TOKYO—Japan’s finance ministry plans to boost government bond issuance by $75 billion to fund an economic stimulus package, potentially stoking concerns about the nation’s fiscal health.

Prime Minister Sanae Takaichi’s cabinet on Friday approved a draft supplementary budget for the fiscal year ending March 2026 that is worth 18.303 trillion yen, or about $117.10 billion. The government now plans to issue an additional 11.696 trillion yen of bonds, including increases in issuance of two- and five-year notes.

Britain’s stock and bond markets flopped Friday morning on new evidence that the country’s Labour Party leadership doesn’t have a clue what to do about the economy or budget. Add this to the list of welfare-state cautionary tales out of Europe.

At one point Friday morning, the yield on the benchmark 10-year government bond, or gilt, had risen 11 basis points to 4.55%. The main London stock index dipped nearly 2%, and the pound fell. This was in response to a Financial Times report Thursday night that Chancellor of the Exchequer Rachel Reeves is abandoning plans to increase income-tax rates in her budget plan this month.

This sounds like good news. but investors interpreted it as a sign that Ms. Reeves and her boss, Prime Minister Keir Starmer, have run out of politically viable ways to balance the government budget—which is true. Estimates of the budget “black hole” Ms. Reeves needs to fill range up to £30 billion per year—the gap between likely spending and revenue if current policies stay the same.

An attempt over the summer to cut some particularly generous welfare benefits collapsed amid a rebellion from Labour backbenchers in Parliament, putting welfare reform off the table. Mr. Starmer is rightly under pressure to increase defense spending. Labour’s promises of economic growth via public “investment” translate mainly to pay increases for government workers.

Argentina’s stocks, bonds and currency surged Monday after the country’s midterm elections delivered a surprising mandate for President Javier Milei to press ahead with his free-market economic overhauls.

The Argentine peso rose around 9% against the U.S. dollar in midmorning trading, the most in more than two decades. A U.S. dollar-denominated government bond maturing in 2046 rose by 11 cents to trade at 66 cents on the dollar, according to Tradeweb data. Argentina’s benchmark stock index, the Merval, was up 17% as bank stocks soared.

Inside the $26 trillion Treasury market, perhaps the deepest and most liquid place for government debt in the world, a particular trade continues to draw scrutiny ahead of year-end. It’s the “basis trade,” a way of profiting on the differences in prices between Treasurys and Treasury futures. While such differences can be relatively tiny, one’s potential profit or loss can be exponentially magnified when leverage is involved.In a nutshell, the basis trade takes an arbitrage approach: It involves borrowing from the repo market for leverage and financing, and then taking a short Treasury futures position and a long Treasury…

The 10-year Treasury yield continued to pull back from 5% on Friday after moving tantalizingly close to surpassing that level in the previous session.

The yield touched 5% at 5:02 p.m. Eastern time on Thursday, only to drift back down, according to Tradeweb data. It ended Friday’s New York session down by 6.3 basis points at 4.924%.

Rising Middle East tensions gave way to renewed safe-haven demand in government debt on Friday that not only sent the 10-year yield BX:TMUBMUSD10Y

lower, but dragged down rates on everything from 3-month Treasury bills BX:TMUBMUSD03M

to the 30-year bond BX:TMUBMUSD30Y.

Investors were trying to catch the proverbial falling knife by taking advantage of a cheaper 10-year Treasury note, the product of recent selloffs. Analysts warn that it’s difficult to have much short-term conviction in catching that knife, however, given the likelihood that the selloff could return.

One big reason is the onslaught of new supply from the U.S. Treasury as the result of the government’s growing borrowing needs, which is raising the risk that investors will keep demanding more compensation to hold long-dated debt to maturity.

On Oct. 30 and Nov. 1, which is the same day as the Federal Reserve’s next policy decision, Treasury is expected to provide updated guidance on its borrowing needs and auction sizes. Treasury’s refunding announcement could even upstage the Federal Open Market Committee — creating “fertile ground for a continuation of the selloff in Treasuries,” said BMO Capital Markets rates strategists Ian Lyngen and Ben Jeffery.

Over the next several weeks, “it becomes much easier to envision a surge in Treasury yields in anticipation of the upcoming coupon supply,” they wrote in a note on Friday. While the 10-year yield has stopped shy of 5%, “we continue to expect this milestone will be reached shortly.”

Stock-market investors have been focused on the prospects of a 5% 10-year yield because such a level would dent the appeal of equities and make government debt a more attractive investment by comparison.

As of Friday, the 10-year yield, used as the benchmark on everything from mortgages to student and auto loans, has jumped 163.9 basis points from its 52-week low of almost 3.29% reached on April 5. The 10-year yield hasn’t ended the New York session above 5% since July 19, 2007.

COMP

ended the day lower as the prospects of a widening conflict in the Middle East triggered a flight-to-safety trade into Treasurys.

Taking a step back, a 5% 10-year yield would imply that a Goldilocks-scenario of a U.S. economy — one that’s neither too hot or too cold, and able to sustain moderate growth — “is here to stay for a decade,” or that the Fed’s main interest-rate target needs to be materially higher on average over the next decade, according to BMO’s Lyngen and Jeffery. One of the biggest questions facing policy makers is whether the economy might be moving into a new stage in which even higher interest rates down the road could be required to cool demand and activity.

Though BMO Capital Markets is biased toward lower yields into the weekend given the absence of major economic data on Friday, technical indicators “continue to favor higher rates in the near-term,” and “our conviction that 5% will ultimately be traded through has grown.”

The stock market always overreacts, and this year it seems as if investors believe dividend stocks have become toxic. But a look at yields on quality dividend stocks relative to the market underlines what may be an excellent opportunity for long-term investors to pursue growth with an income stream that builds up over the years.

The current environment, in which you can get a yield of more than 5% yield on your cash at a bank or lock in a yield of 4.57% on a10-year U.S. Treasury note BX:TMUBMUSD10Y

or close to 5% on a 20-year Treasury bond BX:TMUBMUSD20Y

seems to have made some investors forget two things: A stock’s dividend payout can rise over the long term, and so can it is price.

It is never fun to see your portfolio underperform during a broad market swing. And people have a tendency to prefer jumping on a trend hoping to keep riding it, rather than taking advantage of opportunities brought about by price declines. We may be at such a moment for quality dividend stocks, based on their yields relative to that of the benchmark S&P 500 SPX.

