to argues markets will continue to “melt up” in multiple asset classes: stocks, crypto, gold and silver. And while they may well correct in 2026 or so, market strategist Graham Summers argued late in September that “The great global melt-up is accelerating now” so “investors need to take advantage of this while it lasts.”

Dale Roberts and Retirement Club members believe new and would-be retirees can find shelter in traditional asset allocation, taking partial profits in overvalued U.S. stocks and moving to more reasonably priced international and Canadian equities. Asked whether the popular global asset allocation ETFs can protect retirees against overvalued U.S. stocks, De Goey said such products may soften the blow “but right now the U.S. represents almost two-thirds of global stock market capitalization. So, if all your stocks were in a single global ETF or mutual fund with a cap-weighted mandate, you’d have massive exposure to a massively overvalued market.”

Using annuities and other defensive investments

Investors can instead focus on defensive sector ETFs that overweight niches like consumer staples, utilities and health care. Low-volatility ETFs from providers like BMO ETFs, iShares and Harvest ETFs tend to overweight such defensive sectors and underweight overvalued stocks like the technology giants. However De Goey downplays how well low-volatility ETFs work in bear markets. “If the market falls by 25% and the investor can handle that, they may not need such an ETF. “Low-volatility products are more defensive than market-cap weighted products, but it all depends on how investors react and behave when things go south.”

Asked whether RRSP/RRIF investors can buy protection from market volatility through annuitization or partial annuitization, De Goey said maybe, but he prefers products like the Purpose Longevity Fund, a mutual fund “which offers pension-style diversification and aims to replicate annuity payments for the remainder of the unitholder’s life.”

On protecting against Trump’s trade wars, De Goey agreed retirees should have exposure to the gold and precious metals sectors. His clients are 10% in gold and 8% in resources stocks through products such as Mackenzie Core Resources ETF (TSX:MORE), up 33% this year.

On an adjusted basis, BlackBerry says it earned four cents US per share for the quarter compared with zero cents US per share a year earlier.

Revenue for the company’s latest quarter totalled US$129.6 million, up from US$126.2 million a year earlier. The increase came as its QNX segment revenue rose to US$63.1 million, up from US$54.7 million a year ago, while secure communications revenue fell to US$59.9 million compared with US$66.5 million. Licensing revenue amounted to US$6.6 million, up from $5.0 million a year earlier.

In its outlook for its full year, BlackBerry says it now expects full year revenue of US$519 million to US$541 million, up from earlier guidance for US$508 million to US$538 million.

The company also raised its guidance for its adjusted earnings per share for its full year to between 11 cents US and 15 cents US, up from earlier expectations for between eight cents US and 10 cents US.

Air Canada lowers full-year guidance as hit from strike estimated at $375M

Air Canada (TSX:AC)

Adjusted guidance for the year:

Previous: $3.2 billion to $3.6 billion

Adjusted: $2.9 billion to $3.1 billion

Source Google

Air Canada has lowered its guidance for the year after taking a hit from the flight attendant strike that took place earlier this summer. The Montreal-based airline said in a press release that it estimates the cost of the labour disruption was $375 million on operating income and adjusted earnings before interest, taxes, depreciation and amortization.

Air Canada said that it now expects to make between $2.9 billion and $3.1 billion in adjusted EBITDA for the full year. This is in comparison to the airline’s previous 2025 guidance that it suspended in August, which had projected adjusted EBITDA between $3.2 billion and $3.6 billion.

For the third quarter, Air Canada said it expects operating capacity to decline by around 2% from the same period last year, due to the cancellation of more than 3,200 flights. It also expects operating income between $250 million and $300 million during the quarter.

Article Continues Below Advertisement

The airline said three factors combined for the $375 million financial impact of the strike. The first is an estimated $430 revenue hit from refunds, customer compensation and lower travel bookings. It also had about $90 million in incremental costs associated with reimbursements for customers and some labour operating costs. However, the company also saved $145 million, primarily due to lower fuel costs, which reduced the loss.

