While September lived up to its reputation as a brutal month for stocks, October tends to be a “bear-market killer,” associated with historically strong returns, especially in midterm election years.

Skeptics, however, are warning investors that negative economic fundamentals could overwhelm seasonal trends as what’s traditionally the roughest period for equities comes to an end.

Rough stretch

U.S. stocks ended sharply lower on Friday, posting their worst skid in the first nine months of any year in two decades. The S&P 500 SPX, -1.51%

recorded a monthly loss of 9.3%, its worst September performance since 2002. The Dow Jones Industrial Average DJIA, -1.71%

fell 8.8%, while the Nasdaq Composite COMP, -1.51%

on Friday pushed its total monthly loss to 10.5%, according to Dow Jones Market Data.

October’s track record may offer some comfort as it has been a turnaround month, or a “bear killer,” according to the data from Stock Trader’s Almanac.

“Twelve post-WWII bear markets have ended in October: 1946, 1957, 1960, 1962, 1966, 1974, 1987, 1990, 1998, 2001, 2002 and 2011 (S&P 500 declined 19.4%),” wrote Jeff Hirsch, editor of the Stock Trader’s Almanac, in a note on Thursday. “Seven of these years were midterm bottoms.”

According to Hirsch, Octobers in the midterm election years are “downright stellar” and usually where the “sweet spot” of the four-year presidential election cycle begins (see chart below).

“The fourth quarter of the midterm years combines with the first and second quarters of the pre-election years for the best three consecutive quarter span for the market, averaging 19.3% for the DJIA and 20.0% for the S&P 500 (since 1949), and an amazing 29.3% for NASDAQ (since 1971),” wrote Hirsch.

SOURCE: STOCKTRADERSALMANAC

‘Atypical period’

Skeptics aren’t convinced the pattern will hold true this October. Ralph Bassett, head of investments at Abrdn, an asset-management firm based in Scotland, said these dynamics could only play out in “more normalized years.”

“This is just such an atypical period for so many reasons,” Bassett told MarketWatch in a phone interview on Thursday. “A lot of mutual funds have their fiscal year-end in October, so there tends to be a lot of buying and selling to manage tax losses. That’s kind of something that we’re going through and you have to be very sensitive to how you manage all of that.”

An old Wall Street adage, “Sell in May and go away,” refers to the market’s historical underperformance during the six-month period from May to October. Stock Trader’s Almanac, which is credited with coining the saying, found investing in stocks from November to April and switching into fixed income the other six months would have “produced reliable returns with reduced risk since 1950.”

Strategists at Stifel, a wealth-management firm, contend the S&P 500, which has fallen more than 23% from its Jan. 3 record finish, is in a bottoming process. They see positive catalysts between the fourth quarter of 2022 and the start of 2023 as Fed policy plus S&P 500 negative seasonality are headwinds that should subside by then.

“Monetary policy works with a six-month lag, and between the [Nov. 2] and [Dec. 14] final two Fed meetings of 2022, we do see subtle movement toward a data-dependent Fed pause which would bullishly allow investors to focus on (improving) inflation data rather than policy,” wrote strategists led by Barry Bannister, chief equity strategist, in a recent note. “This could reinforce positive market seasonality, which is historically strong for the S&P 500 from November to April.”

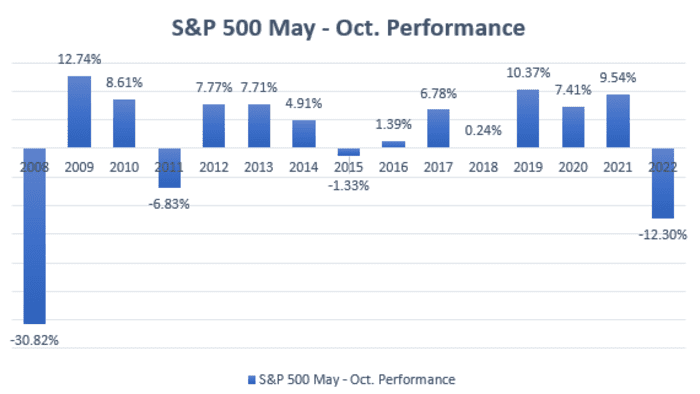

October crashes

Seasonal trends, however, aren’t written in stone. Dow Jones Market Data found the S&P 500 recorded positive returns between May and October in the past six years (see chart below).

SOURCE: FACTSET, DOW JONES MARKET DATA

Anthony Saglimbene, chief markets strategist at Ameriprise Financial, said there are periods in history where October could evoke fear on Wall Street as some large historical market crashes, including those in 1987 and 1929, occurred during the month.

“I think that any years where you’ve had a very difficult year for stocks, seasonality should discount it, because there are some other macro forces [that are] pushing on stocks, and you need to see more clarity on those macro forces that are pushing stocks down,” Saglimbene told MarketWatch on Friday. “Frankly, I don’t think we’re going to see a lot of visibility at least over the next few months.”

One cruel truth the stock market confirmed this past week is that trying to pick the bottom for technology stocks is a fool’s errand. The Nasdaq Composite’s terrible September—it was down 10.5% on the month—has made the bottom-fishing that took place over the summer look ill-advised. As I’ve noted before, the first downturn in tech earlier this year was all about valuations. This new phase of the decline is all about softening earnings. When it comes to price-to-earnings ratios, the market is running into a denominator problem.