Drew Justman of Madison Funds explained during an interview with MarketWatch how he and John Brown, who co-manage the Madison Dividend Income Fund, BHBFX MDMIX and the new Madison Dividend Value ETF DIVL,

use relative dividend yields as part of their screening process for stocks. He said he has never seen such yields, when compared with that of the broad market, during 20 years of work as a securities analyst and portfolio manager.

Dividend stocks are down

Before diving in, we can illustrate the market’s current loathing of dividend stocks by comparing the performance of the Schwab U.S. Equity ETF SCHD,

which tracks the Dow Jones U.S. Dividend 100 Index, with that of the SPDR S&P 500 ETF Trust SPY.

Let’s look at a total return chart (with dividends reinvested) starting at the end of 2021, since the Federal Reserve started its cycle of interest rate increases in March 2022:

FactSet

The Dow Jones U.S. Dividend 100 Index is made up of “high-dividend-yielding stocks in the U.S. with a record of consistently paying dividends, selected for fundamental strength relative to their peers, based on financial ratios,” according to S&P Dow Jones Indices.

The end results for the two ETFs from the end of 2021 through Tuesday are similar. But you can see how the performance pattern has been different, with the dividend stocks holding up well during the stock market’s reaction to the Fed’s move last year, but trailing the market’s recovery as yields on CDs and bonds have become so much more attractive this year. Let’s break down the performance since the end of 2021, this time bringing in the Madison Dividend Income Fund’s Class Y and Class I shares:

Fund

2023 return

2022 return

Return since the end of 2021

SPDR S&P 500 ETF Trust

14.9%

-18.2%

-6.0%

Schwab U.S. Dividend Equity ETF

-3.8%

-3.2%

-6.9%

Madison Dividend Income Fund – Class Y

-4.7%

-5.4%

-9.9%

Madison Dividend Income Fund – Class I

-4.7%

-5.3%

-9.7%

Source: FactSet

Dividend stocks held up well during 2022, as the S&P 500 fell more than 18%. But they have been left behind during this year’s rally.

The Madison Dividend Income Fund was established in 1986. The Class Y shares have annual expenses of 0.91% of assets under management and are rated three stars (out of five) within Morningstar’s “Large Value” fund category. The Class I shares have only been available since 2020. They have a lower expense ratio of 0.81% and are distributed through investment advisers or through platforms such as Schwab, which charges a $50 fee to buy Class I shares.

The opportunity — high relative yields

The Madison Dividend Income Fund holds 40 stocks. Justman explained that when he and Brown select stocks for the fund their investible universe begins with the components of the Russell 1000 Index RUT,

which is made up of the largest 1,000 companies by market capitalization listed on U.S. exchanges. Their first cut narrows the list to about 225 stocks with dividend yields of at least 1.1 times that of the index.

The Madison team calculates a stock’s relative dividend yield by dividing its yield by that of the S&P 500. Let’s do that for the Schwab U.S. Equity ETF SCHD

(because it tracks the Dow Jones U.S. Dividend 100 Index) to illustrate the opportunity that Justman highlighted:

Index or ETF

Dividend yield

5-year Avg. yield

10-year Avg. yield

15-year Avg. yield

Relative yield

5-year Avg. relative yield

10-year Avg. relative yield

15-year Avg. relative yield

Schwab U.S. Dividend Equity ETF

3.99%

3.41%

3.20%

3.16%

2.6

2.1

1.8

1.6

S&P 500

1.55%

1.62%

1.79%

1.92%

Source: FactSet

The Schwab U.S. Equity ETF’s relative yield is 2.6 — that is, its dividend yield is 2.6 times that of the S&P 500, which is much higher than the long-term averages going back 15 years. If we went back 20 years, the average relative yield would be 1.7.

Examples of high-quality stocks with high relative dividend yields

After narrowing down the Russell 1000 to about 225 stocks with relative dividend yields of at least 1.1, Justman and Brown cut further to about 80 companies with a long history of raising dividends and with strong balance sheets, before moving further through a deeper analysis to arrive at a portfolio of about 40 stocks.

When asked about oil companies and others that pay fixed quarterly dividends plus variable dividends, he said, “We try to reach out to the company and get an estimate of special dividends and try to factor that in.” Two examples of companies held by the fund that pay variable dividends are ConocoPhillips COP, -0.29%

and EOG Resources Inc. EOG, +0.52%.

Since the balance-sheet requirement is subjective “almost all fund holdings are investment-grade rated,” Justman said. That refers to credit ratings by Standard & Poor’s, Moody’s Investors Service or Fitch Ratings. He went further, saying about 80% of the fund’s holdings were rated “A-minus or better.” BBB- is the lowest investment-grade rating from S&P. Fidelity breaks down the credit agencies’ ratings hierarchy.

Justman named nine stocks held by the fund as good examples of quality companies with high relative yields to the S&P 500:

Now let’s see how these companies have grown their dividend payouts over the past five years. Leaving the companies in the same order, here are compound annual growth rates (CAGR) for dividends.

Before showing this next set of data, let’s work through one example among the nine stocks:

If you had purchased shares of Home Depot Inc. HD, -0.39%

five years ago, you would have paid $193.70 a share if you went in at the close on Oct. 10, 2018. At that time, the company’s quarterly dividend was $1.03 cents a share, for an annual dividend rate of $4.12, which made for a then-current yield of 2.13%.

If you had held your shares of Home Depot for five years through Tuesday, your quarterly dividend would have increased to $2.09 a share, for a current annual payout of $8.36. The company’s dividend has increased at a compound annual growth rate (CAGR) of 15.2% over the past five years. In comparison, the S&P 500’s weighted dividend rate has increased at a CAGR of 6.24% over the past five years, according to FactSet.

That annual payout rate of $8.36 would make for a current dividend yield of 2.79% for a new investor who went in at Tuesday’s closing price of $299.22. But if you had not reinvested, the dividend yield on your five-year-old shares (based on what you would have paid for them) would be 4.32%. And your share price would have risen 54%. And if you had reinvested your dividends, your total return for the five years would have been 75%, slightly ahead of the 74% return for the S&P 500 SPX during that period.

