LONDON — The Bank of England made its biggest interest rate increase in three decades Thursday, joining the U.S. Federal Reserve and other central banks worldwide in rapid hikes as it tries to beat back stubbornly high inflation fueled by Russia’s invasion of Ukraine and the disastrous economic policies of former Prime Minister Liz Truss.

The central bank boosted its key rate by three-quarters of a percentage point, to 3%, after consumer price inflation returned to a 40-year high in September. The aggressive move comes even as the bank predicted a two-year economic contraction through June 2024, which would be the longest recession since at least 1955, according to the Office for National Statistics.

“If we don’t take action to bring inflation down, it gets worse,” Bank of England Gov. Andrew Bailey told reporters. “There’s no easy outcome in this sense.”

Even so, the central bank should not increase its key rate too far, he said, but with uncertainties ahead, policymakers will “respond forcefully” if needed.

The interest rate decision is the first since Truss’ government announced 45 billion pounds ($52 billion) of unfunded tax cuts that sparked turmoil on financial markets, pushed up mortgage costs and forced Truss from office after just six weeks. Her successor, Rishi Sunak, has warned of spending cuts and tax increases as he seeks to undo the damage and show that Britain is committed to paying its bills.

“High energy, food and other bills are hitting people hard. Households have less to spend on other things. This has meant that the size of the UK economy has started to fall,” the bank said in its November monetary policy report.

The rate increase is the Bank of England’s eighth in a row and the biggest since 1992. It comes after the U.S. Federal Reserve on Wednesday announced a fourth consecutive three-quarter point jump as central banks worldwide combat inflation that is eroding living standards and slowing economic growth.

Central banks have struggled to contain inflation after initially believing that price increases were being fueled by international factors beyond their control. Their response intensified in recent months as it became clear that inflation was becoming embedded in the economy, feeding through into higher borrowing costs and demands for higher wages.

The war in Ukraine boosted food and energy prices worldwide as shipments of natural gas, grain and cooking oil were disrupted. That added to inflation that began to accelerate last year when the global economy began to recover from the COVID-19 pandemic.

Europe has been particularly hard hit by a jump in natural gas prices as Russia responded to Western sanctions and support for Ukraine by curtailing shipments of the fuel used to heat homes, generate electricity and power industry and European nations competed for alternative supplies on global markets.

The U.K. also has struggled as wholesale gas prices increased fivefold in the 12 months through August. While prices have dropped more than 50% since the August peak, they are likely to rise again during the winter heating season, worsening inflation.

The British government sought to shield consumers with a cap on energy prices. But after the turmoil caused by Truss’ economic policies, Treasury chief Jeremy Hunt limited the price cap to six months instead of two years, ending on March 31.

Meanwhile, food prices have jumped 14.6% in the year through September, led by the soaring cost of staples such as meat, bread, milk and eggs, the Office for National Statistics said. That pushed consumer price inflation back to 10.1%, the highest since early 1982 and equal to the level last reached in July.

Increases in the cost of tea bags, milk and sugar mean that even the “humble” cup of tea, which people across the country turn to when they need a break from the pressures of daily life, is getting more expensive, the British Retail Consortium said Wednesday.

“While some supply chain costs are beginning to fall, this is more than offset by the cost of energy, meaning a difficult time ahead for retailers and households alike,” said Helen Dickinson, the consortium’s chief executive.

Truss’ failed economic plan made things worse, driving the pound to a record low against the dollar, threatening the stability of some pension funds and triggering predictions that the Bank of England would boost interest rates higher than expected. That increased mortgage costs as lenders repriced their products.

The economic turmoil is putting homeownership further out of reach for many young people, according to research released this week by Hamptons, a U.K. real estate agency.

Mortgage rates average around 6.5%, compared with 2% a year ago.

That means the average first-time homebuyer would have to make a down payment equal to 41% of the purchase price to keep their monthly repayments at the same level as a similar buyer who made a 10% down payment last year, Hamptons said.

The Federal Reserve raised interest rates by three-quarters of a point in their sixth increase this year. Jerome H. Powell, the Fed chair, said “at some point” it would be appropriate to slow the pace of increases.

Inflation in Turkey rose for the 17th consecutive month in October, hitting 85.5% year-on-year as food and energy prices continued to climb, according to official figures.

Food prices were 99% higher than the same period last year, housing rose by 85% and transport was up 117%, the Turkish Statistical Institute reported Thursday.

The domestic producer price index shows a 157.69% increase annually and was up 7.83% on a monthly basis. The monthly rise in consumer prices was 3.54%.

The dramatic rise in living costs for the country of 85 million has continued unabated for nearly two years, in tandem with significant devaluation of Turkey’s currency, the lira.

Controversially, Turkish President Recep Tayyip Erdogan refuses to raise interest rates, insisting that it would harm the economy. Economists and critics say his policies have continued to hurt the lira and push inflation up, fomenting a currency crisis.

Turkey’s central bank on Oct. 20 slashed its key interest rate by 150 basis points for the third consecutive month of cuts, from 12% to 10.5% — despite Turkish inflation at more than 83% at the time.

Erdogan says the cuts are pro-growth, and that they will continue. The president remains determined to get the country’s interest rate down to single digits by the end of this year.

“My biggest battle is against interest. My biggest enemy is interest. We lowered the interest rate to 12%,” the president said during an event in late September. “Is that enough? It is not enough. This needs to come down further.”

Turkey’s central bank “will remain under pressure from President Erdogan for looser policy,” Liam Peach, senior emerging markets economist at London-based Capital Economics, wrote in an analyst note after the data was released.

He added that “although the CBRT [Central Bank of the Republic of Turkey] said it will deliver one more 150bp interest rate cut at its meeting later this month, there is a risk of further easing beyond that, adding more downward pressure onto the lira.”

The lira was trading roughly flat on the day at 18.61 to the dollar. It’s lost more than 28% of its value against the greenback year-to-date and nearly 50% in the last full year.

The Federal Reserve raised its benchmark interest rate by three-quarters of a point as it seeks to ease inflation. Robert Costa reports on the impact it could have on the midterm elections.

Be the first to know

Get browser notifications for breaking news, live events, and exclusive reporting.

LIVERPOOL, England — On the long picket line outside the gates of Liverpool’s Peel Port, rain-soaked dock workers warm themselves with cups of tea as they listen to 1980s pop.

Dozens of buses, cars and trucks honk in solidarity as they pass.

Dockers’ strikes are not new to Liverpool, nor is depravation. But this latest walk-out at Britain’s fourth-largest port is part of something much bigger, a great wave of public and private sector strikes taking place across the U.K. Railways, postal services, law courts and garbage collections are among the many public services grinding to a halt.

The immediate cause of the discontent, as elsewhere, is the rising cost of living. Inflation in the United Kingdom breached the 10 percent mark this year, with wages failing to keep pace.

But the U.K.’s economic woes long predate the current crisis. For more than a decade, Britain has been beset by weak economic growth, anaemic productivity, and stagnant private and public sector investment. Since 2016, its political leadership has been in a state of Brexit-induced flux.

Half a century after U.S. Secretary of State Henry Kissinger looked at the U.K.’s 1970s economic malaise and declared that “Britain is a tragedy,” the United Kingdom is heading to be the sick man of Europe once again.

The immediate cause of Liverpool dockers’ discontent that brought them to strike is the rising cost of living. | Christopher Furlong/Getty Images

Here in Liverpool, the “scars run very deep,” said Paul Turking, a dock worker in his late 30s. British voters, he added, have “been misled” by politicians’ promises to “level up” the country by investing heavily in regional economies. Conservatives “will promise you the world and then pull the carpet out from under your feet,” he complained.

“There’s no middle class no more,” said John Delij, a Peel Port veteran of 15 years. He sees the cost-of-living crisis and economic stagnation whittling away the middle rung of the economic ladder.

“How many billionaires do we have?” Delij asked, wondering how Britain could be the sixth-largest economy in the world with a record number of billionaires when food bank use is 35 percent above its pre-pandemic level. “The workers put money back into the economy,” he said.

What would they do if they were in charge? “Invest in affordable housing,” said Turking. “Housing and jobs.”

Falling behind

The British economy has been struck by particular turbulence over recent weeks. The cost of government borrowing soared in the wake of former PM Liz Truss’ disastrous mini-budget on September 23, with the U.K.’s central bank forced to step in and steady the bond markets.

