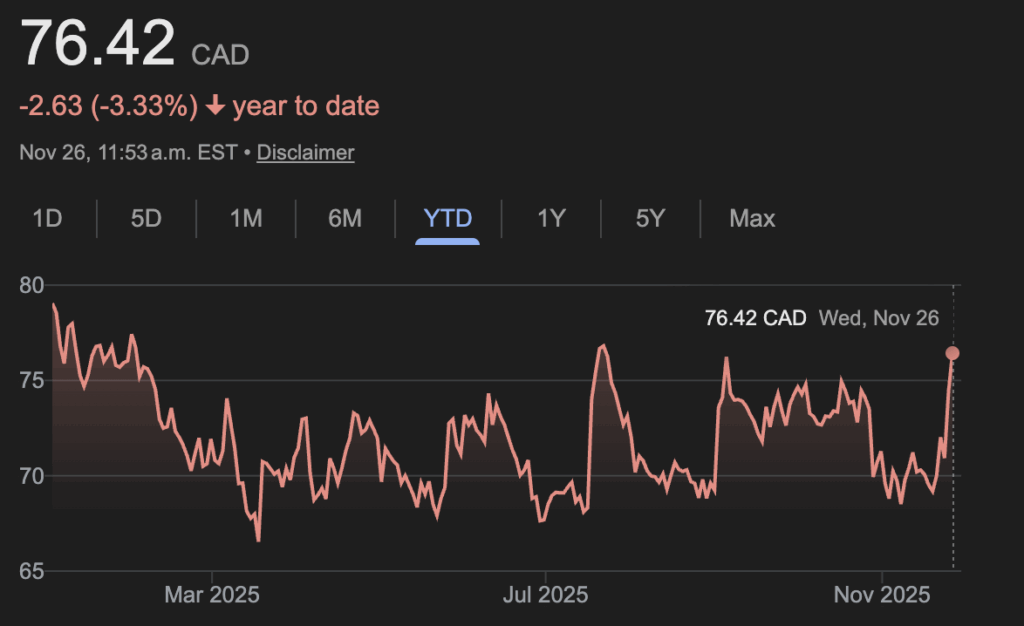

Canopy Growth chief executive Luc Mongeau says MTL’s cultivation expertise, combined with his company’s scale, positions it to improve product quality, expand supply and accelerate its path to profitable growth.

Under the terms of the agreement, MTL shareholders will receive 0.32 of a common share of Canopy Growth and 14.4 cents in cash for each MTL share they hold. Canopy shares closed at $2.40 on the Toronto Stock Exchange on Friday.

The deal requires regulatory and MTL shareholder approval. Closing of the transaction is expected to occur before the end of February.

BlackBerry reports Q3 profit of US$13.7M, up from a loss a year ago

BlackBerry (TSX:BB)

Numbers for its third quarter of 2025:

Profit: $13.7 million (up from loss of $10.5 million a year ago)

Revenue: $141.8 million (down from $143.6 million)

BlackBerry Ltd. reported a third-quarter profit of US$13.7 million, up from a loss of US$10.5 million during the same period a year earlier. The Waterloo-based software company, which keeps its books in U.S. dollars, said Thursday that its earnings per share came in at two cents US, flat compared with the prior year quarter.

BlackBerry says its revenue reached US$141.8 million for the period ended Nov. 30, down from US$143.6 million during the third quarter last year.

John Giamatteo, BlackBerry CEO, says in a press release that the company’s QNX segment reached an all-time high for revenue. QNX segment revenue came in at US$68.7 million, rising 10 per cent from US$62.3 million a year earlier.

Giamatteo says the company’s higher-than-expected overall revenue, coupled with ongoing cost discipline efforts, helped it achieve its strongest profitability in nearly four years during the quarter.

Transat A.T. reports $12.5M Q4 loss compared with $41.2M profit a year ago

Transat A.T. (TSX:TRZ)

Numbers for its fourth quarter of 2025:

Loss: $12.5 million (down from profit of $41.2 million a year ago)

Revenue: $771.6 million (down from $788.8 million)

Travel company Transat A.T. Inc. reported a loss of $12.5 million in its latest quarter compared with a profit of $41.2 million in the same quarter last year. The company says the loss amounted to 52 cents per diluted share for the quarter ended Oct. 31 compared with a profit of $1.05 per diluted share a year earlier.

Article Continues Below Advertisement

Revenue in what was Transat’s fourth quarter totalled $771.6 million, down from $788.8 million a year ago when it benefited from compensation related to Pratt & Whitney GTF engine issues. Excluding the impact of this lower compensation, Transat says revenue increased by 1.5 per cent compared with a year ago.

On an adjusted basis, Transat says it lost 42 cents per share in its latest quarter compared with an adjusted profit of 81 cents per share in the same quarter last year.

Last week, Transat narrowly avoided a costly work stoppage when it reached a new tentative contract with its pilots.

The Canadian Press is Canada’s trusted news source and leader in providing real-time stories. We give Canadians an authentic, unbiased source, driven by truth, accuracy and timeliness.

A trust is a legal arrangement where a person called the settlor transfers assets to a trustee to manage for beneficiaries, based on pre-determined rules. The assets are typically investments, real estate, or a business.

There are two main types of trusts: an “inter vivos” (living) trust, created while the settlor is alive, and a “testamentary” trust, which is written into a will, which takes effect after death.

Trusts can have an income tax motivation, an estate planning benefit, or a practical use to hold assets for a vulnerable beneficiary. That vulnerability could be that the beneficiary is too young, like a minor child, or unable to manage the assets themselves, like someone with an intellectual disability or other impairment. Trusts are also sometimes used to maintain privacy.

The most common trust use case never comes to fruition. People with minor children commonly have wills that include testamentary trusts if they die before their kids attain the age of majority. But since most parents do not die while their kids are young, these trusts are never funded.

Another common use is for business owners who might sell their business someday. A trust can own shares of their company with family members, including minor children, as beneficiaries. In this way, when the trust sells shares of the company in the future, the trust can allocate the capital gain to multiple people. If the shares qualify for the lifetime capital gains exemption, a trust can multiply the exemptions available rather than having a capital gain taxable to the business owner alone.

Principal residence exemption

Speaking of capital gains, in the context of your question, Silvana, it is important to consider what happens to your principal residence when you die.

The principal residence exemption (PRE) allows a taxpayer to claim a tax-free sale for a home that qualifies. You must have ordinarily lived in it during the years you want to claim the exemption. You can only designate one property as your principal residence for each year. However, it can apply to houses, condos, cottages, and similar vacation homes, so does not necessarily need to be the home you primarily live in, nor does it need to be the property where your mail goes.

Income Tax Guide for Canadians

Deadlines, tax tips and more

When someone dies, they are deemed to sell their assets. One exception is if they leave assets to their spouse or common-law partner, in which case, they can generally roll over tax-free or tax-deferred, depending on the asset.

So, if you do not have a spouse or common-law partner, when you die, your executor can claim the principal residence exemption for your home so that no tax results, assuming the property qualifies.

Article Continues Below Advertisement

As such, a trust will probably not save you any income tax for your principal residence, Silvana.

Probate by province

A trust may save you probate fees or estate administration tax though. This varies by province or territory. These costs are payable to validate a will and permit the executor to distribute assets to the beneficiaries.

The lowest probate fees are found in Manitoba and Québec, where there are no probate fees for most estates. Alberta also has relatively low fees, with a flat maximum of just $525 for estates over $250,000.

Ontario charges $14,250 on a $1 million estate (1.5% on the value over $50,000). For a $1 million estate in British Columbia, it would be $13,450 (1.4% on amounts over $50,000, plus a small fee on the first $50,000).

The wide range in fees means that where you live can have a significant impact on the cost of settling an estate subject to probate. Residents in high-fee jurisdictions may be more motivated to mitigate probate fees.

What should you do?

A trust does not die when you do. So, a trust can be written to distribute assets, like your home, when you pass away. This would not form part of your estate, and would therefore avoid probate.

In your case, Silvana, my concern is that you might only be trying to save, say, $15,000 on a $1 million estate, depending where you live. The legal fees to set up a trust might be $5,000 or more, and the going accounting costs to file a T3 Trust and Information Return and prepare annual trust minutes could be $1,000 to $2,000 annually, such that costs could easily eclipse the potential savings.

Trusts have a place, but there may not be a compelling reason to consider one for your principal residence unless the value is quite significant and you live in a high-probate province or territory. Personalized advice is important when complex tax and estate matters are at play.