Home Depot hasn’t been the best dividend grower among the nine stocks named by Justman, but it is a good example of how an investor can build income over the long term, while also enjoying capital appreciation.

Here’s the dividend CAGR comparison for the nine stocks:

This isn’t to say that Justman and Brown have held all of these stocks over the past five years. In fact, Lowe’s Cos. LOW, +0.27%

was added to the portfolio this year, as was United Parcel Service Inc. UPS, -0.16%.

But for most of these companies, dividends have compounded at relatively high rates.

When asked to name an example of a stock the fund had sold, Justman said he and Brown decided to part ways with Verizon Communications Inc. VZ, -0.94%

last year, “as we became concerned about its fundamental competitive position in its industry.”

Summing up the scene for dividend stocks, Justman said, “It seems this year the market is treating dividend stocks as fixed-income instruments. We think that is a short-term issue and that this is a great opportunity.”

The yield on the 30-year Treasury bond briefly rose above 5% again on Friday, opening the door to the likelihood of a more sustainable rise above that mark and the risk that the benchmark 10-year yield follows — moves which could wreak havoc across financial markets.

One big reason is that investors are likely to demand greater compensation for taking risk as yields hover around some of the highest levels of the past 16 years, asset managers said. Corporate credit spreads could keep widening in a sign of worsening economic conditions and higher overall risk. And with returns on government debt becoming a more favorable option for investments, the stock market may be vulnerable to repeated drubbings.

Stock investors nonetheless shook off Friday’s stunning official jobs report for September, which saw the U.S. add almost twice as many jobs as forecasters had expected. All three major stock indexes DJIA

COMP

finished higher even though yields climbed on everything from the 1-month T-bill BX:TMUBMUSD01M

to the 30-year bond BX:TMUBMUSD30Y.

The yield on the long bond finished at 4.941% — the highest level since Sept. 20, 2007 — after rising past 5% during the New York morning. The rate on the 10-year note BX:TMUBMUSD10Y

ended at 4.783%, the second-highest level of this year.

Yields are returning to more normal-looking levels that prevailed before the 2007-2009 recession as the result of aggressive selloffs in government debt. More important than the absolute level of yields is the speed with which they have been heading to 5%. In the words of analyst Ajay Rajadhyaksha of Barclays earlier this week, there’s “no magic level” that will turn the current selloffs into a rally, and stocks have substantial room to reprice lower before bonds stabilize.

“I think the market isn’t breaking yet, but a 5% 10-year yield is coming,” said Robert Daly, who manages $4.5 billion in assets as director of fixed income at Glenmede Investment Management in Philadelphia. “We’re already here on 30s and not that far away on 10s. Investors are trying to figure what level breaks the market, and I don’t think you can put your finger on the pulse as to what that level is.”

Still, “a higher level of interest rates and yields is going to start having ramifications for broader markets at large,” leaving many investors hesitant to buy just about anything due to the volatility, Daly said via phone on Friday, after the release of September’s hot payrolls data.

Friday’s data, which showed the U.S. creating 336,000 new jobs last month or almost double what economists had expected, is opening the door to a possible interest rate hike by the Federal Reserve on Nov. 1. The strong labor market means the Fed’s higher-for-longer mantra in rates is still in play and “the market is in a tenuous position to navigate all these things because of all the uncertainty,” Daly said.

“Yields sustainably above 5% for a longer period of time will act as a weight on the market in terms of how you value risk compensation,” he said. “Investors are going to ask for more compensation to take risk and when you see liquidity evaporate more and more, that’s what’s going to turn the market over.”

Friday’s price action was the second time this week that data related to the robust U.S. labor market has triggered a bonds selloff. On Tuesday, a snapback in U.S. job openings for August sent the 10- and 30-year yields to their highest closing levels since August-September of 2007.

The next day, high-grade corporate-credit spreads widened for a seventh consecutive session. Daniel Krieter, a fixed-income strategist at BMO Capital Markets, wrote that “if rates continue to move higher or simply remain at these elevated levels for a significant period of time, it is going to have a pronounced effect on the creditworthiness of corporate borrowers, particularly in the high yield space.”

In a note on Friday, Krieter’s colleagues, rates strategists Ian Lyngen and Ben Jeffery, wrote that “it’s not difficult to envision 10s maintain a range between 4.75% and 5.00%.”

“The longer 10s hold this range, the more convinced the market will become that elevated yields are here to stay,” Lyngen and Jeffery said. “Admittedly, we’ve been surprised by the muted response in U.S. equities from the spike in yields and expect that’s due in part to the expectation for a swift reversal. In the event a correction fails to materialize, stocks will be overdue for a more meaningful reckoning.”

The risk of “something breaking” will remain top of mind and “there is no shortage of risks facing equities and credit as rates continue to climb,” they added. “It’s not only the outright level of yields, but the length of time that borrowing costs stay elevated will also hold implications for risk asset valuations.”

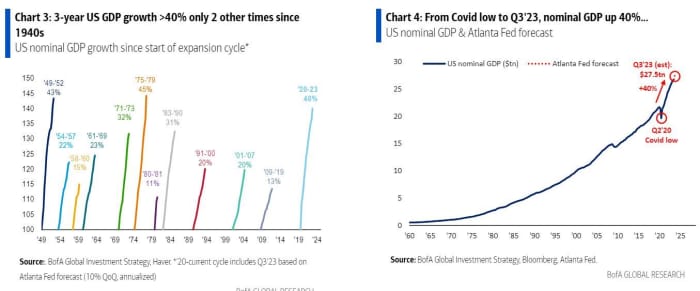

The 10-year Treasury bond is on track for a third year of losses in 2023, something that hasn’t happened in 250 years of U.S. history.

In short, it has never happened, say strategists at Bank of America.

The return for investors putting money in that bond BX:TMUBMUSD10Y

stands at negative 0.3% so far in 2023, after a 17% slump in 2022 and a 3.9% drop in 2021, the bank’s strategists, led by Michael Hartnett, pointed out in a note on Friday.

Here’s a visual on that:

That reflects a “staggering 40% jump in U.S. nominal GDP growth” — factoring in growth and inflation — “since the COVID lows of 2020,” they said, providing this chart:

Bond returns have suffered this year as the Federal Reserve has continued its interest-rate-hiking campaign aimed at getting inflation under control. The “big picture in the 2020s vs. the 2010s is lower stock and bond returns, which we would expect to continue given political, geopolitical, social [and] economic trends,” said Hartnett and the team.