The Air Canada flight attendant strike lasted three days and ended on Aug. 19, though it took longer to ramp up to full operations.

Earlier this month, Air Canada flight attendants massively rejected the employer’s wage offer, with the airline saying the wage portion will now be referred to mediation as previously agreed to by both sides.

The tentative deal that was voted down raised wages for workers and established a pay structure for time worked when aircraft are on the ground.

The Canadian Press is Canada’s trusted news source and leader in providing real-time stories. We give Canadians an authentic, unbiased source, driven by truth, accuracy and timeliness.

The fashion retailer, which operates under the Garage and Dynamite banners, says its profit amounted to 56 cents per diluted share for the quarter ended Aug. 2, up from 38 cents per diluted share in the same quarter last year. On an adjusted basis, Groupe Dynamite says it earned 57 cents per diluted share, up from an adjusted profit of 40 cents per diluted share a year earlier.

Revenue for the 13-week period totalled $326.4 million, up from $239.1 million a year ago, while its comparable store sales rose 28.6%.

In its outlook, Groupe Dynamite says it now expects comparable store sales growth between 17.0% and 19.0% for its full year, up from earlier expectations for between 7.5 and 9.0%. It also raised its expectations for its adjusted earnings before interest, taxes, depreciation and amortization margin to between 32.0% and 33.5%, up from earlier guidance for between 30.3% and 32.3%.

Roots Corp. offered some buzzy marketing campaigns and brand collaborations over the summer in hopes of driving traffic to the retailer but still wound up reporting a loss during the period.

The Toronto-based apparel maker said Wednesday its second-quarter net loss narrowed to $4.4 million compared with a $5.2-million loss a year earlier. The result for the period ended Aug. 2 amounted to a loss of 11 cents per share for the quarter compared with a loss of 13 cents per share a year prior. Meanwhile, second-quarter sales reached $50.8 million, up from $47.7 million.

Roots CEO Meghan Roach told financial analysts on a conference call Wednesday that it is typical for the company to generate about 30% of its sales in the first half of the year, often leaving it with a loss as it heads into the fall and winter.

However, the second-quarter results this year came in spite of tense trade relations between Canada and the U.S., which have made shoppers more cautious. “Despite the dynamic global operating environment, Roots continues to build positive momentum as we head into the second half of the year,” Roots chief financial officer Leon Wu said on the same call as Roach.

Article Continues Below Advertisement

Much of that momentum has come from direct-to-consumer sales, which include corporate retail store and e-commerce sales. In the second quarter, direct-to-consumer sales totalled $41 million, up 12.7% from the year before. Direct-to-consumer comparable sales growth was 17.8%.

Wu saw the increase as a reflection of customers responding well to the company’s spring and summer collections as well as its recent marketing campaigns. The campaigns helped Roots increase engagement and made the brand feel more accessible, Roach said. Included in the campaigns were instances where Roots transformed a parking lot into nature-inspired spaces for golf and tennis.

The company also hosted a pop-up in Toronto to promote a summer capsule collection with ginger ale maker Canada Dry. The collection included hoodies and graphic tees featuring Canada Dry’s logo and vintage advertisements.

“Together, these collaborations amplified brand heat, reinforced our heritage positioning, and extended our reach for authentic Canadian cultural moments,” Roach said. “We will continue to use selective partnerships and experiences to build that brand perception and support full-price sell through into fall.”

Transat A.T. Inc. reported a net income of $399.8 million in its latest quarter compared with a loss of $39.9 million in the same quarter last year, as its revenue rose 4.1%.

The parent company of Air Transat says the profit amounted to $9.97 per share for the quarter ended July 31, compared with a loss of $1.03 per share a year earlier.

On an adjusted basis, Transat says it had a loss of 28 cents per share in its latest quarter, compared with an adjusted loss of 93 cents per share in the same quarter last year.

