Nvidia Corp. shares are back on track to try to turn in their best year ever after closing at a record high Tuesday, as the company reached a $1.2 trillion market capitalization for the first time.

After an initial show of strength, Nvidia walked back gains following its blowout earnings report last week, when the graphics-processing-units maker topped Wall Street’s data-center sales estimates by more than $2 billion for the quarter, and forecast revenue for the current quarter of more than $3 billion above expectations.

Nvidia also closed above a $1.2 trillion market cap for the first time Tuesday, according to Dow Jones Market data.

In a little more than a year, Nvidia’s market capitalization had increased by close to $1 trillion, adding $925 billion in market cap since 2022’s stock price low, hit on Oct. 14, when shares closed below $113 for the first time since August 2020, according to Dow Jones data.

Last fall, Nvidia’s stock was melting down because it had to replace some $400 million in expected data-center sales to China with equipment that would clear a U.S. ban on AI tech as well as deal with inventory write-downs.

Nvidia shares are up 234% year to date, compared with a 17% gain by the S&P 500, and already ahead of their strong 2016 gain of 224%, and back in the running to overcome their best one-year gain of 308% set back in 2001, according to FactSet data.

Nvidia shares were also the second-most active on the S&P 500 on Tuesday, with more than 69 million shares exchanged, second only to Tesla Inc.’s TSLA, +7.69%

more than 132 million shares exchanged by the close.

For their part, Tesla shares posted a 7.8% gain Tuesday, their biggest one-day jump in five months, following a report that Tesla was launching a $300 million AI computing cluster using thousands of Nvidia GPUs.

Also on Tuesday, Nvidia and Alphabet Inc. GOOG, +2.81%

Nvidia Corp. shares rallied in the extended session Wednesday after the maker of graphics processing units that is leading the AI-hardware charge reported a 141% surge in data-center sales and record results.

Nvidia NVDA, +3.17%

shares rallied 9% after hours, following a 3.2% rise in the regular session to close at $471.16, less than 1% below the stock’s record closing high of $474.94, set on July 18, according to FactSet data. A close at such levels on Thursday would mean a new record high for the stock.

The Santa Clara, Calif.-based company reported second-quarter net income of $6.19 billion, or $2.48 a share, compared with $656 million, or 26 cents a share, in the year-ago period. Adjusted earnings, which exclude stock-based compensation expenses and other items, were $2.70 a share, compared with 51 cents a share in the year-ago period.

Revenue surged to a record $13.51 billion from $6.7 billion in the year-ago quarter, driven by a 141% leap in data-center revenue to $10.32 billion.

Analysts surveyed by FactSet had forecast earnings of $2.08 a share on revenue of $11.19 billion, and data-center sales of $8.03 billion.

Nvidia forecast third-quarter revenue of $15.68 billion to $16.32 billion.

Analysts had estimated third-quarter earnings of $2.40 a share on revenue of $12.59 billion, with $9.15 billion of that from data-center sales. For the year, Wall Street, on average, expects earnings of $8.29 a share on $44.54 billion in revenue, a 71% increase from fiscal 2023’s $26.97 billion, with $32.41 billion of that in data-center sales.

“Companies worldwide are transitioning from general-purpose to accelerated computing and generative AI,” said Jensen Huang, founder and chief executive of Nvidia, in a statement. “Leading enterprise IT system and software providers announced partnerships to bring Nvidia AI to every industry. The race is on to adopt generative AI.”

Right after the report, Lopez Research analyst Maribel Lopez told MarketWatch that Nvidia’s “numbers prove just how much money there is in the AI hardware opportunity.”

“While cloud companies are selling AI services, Nvidia is walking away with a bulk of the revenue and profits,” Lopez said. “Nvidia’s minting cash with no apparent slowdown in sight.”

Nvidia shares are up more than 222% on a year-to-date basis, compared with a 42% surge in the PHLX Semiconductor Index SOX,

a 15.5% rise by the S&P 500 SPX

and a 31% gain by the tech-heavy Nasdaq Composite COMP

over the same span.

Nvidia currently stands as the fifth-largest U.S. company by market cap behind Apple Inc. AAPL, +2.19%,

Microsoft Corp. MSFT, +1.41%,

Alphabet Inc. GOOG, +2.71%

GOOGL, +2.55%

and Amazon.com Inc. AMZN, +0.95%.

While all have a big stake in the future of AI, the latter three companies are scrambling to outfit their cloud-service provider data centers with new AI gear amid tight supply.

While Nvidia is considered the overwhelming leader in the AI chip market, Advanced Micro Devices Inc. AMD, +3.57%

is considered a distant second. AMD’s data-center numbers declined in the company’s recent earnings report, although the company didn’t have comparable AI chip sales in its results.

Shares of AMD and TSMC were both up more than 3% after hours Wednesday.

Arm Holdings Ltd. filed its long-awaited initial public offering late Monday, following last year’s failed bid by Nvidia Corp. to acquire the U.K.-based chip architecture company.

Arm has reportedly been seeking to raise $8 billion to $10 billion at a valuation of $60 billion to $70 billion, making its IPO the biggest of the year so far, and a number of large tech companies, including Amazon.com Inc. AMZN, +1.10%, Intel Corp. INTC, +1.19%

and Nvidia NVDA, +8.47%,

are reportedly in the mix to be anchor investors.

At the time of the breakup, chips sales had hit record highs in 2021, surging 26.2% to a record $555.9 billion, fueled by pandemic-triggered shortages. But the chip industry has since swung to a glut.

Arm listed Barclays, Goldman Sachs, JP Morgan, Mizuho, BofA Securities, Citigroup, and Deutsche Bank Securities among the IPO’s underwriters.

Recent reports said SoftBank was in discussions to purchase the 25% stake in Arm that it does not outright own, which is held by its Vision Fund 1, ahead of the IPO.

Arm reported net income of $524 million, or 51 cents a share, on revenue of $2.68 billion for fiscal 2023, which ended March 31, compared with net income of $549 million, or 54 cents a share, on revenue of $2.7 billion, in fiscal 2022, and $388 million, or 38 cents a share, on revenue of $2.03 billion in fiscal 2021.

Arm uses an architecture that is different from the once-standard x86 one built by Intel in the early days of computing.

The company said it has shipped more than 250 billion Arm-based chips since its started in 1990 as a joint venture between Acorn Computers, Apple AAPL, +0.77%

and VLSI Technology. In fiscal 2023, Arm said it shipped 30.6 billion chips.

The company said it is going public as the “resources required to develop leading-edge products are significant and continue to increase exponentially as manufacturing process nodes shrink.” Transistors are expressed in scales of nanometers, with design costs running about $249 million for a 7-nanometer chip and about $725 million for a 2-nm chip.

“As the world moves increasingly towards AI- and [machine language]-enabled computing, Arm will be central to this transition,” the company said in the filing. “Arm CPUs already run AI and ML workloads in billions of devices, including smartphones, cameras, digital TVs, cars and cloud data centers.”

Arm said it is working with Alphabet Inc. GOOG, +0.64%

The so-called Magnificent Seven grouping of technology stocks lost some of its luster this week after four of the seven moved into correction territory, meaning their stocks have fallen at least 10% from their recent peaks.

The corporate-bond market, in contrast, seems to like all seven names.

One caveat: Tesla has no outstanding bonds. In the past, the electric-car maker issued convertible bonds, but they have all been converted into equity.