But while the swift installation of Rishi Sunak, the former chancellor, as prime minister seems to have restored a modicum of calm, the economic backdrop remains bleak. Spending and welfare cuts are coming. Taxes are certain to rise. And the underlying problems cut deep.

U.K. productivity growth since the financial crisis has trailed that of comparator nations such as the U.S., France and Germany. As such, people’s median incomes also lag behind neighboring countries over the same period. Only Russia is forecast to have worse economic growth among the G20 nations in 2023.

In 1976, the U.K. — facing stagflation, a global energy crisis, a current account deficit and labor unrest — had to be bailed out by the International Monetary Fund. It feels far-fetched, but today some are warning it could happen again.

The U.K. is spluttering its way through an illness brought about in part through a series of self-inflicted wounds that have undermined the basic pillars of any economy: confidence and stability.

The political and economic malaise is such that it has prompted unwanted comparisons with countries whose misfortunes Britain once watched amusedly from afar.

“The existential risk to the U.K. … is not that we’re suddenly going to go off an economic cliff, or that the country’s going to descend into civil war or whatever,” said Jonathan Portes, professor of economics at King’s College London. “It’s that we will become like Italy.”

Portes, of course, does not mean a country blessed with good weather and fine food — but an economy hobbled by persistently low growth, caught in a dysfunctional political loop that lurches between “corrupt and incompetent right-wing populists” and “well-intentioned technocrats who can’t actually seem to turn the ship around.”

“That’s not the future that we want in the U.K,” he said.

Reviving the U.K.’s flatlining economy will not happen overnight. As Italy’s experience demonstrates, it’s one thing to diagnose an illness — another to cure it.

Experts speak of an unbalanced model heavily reliant upon Britain’s services sector and beset with low productivity, a result of years of underinvestment and a flexible labor market which delivers low unemployment but often insecure and low-paid work.

“We’re not investing in skills; businesses aren’t investing,” said Xiaowei Xu, senior research economist at the Institute for Fiscal Studies. “It’s not that surprising that we’re not getting productivity growth.”

But any attempt to address the country’s ailments will require its economic stewards to understand their underlying causes — and those stretch back at least to the first truly global crisis of the 21st century.

Crash and burn

The 2008 financial crisis hammered economies around the world, and the U.K. was no exception. Its economy shrunk by more than 6 percent between the first quarter of 2008 and the second quarter of 2009. Five years passed before it returned to its pre-recession size.

For Britain, the crisis in fact began in September 2007, a year before the collapse of Lehman Brothers, when wobbles in the U.S. subprime mortgage market sparked a run on the British bank Northern Rock.

The U.K. discovered it was particularly vulnerable to such a shock. Over the second half of the 20th century, its manufacturing base had largely eroded as its services sector expanded, with financial and professional services and real estate among the key drivers. As the Bank of England put it: “The interconnectedness of global finance meant that the U.K. financial system had become dangerously exposed to the fall-out from the U.S. sub-prime mortgage market.”

The crisis was a “big shock to the U.K.’s broad economic model,” said John Springford, from the Centre for European Reform. Productivity took an immediate hit as exports of financial services plunged. It never fully recovered.

“Productivity before the crash was basically, ‘Can we create lots and lots of debt and generate lots and lots of income on the back of this? Can we invent collateralized debt obligations and trade them in vast volumes?’” said James Meadway, director of the Progressive Economy Forum and a former adviser to Labour’s left-wing former shadow chancellor, John McDonnell.

A post-crash clampdown on City practises had an obvious impact.

“This is a major part of the British economy, so if it’s suddenly not performing the way it used to — for good reasons — things overall are going to look a bit shaky,” Meadway added.

The shock did not contain itself to the economy. In a pattern that would be repeated, and accentuated, in the coming years, it sent shuddering waves through the country’s political system, too.

The 2010 election was fought on how to best repair Britain’s broken economy. In 2009, the U.K. had the second-highest budget deficit in the G7, trailing only the U.S., according to the U.K. government’s own fiscal watchdog, the Office for Budget Responsibility (OBR).

The Conservative manifesto declared “our economy is overwhelmed by debt,” and promised to close the U.K.’s mounting budget deficit in five years with sharp public sector cuts. The incumbent Labour government responded by pledging to halve the deficit by 2014 with “deeper and tougher” cuts in public spending than the significant reductions overseen by former Conservative Prime Minister Margaret Thatcher in the 1980s.

The election returned a hung parliament, with the Conservatives entering into a coalition with the Liberal Democrats. The age of austerity was ushered in.

Austerity nation

Defenders of then-Chancellor George Osborne’s austerity program insist it saved Britain from the sort of market-led calamity witnessed this fall, and put the U.K. economy in a condition to weather subsequent global crises such as the COVID-19 pandemic and the fallout from the war in Ukraine.

“That hard work made policies like furlough and the energy price cap possible,” said Rupert Harrison, one of Osborne’s closest Treasury advisers.

Pointing to the brutal market response to Truss’ freewheeling economic plans, Harrison praised the “wisdom” of the coalition in prioritizing tackling the U.K.’s debt-GDP ratio. “You never know when you will be vulnerable to a loss of credibility,” he noted.

But Osborne’s detractors argue austerity — which saw deep cuts to community services such as libraries and adult social care; courts and prisons services; road maintenance; the police and so much more — also stripped away much of the U.K.’s social fabric, causing lasting and profound economic damage. A recent study claimed austerity was responsible for hundreds of thousands of excess deaths.

Under Osborne’s plan, three-quarters of the fiscal consolidation was to be delivered by spending cuts. With the exception of the National Health Service, schools and aid spending, all government budgets were slashed; public sector pay was frozen; taxes (mainly VAT) rose.

But while the government came close to delivering its fiscal tightening target for 2014-15, “the persistent underperformance of productivity and real GDP over that period meant the deficit remained higher than initially expected,” the OBR said. By his own measure, Osborne had failed, and was forced to push back his deficit-elimination target further. Austerity would have to continue into the second half of the 2010s.

Many economists contend that the fiscal belt-tightening sucked demand out of the economy and worsened Britain’s productivity crisis by stifling investment. “That certainly did hit U.K. growth and did some permanent damage,” said King’s College London’s Portes.

“If that investment isn’t there, other people start to find it less attractive to open businesses,” former Labour aide Meadway added. “If your railways aren’t actually very good … it does add up to a problem for businesses.”

A 2015 study found U.K. productivity, as measured by GDP per hour worked, was now lower than in the rest of the G7 by a whopping 18 percentage points.

“Frankly, nobody knows the whole answer,” Osborne said of Britain’s productivity conundrum in May 2015. “But what I do know is that I’d much rather have the productivity challenge than the challenge of mass unemployment.”

‘Jobs miracle’

Rising employment was indeed a signature achievement of the coalition years. Unemployment dropped below 6 percent across the U.K. by the end of the parliament in 2015, with just Germany and Austria achieving a lower rate of joblessness among the then-28 EU states. Real-term wages, however, took nearly a decade to recover to pre-crisis levels.

Economists like Meadway contend that the rise in employment came with a price, courtesy of Britain’s famously flexible labor market. He points to a Sports Direct warehouse in the East Midlands, where a 2015 Guardian investigation revealed the predominantly immigrant workforce was paid illegally low wages, while the working conditions were such that the facility was nicknamed “the gulag.”

The warehouse, it emerged, was built on a former coal mine, and for Meadway the symbolism neatly charts the U.K.’s move away from traditional heavy industry toward more precarious service sector employment. “It’s not a secure job anymore,” he said. “Once you have a very flexible labor market, the pressure on employers to pay more and the capacity for workers to bargain for more is very much reduced.”

Throughout the period, the Bank of England — the U.K.’s central bank — kept interest rates low and pursued a policy of quantitative easing. “That tends to distort what happens in the economy,” argued Meadway. QE, he said, is a “good [way of] getting money into the hands of people who already have quite a lot” and “doesn’t do much for people who depend on wage income.”

Meanwhile — whether necessary or not — the U.K.’s austerity policies undoubtedly worsened a decades-long trend of underinvestment in skills and research and development (Britain lags only Italy in the G7 on R&D spending). At British schools, there was a 9 percent real terms fall in per-pupil spending between 2009 and 2019, according to the Institute for Fiscal Studies’ Xu. “As countries get richer, usually you start spending more on education,” Xu noted.

