Coinbase, one of the nation’s top cryptocurrency exchanges by trading volume, has agreed to pay $100 million as part of a settlement with New York regulators who allege the firm violated anti-money-laundering laws.

A version of this story first appeared in CNN Business’ Before the Bell newsletter. Not a subscriber? You can sign up right here. You can listen to an audio version of the newsletter by clicking the same link.

New York CNN

—

Inflation fears roiled the markets in 2022. Now, investors may have scarier things to worry about in 2023, according to a report from global research and consulting firm Eurasia Group. Most notable? Concerns about the increasingly chaotic geopolitical landscape.

“Inflation shockwaves” still feature as one of Eurasia’s top political risks for 2023 in a new report.

But perhaps surprisingly, inflation ranks fourth on the list, behind worries about a rogue Russia under the leadership of Vladimir Putin and Xi Jinping’s consolidation of power in China.

Eurasia’s third biggest fear — the increased use of artificial intelligence technology to wreak havoc onthe global economy — only adds to jitters about disruption from Russia and China. Eurasia called AI “a gift to autocrats.”

Eurasia, led by political scientist and author Ian Bremmer, pointed out that Russia’s war with Ukraine may become an even bigger problem for the United States and Europe.

“Nuclear saber-rattling by Moscow will intensify. Putin’s threats will become more explicit,” Eurasia said in its report. It is also concerned that “Kremlin-affiliated hackers will ramp up cyberattacks on Western firms and governments.”

That could mean attempts to disrupt oil pipelines, American and European satellites and other telecom and tech infrastructure, as well as further efforts to influence and sabotage global elections.

“Moscow will step up its rogue behavior…with newly empowered influence operations targeting NATO countries,” Eurasia said in the report.

Eurasia pointed to upcoming Polish elections in 2023 as “the most obvious target” but that other Western nations “will be vulnerable, too.”

Autocracy in China is a potential economic and market headache as well.

“Xi’s drive for state control will produce arbitrary decisions and policy volatility. China’s economy is in a fragile state after two years of harsh Covid-19 controls,” Eurasia noted, pointing out that “plummeting homebuyer and market sentiment have ground growth in the critical real estate sector to a halt, depleting local government revenue.”

Eurasia added that the “backdrop of weakening global growth and deepening domestic challenges demands competent economic management from Beijing.” Instead, “the Chinese leadership is delivering opacity and unpredictability.”

Chinese officials announced in October that they were delaying the release of key economic data, news that Eurasia said “was an ominous sign of things to come for global markets.”

All of this uncertainty comes as China continues to face the growing Covid outbreak in the country. Eurasia fears that “if a severe new strain of Covid were to emerge,” it is “more likely that it would spread widely in China and beyond.

“China would be unlikely to identify the new variant because of reduced testing and sequencing, to recognize more severe disease due to an overwhelmed health system, and to let news of a more severe variant get out given Xi’s track record on transparency,’ Eurasia said. “The world would have little or no time to prepare for a deadlier virus.”

Meanwhile, Eurasia also is worried that Beijing “will deploy new technologies not only to tighten surveillance and control of its own society, but also to spread propaganda on social media and intimidate Chinese language communities overseas.”

None of this is to suggest that worries about rising prices have dissipated.

While inflation is listed as the fourth-biggest risk, Eurasia is still concerned that “rising interest rates and global recession will raise the risk of emerging-market crises.”

Energy prices in particular will remain a sticking point for the global markets and economy as Eurasia notes that “higher oil prices will also increase frictions between OPEC+ and the United States.”

And Eurasia also listed concerns about instability in Iran, shrinking water levels and economic inequality as major global challenges.

Then there’s another new and distinctly 21st century worry: the rise of social media.

“Gen Z has both the ability and the motivation to organize online to reshape corporate and public policy, making life harder for multinationals everywhere and disrupting politics with the click of a button,” Eurasia said, referring to the phenomenon as the “Tik Tok Boom.”

Bankman-Fried, more commonly referred to by his initials, SBF, plead “not guilty” to charges ranging from wire fraud and conspiracy to commit money laundering to conspiracy by misusing customer funds.

SBF appeared in a Manhattan court Tuesday after he was arrested last month in the Bahamas, extradited to the United States and then released by a judge on a $250 million bail package. But as my colleague Kara Scannell reports, the legal drama for SBF is only beginning. The judge set a trial date of October 2.

Prosecutors allege that SBF was in charge of “one of the biggest financial frauds in American history.” They claim that he moved (or stole) billions of dollars from FTX customers to cover losses at the firm’s companion hedge fund, Alameda Research.

The cryptocurrency world was already in turmoil before FTX imploded. The prices of bitcoin, ethereum and other digital coins all plummeted in 2022. But FTX and Alameda were each forced to file for bankruptcy in December after investors rushed to pull deposits.

FTX was once valued at $32 billion, based on funding from private investors. The company was expected to be one of the hottest initial public offerings of 2023 as recently as the middle of last year. Not any more.

Covid woes hurt Apple

(AAPL) last year, as the world’s largest iPhone factory in China faced production disruptions since October due to the pandemic.

But the giant campus, owned by top Apple supplier Foxconn, is reportedly now back at 90% production capacity following worker protests and Covid-related restrictions.

Apple needs to get more of its latest smartphones into people’s pockets. Delays with the various iPhone 14 models have cost the company — and its investors — dearly.

Wedbush Securities analyst Dan Ives estimated in November that disruptions in China led to about $1 billion a week in lost revenue.

And analysts at UBS also said in November that wait times for the new iPhone 14 Pro and 14 Pro Max in the US were more than a month long due to supply chain woes. That couldn’t have come at a worse time since it was just before Christmas and other winter holidays.

Apple’s stock had a tough 2022, like the rest of Big Tech, and it didn’t start off 2023 in a festive fashion either. Shares of Apple hit a new 52-week low Tuesday. Apple’s market value dipped below $2 trillion in the process. Just a year ago, Apple was the first company in the world to reach a $3 trillion market valuation.

Sam Bankman-Fried, the founder of bankrupt cryptocurrency exchange FTX, pleaded not guilty to charges that he defrauded customers out of billions of dollars. His trial is set for October.

Be the first to know

Get browser notifications for breaking news, live events, and exclusive reporting.

Sam Bankman-Fried pleaded not guilty Tuesday to charges related to the collapse of his crypto empire, according to reporters present at his arraignment hearing in a New York federal court Tuesday.

Sam Bankman-Fried, the disgraced founder of bankrupt crypto exchange FTX, is set to appear in person in a Manhattan federal court on Tuesdayto face charges that include cheating investors out of billions of dollars.

Bankman-Fried, known as SBF, is charged witheight criminal counts ranging from wire fraud and conspiracy to commit money laundering to conspiracy by misusing customer funds. Heis expected to plead not guilty. He could face up to 115 yearsin prison if convicted on all charges.

