That means a full day of trading for stocks, which appear poised to book a robust week of gains, despite continued fears of a potential U.S. economic recession as the Federal Reserve works to tame stubbornly high costs of living.

While Friday marks the start of a three-day weekend for the bond market, Treasury yields already have climbed dramatically this year with the Fed’s sharp rate hikes. The central bank aims to temper demand for goods and services by making borrowing costs more restrictive.

Consumers may feel certain effects of inflation in their everyday lives, like when they go to the grocery store. But it can also impact our savings and investments. Here’s what to know.

The benchmark 10-year Treasury rate TMUBMUSD10Y, 3.819%

fell to about 3.8% on Thursday, but was up from a 1.3% low last December. Bond yields move in the opposite direction of prices.

The fresh rally on Wall Street followed the consumer-price index reading for October showing a 7.7% annual rate, down from a 9.1% high in June. The Dow remains down more than 8% from its January peak, the S&P 500 is 17.5% lower and the Nasdaq is 31% below its last record close, according to Dow Jones Market Data.

BEIJING — Asian stock markets surged Friday after U.S. inflation eased by more than expected, spurring hopes the Federal Reserve might scale down plans for more interest rate hikes.

Hong Kong’s market benchmark jumped 5.7% and Seoul rose 3.3%. Shanghai, Tokyo and Sydney advanced. Oil prices edged higher.

Wall Street’s benchmark S&P 500 index soared 5.5% on Thursday for its biggest one-day gain in 2 1/2 years after the government reported consumer prices rose 7.7% over a year ago in October. That was lower than the 8% expected by economists and the fourth month of decline.

The announcement “drove a ‘more dovish’ calibration of interest rate expectations,” said Yeap Jun Rong of IG in a report.

The Fed and central banks in Europe and Asia are raising rates to cool inflation that is at multi-decade highs. Investors worry that might tip the global economy into recession. They hope lower inflation might prompt the Fed to ease off plans for more increases.

Forecasters warned Thursday it was too early to be certain prices are under control. Fed officials have said rates might have to stay elevated for some time.

Hong Kong’s Hang Seng index soared to 16,994.66 and the Nikkei 225 in Tokyo gained 2.9% to 28,229.68.

The Shanghai Composite Index added 1.4% to 3,078.42 after the ruling Communist Party promised to alter quarantine and other anti-virus tactics to reduce the cost of China’s severe “zero-COVID” strategy that has disrupted the economy.

The Kospi in Seoul rose to 2,481.50 and Sydney’s S&P-ASX 200 was up 2.7% at 7,154.20.

India’s Sensex opened up 1.6% to 61,579.12. New Zealand and Southeast Asian markets advanced.

On Wall Street, the S&P 500 gained to 3,956.37, propelled by big gains for tech heavyweights. Amazon soared 12.2%, Apple rose 8.9% and Microsoft climbed 8.2%.

The Dow Jones Industrial Average gained 3.7%, or more than 1,200 points, to 33,715.37.

The Nasdaq composite, dominated by tech stocks, shot up 7.4% to 11,114.15 for its best day since March 2020, when Wall Street was rebounding from a crash at the start of the coronavirus pandemic.

Investors were reassured that U.S. inflation was declining from its June peak of 9.1%, though forecasters said the Fed’s campaign to cool price rises was far from over.

Traders expect the Fed to raise its benchmark lending rate in December but by a smaller margin of half a percent following four increases of 0.75 percentage points, triple its usual margin. That benchmark stands at a range of 3.75% to 4%, up from close to zero in March.

The Fed is trying to slow economic activity to reduce pressure for prices to rise.

The latest figures are a sign the Fed is “on the right path,” but it will face “a lot of variables” over the next few quarters, said Edward Moya of Oanda in a report. He said the benchmark rate could be raised to 5% and “if inflation proves to be sticker, it could be as high as 5.50%.”

Core inflation, which strips out volatile food and energy prices and is more closely watched by the Fed, was 6.3% over a year earlier, down from September’s 6.6% and below the consensus forecast of 6.5%. Core prices rose 0.3% month on month, half of September’s 0.6% gain.

The yield on the 10-year Treasury, which helps set rates for mortgages and other loans, fell to 3.82% from 4.15%. The two-year yield, which more closely follows expectations for Fed action, fell to 4.32% from 4.62% and was on pace for its sharpest fall since 2008.

In energy markets, benchmark U.S. crude gained 20 cents to $86.67 per barrel in electronic trading on the New York Mercantile Exchange. The contract rose 64 cents to $86.47 on Thursday. Brent crude, the price basis for international oil trading, advanced 20 cents to $93.87 per barrel in London. It rose $1.02 to $93.67 the previous session.

The dollar declined to 141.52 yen from Thursday’s 141.83 yen. The euro edged up to $1.0206 from $1.0180.

Crypto lending platform BlockFi announced it was halting withdrawals Thursday night in the wake of the collapse of crypto exchange FTX.

“We are shocked and dismayed by the news regarding FTX and Alameda,” BlockFi said in a tweet. “We, like the rest of the world, found out about this situation through Twitter.”

BlockFi said that due to the “lack of clarity” regarding FTX and Alameda, “we are not able to operate business as usual,” and that until there is “further clarity, we are limiting platform activity, including pausing client withdrawals.”

The company asked clients not to deposit into BlockFi Wallet or Interest Accounts at this time, and said it will share more specifics “as soon as possible,” though it warned it likely would communicate “less frequently” than what its clients and stakeholders are used to.

FTX founder and CEO Sam Bankman-Fried reportedly extended about $10 billion in loans to its affiliated trading firm Alameda Research — amounting to about half of FTX’s customer assets of $16 billion, according to the Wall Street Journal.

“I fucked up, and should have done better,” Bankman-Fried said in a tweet Thursday, saying he had, among other things, misread the use of margin on the platform.

The FTX fiasco has spread fear of a “contagion” across the broader crypto industry, and sent the price of bitcoin BTCUSD, -3.87%

at one point to its lowest level since November 2020.

Just six months ago, CEOs, celebs and world leaders like Bill Clinton and Tony Blair flocked to him, gathering at a Davos-like conference he hosted in the Bahamas where he lives as one of the most outspoken evangelists for the power of the blockchain.

Fast forward to Sunday and Bankman-Fried’s crypto empire came crashing down, the victim of an old-fashioned bank run that quickly exposed the weaknesses of the new finance system he had championed.

Almost overnight, Bankman-Fried’s cryptocurrency exchange, FTX, had gone from being valued at $32 billion to worthless, leaving scores of investors scrambling to get their deposits back and triggering probes in the U.S. by the Securities and Exchange Commission, the Commodities Futures Trading Commission and the Department of Justice, according to reports.

On Thursday, the 30-year-old Bankman-Fried took to Twitter to level with his clients.

“I fucked up, and should have done better,” he wrote.

A very rapid rise

It took less than five years for Bankman-Fried to build a personal fortune that was estimated at its highest point to be more than $26 billion, making him among the richest people in the world.

His schlubby, boyish appearance — ill-fitting t-shirts, gym shorts and a mop of curly hair — made him look more like a college student ripping bong hits in the basement of a frat house than a finance guru, but fit nicely with the anti-establishment ethos that appealed to crypto enthusiasts.

The son of law professors at Stanford University, Bankman-Fried was a wunderkind from an early age. He studied physics and mathematics at the Massachusetts Institute of Technology.

After a stint as an ETF trader for Jane Street Capital, a highly respected Wall Street firm that is known for attracting genius quantitative traders, Bankman-Fried became interested in the concept of effective altruism, a philosophy that focuses on using reason and evidence to find solutions that benefit the most people possible. In 2017, he launched Alameda Research, a quantitative trading firm focused on digital currencies.

Over the next year, he began building his fortune through arbitrage trading of Bitcoin BTCUSD, +11.10%

between exchanges in the U.S. and Japan, where prices were often slightly higher. In 2019, Bankman-Fried launched the crypto exchange FTX.

The timing was fortuitous: as the COVID-19 pandemic spread across the globe the following year, interest in cryptocurrencies among people exploded. FTX took off and brought in the big-name celebrity endorsers and partners, like professional athletes Tom Brady and Steph Curry.

Bankman-Fried soon found himself feted by some of the biggest institutions in finance, attracting investment from the biggest names on Wall Street and beyond like Softbank 9984, -2.65%

Group, Sequoia Capital, Blackrock BLK, +13.26%.

Tiger Global Management and Thoma Bravo. He even raised money from billionaire hedge fund legends Paul Tudor Jones and Israel Englander.

Soon, FTX was among the biggest players in the industry.