Two senior ministers in the coalition government — David Gauke, who served in the Treasury throughout Osborne’s tenure, and ex-Lib Dem Business Secretary Vince Cable — have both accepted that the government might have focused more on higher taxation and less on cuts to public spending. But both also insisted the U.K had ultimately been correct to prioritize putting its public finances on a sounder footing.

It was February 2018 before Britain finally achieved Osborne’s goal of eliminating the deficit on its day-to-day budget.

Austerity was coming to an end, at last. But Osborne had already left the Treasury, 18 months earlier — swept away along with Cameron in the wake of a seismic national uprising.

***

David Cameron had won the 2015 election outright, despite — or perhaps because of — the stringent spending cuts his coalition government had overseen, more of which had been pledged in his 2015 manifesto. Also promised, of course, was a public vote on Britain’s EU membership.

The reasons for the leave vote that followed were many and complex — but few doubt that years of underinvestment in poorer parts of the U.K. were among them.

Regardless, the 2016 EU referendum triggered a period of political acrimony and turbulence not seen in Westminster for generations. With no pre-agreed model of what Brexit should actually entail, the U.K.’s future relationship with the EU became the subject of heated and protracted debate. After years of wrangling, Britain finally left the bloc at the end of January 2020, severing ties in a more profound way than many had envisaged.

While the twin crises of COVID and Ukraine have muddled the picture, most economists agree Brexit has already had a significant impact on the U.K. economy. The size of Britain’s trade flows relative to GDP has fallen further than other G7 countries, business investment growth trails the likes of Japan, South Korea and Italy, and the OBR has stuck by its March 2020 prediction that Brexit would reduce productivity and U.K. GDP by 4 percent.

Perhaps more significantly, Brexit has ushered in a period of political instability. As prime ministers come and go (the U.K. is now on its fifth since 2016), economic programs get neglected, or overturned. Overseas investors look on with trepidation.

“The evidence that the referendum outcome, and the kind of uncertainty and change in policy that it created, have led to low investment and low growth in the U.K. is fairly compelling,” said professor Stephen Millard, deputy director at the National Institute of Economic and Social Research.

Beyond the instability, the broader impact of the vote to leave remains contentious.

Portes argued — as many Remain supporters also do — that much harm was done by the decision to leave the EU’s single market. “It’s the facts, not the uncertainty that in my view is responsible for most of the damage,” he said.

Brexit supporters dismiss such claims.

“It’s difficult statistically to find much significant effect of Brexit on anything,” said professor Patrick Minford, founder member of Economists for Brexit. “There’s so much else going on, so much volatility.”

Minford, an economist favored by ex-PM Truss, acknowledged that “Brexit is disruptive in the short run, so it’s perfectly possible that you would get some short-run disruption.” But he added: “It was a long-term policy decision.”

Where next?

Plenty of economists can rattle off possible solutions, although actually delivering them has thus far evaded Britain’s political class. “It’s increasing investment, having more of a focus on the long-term, it’s having economic strategies that you set out and actually commit to over time,” says the IFS’ Xu. “As far as possible, it’s creating more certainty over economic policy.”

But in seeking to bring stability after the brief but chaotic Truss era, new U.K. Chancellor Jeremy Hunt has signaled a fresh period of austerity is on the way to plug the latest hole in the nation’s finances. Leveling Up Secretary Michael Gove told Times Radio that while, ideally, you wouldn’t want to reduce long-term capital investments, he was sure some spending on big projects “will be cut.”

This could be bad news for many of the U.K.’s long-awaited infrastructure schemes such as the HS2 high-speed rail line, which has been in the works for almost 15 years and already faces a familiar mix of local resistance, vested interests, and a sclerotic planning system.

“We have a real problem in the sense that the only way to really durably raise productivity growth for this country is for investments to pick up,” said Springford, from the Centre for European Reform. “And the headwinds to that are quite significant.”

For dock workers at Liverpool’s Peel Port, the prospect of a fresh round of austerity amid a cost-of-living crisis is too much to bear. “Workers all over this country need to stand up for themselves and join a union,” insisted Delij.

For him, it’s all about priorities — and the arguments still echo back to the great crash of 15 years ago. “They bailed the bankers out in 2007,” he said, “and can’t bail hungry people out now.”

Norwalk, Connecticut — Higher fuel prices are expected to make this a tough winter for homeowners. Nationwide, families can expect to pay nearly 18% more to heat their homes this winter, according to the National Energy Assistance Directors’ Association.

Compared to last year, heating oil is up 25% and natural gas increased 31%, costing homeowners hundreds more.

Lorenzo Wyatt, who owns Home Comfort Practice, which teaches people how to reduce their energy costs, blamed supply and demand.

“You have a global market for energy, for oil, natural gas, and then those costs have gone up because there’s shortages,” Wyatt said.

Drew Todd used to pay about $2 for a gallon of oil to heat his home in Norwalk, Connecticut. Due to inflation, the cost to fill his 100-gallon tank has more than doubled.

“I think it’s going to hit seven bucks, in my opinion,” Todd said, adding that he cannot afford that and will have to rely on “extra sweatshirts” and “extra blankets” if it gets really cold this winter.

After losing his job in March, he applied for a state grant to help pay his energy bill.

“We’re going to keep it up as best as possible,” he said. “We don’t have a lavish lifestyle and we will do what we can.”

Wyatt advises keeping the thermostat at 68 degrees, closing the fireplace damper, removing window air conditioners and keeping drapes closed.

“What you want to do is you want to keep the heat inside,” Wyatt said. “So insulate the ceiling because heat rises. Insulate your walls, fill those wall cavities with insulation.”

Todd is hoping some of those small adjustments will keep his family warm and his wallet fuller this winter.

Stocks fell sharply on Wall Street Wednesday after Federal Reserve Chief Jerome Powell signaled that it’s too early for the central bank to consider pausing its interest rate increases as it tries to crush the worst inflation in decades.

The S&P 500 fell 96 points, or 2.5%, closing at 3,760. It had been up by 1% earlier in the day. The Dow Jones Industrial Average shed 336 points, or 1.6%, at 32,148. The Nasdaq composite fell 3.6%. Before their brief afternoon rally, the indexes had all been in the red much of the day ahead of the Fed’s interest rate policy statement release at 2:00 p.m. Eastern.

Powell’s remarks came after the Fed announced a widely expected fourth straight extra-large rate increase of three-quarters of a percentage point. The market rallied briefly after the central bank released a statement that seemed to suggest it could ease back on the rate-increase program. That was welcome news for markets, which have been worried the recent pace of rate hikes could slow the economy so much that it goes into a recession.

Not so dovish

But during a press conference, Powell said that to bring inflation down, the Fed will need to keep rates high enough to hurt the economy “for some time.”

“It’s very premature, in my view, to think about or to be talking about pausing our rate hikes,” Powell said. “We have a ways to go.”

Paul Ashworth of Capital Economics suggested the Fed’s latest policy statement is less dovish than it sounds, noting that Powell emphasized in his press conference that any pause in rate hikes are a long way away.

“Although market rate expectations fell in response to the release of the statement, those declines were more than reversed during Powell’s hawkish press conference, with the peak in the fed funds rate expected to be slightly above 5.0% next summer,” Ashworth said in a report.

Long-term Treasury yields jumped after a brief pullback. The yield on the two-year Treasury, which tends to track market expectations of future Fed action, rose to 4.61% from 4.55% shortly before the Fed released its statement. The yield on the 10-year Treasury, which helps set mortgage rates, climbed to 4.09% after having fallen to 3.98% earlier in the afternoon.

The Fed’s move raised its key short-term rate to a range of 3.75% to 4%, its highest level in 15 years. It was the central bank’s sixth rate hike this year, a streak that has made mortgages and other consumer and business loans increasingly expensive and heightened the risk of a recession.

More deliberate pace

The Fed’s statement said that, in coming months, it would consider the cumulative impact of its large rate hikes on the economy. It noted that its rate hikes take time to fully affect growth and inflation.

But any encouragement that gave investors faded when Powell said during a press conference that the central bank would rather make a mistake of taking interest rates too high than easing too quickly, noting that a premature pullback on rate hikes could lead inflation to become entrenched, which risks more pain for households.