The group is credited with helping drive the stock market’s gains in the first half of the year, driven by excitement about artificial intelligence. But the rally has stalled in recent weeks as investors have fretted over the potential for U.S. interest-rate increases, surging Treasury yields and China worries, with property developer Evergrande filing for U.S. bankruptcy protection late Thursday.

On Thursday, Meta followed Apple, Microsoft and Nvidia into correction territory, as MarketWatch’s Emily Bary reported. Tesla, meanwhile, is in a bear market, meaning it’s down more than 20% from its recent peak.

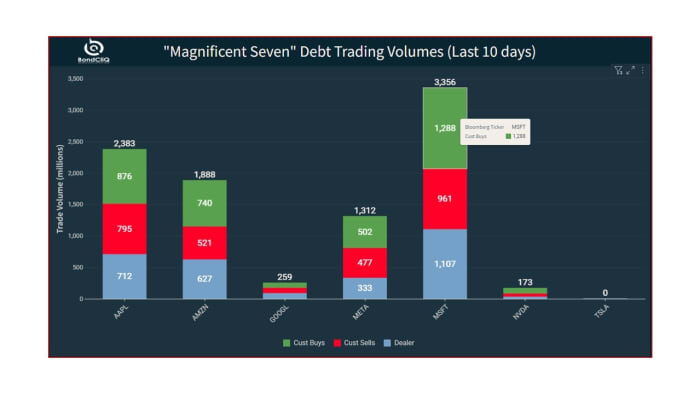

The following series of charts from data-solutions provider BondCliQ Media Services show how many bonds each company has issued by maturity and how they have traded as the stocks have pulled back.

The first chart shows that Microsoft has by far the most bonds, mostly in the 30-year bucket. The software and cloud giant has more than $50 billion in long-term debt, according to its 2023 10-K filing with the Securities and Exchange Commission.

Outstanding Magnificent Seven debt by maturity bucket.

Source: BondCliQ Media Services

This chart shows trading volumes over the last 10 days, divided by trade type. The green shows customer buying, while the red is customer selling. The blue shows dealer-to-dealer flows. Microsoft, for example, has seen almost $1.3 billion in customer buying from dealers in the last 10 days and $960 million in customer sales to dealers.

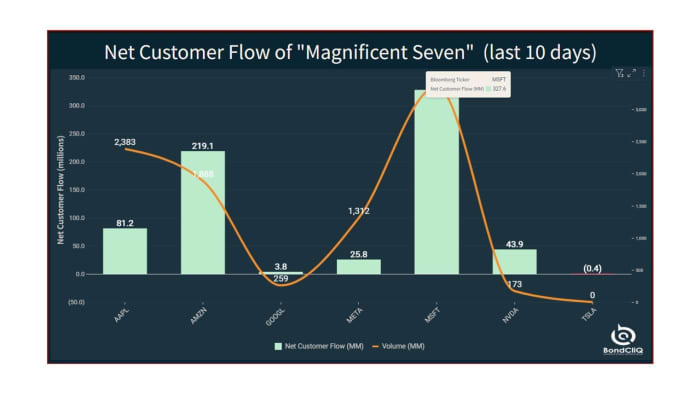

This chart shows that every name in the group has enjoyed better net buying in the last 10 days, with Microsoft leading the way.

Net customer flow of Magnificent Seven debt (last 10 days).

Source: BondCliQ Media Services

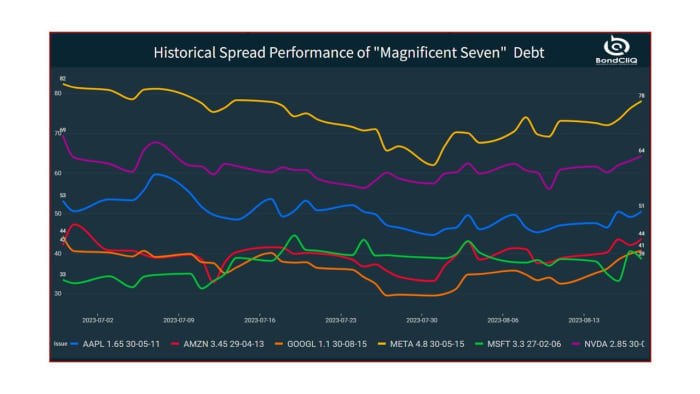

This chart shows spread performance over the last 50 days for an intermediate-term bond from each of the seven issuers. Most have tightened or remained steady over the period.

Historical spread performance of Magnificent Seven debt.

Apple’s stock entered correction Wednesday upon falling more than 10% from its July 31 peak of $196.45. The company sells mainly discretionary products, and right now “consumers are still being pinched” and thinking more carefully about where they spend their money, according to Matt Stucky, senior portfolio manager for equities at Northwestern Mutual Wealth Management.

A wider swath of stocks have joined the S&P 500 SPX, +0.15%’s

upswing after the so-called Magnificent Seven — Apple AAPL, +0.32%,

Amazon AMZN, +1.11%,

Alphabet GOOG, +0.08%,

Microsoft MSFT, -0.72%,

Meta META, -2.11%,

Nvidia NVDA, -0.04%

and Tesla TSLA, +0.37%

— single-handedly propelled the large-cap index into a bull market in early June, with the gauge now up more than 28% from its low notched last October and rising to new highs since April 2022, according to Dow Jones Market Data.

Hopes that the U.S. economy could pull off a soft landing and avoid a recession despite the Federal Reserve’s aggressive interest-rate hikes, as well as receding inflation pressures and expectations for the end of the Fed’s monetary tightening campaign, have underpinned a notable expansion in market breadth over the past two months, according Adam Turnquist, chief technical strategist at LPL Financial.

The S&P 500 Equal Weighted Index SP500EW, +0.27%,

which lagged behind the market-cap-weighted S&P 500 index for most of the year, has now kicked back into gear and staged an impressive comeback in July. The equal-weighted index and the S&P 500 each advanced 3.1% this month, according to FactSet data.

The equal weighting eliminates the distortion of the megacap components and significantly changes several sector weightings in the S&P 500, including technology, which drops from around 29% on the SPX to only 13% on the equal-weighted index, said Turnquist in a Friday note. Meanwhile, the industrials sector has the biggest increase in weight, jumping from 9% on the SPX to 16% on the equal-weighted index.

Another way to quantify and compare market breadth is to look at the percentage of stocks on an index trading above their longer-term 200-day moving average (dma), Turnquist said. In general, if a stock is trading above its 200 dma, it is considered to be in an uptrend, and if the price is below the 200 dma, it is considered in a downtrend. Furthermore, a higher percentage of stocks above their 200 dma implies buying pressure is more widespread — suggesting the market’s advance is likely sustainable.

The chart below shows that 73% of stocks within the S&P 500 are trading above their 200 dma as of July 27, which compares to only 48% at the end of 2022. Moreover, the composition of breadth leadership has turned increasingly bullish. The highest sector readings include technology, industrials, energy, and consumer discretionary.

“So not only is breadth on the index robust, but cyclical stocks are also leading,” said Turnquist.

SOURCE: LPL RESEARCH, BLOOMBERG

Wall Street often views broadening participation in the stock-market rally as a measure of health and a constructive sign of the sustainability of the bull market.

Jimmy Lee, founder and chief executive officer of The Wealth Consulting Group said he is seeing “a lot of money” flowing into areas that are not the Magnificent Seven such as stocks in the industrials, financials, materials, energy and even real-estate sectors.