There’s a certain stigma that can come with a prenuptial or cohabitation agreement, which outlines the fate of a couple’s assets if their marriage or common-law relationship were to end. Some might argue it signals a lack of trust or endurance of the relationship. But the conversation doesn’t have to turn sour, experts say.

Most professionals will recommend a prenup for couples with a wealth disparity, or if one of them is bound to inherit money from family, and even in situations of second marriages, to make clear the division of assets.

From assets to expectations, prenups set the ground rules

But with more people getting together later in life, many already own assets such as a home, vehicle, or have larger investments and savings. Prenups could preserve those assets and keep a record of what each spouse brought into the marriage or cohabitation, said Aimee Schalles, a lawyer and co-founder of Jointly Solutions Ltd., an online prenuptial and cohabitation agreement platform.

“We’re of the view that prenups are for everybody,” Schalles said. “We think even people who don’t have much can benefit from having some clarity in documenting what their arrangements are, and at least what they’re bringing into the relationship.”

Usually, a divorce follows the default provincial family law in the absence of a legal prenuptial agreement.

Holly LeValliant, estate and trust consultant at Scotiatrust, said while she doesn’t always recommend a prenup to all her clients, splits can be hard without a preset agreement. “You don’t marry the same person you divorce,” she said. “You can end up in a situation where you may regret later not having those conversations.”

LeValliant said prenuptials require both partners to disclose their complete financial picture. Hiding assets and debt could make the agreement invalid. The partners also need to each seek independent legal advice, she added.

Have a personal finance question? Submit it here.

Prenups protect assets and offer financial peace of mind

While prenups are primarily made to protect each person’s assets, it can also help avoid having to take on your partner’s debt. In most provinces, what people bring into their marriage remains theirs, including debt, Schalles said. “If you came into a relationship with a lot of student debt, in most provinces, that would be yours to keep and your responsibility to pay,” she said.

Article Continues Below Advertisement

But like assets, debt can accumulate interest—which the partners may have to share. That can be avoided with a prenuptial agreement.

The timing of these agreements is also really important, experts say. For example, a prenuptial agreement can’t be drawn up a day before the wedding, which could lead to one person feeling pressured to sign the papers without a choice or time to find a lawyer.

“The courts look at issues like: When was the wedding planned? Had people travelled into the wedding? Have invitations been sent out?” said LeValliant. “If you’re putting too much pressure on that party where they feel like they have no choice but to sign, it may be a void agreement.”

A flexible prenup grows with your relationship and circumstances

How the conversation about a prenuptial agreement goes might depend on how the subject is brought up.

Talking about a prenuptial is essentially an extension of financial planning, said Blair Evans, assistant vice-president of tax and estate planning at IG Wealth Management. “Sometimes, having a financial discussion is daunting, but the more financial discussions that you do have with your partner, generally, they become less daunting,” he said.

Schalles said the storytelling method could help get through the hard part of bringing it up. “Unfortunately, almost everybody knows someone who’s been through a bad split,” she said.

One way to bring up the word “prenup” without conflict could be sliding it in during financial check-ins. “It could be to say to your partner: ‘Hey, you know, do you remember our friend Jonathan and that horrible split that he had a few years ago and how much stress it caused him and his ex-wife? I don’t want that for either of us,’” Schalles said.

She added: “If we are to find ourselves in this situation, I would prefer for us to have a plan in advance so we don’t find ourselves going through what they went through, because everybody agrees that that’s ugly.”

The companies have proposed the deal as a “merger of equals,” even though Anglo American is worth more than double Teck, as plans include sourcing upper management and board representation roughly equally between the two.

The deal would also see company headquarters of what would be known as Anglo Teck move to Vancouver, as proponents look to sell Canada on the benefits of the deal that will attract regulatory scrutiny.

“We think this is a hugely compelling opportunity for Canada,” said Teck chief executive Jonathan Price in an interview Tuesday. “We will be creating the largest head office in Vancouver, and it really is unprecedented to see a company of the size of Anglo American moving its global headquarters.”