The tech sector has seen significant volatility recently, as speculation mounts on whether there’s an AI bubble percolating after a major rally. For young investors looking for a piece of the action, experts say with the right strategy, it’s possible to participate without risking it all.

Align AI investing with risk tolerance and goals

Dhanji said he usually begins with the basics—assessing his client’s risk profile and financial goals. “Not everyone can tolerate the risks of AI companies because they are more volatile,” Dhanji said.

Investing in AI no longer has to mean owning shares of big-name tech companies. Nvidia, Meta Platforms, and AMD, among others, have been seen as proxies for the AI sector in recent years, but they are not the only options. Companies across the board have now bet huge sums of money on AI and its productivity promises.

If the client’s goals are long-term, such as retirement savings, then having some AI exposure in their portfolio can complement other asset classes, Dhanji said. The volatility of AI stocks makes them unsuitable for short-term financial goals. For example, if you’re saving money to start a business or buy a house, it’s better to keep AI stocks out of the mix.

Another risk, he said, is that technology is evolving so quickly that what you own today may be outdated in a year’s time. “You have to be careful in terms of what you’re investing in,” Dhanji said.

Balanced approach recommended for investing in AI stocks

Most investors Ryan Lee hears from are aware of the volatility, but they want to buy in anyway. Lee, a certified financial planner and founder of Twain Financial, said picking individual AI stocks to invest in can be an “overly risky” move. He also said it’s important to keep in mind how those AI stocks fit in your long-term investment strategy.

Certain index funds in your portfolio might already have exposure to AI companies—such as an exchange-traded fund (ETF) that tracks the Nasdaq. “When you hold a diversified portfolio, you already have exposure,” he said.

Lee said it’s difficult nowadays to ignore AI stocks. “There is AI in the future … and there is going to be growth,” Lee said. “But we just don’t know when that growth is going to happen or whether or not that growth is going to be higher than other industries.”

Article Continues Below Advertisement

Instead of picking individual stocks, some investors might look to AI-centric ETFs, but Dhanji warned against over-concentration. If a young investor has a long-term time horizon, Dhanji recommends 10% to 15% of their portfolio can be allocated to the AI sector. But if the investor is more conservative, Dhanji suggested capping their AI exposure to 5% of the portfolio—or not holding any AI ETFs or stocks at all if that money will be needed in the next three years or so.

Whatever the financial goal and time horizon may be, Dhanji recommended shying away from AI names that are buzzy social media recommendations. “My advice is to avoid the hype train,” Dhanji said. “I’d rather people focus on the companies themselves, making sure they have strong balance sheets and cash flows.”

Dhanji said investing in quality companies with strong balance sheets will help your portfolio weather extreme fluctuations in the market long term, if the AI bubble were to burst. “My recommendation is to have that financial plan in place, know what your cash flows look like, and instead of investing a lump sum all at once and timing the market, you can then dollar average into the market over time,” he said.

Get free MoneySense financial tips, news & advice in your inbox.

The Canadian Press is Canada’s trusted news source and leader in providing real-time stories. We give Canadians an authentic, unbiased source, driven by truth, accuracy and timeliness.

That guide, however, left out one important new entrant. Wealthsimple has since launched direct physical gold trading, and it arrived with a splash. The rollout included a promotional giveaway featuring a one-kilogram gold bar, 10 one-ounce coins, and 50 one-tenth-ounce coins for eligible clients who deposited funds and completed a survey. The promotion wrapped up on December 5.

Wealthsimple has a history of shaking up the Canadian financial services landscape. It moved ahead of the big banks on features like zero-commission options trading, direct indexing, and now physical gold access inside a brokerage account. On paper, that combination of simplicity and novelty is appealing.

The question is whether it holds up beyond the headline hype. Here’s my analysis on how Wealthsimple’s physical gold trading works, and how it stacks up against gold ETPs.

The best robo-advisors in Canada: Which one tops our list

Wealthsimple Physical Gold Trading explained

Wealthsimple’s physical gold offering is not a stock or fund. When you buy it, you are purchasing a fractional, Canadian dollar-denominated digital interest in physical gold reserves. The gold itself is stored at the Royal Canadian Mint and Brinks, and it is held at the “program level on a segregated basis.” In plain terms, your gold is held in trust alongside other Wealthsimple clients’ gold and is kept separate from Wealthsimple’s assets.

You can access this offering through all of Wealthsimple’s self-directed accounts. That includes registered as well as non-registered, taxable accounts.

Trades are executed at CAD spot prices and carry a 1% transaction fee on both buys and sells. That means buying and immediately selling would result in a 2% round-trip cost. However, there is no ongoing storage fee and, like Wealthsimple’s crypto platform, gold trading is available 24 hours a day, seven days a week.

Physical redemption is where the constraints and costs become apparent. Redemption for bullion is only available from non-registered accounts, and it is not cheap. Redeeming a one-ounce coin costs 2.25%, while redeeming a one-tenth-ounce coin costs 11%. These fees cover minting, insurance, and delivery, with fulfillment handled through Silver Gold Bull, one of the largest online bullion dealers. If physical delivery is the goal, the economics clearly improve when redeeming larger amounts rather than small denominations.

Wealthsimple Physical Gold Trading vs. gold ETPs

Right off the bat, the major gold ETPs are generally cheaper to trade and own over short and medium holding periods. To make the comparison concrete, it helps to look at the three Canadian-listed gold vehicles that actually offer physical redemption: the Purpose Gold Bullion Fund (KILO), the Sprott Physical Gold Trust (PHYS), and Canadian Gold Reserves (MNT).

Article Continues Below Advertisement

To approximate total cost of ownership, I combine each product’s management expense ratio (MER) with its most recent 30-day median bid-ask spread. This gives a reasonable estimate of the cost of buying and holding the product, assuming no sale.

KILO is among the most cost-efficient options. It carries a 0.28% MER. At the December 12 market close, it traded with a bid of $61.88 and an ask of $62.00, implying a $0.12 spread, or roughly 0.19%. Compared with Wealthsimple’s 1% upfront fee, KILO remains cheaper for roughly the first three years of holding. Only after that does Wealthsimple’s lack of an ongoing fee begin to offset its higher entry cost.

PHYS is more expensive. Its MER is 0.39%, and on the same date it showed a bid of $45.18 and an ask of $45.40, a $0.22 spread, or roughly 0.49%. In this case, Wealthsimple’s 1% gold trading fee breaks even sooner, but still only after about 1.3 years of holding.

MNT sits in the middle on fees with a 0.35% MER, but its trading costs are meaningfully higher due to poor liquidity. At the December 12 close, MNT had a bid of $64.29 and an ask of $65.00, a $0.71 spread, or roughly 1.10%. In this case, Wealthsimple is cheaper immediately on entry, even before considering MNT’s ongoing MER.

Putting it all together, Wealthsimple’s physical gold offering is not the low-cost choice for short holding periods. Low-MER products like KILO and PHYS are usually cheaper for investors with shorter or medium-term horizons. Wealthsimple only begins to make economic sense over longer holding periods, where avoiding an annual MER eventually outweighs the higher up-front fee. MNT is the main exception, where wide spreads tilt the comparison in Wealthsimple’s favour almost immediately.

But what about redemption?

If your plan is to eventually take possession of your Wealthsimple digital gold, the process is relatively intuitive. You make the request directly through the app, and Wealthsimple states that delivery is handled by insured courier, typically arriving within seven to 10 business days. By comparison, physical redemption of exchange-traded products is far more restrictive.

KILO, for example, only allows redemptions in one-kilogram increments. For context, Silver Gold Bull currently prices a one-kilogram bar at roughly $193,631 CAD, which puts redemption well out of reach of most retail investors.

PHYS is not much more flexible. Its redemption rules require investors to hold enough shares to correspond to a standard London Good Delivery bar, which weighs around 400 troy ounces. That represents a very large capital commitment.

Price growth steadied this year, allowing the Bank of Canada to push its key interest rate down by a full percentage point in 2025 to 2.25%. But with higher prices already baked-in, an increasing number of consumers struggled with debt. The annual rate of inflation slowed to 2.2% in October, the most recent available data, though pressure remained in key areas.

“Essential costs remain elevated as grocery prices rose 3.4% year-over-year, and food costs continue to outpace the general rate of inflation,” said Natasha Macmillan, senior business director of everyday banking at Ratehub.ca, by email. “Add in higher tariffs and supply chain costs, and everyday spending remains a challenge for many households.”

The higher costs have also led to more Canadians falling behind on payments. Equifax Canada said the non-mortgage delinquency rate hit 1.63% in the third quarter, up 14% from a year earlier, while average non-mortgage debt was up $511 from the year before to $22,321.