Last month, a US judge released him on a $250 million bond in his first appearance on American soil since his arrest in the Bahamas,where he lived and ran his businesses. The judge agreed to a bail package proposed by federal prosecutors and lawyers for Bankman-Fried that also requires the former “crypto king” to wear an electronic ankle monitorand remain under house arrest at his parents’ home in Palo Alto, California.

Bankman-Fried’s parents, both law professors at Stanford who co-signed his bond, have “become the target of intense media scrutiny, harassment, and threats,” defense lawyers wrote in a letter to the court, while asking to redact the names of two other co-signers, known as “sureties.”

“There is serious cause for concern that the two additional sureties would face similar intrusions on their privacy as well as threats and harassment if their names appear unredacted on their bonds or their identities are otherwise publicly disclosed,” the letter states.

Prosecutors allege that Bankman-Fried orchestrated “one of the biggest financial frauds in American history,” stealing billions of dollars from FTX customers to cover losses at its sister hedge fund, Alameda Research.

FTX and Alameda both filed for bankruptcy in December after investors rushed to pull their deposits from the exchange, sparking a liquidity crisisand triggering contagion and panic across the crypto industry.

Two senior executives associated with the collapse — Gary Wang, the co-founder of FTX, and Caroline Ellison, who served as Alameda’s CEO— have since pleaded guilty to multiple criminal charges and are cooperating with federal prosecutors, according to unsealed court records.

In addition, the pair face civil fraud charges from the Securities and Exchange Commission.

Wang faces up to 50 years in prison in accordance with federal sentencing guidelines referenced in court. Ellison faces up to 110 years in prison for the seven criminal counts she’s pleaded guilty to, per federal sentencing guidelines.

FTX’s new CEO, John Ray III, who made his name overseeing the liquidation of Enron in the early 2000s, said in a congressional hearing that customer funds deposited on the FTX site were commingled with funds at Alameda, which made a number of speculative, high-risk bets.

Ray described the situation at the two companies as “old-fashioned embezzlement” at the hands of a small group of “grossly inexperienced and unsophisticated individuals.”

— CNN’s Allison Morrow and Kara Scannell contributed to this report.

Martin Shkreli a.k.a. “Pharma Bro,” has some advice from one ex-con to one accused fraudster.

Spencer Platt/Michael M. Santiago/Getty Images

Shkreli – who gained infamy in 2015 as a pharmaceuticals CEO that hiked the price of a lifesaving drug from $13 to $750 and was later found guilty of securities fraud — offered some slammer survival skills to now-disgraced former FTX CEO Sam Bankman-Fried on crypto journalist Laura Shin’s, “Unchained” podcast.

Ahead of Bankman-Fried’s looming legal battle and possible incarceration, Shkreli said he should prepare for prison life and “reinvent” himself if he wants to make it behind bars.

“Sam is going to have a lot of issues because he is a bit of an effeminate guy and his demeanor — some people say autistic sort of sense, or sensibility — is not something that goes over well in prison,” Shkreli said.

Shkreli was sentenced to prison in 2017 and released this past May after serving five years of a seven-year sentence.

Bankman-Fried, a.k.a. SBF, was arrested in the Bahamas earlier this month on several criminal fraud charges. He could face up to 115 years in prison after allegedly stealing billions in customer funds in a Ponzi Scheme between crypto exchange FTX and Alameda Research crypto trading firm. After being extradited to the U.S., SBF was released on a $250 million bond and is living with his parents in California as he awaits trial.

Shkreli’s other advice includes saying SBF should shave his head, deepen his voice, and brush up on rap music, gangs, and “criminal culture.”

While Shkreli said these changes “could save your life” on the inside, he also said the former crypto entrepreneur should hide his Ivy League education and privileged roots.

“He should probably start to reinvent his background and history because the rich white kid from a good neighborhood — that story doesn’t sound great,” Shkreli said.

A group of FTX Trading customers is suing the bankrupt cryptocurrency exchange, alleging that its top executives stole their digital assets and purposely blocked them from making withdrawals.

California resident Austin Onusz filed a class-action lawsuit Tuesday alongside three other FTX users from the Netherlands, Turkey and the United Kingdom. The complaint names FTX founders Sam Bankman-Fried and Gary Wang as defendants as well as Caroline Ellison, former CEO of FTX’s hedge fund, Alameda Research.

Bankman-Fried and Ellison knowingly sent customer crypto funds to Alameda Research without their consent, attorneys representing Onusz allege.

“Such misconduct was in direct violation of FTX’s own customer agreements and terms of service as well as common law and basic principles of honesty and fair dealing,” states the lawsuit, which claims the class-action could encompass more than 1 million FTX customers

Under Bankman-Fried’s leadership, FTX has misplaced up to $2 billion worth of customer digital assets, the lawsuit alleges.

Onusz and the other plaintiffs said in court documents that they stored cash and digital assets on FTX’s platform but haven’t been able to complete a withdrawal since early November. FTX users who cannot access their funds should get priority status once the bankruptcy proceedings end and it’s time to divvy up the company’s remaining assets, the plaintiffs’ attorneys argue.

FTX, which has been accused of negligence and breach of contract in the lawsuit, didn’t immediately respond to a request for comment.

FTX filed for bankruptcy last month after experiencing crypto’s version of a bank run. Customers withdrew about $5 billion in a single day amid rising concerns about FTX’s solvency.

Since then, Bankman-Fried, 30, has been arrested and charged with fraud, conspiracy and money laundering. He was arrested in the Bahamas earlier this month before being extradited to the U.S., where he was released last week on a $250 million bond. Bankman-Fried is now at his parent’s home in California while he awaits trial. The $250 million bond is believed to be the largest ever federal pretrial bond, according to federal prosecutors.

FTX’s new CEO John J. Ray III has called the company’s previous management the worst he’s ever seen in a 40-year career that includes overseeing the Enron bankruptcy. He told federal lawmakers earlier this month that FTX collapsed because the “very small group of grossly inexperienced and unsophisticated individuals” who were running the company “failed to implement virtually any of the systems or controls that are necessary for a company that is entrusted with other people’s money or assets.”

Assistant U.S. attorney Nicolas Roos said last week in U.S. District Court that Bankman-Fried “perpetrated a fraud of epic proportions.”

Khristopher J. Brooks is a reporter for CBS MoneyWatch covering business, consumer and financial stories that range from economic inequality and housing issues to bankruptcies and the business of sports.

This is an opinion editorial by Obi Nwosu, CEO of Fedi and a board member for ₿trust.

In 2020, I predicted that Bitcoin would face attacks during the 2018 to 2023 period but would ultimately emerge successful by the end of it. Although I am not a prophet, it was clear to me that this would be a critical time for Bitcoin. When the bear market hit this year, we saw a “cleansing” of the Bitcoin ecosystem and an opportunity to refocus on its main mission of monetary freedom.

The snowball started in the heat of July with the Celsius bankruptcy, which was the first sign that the ecosystem we were building was not healthy. The fact that we were using a decentralized currency to mirror the centralized financial system did not match the vision for Bitcoin.