The face of crypto

Despite his ballooning wealth, Bankman-Fried maintained the appearance and lifestyle of a teenage gamer. He moved to the Bahamas, where he reportedly lived in a penthouse apartment with 10 roommates.

On Zoom calls, he would often play video games while talking — his favorite game being League of Legends. Profiles of him often noted that he kept a bean bag just feet from his desk to sleep on.

What set Bankman-Fried apart from other crypto tycoons, was his professed interest in working with regulators to create a more robust framework around the nascent industry and treat it more like a traditional finance network.

To that end, Bankman-Fried appeared before Congress to try to explain to skeptical U.S. lawmakers how the crypto industry worked. He also said he welcomed regulation, not always a popular position in the crypto world.

“FTX believes [government agencies] could play an even more prominent role in the digital-asset ecosystem and bring greater investor protections by closing some regulatory gaps,” he said before a senate panel in February. “FTX believes that such efforts would combine the best aspects of traditional finance and digital-asset innovations.”

Bankman-Fried even put his great wealth to play in politics, becoming a major campaign donor for the Democratic party. In 2020, he was one of President Joe Biden’s largest single donors and spent nearly $40 million on political campaigns this year for the midterm elections, according to campaign filings.

As cryptocurrencies have experienced significant declines in prices this year, triggering the collapse of several operations, Bankman-Fried arose as a savior, buying up several failing partners as positioning himself as a kind of Robin Hood for the industry.

A swift collapse

For as fast a rise to the top of the world that Bankman-Fried enjoyed, the fall was just as rapid.

On Sunday, Changpeng Zhao, the CEO of FTX’s competitor, Binance, and an archrival of Bankman-Fried’s, announced on Twitter that his firm, the world’s biggest cryptocurrency exchange, was liquidating its sizable holdings of FTT, the coin issued by FTX, “due to recent revelations that have come to light.”

Bankman-Fried accused Zhao of spreading false rumors. But the damage was done.

Binance’s move triggered a massive selloff with customers seeking to redeem some $5 billion in deposits. FTX didn’t have it and redemptions froze up.

On Tuesday, Bankman-Fried announced that FTX had reached a tentative agreement to be acquired by Binance, due to a “significant liquidity crunch.” The turmoil set off broad declines among several of the most popular cryptocurrencies and even spilled into the world of traditional finance, sending markets tumbling.

The next day, the chaos increased, with reports that FTX and Bankman-Fried were under investigation by several U.S. agencies. By the end of the day, Binance said it was walking away from the deal because due diligence had revealed that “the issues are beyond our control or ability to help.”

Binance’s deal seemed like the only thing preventing FTX from potentially collapsing. “At some point I might have more to say about a particular sparring partner,” Bankman-Fried tweeted on Thursday. “For now, all I’ll say is: well played; you won.”

Also on Thursday, the Wall Street Journal reported that Bankman-Fried had been using some customer deposits to fund risky bets by his Alameda Research firm, setting FTX up for collapse.

With the Binance lifeline gone and with few options available, Bankman-Fried told investors he needed $8 billion or more to plug the hole in FTX’s books, according to reports.

On Twitter, Bankman-Fried said he would focus all his efforts on making sure depositors got their money back. He also tried to explain FTX’s collapse, saying “a poor internal labeling of bank-related accounts meant that I was substantially off on my sense of users’ margin. I thought it was way lower.”

Said Bankman-Fried: “My #1 priority–by far–is doing right by users,” he wrote. “Right now, we’re spending the week doing everything we can to raise liquidity. I can’t make any promises about that.”

BEIJING — Global stock markets fell Thursday ahead of a U.S. inflation update that will likely influence Federal Reserve plans for more interest rate hikes as investors waited to see who will control Congress after this week’s elections.

London, Shanghai, Frankfurt and Tokyo declined. U.S. futures were higher. The euro fell back below $1.

Wall Street’s benchmark S&P 500 index tumbled Wednesday as votes were counted to decide whether Republicans take control of Congress, possibly leading to changes that can unsettle markets. Investors were rattled by the crypto industry’s latest crisis of confidence and weaker profit reports from The Walt Disney Co. and some other companies.

Forecasters expect U.S. government data Thursday to show inflation eased in September but stayed near a four-decade high. That might reinforce arguments that rates have to stay elevated for an extended period to slow economic activity and extinguish inflation.

“An upside surprise today would present a challenge for officials who expect to slow the pace of rate hikes,” Rubeela Farooqi of High-Frequency Economics said in a report.

In early trading, the FTSE 100 in London was 0.1% lower at 7,285.86. The DAX in Frankfurt lost 0.1% to 13,647.47 and the CAC 40 in Paris shed 0.2% to 6,417.98.

On Wall Street, futures for the S&P 500 and the Dow Jones Industrial Average were up 0.3%.

On Wednesday, the S&P 500 lost 2.1%, erasing gains from a three-day rally leading up to Election Day.

Disney sank 13.2% for the largest loss in the S&P 500 after reporting quarterly results that fell short of analysts’ expectations.

The Dow fell 2% and the Nasdaq composite, dominated by tech companies, tumbled 2.5%.

Facebook parent Meta Platforms rose 5.2% after saying it will cut costs by laying off 11,000 employees, or about 13% of its workforce. It is down nearly 70% for the year.

In Asia, Hong Kong’s Hang Seng index fell 1.7% to 16,081.04 and the Nikkei 225 in Tokyo sank 1% to 27,446.10. The Shanghai Composite Index lost 0.4% to 3,036.13.

The Kospi in Seoul declined 0.9% to 2,407.70 and Sydney’s S&P-ASX 200 was off 0.5% at 6,964.00.

India’s Sensex shed 1% to 60,447.97. New Zealand, Bangkok and Jakarta declined while Singapore and Malaysia gained.

The Philippines’ market benchmark lost 0.5% after the government reported the economy grew by 7.6% in the three months ending in September.

Investors worry rate hikes this year by the Fed and central banks in Europe and Asia to cool inflation might tip the global economy into recession. Traders hope indicators that show U.S. housing sales and other activity weakening might prompt the Fed to back off plans for more rate hikes.

In the United States, Republicans were within nine seats of the 218 needed to control the House of Representatives as votes still were being counted in some states. Control of the Senate depended on races in Nevada and Arizona that hadn’t been decided.

The outcome will determine how the next two years of President Joe Biden’s term play out. Republicans are likely to launch a spate of investigations into Biden, his family and his administration if they take power. A GOP takeover of the Senate would hobble the president’s ability to appoint judges.

Still, the election “impact on markets is pretty irrelevant beyond the very near term,” said David Chao of Invesco in a report. “Investors should be worried about inflation, since that will help to dictate the Fed’s future path.”

Forecasters expect Thursday’s data to show inflation decelerated to 7.9% in September from the previous month’s 8.3%. However, prices were expected to rise 0.6% compared with August, accelerating from July’s 0.1% increase.

Core inflation, which strips out volatile food and energy prices to show a clearer trend, is expected to accelerate to 6.5% from August’s 6.3%. That suggests costs of rent, medical services, autos and other goods and services still are rising in response to strong demand.

Traders expect the Fed to raise rates again next month but by a smaller margin of one-half percentage point after a series of 0.75 percentage-point increases. The Fed’s key lending rate is a range of 3.75% to 4%, up from close to zero in March. A growing number of investors expect it to exceed 5% next year.

Also Wednesday, cryptocurrencies fell amid worries about the industry’s financial strength after a big player, Binance, called off a deal to buy troubled rival FTX. That at least temporarily ended hopes for a bailout after FTX users scrambled to pull out their money.

Bitcoin fell 14% from a day earlier to $15,900. That is down 77% from last year’s high of $69,000.

The yield on the 10-year Treasury, which helps dictate rates for mortgages and other loans, fell to 4.08% from 4.13% late Tuesday. The two-year yield, which tends to more closely track expectations for Fed action, dropped to 4.60% from 4.66%.

In energy markets, benchmark U.S. crude shed 49 cents to $85.34 per barrel in electronic trading on the New York Mercantile Exchange. Brent crude, the price basis for international oil trading, lost 42 cents to $92.23 per barrel in London.

The dollar gained to 146.31 yen from Wednesday’s 145.56 yen. The euro declined to 99.83 cents from $1.0073.

Binance, the world’s largest crypto exchange, is abandoning its proposed acquisition of the non-U.S. assets of rival FTX, amid the latter’s liquidity crunch.

“As a result of corporate due diligence, as well as the latest news reports regarding mishandled customer funds and alleged US agency investigations, we have decided that we will not pursue the potential acquisition of FTX.com,” according to a tweet by Binance’s official account Wednesday.