LoanFinder is moments away from showing your personalized loan matches

In under 60 seconds, get matched with a personalized list of loan providers based on your needs and approval likelihood. No SIN required.

Taxes in 2025

The federal government delivered a 1% income tax cut this year, reducing the lowest marginal rate to 14%. Because the cut went into place midway through the year, the effective rate will be 14.5% this year. The full cut will go into place in 2026. That means savings of about $206 this year, and a $420 tax cut next year, or a potential $840 in savings for a two-income household. “For many households in the middle-income range, this change may provide noticeable after-tax relief,” said Macmillan.

Prime Minister Mark Carney also cancelled the hike to the capital gains inclusion rate that his predecessor had proposed. The increase would have made two-thirds of capital gains subject to income tax, but instead it remains at half. Proponents had noted that the inclusion rate would have only changed for those with $250,000 or more in capital gains and affect an estimated 0.13% of Canadians, but Carney said that halting the increase should catalyze investment and incentivize entrepreneurs to take risks.

For those shopping for a first home, eligibility for a GST rebate on new homes up to $1 million went into place for purchases on or after May 27. The government has still to pass the law that will allow payouts, but the rebate will save first-time buyers up to $50,000. Homes sold between $1 million and $1.5 million receive a partial rebate.

Carney also removed the personal carbon tax as of April 1 in his first move as prime minister, saying it had become too divisive. The removal of the carbon tax and related rebate, however, still meant many Canadians came out ahead, especially those who drive less. The government had estimated the net benefit to households was between $157 and $723 last year, depending on the province, with lower-income Canadians generally seeing higher benefits.

Banking

An expanded program to offer low- and no-cost bank accounts went into effect at the start of December. Canadians can now get a bank account for no more than $4 a month from 14 financial institutions with 50% more debit transactions included as part of the fee.

Article Continues Below Advertisement

No-fee accounts must be available for students, Canadians 18 and under, beneficiaries of registered disability savings plans, and seniors receiving the guaranteed income supplement, while other groups could also be eligible. Newcomers can access a free account in their first year.

The government also launched consultations on increasing deposit insurance to cover $150,000, up from $100,000, but it has yet to formally make the change.

Artificial Intelligence

AI has been showing up everywhere this year, for better or for worse. On a markets level, it has raised concerns about a massive speculative bubble that threatens to hit retail investors if it pops, though so far the bet on continued growth in AI has largely made them richer.

It has also meant some people getting potentially unreliable financial guidance, while also opening up new avenues to those who find it hard to talk about their financial problems with a human.

Bruce Sellery, chief executive of Credit Canada, said that while AI has created concerns about fraud and job losses, the non-profit has also seen benefits as it launched its own AI agent called Mariposa. “You can actually complete an entire credit counselling appointment, including a debt assessment, without talking to a human if you don’t want to. It’s genius,” he said by email.

Looking ahead to 2026

Next year, some of the big changes expected include the potential for open banking to finally launch. The system will give Canadians more control of their financial data, allowing them to safely control multiple accounts in one place, among other benefits.

Trade issues will also still loom as the review of the Canada-United States-Mexico Agreement approaches. Any further disruptions in trade could threaten jobs in Canada, while also putting more pressure on inflation to force the Bank of Canada to raise rates.

As it stands, analysts expect the central bank to start to raise rates later next year or at the start of 2027, but as Bank of Canada governor Tiff Macklem said, the future is especially hard to predict these days. “Uncertainty remains high, and the range of possible outcomes is wider than usual,” Macklem said in a press conference Wednesday.

A judge in Mali ordered in June that Barrick’s Loulo-Gounkoto gold complex be placed under provisional administration for six months.

Under the deal announced Monday, Barrick says all charges brought against the company, its affiliates, and employees will be dropped and steps for the release of the four detained Barrick employees will be undertaken. It also says that the provisional administration of the Loulo-Gounkoto complex will be terminated and operational control will be handed back to the company.

Barrick says its subsidiaries will withdraw the arbitration claims pending before the International Centre for Settlement of Investment Disputes.

Alimentation Couche-Tard earns US$740.6M in Q2, rising from the previous year

Alimentation Couche-Tard Inc. (TSX:CTD)

Numbers for its second quarter:

Profit: $740.6 million (up from $708.8 million a year ago)

Sales: $17.9 billion (up from $17.4 billion)

Alimentation Couche-Tard Inc. says its net earnings attributable to shareholders came in at US$740.6 million during the second quarter, compared with US$708.8 million for the same period a year earlier. This amounted to 79 cents US per share in net earnings attributable to shareholders, rising from 75 cents US during the prior year quarter.

The Laval, Que.-based company, which keeps its books in U.S. dollars, says its revenue amounted to US$17.9 billion during the period ended Oct. 12, up 2.6% year-over-year from US$17.4 billion.

Total merchandise and service revenues came in at US$4.7 billion during the second quarter, rising 6.6% from the same period a year earlier.

Couche-Tard CEO Alex Miller says the company reported same-store sales growth across all of its geographies for the second straight quarter.

Filipe Da Silva, Couche-Tard’s chief financial officer, says in a press release that the company bought back nearly US$900 million of its shares during the quarter.

Blue Ant Media Group signs deal to buy Thunderbird Entertainment for $89 million

Blue Ant Media Corp. has signed a stock-and-cash agreement worth $89 million to buy Thunderbird Entertainment Group Inc. Blue Ant chief executive Michael MacMillan says the acquisition of Thunderbird is expected to add scale and complementary capabilities that strengthen Blue Ant’s studio business and enhance its earnings and cash flow.

Vancouver-based Thunderbird’s production businesses include Atomic Cartoons and Great Pacific Media.

Under the deal, Thunderbird shareholders will have the option to receive 0.2165 of a Blue Ant subordinate voting share, $1.77 in cash or a combination both for each Thunderbird share they hold. The maximum amount of cash available under the offer is limited to $40 million.

The deal, which requires shareholder approval, is also subject to customary closing conditions including court and regulatory approvals. The transaction is expected to close in the first quarter of 2026.

Brookfield and GIC make offer for Australia’s National Storage REIT

Canada’s Brookfield and Singaporean sovereign wealth fund GIC have made a takeover offer for National Storage REIT, an Australian self-storage company, valued at about A$4 billion or the equivalent of roughly C$3.7 billion.

National Storage confirmed it has received an unsolicited, non-binding, indicative and conditional proposal. The company has about 94,500 residential and commercial customers at more than 270 storage centres across Australia and New Zealand.

Under terms of the offer, National Storage securityholders would receive A$2.86 cash per stapled security.

The offer is being made on the basis that a dividend or distribution of six Australian cents may be paid, in which case, the cash payable per stapled security will be reduced by the same amount.

Chris Merrick, founder and owner of Merrick Financial, said there are a few different kinds of cash ETFs, but many work by essentially taking positions in high-interest savings accounts at large banks. Others invest in low-risk debt securities like bonds, known as money market ETFs. He highlighted that cash ETFs provide the ability to preserve capital while offering liquidity, unlike guaranteed investment certificates, which lock in the money for a specified period of time. “The liquidity is good. You get the interest income, which is better than a bank savings account. And often they’re kept for short-term goals,” he said.

Merrick said cash ETFs pay monthly interest based on current borrowing rates set by the Bank of Canada. “When the rates go down, unfortunately like now, the interest rates are dropping for cash ETFs,” Merrick said.

Erika Toth, director and head of ETF and portfolio consulting at BMO Global Asset Management, said that despite the comparatively lower yields, one of BMO’s top-selling ETFs over the past year has been one of its money market ETFs. Toth said they can offer advantages like “the ability to de-risk a portfolio if an investor wants to move out of equities or bonds,” since cash ETFs are a more conservative asset compared with more volatile stocks.

Liquidity and returns without market exposure

Cash ETFs can also help investors navigate times of transition.

As investors age, Toth said the need for cash flow rises, leading some to look for safer assets to put their money into, but young clients find them useful when saving for certain financial goals. “Even younger clients—saving up to buy homes or saving up for renovations or for children’s education, it’s still a good way to make sure you’re getting paid something on your cash and the funds are readily available.” Toth said cash ETFs could help someone who recently got out of the market and wants the cash they have on the sidelines to be productive.

Philip Petursson, chief investment strategist at IG Wealth Management, said cash ETFs can be a good option for any investors looking to earn a yield while maintaining liquidity of their cash holdings. “I think any time an investor has a requirement where they need the cash within 12 months and they don’t want to be subject to any market volatility at all, I think this would be a good place to be putting your money,” he said.