The S&P 500’s industrials sector SP500.20, +0.23%

climbed 2.9% in July, while the financials sector SP500.40, +0.44%

advanced over 4.7% this month. The S&P 500’s energy sector SP500.10, +2.00%,

which had been the biggest laggard when the rest of the markets exited the bear market in June, jumped 7.3% month to date after the U.S. oil benchmark CL.1, -0.20%

Meanwhile, the tech-heavy S&P 500’s communication-services sector SP500.50, -0.03%

rose 6.7% in July, while the consumer-discretionary sector SP500.25, +0.56%

gained 2.4% and the information-technology sector SP500.45, +0.13%

was up 2.6%, according to FactSet data.

Stephen Hoedt, managing director of equity and fixed income research at Key Private Bank, told MarketWatch in an interview that he doesn’t see “any reason to get bearish here with the fundamentals that are underlying,” which gives investors reason to rotate toward the more cyclical areas such as energy, financials and industrials, while broadening the market away from just being concentrated in the megacap technology names.

“The growth has been a surprise this year for everyone, so that’s what the market got wrong coming into this year. When I look at growth, nominal GDP growth translates directly into earnings and we’ve seen earnings continue to surprise on the upside,” Hoedt said.

Hoedt pointed to the direction of the 12-month forward earnings estimate for the S&P 500 as an important indicator. “As long as the direction of the 12-month forward earnings number for the S&P 500 is going up, it’s really, really difficult to be bearish on the stock market,” he said. “It seems to me that we may start to see another inflection higher in forward earnings revisions that take into account this stronger growth environment that we’re in.”

However, the broadening of the stock-market rally and the bullish sentiment were also driving some on Wall Street to believe stocks are overbought and due for a correction.

Lee said there’s still too much pessimism out there and too much concern that some investors haven’t chased the market yet. “In the second half of this year, when the Fed does stop raising rates and if the economy stays out of recession, you can see major money — trillions of dollars moving from the money market into equities and other risk assets,” he told MarketWatch in a phone interview on Friday.

“When that happens, it’s probably going to push valuations even further. So I would imagine when that happens is when you can expect more of a correction to occur, but I think that we still have more room to go before that happens.”

U.S. stocks ended higher on Monday, finishing up July on a positive note. Three major stock indexes rallied this month, with the S&P 500 up 3.1% and booking its fifth monthly gain. The tech-heavy Nasdaq Composite COMP, +0.21%

gained 4.1% month to date, while the Dow Jones Industrial Average DJIA, +0.28%

advanced 3.4%, according to Dow Jones Market Data.

There are two certainties in the tech world when it comes to digital advertising: Google and Meta. And then there’s everyone else.

Through economic thick and thin, Google and Meta are the gold standards by virtue of broad reach (billions of people globally), product dominance (in search and social media, respectively) and in their positions in the lightning-fast AI race. This week’s earnings results for Alphabet Inc. GOOGL, +2.46%

Both companies rebounded from recent wobbly digital ads sales of their own through giganticconsumer reach and aggressive plans to parlay AI into ad sales. Google has developed (or dabbled) in some form of AI for at least seven years, and in a conference call with analysts Wednesday, Meta Chief Executive Mark Zuckerberg said his company will focus in the near term on AI to develop agents, ad features in existing products like Instagram and Reels, and internal productivity and efficiency. “We want to scale them, but they are hard to forecast,” he admitted.

“We continue to believe it will take multiple quarters of improved execution for many investors to get more comfortable with the story longer term,” JP Morgan analysts said in a note on Snap earlier this month.

Digital-advertising leader Google sought to remind everyone it has been doing AI a long time while Microsoft Corp. MSFT, +2.31%,

a major investor in ChatGPT pioneer OpenAI, tempered its approach, Josh Wetzel, chief revenue officer at OneSignal, said in an interview. “AI’s greatest immediate value may be for Facebook advertising,” he said, pointing to it as an efficient and effective tool after Facebook encountered issues with data-privacy changes Apple Inc. AAPL, +1.35%

made to mobile devices.

“Meta’s solid quarter adds further evidence to the view that advertisers are choosing to spend their budget on the so-called market leaders, such as Facebook and Instagram, at the expense of the smaller social-media networks, like Snap,”said Jesse Cohen, senior analyst at Investing.com.

Jon Oberlander, executive vice president of social at digital-marketing agency Tinuiti, added: “It is, to some extent, still Meta/Google’s game, especially for performance advertisers, as the ROI and scale advertisers can find in the mid-lower funnel gap above other platforms.”

At the same time, Forrester analyst Kelsey Chickering said linear television ad revenue will slow between now and 2027 to about $65 billion from $70 billionas traditional TV continues to lose the under-25 crowd that has fled to streaming services and creator-heavy platforms like Snapchat and TikTok.

Digital advertising is on track to grow in the high single digits, or more, in 2023, slightly ahead of June’s forecast estimates from GroupM and Magna of around 8% each, according to Brian Wieser, head of Madison and Wall, a media and advertising consultancy for investors.

Most of that growth will benefit Google, Meta, and Microsoft’s LinkedIn, according to data from Emburse. Conversely, Emburse found ad spending on Twitter/X has plunged 54% from a year ago in May, before Elon Musk bought the company.

“Google, Meta and LinkedIn are platforms where people go to consume information, search for ideas, or give context to what they experiencing in their personal or work lives,” Emburse Chief Experience Officer Johann Wrede said.

While Alphabet CEO Sundar Pichai boasted Wednesday of “continued leadership in AI and our excellence in engineering and innovation are driving the next evolution of Search” and other services, as well as improved YouTube ad sales, Meta’s addition of potential X-killer Threads could dramatically inflate its ad sales going forward.

Zuckerberg sees potential in Threads long term despite a plunge in its user sign-ups because X is hemorrhaging advertising clients, and this week reportedly slashed ad costs to lure business customers.

“The launch of Threads holds great promise for Meta. While there are currently no ads on the app, it’s inevitable that they will come and the ability to use data from other Meta properties for targeting is a highly lucrative proposition for brands,” Aaron Goldman, chief marketing officer at Mediaocean, said in an email.

That translates to more near-term pain for smaller platforms such as Snap and X, which are posting negative growth, Michael Nathanson of SVB MoffettNathanson warned in a note Wednesday.

“The truth is that Alphabet started integrating machine learning and artificial intelligence into their products and ad solutions close to a decade ago,” he said. Snap and others are scrambling to catch up.

Facebook parent Meta Platforms Inc. is raking in digital ads, as its earnings attest, and Wall Street is rewarding it. The company’s stock rose about 7% in after-hours trading Wednesday.

Meta META, +1.39% reported fiscal second-quarter net income of $7.79 billion, or $2.98 a share, compared with net income of $6.7 billion, or $2.46 a share, in the year-ago quarter.

Revenue climbed 11% to $32 billion from $28.8 billion in the year-ago quarter.

Analysts surveyed by FactSet had expected on average net income of $2.91 a share on revenue of $31.1billion.

A rebound in advertising, the monetization of Instagram and Reels, and AI-fueled ad targeting and measurement contributed to the quarter’s performance. Meta’s better-than-expected performance comes on the heels of a similarly strong quarter from Google parent GOOGL, +5.78%

“We had a good quarter. We continue to see strong engagement across our apps and we have the most exciting roadmap I’ve seen in a while with Llama 2, Threads, Reels, new AI products in the pipeline, and the launch of Quest 3 this fall,” Meta Chief Executive Mark Zuckerberg said in a statement announcing the results. AI has been an increasingly dominant story line for Meta, which has quickly shifted its focus from the metaverse. Zuckerberg said AI remains the company’s near-term focus, with metaverse poised to have a long-term impact.