The market downturn, the weaker economy, and the reversal of some pandemic-era trends have exposed weaknesses in the business models of companies such as

Peloton Interactive

(SNAP), and investors have adjusted valuations accordingly. But there are still some powerful underlying secular trends that should eventually drive tech stocks higher. Investors with long time horizons and strong stomachs might consider inching into the market. I have a few ideas on where to look.

Most financial planners advise young people to start saving early — and often — for retirement so they can take advantage of the so-called eighth wonder of the world – the power of compound interest.

And many advisers routinely urge those entering the workforce to contribute to their 401(k), especially when their employer is matching some portion of the amount the worker is contributing. The matching contribution is – essentially – free money.

New research, however, indicates that many young people should not save for retirement.

The reason has to do with something called the life-cycle model, which suggests that rational individuals allocate resources over their lifetimes with the aim of avoiding sharp changes in their standard of living.

Put another way, individuals, according to the model which dates back to economists Franco Modigliani, a Nobel Prize winner, and Richard Brumberg in the early 1950s, seek to smooth what economists call their consumption, or what normal people call their spending.

According to the model, young workers with low income dissave; middle-aged workers save a lot; and retirees spend down their savings.

Source: Bogleheads.org

The just-published research examines the life-cycle model even further by looking at high- and low-income workers, as well as whether young workers should be automatically enrolled in 401(k) plans. What the researchers found is this:

1. High-income workers tend to experience wage growth over their careers. And that’s the primary reason why they should wait to save. “For these workers, maintaining as steady a standard of living as possible therefore requires spending all income while young and only starting to save for retirement during middle age,” wrote Jason Scott, the managing director of J.S. Retirement Consulting; John Shoven, an economics professor at Stanford University; Sita Slavov, a public policy professor at George Mason University; and John Watson, a lecturer in management at the Stanford Graduate School of Business.

2. Low-income workers, whose wage profiles tend to be flatter, receive high Social Security replacement rates, making optimal saving rates very low.

Middle-aged workers will need to save more later

In an interview, Scott discussed what some might view as a contrary-to-conventional wisdom approach to saving for retirement.

Why does one save for retirement? In essence, Scott said, it’s because you want to have the same standard of living when you’re not working as you did while you were working.

“The economic model would suggest ‘Hey, it’s not smart to live really high in the years when you’re working and really low when you’re retired,’” he said. “And so, you try to smooth that out. You want to save when you have relatively high income to support yourself when you have relatively low income. That’s really the core of the life-cycle model.”

But why would you spend all your income when you’re young and not save?

“In the life-cycle model, we are assuming you are getting the absolute most happiness you can out of income each year,” said Scott. “In other words, you are doing your best at age 25 with $25,000, and there is no way to live ‘cheaply’ and do better,” he said. “We also assume a given amount of money is more valuable to you when you are poor compared to when you are wealthy.” (Meaning $1,000 means a lot more at 25 than at 45.)

Scott also said that young workers might also consider securing a mortgage to buy a house rather than save for retirement. The reasons? You’re borrowing against future earnings to help that consumption, plus, you’re building equity that could be used to fund future consumption, he said.

Are young workers squandering the advantage of time?

Many institutions and advisers recommend just the opposite of what the life-cycle model suggests. They recommend that workers should have a certain amount of their salary salted away for retirement at certain ages in order to fund their desired standard of living in retirement. T. Rowe Price, for instance, suggests that a 30-year-old should have half their salary saved for retirement; a 40-year-old should have 1.5 times to 2 times their salary saved; a 50-year-old should have 3 times to 5.5 times their salary saved; and a 65-year-old should have 7 times to 13.5 times their salary saved.

Scott doesn’t disagree that workers should have savings benchmarks as a multiple of income. But he said a high-income worker who waits until middle age to save for retirement can easily reach the later-age benchmarks. “Savings for retirement probably is more in the zero range until 35 or so,” Scott said. “And then it is probably faster after that because you want to accumulate the same amount.”

Plus, he noted, the home equity a worker has could count toward the savings benchmark as well.

So, what about all the experts who say young people are best positioned to save because they have such a long timeline? Aren’t young workers just squandering that advantage?

Not necessarily, said Scott.

“First: saving earns interest, so you have more in the future,” he said. “However, in economics, we assume that people prefer money today compared to money in the future. Sometimes this is called a time discount. These effects offset each other, so it depends on the situation as to which is more significant. Given interest rates are so low, we generally think time discounts exceed interest rates.”

And second, Scott said, “early saving could have a benefit from the power of compounding, but the power of compounding is certainly irrelevant when after-inflation interest rates are 0% – as they have been for years.”

In essence, Scott said, the current environment makes a front-loaded lifetime spending profile optimal.

Low-income workers don’t need to save either

As for those with low income, say in the 25th percentile, Scott said it’s less about the “income ramp that really moves saving” and more that Social Security is extremely progressive; it replaces a large percentage of one’s preretirement income. “The natural need to save is not there when Social Security replaces 70, 80, 90% (of one’s preretirement income),” he said.