Over the long term though, Petursson said cash can be a drag on a portfolio because of its lower returns, meaning investors will miss out on higher growth opportunities. He added that holding around 5% of a portfolio in a cash ETF can help an investor deploy into the market during periods of volatility.

Merrick noted one of the downsides is that they are not covered by the Canada Deposit Insurance Corp., which guarantees money in Canadian bank accounts of up to $100,000 per account type at a financial institution. He said that for some people, the security afforded by CDIC protection matters, while others are indifferent. “As the saying goes, liquidity and security don’t matter until they are everything. But I feel that the chances of needing this are fairly low,” Merrick said.

Article Continues Below Advertisement

Get free MoneySense financial tips, news & advice in your inbox.

The Canadian Press is Canada’s trusted news source and leader in providing real-time stories. We give Canadians an authentic, unbiased source, driven by truth, accuracy and timeliness.

I had originally planned to focus exclusively on that book but ended up on a related project on my own site, which involved asking more than a dozen financial advisors on both sides of the border what they think of the 4% Rule and the tweaks Bengen covers in his follow-up book. The survey was conducted via LinkedIn and Featured.com, which has long supplied content for my site. You can see the complete set of responses on my blog, but at over 5,000 words, it’s a tad long for the space normally assigned to this Retired Money column.

Here, I focus on the most insightful comments and add a few thoughts of my own. Let’s jump right in.

Trusts and estates expert Andrew Izrailo, Senior Corporate and Fiduciary Manager for Astra Trust, recaps the basic thrust of the original 4% Rule:

“The 4% Rule, created by CFP Bill Bengen in the 1990s, remains one of the most referenced retirement withdrawal guidelines. It suggests withdrawing 4% of your portfolio in the first year of retirement and adjusting that amount for inflation each year. The idea was to provide a sustainable income stream for at least 30 years without depleting your savings.”

Bengen’s new book “revisits this concept using updated data and broader asset allocations,” summarizes Izrailo, “He now argues the safe withdrawal rate could rise to around 4.7%, supported by stronger market performance and portfolio diversification beyond the original stock-bond mix.”

4% is just a starting point

Like many of the other retirement experts polled, Izraelo sees the 4% Rule as “a reliable starting point, but not a fixed rule.” The 4% guideline “offers structure for retirees who need clarity on how much to withdraw each year, but real-world conditions require flexibility.”

For American investors, Izrailo still begins with 4% as a baseline because “it remains simple and conservative. Then I evaluate three major factors before adjusting: market volatility, portfolio performance, and expected longevity.” For Canadian retirees, “I tend to start lower, around 3.5%, due to differences in taxation, mandatory RRIF withdrawal rules, and the impact of currency and inflation differences compared to U.S. portfolios.”

Compare the best TFSA rates in Canada

Toronto-based wealth advisor Matthew Ardrey of TriDelta Financial was not part of the Featured roundup but agreed with the general view that while a helpful starting point, the 4% Rule is only a guideline. “When I meet with a client, I don’t rely on the 4% rule at all,” said Ardrey, who has worked with clients for more than 25 years. “I’ve learned that rules of thumb—like the 4% rule—pale in comparison to the clarity and confidence that come from a well-crafted” and personalized financial plan. Such a plan should reflect each person’s unique circumstances, priorities, and goals, allowing them to build the right decumulation strategy for their situation.

“I would never want a broad guideline to stand in the way of someone taking their dream retirement vacation or helping their children purchase their first home,” he says. “Instead, I focus on creating a detailed plan that shows exactly how those goals can be achieved. And of course, life isn’t linear. A strong plan is something we can revisit and adjust as life changes, providing updated guidance to help keep retirement on track.”

Article Continues Below Advertisement

After reading A Richer Retirement, tour operator Nassira Sennoune says Bengen succeeds in transforming “what was once seen as a strict withdrawal formula into a flexible approach that prioritizes experience, adaptability, and peace of mind … Bengen’s message is that Retirement should not revolve around fear or limitation. Instead, it should be about living fully within realistic financial boundaries. By adjusting withdrawals according to personal goals, market performance, and the natural flow of retirement years, retirees can enjoy their savings as a source of freedom rather than anxiety.”

Almost all the experts caution against taking a one-size-fits-all approach to the 4% Rule or its variants. Financial advisor and educator Winnie Sun, Executive Producer of ModernMom, has over 20 years working with clients. She starts with 4% as the baseline, then adjusts it based on actual client spending patterns and market conditions. “I had a couple last year who were terrified to spend more than their calculated 4%—even though their portfolio had grown 30%—and they were skipping vacations they’d dreamed about for decades. We bumped them to 5.5% for two years because the math worked and life is short: they finally took that trip to Italy. The biggest mistake I see isn’t about the percentage itself, it’s that people forget about tax efficiency in withdrawal sequencing.”

Oakville, Ontario-based insurance broker James Inwood says the 4% rule is “a decent guideline, but it’s not some magic number you can set and forget. I’ve watched people get into trouble because they didn’t account for medical bills, which are a real wild card here in Canada,” he shares. “I always tell people to build in a cash buffer and check in on that withdrawal rate every couple of years instead of just locking it in permanently.”

Broader asset allocation

Bengen is now recommending a broader asset diversification to add in small percentages of international equities and small-cap stocks in addition to his historic investment portfolio of 50% U.S. large-cap stocks and 50% intermediate bonds, says attorney Lisa Cummings. “He claims with this broader diversification the safe withdrawal rate could now be up to 4.7% under the best-case scenario, 4.15% worst case.”

Today’s retirees have to deal with both rising inflation and longer lifespans, she adds, so she advises clients to have a two-year cash cushion in case of prolonged negative markets, and otherwise maintain a flexible annual withdrawal range ranging between 3.5 and 4.5%.

David Fritch, a CPA with 40 years of experience serving small business owners, stopped treating the 4% Rule as gospel once he noticed their retirement income rarely came from just traditional investment portfolios. “Most had business sale proceeds, real estate holdings, and irregular cash flows that made the 4% rule almost irrelevant.”

He also realized the sequence of withdrawals and which vehicles created the withdrawals were more important than mere annual percentages. “Forget the percentage and work backward from your actual monthly expenses, then layer in guaranteed income sources (Social Security, pensions, annuities) before touching portfolio money. Most of my retired clients ended up withdrawing 2–3% because they structured things right on the front end.”

Late-career income fluctuations can change calculations

Digital marketer Fred Z. Poritsky says late-career income career changes can radically affect retirement withdrawal math. The 4% rule assumes you’re done earning but “if you’re keeping one foot in the working world (consulting, part-time, passion projects that earn), you can probably push 5–6% in those active years since you’re adding income streams.”

The results announced late Wednesday provided a pulse check on the frenzied spending on AI technology that has been fueling both the stock market and much of the overall economy since OpenAI released its ChatGPT three years ago.

Nvidia has been by far the biggest beneficiary of the run-up because its processors have become indispensable for building the AI factories that are needed to enable what’s supposed to be the most dramatic shift in technology since Apple released the iPhone in 2007. But in the past few weeks, there has been a rising tide of sentiment that the high expectations for AI may have become far too frothy, setting the stage for a jarring comedown that could be just as dramatic as the ascent that transformed Nvidia from a company worth less than $400 billion three years ago to one worth $4.5 trillion at the end of Wednesday’s trading.

Nvidia’s report for its fiscal third quarter covering the August-October period elicited a sigh of relief among those fretting about a worst-case scenario and could help reverse the recent downturn in the stock market.

“The market should belt out a heavy sigh, given the skittishness we have been experiencing,” said Sean O’Hara, president of the investment firm Pacer ETFs.

The company’s stock price gained more than 5% in Wednesday’s extended trading after the numbers came out. If the shares trade similarly Thursday, it could result in a one-day gain of about $230 billion in stockholder wealth.

Nvidia earned $31.9 billion, or $1.30 per share, a 65% increase from the same time last year, while revenue climbed 62% to $57 billion. Analysts polled by FactSet Research had forecast earnings of $1.26 per share on revenue of $54.9 billion. What’s more, the Santa Clara, California, company predicted its revenue for the current quarter covering November-January will come in at about $65 billion, nearly $3 billion above analysts’ projections, in an indication that demand for its AI chips remains feverish.

The incoming orders for Nvidia’s top-of-the-line Blackwell chip are “off the charts,” Nvidia CEO Jensen Huang said in a prepared statement that described the current market conditions as “a virtuous cycle.” In a conference call, Nvidia Chief Financial Officer Collette Kress said that by the end of next year the company will have sold about $500 billion in chips designed for AI factories within a 24-month span Kress also predicts trillions of dollars more will be spent by the end of the 2020s.