Price is set to become deputy CEO of the combined company, while Anglo American chief executive Duncan Wanblad and chief financial officer John Heasley would move to Vancouver to maintain their roles at Anglo Teck. Teck chair Sheila Murray will be chair of Anglo Teck, while board seats would be equally split between the two companies.

Merger faces Ottawa review under Investment Canada Act

The deal will be subject to review by the Investment Canada Act, which can be used to block deals deemed not in the national interest. BHP Group’s attempted takeover of PotashCorp (now Nutrien) was halted in 2010 after the government found it wasn’t a net benefit. Canadian Industry Minister Melanie Joly said in a statement that the federal government will address several issues as it considers the merger, including the combined firm’s pledge to have its senior leadership based in and reside in Canada.

The deal also includes about $4.5 billion in spending commitments to Canada over five years. It’s not clear how much of that spending is new, but Price said the combined company would also open the potential for more development in the country going forward. “As a larger company with a bigger balance sheet and much greater financial resilience, we will have the ability to invest in some of the larger projects here in Canada, for example, the likes of Galore Creek, that would be very difficult for a smaller company to handle.”

Anglo Teck would maintain its listings on the London and Johannesburg stock exchanges and also apply for listings on the Toronto and New York stock exchanges. The plan is to keep the company incorporated in London, which would mean the S&P/TSX composite index would lose Teck from its listings, since companies need to be based in the country to be included.

Keeping the company incorporated in London is both for technical reasons, and allows for wider exposure to capital, but shouldn’t take away from the deal meaning a move of the company, said Wanblad in the interview. “Without a doubt, you know, this is absolutely going to be a Canadian company,” he said.

Article Continues Below Advertisement

Compare the best TFSA rates in Canada

Teck investors left with 37.6% and no takeover premium

There have been long-standing concerns about Canadian mining giants getting snapped up by larger foreign rivals, including then-Xstrata buying Falconbridge in 2006 and the following year Vale buying Inco and Rio Tinto buying Alcan.

Teck itself was subject to a proposed US$23 billion takeover by Glencore in 2023, only for the company to end up buying Teck’s coal business for US$7.3 billion after a protracted fight. Anglo American is no stranger to being a takeover target itself, as BHP Group made a US$49 billion offer just last year that ultimately fell through.

Anglo’s proposed deal with Teck would see Teck shareholders get 1.3301 Anglo American shares for each class A and class B share they own. Anglo also plans a roughly US$4.5 billion dividend to its shareholders to help balance out its value compared with Teck, but Anglo shareholders will still own about 62.4% of the combined company, while existing Teck shareholders will hold 37.6%, on a fully diluted basis.

The deal comes without a premium for Teck shareholders, and as the company struggles with operational issues at its massive Quebrada Blanca (QB) project in Chile, but Price said it still makes sense for investors. “Teck shareholders will get exposure to what will be one of the largest and highest quality copper-focused companies in the world.”

Combining the two companies could also mean about US$800 million in pre-tax annual synergies, plus a significant boost to the value at QB because it could be run in tandem with the nearby Collahuasi mine that Anglo part-owns.

The issues at QB, which Teck further outlined just last week, has put short-term pressure on the company’s stock price, said National Bank analyst Shane Nagle. “At current prices, shares are pricing in a significant reduction in the near-term operating outlook, which we believe is far too punitive given the quality of Teck’s underlying portfolio.” He said he’s not surprised to see interest in Teck given its challenges, but with the company now in play there’s likely to be several interested parties willing to pay a premium for the company’s portfolio.

Teck and Anglo shares rally on merger news

So far, shareholders of both companies seem pleased with the deal. Teck’s shares were up more than 14% in midday trading on the Toronto Stock Exchange, while Anglo American’s were up more than 8% on the London exchange. The deal has a US$330 million break fee, while the companies say they expect the merger to be completed in the next 12 to 18 months pending regulatory and shareholder approvals.

A two-thirds majority vote by Teck’s class A and class B shareholders, voting as separate classes, is required to approve the deal, while a majority vote is needed by the Anglo American shareholders.