“What the Fed statement giveth, the Fed chairman taketh away,” Chris Zaccarelli, chief investment officer for independent Advisor Alliance said in a note.

“The Fed statement – especially the part that referred to ‘cumulative tightening’ – made traders very excited that a step-down or pause in rate hikes was upon us, however, the press conference took that hope away once Chairman Powell spoke about how far in the future was the timeline for them to stop their rate hikes,” Zaccarelli said.

Powell said that regardless of whether the Fed dials down its interest rate hike in December, it may still end up pulling its key short-term rate ultimately to a higher level than previously thought because of data show inflation is worse than expected.

The path ahead for the Fed is closely tied to whether inflation cools from its hottest levels in four decades. Wall Street is concerned about inflation squeezing consumers and businesses while worries grow that the Fed could bring on a recession by slowing the economy too much.

Markets racked by uncertainty

“At the end of the day, the markets like certainty and they don’t have certainty from the Fed,” said Ryan Grabinski, managing director of investment strategy at Strategas, a Baird company.

Wall Street has been closely watching the latest economic data, which is heavy on the employment market this week. The job market has remained strong despite inflation, which is being taken as a sign that the Fed will have to remain aggressive in its fight against high prices.

The latest jobs data from private payroll company ADP shows that companies added positions at a greater pace than expected in October. The report follows hotter-than-expected data from the government Tuesday on job openings.

“It’s sort of confirming that the Fed still has more work to do,” Grabinski said.

Investors will get more employment data with the government’s weekly unemployment report on Thursday and a broader monthly jobs report on Friday. They have been closely watching the latest round of company earnings to get a better sense of inflation’s impact on corporate profits and outlooks. It’s been a mixed bag so far.

The 11 sectors in the S&P 500 were in the red after shedding all their gains after the brief rally following the Fed statement. Technology stocks and retailers were among the biggest weights on the index.

Drugstore operator CVS rose 3.6% after raising its profit forecast following a strong third quarter. Casino operator Caesars Entertainment rose 2.1% after beating Wall Street’s third-quarter profit and revenue forecasts.

Short-term vacation rental marketplace Airbnb fell 10.8% after warning investors that bookings growth will slow in the fourth quarter. Beauty products maker Estee Lauder slid 6.4% after slashing its profit forecast as COVID-19 lockdowns in China and inflation hurt business.

The Federal Reserve on Wednesday approved a fourth consecutive three-quarter point interest rate increase and signaled a potential change in how it will approach monetary policy to bring down inflation.

In a well-telegraphed move that markets had been expecting for weeks, the central bank raised its short-term borrowing rate by 0.75 percentage point to a target range of 3.75%-4%, the highest level since January 2008.

The move continued the most aggressive pace of monetary policy tightening since the early 1980s, the last time inflation ran this high.

Along with anticipating the rate hike, markets also had been looking for language indicating that this could be the last 0.75-point, or 75 basis point, move.

The new statement hinted at that policy change, saying when determining future hikes, the Fed “will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.”

Economists are hoping this is the much talked about “step-down” in policy that could see a rate increase of half a point at the December meeting and then a few smaller hikes in 2023.

This week’s statement also expanded on previous language simply declaring that “ongoing increases in the target range will be appropriate.”

The new language read, “The Committee anticipates that ongoing increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time.”

On balance, Powell dismissed the idea that the Fed may be pausing soon though he said he expects a discussion at the next meeting or two about slowing the pace of tightening.

He also reiterated that it may take resolve and patience to get inflation down.

“We still have some ways to go and incoming data since our last meeting suggests that the ultimate level of interest rates will be higher than previously expected,” he said.

Still, Powell repeated the idea that there may come a time to slow the pace of rate increases. He has said this at recent news conferences

“So that time is coming, and it may come as soon as the next meeting or the one after that. No decision has been made,” he said.

The chairman also expressed some pessimism about the future. He noted that he now expects the “terminal rate,” or the point when the Fed stops raising rates, to be higher than it was at the September meeting. With the higher rates also comes the prospect that the Fed will not be able to achieve the “soft landing” that Powell has spoken of in the past.

“Has it narrowed? Yes,” he said in response to a question about whether the path has narrowed to a place where the economy doesn’t enter a pronounced contraction. “Is it still possible? Yes.”

However, he said the need for still-higher rates makes the job more difficult.

“Policy needs to be more restrictive, and that narrows the path to a soft landing,” Powell said.

Along with the tweak in the statement, the Federal Open Market Committee again categorized growth in spending and production as “modest” and noted that “job gains have been robust in recent months” while inflation is “elevated.” The statement also reiterated language that the committee is “highly attentive to inflation risks.”

The rate increase comes as recent inflation readings show prices remain near 40-year highs. A historically tight jobs market in which there are nearly two openings for every unemployed worker is pushing up wages, a trend the Fed is seeking to head off as it tightens money supply.

Concerns are rising that the Fed, in its efforts to bring down the cost of living, also will pull the economy into recession. Powell has said he still sees a path to a “soft landing” in which there is not a severe contraction, but the U.S. economy this year has shown virtually no growth even as the full impact from the rate hikes has yet to kick in.

At the same time, the Fed’s preferred inflation measure showed the cost of living rose 6.2% in September from a year ago – 5.1% even excluding food and energy costs. GDP declined in both the first and second quarters, meeting a common definition of recession, though it rebounded to 2.6% in the third quarter largely because of an unusual rise in exports. At the same time, housing demand has plunged as 30-year mortgage rates have soared past 7% in recent days.

On Wall Street, markets have been rallying in anticipation that the Fed soon might start to ease back as worries grow over the longer-term impact of higher rates.

The Dow Jones Industrial Average has gained more than 13% over the past month, in part because of an earnings season that wasn’t as bad as feared but also due to growing hopes for a recalibration of Fed policy. Treasury yields also have come off their highest levels since the early days of the financial crisis, though they remain elevated. The benchmark 10-year note most recently was around 4.09%.

There is little if any expectation that the rate hikes will halt anytime soon, so the anticipation is just for a slower pace. Futures traders are pricing a near coin-flip chance of a half-point increase in December, against another three-quarter point move.

Current market pricing also indicates the fed funds rate will top out near 5% before the rate hikes cease.

The fed funds rate sets the level that banks charge each other for overnight loans, but spills over into multiple other consumer debt instruments such as adjustable-rate mortgages, auto loans and credit cards.

WASHINGTON (AP) — The Federal Reserve pumped up its benchmark interest rate Wednesday by three-quarters of a point for a fourth straight time but hinted that it could soon reduce the size of its rate hikes.

The Fed’s move raised its key short-term rate to a range of 3.75% to 4%, its highest level in 15 years. It was the central bank’s sixth rate hike this year — a streak that has made mortgages and other consumer and business loans increasingly expensive and heightened the risk of a recession.

But in a statement, the Fed suggested that it could soon shift to a more deliberate pace of rate increases. It said that in coming months it would consider the cumulative impact of its large rate hikes on the economy. It noted that its rate hikes take time to fully affect growth and inflation.

Those words indicated that the Fed’s policymakers may think borrowing costs are getting high enough to possibly slow the economy and reduce inflation. If so, that would suggest that they don’t need to raise rates as quickly as they have been doing.

Still, for now, the persistence of inflated prices and higher borrowing costs is pressuring American households and has undercut the ability of Democrats to campaign on the health of the job market as they try to keep control of Congress. Republican candidates have hammered Democrats on the punishing impact of inflation in the run-up to the midterm elections that will end Tuesday.

The Fed’s statement Wednesday was released after its latest policy meeting. Many economists expect Chair Jerome Powell to signal at a news conference that the Fed’s next expected rate hike in December may be only a half-point rather than three-quarters.

Typically, the Fed raises rates in quarter-point increments. But after having miscalculated in downplaying inflation last year as likely transitory, Powell has led the Fed to raise rates aggressively to try to slow borrowing and spending and ease price pressures.

Wednesday’s latest rate increase coincided with growing concerns that the Fed may tighten credit so much as to derail the economy. The government has reported that the economy grew last quarter, and employers are still hiring at a solid pace. But the housing market has cratered, and consumers are barely increasing their spending.

The average rate on a 30-year fixed mortgage, just 3.14% a year ago, surpassed 7% last week, mortgage buyer Freddie Mac reported. Sales of existing homes have dropped for eight straight months.