“In many ways, the two are interrelated,” Zuckerberg said of AI and metaverse in a conference call with analysts. He also spotlighted the potential of Threads, a Twitter-like service that launched earlier this month with much fanfare. “When it gets to hundreds of millions of users, we’ll see how it monetizes,” he said. “It is a long road ahead.”

Meta executives forecast third-quarter revenue of $32 billion to $34.5 billion, while analysts on average were expecting $31.2 billion, according to FactSet.

Facebook had 2.06 billion daily active users, up 5% from a year ago, and the “family” of Meta apps — which includes Instagram — reported daily active users of 3.07 billion, up 7%.

There were blips amid the hoopla, however. Meta says it expects 2023 total expenses will be in the range of $88 billion to $91 billion, compared to the prior range of $86 billion to $90 billion because of legal-related expenses in the second quarter. And Meta’s headcount dropped 14% from a year ago to 71,469 as of June 30. Zuckerberg said Meta’s austerity program will continue into 2024.

Meta’s stock improved 1.4% to $298.57 in the regular session. The stock has sky-rocketed 148% so far this year, while the broader S&P 500 index SPX, -0.02%

has increased 19%.

Google parent Alphabet Inc.’s stock jumped 6% in after-hours trading Tuesday after the company beat estimates on the top and bottom line, and announced the transition of Chief Financial Officer Ruth Porat to president and chief investment officer in September.

Fueled by strong advertising sales, Alphabet GOOGL, +0.56%

GOOG, +0.75% racked up fiscal second-quarter net income of $18.4 billion, or $1.44 a share, compared with net income of $16 billion, or $1.21 a share, in the same quarter a year ago.

Total revenue was $74.6 billion, compared with $69.7 billion a year ago. Sales minus traffic-acquisition costs were $62.06 billion, vs. $57.5 billion last year.

Analysts surveyed by FactSet had expected on average net earnings of $1.34 a share on revenue of $72.85 billion and ex-TAC revenue of $60.25 billion.

“There’s exciting momentum across our products and the company, which drove strong results this quarter,” Alphabet Chief Executive Sundar Pichai said in a statement. “Our continued leadership in AI and our excellence in engineering and innovation are driving the next evolution of Search, and improving all our services.”

During a conference call Tuesday afternoon, he highlighted the intertwining of advertising and Alphabet’s strides in generative AI. He added the company continues to consolidate and align operations to streamline spending.

Shares of Alphabet have advanced 39% so far this year largely on the strength of generative AI and its potential. The broader S&P 500 index SPX, +0.28%

is up 19%. Alphabet’s stock inched up 0.6% to $122.21 in the regular session Tuesday.

Google’s total advertising sales improved to $58.14 billion from $56.3 billion a year ago, and edged analysts’ average expectations of $57.45 billion. Google Cloud hauled in $8 billion, compared with $6.3 billion last year. YouTube ad sales rebounded to $7.7 billion from $7.34 billion a year ago.

“The proverbial floodgates aren’t opening yet but clients are starting to see pockets of opportunity and are willing to invest for a direct return,” Aaron Levy, vice president of paid search at Tinuiti, said in an email.

Porat, who has played an essential role in Google’s advertising success since she became CFO in 2015, will start her new role on Sept. 1. She will be responsible for Alphabet’s investments in its Other Bets portfolio, and the company’s investments in countries and communities around the world. Porat will continue to report to Pichai.

“We see technology can make so much of a difference in people’s lives… and in economic growth globally,” Porat said during the conference call late Tuesday.

The monetization of AI continues to be an obsession of investors and Wall Street. Microsoft Corp.’s MSFT, +1.70%

AI version, Bing, hit the market first, but Google’s competing entry, Bard, is making headway, according to analysts. Alphabet is ramping up AI initiatives to improve operational efficiency and productivity.

When asked on the call about AI monetization, Pichai said the technology expands the company’s total addressable market, brings in potential new customers, deepens the versatility of its product portfolio, and differentiates core products such as cybersecurity.

AI’s importance was underscored by a Wall Street Journal report on Tuesday that Google co-founder Sergey Brin has been spotted at the company’s Mountain View, Calif., headquarters in recent weeks working with AI researchers on a large-scale project. Brin has been largely out of sight after stepping down from an executive role at parent company Alphabet in 2019.

This copy is for your personal, non-commercial use only. To order presentation-ready copies for distribution to your colleagues, clients or customers visit http://www.djreprints.com.

Shares of big tech companies have coasted through this year on AI euphoria, but as Microsoft Corp., Alphabet Inc. and Meta Platforms Inc. prepare to report results this week, some investors are starting to ask how much those AI advancements might actually cost.

Those questions have surfaced after several months during simply saying “AI” on earnings calls appeared to be enough for investors. If the economy sours though — as some expect in the second half of this year or next year — big tech’s AI ambitions could go with it.

“Given the exorbitant costs associated with the development, hosting and serving of AI products, many investors are concerned about the potential for [fiscal 2024] commentary regarding a material increase,” Jefferies analyst Brent Thill wrote, according to a MarketWatch earnings preview for Microsoft’s MSFT, -0.89%

results.

GOOG, +0.65%,

which both report on Tuesday, have been in heated competition in the world of online search and digital advertisements, as Microsoft leans more on its massive investments in research lab OpenAI to muscle up its own search capabilities. But a Deutsche Bank analyst said that so far, Google appears to have the upper hand in that battle.

Still, for Microsoft, after a broader pullback in IT spending earlier this year, analysts have found more to like about its cloud-computing business — namely market-share gains, generally-sturdy demand, and whatever ways AI can fit into the equation. Wolfe Research analyst Alex Zukin, in a recent note, said he believed “the focus will turn from what is good enough, to how good can it be,” as Microsoft moves deeper into AI.

“How good can it be?” might also be a question for Meta META, -2.73%,

which reports second-quarter results on Wednesday.

Shares of the social-media company have more than doubled in value so far this year. JMP analyst Andrew Boone, in a recent note, cited likely improvements in Meta’s digital ad segment, better engagement, and a broader advertising backdrop that “appears to be stable” after a slowdown in spending, Still, there are signs that the initial user attraction to Threads, Meta’s answer to Twitter, has fizzled.

Quick-service restaurant chains Chipotle Mexican Grill Inc. CMG, +0.20%

and McDonald’s Corp. MCD, -0.51%

also report, with BofA analysts expecting an “almost normal” quarter for the industry, after spending at chain restaurants grew last month and costs for some ingredients started to ease following two years of supply disruptions. Auto makers General Motors Co. GM, -1.81%

and Ford Motor Co. F, -0.71%

also report, and while parts shortages that have constrained vehicle production have shown signs of fading, so has electric-vehicle “euphoria.”

The calls to put on your calendar

Visa, Mastercard: Earlier this month executives from the big banks said U.S. consumers are generally doing OK despite still-rampant inflation, although perhaps less OK than in prior months. This week credit-card giants Visa Inc. and Mastercard Inc. report results on Tuesday and Thursday, respectively. The profit, sales and credit-card volume figures from Visa V, -0.15%

and Mastercard MA, -0.14%

will offer more specifics on consumer spending, as vacations and concerts compete with more expensive and more pressing needs, like groceries and other bills.

Shares of Visa and Mastercard are up so far this year, but some analysts said there could be more room investors to step in. SVB MoffettNathanson analyst Lisa Ellis recently said shares of both companies were hovering at “unusually attractive” levels.