In essence, the more Social Security replaces of your preretirement income, the less you’ll need to save. The Social Security Administration and others are currently researching what percent of preretirement income Social Security replaces by income quintile, but previously published research from 2014 shows that Social Security represented nearly 84% of the lowest income quintile’s family income in retirement while it only represented about 16% of the highest income quintile’s family income in retirement.

Source: Social Security Administration

Is it worth auto-enrolling young workers in a 401(k) plan?

Scott and his co-authors also show that the “welfare costs” of automatically enrolling younger workers in defined-contribution plans—if they are passive savers who do not opt-out immediately—can be substantial, even with employer matching. “If saving is suboptimal, saving by default creates welfare costs; you’re doing the wrong thing for this population,” he said.

Welfare costs, according to Scott, are the costs of taking an action compared to the best possible action. “For example, suppose you wanted to go to restaurant A, but you were forced to go to restaurant B,” he said. “You would have suffered a welfare loss.”

In fact, Scott said young workers who are automatically enrolled into their 401(k) might consider when they’re in their early 30s taking the money out of their retirement plan, paying whatever penalty and taxes they might incur, and use the money to improve their standard of living.

“It’s optimal for them to take the money and use it to improve their spending,” said Scott. “It would be better if there weren’t penalties.”

Why is this so? “If I didn’t understand that I was being defaulted into a 401(k) plan, and I didn’t want to save, then I suffered a welfare loss,” said Scott. “We assume people figure out after five years that they were defaulted. At that point, they want their money out of the 401(k), and they are optimally willing to pay the 10% penalty to get their money out.”

Scott and his colleagues assessed welfare costs by figuring out how much they have to compensate young workers at that five-year point so that they are OK with having been inappropriately forced to save. Of course, the welfare costs would be lower if they didn’t have to pay the penalty to cash out their 401(k).

And what about workers who are automatically enrolled in a 401(k)? Are they not creating a savings habit?

Not necessarily. “The person who is confused and defaulted doesn’t really know it’s happening,” said Scott. “Maybe they’re getting a savings habit. They’re certainly living without the money.”

Scott also addressed the notion of giving up free money – the employer match — by not saving for retirement in an employer-sponsored retirement plan. For young workers, he said the match isn’t enough to overcome the cost of, say, five years of below-optimal spending. “If you think it’s for retirement, the match-improved benefit in retirement doesn’t overcome the cost of losing money when you’re poor,” said Scott. “I’m simply noting that if you are not consciously making the choice to save, it is hard to argue you are making a saving habit. You did figure out how to live on less, but in this case, you did not want to, nor do you intend to continue saving.”

The research raises questions and risks that must be addressed

There are plenty of questions the research raises. For instance, many experts say it’s a good idea to get in the habit of saving, to pay yourself first. Scott doesn’t disagree. For instance, a person might save to build an emergency fund or a down payment on a house.

As for the folks who might say you’re losing the power of compounding, Scott had this to say: “I think the power of compounding is challenged when real interest rates are 0%.” Of course, one could earn more than 0% real interest but that would mean taking on additional risk.

“The principle is about, ‘Should you save when you are relatively poor so you can have more when you are relatively rich?’ The life-cycle model says, ‘No way.’ This is independent of how you invest money between time periods,” Scott said. “For investing, our model does look at riskless interest rates. We argue that investment expected returns and risks are in equilibrium, so the core result is unlikely to change by introducing risky investments. However, it is definitely a limitation of our approach.”

Scott agreed there are risks to be acknowledged, as well. It’s possible, for instance, that Social Security, because of cuts to benefits, might not replace a low-income worker’s preretirement salary as much as it does now. And it’s possible that a worker might not experience high wage growth. What about people having to buy into the life-cycle model?

“You don’t have to buy into all of it,” said Scott. “You have to buy into this notion: You want to save when you’re relatively rich in order to spend when you’re relatively poor.”

So, isn’t this a big assumption to make about people’s career/pay trajectory?

“We consider relatively rich wage profiles and relatively poor wage profiles,” said Scott. “Both suggest young people should not save for retirement. I think the vast majority of median wage or higher workers experience a wage increase over their first 20 years of working. However, there is certainly risk in wages. I think you could rightly argue that young people might want to save some as a precaution against unexpected wage declines. However, this would not be saving for retirement.”

So, should you wait to save for retirement until you’re in your mid-30s? Well, if you subscribe to the life-cycle model, sure, why not? But if you subscribe to conventional wisdom, know that consumption might be lower in your younger years than it needs to be.

NEW YORK — Wall Street is drifting around its worst levels in almost two years Friday as the end nears for what’s been a miserable month for markets around the world.

The S&P 500 was virtually unchanged in midday trading after flipping between small losses and gains through the morning. It’s hovering around its lowest level since November 2020, and it’s on pace to close out its sixth weekly loss in the last seven, one of its worst months since the early 2020 coronavirus crash and its third straight losing quarter.

The Dow Jones Industrial Average was down 95 points, or 0.3%, at 29,130, as of noon Eastern time, and the Nasdaq composite was 0.4% higher.

The main reason for this year’s struggles for financial markets has been fear about a possible recession, as interest rates soar in hopes of beating down the high inflation that’s swept the world.