“Our hope was to be able to support FTX’s customers to provide liquidity, but the issues are beyond our control or ability to help,” Binance wrote.

Executives at Binance have found a gap, likely in billions and possibly more than $6 billion, between the liabilities and assets of FTX, Bloomberg reported Wednesday, citing an anonymous source familiar with the matter.

Representatives at Binance and FTX didn’t immediately respond to a request seeking comments.

On Tuesday, Changpeng Zhao, Binance’s chief executive, said the exchange had signed a letter of intent to acquire FTX.com, a separate entity from FTX.US, after FTX “asked for help.”

Investors are worried about any contagion, as concerns over FTX’s solvency spilled over to the already battered crypto market. BitcoinBTCUSD plunged Wednesday to as low as $16,863, the lowest level since November 2020.

FTX is the third largest crypto exchange by trading volume, according to CoinMarketCap.

MarketWatch readers: Ask our Washington bureau chief Robert Schroeder about the results of Tuesday’s midterm elections — and what comes next — during a live, dynamic session beginning at 11 a.m. Eastern on Wednesday.

Before the Q&A starts, please start leaving your questions and comments here and let us know what’s on your mind.

TOKYO — Asian stocks advanced Monday as investors weighed uncertainties such as the U.S. mid-term elections and China‘s possible moves to ease coronavirus restrictions.

Oil prices fell and U.S. futures edged lower.

China reported its trade shrank in October as global demand weakened and anti-virus controls weighed on domestic consumer spending. Exports declined 0.3% from a year earlier, down from September’s 5.7% growth, the customs agency reported Monday. Imports fell 0.7%, compared with the previous month’s 0.3% expansion.

Speculation about a possible relaxation of China’s zero-COVID strategy has had a huge impact on markets. On Monday, Hong Kong’s Hang Seng index gained 2.8% to 16,612.61 and the Shanghai Composite rose 0.2% to 3,077.85.

There has been no official confirmation in China of a major change.

“Over the weekend, Beijing has dashed hopes of China re-opening in the horizon, by reasserting of zero-COVID policies. And this could induce fresh caution,” Tan Boon Heng at Mizuho Bank in Singapore said in a report.

In the U.S., Tuesday’s election will decide control of Congress and key governorships. History suggests the party in power may suffer significant losses in the midterms, and decades-high inflation has become a significant issue for the Democrats.

Analysts say regional markets may take a wait-and-see approach ahead of the U.S. mid-term vote.

Japan’s benchmark Nikkei 225 jumped 1.2% to finish at 27,527.64. Australia’s S&P/ASX 200 gained 0.6% to 6,933.70. South Korea’s Kospi gained nearly 1.0% to 2,371.79.

Shares rose in Taiwan and but edged lower in India.

Wall Street stocks ended last week with a rally but only after yo-yoing several times. Market watchers had data on the U.S. jobs market to digest, considering what it might mean for interest rates and the odds of a recession.

The S&P 500 recorded its first weekly loss in the last three, despite Friday’s gain 1.4% to 3,770.55. The Dow rose 1.3% to 32,403.22, and the Nasdaq climbed 1.3% to 10,475.25. Both also finished with losses for the week.

The unemployment rate ticked higher in October, employers added fewer jobs than they had a month earlier and gains for workers’ wages slowed a touch. The slowdown was still more modest than economists expected. And so the Fed is expected to keep hiking rates.

Fed Chair Jerome Powell has called out a still-hot jobs market as one of the reasons the central bank may ultimately have to raise rates higher than earlier thought. Such moves could cause a recession.

The yield on the two-year Treasury fell to 4.68% from 4.72% late Thursday. The 10-year yield, which helps dictate rates for mortgages and other loans, edged higher to 4.16% from 4.15%.

In energy trading, benchmark U.S. crude fell $1.26 to $91.54 a barrel in electronic trading on the New York Mercantile Exchange. Brent crude, the international standard, lost $1.18 cents in London to $97.39 a barrel.

In currency trading, the U.S. dollar edged up to 147.29 Japanese yen from 146.92 yen. The euro rose to 99.43 cents from 99.15 cents.

———

Yuri Kageyama is on Twitter https://twitter.com/yurikageyama

BEIJING — China’s trade shrank in October as global demand weakened and anti-virus controls weighed on domestic consumer spending.

Exports declined 0.3% from a year earlier to $298.4 billion, down from September’s 5.7% growth, the customs agency reported Monday. Imports fell 0.7% to $213.4 billion, compared with the previous month’s 0.3% expansion.

China’s global trade surplus edged up 0.9% from a year earlier to $85.2 billion.

Forecasters expected Chinese trade to weaken as global demand cooled following interest rate hikes by the Federal Reserve and other central banks to rein in surging inflation.

At home, consumer demand has been hurt by a “Zero COVID” strategy that has repeatedly shut down large sections of cities to contain virus outbreaks. That has disrupted business and confined millions of people to their homes for weeks at a time.

Economic growth picked up to 3.9% over a year earlier in the quarter ending in September from 2.2% in the first six months of 2022. But forecasters say activity is weakening as closures spread in response to a spike in infections.

“The economy slowed again in October due to the tightened Covid controls as well as the slowing external demand,” said Larry Hu of Macquarie Group in a report.

The downturn in Chinese demand hurts developing countries that supply oil, soybeans and other raw materials and the United States, Europe, Japan and other suppliers of consumer goods and microchips and other components and technology needed by manufacturers.

Exports to the United States rose 35.3% over a year earlier to $47 billion despite lingering tariff hikes in a trade war over Beijing’s technology ambitions. Imports of U.S. goods rose $52.4% to $12.8 billion.

China’s politically sensitive trade surplus with the United States swelled 29.9% to $34.2 billion.

Imports from Russia, mostly oil and gas, more than doubled, rising 110.5% over a year ago to $10.2 billion.

China can buy Russian energy exports without running afoul of sanctions imposed on President Vladimir Putin’s government by the United States, Europe and Japan. Beijing is stepping up purchases to take advantage of Russian discounts. That irks Washington and its allies by topping up the Kremlin’s cash flow and limiting the impact of sanctions.

Exports to the 27-nation European Union edged up 5.5% to $44.1 billion while imports of European goods shrank 15.5% to $21.4 billion. China‘s surplus with the EU widened by 38.1% to $22.7 billion.

For the first 10 months of the year, China’s exports rose 11.1% to $3 trillion while imports gained 3.5% to $2.3 trillion, the General Administration of Customs announced. The country’s trade surplus was $727.7 billion.

Coinbase Global Inc. late Thursday reported a wider quarterly loss and a 54% drop in revenue, saying the headwinds for its business will continue and likely intensify next year.

Coinbase COIN, -8.09%

said it lost $545 million, or $2.43 a share, in the quarter, swinging from earnings of $406 million, or $1.62 a share, in the year-ago period.

Revenue dropped to $576 million from $1.24 billion a year ago.

Analysts surveyed by FactSet expected the crypto exchange to report a loss of $2.38 a share on revenue of $641 million.

Shares traded lower immediately after the report, but at last check were rising more than 8% in the extended session.

The quarter was “mixed” for Coinbase, the company said in a letter to shareholders. “Transaction revenue was significantly impacted by stronger macroeconomic and crypto market headwinds, as well as trading volume moving offshore.”

On the plus side, Coinbase saw “strong growth in our subscription and services revenue,” it said.

Those headwinds, however, continued to impact transaction revenue, which was down 44% quarter on quarter, Coinbase said in the letter.

Trading volume dropped to $159 billion in the quarter from $217 billion in the second quarter.

“For 2022, we remain cautiously optimistic that we will operate within the $500 million adjusted EBITDA loss guardrail that we previously communicated,” the company said. That assumes that the crypto market does not deteriorate further, it said.

For next year, however, Coinbase is “preparing with a conservative bias and assuming that the current macroeconomic headwinds will persist and possibly intensify,” the company said.

Ever since Starbucks Corp. rolled out longer-term financial targets in September, Wall Street has wondered how the coffee chain might meet what analysts say were ambitious goals, as rising prices drain consumer spending. For at least the year ahead, executives on Thursday called out three ways to get there: higher prices, younger customers and cold, customizable beverages.

For the fiscal year ahead, executives for the coffee chain on Thursday said they expected global same-store sales to be “near the high end” of its long-term target of between 7% to 9% growth. FactSet expects growth of 8.6%.

When an analyst asked what gave management confidence in that target, interim Chief Executive Howard Schultz said that its coffee was an “affordable luxury,” and that it was armed with a loyalty program that it didn’t have in years past. And they said its customers were getting younger, not older.