This once again highlighted the existence of two alternate and diverging realities for Bitcoin: “real” Bitcoin, which is rising from the bottom up and focuses on the value Bitcoin can bring to the world, and “regulated” Bitcoin, which is focused on price and committed to regulatory systems and adoption through speculation.

I sold Coinfloor in 2021 because I realized that exchanges like ours were too often dedicated to keeping their users trapped in regulated Bitcoin land. As we near the end of 2022, the negative effects of this have been painfully demonstrated by the collapse of FTX, the regulatory fallout and the losses incurred by so many innocent people.

On the other hand, real Bitcoin is flourishing in the Global South and post-Soviet regions, where innovation is addressing the narrative that Bitcoin has no good use cases. For instance, a new version of frontier towns is emerging, combining renewable energy, Bitcoin mining, internet connectivity and community custody. As I have long suspected, real Bitcoin adoption can only come from the people, and Fedimint and Fedi seek to be key in achieving hyperbitcoinization. The world will experience the most primitive form of protection — humans united — translated and turbocharged through the highest technology.

In the coming years, communities will play a crucial role in defining the path for Bitcoin. Bitcoiners are already empowering communities around the globe, but it is vital that our global community also stays united to win this battle. As I predicted in my 2020 post, we will certainly succeed in this endeavor and so I am more convinced than ever that Bitcoin will win in 2023.

This is a guest post by Obi Nwosu. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

Caroline Ellison has apologized for stealing billions in customer deposits at crypto exchange platform FTX to make bets at Alameda Research, the hedge fund she ran.

“‘I am truly sorry for what I did.’”

— Caroline Ellison, former head of Alameda Research

Ellison made her comments in front of a judge in New York federal court, as she pleaded guilty to helping Sam Bankman-Fried make away with billions in customer funds while misleading investors and lenders and playing down the risk of their crypto trading platform.

“‘I knew that it was wrong.’”

— Ellison

Along with Ellison, Zixiao “Gary” Wang, a former FTX chief technology office and co-founder, 29, pleaded guilty Monday this week during separate hearings.

Federal authorities and regulators are making the case that Wang wrote software code, at Bankman-Fried’s behest, to create backdoors into FTX’s systems that allowed Ellison’s Alameda access to customer money and prop up FTX’s own token, FTT.

The pair each potentially face decades in prison sentences if convicted after pleading guilty to charges that included wire fraud, securities and commodities fraud in exchange for leniency.

Both have agreed to cooperate with authorities to lay the groundwork for Bankman-Fried’s own case as the alleged brains behind of one of the biggest crypto frauds in recent memory.

FTX filed for bankruptcy on Nov. 11 when Bankman-Fried was ousted from the company he co-founded in 2019.

The collapse of FTX was, perhaps, hastened by its competitor, Binance, who announced it was unloading $500 million in FTT tokens in November due to “recent revelations that have come to light” about the company’s books. That triggered mass redemptions by depositors, which FTX couldn’t meet.

Ellison is a Stanford University graduate who grew up in the suburbs of Boston, the daughter of two MIT economists, according to the Wall Street Journal. After graduation, she worked at quantitative trading firm Jane Street, where she met fellow trader Bankman-Fried. She was rumored to be in a relationship with Bankman-Fried, who is an MIT grad, according to reports.

Cryptocurrency entrepreneur Sam Bankman-Fried walked out of a Manhattan courthouse Thursday with his parents after they agreed to sign a $250 million bond and keep him at their California home while he awaits trial on charges that he swindled investors and looted customer deposits on his FTX trading platform.

The $250 million bond is believed to be the largest federal pretrial bond ever, said assistant U.S. attorney Nicolas Roos.

Roos said in U.S. District Court that Bankman-Fried, 30, “perpetrated a fraud of epic proportions.”

Bankman-Fried’s bail conditions are strict. He has already surrendered his passport and won’t be allowed travel documents, the court said. He cannot own firearms, open any lines of credit or start new businesses, and must seek government approval for any transactions over $1,000.

Bankman-Fried’s parents, both law professors, put their home’s equity as collateral for the bond. Bankman-Fried will be permitted to leave the Palo Alto home only for exercise or legal proceedings, the court said. The court also mandated that Bankman-Fried undergo mental health and substance abuse treatment. The entrepreneur was required to get an electronic monitoring bracelet before leaving the courthouse.

FTX founder Sam Bankman-Fried leaves court following his extradition to the U.S., Thursday Dec. 22, 2022, in New York. Bankman-Fried’s parents agreed to sign a $250 million bond and keep him at their California home while he awaits trial on charges that he swindled investors and looted customer deposits on his FTX trading platform.

Yuki Iwamura / Associated Press

Fraud or error?

Prosecutors agreed to bail because Bankman-Fried did not fight extradition, saving the govenment from a potentially yearslong, drawn-out process, Roos said.

Reunited with his parents and lawyers inside the courthouse, an apparently silent Bankman-Fried shook the hands of a supporter before heading out the door, where photographers and video crews rushed him as he got into a car and left.

Bankman-Fried wore a suit and tie in court and sat between his attorneys. Two U.S. marshals sat behind him. Near the end of the hearing, Magistrate Judge Gabriel W. Gorenstein asked Bankman-Fried whether he understood he would face arrest and owe $250 million if he chose to flee.

“Yes, I do,” Bankman-Fried answered.

Sam Bankman-Fried, founder and former CEO of crypto currency exchange FTX, is walked in handcuffs to a plane during his extradition to the United States at Lynden Pindling international airport in Nassau, Bahamas December 21, 2022.

RBPF / REUTERS

His first U.S. court appearance comes after the onetime crypto wunderkind was flown from the Bahamas to the U.S. on Wednesday. Bankman-Fried was arrested earlier this month on charges of wire fraud, conspiracy, money laundering and other financial crimes.

While he was in the air Wednesday, the U.S. attorney in Manhattan announced that two of Bankman-Fried’s closest business associates had also been charged and had secretly agreed to plea deals.

Caroline Ellison, 28, the former chief executive of Bankman-Fried’s trading firm, Alameda Research, and Gary Wang, 29, who co-founded FTX, pleaded guilty to charges including wire fraud, securities fraud and commodities fraud.

U.S. Attorney Damian Williams said in a video statement that both were cooperating with investigators and had agreed to assist in any prosecution. He warned others who enabled the alleged fraud to come forward.

“If you participated in misconduct at FTX or Alameda, now is the time to get ahead of it,” he said. “We are moving quickly, and our patience is not eternal.”

Possibility of decades in prison

Prosecutors and regulators contend that Bankman-Fried was at the center of several illegal schemes to use customer and investor money for personal gain. He faces the possibility of decades in prison if convicted on all counts.

In a series of interviews before his arrest, Bankman-Fried said he made mistakes running FTX and Alameda but that he never intended to defraud anyone.