Under an amended offer announced Monday, Strathcona is offering 0.80 of a share per MEG share it does not already own. Its earlier overture was a combination of cash and stock. The latest offer is worth $30.86 per share, up from its earlier bid valued at $28.02 per share.

The Cenovus offer would see MEG shareholders choose between $27.25 in cash or 1.325 Cenovus common shares for each MEG share, subject to certain limits.

Strathcona claims MEG deal hands Cenovus the upside, not shareholders

Strathcona is calling the Cenovus deal “lopsided” and the MEG board’s sale process “broken” for accepting that offer.

“Congratulations, MEG board—you are in first place in the last 20 years for leaving the most amount of money on the table for your shareholders. You win the prize,” Strathcona executive chairman Adam Waterous said in an interview Monday.

Waterous noted Cenovus’ stock jumped 10% in the days following news of its deal with MEG, but typically an acquirer’s share price would fall after such an announcement. Waterous says that equates to a $3.9-billion gain in Cenovus’ stock market value that MEG shareholders are mostly not able to enjoy, as they would only own 4% of a post-takeover company.

Compare the best TFSA rates in Canada

New bid highlights choice between short-term cash and long-term gains

Under the Strathcona deal, MEG shareholders would own 43% of the new entity.

“These are two radically different paths. One is a cash exit, leaving Cenovus a $3.9-billion gain,” Waterous said. “And the second is you’re not getting off the train, you stay on the train and you try to capture that over time.”

The new offer expires on Oct. 20. MEG and Cenovus did not respond to a request for comment on Monday.

Article Continues Below Advertisement

MEG’s board has raised concerns about Strathcona’s majority shareholder—Waterous Energy Fund, which Waterous runs—selling its stake after the takeover. Waterous said he’d be in it for the long haul and there is no intention of exiting after a potential deal closes. He said Monday that his fund would be willing to enter into a lockup agreement not to sell the shares if MEG were to support its bid.

Waterous slams MEG board, says Cenovus deal will be a business school case study

The Cenovus deal must be approved by a two-thirds majority vote by MEG shareholders expected to be held on Oct. 9. Strathcona says it intends to vote its 14.2% interest in MEG against the deal.

“I have not spoken to a single MEG shareholder who is happy with the MEG board deal with Cenovus,” Waterous said. “This is going to be taught in business schools about boards of directors’ dereliction of fiduciary duty.”

Cenovus and MEG have side-by-side oilsands properties at Christina Lake, south of Fort McMurray, Alta. Strathcona also has operations in the region, and Waterous said a combination with his firm would offer similar benefits.

MEG shares rose two per cent, or 58 cents, to $28.93 in early afternoon trading on the TSX. Cenovus stock fell nine cents or about half a percentage point to $22.02, while Strathcona fell 62 cents, or 1.6% to $37.80.

Get free MoneySense financial tips, news & advice in your inbox.

The Canadian Press is Canada’s trusted news source and leader in providing real-time stories. We give Canadians an authentic, unbiased source, driven by truth, accuracy and timeliness.

Invest 91-L is expected to become a tropical depression this weekend, according to the National Hurricane Center.The tropical wave, tagged as Invest 91-L, is producing concentrated but disorganized showers and thunderstorms over the eastern tropical Atlantic. The environmental conditions appear conducive for the system to continue developing.According to the NHC, the system is expected to be near the Lesser Antilles by mid-next week. A tropical depression is expected to form this weekend.At this time, it is too early to determine what, if any, impacts this disturbance may cause.Formation chances for the next 48 hours: 60%Formation chances for the next seven days: 90% Global modelsModels are taking the system toward the Caribbean islands. If it rapidly intensifies, the system would recurve. The weaker the system stays, the further it shifts westward. However, once the wave develops into a tropical depression, it will be easier to determine its potential path. Hurricane season 2025The Atlantic hurricane season runs from June 1 through Nov. 30. Stay with WESH 2 online and on-air for the most accurate Central Florida weather forecast.>> More: 2025 Hurricane Survival GuideThe First Warning Weather team includes First Warning Chief Meteorologist Tony Mainolfi, Eric Burris, Kellianne Klass, Marquise Meda and Cam Tran.>> 2025 hurricane season | WESH long-range forecast>> Download Very Local | Stream Central Florida news and weather from WESH 2

Invest 91-L is expected to become a tropical depression this weekend, according to the National Hurricane Center.