“Not only has it gotten younger, but that young, Gen Z customer tends to have significantly more discretionary money at their disposal,” he said. “And their loyalty to Starbucks has been quite significant and predicted.”

He said Starbucks SBUX, +0.12%

had raised prices by nearly 6% over the past 12 months and hadn’t seen demand subside. And he said cold coffee beverages made up 76% percent of total drink sales in its U.S. company-owned stores. In the fourth quarter, more than half of beverages overall in those stores were customized, leading to $1 billion in sales a year for add-on syrups, foams and other ingredients.

“I think customization, which we spoke a lot about in our prepared remarks, is obviously giving us the ticket is becoming more accretive,” he said.

Management said they expect U.S. same-store sales growth of 7% to 9% for the year ahead. For China, they’re banking on “outsize” growth for the metric — interrupted by a decrease in the first-quarter — as the nation potentially emerges from pandemic-related lockdowns.

For overall revenue, they expect gains of between 10% and 12%. Management also said they would resume their buyback program in fiscal 2023.

Even as the Federal Reserve tries to chart a path to lower prices, Starbucks is the latest company to say it still has “pricing power,” or the ability to charge customers more. Snack maker Mondelez International MDLZ, -0.93%,

earlier in the week, said it planned to raise prices through next year. Similarly, its own chief executive also described its snacks as an “affordable indulgence.”

Prior to the call, Starbucks reported fiscal fourth-quarter results that beat expectations, helped by a boost in U.S. sales and higher prices.

The coffee chain reported net income of $878 million, or 76 cents a share, compared with $1.76 billion, or $1.49 a share, in the same quarter last year. Revenue rose 3% to $8.4 billion, compared with $8.15 billion in the prior-year quarter.

Same-store sales rose 7% worldwide, helped largely by bigger ticket sizes, even as actual transaction volume remained muted. They were up 11% in the U.S. But international same-store sales fell 5%, with a 16% drop in China.

Excluding restructuring, impairment and other costs, Starbucks earned 81 cents per share, compared with 99 cents a year earlier. U.S. members of its loyalty program who were active for three months rose 16% to 28.7 million.

Analysts polled by FactSet expected Starbucks to report adjusted earnings per share of 72 cents, on revenue of $8.323 billion. Same-store sales were expected to rise 4.2%.

Shares rose 2.4% after hours.

As with other restaurants and retailers, Starbucks’ sales this year have been helped by price increases. Analysts have also said higher-income consumers, who might not mind higher prices as much, as well as demand for cold beverages, have propelled demand. While China’s COVID-19 restrictions have weighed on sales, analysts say demand trends are strong elsewhere.

“The U.S. business is humming, and the China risk is increasingly understood,” Wedbush analyst Nick Setyan wrote in a research note ahead of Starbucks’ earnings.

The earnings report comes as Starbucks battles a nascent unionization push at some of its stores. Some bargaining efforts between the company and the union members have stalled, amid allegations from both of bad-faith negotiations. The company over the past year has spent more to raise employee pay and rolled out other incentives at non-union stores.

Starbucks stock has tumbled 27% so far this year. The S&P 500 Index SPX, -1.06%,

by comparison, is down around 22%.

How good is a company’s chief executive officer at investing your money most efficiently? This is an important question for long-term investors. It may underline the difference between a steady long-term performer and a flash in the pan.

And Apple Inc. AAPL, -4.24%

now makes up 7% of the SPDR S&P 500 ETF Trust SPY, -1.03%,

the first and largest exchange-traded fund (with $360 billion in assets), which tracks the benchmark S&P 500 SPX, -1.06%.

That’s close to an all-time record, and the iPhone maker has a whopping 14.1% position in the Invesco QQQ Trust QQQ, -1.95%,

which tracks the Nasdaq-100 Index NDX, -1.98%.

Looking at the full Nasdaq Index COMP, -1.73%,

which has 3,747 stocks, Apple takes a 13.5% position.

Apple now makes up 7.3% of the S&P 500 by market capitalization, close to the 8% record it set late in September.

FactSet

This is very much an Apple stock market, with the company topping the broad indexes that are weighted by market capitalization. You are likely to be invested in the company indirectly. You also might be feeling Apple’s impact in other ways. Apple’s App Store ecosystem drives more than $600 billion in annual revenue for developers.

Tim Cook’s tenure as Apple’s CEO has been nothing short of breathtaking when measured by the company’s financial performance. Apple is not one of the fastest-growing companies when measured by sales or earnings — it is too big for that. But its excellent stock performance has reflected Cook’s ability to deploy invested capital with improving efficiency. Cook has also been a market trendsetter in other important ways. He has Apple repurchasing $90 billion of its shares annually, setting the pace for stock buybacks in the market. Cook’s steady hand has also helped Apple withstand the market’s tech wreck and remain a stable pillar for the teetering Nasdaq Composite index generally. For all these reasons, Cook has earned a spot on the MarketWatch 50 list of the most influential people in markets.

Apple keeps improving by this important measure

Investors in the stock market are looking for growth over the long term. The best measure of that is whether or not a company’s share price goes up or down. But Cook isn’t just managing Apple’s stock. Digging a bit deeper into the company’s actual operating performance can provide some insight into what a good job Cook has done.

What should a corporate manager focus on? The stock price? How about the most efficient and most profitable way to provide goods and services? There are different ways to do this, and Apple has focused on quality, reliability and excellent service to build customer loyalty.

Apple’s commitment can be experienced by anyone who calls the company for customer service. It is easy to get through to a well-trained representative who will solve your problem. How many companies can say that at a time when it seems many companies cannot even handle answering the phone?

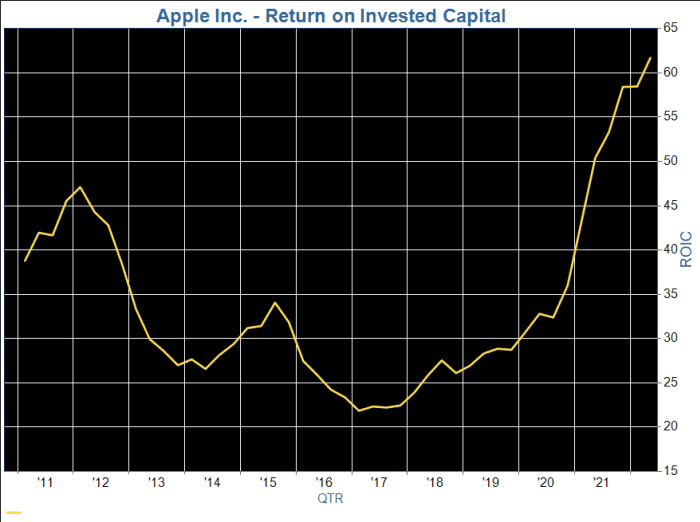

Apple’s returns on invested capital have increased markedly over the past six years.

FactSet

A company’s return on invested capital (ROIC) is its profit divided by the sum of the carrying value of its common stock, preferred stock, long-term debt and capitalized lease obligations. ROIC indicates how well a company has made use of the money it has raised to run its business. It is an annualized figure, but available quarterly, as used in the chart above.

The carrying value of a company’s stock may be a lot lower than its current market capitalization. The company may have issued most of its shares long ago at a much lower share price than the current one. If a company has issued shares recently or at relatively high prices, its ROIC will be lower.

A company with a high ROIC is likely either to have a relatively low level of long-term debt or to have made efficient use of the borrowed money.

Among companies in the S&P 500 that have been around for at least 10 years, Apple placed within the top 20 for average ROIC for the previous 40 reported fiscal quarters as of Sept. 1.

As you can see on the chart, Apple’s ROIC has improved dramatically over the past five years, even as the wide adoption of the company’s products and services has led to an overall slowdown in sales growth.

A quick comparison with other giants in the benchmark index

It might be interesting to see how Apple stacks up among other large companies, in part because some businesses are more capital-intensive than others. For example, over the past four quarters, Apple’s ROIC has averaged 52.9%, while the average for the S&P 500 has been a weighted 12.1%, by FactSet’s estimate.