In a conference call preamble that has become like a State of the AI Market address, Huang seized the moment to push back against the skeptics who doubt his thesis that technology is at tipping point that will transform the world. “There’s been a lot of talk about an AI bubble. From our vantage point, we see something very different,” Huang insisted while celebrating “depth and breadth” of Nvidia’s growth.

Article Continues Below Advertisement

The upbeat results, optimistic commentary and ensuring reaction reflects the pivotal role that Nvidia is playing in the future direction of the economy — a position that Huang has leveraged to forge close ties with President Donald Trump, even as the White House wages a trade war that has inhibited the company’s ability to sell its chips in China’s fertile market.

Trump is increasingly counting on the tech sector and the development of artificial intelligence to deliver on his economic agenda. For all of Trump’s claims that his tariffs are generating new investments, much of that foreign capital is going to data centers for AI’s computing demands or the power facilities needed to run those data centers.

“Saying this is the most important stock in the world is an understatement,” Jay Woods, chief market strategist of investment bank Freedom Capital Markets, said of Nvidia.

The boom has been a boon for more than just Nvidia, which became the first company to eclipse a market value of $5 trillion a few weeks ago, before the recent bubble worries resulted in a more than 10% decline. As OpenAI and other Big Tech powerhouses snap up Nvidia’s chips to build their AI factories and invest in other services connected to the technology, their fortunes have also been soaring. Apple, Microsoft, Google parent Alphabet Inc. and Amazon all boast market values in the $2 trillion to $4 trillion range.

Freezer issue dents Metro’s bottom line in Q4, says costs to continue into Q1

Metro Inc. (TSX:MRU)

Numbers for its fourth quarter of 2025:

Profit: $217 million (down from $219.9 million a year ago)

Revenue: $5.11 billion (up from $4.94 billion)

Grocery and drugstore retailer Metro Inc. was hit by costs related to problems at its frozen food distribution centre in Toronto in the fourth quarter, with financial impacts expected to continue into the first quarter. The company said operations at the facility resumed last week after it was shut down for almost two months, but the temporary closure cost it $22.5 million in Q4 as it reported slightly lower annual profits.

Metro chief executive Eric La Flèche said the company expects the distribution centre to be essentially back to normal by the end of December. “I want to thank all our teams who continue to execute our contingency plan to supply our stores, thereby minimizing the impact on our customers,” he said in a statement on Wednesday.

Metro was forced to stop work at the Toronto frozen food distribution centre on Sept. 12 due to an issue with its refrigeration system. It resumed operations on Nov. 10. La Flèche said on the call that a mechanical issue, not one related to automation, was responsible for the problems with the refrigeration system. He added that the company is currently working with insurers to confirm the amount it will be able to recover.

“Looking forward to Q1 of 2026, we estimate that the direct costs associated with the rental of temporary chilling equipment and with the execution of our contingency plan will impact our net earnings by approximately $15 million to $20 million,” chief financial officer Nicolas Amyot said on the company’s conference call Wednesday.

“There was a lag,” said Deierling, speaking in Toronto on Wednesday alongside other tech sector executives on the sidelines of the Cisco Connect conference. “All of a sudden I have all this bandwidth for the internet and the dot-com era, but now I actually need Amazon and Uber and Netflix and all of these other businesses.”

AI tech is ready, no wait required

While those use cases did develop over time, Deierling said AI doesn’t have to wait decades. He said applications for software built on AI technology “already exist” and companies can take advantage of them right away.

“In the dot-com era, by the late 1990s, early 2000s, you started to see inventory build up … and people were shipping things that actually weren’t selling through. We don’t see that at all,” he said in an interview. “This stuff gets used as soon as it gets built.”

The hopeful outlook came just hours before the company reported its latest quarterly earnings Wednesday, potentially easing some analysts’ recent jitters. The company posted net income of US$31.9 billion for the third quarter, up from US$19.3 billion a year ago, while revenue rose 62%. Nvidia’s sales of the computing chipsets known as graphics processing units—which are used to help train powerful AI systems like the technology behind ChatGPT and image generators—surged beyond analysts’ expectations.

Nvidia, Wall Street’s largest stock which briefly topped US$5 trillion in value, has struggled this month, losing more than 10% on the S&P 500 as of Tuesday. As of late-morning Thursday, the stock was trading roughly 6% higher. Analysts have been closely watching the stock for potential indications of how the AI sector might continue to perform because other companies rely on Nvidia’s chips to ramp up their own AI efforts.

The best online brokers, ranked and compared

AI demand strong despite profit concerns

While stocks linked to AI have been surging for years, there have been mounting concerns that the outsized level of spending in the industry may not lead to as much profit as hoped. Other leaders in the sector also downplayed those worries at Wednesday’s conference. Francois Chadwick, chief financial officer for Toronto tech firm Cohere, likened demand for AI to a “constant drumbeat.”

“There is a real need,” said Chadwick in an interview, adding that in the early days of the internet, some tech companies were “building things that no one really even needed or wanted. Right now, there’s the demand, there is the need. Companies, enterprises, governments—everyone’s asking for this.”

That doesn’t mean all investment in AI is going to bear fruit, cautioned Tom Gillis, senior vice-president and general manager of infrastructure and security at Cisco. He said that with disruption of this scale, there “has to be winners and losers. Someone is going to be making a bet and doing something that turns out to be wrong,” said Gillis.

Article Continues Below Advertisement

“But do I think there’s going to be some sort of retraction and like, ‘Oh, it turns out AI isn’t that useful?’ Just hop on to your chat interface and then you tell me … It’s really, really, really valuable and so I think it justifies a significant amount of capital to drive that change.”

Canada strong in research, slow in deployment

A study released last month found just 8% of Canadian organizations qualify as “AI-ready.” The CiscoAI Readiness Index said nearly three-quarters of those surveyed in Canada plan to deploy AI agents and 34% expect them to work alongside employees within a year, but few have the secure infrastructure to sustain it. Those that are fully prepared are 50% more likely to see measurable value.

Deierling described Canada as “ahead on research and behind on deployment” when it comes to AI usage. “And I don’t understand why,” he said. “I mean, you have the core capacity, the people that understand this. You have all kinds of businesses that should benefit from this, and so I think it’s just a matter of will.”

But Deierling acknowledged that many companies remain fearful of AI. He said the key is to start out small, often focusing on internal use cases, rather than “risk your entire business on some AI that you may not understand how to implement.”

“Every company is ready to use AI, they just don’t know it,” he said. “The risk isn’t that high. Deploy something and start using it and what you’ll find is that there’s so much productivity gains that the demand will just completely drive the next generation.”

Get free MoneySense financial tips, news & advice in your inbox.

The Canadian Press is Canada’s trusted news source and leader in providing real-time stories. We give Canadians an authentic, unbiased source, driven by truth, accuracy and timeliness.

Users can make transactions, save, and earn rewards on their stablecoins without the volatility often associated with cryptocurrencies. Some experts even believe that stablecoins and other crypto technologies could compete with, and eventually even displace, today’s traditional payment systems.

Cryptocurrency exchanges allow users to make faster payments, pay low fees, and have better access to financial tools. For example, Coinbase has partnered with Shopify to accept USDC payments on select Shopify stores, giving users a convenient payment option that doesn’t rely on traditional banking networks.

Inside Coinbase’s USDC Rewards (and why it could be a game changer)

Coinbase’s USDC Rewards show how finance is shifting to put consumers first. The platform focuses on customer success, using technology to help Canadians grow and manage their money.

featured

Coinbase

go to site

Account minimum: $1

Trading fees: 0% – 2% per transaction. Varies by transaction amount and type (Simple, Advanced)

Welcome offer: None at this time

go to site

Here’s how it works: you earn 3.85% uncapped rewards* on your daily USDC balance, and the rewards you earn are deposited at the end of the week. Coinbase One members earn 4.25% automatically on their USDC holdings.

With USDC Rewards, you can enjoy more control over your money while being rewarded for your participation.

Higher potential returns come with risks. Stablecoins aren’t covered by CDIC insurance, which means your money isn’t protected like it is in a traditional bank account. The GENIUS Act provides a framework for U.S. financial regulation, and USDC already meets many existing crypto rules—but some risks remain.

If you prefer to play it safe, spreading your money across different accounts or investments can reduce risk. For others, USDC Rewards offers the chance to earn more than a regular savings account and be rewarded for your loyalty. You’ll also have full access to your funds, so you can sell, send, or convert stablecoins anytime without lock-ups.