Blerina Uruci, an economist at T. Rowe Price, suggested that falling home sales are “the canary in the coal mine” that demonstrate that the Fed’s rate hikes are weakening a highly interest-rate sensitive sector like housing. Uruci noted, though, that the Fed’s hikes haven’t yet meaningfully slowed much of the rest of the economy, particularly the job market or consumer demand.

“So long as those two components remain strong,” she said, the Fed’s policymakers “cannot count on inflation coming down” close to their 2% target within the next two years.

Several Fed officials have said recently that they have yet to see meaningful progress in their fight against rising costs. Inflation rose 8.2% in September from 12 months earlier, just below the highest rate in 40 years.

Still, the policymakers may feel they can soon slow the pace of their rate hikes because some early signs suggest that inflation could start declining in 2023. Consumer spending, squeezed by high prices and costlier loans, is barely growing. Supply chain snarls are easing, which means fewer shortages of goods and parts. Wage growth is plateauing, which, if followed by declines, would reduce inflationary pressures.

Yet the job market remains consistently strong, which could make it harder for the Fed to cool the economy and curb inflation. This week, the government reported that companies posted more job openings in September than in August. There are now 1.9 available jobs for each unemployed worker, an unusually large supply.

A ratio that high means that employers will likely continue to raise pay to attract and keep workers. Those higher labor costs are often passed on to customers in the form of higher prices, thereby fueling more inflation.

Ultimately, economists at Goldman Sachs expect the Fed’s policymakers to raise their key rate to nearly 5% by March. That is above what the Fed itself had projected in its previous set of forecasts in September.

Outside the United States, many other major central banks are also rapidly raising rates to try to cool inflation levels that are even higher than in the U.S.

Last week, the European Central Bank announced its second consecutive jumbo rate hike, increasing rates at the fastest pace in the euro currency’s history to try to curb inflation that soared to a record 10.7% last month.

Likewise, the Bank of England is expected to raise rates Thursday to try to ease consumer prices, which have risen at their fastest pace in 40 years, to 10.1% in September. Even as they raise rates to combat inflation, both Europe and the U.K. appear to be sliding toward recession.

The U.S. central bank has raised the benchmark short-term borrowing rate a total of six times this year, including 75 basis point increases in June, July and September, in an effort to cool down inflation, which is still near 40-year highs and causing most consumers to feel increasingly cash strapped. A basis point is equal to 0.01 of a percentage point.

A policy statement after the announcement noted that the Fed is considering the “cumulative” impact of its hikes so far when determining future rate increases. Economists are hoping this signals plans to “step-down” the pace of increases going forward, which could mean a half point hike at the December meeting and then a few smaller raises in 2023. Still, stocks tumbled after Federal Reserve Chair Jerome Powell said there were more rate hikes ahead.

“Americans are under greater financial strain, there’s no question,” said Chester Spatt, professor of finance at Carnegie Mellon University’s Tepper School of Business and former chief economist of the Securities and Exchange Commission.

The federal funds rate, which is set by the central bank, is the interest rate at which banks borrow and lend to one another overnight. Although that’s not the rate consumers pay, the Fed’s moves still affect the borrowing and saving rates they see every day.

By raising rates, the Fed makes it costlier to take out a loan, causing people to borrow and spend less, effectively pumping the brakes on the economy and slowing down the pace of price increases.

“Unfortunately, the economy will slow much faster than inflation, so we’ll feel the pain well before we see any gain,” said Greg McBride, Bankrate.com’s chief financial analyst.

Already, “mortgage rates have rocketed to 16-year highs, home equity lines of credit are the highest in 14 years, and car loan rates are at 11-year highs,” he said.

• Mortgage rates are already higher. Even though 15-year and 30-year mortgage rates are fixed and tied to Treasury yields and the economy, anyone shopping for a home has lost considerable purchasing power, in part because of inflation and the Fed’s policy moves.

Along with the central bank’s vow to stay tough on inflation, the average interest rate on the 30-year fixed-rate mortgage hit 7%, up from below 4% back in March.

On a $300,000 loan, a 30-year, fixed-rate mortgage at December’s rate of 3.11% would have meant a monthly payment of about $1,283. Today’s rate of 7.08% brings the monthly payment to $2,012. That’s an extra $729 a month or $8,748 more a year, and $262,440 more over the lifetime of the loan, according to LendingTree.

The increase in mortgage rates since the start of 2022 has the same impact on affordability as a 35% increase in home prices, according to McBride’s analysis. “If you had been approved for a $300,000 mortgage in the beginning of the year, that’s the equivalent of less than $200,000 today.”

For home buyers, “adjustable-rate mortgages may continue to be more popular among consumers seeking lower monthly payments in the short term,” said Michele Raneri, vice president of U.S. research and consulting at TransUnion. “And consumers looking to tap into available home equity may continue to look towards HELOCs,” she added, rather than refinancing.

Yet adjustable-rate mortgages and home equity lines of credit are pegged to the prime rate, so those will also increase. Most ARMs adjust once a year, but a HELOC adjusts right away. Already, the average rate for a HELOC is up to 7.3% from 4.24% earlier in the year.

• Credit card rates are rising. Since most credit cards have a variable rate, there’s a direct connection to the Fed’s benchmark. As the federal funds rate rises, the prime rate does as well, and your credit card rate follows suit within one or two billing cycles.

That means anyone who carries a balance on their credit card will soon have to shell out even more just to cover the interest charges. “This latest interest rate hike will most acutely impact those consumers who do not pay off their credit card balances in full through higher minimum monthly payments,” Raneri said.

Because of this rate hike, consumers with credit card debt will spend an additional $5.1 billion on interest, according to an analysis by WalletHub. Factoring in the rate hikes from March, May, June, July, September and November, credit card users will wind up paying around $25.6 billion more in 2022 than they would have otherwise, WalletHub found.

Already credit card rates are near 19%, up from 16.34% in March. “That’s the highest since the Fed began tracking in 1994 and is more than a full percentage point higher than the previous record set back in 2019,” according to Matt Schulz, chief credit analyst at LendingTree. And rates are only going to continue to rise, he said. “We’ve still got a ways to go before those rates hit their peak.”

The best thing you can do now is pay down high-cost debt — “0% balance transfer credit cards are still widely available, especially for those with good credit, and can help you avoid accruing interest on the transferred balance for up to 21 months,” Schulz said.

“That can be an absolute godsend for folks struggling with card debt,” he added.

Otherwise, consolidate and pay off high-interest credit cards with a lower-interest home equity loan or personal loan, Schulz advised.

• Auto loans are more expensive. Even though auto loans are fixed, payments are getting bigger because the price for all cars is rising along with the interest rates on new loans, so if you are planning to buy a car, you’ll pay more in the months ahead.

The average interest rate on a five-year new car loan is currently 5.63%, up from 3.86% at the beginning of the year and could surpass 6% with the central bank’s next moves, although consumers with higher credit scores may be able to secure better loan terms.

Paying an annual percentage rate of 6% instead of 5% would cost consumers $1,348 more in interest over the course of a $40,000, 72-month car loan, according to data from Edmunds.

Still, it’s not the interest rate but the sticker price of the vehicle that’s causing an affordability problem, McBride said. “Rising rates doesn’t help, certainly.”

• Student loans vary by type.Federal student loan rates are also fixed, so most borrowers won’t be affected immediately. But if you are about to borrow money for college, the interest rate on federal student loans taken out for the 2022-2023 academic year are up to 4.99%, from 3.73% last year and 2.75% in 2020-2021.

If you have a private loan, those loans may be fixed or have a variable rate tied to the Libor, prime or T-bill rates, which means that as the Fed raises rates, borrowers will likely pay more in interest, although how much more will vary by the benchmark.

Currently, average private student loan fixed rates can range from 3.22% to 14.96%, and from 2.52% to 12.99% for variable rates, according to Bankrate. As with auto loans, they vary widely based on your credit score.

• Only some savings account rates are higher. The silver lining is that the interest rates on savings accounts are finally higher after several consecutive rate hikes.

Thanks, in part, to lower overhead expenses, top-yielding online savings account rates are as high as 3.5%, according to Bankrate, much higher than the average rate from a traditional, brick-and-mortar bank.