The number to watch

Mattel outlook, and anything ‘Barbie’-related: The “Barbie” movie hit theaters nationwide on Friday. And after an epic marketing campaign, Mattel Inc.’s investors, banking on the film to drive a rebound for the toy maker during the second half of this year, will be zeroed in on the box-office results following the film’s debut on Friday.

Expectations for the film are huge. And when Mattel MAT, -0.42%

reports second-quarter results on Wednesday, executives could offer the first answers to some big questions: Has the film helped revive toy sales? Sales for anything else? Will the “Barbenheimer” effect help or hurt financials?

The film — directed by Greta Gerwig, written Gerwig and Noah Baumbach, and starring Margot Robbie and Ryan Gosling — brings together two writers with indie bona fides and two actors with mainstream starpower. Reviews so far have been favorable, and Barbie is already Mattel’s most profitable franchise. But the movie isn’t directly geared toward children, movie theaters have struggled to get back on track after pandemic lockdowns, and toy demand through this year has been weak after ballooning during the pandemic. And some analysts don’t expect “Barbie” to do much for Mattel’s stock.

Emily Bary and Jon Swartz contributed reporting to this story.

With the release this weekend of the new “Barbie” movie starring Margot Robbie and Ryan Gosling, there’s growing attention being paid to the world of Barbie collectibles. As in the hundreds of dolls that have been released over the years, to say nothing of such accessories as Barbie outfits and furniture.

But there’s one collectible above all — the holy grail of Barbies, if you will. We’re referring to Barbie No. 1, the first doll ever released by Mattel to bear the Barbie name, dating from 1959.

Barbie fanatics speak of it in reverent terms. “I lost sleep over this doll,” one collector said in a YouTube GOOGL, +0.69% GOOG, +0.65%

video that documented the arrival and unboxing of a Barbie No. 1.

Needless to say, collectors will pay a pretty penny for a Barbie No. 1. Prices can easily reach $10,000-plus, according to Barbie experts. The original doll sold for about $3, but there’s a Barbie No. 1 doll on eBay EBAY, -1.02% currently going for $25,000.

But before you plunk down five figures for an investment-grade doll, we figured you might want to know a little more about this one-of-a-kind Barbie. Here goes:

What makes the ‘Holy Grail’ Barbie so special?

Obviously, it’s all about being the first of its kind, not unlike a baseball player’s rookie card (the 1952 Mickey Mantle card is often considered the holy grail of sports collectibles, though that can sell for millions of dollars). It’s also about rarity. Experts say around 300,000 to 350,000 of those debut Barbies were sold in 1959, but the number of Barbie No. 1s that survived throughout the years — dolls are sold as toys, after all, not necessarily collectibles — is considerably less.

(Mattel MAT, -0.42%

reportedly now releases about 60 million Barbies annually, but the company didn’t respond to a MarketWatch request for comment and information.)

Are there any really rare examples of the original Barbie?

Red-headed Barbie No. 1s are known to exist. Marl Davidson, a Barbie dealer based in Bradenton, Fla., says she once sold one for $50,000, and perhaps the holiest of holy grails is a salesman’s Barbie sample case dating from the doll’s early years. Davidson says she believes only two or three are around. And one surfaced? “It could go for $1 million,” she says.

And what makes some Barbie No. 1s more valuable than others?

As with almost any collectible category, it’s all about condition. Barbie buyers are looking for a No. 1 that’s as close to mint condition as possible, with all the original items — namely, the box, black stand, sunglasses, shoes, brochure and zebra-striped swimsuit. (There are also outfits and accessories dating from Barbie’s early years, but these were sold separately; Verderame says a popular outfit from this period can sell for $150 to $200.)

Ironically, if the Barbie has stayed in the original box, it may affect the condition — Verderame explains that the packaging is acidic so it can “damage the piece over time,” but she says collectors still “want it in the box.”

Then, there’s the hair color. The original Barbie came in both blonde and brunette versions. Verderame says the blondes are generally more sought after since that’s what most people think of as the Barbie classic. But Davidson says brunettes can actually have value since there were fewer made of them. Then again, she says, the collectors “who can afford it will have one of everything.”

How can you tell if a first-edition 1959 Barbie is a fake?

There are various elements that will signify an original Barbie — most notably, a marking on the doll’s, um, right buttock (this also applies to later Barbies, though). Also look for holes in the feet and what the Doll Reference site describes as “tight curly bangs,” among other identifiers. It’s worth keeping in mind that you might find an original No. 1 doll, but with other parts that are not original — say, a replacement stand.

What’s the current market for the original Barbie?

It’s soaring because of the movie, Verderame says. She notes that Barbie No. 1s that went for $10,000 as recently as three months ago are now selling in the $15,000-$25,000 range. Verderame anticipates the market will cool off after the fervor for the Warner Bros. WBD, -1.37%

film dies down. But Davidson remains bullish on Barbie’s longer-term prospects because of the doll’s iconic appeal: “The price can only go up,” she says.

Are there any affordable alternatives to a first-edition Barbie?

Davidson says collectors can also consider Barbie No. 3 as a collectible. It’s a very early model, but it has a far more approachable price — Davidson says collectors can find one between $1,000 and $3,000.

If you want something way more affordable that still has potential to appreciate, Verderame says to consider iconic Barbies from the 1990s and 2000s that are currently selling for between $50 and $150.

But if you insist on a Barbie No. 1, Davidson says you can always buy one in lesser condition for a lesser price. Still, even a bald Barbie No. 1 won’t come cheap, she warns. “It’s going to go for a couple of grand,” she says.

Late on Wednesday, Tesla Inc. TSLA, -1.10%

reported that quarterly sales were up 47% from a year earlier. But the stock tumbled 10% on Thursday.

Tesla’s shares are still up 113% this year. The company is among a group of 13 in the S&P 500 that stand out with high growth expectations for sales, earnings and free cash flow through 2025.

But less than half of analysts polled by FactSet rate Tesla a buy. Emily Bary explains what they are worried about.

Chipotle Mexican Grill is among 14 stocks named by Michael Brush for consideration by investors looking to ride along with long-term improvement of U.S. labor productivity.

AP

The S&P 500 SPX, +0.03%

has returned 19% this year, following its 18% decline in 2022. On the same basis, with dividends reinvested, the benchmark index is still down 2% since the end of 2021.

The Dow Jones Industrial Average DJIA, +0.01%

is up 6% this year. The venerable index has trailed the S&P 500, but its closing level of 35,255.18 on Thursday was only 4% shy of its record close a 36,799.65 on Jan. 4, 2022. Joseph Adinolfi explains Dow Theory, which according to technical analysts is sending a strong bullish signal for the stock market.

Even if you have resisted the idea of a Roth IRA, you may soon be forced to have one

This year if you are age 50 or older and are already maxing-out your contribution to a 401(K), 403(B) or other qualified employer-sponsored tax-deferred retirement plan at $22,500, you can make an additional “catch up” tax deductible contribution of $7,500 for a total of $30,000. But starting in 2024, the catch up contribution will no longer be tax deductible if you earn at least $145,000 a year. You can still make the contribution with after-tax money into a Roth 401(K) account that your plan administrator may already have set up for you.