The Federal Reserve has been at the forefront of the global campaign to slow economic growth and hurt job markets just enough to undercut inflation but not so much that it causes a recession. More data arrived Friday to suggest the Fed will keep its foot firmly on the brakes on the economy, raising the risk of its going too far and causing a downturn.

The Fed’s preferred measure of inflation showed prices rising even faster than economists expected last month, while spending by consumers rebounded. That should keep the Fed on track to keep raising rates and hold them at high levels a while, as it’s loudly and repeatedly promised to do.

Vice Chair Lael Brainard was the latest Fed official on Friday to insist it won’t pull back on rates prematurely. That helped to keep snuffed out hopes on Wall Street for a “pivot” toward easier rates as the economy slows.

“At this point, it’s not a matter of if we’ll have a recession, but what type of recession it will be,” said Sean Sun, portfolio manager at Thornburg Investment Management.

Higher interest rates knock down one of the main levers that set prices for stocks. The other also looks to be under threat as the slowing economy, high interest rates and other factors weigh on corporate profits.

Nike slumped 11.8% in what could be its worst day in two decades after it said its profitability weakened during the summer because of discounts needed to clear suddenly overstuffed warehouses. The amount of shoes and gear in Nike’s inventories swelled by 44% from a year earlier. This year’s powerful surge for the U.S. dollar against other currencies also hurt the company. Its worldwide revenue rose only 4%, instead of the 10% it would have if currency values had remained the same.

Nike isn’t the only company to see its inventories balloon. So have several big-name retailers, and such bad news for businesses could actually mean some relief for shoppers if it leads to more discounts. It echoed some glimmers of encouragement buried within Friday’s report on the Fed’s preferred gauge of inflation. That showed some slowing of inflation for goods, even as price gains kept accelerating for services.

Another report on Friday also offered a glimmer of hope. A measure of consumer sentiment showed U.S. expectations for future inflation came down in September. That’s key for the Fed because expectations for higher inflation among households can create a debilitiating, self-reinforcing cycle that worsens it.

Treasury yields eased a bit on Friday, letting off some of the pressure that’s built on markets.

The yield on the 10-year Treasury fell to 3.73% from 3.79% late Thursday. The two-year yield, which more closely tracks expectations for Fed action, sank to 4.13% from 4.19%.

Still, a long list of other worries continues to hang over global markets, including increasing tensions between much of Europe and Russia following the invasion of Ukraine. A controversial plan to cut taxes by the U.K. government also sent bond markets spinning on fears it could make inflation even worse. Bond markets calmed a bit after the Bank of England pledged mid-week to buy however many U.K. government bonds are needed to bring yields back down.

The stunning and swift rise of the U.S. dollar against other currencies, meanwhile, raises the risk of creating so much stress that something cracks somwhere in global markets.

Stocks around the world were mixed after a report showed that inflation in the 19 countries that use Europe’s euro currency spiked to a record and data from China said that factory activity weakened there.

——

AP Business Writers Joe McDonald and Matt Ott contributed.

This week Freddie Mac said the average interest rate on a 30-year mortgage loan in the U.S. had climbed to 6.70% from 6.29% the week before and 6.02% two weeks ago. The average rate a year ago was 3.01%.

Would-be sellers who have low-rate mortgage loans are reluctant if it means they need to take out a new loan to fund their next home. Would-be buyers are forced out of the market, as the monthly principal and interest payment for a new 30-year loan, based on Freddie Mac’s figures, has increased 53% from a year ago.

Home-sale contracts are being canceled at a record pace in some areas.

The dollar has strengthened as the Federal Reserve has taken the lead among central banks in raising interest rates. This is reverberating across the world, making it more costly for countries to make interest payments on dollar-denominated debt and increasing the cost of any commodity traded in dollars.

The rising dollar lowers prices on imported goods for Americans and can also lower their international travel costs. But Michael Wilson, Morgan Stanley’s chief equity strategist, warns that earnings for the S&P 500 SPX, -1.51%

would decline as a direct result of the strong dollar and called the current foreign-exchange backdrop an “untenable situation” for the stock market.

This is what happens when bearish sentiment runs high

Michael Brush interviews David Baron, co-manager of the Baron Focused Growth Fund BFGFX, -0.76%,

who describes opportunities cropping up as institutional investors dump stocks. He also explains his winning long-term strategy, which has included a very long-term investment in Tesla Inc. TSLA, -1.10%.

When interest rates rise, bond prices fall. But it also means that if you have money to put to work, bond yields have become much more attractive.

Khuram Chaudhry, a European equity quantitative strategist at JPMorgan in London, makes the case for buying bonds now.

What about preferred stocks?

Getty Images/iStockphoto

Preferred stocks feature stated dividend yields and prices that move the same way bond prices do. That means prices for many issues are now heavily discounted to face value and that current yields are much higher than they were at the end of 2021. Here’s an in-depth guide on how to research preferred stocks and make your own selections.

Stanley Druckenmiller predicted a “hard landing” in 2023 for the U.S. economy while speaking at CNBC’s Delivering Alpha Investor Summit on Sept. 28.

Bloomberg

Stanley Druckenmiller predicted a U.S. recession in 2023 as a result of monetary policy tightening by the Federal Reserve. That may not be much of a stretch, considering that the U.S. economy contracted during the first half of 2022, according to revised GDP figures from the Bureau of Economic Analysis.