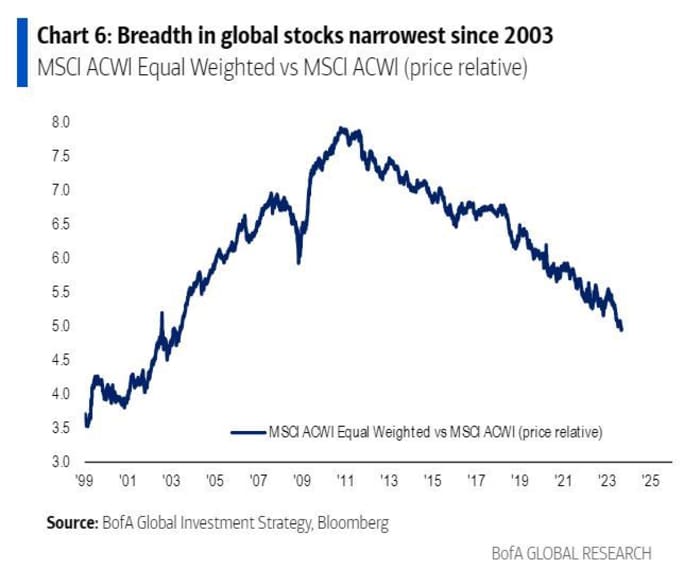

SPX,

but the bounce since COVID pandemic restrictions began to be lifted has been very concentrated in U.S. stocks, especially the technology sector, with breadth in global markets “breathtakingly bad,” the analysts said. Breadth refers to the number of stocks actively participating in a rally.

Breadth is the worst since 2003 for the MSCI ACWI, which captures large- and midcap-stock representation across 23 developed markets and 24 emerging ones.

As for the latest weekly flows into funds, Bank of America reported that $10.3 billion went to stocks, $6.5 billion to cash and $1.7 billion to bonds, with $300 million draining from gold GC00, -0.06%.

The yield on the 10-year Treasury was holding steady on Friday at 4.102% after data showed the U.S. economy generated 187,000 jobs in August, but the unemployment rate rose to 3.8% from 3.5%, and job gains were revised lower for July and June.

The 10-year Treasury bond is on track for a third year of losses in 2023, something that hasn’t happened in 250 years of U.S. history.

In short, it has never happened, say strategists at Bank of America.

The return for investors putting money in that bond BX:TMUBMUSD10Y

stands at negative 0.3% so far in 2023, after a 17% slump in 2022 and a 3.9% drop in 2021, the bank’s strategists, led by Michael Hartnett, pointed out in a note on Friday.

Here’s a visual on that:

That reflects a “staggering 40% jump in U.S. nominal GDP growth” — factoring in growth and inflation — “since the COVID lows of 2020,” they said, providing this chart:

Bond returns have suffered this year as the Federal Reserve has continued its interest-rate-hiking campaign aimed at getting inflation under control. The “big picture in the 2020s vs. the 2010s is lower stock and bond returns, which we would expect to continue given political, geopolitical, social [and] economic trends,” said Hartnett and the team.

SPX,

but the bounce since COVID pandemic restrictions began to be lifted has been very concentrated in U.S. stocks, especially the technology sector, with breadth in global markets “breathtakingly bad,” the analysts said. Breadth refers to the number of stocks actively participating in a rally.

Breadth is the worst since 2003 for the MSCI ACWI, which captures large- and midcap-stock representation across 23 developed markets and 24 emerging ones.

As for the latest weekly flows into funds, Bank of America reported that $10.3 billion went to stocks, $6.5 billion to cash and $1.7 billion to bonds, with $300 million draining from gold GC00, +0.02%.

The yield on the 10-year Treasury was holding steady on Friday at 4.102% after data showed the U.S. economy generated 187,000 jobs in August, but the unemployment rate rose to 3.8% from 3.5%, and job gains were revised lower for July and June.

While negative returns might stir bad memories of last year’s shocking losses for bonds, stocks and nearly everything else, investors holding Treasury debt issued at 2023’s higher yields might want to sit back and take stock.

“This is the top thing we hear,” said Ryan Murphy, director of fixed-income business development at Capital Group, of evaporating returns in what’s been a tough August. “You saw the worst bond market in 40 years last year. Investors, they are tired, and feel beaten up.”

Murphy’s message to clients is this: “In bonds, you earn the money over time.” And those dwindling bond returns since January? “Approach it with a deep breath, and know this is going to work out in the end.”

Capital Group’s laid-back style and lack of “a star CEO” earned it recognition by Institutional Investor in March as “a new bond leader” without a king, in large part because it attracted $100 billion in funds over the past five years, or twice the total of its peers.

Recent volatility in interest rates again zapped yearly gains in many bond funds, as Fed officials continued to warn that a roaring labor market and robust spending could keep inflation from receding to the central bank’s 2% annual target.

The spike in long-term bond yields makes older, lower-yielding securities look comparatively less attractive. That’s reflected in the yearly return on a key Bloomberg U.S. government bond and note index, which turned negative for the first time since March (see chart), when several regional banks failed, stoking fears of a broader banking crisis.

Returns on U.S. government bonds turn negative for the year.

FactSet

However, a look back at August 2022 shows the 10-year Treasury yield starting around 2.6%, according to FactSet.

By contrast, Treasury bill yields BX:TMUBMUSD06M

neared 5.5% on Thursday, or “north of anything we’ve seen over the past 15 years,” Murphy said. And for investors looking to lock in longer-term yields, the 10-year Treasury rate BX:TMUBMUSD10Y

touched 4.307% on Thursday, its highest level since November 2007, according to Dow Jones Market Data.

“It’s becoming more expensive for the government and companies to finance debt because of the rapid climb in rates,” Murphy said of the drag of higher long-term interest rates.

On the flip side, it’s also been one of the best stretches for lenders and bond investors in terms of getting paid to act as creditors since the 2007-2008 global financial crisis, but without a U.S. recession — or at least not yet.