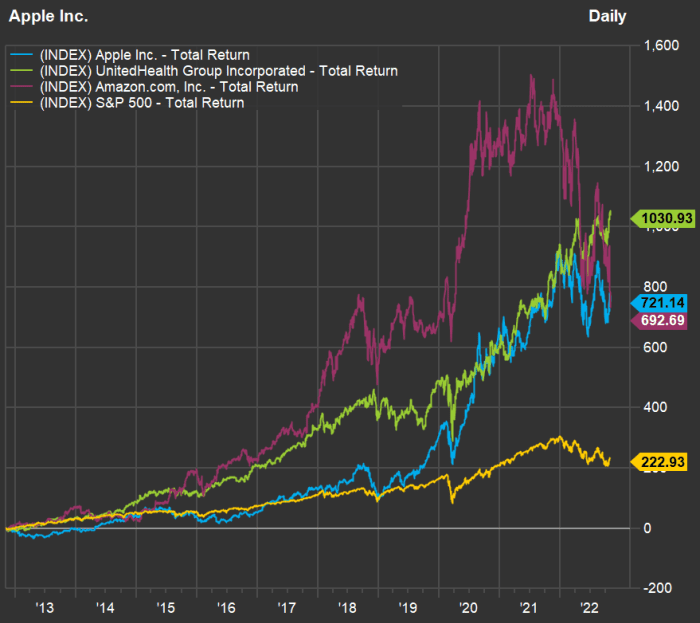

Here are the 10 companies in the S&P 500 reporting the highest annual sales for their most recent full fiscal years, with a comparison of average ROIC over the past 40 reported quarters:

Among the largest 10 companies in the S&P 500 by annual sales, Apple takes the top ranking for average ROIC over the past 10 years, while ranking second for total return behind UnitedHealth Group Inc. UNH, +0.03%

and ahead of Amazon.com Inc. AMZN, -3.06%.

UnitedHealth has been able to remain at the forefront of managed care during the period of transition for healthcare in the U.S., in the wake of President Barack Obama’s signing of the Affordable Care Act into law in 2010.

Here’s a chart showing 10-year total returns for Apple, UnitedHealth Group, Amazon and the S&P 500:

FactSet

Apple is only slightly ahead of Amazon’s 10-year total return. But what is so striking about this chart is the volatility. Apple has had a smoother ride. During the bear market of 2022, Apple’s stock has declined 18%, while the S&P 500 has gone down 20%, the Nasdaq has fallen 32% (all with dividends reinvested) and Amazon has dropped 45%.

The broad indexes would have fared even worse so far this year without Apple.

The global tally of COVID-19 cases fell 17% in the week through Oct. 30 from the previous week, while the death toll fell 5%, the World Health Organization said in its weekly update on the virus.

The omicron variant BA.5 remained dominant globally, accounting for 74.9% of cases sent to a central database. WHO reiterated that newer sublineages of omicron, including BQ.1 and XBB, still appear no more lethal than earlier ones and do not warrant the designation of “variant of concern.”

But BQ.1 rose in prevalence to 9.0% globally from 5.7% a week ago, while XBB rose to 1.5% from 1.0%.

“WHO will continue to closely monitor the XBB and BQ.1 lineages as part of omicron and requests countries to continue to be vigilant, to monitor and report sequences, as well as to conduct independent and comparative analyses of the different omicron sublineages,” the agency wrote.

WHO has cautioned that changes in testing and reduced surveillance of the virus are making some of the numbers unreliable and has urged leaders to renew efforts to monitor and track developments.

In the U.S., known cases of COVID remain at their lowest level since mid-April, although the true tally is likely higher given how many people overall are testing at home, where data are not being collected.

The daily average for new cases stood at 39,090 on Wednesday, according to a New York Times tracker, up 3% versus two weeks ago. The daily average for hospitalizations was up 2% to 27,161, while the daily average for deaths was down 6% to 345.

But cases are climbing in some states, raising concerns among health experts. In Nevada, cases are up 92% from two weeks ago, followed by Missouri, where they are up 75%, Tennessee, where they are up 69%, Louisiana, where they are up 68%, and New Mexico, where they have climbed 54%.

Physicians are reporting high numbers of respiratory illnesses like RSV and the flu earlier than the typical winter peak. WSJ’s Brianna Abbott explains what the early surge means for the coming winter months. Photo illustration: Kaitlyn Wang

• COVID vaccine maker Moderna MRNA, -2.21%

posted far weaker-than-expected third-quarter earnings on Thursday and lowered full-year sales guidance by up to $3 billion. The Cambridge, Mass.-based biotech firm said advance purchase agreements, or APAs, for delivery this year are now expected to total $18 billion to $19 billion of product sales, down from guidance of $21 billion that it provided when it reported second-quarter earnings. The FactSet consensus is for full-year sales of $21.3 billion. For fiscal 2023, Moderna has APAs of $4.5 billion to $5.5 billion. The FactSet consensus for 2023 sales is for $9.4 billion.

• Virax Biolabs Group Ltd. VRAX, +36.26%

stock jumped after the biotechnology company said its triple-virus antigen rapid test kit, which tests for RSV, influenza and COVID, has been launched in the European Union, Dow Jones Newswires reported. The test kit, which can be used in both at-home and point-of-care settings, has also been launched in other markets that accept the CE mark, Virax Biolabs said.

Testing sewage to track viruses has drawn renewed interest after recent outbreaks of diseases like monkeypox and polio. WSJ visited a wastewater facility to find out how the testing works and what it can tell us about public health. Photo illustration: Ryan Trefes

• Royal Caribbean Group RCL, +4.11%

posted its first quarterly profit since the start of the pandemic, but the cruise-line company said it expected a loss for the current quarter, sending its stock lower on Thursday. Load factors were 96% overall and booking volumes were “significantly higher” than in the same period of prepandemic 2019, as the easing of testing and vaccination protocols provided a boost. For the fourth quarter, the company expects adjusted per-share losses of $1.30 to $1.50, compared with the FactSet loss consensus of 71 cents, and projects revenue of “approximately” $2.6 billion, below the FactSet consensus of $2.7 billion.

• The death of a 3-year-old boy in northwestern China following a suspected gas leak at a locked-down residential compound has triggered a fresh wave of outrage at the country’s stringent zero-COVID policy, CNN reported. The boy’s father said in a social media post on Wednesday that COVID workers tried to prevent him from leaving their compound in Lanzhou, the capital of Gansu province, to seek treatment for his child, resulting in what he believes was a fatal delay. The post was met with an outpouring of public anger and grief, with several related hashtags racking up hundreds of millions of views over the following day on Weibo, China’s Twitter-like platform.

The U.S. leads the world with 97.6 million cases and 1,071,582 fatalities.

The Centers for Disease Control and Prevention’s tracker shows that 226.9 million people living in the U.S., equal to 68.4% of the total population, are fully vaccinated, meaning they have had their primary shots.

So far, just 22.8 million Americans have had the updated COVID booster that targets the original virus and the omicron variants, equal to 7.3% of the overall population.

LONDON — The Bank of England made its biggest interest rate increase in three decades Thursday, joining the U.S. Federal Reserve and other central banks worldwide in rapid hikes as it tries to beat back stubbornly high inflation fueled by Russia’s invasion of Ukraine and the disastrous economic policies of former Prime Minister Liz Truss.

The central bank boosted its key rate by three-quarters of a percentage point, to 3%, after consumer price inflation returned to a 40-year high in September. The aggressive move comes even as the bank predicted a two-year economic contraction through June 2024, which would be the longest recession since at least 1955, according to the Office for National Statistics.

“If we don’t take action to bring inflation down, it gets worse,” Bank of England Gov. Andrew Bailey told reporters. “There’s no easy outcome in this sense.”

Even so, the central bank should not increase its key rate too far, he said, but with uncertainties ahead, policymakers will “respond forcefully” if needed.

The interest rate decision is the first since Truss’ government announced 45 billion pounds ($52 billion) of unfunded tax cuts that sparked turmoil on financial markets, pushed up mortgage costs and forced Truss from office after just six weeks. Her successor, Rishi Sunak, has warned of spending cuts and tax increases as he seeks to undo the damage and show that Britain is committed to paying its bills.

“High energy, food and other bills are hitting people hard. Households have less to spend on other things. This has meant that the size of the UK economy has started to fall,” the bank said in its November monetary policy report.

The rate increase is the Bank of England’s eighth in a row and the biggest since 1992. It comes after the U.S. Federal Reserve on Wednesday announced a fourth consecutive three-quarter point jump as central banks worldwide combat inflation that is eroding living standards and slowing economic growth.

Central banks have struggled to contain inflation after initially believing that price increases were being fueled by international factors beyond their control. Their response intensified in recent months as it became clear that inflation was becoming embedded in the economy, feeding through into higher borrowing costs and demands for higher wages.

The war in Ukraine boosted food and energy prices worldwide as shipments of natural gas, grain and cooking oil were disrupted. That added to inflation that began to accelerate last year when the global economy began to recover from the COVID-19 pandemic.