After the new U.K. government of Prime Minister Liz Truss announced a massive tax cut along with a new spending program to help counter rising fuel costs and new borrowing, the pound hit a new low against the dollar on Sept. 26 as investors and money managers panicked and sold-off U.K. government bonds. Steve Goldstein explains how and why the Bank of England came tot the rescue.

After Tesla CEO Elon Musk said the upcoming Cybertruck would be sufficiently waterproof to “serve briefly as a boat,” the San Francisco Bay Ferry offered this advice to patrons.

Want more from MarketWatch? Sign up for this and other newsletters, and get the latest news, personal finance and investing advice.

FILE – Reserve Bank of India (RBI) Governor Shaktikanta Das gestures during a press conference after RBI’s bi-monthly monetary policy review meeting in Mumbai, India, on Feb. 6, 2020. India’s central bank on Friday, Sept. 30, 2022, raised its key interest rate by 50 basis points to 5.90% in its fourth hike this year and said the economies of developing countries were confronted with challenges of slowing growth, elevated food and energy prices, debt distress and currency depreciation. (AP Photo/Rajanish Kakade, File)

India’s central bank has raised its key interest rate to 5.90% and said developing economy were facing slowing growth, elevated food and energy prices, debt distress and currency depreciation

NEW DELHI — India’s central bank on Friday raised its key interest rate by 50 basis points to 5.90% in its fourth hike this year and said developing economies were facing challenges of slowing growth, elevated food and energy prices, debt distress and currency depreciation.

Reserve Bank of India Governor Shaktikanta Das projected inflation at 6.7% in the current fiscal year which runs to next March. June was the sixth consecutive month with inflation above the central bank’s tolerance level of 6%, he said in a statement after a meeting of the bank’s monitoring committee.

He said the central bank will remain focused on the withdrawal of the accommodative monetary policy.

The bank’s monetary committee slashed the real economic growth forecast to 7% for the current financial year from 7.2% forecast in August. The economic growth for the first quarter of the next financial year is expected around 6.7%.

Das said the world has been confronted with one crisis after another, but India has withstood shocks from the coronavirus pandemic and the conflict in Ukraine.

Das also said the Indian rupee has depreciated by 4% since April against 14% appreciation in the U.S. dollar. “The rupee has fared better than many other currencies” and the Reserve Bank Of India’s foreign exchange reserves umbrella remains strong, he said.

The Indian rupee has plunged to an all-time low of 81.58 rupees to one U.S. dollar.

VANCOUVER, Wash., August 15, 2022 (Newswire.com)

– Today, Sinceri Senior Living (Sinceri SL) announced their partnership with Second Act Financial Services (Second Act) which offers senior living financing solutions for prospective residents of Sinceri Senior Living Communities. With the synergies between the two organizations and their shared values, Sinceri and Second Act look forward to serving seniors by connecting them with payment options and exceptional senior living services.

April Young, VP of Sales at Sinceri Senior Living, shared this about the new partnership between Sinceri and Second Act, “Navigating the world of senior living and payment options can be challenging – not only for prospective residents but also for our team members at Sinceri. This is why I’m so pleased to be partnering with Second Act Financial Services. Their team boasts a wealth of knowledge for senior living payment options, and furthermore, delivers exceptional customer service to both our Sales teams at Sinceri, and the prospective residents and families that we are seeking to serve. It has been a pleasure working with Second Act, and we’re so excited to have their partnership, and enablement to serve more seniors than ever before.”

At Sinceri Senior Living, their core values revolve around the residents that they serve. As part of their holistic care, Sinceri staff are encouraged through their Life Enrichment and Meaningful Moments programming to learn all that they can about the residents that they are caring for. This is similar to the mission of Second Act, which is focused around understanding the needs of the seniors they serve and delivering valuable resources and information in a friendly and kindhearted manner.

Elias Papasavvas, CEO & Founder of Second Act Financial Services, had this to share about the new partnership with Sinceri Senior Living, “We are honored to be chosen as a provider of payment solutions and helpful information to the Sinceri families. The Sinceri spirit is one of service to seniors with integrity and the utmost care, a moral compass all of us at Second Act share. Together, we shall help more families and seniors enjoy the senior living they have earned and deserve.”

About Sinceri Senior Living:

Sinceri Senior Living is a premier, senior living management company that provides service to seniors in 21 states, serving approximately 3,800 seniors across the U.S. Sinceri Senior Living manages all levels of care, including independent living, assisted living, memory care, and skilled nursing communities. From the legacy of its first dedicated memory care community more than 35 years ago, Sinceri Senior Living has built a reputation for expertly managing senior living properties, including owned and managed facilities, with highly sought personalized care and exceptional, unique programming for residents and their families.

Second Act Financial Services is a leader in Point of Service and Point of Sale financing solutions for senior living. The Second Act founding leadership has pioneered and led this field for over twenty years serving thousands of senior living communities across the United States. Through Second Act, a senior-focused Division of Liberty Savings Bank, F.S.B. of Wilmington, Ohio, families and seniors can access fast and fair bridge financing which can save seniors up to 50% from existing senior living bridge financing options today. Through Second Act Financial Services LLC, families have access to a wealth of information and additional solutions to pay for senior living including Real Estate Solutions, Veteran Benefits and Insurance Solutions.