What’s also different from last year is that the Fed already jacked up interest rates to a 22-year high of 5.25%-5.5% in July, and has signaled it’s likely nearly finished with hikes in this cycle.

Record cash on the sidelines

Murphy pointed to a mountain of cash on the sidelines, in the form of assets in money-market funds, as another potential stabilizer for markets.

Assets in money-market funds hit a record $5.57 trillion for the week ending Wednesday, according to data from the Investment Company Institute.

“What’s really interesting is that there’s been two bursts of investors going into money-market funds. There was a big shift right at the onset of COVID, and another burst over the past 12-18 months since the beginning of the rate-hiking cycle,” Murphy said.

Looking back to 2008, he pointed to a similar buildup in money-market assets, and a roughly $1.1 trillion wall of cash subsequently leaving the sector, as financial assets began to recover in the wake of the financial crisis.

“What we did see, while not all of it, was a healthy amount went back into fixed-income in the following years,” Murphy said.

Stocks closed lower Thursday and were headed for another week of losses, with the Dow Jones Industrial Average DJIA

2.3% lower on the week so far, the S&P 500 index SPX

down 2.1% and the Nasdaq Composite Index off 2.4%, according to FactSet.

A worsening U.S. fiscal situation caught stock and bond investors off guard in the past week and now a round of approaching government auctions is about to provide a crucial test for Treasurys.

The question in the days ahead is whether risks to the demand for U.S. government debt are growing. If so, that could put upward pressure on Treasury yields, which would undermine the performance of stocks. However, if investors end up caring less about the fiscal situation than they do about the possibility of slowing economic growth and decelerating inflation, government debt’s safe-haven appeal could be reinforced, putting a limit on how high yields might go.

Concern about the deteriorating fiscal outlook was a factor behind the past week’s rise in long-term Treasury yields. Ten- BX:TMUBMUSD10Y

and 30-year yields BX:TMUBMUSD30Y

respectively jumped to 4.188% and 4.304% on Thursday, the highest levels since early November, as investors sold off long-term government debt — which took the shine off U.S. stocks. By Friday, though, a moderating pace of U.S. job creation for July sent yields into reverse, giving equities a temporary lift during the final trading session of the week.

At issue is the extent to which potential buyers of Treasurys may be deterred by Fitch Ratings’ Aug. 1 decision to cut the U.S. government’s top AAA rating, at a time when the government is about to unleash what Barclays rates strategists describe as a “tsunami” of supply. A total of $103 billion in 3-, 10-and 30-year Treasurys come up for sale between Tuesday and Thursday. In addition, a spate of Treasury bills are scheduled to be auctioned starting on Monday.

Gene Tannuzzo, global head of fixed income at Boston-based Columbia Threadneedle Investments, said that while he and his team still have room to add T-bills to the government money-market funds they oversee during the week ahead, they haven’t made up their minds about whether to buy more longer-dated maturities for their bond funds.

“While we are comfortable that the Fed is at or near the end of its rate hikes, there are a lot more questions about the durability of the economic recovery, the degree that inflation will remain low, and the risk premium that needs to be put in at the long end,” Tannuzzo said via phone.

Treasury’s $1 trillion third-quarter borrowing plans, along with some technical issues and the Bank of Japan’s decision to switch to a more flexible yield-curve control approach, might reduce demand for U.S. government debt, he said. Columbia Threadneedle managed $617 billion as of June.

“One can’t ignore the risk of an unruly rise in yields, but our view is that this is a low risk and what the Treasury auctions may produce instead is ‘indigestion,’ driven by poor technicals and low liquidity, Fitch’s downgrade, and the Bank of Japan action — and by the end of August, we should be past much of this,” he told MarketWatch.

Risks to the demand for Treasurys may become obvious soon, given Tuesday-Thursday’s $103 billion in total sales of 3-, 10- and 30-year securities, according to analyst John Canavan of U.K.-based Oxford Economics. The main “question mark” for the market’s ability to absorb the increased Treasury issuance will be whether or not domestic investment funds continue to show interest, Canavan wrote in a note distributed on Friday.

Source: Oxford Economics.

“ ‘My suspicion is that with higher rates comes equally solid demand’ at upcoming auctions.”

— John Flahive, head of fixed income at BNY Mellon Wealth Management

Market players have had little difficulty absorbing Treasury coupon issuances in recent years because of flight-to-safety trades made after the U.S. onset of the Covid-19 pandemic in 2020. Now, however, increased auction sizes are being accompanied by still-elevated inflation, better-than-expected economic growth, and the possibility of more rate hikes by the Federal Reserve — which is likely to complicate the market’s ability to absorb the increased supply “without hiccups,” Canavan said.

On the flip side of the debate is John Flahive, head of fixed income at BNY Mellon Wealth Management in Boston, which managed $286 billion in assets as of June. He said equity markets will continue to be much more focused on economic developments and earnings. And as long as the latter of the two remains robust, stocks “can grind higher in a low-volatility environment,” Flahive said via phone.

Saying he does not expect his team to be a major participant in the Treasury auctions, Flahive said that the bond market’s reaction in the past week was “a little overdone” and “we always felt that there was a limited to how much yields could go up to reflect more government debt.”

“My suspicion is that with higher rates comes equally solid demand” at upcoming auctions, he said. “I’m still optimistic about rates going back down over time as the result of a slowing economy and decelerating inflation. We continue to like the bond market and see a better-than-even chance that yields go down as the economy continues to weaken in the quarters ahead.”

Friday’s reaction to July’s official jobs report, which showed the U.S. added a modest 187,000 new jobs, provided a breather from the past week’s run-up in Treasury yields.

On Friday, the 30-year Treasury yield fell 9 basis points to 4.214%, yet still ended with its biggest weekly gain since early February. The 10-year rate, which dropped 12.8 basis points to 4.06%, finished with a third straight week of advances.

Stocks fell Friday, leaving major indexes with weekly declines. The Dow Jones Industrial Average DJIA

posted a 1.1% weekly fall, while the S&P 500 SPX

shed 2.3% and the Nasdaq Composite COMP

retreated 2.9%. The soft start to August comes after a run of sharp gains for equities. The S&P 500 remains up 16.6% for the year to date.

The economic calendar for the week ahead includes U.S. inflation updates.