Bankman-Fried is charged with using money, illicitly taken from FTX customers, to enable trades at Alameda, spend lavishly on real estate, and make millions of dollars in campaign contributions to U.S. politicians.

FTX, founded in 2019, rode the crypto investing phenomenon to great heights quickly, becoming one of the world’s largest exchanges for digital currency. Seeking customers beyond the tech world, it hired the comic actor and writer Larry David to appear in a TV ad that ran during the Super Bowl, hyping crypto as the next big thing.

Bankman-Fried’s crypto empire, however, abruptly collapsed in early November when customers pulled deposits en masse amid reports questioning some of its financial arrangements.

FTX founder Sam Bankman-Fried is set to be released from federal custody after his attorneys struck a deal with prosecutors on a bail amount of $250 million, according to multiple reports.

A federal prosecutor announced Wednesday night that two associates of former FTX CEO Sam Bankman Fried had agreed to plea deals on charges related to the collapse of the cryptocurency exchange. The prosecutor also said Bankman-Fried was being flown to the United States from the Bahamas to face charges stemming from the scandal.

U.S. Attorney Damian Williams said Carolyn Ellison, the former CEO of Alameda Research, a trading firm started by Bankman-Fried, and Gary Wang, who co-founded FTX along with Bankman-Fried, pleaded guilty in the Southern District of New York to charges related to “their roles in the fraud that contributed to FTX’s collapse.” Both are cooperating with the Southern District, he said.

The charges against them include wire fraud, securities fraud and commodities fraud.

“Gary has accepted responsibility for his actions and takes seriously his obligations as a cooperating witness,” an attorney for Wang told CBS News in a statement.

The Securities and Exchange Commission also announced civil charges against Ellison and Wang Wednesday.

Bankman-Fried appeared at a Bahamian Magistrate’s Court Wednesday and said he’d agreed to be extradited to the U.S. He was then taken back to prison, where he waited for a plane for the trip, according to Bahamian news organization Our News.

Williams said Bankman-Fried is in FBI custody and “on his way back to the United States. He will be transported directly to the Southern District of New York and he will appear in court before a judge in this district as soon as possible.”

Bahamian authorities arrested Bankman-Fried last week at the request of the U.S. government. U.S. prosecutors allege he played a central role in the rapid collapse of FTX and hid its problems from the public and investors. The SEC said Bankman-Fried illegally used investors’ money to buy real estate on behalf of himself and his family.

The 30-year-old could potentially spend the rest of his life in jail.

In media interviews, Bankman-Fried — the son of two Stanford professors and a prolific political donor — has maintained that he erred in his running of FTX, but that he didn’t commit fraud.

Bankman-Fried was denied bail Friday after a Bahamian judge ruled that he posed a flight risk. The founder and former CEO of FTX, once worth tens of billions of dollars on paper, was being held in the Bahamas’ Fox Hill prison, which has been cited by human rights activists as having poor sanitation and being infested with rats and insects.

Once he’s back in the U.S., Bankman-Fried’s attorney will be able to request that he be released on bail.

Sam Bankman-Fried told a Bahamian court Wednesday that he has agreed to be extradited to the U.S. to face criminal charges related to the collapse of cryptocurrency exchange FTX.

The former FTX CEO appeared at a Magistrate’s Court and then was taken back to prison, where he is awaiting an airplane to take him to the United States, according to Bahamian news organization Our News. A source familiar with the situation told CBS News he was expected to depart for the U.S. Wednesday night.

Bahamian authorities arrested Bankman-Fried last week at the request of the U.S. government. U.S. prosecutors allege he played a central role in the rapid collapse of FTX and hid its problems from the public and investors. The Securities and Exchange Commission said Bankman-Fried illegally used investors’ money to buy real estate on behalf of himself and his family.

The 30-year-old could potentially spend the rest of his life in jail.

In media interviews, Bankman-Fried — the son of two Stanford professors and a prolific political donor — has maintained that he erred in his running of FTX, but that he didn’t commit fraud.

Bankman-Fried was denied bail Friday after a Bahamian judge ruled that he posed a flight risk. The founder and former CEO of FTX, once worth tens of billions of dollars on paper, is being held in the Bahamas’ Fox Hill prison, which has been cited by human rights activists as having poor sanitation and being infested with rats and insects.

Once he’s back in the U.S., Bankman-Fried’s attorney will be able to request that he be released on bail.

Thanks for reading CBS NEWS.

Create your free account or log in for more features.

A Bahamas judge on Wednesday approved the extradition of former billionaire Sam Bankman-Fried, the founder of befallen crypto exchange FTX, from a Nassau jail to the United States, where the former crypto wunderkind faces a slew of criminal charges.

Sam Bankman-Friedstarted the cryptocurrency exchange FTX in 2019 at watched it all come crashing down in 72 hours.

Photo By Tom Williams/CQ-Roll Call, Inc via Getty Images

Bankman-Fried was once seen as the King of Crypto. He promised big returns for customers and investors and even tried to help the government impose regulations on the industry. That was until crypto giant Binance expressed concerns over FTX’s financial stability and falling crypto prices sparked a bank run, revealing FTX and its sister company Alameda Research were suspiciously working together to pay off debts, according to The New York Times — and leaving an $8 billion hole in its accounts.

FTX attracted major investors including SoftBank and BlackRockand boasted celebrity endorsements from the likes of Tom Brady and Shaquille “Shaq” O’Neal. Still, the company’s low-risk, high-reward business model appeared almost too good to be true.And it was.

In the wake of the FTX collapse, between $1 billion and $2 billion in client money has gone unaccounted for, according toReuters.

SBF has since been arrested and charged with several counts of fraud, and prosecutors say he orchestrated “one of the biggest financial frauds in American history.” He could face up to 115 years in prison.

While the crypto scandal is still unfolding, here’s everything to know about Bankman-Fried.

Who Is Sam Bankman-Fried?

Before Sam Bankman-Fried was embroiled in the FTX scandal, he was known as a rising crypto wiz and an academic standout.

Also known simply as “SBF,” Bankman-Fried was raised in California by his parents, Joseph Bankman and Barbara Fried, who were both Stanford University law professors, according to Reuters. He excelled in mathematics and went on to graduate from the Massachusetts Institute of Technology (MIT) in 2014.

How Did SBF Make His Money?

After graduation, Bankman-Fried worked for Jane Street Capital in New York City, where he traded currencies, futures, and exchange-traded funds. SBF stayed with the company for three years before leaving to start his own crypto trading firm, Alameda Research, in 2017 when he was 25 years old.

Alameda was based in Hong Kong and turned a profit by taking advantage of the price differences in Bitcoin around the world. The company would purchase Bitcoin in Asia and sell it elsewhere, in order to pocket the currency difference, per The New York Times.

Although Alameda operated much like a traditional Wall Street firm, it had no regulatory oversight, which scared investors, the outlet reported. To help generate revenue for Alameda’s trades, SBF launched a cryptocurrency exchange, FTX, in 2019, which greatly benefited from the increased demand for crypto.