Europe has been particularly hard hit by a jump in natural gas prices as Russia responded to Western sanctions and support for Ukraine by curtailing shipments of the fuel used to heat homes, generate electricity and power industry and European nations competed for alternative supplies on global markets.

The U.K. also has struggled as wholesale gas prices increased fivefold in the 12 months through August. While prices have dropped more than 50% since the August peak, they are likely to rise again during the winter heating season, worsening inflation.

The British government sought to shield consumers with a cap on energy prices. But after the turmoil caused by Truss’ economic policies, Treasury chief Jeremy Hunt limited the price cap to six months instead of two years, ending on March 31.

Meanwhile, food prices have jumped 14.6% in the year through September, led by the soaring cost of staples such as meat, bread, milk and eggs, the Office for National Statistics said. That pushed consumer price inflation back to 10.1%, the highest since early 1982 and equal to the level last reached in July.

Increases in the cost of tea bags, milk and sugar mean that even the “humble” cup of tea, which people across the country turn to when they need a break from the pressures of daily life, is getting more expensive, the British Retail Consortium said Wednesday.

“While some supply chain costs are beginning to fall, this is more than offset by the cost of energy, meaning a difficult time ahead for retailers and households alike,” said Helen Dickinson, the consortium’s chief executive.

Truss’ failed economic plan made things worse, driving the pound to a record low against the dollar, threatening the stability of some pension funds and triggering predictions that the Bank of England would boost interest rates higher than expected. That increased mortgage costs as lenders repriced their products.

The economic turmoil is putting homeownership further out of reach for many young people, according to research released this week by Hamptons, a U.K. real estate agency.

Mortgage rates average around 6.5%, compared with 2% a year ago.

That means the average first-time homebuyer would have to make a down payment equal to 41% of the purchase price to keep their monthly repayments at the same level as a similar buyer who made a 10% down payment last year, Hamptons said.

LIVERPOOL, England — On the long picket line outside the gates of Liverpool’s Peel Port, rain-soaked dock workers warm themselves with cups of tea as they listen to 1980s pop.

Dozens of buses, cars and trucks honk in solidarity as they pass.

Dockers’ strikes are not new to Liverpool, nor is depravation. But this latest walk-out at Britain’s fourth-largest port is part of something much bigger, a great wave of public and private sector strikes taking place across the U.K. Railways, postal services, law courts and garbage collections are among the many public services grinding to a halt.

The immediate cause of the discontent, as elsewhere, is the rising cost of living. Inflation in the United Kingdom breached the 10 percent mark this year, with wages failing to keep pace.

But the U.K.’s economic woes long predate the current crisis. For more than a decade, Britain has been beset by weak economic growth, anaemic productivity, and stagnant private and public sector investment. Since 2016, its political leadership has been in a state of Brexit-induced flux.

Half a century after U.S. Secretary of State Henry Kissinger looked at the U.K.’s 1970s economic malaise and declared that “Britain is a tragedy,” the United Kingdom is heading to be the sick man of Europe once again.

The immediate cause of Liverpool dockers’ discontent that brought them to strike is the rising cost of living. | Christopher Furlong/Getty Images

Here in Liverpool, the “scars run very deep,” said Paul Turking, a dock worker in his late 30s. British voters, he added, have “been misled” by politicians’ promises to “level up” the country by investing heavily in regional economies. Conservatives “will promise you the world and then pull the carpet out from under your feet,” he complained.

“There’s no middle class no more,” said John Delij, a Peel Port veteran of 15 years. He sees the cost-of-living crisis and economic stagnation whittling away the middle rung of the economic ladder.

“How many billionaires do we have?” Delij asked, wondering how Britain could be the sixth-largest economy in the world with a record number of billionaires when food bank use is 35 percent above its pre-pandemic level. “The workers put money back into the economy,” he said.

What would they do if they were in charge? “Invest in affordable housing,” said Turking. “Housing and jobs.”

Falling behind

The British economy has been struck by particular turbulence over recent weeks. The cost of government borrowing soared in the wake of former PM Liz Truss’ disastrous mini-budget on September 23, with the U.K.’s central bank forced to step in and steady the bond markets.

But while the swift installation of Rishi Sunak, the former chancellor, as prime minister seems to have restored a modicum of calm, the economic backdrop remains bleak. Spending and welfare cuts are coming. Taxes are certain to rise. And the underlying problems cut deep.

U.K. productivity growth since the financial crisis has trailed that of comparator nations such as the U.S., France and Germany. As such, people’s median incomes also lag behind neighboring countries over the same period. Only Russia is forecast to have worse economic growth among the G20 nations in 2023.

In 1976, the U.K. — facing stagflation, a global energy crisis, a current account deficit and labor unrest — had to be bailed out by the International Monetary Fund. It feels far-fetched, but today some are warning it could happen again.

The U.K. is spluttering its way through an illness brought about in part through a series of self-inflicted wounds that have undermined the basic pillars of any economy: confidence and stability.

The political and economic malaise is such that it has prompted unwanted comparisons with countries whose misfortunes Britain once watched amusedly from afar.

“The existential risk to the U.K. … is not that we’re suddenly going to go off an economic cliff, or that the country’s going to descend into civil war or whatever,” said Jonathan Portes, professor of economics at King’s College London. “It’s that we will become like Italy.”

Portes, of course, does not mean a country blessed with good weather and fine food — but an economy hobbled by persistently low growth, caught in a dysfunctional political loop that lurches between “corrupt and incompetent right-wing populists” and “well-intentioned technocrats who can’t actually seem to turn the ship around.”

“That’s not the future that we want in the U.K,” he said.

Reviving the U.K.’s flatlining economy will not happen overnight. As Italy’s experience demonstrates, it’s one thing to diagnose an illness — another to cure it.

Experts speak of an unbalanced model heavily reliant upon Britain’s services sector and beset with low productivity, a result of years of underinvestment and a flexible labor market which delivers low unemployment but often insecure and low-paid work.

“We’re not investing in skills; businesses aren’t investing,” said Xiaowei Xu, senior research economist at the Institute for Fiscal Studies. “It’s not that surprising that we’re not getting productivity growth.”

But any attempt to address the country’s ailments will require its economic stewards to understand their underlying causes — and those stretch back at least to the first truly global crisis of the 21st century.

Crash and burn

The 2008 financial crisis hammered economies around the world, and the U.K. was no exception. Its economy shrunk by more than 6 percent between the first quarter of 2008 and the second quarter of 2009. Five years passed before it returned to its pre-recession size.

For Britain, the crisis in fact began in September 2007, a year before the collapse of Lehman Brothers, when wobbles in the U.S. subprime mortgage market sparked a run on the British bank Northern Rock.

The U.K. discovered it was particularly vulnerable to such a shock. Over the second half of the 20th century, its manufacturing base had largely eroded as its services sector expanded, with financial and professional services and real estate among the key drivers. As the Bank of England put it: “The interconnectedness of global finance meant that the U.K. financial system had become dangerously exposed to the fall-out from the U.S. sub-prime mortgage market.”

The crisis was a “big shock to the U.K.’s broad economic model,” said John Springford, from the Centre for European Reform. Productivity took an immediate hit as exports of financial services plunged. It never fully recovered.

“Productivity before the crash was basically, ‘Can we create lots and lots of debt and generate lots and lots of income on the back of this? Can we invent collateralized debt obligations and trade them in vast volumes?’” said James Meadway, director of the Progressive Economy Forum and a former adviser to Labour’s left-wing former shadow chancellor, John McDonnell.

A post-crash clampdown on City practises had an obvious impact.

“This is a major part of the British economy, so if it’s suddenly not performing the way it used to — for good reasons — things overall are going to look a bit shaky,” Meadway added.

The shock did not contain itself to the economy. In a pattern that would be repeated, and accentuated, in the coming years, it sent shuddering waves through the country’s political system, too.

The 2010 election was fought on how to best repair Britain’s broken economy. In 2009, the U.K. had the second-highest budget deficit in the G7, trailing only the U.S., according to the U.K. government’s own fiscal watchdog, the Office for Budget Responsibility (OBR).

The Conservative manifesto declared “our economy is overwhelmed by debt,” and promised to close the U.K.’s mounting budget deficit in five years with sharp public sector cuts. The incumbent Labour government responded by pledging to halve the deficit by 2014 with “deeper and tougher” cuts in public spending than the significant reductions overseen by former Conservative Prime Minister Margaret Thatcher in the 1980s.

The election returned a hung parliament, with the Conservatives entering into a coalition with the Liberal Democrats. The age of austerity was ushered in.