On Monday, June consumer-credit data is set to be released. Tuesday brings the NFIB’s small business optimism index, plus data on the U.S. trade balance and wholesale inventories. Then on Thursday, weekly initial jobless claims and the July consumer-price index are released. That’s followed on Friday by the producer-price index for last month and an August consumer-sentiment reading.

Meanwhile, portfolio manager and fixed-income analyst John Luke Tyner at Alabama-based Aptus Capital Advisors, which manages roughly $5 billion in assets, said he plans to follow the Treasury auctions, but doesn’t usually participate in them.

“One of the biggest trends we’ve seen is the continued increase in the issuance amounts from Treasury. Whatever we are budgeting for is never enough, which justifies the Fitch downgrade,” Tyner said via phone. “It’s tough to say people aren’t going to buy U.S. debt, but you’ve got to entice them to buy duration and take the risk.

“The U.S. is not an emerging market, but ultimately we are going to see the market rate that participants require be higher, with a notable uptick in term premia,” he said. “What we could see in the face of all this issuance is a grind up in yields on an auction-by-auction basis. If I look at the technicals, a 4.9%-5% yield on the 10-year note seems in the cards,” and “it will be difficult for stocks to hold or expand from full valuations as rates run up.”

Worries about a possible policy tweak by the Bank of Japan threw a wet blanket on a stretched U.S. stock-market rally Thursday, with the Dow Jones Industrial Average snapping its longest winning streak since 1987 after the 10-year Treasury yield surged back above the 4% level.

The Japanese yen also strengthened after a news report said policy makers on Friday would discuss a possible tweak to the Bank of Japan’s so-called yield-curve control policy that would loosen the cap on long-dated government bond yields.

Nikkei, without citing sources, reported that BOJ officials would talk about the matter at Friday’s policy meeting and that the potential change would allow the yield on the 10-year Japanese government bond TMBMKJP-10Y, 0.440%

to trade above its cap of 0.5% “to some degree.”

‘Ultimate fear’

Why is that a negative for U.S. Treasurys and, in turn, U.S. stocks?

The “ultimate fear” is that Japanese investors, who have vast holdings of U.S. fixed income, including Treasury notes and other securities, “begin to see a higher level of yields in their own backyard,” Torsten Slok, chief economist at Apollo Global Management, told MarketWatch in a phone interview. That could prompt heavy liquidation of those U.S. positions as investors repatriate holdings to reinvest the proceeds at home.

That dynamic explains the knee-jerk reaction that saw the 10-year U.S. Treasury yield TMUBMUSD10Y, 4.004%

surge more than 16 basis points to end above 4%, he said. Yields rise as debt prices fall.

The surge in yields, in turn, saw stocks give up early gains, with U.S. indexes ending lower across the board.

What is yield curve control?

The Bank of Japan began implementing yield curve control, or YCC, in 2016, a policy that aims to keep government bond yields low while ensuring an upward-sloping yield curve. Under YCC, the BOJ buys whatever amount of JGBs is necessary to ensure the 10-year yield remains below 0.5%.

Nikkei said a possible tweak would allow gradual increases in the yield above 0.5%, but would clamp down on any sudden spikes, allowing the BOJ to rein in fluctuations driven by speculators.

Global market participants are sensitive to changes in YCC. The BOJ sent shock waves through markets in December when it lifted the cap from 0.25% to 0.5%. Investors were rattled by the prospect of the Bank of Japan giving up its role as the remaining low-rate anchor among major central banks.

BOJ Gov. Kazuo Ueda in May said the bank would start shrinking its balance sheet and end its yield-curve control policy if a 2% inflation looks achievable and sustainable after many years of undershooting.

Yen rallies

The yield on the 10-year JGB has traded above 0.4%, but remained below the 0.5% cap. Continued interest rate rises by the Federal Reserve and other major central banks in the past year have raised worries that the 10-year JGB yield could test the limit, Nikkei reported. Those rate hikes, meanwhile, have added pressure to the yen, whose weakness is seen contributing to inflation pressures.

The yen USDJPY, -0.02%

strengthened following the report. The U.S. dollar was off 0.5% versus the currency, fetching 139.48 yen.

The Dow Jones Industrial Average DJIA, -0.67%

ended the day down nearly 240 points, or 0.7%, snapping a 13-day winning streak, while the S&P 500 SPX, -0.64%

declined 0.6% and the Nasdaq Composite COMP, -0.55%

lost 0.5%.

Japanese stocks have solidly outpaced strong gains for U.S. equities in 2023, with the Nikkei 225 NIK, +0.68%

up 26% so far this year versus an 18.7% rise for the S&P 500.

Investors are waiting to see what the Bank of Japan actually has to say.

While the Nikkei report helped “exaggerate” a selloff in Treasurys, the market may be inoculated against bigger swings after the BOJ’s December adjustment to the rate band, said Ian Lyngen and Benjamin Jeffery, rates strategists at BMO Capital Markets, in a note.

The analysts said they expect that “the magnitude of the follow through repricing in U.S. rates will be comparatively more contained than would otherwise be expected.”

More recently, the weak yen has raised the cost of hedging long Treasury positions for Japanese investors. So a stronger yen resulting from a shift toward tighter policy would help make hedging costs for owning Treasurys less onerous for Japanese investors as well, Lyngen and Jeffery wrote, “which over the longer term may begin to make Treasurys more attractive to Japanese buyers and add to the list of sources for duration demand.”

That could make U.S. debt more attractive to new Japanese buyers, Slok agreed.

But that’s oveshadowed by the near-term worry, Slok said, that existing Japanese investors will be inclined to sell Treasurys. Flow data will be very much in focus if the Bank of Japan follows through on the apparent trial balloon floated in the Nikkei report.

Investors will be watching, he said, to see “if the train is leaving the station.”

House Speaker Kevin McCarthy on Tuesday said he “didn’t see any new movement” toward ending Washington’s standoff over the debt ceiling, as he assessed how a much-anticipated meeting on the issue went.

President Joe Biden hosted the meeting at the White House with the country’s four top lawmakers, and beforehand analysts had predicted it would not result in a deal.

As President Joe Biden prepares to host a much-anticipated meeting on the U.S. debt ceiling with the country’s four top lawmakers, analysts are predicting there won’t be a deal yet on this issue.