Second Act is a senior-focused Division of Liberty Savings Bank, FSB, NMLS #408905; Lending and loan services provided by Liberty Savings Bank, F.S.B. NMLS # 408905. Equal Housing Lender. www.NMLSConsumerAccess.org. Equal Housing Lender. Federally Chartered Institution. All other services provided by Second Act Financial Services, LLC.

ATLANTA, July 28, 2022 (Newswire.com)

– Rausch Advisory Services LLC, a leading veteran-led & owned Business Advisory firm headquartered in Georgia, announced today that it has been awarded a General Services Administration (GSA) Multiple Award Schedule (MAS) Contract (CONTRACT #47QRAA22D00BC). This award provides all Federal Civilian Agencies (FCA), Department of Defense (DOD) agencies, and state and local governments the ability to purchase professional services in Internal Auditing, Highly Adaptive Cybersecurity, and Accounting & Finance from Rausch Advisory Services through the approved GSA Schedule Contract.

“We are incredibly proud of this achievement. This contract is further validation of the unmatched value we bring to our clients and the trust that they have placed in us,” said Michael Lisenby, CEO of Rausch Advisory Services LLC. “Through our delivery model we have successfully performed services for clients nationally in every business sector across 23 countries to date. Our expertise and our customer oriented results coupled with a transparent pricing model and the strength of our team, ensured our credibility with the GSA and the award of the contract.”

One of Rausch Advisory Services’ differentiators is the Rausch Assessment Platform, which delivers assessments in up to 46 languages to help our clients manage their regulatory compliance concerns. This, together with an experienced hiring model, has been instrumental in Rausch Advisory Services’ growth in the areas of Finance & Accounting, Internal Audit, Information Security, and Professional Personnel Placement.

“This is an ideal opportunity for Rausch Advisory Services to enhance and grow their service offerings in the government sector,” said Marie Mouchet, Rausch Advisory Board Member and former CIO. “Rausch is a uniquely positioned company to deliver excellence in this new partnership.”

ABOUT RAUSCH ADVISORY SERVICES LLC:

Founded in 2013, Rausch Advisory Services is headquartered in Atlanta, GA, with a west coast office in San Francisco. Rausch serves clients in the areas of Finance & Accounting, Internal Audit, Information Security, and Professional Placement. Rausch delivers innovative solutions that address compliance, enterprise risk, information technology, and human resource capital. Rausch delivers globally through project lead solutions, co-sourcing, staff augmentation, professional placement services, and customized technology deployment. For more information, visit https://rauschadvisory.com

Press Contact Information Name: Michael Lisenby Email: mlisenby@rauschadvisory.com

The IRS has recently announced a number of changes related to identification requirements impacting Qualified Intermediaries (QIs). This blog is the first of a two-part series and describes how the current design of the Secure Access Account (SAA), and in particular the request to provide a US Tax identification number to validate the QI’s Responsible Officials identity, would impair the QIs’ capabilities to comply with their electronic reporting obligations through FIRE. The second part of this series, covering QI’s new due diligence challenges linked to their non-US account holders’ US Tax identification number requirement for 1446(a) and 1446(f) purposes, will follow in a separate blog.

On 26 July 2021 the IRS announced (IRS release available here) it is substantially transforming the existing application procedure for Filing Information Returns Electronically (FIRE) transitioning from Form 4419 to the Information Returns (IR) Application system to obtain the Transmitter Control Code (TCC) required to file electronically via FIRE.

This transformation is particularly relevant for QIs since they have no other option than filing Forms 1042-S (and sometimes Forms 1099) electronically via FIRE.

Currently, the planned changes are not fit for most QIs. Specifically, the system preliminary requires QI’s Responsible Officials to validate their identify through a SAA, unfortunately designed for individuals with US tax filing requirements.

Luckily this transition is happening progressively and thus most QIs are not yet impacted provided that prior to August 2022 they ensure that the identifying information (legal business name, mailing address, and/or contact information) associated with their active TCC received before 26 September 2021 is current and correct to log into the FIRE System.

We recommend that QIs immediately validate that the information the IRS has on file is current and correct. If changes are needed, QIs should use paper Form 4419 (Rev. 9-2021) to update this information given that as of 2 August 2022, the IRS will discontinue the paper form process to transition to the IR TCC application system to make such changes. As of this date the complex issues of gaining access to the new system will be a reality for QIs with the risk of being shut out of FIRE if their legal business name is incorrect (e.g., spelling, abbreviations, special characters and spacing do not match the IRS records).

New FIRE users

As of 26 September 2021, new FIRE users can no longer make use of paper and fill-in versions of Form 4419 to request an original TCC, the five-digit number required to file electronic returns through FIRE. Instead, they need to use the new online IR Application for TCC. Additionally, in order to access the IR Application for TCC, new FIRE users are firstly required to verify their identity by creating a Secure Access Account (SAA) to improve security features and thus protect from fraudulent access.

Since at least two Responsible Officials need to be listed on the IR Application for TCC, both persons need to create their own respective SAA.