The bottom line

For Canadians frustrated with low-yield savings accounts, Coinbase’s USDC Rewards program offers a compelling alternative. By paying rewards on USDC, it helps you earn competitive returns while keeping your money accessible—something that’s hard to find with traditional banks.

When the time comes, RRSP, or registered retirement savings plan accounts, are converted to RRIF, or registered retirement income fund accounts, a change that needs to be made by the end of the year that you turn 71.

Shifting your portfolio for RRIF withdrawals

You can hold the same investments in a RRIF as you hold in an RRSP, but you won’t be able to continue making fresh contributions like you did before the conversion. Rather, the opposite will be the case. You are required to withdraw amounts based on your age every year, with the percentage rising as you get older. “It’s designed to be depleted throughout your lifetime. So I find that’s challenging for a lot of people,” Andrade says.

Part of the shift in retirement can be a change in the composition of your portfolio. Andrade said she typically takes a “bucketing” approach for clients when building a RRIF portfolio, with a portion set aside in something with no or very little risk that can be used for withdrawals. That way, if the overall market takes a downturn, clients aren’t forced to sell investments at a loss because they need the cash.

Planning withdrawals to protect retirement income

Andrade says having the available cash is important when you are depending on your investments to pay for your retirement. “I want to make sure the money is there when I need it and if the market performs poorly or there’s a downturn, you still have time to recover,” she says.

Withdrawals from an RRIF are considered taxable income. So even though the money may have come from capital gains or dividend income inside the RRIF, when you withdraw it, it’s taxed as income, making the planning of the withdrawals important.

There is no maximum to your RRIF withdrawals in any given year, but you may incur a significant tax hit if the amount is large and pushes you into a higher tax bracket. If a big withdrawal pushes your income high enough, you could also face clawbacks to your OAS.

Tailor your retirement plan to your needs

Just because you are taking the money out of a RRIF account doesn’t mean you have to spend it. If you don’t need the money and have the contribution room, you can take the money and deposit it into a TFSA where it will grow, sheltered from tax.

Sandra Abdool, a regional financial planning consultant at RBC, says having money outside of your RRIF can help you avoid making big withdrawals and facing a large tax hit if you suddenly find yourself with a pricey home repair or needing to make big-ticket purchase like a new vehicle.

Article Continues Below Advertisement

“How you weave this is very much specific to each client. It’s really going to depend on what are your sources, how much income do you need, what is your current tax bracket, and what is the tax bracket projected to be by the time you get to 71,” she says.

Abdool says you should be having conversations with your financial adviser well before retirement to ensure you are ready when the time comes. “By putting a plan in place, you’re going to be prepared knowing that the income you’re looking for will be there and you’ll have the peace of mind knowing how things are going to unfold in the future,” she said.

Get free MoneySense financial tips, news & advice in your inbox.

The Canadian Press is Canada’s trusted news source and leader in providing real-time stories. We give Canadians an authentic, unbiased source, driven by truth, accuracy and timeliness.

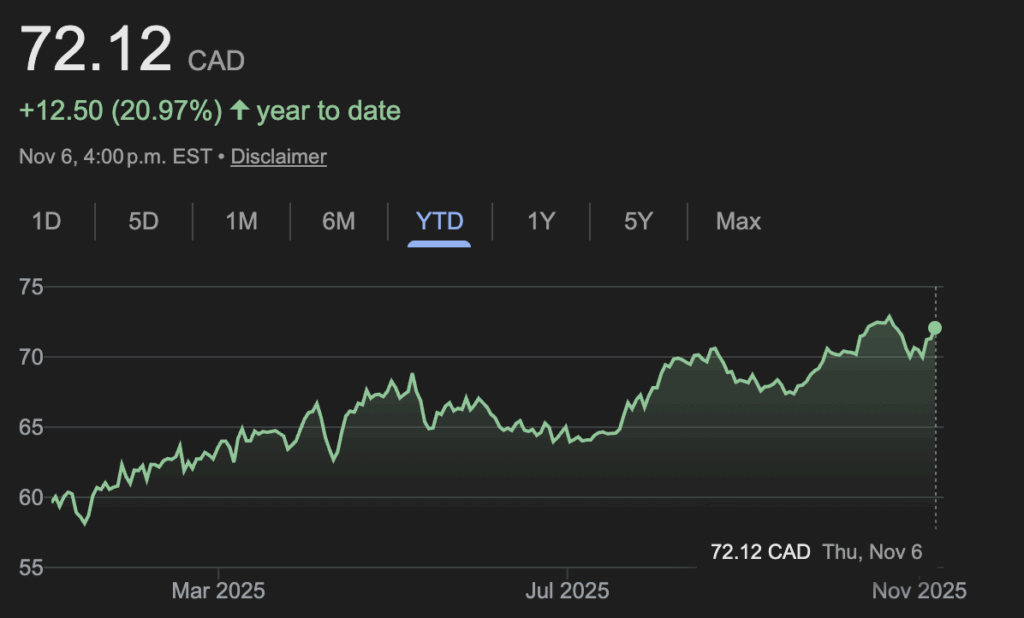

Revenue totalled US$4.15 billion, up from US$3.37 billion. On an adjusted basis, Barrick says it earned 58 cents per share in its latest quarter compared with an adjusted profit of 30 cents per share a year ago.

Gold production in the quarter totalled 829,000 ounces, down from 943,000 ounces a year ago, while the company’s realized gold price rose to US$3,457 per ounce, up from US$2,494 per ounce a year ago. Copper production amounted to 55,000 tonnes, up from 48,000 tonnes a year ago, while Barrick’s realized copper price for the quarter was US$4.39 per pound, up from US$4.27 per pound in the same quarter last year.

Barrick increased its quarterly base dividend to 12.5 cents US per share from 10 cents US and declared an additional performance dividend for the quarter of five cents US per share for a total payment of 17.5 cents US per share.

In September, Barrick appointed Mark Hill to become interim president and CEO following the sudden departure of Mark Bristow from the top job. The company says it is working with an executive search firm to find a permanent president and CEO.

MEG Energy reports $159M in Q3 profit, down from last year

MEG Energy Corp. (TSX:MEG)

Numbers for its third quarter of 2025:

Profit: $159 million (down from $167 million a year ago)

Revenue: $1.18 billion (down from $1.27 billion)

Oilsands producer MEG Energy Corp. says its profits fell during the third quarter. Net earnings for the period ended Sept. 30 amounted to $159 million, down from $167 million during the same period a year earlier. Diluted earnings per share were flat year-over-year at 62 cents.

Revenue came in at $1.18 billion during the quarter, down from $1.27 billion during the same period last year. Production for the quarter reached a record of 108,166 barrels per day compared with 103,298 during the prior-year quarter.

Last week, shareholders in MEG Energy voted in favour of an $8.6-billion takeover by Cenovus Energy Inc. (TSX:CVE) in a deal that is expected to close this month after a final court approval and other customary conditions.

Grocery and drugstore retailer Loblaw reports Q3 profit and revenue up from year ago

Loblaw Cos. Ltd. (TSX:L)

Numbers for its third quarter of 2025:

Profit: $794 million (up from $777 million a year ago)

Revenue: $19.40 billion (up from $18.54 billion)

Grocery and drugstore retailer Loblaw Cos. Ltd. reported its third-quarter profit and revenue rose compared with a year ago. The company behind Loblaws and Shoppers Drug Mart says it earned a profit attributable to common shareholders of $794 million or 66 cents per diluted share for the quarter ended Oct. 4. The result compared with a profit of $777 million or 63 cents per diluted share in the same quarter last year.

Article Continues Below Advertisement

Revenue for the 16-week period totalled $19.40 billion, up from $18.54 billion a year earlier.

The company’s hard discount and Real Canadian Superstore banners outperformed its conventional stores as consumers continue to hunt for value, Loblaw said in a release. Food retail same-store sales were up two per cent, while drug retail same-store sales rose four per cent with pharmacy and health-care same-store sales growth of 5.9 per cent and a gain of 1.9 per cent for front store same-store sales.

RBC analyst Irene Nattel said in a note to clients it was “another solid quarter” for the company, however, same-store food sales and revenue was “a string bean shy of forecast.”

On an adjusted basis, Loblaw says its earned 69 cents per diluted share in its latest quarter, up from an adjusted profit of 62 cents per diluted share a year ago.