The company was valued at $32 billion in January 2022, according to CNBC.

SBF discussed crypto regulations and testified in front of Congress in December 2021, detailing his then-supposedwillingness to add regulations to the industry, something typically feared by crypto-enthusiasts.Despite facing legal troubles for the FTX collapse, SBF said that helping to regulate the industry is still important to him inan interview with The New York Times.

What Is Sam Bankman-Fried’s Net Worth?

Just days before Sam Bankman-Fried’s crypto empire collapsed, he had an estimated net worth of $15.6 billion, according to Bloomberg Billionaires Index. After his fortune plummeted, he was left with $1 billion. The 94% drop in his wealth is among the biggest one-day collapses the tracker has ever seen.

At his peak, SBF was worth an estimated $26.5 billion, with most of his money tied up in his companies.

Earlier this year, SBF pledged to give away 99% of his fortune to charitable organizations, and his FTX Foundation has donated over $190 million to several causes including animal welfare and global poverty, according to Vox. SBF also outlined his charitable intentions in a post to the Giving Pledge website, which has since been removed.

Image credit: Jeenah Moon/Bloomberg via Getty Images

What Is FTX and What Went Wrong?

FTX is a cryptocurrency exchange platform that worked in close collaboration with Alameda Research.

In addition to charging customers to trade on the platform, FTX created the FTT token, which was mainly bought and sold by Alameda on the exchange, per The New York Times. As the token’s main market marker, it was allowed to set the price for the token at a big discount, attracting people to the platform with promises of a high return on their investment.

The business model attracted major investors including Softbank and Blackrock, in addition to several celebrity entrepreneurs, including Gwyneth Paltrow and baseball star David Ortiz.

However, FTX’s close workings with Alameda went under the radar, including SBF’s reported romantic relationshipwithCaroline Ellison, who worked as Alameda’s co-CEO with Sam Trabucco.

According to an SEC filing, Ellison said she and others were aware Alameda had been using FTX customer funds.

“During a meeting with Alameda employees on or about November 9, 2022, Ellison admitted that she, Bankman-Fried, Wang, and Singh were aware that FTX customer funds had been used by Alameda,” the complaint reads.

Ellison has yet to be charged in the case.

Together, FTX and Alameda provided billions in funding to 246 crypto companies, but despite SBF’s push for more crypto, investors started to back out as a result of fluctuating crypto prices and withdrew funds from their accounts.

As Alameda struggled to pay back its lenders, it began to use customer funds deposited in FTX to pay back its investors. FTX reportedly lent an estimated $10 billion of customer funds to Alameda.

Then, in a last-ditch effort to save Alameda, Binance proposed a deal to buy the company, but it fell through after analyzing FTX’s books, according to The New York Times. After Binance’s CEO Changpeng Zhao announced he would sell his FTT tokens due to fears concerning the company’s financial stability, he sparked panic and traders withdrew $6 billion from the platform in just 72 hours.

The bank run exposed an $8 billion hole in FTX and Alameda’s accounts.

After struggling to raise more capital for the business, FTX filed for bankruptcy on November 11, 2022. SBF announced he’s be stepping down as CEO that same day and would be replaced by lawyer John J. Ray III.

What Did Sam Bankman-Fried Do and Why Was He Arrested?

U.S. prosecutors have accused Sam Bankman-Fried of defrauding FTX customers by misappropriating funds to pay debts and expenses for its sister company Alameda Research. According to prosecutors, SBF also provided false and misleading information to investors, in addition to attempting to hide his earnings through wire fraud, according to The New York Times.

SBF was arrested in the Bahamas at his apartment complex after the United States filed criminal charges against him on December 12, stating they were “likely to request his extradition,” the government of the Bahamas said in a statement to the outlet. He is facing criminal charges of wire fraud, wire fraud conspiracy, securities fraud, securities fraud conspiracy, and money laundering.

Additionally, the Securities and Exchange Commission has authorized charges “relating to Mr. Bankman-Fried’s violations of our securities laws.”

So far, SBF is the only person charged in the indictment.

What Is Sam Bankman-Fried Saying in the Wake of the FTX Collapse?

After FTX imploded, Sam Bankman-Fried has been vocal about what transpired.

Just one day before the company filed bankruptcy, SBF took to Twitter to issue a public apology.

Additionally, he suggested that poor internal organization contributed to their inability to return funds to customers.

5) The full story here is one I’m still fleshing out every detail of, but as a very high level, I fucked up twice.

The first time, a poor internal labeling of bank-related accounts meant that I was substantially off on my sense of users’ margin. I thought it was way lower.

Furthermore, SBF said he “did not ever try to commit fraud” at the DealBook Summit on November 30, stating he “screwed up” and failed to protect his customers. He claims to have been truthful following the FTX fallout, stating, “I don’t know of times when I lied.”

He went on to issue an interview with The New York Times, telling the outlet, “It could be worse.” He explained that he didn’t realize how much borrowing was going on between FTX and Alameda, and the significant risk it posed. Additionally, SBF blamed himself for not seeing trouble ahead.

“Had I been a bit more concentrated on what I was doing, I would have been able to be more thorough,” he said. “That would have allowed me to catch what was going on on the risk side.”

Prior to his arrest, SBF told the NYT he was “working constructively with regulators, bankruptcy officials, and the company to try to do what’s best for consumers.”

Image credit: (Photo by Mario Duncanson / AFP) (Photo by MARIO DUNCANSON/AFP via Getty Images)

What Is Next for Sam Bankman-Fried?

Following his arrest, Bankman-Fried has been at Fox Hill prison in Nassau, Bahamas, and was denied bail. He has agreed to be extradited to the U.S., and a judge ordered his extradition hearing to be held on Feb. 8, 2023, per CoinDesk. Once he is back on U.S. soil, he will be arraigned in Federal District Court in Manhattan and face a bail hearing.

But sources close to the case told CNN he may return to the States sooner and will be seeking bail to hopefully avoid detention.

In addition to the criminal charges SBF is facing, he is also dealing with a class action lawsuit claiming that the celebrities who endorsed FTX, including Kevin O’Leary and Gisele Bundchen, were engaging in deceptive practices to “induce confidence and to drive consumers to invest in what was ultimately a Ponzi scheme,” according to the lawsuit.

It’s possible SBF could work out a deal that includes both his criminal and civil cases, Reuters reported. Additionally, prosecutors will ask for restitution for those who lost money in the collapse.

Prior to Bankman-Fried’s arrest, he was supposed to testify in front of the House Financial Services Committee about the FTX collapse.

“The American public deserves to hear directly from Mr. Bankman-Fried about the actions that’ve harmed over one million people,” Representative Maxine Waters, who chairs the committee, said in a statement, per NYT. “The public has been waiting eagerly to get these answers under oath before Congress, and the timing of this arrest denies the public this opportunity.”