The IR Application for TCC currently foresees that users need to provide the following information amongst other to create an SAA:

The user’s Social Security number (SSN) or Individual Tax Identification Number (ITIN);

The user’s tax filing status and mailing address from the most recently filed tax return;

A financial account number linked to the user from one of these account (last eight digits of Visa, Mastercard or Discover Credit Card, Student loan, Mortgage or home equity loan, Home equity line of credit, or Auto loan); and

A US-based cell phone in the name of the user (for faster registration) or a mailing address where the user can receive an activation code by mail.

Existing FIRE users

Existing FIRE users (i.e., those who submitted their TCC Application prior to 26 September 2021) were originally scheduled to transition to the IR Application for TCC in Fall 2022.

However, on 16 June 2022, the IRS granted existing FIRE users more time to transition to the new system (IRS release available here). Those existing TCCs will remain active until 1 August 2023. After that date, any FIRE TCC that does not have a completed IR Application for TCC will be dropped and will no longer be available for e-filing. Accordingly, existing FIRE users will need to validate their identity via the SAA, log in to IR application for TCC and complete the online application between September 2022 and 1 August 2023.

Existing FIRE users, not yet transitioning to the IR Application, are currently allowed to use paper Form 4419 (Rev. 9-2021) to revise identifying information (legal business name, mailing address, and/or contact information) associated with an active TCC received before 26 September 2021.

However, paper Form 4419 will be discontinued as of 2 August (IRS release available here) to transition to the IR Application for TCC also for purpose of revising existing TCC information. Therefore, prior to August 2022, existing FIRE users will need to ensure that the information on their application (submitted via Form 4419) contains the current contact’s name, current email address and current telephone number and verify that the company’s current legal business name is correct (spelling, abbreviations, special characters and spacing) to match the IRS records. If any information needs to be updated, the changes through Form 4419 need to be received by the IRS by 1 August 2022. Notably, as certain QIs have already started experiencing, an incorrect legal business name will trigger the inability to file information returns electronically via FIRE.

QIs may risk being unable to create an SAA and consequently left out of FIRE

As mentioned above, the setup of an SAA, currently foreseen by the IR Application for TCC, requires either an SSN or an ITIN.

At its most basic level, an SSN is used by US citizens and authorized noncitizen residents (i.e., noncitizens authorized to work in the US).

An ITIN is a tax processing number issued by the IRS to individuals who are required to have a US taxpayer identification number but who do not have and are not eligible to obtain an SSN from the Social Security Administration. In general individuals must have a filing requirement and file a valid federal income tax return to receive an ITIN unless they meet an exception. However, a specific exception applies for a non-US representative of a foreign corporation who needs to obtain an ITIN for the purpose of meeting e-filing requirements.

Since employees of QIs generally do not have a connection to the United States, other than working at a bank that holds US securities, they cannot apply for an SSN. However, based on the above-mentioned exception, they can apply for an ITIN.

Accordingly, some QIs have already asked certain of their non-US employees to apply for an ITIN via Form W-7 to create an SAA to be able to obtain a TCC via the IR Application to continue to use FIRE.

Unfortunately, this appears to not yet be sufficient to ensure the creation of an SAA. Although the instructions for Form W-7 allow to apply for an ITIN for e-filing purposes absent a US filing requirement, the SAA presumes a US filing requirement and consequently asks for the user’s tax filing status. This misalignment results in an insurmountable obstacle for most QI’s employees unable to create their SAA. As a result, QIs cannot obtain the required new TCC.

What are the alternatives?

The IRS, through its Frequently Asked Questions about the IR Application for TCC originally envisaged two options:

Enlist a third party to file on their behalf; or

Purchase a software package to support their electronic filing.

An IRS representative, speaking at the last Kaplan Financial Education tax conference in June 2022, indicated that the FAQ was revised to no longer refer to option 2 above, leaving as sole alternative option 1.

Although option 1 is technically possible, QIs face many issues to put in place the necessary infrastructure to enable it to outsource this activity to a 3rd party in light of client confidentiality (e.g., the case of Form 1099 or nominative Form 1042-S reporting).

At the same conference, the IRS indicated it is aware of the implementation issues that non-US filers are facing and that “this is actively being worked and considered”. The IRS representative encouraged stakeholders to bring forward alternatives and provide comments to notify the Service of concrete examples of the challenges that non-US filers are facing.

Deloitte’s view

Although SAA is today a limited problem for QIs that are existing FIRE users, given they still have more than a year to transition to the new IR TCC application, they immediately need to check that the information associated with their current TCC is correct. If this is not the case, QIs need to make sure that the IRS receives the corrected legal business name via Form 4419 by 1 August 2022 at the latest to avoid being shut out of the FIRE system (after this date, revising the information associated with a TCC will only be possible through the IR TCC application system with the current SAA issues described above).

QIs that are existing FIRE users having submitted their TCC Application prior to 26 September 2021, will meanwhile also face the aforementioned SAA issues in case they need an additional TCC or to add a new Form Type. This is because in both circumstances the completion of the IR Application for TCC is required.

Although Deloitte recognizes the need to strengthen validation controls to protect against unauthorized filing and input of fraudulent information returns, it is clear that SAA, as currently designed, does not work for QIs.

QI’s Responsible Officials don’t generally have US tax filing requirements, and as such are unable to populate the user’s tax filing status necessary to go through SAA.