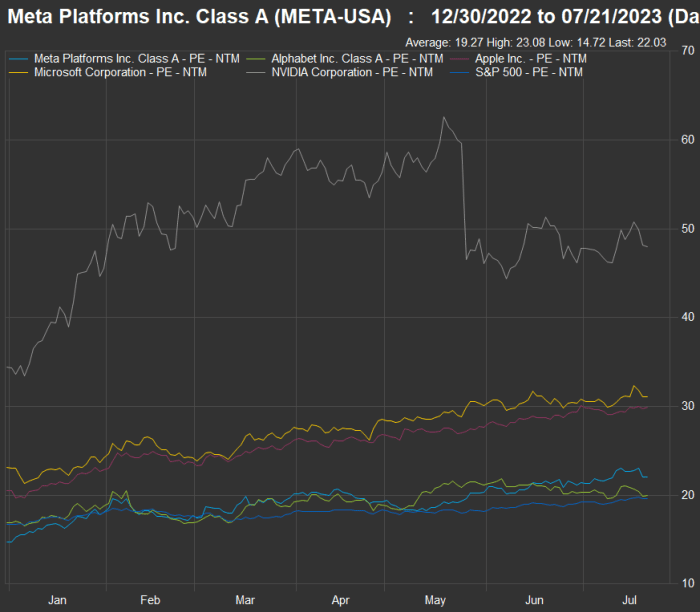

Shares of Meta Platforms Inc. and Alphabet Inc. trade only slightly higher than the S&P 500 on a forward price-to-earnings bases, while Nvidia Corp., Microsoft Corp. and Apple Inc. trade much higher.

FactSet

Leslie Albrecht looks at Meta Platforms Inc. META, -2.73%,

which is Facebook’s holding company and has a hit on its hands with the new Threads social-media platform, and Google holding company Alphabet Inc. GOOGL, +0.69%,

to consider which stock is a better buy.

In The Ratings Game column, MarketWatch reporters track analysts’ thoughts about various stocks. Here’s a sampling of this week’s coverage:

You don’t know every bad factor causing air travel to be nothing but harassment

Getting there is half the fun.

Getty Images

The U.S. flying scene — from shortages of equipment and labor (and runways) to ill-staffed air-traffic control towers — is a well-known nightmare for U.S. travelers. But there is more to the story. Jeremy Binckes looks into other factors that may surprise you and cause great inconvenience this summer.

The Federal Reserve is expected to raise interest rates again next week

The Federal Open Market Committee will meet next Tuesday and Wednesday, to be immediately followed by a policy announcement. Economists expect the central to raise the federal-funds rate by another quarter point. The question is whether or not this will end the Fed’s inflation-fighting rate cycle.

How much would you pay for 100% downside protection in the stock market?

MarketWatch illustration/iStockphoto

Over the past 30 years, the SPDR S&P 500 ETF Trust SPY,

has returned 1,650%, for an average annual return of 10%, with dividends reinvested, according to FactSet. But it hasn’t been a smooth ride. The ETF, which tracks the benchmark S&P 500, fell 18% last year and 37% during 2008, for example. And there have been even larger declines if the analysis isn’t confined to calendar years.

But can you ride through market declines? Many studies have shown that most investors who try to time the market sell after a decline has started and buy back in well after a recovery is under way, which means their long-term performance can suffer significantly.

In this week’s ETF Wrap column (and emailed newsletter), Isabel Wang describes a new buffered fund that can give you 100% downside protection over a two-year period, in return for a cap on your potential gains in the stock market. Here’s the price you would pay for the protection.

The World Cup games have started

Hannah Wilkinson scored the home team’s first goal against Norway during the first World Cup game in Auckland, New Zealand, on July 20.

Getty Images

The Women’s World Cup began Thursday with an upset victory by New Zealand over Norway.

James Rogers reports on what is expected to be a much easier environment for FIFA and corporate sponsors than that of last year’s Men’s World Cup in Qatar.

U.S. Soccer Federation President Cindy Parlow Cone participated in MarketWatch’s Best New Ideas in Money podcast and spoke about the long-term effort to achieve equal treatment for women soccer players.

More coverage of the World Cup:

Want more from MarketWatch? Sign up for this and other newsletters to get the latest news and advice on personal finance and investing.

Yahoo, an early trailblazer of the Internet boom, is “very profitable,” and ready to return to public markets via an initial public offering.

That’s according to Chief Executive Jim Lanzone, who made the comment in an interview with the Financial Times published Tuesday. Yahoo soared to prominence in the 1990s, rising in the public consciousness alongside its share price — under the ticker symbol “YHOO” — during the dot-com boom.

Apollo Funds purchased the Yahoo business from Verizon Communications Inc. VZ, +0.24%

in 2021.

The web services provider, which competes with the likes of Google parent Alphabet Inc. GOOGL, +0.17% and Facebook parent Meta Platforms Inc. META, -0.33%,

said earlier this year that more than 20% of its workforce would be laid off. At the time, Lanzone reportedly said that the cuts would be made in an unprofitable area of its business but that they would be “tremendously beneficial” to the company overall.

“Whether it’s finance, or sports or news, that’s still what we do, and why we’re No. 1, or No. 2, in all these important categories all these years later,” Lanzone reportedly told the FT. “While the company has had struggles [at] different points in time, we’re still huge in traffic, and we have our best days ahead of us productwise.”

He said Yahoo would be aggressively looking at the chance to build businesses in related sectors via M&A — it recently bought Wagr, a sports-betting app. While Yahoo is still “too small” to take on Google and Microsoft’s MSFT, -0.75%

search engine Bing, Lanzone said he’s optimistic, and also sees AI offering up new opportunities for the company.

Meta Platforms Inc.’s answer to Twitter is poised to launch, according to a new report, as Elon Musk’s faltering microblogging app struggles to hold onto advertisers and over the weekend placed restrictions on posts viewed by users.

The Wall Street Journal reported late Monday that Meta’s META, -0.33%

Threads will be released Thursday, and is expected to be built off of Instagram user data, giving it the potential to catch on and grow quickly.

Bloomberg News also reported it would launch Thursday, citing a listing on Apple Inc.’s AAPL, -0.78%

App Store.

Threads allows users to port their Instagram username to a new platform that essentially opens direct-message chats on a more public forum. The Facebook parent company has been developing a text-based platform for some time.

Twitter, meanwhile, continues to seek ways to stem hemorrhaging advertising under new Chief Executive Linda Yaccarino as it puts a stranglehold on what subscribers can view. In a tweet Saturday, Musk — who acquired Twitter for $44 billion in October — said verified accounts were at one point limited to reading 6,000 posts a day. For unverified accounts, the number was 600 posts a day, while new account could only see 300. That number was later upgraded to 10,000, 1,000 and 500, respectively.

Animosity between Musk and Meta co-founder and Chief Executive Mark Zuckerberg has been growing as the Twitter-rival app gets closer to market, culminating in Musk’s cage-fight challenge to Zuckerberg last month.

The heads of prominent U.S. and Indian companies will meet at the White House on Friday with President Joe Biden and Indian Prime Minister Narendra Modi to discuss investment in areas including artificial intelligence.

Those attending include Sam Altman, CEO of OpenAI, as well as Apple AAPL, +0.04%

CEO Tim Cook and Google GOOG, -0.49%

GOOGL, -0.41%

CEO Sundar Pichai. Indian company executives include Mukesh Ambani, chair of Reliance Industries, and Anand Mahindra, chair of Mahindra Group.

“The president and Prime Minister Modi of the Republic of India will meet with senior officials and CEOs of American and Indian companies gathered to discuss innovation, investment, and manufacturing in a variety of technology sectors, including AI, semiconductors, and space,” the White House said.

Friday’s meeting is part of Modi’s high-profile visit to Washington, which included a state dinner at the White House and the announcement of a number of business deals.