The tropical wave, tagged as Invest 91-L, is producing concentrated but disorganized showers and thunderstorms over the eastern tropical Atlantic.

The environmental conditions appear conducive for the system to continue developing.

According to the NHC, the system is expected to be near the Lesser Antilles by mid-next week. A tropical depression is expected to form this weekend.

At this time, it is too early to determine what, if any, impacts this disturbance may cause.

Formation chances for the next 48 hours: 60%

Formation chances for the next seven days: 90%

Global models

Models are taking the system toward the Caribbean islands. If it rapidly intensifies, the system would recurve.

The weaker the system stays, the further it shifts westward.

However, once the wave develops into a tropical depression, it will be easier to determine its potential path.

Hurricane season 2025

The Atlantic hurricane season runs from June 1 through Nov. 30. Stay with WESH 2 online and on-air for the most accurate Central Florida weather forecast.

The National Hurricane Center tagged Invest 91-L in the Atlantic Ocean on Thursday morning. The tropical wave, tagged as Invest 91-L, is located several hundred miles west-southwest of the Cabo Verde Islands. Showers and thunderstorms are associated with this tropical wave. The environmental conditions appear conducive for the system to continue developing.According to the NHC, the system is expected to move westward to west-northwestward at a speed of 5 to 10 mph across the eastern and central tropical Atlantic throughout the week. A tropical depression is expected to form this week or next week.At this time, it is too early to determine what, if any, impacts this disturbance may cause.Formation chances for the next 48 hours: 60%Formation chances for the next seven days: 90% Global modelsRecent trends indicate a westward shift in the system’s trajectory. Both the European and GFS models are keeping the system from making landfall in the U.S.However, once the wave develops into a tropical depression, it will be easier to determine its potential path. Hurricane season 2025The Atlantic hurricane season runs from June 1 through Nov. 30. Stay with WESH 2 online and on-air for the most accurate Central Florida weather forecast.>> More: 2025 Hurricane Survival GuideThe First Warning Weather team includes First Warning Chief Meteorologist Tony Mainolfi, Eric Burris, Kellianne Klass, Marquise Meda and Cam Tran.>> 2025 hurricane season | WESH long-range forecast>> Download Very Local | Stream Central Florida news and weather from WESH 2

The tropical wave, tagged as Invest 91-L, is located several hundred miles west-southwest of the Cabo Verde Islands.

Showers and thunderstorms are associated with this tropical wave. The environmental conditions appear conducive for the system to continue developing.

According to the NHC, the system is expected to move westward to west-northwestward at a speed of 5 to 10 mph across the eastern and central tropical Atlantic throughout the week.

A tropical depression is expected to form this week or next week.

At this time, it is too early to determine what, if any, impacts this disturbance may cause.

Formation chances for the next 48 hours: 60%

Formation chances for the next seven days: 90%

Global models

Recent trends indicate a westward shift in the system’s trajectory.

Both the European and GFS models are keeping the system from making landfall in the U.S.

This content is imported from Twitter.

You may be able to find the same content in another format, or you may be able to find more information, at their web site.

However, once the wave develops into a tropical depression, it will be easier to determine its potential path.

Hurricane season 2025

The Atlantic hurricane season runs from June 1 through Nov. 30. Stay with WESH 2 online and on-air for the most accurate Central Florida weather forecast.

With Bay and Wall Streets trading in record territory, and certain high-flying stocks like Nvidia making headlines for their share price rallies, it’s tempting for investors—especially those who are just starting their investment journey and who might not have a lot of money to invest right off the bat—to want to jump in on the action.