“Savers are seeing the best yields since 2009 — if they’re willing to shop around,” McBride said. Still, because the inflation rate is now higher than all of these rates, any money in savings loses purchasing power over time.

Now is the time to boost that emergency savings, McBride advised. “Not only will you be rewarded with higher rates but also nothing helps you sleep better at night than knowing you have some money tucked away just in case.”

“More broadly, it makes sense to be more cautious,” Spatt added. “Recognize that employment is maybe less secure. It’s reasonable to expect we’ll see unemployment going up, but how much remains to be seen.”

The below is an excerpt from a recent edition of Bitcoin Magazine Pro, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

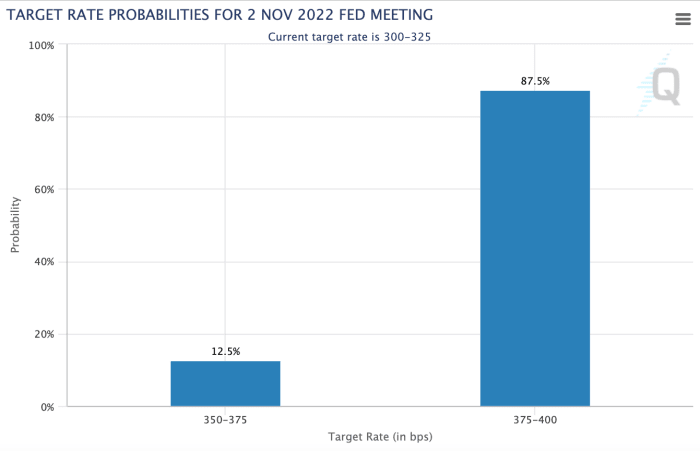

November FOMC Meeting

All eyes across global markets are on the November FOMC meeting. At this point in the global liquidity cycle, seemingly every asset class is part of the same implicit trade. The tough talk from the Fed, the central bank of the dollar indebted world, has held up so far in 2022, as they embark upon the fastest tightening cycle in modern history.

Consensus for the size of the rate hike is 75bps, which would raise the policy rate to 4.00%.

Consensus for the size of the rate hike is 75bps, which would raise the policy rate to 4.00%.

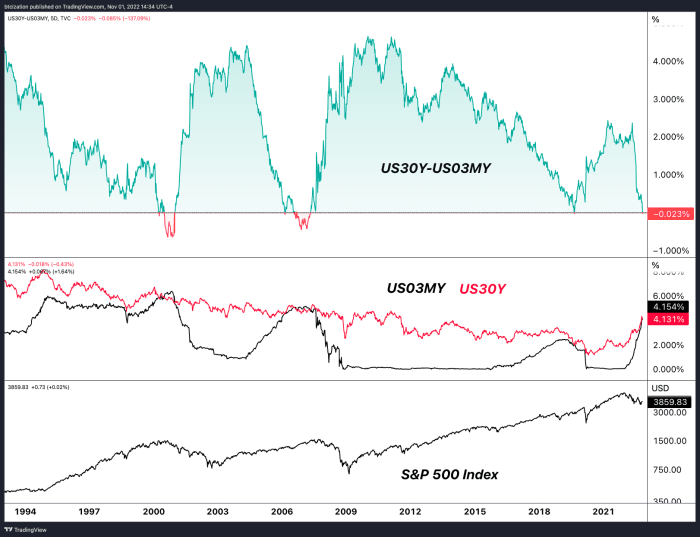

Much of this hiking has already priced itself into the front end of the U.S. Treasury curve, which has led to all sorts of inversions across various maturities.

In terms of the yield curve, across any duration that matters, an inversion has happened — a phenomenon that typically occurs before an economic slowdown, as short term yields rising disincentivizes the investment of capital over long durations due to “attractive” short end yields. Lend your money to the U.S. government for 30 years and lock in 4.13% or for three months at 4.13% and reevaluate then? Duration risk is real and the pace of this tightening cycle on the backs of record inflationary conditions across the globe has left investors uneasy on the long-term prospect of government paper. No kidding.

U.S. Treasury yield curve inversion with short-term yields higher than long-term yields.

Arguably, the Fed is still behind the curve and, per their mandate, shouldn’t have “let” inflationary pressures get this out of control while still stoking the flames with zero-interest rate policy and $120B/month of quantitative easing bond purchases. Due to the blunder and subsequent hit to their credibility, the Fed is attempting to induce pain in the labor market and in asset prices until inflationary concerns abate.

It’s a bold strategy and it’s one that is entirely destined to fail. But they’ll likely end up crashing everything while trying. However, the nominal economy — meaning gross domestic product expectations (not inflation adjusted) and the labor market — is still piping hot. The market looks to be believing that Fed policy is in an entirely new regime going forward.

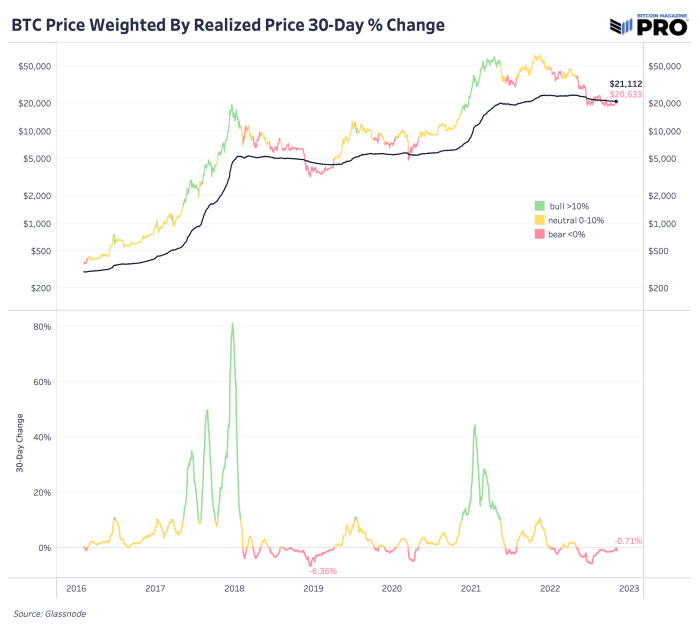

Shown below is the bitcoin price with its average on-chain holder cost basis (realized price). Bitcoin is in a classic bear market consolidation phase, that many may not have more pain ahead. These periods, where panicked/leveraged investors transfer their holdings to the prudent and well capitalized, are what create the conditions for the next bull run.

Federal Reserve policymakers are meeting Wednesday and it’s likely they will raise interest rates by another 75 basis points in a continued effort to curb inflation. Previous rate increases have pushed the average 30-year fixed mortgage rate above 7%. Nancy Chen reports on how already-high rates are affecting the housing market.

Be the first to know

Get browser notifications for breaking news, live events, and exclusive reporting.

The Federal Reserve is expected to raise interest rates by three-quarters of a percentage point Wednesday and then signal that it could reduce the size of its rate hikes starting as soon as December.

Markets are primed for the fourth 75-basis point hike in a row, and investors are anticipating the Fed will slow down its pace before winding down the rate-hiking cycle in March. A basis point is equal to 0.01 of a percentage point.

“We think they hike just to get to the end point. We do think they hike by 75. We think they do open the door to a step down in rate hikes beginning in December,” said Michael Gapen, chief U.S. economist at Bank of America.

Gapen said he expects Fed Chair Jerome Powell to indicate during his press briefing that the Fed discussed slowing the pace of rate hikes but did not commit to it. He expects the Fed would then raise interest rates by a half percentage point in December.

U.S. Federal Reserve Board Chairman Jerome Powell takes questions from reporters after the Federal Reserve raised its target interest rate by three-quarters of a percentage point to stem a disruptive surge in inflation, during a news conference following a two-day meeting of the Federal Open Market Committee (FOMC) in Washington, June 15, 2022.

Elizabeth Frantz | Reuters

“The November meeting isn’t really about November. It’s about December,” Gapen said. He expects the Fed to raise rates to a level of 4.75% to 5% by spring, and that would be its terminal rate — or end point. The 75 basis point hike Wednesday would take the fed funds rate range to 3.75% to 4%, from a range of zero to 0.25% in March.

“The market is very fixated on the fact there’s going to be 75 in November, 50 [basis points] in December, 25 on Feb. 1 and then probably another 25 in March,” said Julian Emanuel, head of equity, derivatives and quantitative strategy at Evercore ISI. “So in reality, the market already thinks this is happening, and from my point of view, there’s no way the outcome of his press conference is going to be more dovish than that.”