The hearing went ahead without SBF, and FTX’s new CEO John Ray spoke in his place. He called the relationship between Alameda and FTX “old-fashioned embezzlement” and blamed the collapse and financial fallout on the “absolute concentration of control in the hands of a small group of grossly inexperienced and unsophisticated individuals who failed to implement virtually any of the systems or controls that are necessary for a company entrusted with other people’s money or assets.”

His testimony went on for four hours, stating he is in the process of getting to the bottom of the scandal and figuring out how to repay lenders and customers. However, the unorganization at FTX has made that a challenge.

“Even with most failed companies, we have a fair roadmap of what happened,” Ray said, adding, “We’re dealing with a literal paperless bankruptcy.”

When asked what role SBF would play in the company going forward, Ray responded: “Zero.”

Opinions expressed by Entrepreneur contributors are their own.

Lenox, Massachusetts, is known for its picturesque New England charm. It’s a cultural hotspot, home to the Tanglewood Music Center and Norman Rockwell Museum. It’s also known for its historic homes and local restaurants. It can feel like a place out of time, but 2022 is catching up with Lenox in the demise of the FTX cryptocurrency exchange, which may directly affect the town’s economic future.

According to The Berkshire Eagle, Ryan Salame, previously co-CEO at FTX subsidiary FTX Digital Markets, invested $6 million in acquiring Lenox restaurants and real estate.

FTX infamously declared bankruptcy on Nov. 11, and its founder, Sam Bankman-Fried, was arrested last week in the Bahamas pending extradition to the U.S. Bankman-Fried, also known as SBF, has been accused of redirecting FTX customers’ money to his trading company, Alameda. Bankman-Fried also allegedly used some of these funds to buy luxury real estate and make hefty political donations.

Business Insider reports that court papers note that Ryan Salame, whom Alameda loaned $55 million at one point, alerted authorities of problems at FTX days before the company filed for bankruptcy. In addition, the Wall Street Journal reported that Salame was physically ill upon learning of the company’s collapse.

Speaking to the Eagle, Lenox Chamber of Commerce director Jennifer Nacht said, “I feel really badly for Ryan, and yes, I am concerned about what it means for Lenox. I know Heritage and Firefly [two eateries owned by Salame’s Lenox Eats] are continuing to operate as normal. Everything else is on hold until further notice.”

“It’s so crazy that something of this global magnitude has such a direct effect on our little town,” Nacht added.

For his part, Salame has been publicly quiet, not responding to questions about his interests in Lenox or anything else. His last tweet was posted on Nov. 6, five days before FTX collapsed. It read, “It’s so powerful learning who your friends are! Very excited to grow with them in the long term. It’s not hard to genuinely figure out who cares about customers and who doesn’t if you look past the insanity.”

Sam Bankman-Fried, the former billionaire crypto wunderkind now jailed in the Bahamas and facing a litany of criminal charges for alleged fraud, did not agree to extradition back to the U.S. as expected in a Monday court hearing.

Let me tell you a story about what happens when you, and others, leave your bitcoin on exchanges. You might be surprised to hear what that means for your holdings. It might sound a lot like your own.

Let’s call our character Bill. Bill has been cautiously watching bitcoin for years, hearing about it in passing and reading a few articles. After inadvertently saving a lot of cash due to lockdowns, he decided to dive into bitcoin at last. A friend told him to check out Coinbase, Binance or another popular and “trusted” exchange in order to buy his first chunk of bitcoin.

So, Bill created an account and uploaded his face, ID, social security number, address and every other relevant detail about his life until he finally reached the “Buy Bitcoin” screen. He picked up a fraction of a bitcoin, but after all that trouble, he thought to himself:

“I don’t need to learn all these complicated technical details about hardware wallets and self custody — I just want my bitcoin safe.”

Bill reviewed the exchange’s website and decided that the security experts at the exchange, with their wiz-bang cold storage and state-of-the-art encryption, would be better at securing his bitcoin than he himself would be.

Bill was very pleased with himself after making that decision — not only did this exchange make investing in bitcoin simple, it gave him peace of mind knowing that someone else was responsible for keeping his assets safe from any kind of theft or malicious activity. After all, why should he have to worry about such things when there were professionals available who could handle them instead?

Bill has since become quite comfortable with the idea of trusting exchanges with his bitcoin — his coins are now safe from his own mistakes!

When Trust Disappears: The Fall Of FTX

When Bill turned on the news one morning and found out that the massive crypto exchange FTX had just paused withdrawals and seemed to “accidentally” lose $10 billion, roughly a third of its market cap, he was shocked.

How could a firm with its logo on the side of a major sports stadium and a CEO who appeared on CNBC, Bloomberg and in front of the U.S. Congress(!) to talk about digital assets and regulation have lost — or likely stolen — so much from right under everyone’s nose?

Now Bill was stuck between a rock and a hard place. He was suspicious of his own exchange, but setting up his own hardware wallet seemed so difficult and scary. It would require him to invest in a physical device, acquire the necessary knowledge to secure it properly and keep track of his seed phrase backup. Even if he figured out the basics, there was still the risk of misplacing his device or improperly storing his backup and losing access to his bitcoin.

FTX was shocking, but surely Bill’s exchange would never conduct itself the same way. People would see it before it was coming, and he’d have time to get out, right?

Reasons To Take Your Bitcoin Off Exchanges

It’s clear that trusting your bitcoin to an exchange brings with it the risk that you’ll log in one morning to find that your bitcoin just isn’t there. If you hold your bitcoin yourself using a hardware wallet, this can’t happen.

However, there’s another big reason it’s important to take your bitcoin off exchanges: the bitcoin price.

How could self custody affect bitcoin’s price? Everything in economics says that buying and selling affect the market price for a good, not who holds it. However, self custody is very important to price — and it has to do with something I’ll call “paper BTC.”

Introducing The Next Big Thing: Paper BTC

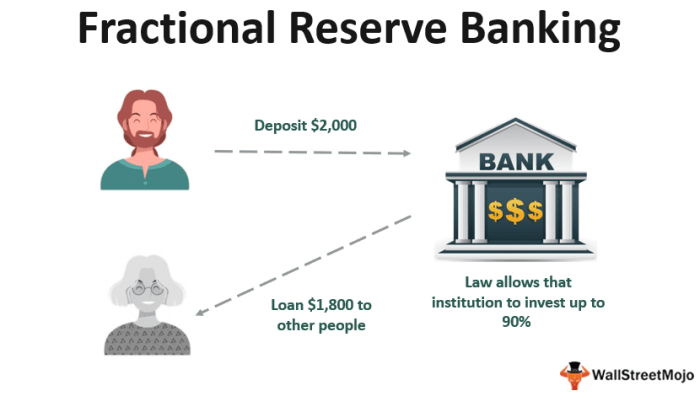

Let’s look at how an exchange works by considering a hypothetical exchange called ExchangeCorp, owned and operated by a jolly entrepreneur named Bernie. ExchangeCorp built an uncomplicated way to buy bitcoin, and hired a team of security experts to make sure hackers are kept at bay. Over time and through great marketing campaigns, ExchangeCorp built trust with traders and investors, drawing many in to store their bitcoin on the exchange.