Manulife reports $1.8 billion in Q3 earnings, down slightly year-over-year

Manulife Financial Corp. (TSX:MFC)

Numbers for its third quarter of 2025:

Profit: $1.8 billion (down from $1.84 billion a year ago)

Manulife Financial Corp. reported $1.8 billion in net income attributed to shareholders during the third quarter, down slightly from $1.84 billion during the same period a year earlier. The insurer says adjusted earnings, or what it calls core earnings, came in at $2 billion compared with $1.83 billion during the prior year quarter.

Manulife CEO Phil Witherington says the company’s core earnings in Asia and Canada reached record levels. Core earnings for Manulife’s Asia segment came in at US$550 million, while core earnings for its Canada segment came in at $428 million.

Manulife’s earnings came as the company launched a new platform with the stated goal of helping people live longer and more financially secure lives, called the Longevity Institute. The company says it is committing $350 million to the platform through 2030.

The chart below compares total returns, which measure both price appreciation and reinvested dividends, across major Canadian and U.S. equity benchmarks since 2016.

While the S&P 500 and S&P/TSX 60 have surged higher, Canadian real estate investment trusts (REITs) have badly lagged. The gap hasn’t narrowed meaningfully either. Even with distributions reinvested, the S&P/TSX Capped REIT Index remains well below its pre-COVID highs, with little evidence of a sustained rebound.

I’m not a value investor by nature, nor a sector picker, but divergences like this give me pause. Canadian REITs may quietly represent one of the few asset classes that aren’t overvalued today—and could offer genuine recovery potential in the years ahead, especially as interest rates fall.

The irony is that many Canadians still see real estate as the path to financial independence after decades of soaring home prices, even with the recent downturn in major cities like Toronto. Yet few consider REITs, which do the same thing at scale, with diversification and liquidity that private property ownership can’t match, especially when packaged into an exchange-traded fund (ETF).

The ABCs of Canadian REIT investing

REITs have their own nuances that make them very different from regular stocks. You can’t analyze them using the same metrics you’d apply to a company like Dollarama. That’s because REITs are pass-through vehicles: they’re exempt from paying corporate income tax as long as they distribute most of their taxable income to unitholders.

Unlike operating companies that make money by selling products or services, REITs earn revenue primarily from rent. They own portfolios of income-producing real estate and pass that rental income on to investors through distributions, which are usually paid monthly and tend to be higher than the average dividend yield from stocks in other sectors.

Canadian REITs span a variety of sub-sectors, including:

Office: properties leased to businesses and professional firms

Retail: shopping centers and standalone stores

Residential: apartment complexes and multi-family housing

Industrial: warehouses, logistics hubs, and distribution centers

Diversified: a mix of several categories above

Because of how REITs operate, you can’t value them using conventional measures like earnings per share (EPS) or price-to-earnings (P/E) ratios. In fact, those figures can be misleading on sites like Yahoo Finance or Google Finance. That’s because REITs use significant non-cash charges such as depreciation, which can artificially depress reported earnings even when cash flow is strong.

Article Continues Below Advertisement

The key metric for REITs is funds from operations (FFO). FFO adjusts net income by adding back depreciation and amortization (which are non-cash expenses) and subtracting any gains or losses from property sales. In simple terms, FFO is a more accurate measure of a REIT’s true cash-generating ability.

Once you know the FFO, you can calculate price-to-FFO, the REIT equivalent of a price-to-earnings ratio. It tells you how expensive a REIT is relative to its cash flow. Comparing a REIT’s price-to-FFO to its own historical average and to peers within the same subsector (e.g., residential vs. residential) gives a much fairer sense of value.

FFO is also used to judge whether a REIT’s distribution is sustainable. Since REITs pay out most of their income, the payout ratio is typically based on the percentage of FFO, not earnings. A lower payout ratio suggests more cushion to maintain distributions through economic downturns.

Supporting FFO is the occupancy rate, which measures how much of a REIT’s property portfolio is currently leased. It’s usually reported quarterly and varies by sector. As of late 2025, occupancy remains strongest in residential REITs, driven by housing demand, while office REITs continue to face pressure from remote work trends. Generally, you want to see occupancy of 95% or higher.

Another useful valuation tool is net asset value (NAV) per unit, which estimates the fair value of a REIT’s underlying real estate after liabilities. NAV divides the total appraised property value minus debt by the number of outstanding share units. The market price of a REIT can trade at a premium or discount to NAV—there’s no guarantee it will converge—but it’s still a good reality check for whether a REIT looks undervalued.

The best place to find these figures is in a REIT’s quarterly reports and audited financial filings. Some data providers, like ALREITs, compile these metrics for most Canadian-listed REITs.

Personally, I prefer REIT ETFs over picking individual REITs. Valuing REITs properly requires a working knowledge of specialized metrics. And while each REIT is diversified internally, most still focus on one property type or region. A REIT ETF spreads that exposure across multiple sectors and issuers, averaging out risks and simplifying portfolio management.

In Canada, REIT ETFs generally fall into two camps: passive index trackers and actively managed funds. Each has its strengths, and I’ll walk through some of the more notable examples in both categories, along with their pros and cons.

The Montreal-based airline says operating revenues during the quarter came in at $5.77 billion, falling around 5% from $6.1 billion during the third quarter last year.

Results for the three-month period ended Sept. 30 include the three-day work stoppage by more than 10,000 flight attendants in August that shut down operations and caused more than 3,000 flight cancellations.

Air Canada CEO Michael Rousseau says the latest results met the company’s revised estimate that was lowered to adjust for the labour disruption that occurred during the peak of the summer season. In September, Air Canada lowered its full-year guidance while estimating the cost of the strike at $375 million.

Profit: $409 million (down from $420 million a year ago)

Revenue: $2.94 billion (up from $2.77 billion)

Fortis Inc. raised its dividend as it reported a third-quarter profit of $409 million. The power utility says it will now pay a quarterly dividend of 64 cents per share, up from 61.5 cents per share.

The increased payment to shareholders came as Fortis says its third-quarter profit amounted to 81 cents per share, down from $420 million or 85 cents per share in the same quarter last year. On an adjusted basis, the company says it earned 87 cents per share in its latest quarter, up from 85 cents per share a year ago.

Revenue for the quarter totalled $2.94 billion, up from $2.77 billion in the same quarter last year.

In its outlook, Fortis announced a new five-year capital plan for 2026-2030 that totals $28.8 billion, an increase of $2.8 billion compared with its previous five-year plan.

Thomson Reuters reports third-quarter profit and revenue up from year ago

Thomson Reuters Corp. (TSX:TRI)

Numbers for its third quarter of 2025:

Profit: $423 million (up from $301 million a year ago)

Revenue: $1.78 billion (up from $1.72 billion)

Thomson Reuters Corp. reported a profit of US$423 million in its latest quarter, up from US$301 million in the same period a year earlier, as its revenue rose 3%. The company, which keeps its books in U.S. dollars, says the profit amounted to 94 cents US per diluted share for the quarter ended Sept. 30, up from 67 cents US per diluted share in the same quarter last year.

Article Continues Below Advertisement

Revenue totalled US$1.78 billion, up from US$1.72 billion a year ago. On an adjusted basis, Thomson Reuters says it earned 85 cents US per share, up from an adjusted profit of 80 cents US per share in the same quarter last year.

In September, the company acquired Additive AI Inc., a U.S.-based specialist in AI-powered tax document processing for tax and accounting professionals. The company also sold its remaining minority interest in the Elite business, a provider of financial practice management solutions to law firms.

Suncor reports decline in third-quarter profits, record production

Suncor Energy Inc. (TSX:SU)

Numbers for its third quarter of 2025:

Profit: $1.62 billion (down from $2.02 billion a year ago)

Revenue: $6.17 billion (down from $6.32 billion)

Oilsands giant Suncor Energy Inc. has reported a decline in third-quarter profits amid weak oil prices, while production and refinery throughput hit new records. Net earnings were $1.62 billion during the three months ended Sept. 30, down from $2.02 billion a year earlier. The profit amounted to $1.34 per share compared to $1.59 per share.

Operating revenues net of royalties were $6.17 billion, down from $6.32 billion during the same 2024 quarter.

Total upstream production in the quarter was 870,000 barrels of oil equivalent per day, up from 828,600 boe/d. Suncor’s refineries processed 491,700 barrels per day, an increase from 487,600 barrels in the year-ago quarter.

“Our people continue to deliver shareholder value with a culture that every barrel and every dollar matters,” CEO Rich Kruger said in a news release Tuesday. “Underpinned by our integrated business model, we are elevating overall performance and generating higher, more reliable and more ratable free cash flow with less volatility and dependence on the external business environment.”