The stock market has already rallied on expectations of a slowdown in rate hikes by the Fed, after a final 75 basis point hike Wednesday afternoon. But strategists also say the market’s reaction could be violent if the Fed disappoints. The challenge for Powell will be to walk a fine line between signaling less-aggressive hikes are possible and upholding the Fed’s pledge to battle inflation.

Stock picks and investing trends from CNBC Pro:

For that reason, market pros expect the Fed chair to sound hawkish, and that could rattle stocks and send bond yields higher. Yields move opposite price.

“I think he’s going to try to execute the fine art of getting off the 75 [basis points] without creating euphoria and influencing financial conditions too easy,” said Rick Rieder, BlackRock chief investment officer of global fixed income. “I think the way the market is pricing, I think that’s what they’re going to do, but I think he’s really got to thread the needle on not getting people too excited about the direction of travel. Fighting inflation is their primary objective.”

As the Fed has raised interest rates, the economy is beginning to show signs of slowing. The housing market is slumping, as some mortgage rates have nearly doubled. The 30-year fixed rate mortgage was at 7.08% in the week of Oct. 28, up from 3.85% in March, according to Freddie Mac.

“I think [Powell] will say that four 75-basis point hikes is an awful lot and with this long and variable lag, you need to step back and see the impact. You’re seeing it in housing. You’re starting to see it in autos,” said Rieder. “You’re seeing it in some of the retailer slowdowns, and you’re certainly seeing it in the surveys. I think the idea that you’re slowing, it’s important how he describes it.”

The Fed should be dependent on incoming data, and while inflation is coming down, the pace of decline is unclear, Rieder said.

“If inflation continues to be surpisingly high, he shouldn’t shut off his options,” he said.

Gapen expects the economy to dip into a shallow recession in the first quarter. He said the equity market would be concerned if inflation were to stay so high the Fed would have to raise rates even more sharply than expected, threatening the economy even more.

“The markets want to be relieved, particualy the equity maket,” said Rieder. “I think what happens to the equity market and the bond market are different because of the technicals and the leverage. … But I think the market wants to believe that the Fed, they’re going to get to 5% and stay there for awhile. People are tired of getting bludgeoned, and I think they want to believe the bludgeoning is over.”

NEW YORK — Stocks gave up early gains and ended lower on Wall Street after an unexpectedly strong report on the job market raised concerns that the Federal Reserve will need to keep the pressure on inflation with aggressive interest rate increases. Those high rates are intended to slow the economy, and the fear is the Fed may go too far and cause a recession. Several companies rose after reporting solid earnings or outlooks, including Pfizer and Uber. The S&P 500 fell 0.4% Tuesday. Long-term Treasury yields reversed course from an early slide and rose back near multiyear highs.

THIS IS A BREAKING NEWS UPDATE. AP’s earlier story follows below.

Stocks on Wall Street gave up early gains and turned lower in afternoon trading Tuesday after an unexpectedly strong report on the job market raised concerns that the Federal Reserve will need to keep the pressure on inflation with aggressive interest rate increases.

The S&P 500 fell 0.4% as of 3:31 p.m. Eastern. It had been up as much as 1% shortly after trading opened. The Dow Jones Industrial Average fell 72 points, or 0.2%, to 32,660 and the Nasdaq fell 0.8%.

Big technology stocks were the biggest weights on the market. The companies, with their big valuations, have more heft in pushing the broader market up or down. Also, rising interest rates tend to make the sector look less attractive because of its those high valuations. Apple fell 1.6%.

Small company stocks held up better than the rest of the market. The Russell 2000 rose 0.4%.

The Labor Department reported that U.S. job openings rose unexpectedly in September, suggesting that the labor market is not cooling as fast as the Fed hoped for as it tries to slow economic growth.

The latest jobs data, which comes ahead of a broader employment report on Friday, is disappointing for investors who are looking for signs that inflation is easing and that the Fed might consider tempering its interest rate increases.

“That really fuels the expectation that the Fed has to do more hiking,” said Jason Draho, head of asset allocation for the Americas at UBS Global Wealth Management. “The labor market is still too tight for the Fed.”

Wall Street is concerned that the central bank is being too aggressive in slowing the economy, running the risk that it could bring on a recession.

Long-term Treasury yields turned higher after the report in job openings came out and rose back near multiyear highs. Those high rates have helped push mortgage rates above 7% this year.

The yield on the 10-year Treasury rose to 4.06% from 3.93% earlier in the morning.

The yield on the two-year Treasury, which tends to reflect market expectations of future moves by the Federal Reserve, rose to 4.53% from 4.40%.

“The issue for investors is figuring out how long the hiking cycle will last,” Draho said. “(Fed Chair Jerome) Powell will want to leave all options on the table.”

Stocks are coming off a strong rally in October that resulted in big monthly gains for some of the major indexes. Even so, they remain in the red for the year, including the S&P 500, which is down 19%.

Several big companies made solid gains following encouraging earnings reports and forecasts.

Pfizer rose 3.3% after reporting strong results and raising its profit forecast for the year. Uber surged 12.4% after giving investors a strong forecast for future bookings. Rival Lyft rose 4.5%.

Earnings remain a big focus for investors this week. CVS reports its results on Wednesday and Starbucks reports earnings on Thursday.

Outside of earnings, Abiomed surged 50.1% after health care giant Johnson & Johnson said it will pay $16.6 billion for the heart pump maker. Johnson & Johnson fell 0.1%.

The Fed is beginning a two-day policy meeting that’s expected to result in its sixth interest rate increase of the year as the central bank fights the worst inflation in four decades. The widespread expectation is for the Fed to push through another increase that’s triple the usual size, or three-quarters of a percentage point.

For its final policy meeting of the year, in December, opinions are currently split among investors as to whether the Fed will make another three-quarters point move or dial back to a half-point increase.

“The big focus is not so much on what the rate hike is going to be, but really what the comments are coming out of this week’s meeting in terms of any indications of whether there’ll be a little bit of softening as we move into early next year,” said Greg Bassuk, CEO at AXS Investments.

———

AP Business writers Joe McDonald, Elaine Kurtenbach and Matt Ott contributed to this report.

WASHINGTON — U.S. job openings rose unexpectedly in September, suggesting that the American labor market is not cooling as fast as the inflation fighters at the Federal Reserve hoped.

Employers posted 10.7 million job vacancies in September, up from 10.3 million in August, the Labor Department said Tuesday. Economists had expected the number of job openings to drop below 10 million for the first time since June 2021.

For the past two years, as the economy rebounded from 2020’s COVID-19 recession, employers have complained they can’t find enough workers. With so many jobs available, workers can afford to resign and seek employment that pays more or offers better perks or flexibility. So companies have been forced to raise wages to attract and keep staff. Higher pay has contributed to inflation that has hit 40-year highs in 2022.

In another sign the labor market remains tight and employers unwilling to let workers go, layoffs dropped in September to 1.3 million, fewest since April. But the number of people quitting their jobs slipped in September to just below 4.1 million, still high by historical standards.

To combat higher prices, the Federal Reserve has hiked its benchmark interest rate five times this year and is expected to deliver another increase Wednesday and again at its meeting in December. The central bank is aiming for a so-called soft landing — raising rates just enough to slow economic growth and bring inflation down without causing a recession.

Fed Chair Jerome Powell has expressed hope that inflationary pressure can be relieved by employers cutting job openings, not jobs.

The numbers: A closely-watched index that measures U.S. manufacturing activity fell 0.7 percentage points to 50.2 in October, according to the Institute for Supply Management on Tuesday.

Economists surveyed by the Wall Street Journal had forecast the index to inch down to 50. Any number below 50% reflects a shrinking economy.

It is the lowest level since May 2020.

Key details: The index for new orders remained in contraction territory, rising 2.1 points to 47.1. The production index rose 1.7 points to 52.3.

The employment index rose 1.3 points to 50 in October.

Supplier deliveries fell 5.6 points to 46.8 in October. This is the first time that deliveries were in a “faster” territory since February 2016.

The price index dropped 5.1 points to 46.6., also the lowest reading since the pandemic. Pricing power is shifting back to the buyer, the ISM said.

Only 8 of the 18 manufacturing industries reported growth in October.