When users keep their bitcoin with ExchangeCorp, the CEO Bernie and his team maintain control over those coins. Customers simply have a claim on their coins: they can log in and see their balance as well as request to withdraw their coins. However, if Bernie wants to transfer those coins owed to his customers to other Bitcoin addresses, he’s technically able to do so without any customer’s permission.

When Bernie kicks up his feet and looks at the balances in ExchangeCorp’s vault, he’s pleased to see tens of thousands of bitcoin that his customers have deposited sitting pretty. Since ExchangeCorp is doing well, more bitcoin are always coming in than going out.

So Bernie gets a wise idea. He could lend out some of those customer coins, earn some interest, and get the coins back without anyone noticing. He would get richer, and the risk of enough ExchangeCorp customers asking for withdrawals at one time to draw its vault’s massive balance down to zero is miniscule. So Bernie loans out thousands of coins here and there to hedge funds and businesses.

Now there’s another set of claims to consider. Customers have a claim on their bitcoin at ExchangeCorp, but ExchangeCorp no longer has the actual bitcoin — they only have a claim on the coin they lent out. What customers now have is a claim on Paper BTC held by ExchangeCorp, with the real bitcoin in the hands of borrowers.

This is where things get weird. All of ExchangeCorp’s customers still think they have a direct claim on real bitcoin held safely by ExchangeCorp. However, that real bitcoin is in fact in the hands of those who borrowed from ExchangeCorp, and those entities are selling it out in the market.

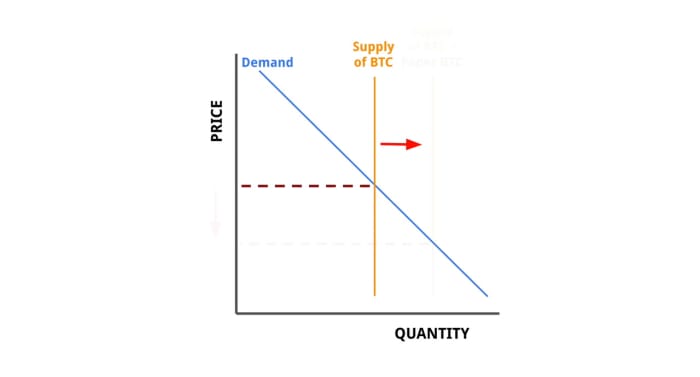

What happens when ExchangeCorp lends out a large quantity of the bitcoin its customers deposited? A lot of extra bitcoin starts to float around in the market, because investors who think they’re holding actual bitcoin are only holding paper BTC. All of that extra supply of bitcoin in the market absorbs buy pressure, which suppresses the price of bitcoin.

Let’s look at simple supply and demand here:

When paper BTC comes into the market, because market participants are unaware that this new supply is not real bitcoin, it has the same effect as increasing the supply of real bitcoin — until the fraud is uncovered.

Does this hypothetical story sound anything like the recent news around FTX?

The Paper BTC At The Center Of The FTX Fraud

The story of ExchangeCorp and Bernie is exactly the story of FTX and its founder Sam Bankman-Fried, with some save-the-world complexes, study drugs and polyamorous orgies redacted.

By lending out customer funds, FTX essentially inflated the supply of bitcoin by taking advantage of the trust users placed in FTX to safeguard their funds. FTX created tons of paper BTC.

Just how much paper BTC might FTX have created? We cannot be sure of the exact amounts given its absolutely horrid bookkeeping, but the estimate below suggests FTX had 80,000 paper BTC on its books — bitcoin owed to customers that is not backed by real bitcoin.

That would represent a staggering 24% of the roughly 330,000 new bitcoin that were created over the past year through the predictable mining issuance process. That is a ton of extra bitcoin entering the market that nobody — aside from a small group of insiders at FTX — knew about!

It’s impossible to tell where the price would have gone without that extra bitcoin supply entering the market, but we can be almost certain that the price would have climbed higher than it did in 2021.

While the FTX collapse is recent and still unfolding, history has a few cautionary tales to tell about the dangers of paper assets and price manipulation. The story of gold’s failure to resist centralized capture, for instance, can tell us where Bitcoin is headed if we continue to trust exchanges and third parties to hold our bitcoin for us.

The Fall Of Gold

Gold was once used in daily transactions — it takes no more than a visit to a museum of ancient history to see the collections of old gold coins once circulating in local markets. The traditional view of the demise of gold as a transactional currency was that it became too cumbersome or too valuable to continue to function well as a means to buy groceries and beer.

However, this story omits a few key components that only reveal themselves when we trace the evolution that societies took from gold coins to paper bills and digital bank accounts.

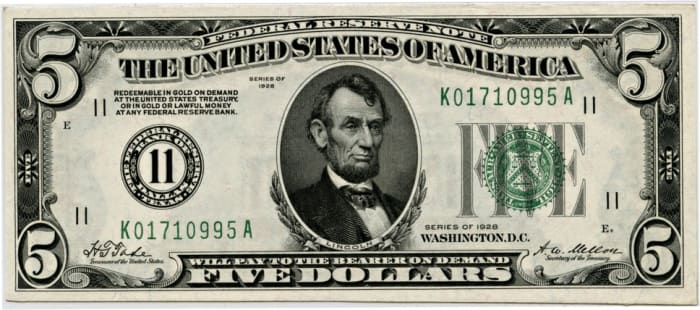

Centuries ago, banks started taking customer’s gold in exchange for bank notes — giving customers a measure of security for their gold and a more convenient means of transacting. However, entrusting a bank with your precious metal meant the bank was able to lend it out or make bad investments without the depositor’s consent. When a bank was caught between bad loans and a high rate of depositor withdrawals, they had to declare bankruptcy and shut down — leaving many depositors penniless, holding paper claims on gold now worth nothing at all.

Then central banks came along to “fix” the problem of bankrupt banks leaving depositors penniless. Central banks held gold for people and commercial banks, giving them banknotes from the central bank as receipts for their gold. By 1960, central bank official holdings accounted for about 50% of all aboveground gold stocks, with their banknotes circulating freely. Commercial banks and individuals didn’t mind, since each note was convertible to a set weight of gold by the central bank that issued it.

Notice the note in the upper left? This $5 Federal Reserve note — also known as a $5 bill — is redeemable in gold. Source

This would have worked well, except that central banks — especially the Federal Reserve in the U.S. — started creating more bills than they had gold to back. Creating more bills than the Fed had gold to back was essentially creating paper gold, since each bill was a claim on gold. Doing this in secret meant the Fed was manipulating the price of gold, given the extra circulating supply which the market was not aware of. When many depositors of gold at the Federal Reserve — like the French government — started questioning the Fed’s gold holdings and creating the threat of a run on gold in the U.S., the U.S. government had to intervene.