Austerity nation

Defenders of then-Chancellor George Osborne’s austerity program insist it saved Britain from the sort of market-led calamity witnessed this fall, and put the U.K. economy in a condition to weather subsequent global crises such as the COVID-19 pandemic and the fallout from the war in Ukraine.

“That hard work made policies like furlough and the energy price cap possible,” said Rupert Harrison, one of Osborne’s closest Treasury advisers.

Pointing to the brutal market response to Truss’ freewheeling economic plans, Harrison praised the “wisdom” of the coalition in prioritizing tackling the U.K.’s debt-GDP ratio. “You never know when you will be vulnerable to a loss of credibility,” he noted.

But Osborne’s detractors argue austerity — which saw deep cuts to community services such as libraries and adult social care; courts and prisons services; road maintenance; the police and so much more — also stripped away much of the U.K.’s social fabric, causing lasting and profound economic damage. A recent study claimed austerity was responsible for hundreds of thousands of excess deaths.

Under Osborne’s plan, three-quarters of the fiscal consolidation was to be delivered by spending cuts. With the exception of the National Health Service, schools and aid spending, all government budgets were slashed; public sector pay was frozen; taxes (mainly VAT) rose.

But while the government came close to delivering its fiscal tightening target for 2014-15, “the persistent underperformance of productivity and real GDP over that period meant the deficit remained higher than initially expected,” the OBR said. By his own measure, Osborne had failed, and was forced to push back his deficit-elimination target further. Austerity would have to continue into the second half of the 2010s.

Many economists contend that the fiscal belt-tightening sucked demand out of the economy and worsened Britain’s productivity crisis by stifling investment. “That certainly did hit U.K. growth and did some permanent damage,” said King’s College London’s Portes.

“If that investment isn’t there, other people start to find it less attractive to open businesses,” former Labour aide Meadway added. “If your railways aren’t actually very good … it does add up to a problem for businesses.”

A 2015 study found U.K. productivity, as measured by GDP per hour worked, was now lower than in the rest of the G7 by a whopping 18 percentage points.

“Frankly, nobody knows the whole answer,” Osborne said of Britain’s productivity conundrum in May 2015. “But what I do know is that I’d much rather have the productivity challenge than the challenge of mass unemployment.”

‘Jobs miracle’

Rising employment was indeed a signature achievement of the coalition years. Unemployment dropped below 6 percent across the U.K. by the end of the parliament in 2015, with just Germany and Austria achieving a lower rate of joblessness among the then-28 EU states. Real-term wages, however, took nearly a decade to recover to pre-crisis levels.

Economists like Meadway contend that the rise in employment came with a price, courtesy of Britain’s famously flexible labor market. He points to a Sports Direct warehouse in the East Midlands, where a 2015 Guardian investigation revealed the predominantly immigrant workforce was paid illegally low wages, while the working conditions were such that the facility was nicknamed “the gulag.”

The warehouse, it emerged, was built on a former coal mine, and for Meadway the symbolism neatly charts the U.K.’s move away from traditional heavy industry toward more precarious service sector employment. “It’s not a secure job anymore,” he said. “Once you have a very flexible labor market, the pressure on employers to pay more and the capacity for workers to bargain for more is very much reduced.”

Throughout the period, the Bank of England — the U.K.’s central bank — kept interest rates low and pursued a policy of quantitative easing. “That tends to distort what happens in the economy,” argued Meadway. QE, he said, is a “good [way of] getting money into the hands of people who already have quite a lot” and “doesn’t do much for people who depend on wage income.”

Meanwhile — whether necessary or not — the U.K.’s austerity policies undoubtedly worsened a decades-long trend of underinvestment in skills and research and development (Britain lags only Italy in the G7 on R&D spending). At British schools, there was a 9 percent real terms fall in per-pupil spending between 2009 and 2019, according to the Institute for Fiscal Studies’ Xu. “As countries get richer, usually you start spending more on education,” Xu noted.

Two senior ministers in the coalition government — David Gauke, who served in the Treasury throughout Osborne’s tenure, and ex-Lib Dem Business Secretary Vince Cable — have both accepted that the government might have focused more on higher taxation and less on cuts to public spending. But both also insisted the U.K had ultimately been correct to prioritize putting its public finances on a sounder footing.

It was February 2018 before Britain finally achieved Osborne’s goal of eliminating the deficit on its day-to-day budget.

Austerity was coming to an end, at last. But Osborne had already left the Treasury, 18 months earlier — swept away along with Cameron in the wake of a seismic national uprising.

***

David Cameron had won the 2015 election outright, despite — or perhaps because of — the stringent spending cuts his coalition government had overseen, more of which had been pledged in his 2015 manifesto. Also promised, of course, was a public vote on Britain’s EU membership.

The reasons for the leave vote that followed were many and complex — but few doubt that years of underinvestment in poorer parts of the U.K. were among them.

Regardless, the 2016 EU referendum triggered a period of political acrimony and turbulence not seen in Westminster for generations. With no pre-agreed model of what Brexit should actually entail, the U.K.’s future relationship with the EU became the subject of heated and protracted debate. After years of wrangling, Britain finally left the bloc at the end of January 2020, severing ties in a more profound way than many had envisaged.

While the twin crises of COVID and Ukraine have muddled the picture, most economists agree Brexit has already had a significant impact on the U.K. economy. The size of Britain’s trade flows relative to GDP has fallen further than other G7 countries, business investment growth trails the likes of Japan, South Korea and Italy, and the OBR has stuck by its March 2020 prediction that Brexit would reduce productivity and U.K. GDP by 4 percent.

Perhaps more significantly, Brexit has ushered in a period of political instability. As prime ministers come and go (the U.K. is now on its fifth since 2016), economic programs get neglected, or overturned. Overseas investors look on with trepidation.

“The evidence that the referendum outcome, and the kind of uncertainty and change in policy that it created, have led to low investment and low growth in the U.K. is fairly compelling,” said professor Stephen Millard, deputy director at the National Institute of Economic and Social Research.

Beyond the instability, the broader impact of the vote to leave remains contentious.

Portes argued — as many Remain supporters also do — that much harm was done by the decision to leave the EU’s single market. “It’s the facts, not the uncertainty that in my view is responsible for most of the damage,” he said.

Brexit supporters dismiss such claims.

“It’s difficult statistically to find much significant effect of Brexit on anything,” said professor Patrick Minford, founder member of Economists for Brexit. “There’s so much else going on, so much volatility.”

Minford, an economist favored by ex-PM Truss, acknowledged that “Brexit is disruptive in the short run, so it’s perfectly possible that you would get some short-run disruption.” But he added: “It was a long-term policy decision.”

Where next?

Plenty of economists can rattle off possible solutions, although actually delivering them has thus far evaded Britain’s political class. “It’s increasing investment, having more of a focus on the long-term, it’s having economic strategies that you set out and actually commit to over time,” says the IFS’ Xu. “As far as possible, it’s creating more certainty over economic policy.”

But in seeking to bring stability after the brief but chaotic Truss era, new U.K. Chancellor Jeremy Hunt has signaled a fresh period of austerity is on the way to plug the latest hole in the nation’s finances. Leveling Up Secretary Michael Gove told Times Radio that while, ideally, you wouldn’t want to reduce long-term capital investments, he was sure some spending on big projects “will be cut.”

This could be bad news for many of the U.K.’s long-awaited infrastructure schemes such as the HS2 high-speed rail line, which has been in the works for almost 15 years and already faces a familiar mix of local resistance, vested interests, and a sclerotic planning system.

“We have a real problem in the sense that the only way to really durably raise productivity growth for this country is for investments to pick up,” said Springford, from the Centre for European Reform. “And the headwinds to that are quite significant.”

For dock workers at Liverpool’s Peel Port, the prospect of a fresh round of austerity amid a cost-of-living crisis is too much to bear. “Workers all over this country need to stand up for themselves and join a union,” insisted Delij.

For him, it’s all about priorities — and the arguments still echo back to the great crash of 15 years ago. “They bailed the bankers out in 2007,” he said, “and can’t bail hungry people out now.”

It is three weeks before Black Friday, but the Federal Reserve is about to make the post-holiday debt hangover a little more intense.

By the time the latest rate hikes filter through the very rate-sensitive credit card industry and pump up customers’ annual percentage rates a little more, experts say it will be some point in December 2022 or January 2023. Right in time for many holiday gifts and expenses to post on credit cards bills — and there to make the costs of a carried balance a little extra expensive.

What’s different now is the presence of four-decade high inflation, coupled with fast-rising interest rates that the Fed hopes will ultimately cool those rising prices, although without sending the economy to a recessionary thud.