Also Tuesday, Suncor announced it will raise its quarterly dividend by 5% to 60 cents per share.

Uranium miner Cameco raises annual dividend, reports small Q3 loss

Cameco (TSX:CCO)

Numbers for its third quarter of 2025:

Loss: $158,000 (down from profit of $7.4 million a year ago)

Revenue: $614.6 million (down from $720.6 million)

Cameco raised its dividend and reported a small net loss in its most recent quarter. The uranium miner says it will pay an annual dividend of 24 cents per share, up from 16 cents. The increased payment to shareholders came as Cameco posted a net loss of $158,000 or zero cents per diluted share for the quarter ended Sept. 30 compared with a profit of $7.4 million or two cents per diluted share a year earlier.

But long-term confidence doesn’t mean that Canadians are untouched by the current economic environment. While 68% said they’re confident they’ll ultimately meet their milestones, over half (51%) said that they’re currently putting off at least one major financial goal.

How can Canadians make sure that they hit the milestones they’re planning for? FP Canada’s survey highlights ahuge confidence gap between those who currently work with a financial planner and those who don’t.Of those working with a financial planner, 79% say they’re confident about their goals, compared with just 59% of those without professional guidance.

Laura Bishop, Qualified Associate Financial Planner (QAFP) at IG Wealth Management, says that financial planners can help Canadians of all ages and income levels prepare for life milestones with the help of an expert who knows the market in and out. “It’s not just for the wealthy,” she says. “It’s for anyone who wants to make intentional decisions about their money.”

Find a qualified financial advisor near you

Search our directory of credentialled advisors providing financial and investing services across Canada.

The biggest challenges to Canadians’ financial plans come from daily life

Among the most significant challenges Canadians said they face when planning for life milestones include paying off debt (31%) and general economic uncertainty (35%).

But the biggest challenge of all? For 41% of Canadians, not enough is left over once their necessary expenses are paid. For survey respondents aged 35-54, nearly half (48%) named this as their primary challenge.

In other words, it’s not just the big swoops and dips of economic uncertainty, or the individual burden of debt, that’s putting a pause on some Canadians’ financial confidence. For many Canadians, daily life is too expensive to make steps toward big financial plans right now.

The generational planning split: Travel comes first for Gen Z

The three most common life milestones that Canadians are saving for today include retirement or semi-retirement (50%), travel (42%), and buying a home (19%). But for younger Canadians, travel takes top priority, while more traditional goals like retirement and homeownership are taking a back seat.

These are the top milestones for Canadians aged 18-34:

43% are saving for travel

38% are saving to buy a home

34% are saving for retirement

Compare those with the top milestones for the 35-54 age group:

Article Continues Below Advertisement

61% are saving for retirement

47% are saving for travel

25% are saving for their children’s education

For both age groups, travel is a major financial priority, even beating out goals like retirement, homeownership, and education.

Best savings accounts in Canada

Find the best and most up-to-date savings rates in Canada using our comparison tool

A spending mindset

According to Bishop, Canadians’ love of travel isn’t just a coincidence. She links it to the COVID-19 pandemic, noting that since 2020 many Canadians have shifted away from just focusing on long-term savings goals to include short-term spending in their financial priorities.

“Since COVID,” she says, “a lot more people are looking at living their best life.”

“It’s about clarity”: How working with a financial planner can build confidence around money

Bishop doesn’t want Canadians to put off working with a financial planner out of a misplaced fear that they’ll lose control over their finances—or a belief that it’s only a service for the very wealthy.

Anyone can work with a financial planner, she says, and young people in particular can benefit from the financial education and insights they offer. “It’s not about giving up control; it’s about gaining clarity.”

For Bishop, the job of a financial planner is about more than expertise in markets or investment strategies. “Money is an emotional conversation,” she says. Many people, especially those who don’t feel confident about their financial goals, don’t tell even their closest friends about their financial situation—but Bishop has these honest, open conversations every day with her clients.

“A good planner will help clarify and simplify complex decisions,” Bishop says. “A great planner will align those decisions with your priorities, your goals, and a personalized plan for you.”

Get free MoneySense financial tips, news & advice in your inbox.

R.E. Hawley is a senior writer and editor with over a decade of combined experience in the education and insurance spaces. R.E. values creating accessible content on complex financial topics that people can use to make informed decisions.

There have been increasing calls to simplify the rules to make it easier to launch Canadian-dollar linked stablecoins, and stem the potential outflow of capital from the country. “At a minimum, from a sovereignty perspective, Canadians should want a Canadian stablecoin,” said Didier Lavallée, chief executive of digital assets company Tetra Digital Group.

U.S. stablecoin dominance puts pressure on Canada

Concerns have risen since the United States passed legislation this past summer that establishes clear rules around the sector, and further entrenched U.S.-dollar dominance in the space that touts faster and cheaper money transfers.

Because stablecoins are meant to reflect the value of conventional currencies, issuers need to buy hard assets like dollars to back them up. No Canadian-dollar pegged stablecoins means more money flowing out of Canada, and into U.S. dollars and U.S. government bonds.

“Canada should also weigh the merits of federal stablecoin regulation,” said Ron Morrow, executive director of payments at the Bank of Canada, in a September speech.

His former colleague Timothy Lane, who stepped down as deputy governor in 2022, was a little more blunt in an October report for the Global Risk Institute. “Stablecoins are becoming too important to be ignored,” said Lane. “There is now an increasing sense of urgency about establishing a coherent framework for regulating stablecoins in Canada.”

Peter Routledge, head of Canada’s banking regulator, has also said he’s worried about the fast moving space and will be watching the budget closely on Nov. 4, while John Ruffolo, managing partner at Maverix Private Equity, has been one of the most outspoken in the need to respond.

One of Ruffolo’s biggest worries is that some people and businesses could start to leave money in the stablecoin sphere, rather than in bank deposits. That’s already how stablecoins first gained traction: as a stable place for crypto-traders to park money between bets, without having to exchange it back into conventional currencies.

Given banks use deposits as an anchor for lending, he’s warned that even if 5% of Canadian bank deposits, or some $135 billion, went into U.S. stablecoins, it would have a knock-on effect of erasing as much as $675 billion in domestic lending capacity.

Article Continues Below Advertisement

Private sector leads Canada’s stablecoin push

The rising calls have increased expectations of some movement from the federal government, but given how slowly past promises like open banking have actually rolled out, some companies like Tetra aren’t waiting around for change before pushing ahead with their own stablecoins. “Financial innovation in this country takes quite a long time,” said Lavallée.

Because Tetra is already registered as a Canadian trust company, Lavallée sees an easier road than others to getting regulatory approval through the current system. Tetra’s efforts have also had a boost from major backers like Wealthsimple, National Bank, ATB Financial, and Shopify, which chipped in on a $10 million financing to help ready a stablecoin for release aimed at early next year.

The best crypto platforms and apps

We’ve ranked the best crypto exchanges in Canada.

Elsewhere, Transactix Financial Inc. announced plans in May to move forward on its own token, and just last week Loon Technology Inc. announced it had raised $3 million to get its own Canadian-dollar stablecoin going.

The companies are all working to navigate an existing system that some, at least, aren’t so concerned about. “I think it’s working well,” said Grant Vingoe, head of the Ontario Securities Commission that’s taken a lead role in stablecoin oversight.

Uptake and impact of stablecoins still unclear

While the U.S. has used legislation, Canada’s approach to working with each issuer is more adaptable in the fast-moving crypto space, he said. “There’s a lot to be said for a more tailored, direct engagement approach, where you express your concerns and requirements … rather than try and codify it once and for all.”

So far that approach has yielded a single issuer, Circle, getting the blessing of regulators for its U.S. dollar-pegged stablecoin.

But Vingoe is also still skeptical about how much uptake there will actually be for stablecoins. “I think it’s still an open question whether stablecoins will be used extensively as a payment mechanism.” Improvements to the existing payment system could end up being better or more efficient, he said.

Some have pointed to central banks possibly issuing their own digital currencies, though the Bank of Canada has shelved work on such efforts.

As noted in the previous edition of this column, Bitcoin’s (BTC) strongest months have historically been October and November—up an average of 21.89% and 46.02%, respectively. In keeping with this promise, the crypto market started October strong as BTC ran up from about $114,000 (all figures in U.S. dollars unless otherwise specified) on October 1 to a new high of over $126,000 on October 7. Ethereum (ETH), XRP, Solana (SOL), Binance Coin (BNB), and other altcoins also saw impressive runaway gains in the first week of October.