In 1971, this came to a head with the Nixon shock. One night, President Nixon announced the U.S. would temporarily stop allowing depositors to trade in their Federal Reserve notes for the gold they promised.

This temporary halt in withdrawals was never lifted. Since all currencies were connected to gold through the U.S. dollar under the Bretton Woods agreement, the Nixon Shock meant that the entire world went off the gold standard at once. All currencies were now just pieces of paper, instead of notes giving the holder a claim on a quantity of gold.

This was only achievable because gold, over time, was deposited into commercial banks and then to central banks. Once central banks held most of the gold, they could manipulate the price of gold and remove it entirely from daily commerce. Everyday people chose the convenience of paper notes over the security of holding gold, and paid the price.

Instead of a neutral money backed by a precious metal that is difficult to dig up and impossible to synthesize, currencies became easy to print and thus highly politicized. Keeping the dollar at the top of the food chain no longer required restraint and good stewardship to ensure its backing in gold. Instead, it required military expeditions and strong policing to ensure global governments and citizens continued to use the dollar to transact.

A return to gold at this point would be impractical — the world’s commercial networks span too great a distance with transactions happening at too high a speed. With paper currency and eventually digital banking systems, what we gained in speed and convenience we lost in soundness and neutrality. We lost our savings, our social cohesion and our political institutions as a result.

Preventing Bitcoin’s Fall

Taking your bitcoin off of your exchange is not just good practice for your own security, it’s protecting the price of your bitcoin as well. Our freedoms depend on individuals having control over their own wealth. When we entrust our wealth to companies or states, we go down the path we witnessed with gold.

Thanks to bitcoin’s divisibility and digital nature, it overcomes the hurdles that held gold back from supporting our modern, interconnected economy. Bitcoin can support a global marketplace, but it will only get there if we each hold our own bitcoin.

Don’t let the banksters and bureaucrats manipulate the price of your bitcoin: take it off the exchange and get it on your own hardware wallet.

This is a guest post by Captain Sidd. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

As Web3 Is Going Just Great’sMolly White reports, the deal was supposed to run for seven years, and involve FTX making “substantial payments” to Riot, starting with $12.5 million for the 2022 calendar year (and escalating to $12.875 for 2023, and so on). So far only $6.25 million of that 2022 sum has been paid, and there is almost zero chance Riot will ever see another cent, so the company has filed a case with a Bankruptcy Court in Delaware seeking to have the rest of the sponsorship deal nullified.

In strictly business terms, that’s perfectly understandable. As Riot points out in their filing, FTX have declared bankruptcy, which should send the whole deal straight into the bin, no questions asked. Just in case anyone does ask questions, though, Riot have added, “There is simply no way for FTX to cure the reputational harm already caused to Riot as a result of the highly public disrepute wrought by the debacle preceding FTX’s bankruptcy filing. FTX cannot turn back the clock and undo the damage inflicted on Riot in the wake of its collapse.”

Prior to, and throughout this media firestorm, Riot’s image and reputation to its customer base, remained inextricably linked to FTX through its former CEO, Mr. Bankman-Fried. Media outlets and Twitter commentators splashed images of Mr. Bankman-Fried playing League of Legends—Riot Games’ game— at the same time that FTX was crashing. Mr. BankmanFried is famous for his affinity for the game. He is well-known among investors to play League of Legends during meetings. He acknowledged on Twitter that he played “a lot more [League of Legends] than you’d expect from someone who routinely trades off sleep vs work.” Even Mr. Bankman-Fried’s ranking in League of Legends has been the subject of online commentary with public figures Alexandria Ocasio-Cortez and Elon Musk weighing in.

Even back when this deal was first signed, in August 2021, it was agonisingly clear what the endgame for this whole scam was going to be, whether it was video game developers or NBA teams or overly-eager celebrities.

You would think Riot would know this, especially now in the middle of all this, but another part of the filing argues that the FTX deal needs to be terminated because it is preventing the company from further “commercializing the crypto-exchange sponsorship category…currently owned by FTX.” Fool me once, shame on you, etc, etc.

Cryptocurrency firms reeling from the epic collapse of FTX and its aftereffects received yet another unwelcome development on Sunday’s talk shows.

Senator Sherrod Brown, chair of the Senate banking committee, took questions on NBC’s Meet the Press today about how lawmakers should approach cryptocurrencies after the FTX debacle.

Host Chuck Todd asked the lawmaker whether regulating crypto would give a “green light” to something that many people think should be banned.

Brown, referring to government agencies—the Treasury, the Securities and Exchange Commission, and the Commodity Futures Trading Commission—replied, “We want them to do what they need to do…maybe banning.”

His comments follow ones made by Senator Jon Tester, who serves on the same banking committee and was asked by Todd last weekend whether crypto should be regulated or banned.

“One or the other,” he answered. “It’s not been able to pass the smell test for me…I see no reason why this stuff should exist. I really don’t.”

Crypto an ‘investment in nothing’

But it isn’t just lawmakers in Washington, D.C.—many top business leaders feel the same way.

In September, JPMorgan Chase CEO Jamie Dimon called crypto a “decentralized Ponzi scheme” that’s not “good for anybody.”

Charlie Munger, vice chairman of Berkshire Hathaway and Warren Buffett’s business partner, said this summer: “Crypto is an investment in nothing…I think anybody that sells this stuff is either delusional or evil. I’m not interested in undermining the national currencies of the world.”

Munger went so far as to praise Chinese leader Xi Jinping for being “smart enough” to ban Bitcoin in China.

But Brown on Sunday acknowledged banning crypto is “very difficult because it will go offshore and who knows how that will work…This is a complicated, unregulated pot of money.”

FTX founder Sam Bankman-Fried based his business in the Bahamas, where he reportedly led a lavish penthouse lifestyle and, according to federal prosectors, misused billions of dollars in customer funds.

Bahamian authorities arrested him on Monday following a formal notification by the U.S. government that it had filed criminal charges against him and would likely request his extradition. The U.S. and the Bahamas have had an extradition process in place since 1994.

Crypto ‘doesn’t get a free pass’

Brown this week thanked the U.S. and Bahamian officials behind the arrest, adding in a statement, “I trust that Mr. Bankman-Fried will soon be brought to justice. It is clear he owes the American people an explanation.”

He added, “Things that look and behave like securities, commodities, or banking products need to be regulated and supervised by the responsible agencies who serve consumers…Crypto doesn’t get a free pass because it’s bright and shiny.”

Brian Armstrong, CEO of crypto exchange Coinbase, noted in tweet last month that FTX was “an offshore exchange not regulated by the SEC.”

His company is based the U.S. and as a publicly traded firm has more transparency than FTX did. This week, Coinbase shares fell to an all-time low.

“The problem is that the SEC failed to create regulatory clarity here in the US, so many American investors (and 95% of trading activity) went offshore,” he wrote. “Punishing US companies for this makes no sense.”

Our new weekly Impact Report newsletter examines how ESG news and trends are shaping the roles and responsibilities of today’s executives. Subscribe here.