Wednesday’s rate move is the fourth straight 75-basis-point rate hike to the federal funds rate, taking it to the 3.75% -4% range, when it was near zero last year’s holiday season. By now, Americans are all too acquainted with 2022’s fast-rising interest rates. They just haven’t gone through a Christmas and Hanakkuh with it yet.

“It’s not the time to overspend and have a problem with paying your bills later. We know the economy is sending mixed messages,” said Michele Raneri, vice president of financial services research and consulting at TransUnion TRU, -4.31%,

one of the country’s three major credit reporting companies.

It’s extra important to think through a holiday budget and how much relies on credit, she said. “People need to think about how much they can afford to repay and how long it will take to repay it.”

Holiday spending could be the same as 2021 for many people — but not everyone

Now, two forecasts suggest many people ready to spend the same amount for this year’s holiday cheer as they did last year.

People are planning to spend an average $1,430 on gifts, travel and entertainment this year, which is around the $1,447 spent last year, according to PwC researchers. Three-quarters of people said they were planning to spend the same or more than last year and respondents said credit cards were one of their top ways to pay.

“ Compared to last year, credit card balances are getting bigger, more people are sitting on balances and debt costs are getting pricier.”

By another measure, Americans will pay an average $1,455 on holiday-related gifts and experiences, essentially flat from last year, say Deloitte researchers.

More than one-third of surveyed consumers say their financial outlook is worse than the same point last year. Nearly one-quarter of people were concerned about credit card debt as of late September, Deloitte’s numbers show in an ongoing tracking of consumer mood.

It’s understandable to see the concern with households amassing a collective $890 billion in credit card debt through the second quarter. Compared to last year, balances are getting bigger, more people are sitting on balances and debt costs are getting pricier because the interest rates applied to those balances are rising.

When people were carrying a credit card balance month to month, the sum was $5,474 on average, according to Raneri. That’s through the end of September and it’s a nearly 13% rise year over year, she said. The 164 million people carrying a balance is a 5% increase from last year, she noted.

Credit cards carrying a balance during the third quarter had an average 18.43% APR, Federal Reserve data shows. That’s up from 16.65% in the second quarter and up from 17.13% in 2021’s third quarter.

How the Fed influences credit card rates

Credit card issuers typically determine their rates by applying a “prime rate” — typically three percentage points on top of the federal funds rate — and the issuer’s profit margin, said Ted Rossman, senior industry analyst at Bankrate.com.

By late October, the rate on new card offers was 18.73%, according to Bankrate data. At this point last year, it was 16.31%, Rossman said. In a few weeks, the rates on new offers should beat the all-time record of an average 19% APR, exclusive to new offers, he added.

While it can take a billing cycle or two for a higher APR to make its way to an existing credit card account, Rossman noted the APRs on new offers could rise in a matter of days.

Here’s a hypothetical to show how much more expensive credit card debt becomes with every extra hike. Suppose the $5,474 balance is on a credit card with the current 18.73% average. If a person has to resort to minimum payments, Rossman said, they’d be paying $7,118 just in interest to pay off the debt.

“ In a few weeks, the rates on new credit card offers should beat the all-time record of an average 19% APR.”

What if the 18.73% APR gets kicked up 75 basis points to 19.48%? If that same borrower has to pay minimums, they are now paying $7,417 in interest to snuff the principal debt of $5,474, Rossman said.

The example has its limits because people may pay more than the minimum and they may incur more credit card debt as they pay off the old one. But it shows a bigger point: “Unfortunately, anybody dealing with credit card debt is a loser from the series of rate hikes. It was already expensive. It’s getting more so,” Rossman said.

When do rate hikes stop?

While decisions during the Fed’s November meeting can have a ripple effect on holiday-time borrowing costs, observers say the real question about Wednesday is the clues Federal Reserve Chairman Jerome Powell drops for what’s next. The central bank’s committee voting on interest rate increases reconvenes in mid-December.

On Wednesday, the Fed said in a statement it expected further rate increases, but also said it would be watching to see if there were lag effects with its tightening policies, which could slow or limit the total amount of increases.

“People, when they hear lags, they think about a pause. It’s very premature, in my view, to think about or be talking about pausing our rate hike. We have a ways to go,” Powell told reporters at a Wednesday afternoon press conference.

The economy is strong enough to handle higher rates, Powell said. For one thing, households have “strong balance sheets” and “strong spending power,” he noted.

Stock markets first jumped higher after the latest interest rate announcement. But they gave up the gains — and then some — by the end of the day. The Dow Jones Industrial Average DJIA, -1.55%

was down more than 500 points, or 1.6% while the S&P 500 SPX, -2.50%

was down 2.5% and the Nasdaq Composite COMP, -3.36%

closed 3.4% lower.

Top economists in major North American-based banks forecasted the Fed will keep raising interest rates “until the first quarter of next year before potentially lowering rates through the end of 2023,” Sayee Srinivasan, chief economist at the American Bankers Association, the banking sector’s trade association, said ahead of Wednesday’s latest rate hike.

“Top economists polled as part of a banking industry panel expect Fed rate increases through at least the first quarter of 2023.”

The forecast, coming through an ABA advisory committee, is no sure thing. “Everything depends on the ability of the Fed to bring inflation down, so that will remain their clear priority,” said Srinivasan.

Meanwhile, rising costs may cause more people to put the holiday cheer on plastic, even their decorations. The majority of Christmas tree growers in one poll are expecting wholesale prices to climb 5% to 15% for this season.

ST. PAUL, Minn. — The political fight is only getting fiercer over whether it’s financially wise or “woke” folly to consider a company’s impact on climate change, workers’ rights and other issues when making investments.

Republicans from North Dakota to Texas are ramping up their criticism of “ESG investing,” a fast-growing movement that says it can pay dividends to consider environmental, social and corporate-governance issues when deciding where to invest pension and other public funds. At the same time, Democrats in traditionally blue states like Minnesota are considering whether to make ESG principles an even bigger part of their investment strategies.

The “E” for environment component of ESG often gets the most attention because of the debate over whether to invest in fossil-fuel companies. In the wide-ranging social, or S, bucket, investors look at how companies treat their workforces, reckoning a happier group with less turnover can be more productive. For the G, or governance aspect, investors make sure companies’ boards keep executives accountable and pay CEOs in a way that incentivizes the best performance for all stakeholders.

The ESG industry has scorekeepers that give companies ratings on their environmental, social and governance performance. Poor scores can steer investors away from companies or governments seen as bigger risks, which can in turn raise their borrowing costs and hurt them financially.

Florida has become one of the hottest battlegrounds for ESG. Gov. Ron DeSantis in August prohibited state fund managers from using ESG considerations as they decide how to invest state pension plan money. And even as his state cleans up from the environmental destruction caused by Hurricane Ian, DeSantis plans to ask the Florida Legislature in 2023 to go even further by prohibiting “discriminatory practices by large financial institutions based on ESG social credit score metrics.”

Pension funds are often caught in the middle of the battles. Questions are flowing into the Florida Education Association from teachers about what DeSantis’ moves will mean for their retirements.

“I usually tell them it’s still unclear what this exactly means,” said Andrew Spar, president of the union, which represents 150,000 teachers and educators across the state. Much is still to be determined, including exactly which funds the pension investments will steer toward.

In contrast, the Minnesota State Board of Investment is considering a proposal to adopt a goal of making its $130 billion in pension and other funds carbon-neutral. The board already uses shareholder votes to advance climate issues. It seeks out climate-friendly investment opportunities and eschews investments in thermal coal. While the new proposal goes farther, it does not call for total divestment from fossil fuel companies, as many climate change activists advocate.

The ESG debate has spilled into the race for Minnesota’s state auditor. Democratic incumbent Julie Blaha — who has singled out DeSantis as one of the leaders she believes are politicizing the discussion about ESG — has cited the investment board’s high returns in recent years as evidence the approach works.

“To be a good fiduciary, you have to consider all the risks, and the evidence is clear that climate risk is investment risk,” Blaha said.

But Blaha’s Republican challenger, Ryan Wilson, says investment returns must come first, and that all risks must be considered. He says the board shouldn’t “disproportionately dictate” that climate risk should matter more than other risks.

Proponents say considering a company’s performance on ESG issues can boost returns and limit losses over the long term while being socially responsible at the same time. By using such a lens, they say investors can avoid companies that are riskier than they appear on the surface, with stock prices that are too high. An ESG approach could also unearth opportunities that may be underappreciated by Wall Street, the thinking goes.

As for returns, there is no consensus on whether an ESG approach means lower or higher returns.