Nvidia Corp. headed toward market-capitalization gains of nearly $200 billion in after-hours trading Wednesday, which could put the chip maker within sight of becoming only the seventh U.S. company to top a valuation of $1 trillion.

Nvidia ended Wednesday’s session with a market cap — the total value of all shares in existence — of roughly $754.3 billion, according to FactSet. A 25% increase would add nearly $189 billion to that total, putting the company within striking distance of $1 trillion. Only six U.S. companies have ever attained a $1 trillion market cap: Apple Inc. AAPL, +0.16%

and Microsoft Corp. MSFT, -0.45%

are currently worth more than $2 trillion apiece; Google parent Alphabet Inc. GOOGL, -1.35%

and Amazon.com Inc. AMZN, +1.53%

have valuation of more than $1 trillion; and Facebook parent Meta Platforms Inc. META, +1.00%

and Tesla Inc. TSLA, -1.54%

have both touched the $1 trillion plateau previously.

Nvidia’s market cap was ahead of both Meta and Tesla as of Wednesday’s close, with both worth less than $650 billion, showing the potential fleeting nature of such a valuation. Nvidia’s record market cap is $834.4 billion, established on Nov. 29. 2021, according to Dow Jones Market Data.

If Nvidia’s gains hold through Thursday’s trading session, the company could challenge for the largest one-day market-cap gain in history. The biggest currently on record was Amazon’s $191.2 billion increase on Feb. 4, 2022, according to Dow Jones Market Data, followed closely by a $190.9 billion gain by Apple on Nov. 10, 2022. Nvidia also stands to gain more than rival Advanced Micro Devices Inc. AMD, +0.14%

is worth in total — AMD ended Wednesday’s session with a market cap of $174.4 billion.

Nvidia is closing in on the rare $1 trillion plateau because of huge gains in its stock this year, as hopes and hype about generative AI have flooded the tech sector. After OpenAI debuted its ChatGPT AI offering, and investor Microsoft quickly integrated the chatbot into many of its services, expectations for the technology have exploded.

Despite the hype, most companies have avoided providing hard figures for revenue gains expected from AI. Nvidia’s fiscal second-quarter forecast — which calls for roughly $11 billion in sales, nearly 33% higher than Nvidia’s previous quarterly record of $8.28 billion — could be seen as the first sign of a wave of fresh spending coursing through the tech sector.

Other companies have indicated that they will be forced to spend to develop their technology before reaping large financial rewards from it. Microsoft, for example, disclosed to investors last month that capital expenditures are increasing as it builds AI capabilities into its Azure cloud-computing platform — spending that is largely going toward Nvidia.

That is a rather typical path for large jumps in tech spending: Companies that make the necessary hardware see gains before the companies that use that gear can develop offerings that take advantage of it. Other gear makers joined Nvidia in the sharp move higher in after-hours trading Wednesday, including AMD, which gained more than 10%; chip maker Marvell Technology Inc. MRVL, -1.31%,

which increased more than 5%; and networking specialist Arista Networks Inc. ANET, +0.53%,

which added about 5%.

Alphabet and Microsoft stocks both increased around 2% in after-hours trading, and software companies that have made AI a core part of their offerings also saw gains. Palantir Technologies Inc. PLTR, -3.24%

and C3.ai Inc. AI, +2.54%

shares both increased more than 8%, for example.

Nvidia Corp. executives predicted record revenue well beyond anything the company has experienced Wednesday, pushing shares toward all-time highs, as margins improve with AI-driven data-center sales.

Nvidia NVDA, -0.49%

guided for second-quarter revenue of $11 billion, plus or minus 2%; the chip maker has never before reported quarterly revenue higher than $8.29 billion, which it hit in the fiscal first quarter a year ago. Analysts on average were expecting $7.17 billion, according to FactSet, a gain from the $6.7 billion in sales Nvidia put up in the fiscal second quarter last year.

On the conference call with analysts, Huang said the simple way to think about it is that the world has “a trillion dollars of data center installed and it used to be 100% CPU,” or central processing units, as opposed to Nvidia’s graphics processors that data centers and AI models have embraced in recent years. And while the world’s data-center budget is strapped, at the same time larger and larger AI models require more and more computing power, he said.

“The easiest way to think about that is over the next four or five, 10 years, most of that trillion dollars, and compensating adjusting for all the growth in data center still, it will be largely generative AI,” Huang said.

“What happened is, when generative AI came along, it triggered a killer app for this computing platform that’s been in preparation for some time,” he added.

The company forecast adjusted gross margins of 70% for the second quarter, after reporting 66.8% for the first quarter, not only as higher data-center margins counter the deficit in gaming, but as Nvidia Chief Financial Officer Colette Kress said on the call: ” We believe the channel inventory correction is behind us.”

Shares soared more than 25% in after-hours trading, following a 0.5% decline in the regular session to $305.38. Nvidia’s record closing price is $333.76 and the all-time intraday high is $346.47, according to FactSet data. After-hours “prices” topped both of those marks, reaching more than 14% beyond all-time highs for the regular session, as shares registered as high as $395, according to FactSet. The last time Nvidia shares rallied as much in a single session was Nov. 11, 2016, when shares surged 29.8% after the company reported that profit more than doubled.

Meanwhile, shares of rival Advanced Micro Devices Inc. AMD, +0.14%

rallied 6% after hours.

Nvidia did not provide full-year guidance, but Chief Executive Jensen Huang has been effusive in his predictions that increased focus on AI from Big Tech partners such as Microsoft Corp. MSFT, -0.45%

and Alphabet Inc. GOOGL, -1.35% GOOG, -1.34%

will lead to revenue gains in the near future. Speaking to the media at Nvidia’s developers conference in March, he said that generative AI has only accounted for a “tiny, tiny, tiny” single-digit percentage of revenue over the past 12 months, but predicted that in the next year, revenue from generative AI will grow to be “quite large — exactly how large, it’s hard to say.”

Nvidia reported fiscal first-quarter earnings of $2.04 billion, or 82 cents a share, on sales of $7.19 billion, a decline from $8.29 billion a year ago but well ahead of expectations. After adjusting for stock compensation and other effects, the chip maker reported earnings of $1.09 a share, a decline from $1.36 a share a year ago. Analysts on average were expecting adjusted earnings of 92 cents a share on sales of $6.53 billion, according to FactSet.

Gaming sales for the first quarter fell 38% to $2.24 billion, while data-center sales at Nvidia rose 14% to a record $4.28 billion, “led by growing demand for generative AI and large language models using GPUs based on our Nvidia Hopper and Ampere architectures.”

“The revenue growth reflects strong demand from large consumer internet companies and cloud service providers,” the company said in a statement. “Enterprise demand for GPU platforms was strong, although general purpose networking solutions declined both sequentially and from a year ago.”

Analysts had expected gaming sales of $1.97 billion — nearly half of last year’s $3.62 billion — and data-center sales of $3.9 billion, a 4% increase from a year ago. Auto chip sales soared 114% to $296 million from a year ago.

Nvidia’s profit and sales have declined in recent quarters as the company deals with oversupply in the market, a result of pandemic-era shortages flipping to a glut after demand for personal computers and gaming gear waned. Analysts expect that trend to end with this report, however, as demand for gear that can power artificial intelligence kicks into higher gear amid a bevy of promises from tech companies about the power of generative AI.

When investors think of technology stocks, they might automatically gravitate toward “the next big thing,” or to the giant companies that dominate the S&P 500 SPX, -0.40%.

But Robert Stimson, chief investment officer of Oak Associates Funds, makes a case for diversification through exposure to smaller innovators which he believes are “overlooked in this environment.”