If the meeting at the White House, scheduled for around 4 p.m. Eastern time Tuesday, were to conclude with an agreement, that would be very surprising, said Chris Krueger, managing director at TD Cowen’s Washington Research Group, in a note on Tuesday.

Australian government bond prices plunged and the country’s currency surged after the central bank surprised markets on Tuesday with another rate hike.

The Reserve Bank of Australia raised its benchmark borrowing costs by 25 basis points to 3.85% after traders had expected no move.

The RBA said inflation, which is running at an annual rate…

Do you want the good news about the Federal Reserve and its chairman Jerome Powell, the other good news…or the bad news?

Let’s start with the first bit of good news. Powell and his fellow Fed committee members just hiked short-term interest rates another 0.25 percentage points to 4.75%, which means retirees and other savers are getting the best savings rates in a generation. You can even lock in that 4.75% interest rate for as long as five years through some bank CDs. Maybe even better, you can lock in interest rates of inflation (whatever it works out to be) plus 1.6% a year for three years, and inflation (ditto) plus nearly 1.5% a year for 25 years, through inflation-protected Treasury bonds. (Your correspondent owns some of these long-term TIPS bonds—more on that below.)

The second bit of good news is that, according to Wall Street, Powell has just announced that happy days are here again.

The S&P 500 SPX, +1.05%

jumped 1% due to the Fed announcement and Powell’s press conference. The more volatile Russell 2000 RUT, +1.49%

small cap index and tech-heavy Nasdaq Composite COMP, +2.00%

both jumped 2%. Even bitcoin BTCUSD, +1.00%

rose 2%. Traders started penciling in an end to Federal Reserve interest rate hikes and even cuts. The money markets now give a 60% chance that by the fall Fed rates will be lower than they are now.

It feels like it’s 2019 all over again.

Now the slightly less good news. None of this Wall Street euphoria seemed to reflect what Powell actually said during his press conference.

Powell predicted more pain ahead, warned that he would rather raise interest rates too high for too long than risk cutting them too quickly, and said it was very unlikely interest rates would be cut any time this year. He made it very clear that he was going to err on the side of being too hawkish than risk being too dovish.

Actual quote, in response to a press question: “I continue to think that it is very difficult to manage the risk of doing too little and finding out in 6 or 12 months that we actually were close but didn’t get the job done, inflation springs back, and we have to go back in and now you really do have to worry about expectations getting unanchored and that kind of thing. This is a very difficult risk to manage. Whereas…of course, we have no incentive and no desire to overtighten, but if we feel that we’ve gone too far and inflation is coming down faster than we expect we have tools that would work on that.” (My italics.)

If that isn’t “I would much rather raise too much for too long than risk cutting too early,” it sure sounded like it.

Powell added: “Restoring price stability is essential…it is our job to restore price stability and achieve 2% inflation for the benefit of the American public…and we are strongly resolved that we will complete this task.”

Meanwhile, Powell said that so far inflation had really only started to come down in the goods sector. It had not even begun in the area of “non-housing services,” and these made up about half of the entire basket of consumer prices he’s watching. He predicts “ongoing increases” of interest rates even from current levels.

And so long as the economy performs in line with current forecasts for the rest of the year, he said, “it will not be appropriate to cut rates this year, to loosen policy this year.”

Watching the Wall Street reaction to Powell’s comments, I was left scratching my head and thinking of the Marx Brothers. With my apologies to Chico: Who you gonna believe, me or your own ears?

Meanwhile, on long-term TIPS: Those of us who buy 20 or 30 year inflation-protected Treasury bonds are currently securing a guaranteed long-term interest rate of 1.4% to 1.5% a year plus inflation, whatever that works out to be. At times in the past you could have locked in a much better long-term return, even from TIPS bonds. But by the standards of the past decade these rates are a gimme. Up until a year ago these rates were actually negative.

Using data from New York University’s Stern business school I ran some numbers. In a nutshell: Based on average Treasury bond rates and inflation since the World War II, current TIPS yields look reasonable if not spectacular. TIPS bonds themselves have only existed since the late 1990s, but regular (non-inflation-adjusted) Treasury bonds of course go back much further. Since 1945, someone owning regular 10 Year Treasurys has ended up earning, on average, about inflation plus 1.5% to 1.6% a year.

“Real yields of 1.5% today are very attractive,” he tells me. “We know that real yields are in a centuries’ long secular decline because markets become more efficient and real growth is declining due to demographics and other factors. That means that every year real yields drop a little bit more and the average over the next 10 or 30 years is likely to be lower than 1.5%. Looking ahead, TIPS are priced as a bargain right now and they provide secure income, 100% protected against inflation and backed by the full faith and credit of the United States government.”

Meanwhile the bond markets are simultaneously betting that Jerome Powell will win his fight against inflation, while refusing to believe him when he says he will do whatever it takes.

Make of that what you will. Not having to care too much about what the bond market says is yet another reason why I generally prefer inflation-protected Treasury bonds to the regular kind.

In the first trading day of the new year, U.S. financial markets were bogged down by the almost universal view that a recession is approaching.

A stocks rally fizzled out within the first 30 minutes of opening gains. Gold, a traditional safe haven, touched its highest level in six months, rising alongside silver and platinum. And 10- to 30-year Treasury yields, nestled in what’s known as the long end of the bond market, fell as investors jumped into government bonds — driving those yields down respectively to around 3.8% and 3.9%.

At the heart of the market moves was the strong sense that an economic downturn is all but inevitable at this point, following months of central bank interest rate hikes around the world — with the International Monetary Fund‘s chief Kristalina Georgieva warning that the economies of the U.S., European Union and China are all slowing simultaneously. Scion Asset Management founder Michael Burry said he expects another “inflation spike” after recession rocks the U.S., and former New York Fed President William Dudley said a U.S. economic downturn “is pretty likely.”

“Recession is what everyone is betting on,” said Ben Emons, senior portfolio manager and head of fixed income/macro strategy at NewEdge Wealth in New York. “And, the thinking is, therefore inflation will decelerate faster than what people anticipate and the Federal Reserve could move quicker to a rate cut. But the whole narrative of a recession is something that’s bothering the stock market and other asset classes because it will mean shrinking margins and earnings.”