Big picture: Manufacturing has been slowing recently led by softening business spending and fading demand for consumer goods. Economists think it is inevitable the index slips below the 50 threshold.

In a separate data, the S&P global U.S. manufacturing PMI inched up to 50.4 in its “final” reading in October from the “flash” reading of 49.9. This is down from a reading of 52 in September.

What ISM said: Manufacturing is slowing down and could soon enter contraction territory, but that doesn’t mean there will be a recession in the U.S., said Timothy Fiore, chair of the ISM factory business survey.

“I don’t see a collapse of new orders. I don’t see a collapse of the PMI,” Fiore said.

Looking ahead: “Recession jitters among manufacturers won’t disappear any time soon…manufacturing will endure more pain as demand weakens at home and abroad while prices stay high and interest rates remain fairly elevated,” said Oren Klachkin, economist at Oxford Economics.

DUBAI, United Arab Emirates — Oil giant Saudi Aramco on Tuesday reported a $42.4 billion profit in the third quarter of this year, buoyed by the higher global energy prices that have filled the kingdom’s coffers but helped fuel inflation worldwide.

The oil firm’s profits will help fund the kingdom’s assertive Crown Prince Mohammed bin Salman’s plans for a futuristic city on the Red Sea coast, but also comes as the U.S. grows increasingly frustrated by higher prices at the pump chewing into American consumer’s wallets.

Those tensions yet again have chilled relations between Riyadh and Washington before the Nov. 8 midterm elections.

In a note to investors, the predominantly state-owned oil company said its average barrel of crude sold for $101.70 in the third quarter — up from $72.80 at the same point last year. It’s Aramco’s second-largest quarterly profit in its history, just before its second-quarter results this year saw a profit of $48.4 billion.

It put its profits so far in 2022 at $130.3 billion, compared to $77.6 billion in 2021.

“While global crude oil prices during this period were affected by continued economic uncertainty, our long-term view is that oil demand will continue to grow for the rest of the decade given the world’s need for more affordable and reliable energy,” Aramco CEO Amin H. Nasser said in a statement.

Aramco will keep its dividend this quarter at $18.8 billion, the world’s highest.

Benchmark Brent crude traded just shy of $95 a barrel Tuesday. The sliver of Aramco that the kingdom has put on Riyadh’s Tadawul stock market stood at $9.29 a share before trading Tuesday — putting its valuation at just over $2 trillion. Only Apple’s valuation, at $2.44 trillion, is higher.

OPEC and a loose confederation of other countries led by Russia agreed in early October to cut its production by 2 million barrels of oil a day, beginning in November.

OPEC, led by Saudi Arabia, has insisted its decision came from concerns about the global economy. Analysts in the U.S. and Europe warn a recession looms in the West from inflation and subsequent interest rate hikes, as well as food and oil supplies being affected by Russia’s war on Ukraine.

In Washington, anger has grown with Saudi Arabia, particularly from President Joe Biden, who traveled to the kingdom in July and shared a fist bump with Crown Prince Mohammed. Biden recently warned the kingdom that “there’s going to be some consequences for what they’ve done.”

Saudi Arabia lashed back, publicly claiming the Biden administration sought a one-month delay in the OPEC cuts that could have helped reduce the risk of a spike in gas prices ahead of the U.S. midterm elections.

Biden on Monday separately accused oil companies of “war profiteering” as he raised the possibility of imposing a windfall tax on American energy companies if they don’t boost domestic production.

———

Follow Jon Gambrell on Twitter at www.twitter.com/jongambrellAP.

PCK Schwedt oil refinery in Schwedt, Germany on Monday, May 9, 2022.

Krisztian Bocsi | Bloomberg | Getty Images

ABU DHABI, United Arab Emirates — Politicians and governments around the world are bracing for potential civil unrest as many countries grapple with mounting energy costs and rising inflation.

The global economy is facing an onslaught from multiple sides — a war in Europe, and shortages of oil, gas and food, and high inflation, each of which has worsened the next.

Concerns are centered on the coming winter, especially for Europe. Cold weather, combined with an oil and gas shortage stemming from Western sanctions on Russia for its invasion of Ukraine, threatens to upend lives and businesses.

But as much concern as there is ahead of this winter, it’s really the winter of 2023 that people should be worried about, major oil and gas executives have warned.

Energy prices “are approaching unaffordability,” with some people already “spending 50% of their disposable income on energy or higher,” BP CEO Bernard Looney told CNBC’s Hadley Gamble during a panel at the Adipec conference in Abu Dhabi.

We are in good shape for this winter. But as we said, the issue is not this winter. It will be the next one, because we are not going to have Russian gas.

Claudio Descalzi

CEO of Eni

But through a combination of high gas storage levels and government spending packages to subsidize people’s bills, Europe may be able to manage the crisis this year.

“I think it has been addressed for this winter,” Looney said. “It’s the next winter I think many of us worry, in Europe, could be even more challenging.”

The CEO of Italian oil and gas giant Eni expressed the same worry.

For this winter, Europe’s gas storage is around 90% full, according to the International Energy Agency, providing some assurance against a major shortage.

But a large proportion of that is made up of Russian gas imported in previous months, as well as gas from other sources that was easier than usual to buy since major importer China was buying less due to its slower economic activity.

“We are in good shape for this winter,” Eni chief Claudio Descalzi said during the same panel. “But as we said, the issue is not this winter. It will be the next one, because we are not going to have Russian gas – 98% [less] next year, maybe nothing.”

This could lead to serious social unrest — already, small to medium-sized protests have cropped up around Europe.

Anti-government protests in Germany and Austria in September and in the Czech Republic last week — the latter of which has seen household energy bills surge tenfold — may be a small taste of what’s to come, analysts have warned. Some energy executives agreed.

Yes, there is a real risk that governments without a steady hand on policy shaping in Asia can deal with unrest.

Datuk Tengku Muhammad Taufik

CEO of Petronas

“We’ve seen that any shocks to the price at the pump, or something as simple as LPG [liquefied petroleum gas] for cooking, can cause unrest,” the CEO of Malaysian oil and gas company Petronas, Datuk Tengku Muhammad Taufik, said.

He described how a strengthening dollar and rising fuel prices pose a serious risk to many Asian economies – massive populations that are some of the biggest oil and gas importers in the world. And this is happening while subsidies are already in place to help ease prices for citizens.

Inflation in the euro zone remains extremely high. Protestors in Italy used empty shopping trolleys to demonstrate the cost-of-living crisis.

Many Asian economies were already reeling from the pandemic, which caused “vast swaths of [small and medium enterprises] in Asia to just collapse,” Taufik said. “So, yes, there is a real risk that governments without a steady hand on policy shaping in Asia can deal with unrest.”

Much of the anger of protesters is also directed at the energy companies, which have been making record profits as bills get higher and higher.

Responding to this, many of the CEOs who spoke to CNBC said it’s an issue of market supply and demand, and that it’s up to governments to implement policies more conducive to energy investment. That investment, they stressed, has taken a hit in recent years as countries push for the transition to renewables.

The world has to face “the practicalities and realities of today and tomorrow,” BP’s Looney said, stressing the need to “invest in hydrocarbons today, because today’s energy system is a hydrocarbon system.”

Many policymakers and institutions still decry the use of fossil fuels, warning the far bigger crisis is that of climate change. In June, United Nations Secretary General Antonio Guterres called for abandoning fossil fuel finance, and called any new funding for exploration “delusional.”

The oil executives argued that this approach simply isn’t realistic, nor is it an option if countries want economic and political stability.

Read more about energy from CNBC Pro

At the same time, however, they admitted that the energy transition itself does need greater focus and investment in order to avert a larger crisis next year and beyond, when there is no Russian gas in storage and other options are increasingly expensive.

“In Europe, we pay at least six, seven times to [as much as] 15 times the energy costs with respect to the U.S.,” ENI’s Descalzi said.

“So what we have done in Europe, each country, gave incentive subsidies to try to reduce the cost for industry and for citizens. How long that can continue?” he asked.

“I don’t know, but it’s impossible that it can continue forever. All these countries have a very high debt,” he said. “So they have to find a structural way to solve this issue. And the structural way is what we said until now — we have to increase and be faster on the transition. That is true.”

“But,” he added, “we have to understand, from a technical point of view, what is affordable and what is not.”