The River Oak Discovery Fund RIVSX, +0.98%

invests in tech-oriented companies with market capitalizations of $5 billion or less, with an average of about $2 billion. It has a five-star rating, the highest, from Morningstar, despite having what the investment information firm considers “above average” annual expenses of 1.19% of assets under management. The fund is ranked in the 6th percentile among 546 funds in Morningstar’s “Small Blend” category for five-year performance and in the 13th percentile among 374 funds for 10-year performance. The performance comparisons are net of expenses.

The Black Oak Emerging Technologies Fund BOGSX, +1.54%

has more of a midcap focus, with some small-cap stocks and follows a similar strategy to that of RIVSX. But with no restriction on the size of companies this fund invests in, “we don’t have to sell stocks,” Stimpson said. So long-term holdings of this fund include Apple Inc. AAPL, -0.05%

and Salesforce.com Inc. CRM, +0.69%.

This fund is rated three stars within Morningstar’s “Technology” category and has a lower expense ratio of 1.03%.

Both funds are concentrated. The River Oak Discovery Fund held 34 stocks and the Black Oak Emerging Technologies Fund held 35 stocks as of March 31. Lists of both funds’ largest holdings are below.

During an Interview, Stimpson, who co-manages both funds, said that when investing in the small-cap technology space, he and colleagues identify companies that are “focused on niches.

“I want a company that knows who they are, what they do and do it well, rather than a small company trying to growing into the next Microsoft, Google or Salesforce,” he said.

Stimpson said Oak Associates pays close attention to what corporate management teams say during earnings calls and in presentations, preferring comments related to improving sales and operations with a market niche, rather than expressions of grand visions for exponential growth.

That type of narrow focus can support higher valuations over time, Stimpson said. “They have better execution, a better ability to fend-off competition and they are quality acquisition candidates.”

“ “I caution everyone that until there is revenue, earnings and a product, the hype can be more dangerous than an opportunity.” ”

— Robert Stimpson, chief investment officer at Oak Funds, when discussing AI and ChatGPT.

All of those factors can be important to investors, considering how easily tech giants such as Microsoft Corp. MSFT, +1.00%

or Google holding company Alphabet Inc. GOOGL, +2.89%

GOOG, +2.88%

can begin to compete with smaller innovative companies because they can afford to make such large investments, he said.

Simpson went further, saying that when running screens for “quality” metrics, such as improving free cash flow yields, the Oak Associates team also looks for “shareholder friendly practices.” For example, a company may be repurchasing shares. But are the buybacks lowering the share count significantly (which boosts earnings per share) or are they merely mitigating the dilution caused by the shoveling of new shares to executives as part of their compensation?

Finally, Simpson cautioned investors not to get caught up in tech-focused hype.

“When I talk to our clients, I get questions about AI and ChatGPT and how to play it. People get focused on a new great tech innovation,” he said. “You can replace ChatGPT with bitcoin, metaverse or 3-D printing.”

“I caution everyone that until there is revenue, earnings and a product, the hype can be more dangerous than an opportunity.”

Two examples

These companies are held by theRiver Oak Discovery Fund and the Black Oak Emerging Technologies Fund.

Cirrus Logic Inc. CRUS, -2.37%

is the largest holding of the River Oak Discovery Fund. Stimpson calls the company “a derivative play on the success of Apple.”

“They are focused on the chips that go into mobile and [vehicles],” as well as the needs of their customers, including Apple, “rather than problem areas of the chip sector, such as memory or PCs. They are not talking about chips for AI, for example,” Stimpson said.

Cirrus focuses on systems and related software used in audio systems..

Kulicke & Soffa Industries Inc. KLIC, +1.92%

makes equipment, tools and related software used by a variety of manufacturers of computer chips and integrated electronic devices.

Stimpson likes the company as a long-term play on the worldwide disruption in semiconductor manufacturing and supply, in the wake of the Covid-19 pandemic. “All chip companies learned that any supply disruption in Southeast Asia is a problem. Over time, the opportunities for semiconductor equipment makers are very good. There will be more plants in more locations, so more equipment,” he said.

He said KLICK was in a “protected” position, with returns on equity of about 20% and free cash flow yields of about 10%.

Top holdings of the funds

Here are the largest 10 holdings of the River Oak Discovery Fund as of March 31:

The market capitalization of Apple Inc. has surpassed that of the entire Russell 2000for two weeks, the longest stretch on record, according to Bloomberg data.

Apple’s market capitalization,which measures how much the company is worth based on the value of all its outstanding stock, surpassed that of the Russell 2000 RUT, +1.19%

on April 27 and has held higher through Monday. The only other time that occurred was Sept. 1, 2020, when Apple’s valuation passed that of the small-cap index for only a day.

Apple’s premium over this group of small-cap stocks continued to widen over the past two weeks as the consumer-technology giant reported earnings that surpassed Wall Street analysts’ expectations.

With a market capitalization of roughly $2.7 trillion, Apple is now worth roughly $100 billion more than the combined value of all 2,000 stocks in the Russell 2000, according to Bloomberg data shared with MarketWatch.

To be sure, the gap narrowed somewhat on Monday as Apple shares declined by 0.4% to $171.80, while the Russell 2000 gained 1.3% to trade at 1,763.

A team of stock-market analysts from Bespoke Investment Group illustrated the trend in a chart shared on Twitter Monday.

U.S. equity benchmarks have powered higher in 2023, but some say the strength in popular indexs like the S&P 500 and Nasdaq Composite has masked weakness in other corners of the market.

Both the S&P 500, which has risen more than 7% year-to-date, and the Nasdaq Composite, which has risen nearly 18%, owe the bulk of their gains to a handful of megacap technology stocks including Apple, Microsoft Corp. MSFT, +0.16%,

Alphabet Inc. GOOG, -0.81%

and Nvidia Corp. NVDA, +2.16%

The top 10 stocks in the S&P 500 hold a 29% weight in the index, and have been responsible for around 70% of its year-to-date performance gains, according to a MarketWatch report from last week.

The Russell 2000, meanwhile, is essentially unchanged since the start of 2023. Apple, by comparison, has risen more than 32% since Jan. 1, according to FactSet data. The relative weakness in small-caps has inspired discussion about whether this might be a buying opportunity, as market strategists told Barron’s.

Small-caps have struggled against a plethora of headwinds since the start of 2023. Shrinking corporate earnings, a string of regional-bank failures and signs of a looming recession have taken a heavy toll. Facing so much uncertainty, equity investors have sought safety in shares of megacap technology names this year following a punishing selloff in 2022.

“It is pretty incredible that one company could overtake an entire universe of small-cap stocks in terms of size,” said Callie Cox, U.S. equity strategist at eToro, during a phone interview with MarketWatch. “To me, it really speaks to how beaten down small-caps are.”

When Apple reported earnings for the quarter ended in March last week, the company’s management revealed a surprise growth in its iPhone business, which helped to overcoming a shortfall in Mac revenue. The company also promised investors billions more in dividends and stock repurchases, which helped to boost the stock price. Apple’s shares traded higher in response.

Vice President Kamala Harris will host the chief executives of Alphabet GOOG GOOGL, Microsoft MSFT, OpenAI and Anthropic at the White House on Thursday to discuss artificial-intelligence issues.

Harris and senior administration officials aim to have a “frank discussion” of the risks in AI development and of “ways we can work together to ensure the American people benefit from advances in AI while being protected from its harms,” according to an invitation for the meeting obtained by MarketWatch.