Indeed, a much-hoped for rally in stocks around this time of the year, known as the “Santa Claus rally,” is failing to materialize, with just one more trading session left on Wednesday before the end of that seasonal period. The in-house research arm of BlackRock Inc., the world’s largest asset manager, described recession as “foretold” on Tuesday and said it is “tactically underweight” developed-market stocks, which are still “not pricing the recession we see ahead.” That’s the case even though global stocks ended 2022 down by 18% and bonds fell 16%, said Jean Boivin, head of the BlackRock Investment Institute, and others.

Sources: BlackRock Investment Institute, Refinitiv, Bloomberg.

“We see stock rallies built on hopes for rapid rate cuts fizzling. Why? Central banks are unlikely to come to the rescue in recessions they themselves caused to bring inflation down to policy targets. Earnings expectations are also still not fully reflecting recession, in our view. But markets are now pricing in more of the damage we see – and as this continues, it would pave the way for us to turn more positive on risk assets,” Boivin and others at BlackRock Investment Institute wrote in a note Tuesday.

“Even with a recession coming, we think we are going to be living with inflation,” they said.

Interestingly, the financial market’s focus on a 2023 recession is being accompanied by the view that such a downturn will help cure inflation, allowing central banks to end, slow, or even reverse their monetary policy-tightening campaigns. That view was buttressed by Tuesday’s release of inflation data out of Germany, which showed that the annual rate from the consumer price index fell by more than expected in December to a four-month low. Back in the U.S., fed funds futures traders priced in a greater likelihood of a smaller-than-usual, 25-basis point rate hike by the Federal Reserve in February.

As of Tuesday afternoon, all three major U.S. stock indexes DJIASPX were down, led by a 1.3% drop in the Nasdaq Composite.

Meanwhile, a rally in Treasurys moderated relative to earlier in the day. The 10-year Treasury yield TMUBMUSD10Y, 3.785%,

a benchmark for borrowing costs, dropped back to levels last seen around Dec. 23-26, a period when conditions were “totally illiquid and no one was trading,” said Emons of NewEdge Wealth.

U.S. stocks turned higher at midday Tuesday, as investors gauged whether the recent losing streak in equities has been overdone. Traders also weighed the potential rippled effects of the Bank of Japan’s surprise announcement to put a higher ceiling on government bond yields.

How are stocks are trading

The S&P 500 SPX, +0.45%

rose 9 points, or 0.2%, to 3,814.

The Dow Jones Industrial Average DJIA, +0.63%

was up 114 points, or 0.3%, at 32,866.

The Nasdaq Composite COMP, -1.76%

was up 26 points, or 0.2%, to 10,578.

Stocks fell for a fourth straight session on Monday. The Nasdaq Composite was down 6.3% over that stretch, and has retreated 32.6% so far this year.

What’s driving markets

Wall Street is looking to avoid a fifth straight losing session, while investors weighed the implications of a surprise monetary policy shift by the Bank of Japan.

The S&P 500 closed the previous day near a six-week low as concerns intensify that central banks’ hiking of borrowing costs to combat inflation will push economies into recession and cause corporate earnings to fall.

The Bank of Japan had been an outlier among major central banks by having maintained rates at the zero lower bound, while others embarked on their biggest tightening cycle in a generation, noted Henry Allen, strategist at Deutsche Bank.

But on Tuesday the BoJ doubled the cap on the country’s 10-year bond, from 0.25% to 0.5%, causing the yen to jump more than 3%, while whacking equities in the region and giving U.S. stock investors more to consider.

The BoJ kept its short-term interest rate at minus 0.1%, but the raising of the yield at which it will allow bonds to trade was seen as a step towards the ending of its era of ultra-loose monetary policy. The Nikkei 225 NIK, -2.46%

fell 2.5%.

“It’s important not to underestimate the impact this could have, because tighter BoJ policy would remove one of the last global anchors that’s helped to keep borrowing costs at low levels more broadly,” Allen added.

The 10-year U.S. Treasury yield TMUBMUSD10Y, 3.692%

stood at 3.685% as the equivalent maturity Japanese government bond TMBMKJP-10Y, 0.417%

climbed to 0.418%.

However, some analysts argued that recent drops in U.S. stocks were starting to go too far.

“I think we’ve been oversold the last couple weeks,” Joe Saluzzi, partner at Themis Trading, said in a phone interview. There’s the macroeconomic pressures weighing on stocks, but Saluzzi said the recent run of heavy selling may also be partly attributable to year-end tax loss harvesting in order to reap tax benefits from the year’s losses.

The Bank of Japan announcement may have unsettled some early trading, he said. But ultimately, there’s just one central bank in the mind of U.S. equity investors, Saluzzi noted.

Until the Federal Reserve is clear that its own interest rate hikes are complete, markets will be choppy, Saluzzi said. “The economy is weakening. No matter what the Fed said, they are not going to be doing much more,” he said.

“U.S. equity markets remain trending lower in the short run, but are close to near-term support which should materialize between 12/21-12/23 at marginally lower levels,” wrote Mark Newton, head of technical strategy at Fundstrat, in a note to clients.

“The percentage of stocks above their 20-day moving average is nearing single-digit territory, which normally provides relief for longs. Overall, I don’t expect markets to go down much further in December, and risk/reward for trading shorts looks sub-par with SPX not far above targets at 3,725.

“This might materialize at 3775-3800 before allowing for a minor bounce, and then retest into Wednesday-Friday. However, I’m fully expecting a bounce next week into year-end, regardless if it proves temporary,” Newton concluded.

Tuesday morning data gave another window to a slowing economy. Building permits and housing starts were both down in November.

Companies in focus

3M Co. MMM, -0.34%

is phasing out the manufacturing of so-called “forever chemicals” like fluoropolymers, fluorinated fluids, and PFAS-based additive products by the end of 2025. The phase-out process will include taking mostly non-cash charges of $1.3 billion to $2.3 billion to exit the line of business. Shares are down 0.5% in mid-morning trading.

Wells Fargo& Co. WFC, -1.06%

is being ordered to pay a civil penalty of $1.7 billion and return more than $2 billion to consumers, according to the Consumer Financial Protection Bureau. The regulator said the fines and consumer redress are connected to “widespread mismanagement” of auto loans, mortgages and deposit accounts, the CFPB said. Shares were off 1.1% in mid-morning trading.