At the same time, since non-US applicants will generally not have a US-based mobile phone, requesting them to provide, at SAA set-up, an international postal mail to receive a one-time code that is only valid for 30 days appears an inappropriate way of communication; experience shows that IRS mail is sometimes received by QIs after 30-days of issuance.

It is unclear whether it is feasible for non-US applicants to provide the required information pertaining to a financial account or whether such account must be one maintained in the US linked to their name.

Therefore, we encourage the IRS to make the SAA process accessible to QIs and more broadly to non-US filers. For this purpose, we would suggest keeping the ITIN requirement consistent with the instructions for Form W-7, while eliminating the need to provide the user’s tax filing status. Moreover, we propose to allow non-US applicants to access the SAA without requesting any financial information and giving the option to provide a non-US phone number or a non-US e-mail address to receive the one-time code through the SAA process.

There are clearly several obstacles to overcome in order for QIs to have the required access to fulfil their reporting obligations as of August 2023. However, it is quite clear that obtaining an ITIN (which usually takes a few months) will be most likely one of the steps of the transition process. Deloitte, as Certifying Acceptance Agent (CAA), can assist and simplify the ITIN application procedure in the following ways:

Support with the completion of Form W-7

Review and authenticate the applicant’s passport to verify his/her identity and foreign status

Submit to the IRS the completed Form W-7 together with a copy of the applicant’s passport; and

Brandi heads Deloitte’s Financial Services Tax team in Switzerland and Liechtenstein. She has extensive expertise in advising the Swiss financial services industry on the implementation of US and international transparency regimes (including QI, FATCA, Section 871(m), CRS, MDR and DAC6). Brandi also leads the Financial Services Tax team’s efforts relating to innovative technology solutions. Brandi is a US Certified Public Accountant and has 20 years of experience with Deloitte and has worked in London, San Diego and Zurich.

Karim leads the Tax Transparency team in the Suisse Romande and Ticino markets within the Financial Services Tax practice and is responsible for services relating to QI, FATCA, CRS, 871(m) and DAC6. He is a technical advisor and subject matter expert to financial institutions in the banking, trust, and insurance sectors. Prior to joining Deloitte, Karim worked for eight years in support teams of Swiss banks, in particular in areas relating to operations, project and change management as well as operational taxes.

Elena Bonsembiante – Manager Financial Services Tax

Elena is a QI, FATCA and CRS specialist and an Italian certified public accountant. She is leading as Manager several QI, FATCA and CRS projects for middle sized banks in the French and Italian speaking areas. Prior to joining Deloitte Switzerland, she worked for Deloitte Italy and other Italian Tax Firms.

NEW YORK, June 9, 2022 (Newswire.com)

– Zoe, a wealth platform that accelerates wealth creation through exceptional client experience and innovative technology, revealed the meticulous vetting process that qualifies advisors accepted onto their platform. Zoe, recognized as one of Fast Company’s 2022 Most Innovative Companies, connects clients with the top 5% of wealth advisors in the country. Today, Zoe shared the characteristics that all registered investment advisory (RIA) firms must embody.

“The value of finding the right financial advice is immense. Zoe aims to help clients find the highest-quality guidance to manage and grow their wealth. The way to deliver on that promise is to partner only with the top advisors nationwide, which is where our vetting process becomes crucial,” said Andres Garcia-Amaya, CFA, Zoe’s Founder and CEO. “Each of our Network Advisors works to deliver the great advice and experience their Zoe clients deserve.”

The nationwide company has established a five-step process to guarantee the quality of the advisors with whom they connect each client. Once Zoe’s team has confirmed the education and credentials of advisors, they review advisors’ work histories to ensure that they have at least five years of relevant client-facing experience. Then, to fulfill their promise to help each client identify the best fit for their financial goals, Zoe’s experts interview the advisors. Only those who are objective, unbiased, and have reasonable fees for clients move to the next step. Next, wealth advisors are assessed on their subject-matter expertise, communication skills, financial and investment processes, and operational efficiency. Finally, the Zoe team evaluates the overall client experience offered to ensure advisors lead with and provide comprehensive wealth planning tailored to clients’ needs and goals. After completing this rigorous process, out of the total of applicants, only the top 5% of financial advisors in the United States get accepted.

Clients can connect with high-caliber firms through the Zoe Platform to manage their wealth, knowing that they are among the best independent practices in the country. In addition to Andres Garcia-Amaya, CFA, receiving a nomination for RIA Intel’s Industry Advocate Award, Zoe is proud to partner with firms honored by prestigious industry recognitions. The company is in partnership with several RIAs nominated for this year’s RIA Intel’s Inaugural Awards, WealthManagement.com’s “Wealthies,” and InvestmentNews’ 40 Under 40 awards. To mention a few, Creative Planning, Beacon Pointe Advisors, CAPTRUST, and Falcon Wealth Planning are finalists for RIA Intel’s 2022 Firm of the Year Award.

Zoe-Certified Advisors are personable and client-centric in every decision. They focus on helping clients grow and protect their wealth while making their journeys enjoyable. For example, Jacky L Petit-Homme, CFP®, nominated for RIA Intel’s Advisor of the Year, embodies the values Zoe seeks when interviewing candidates for their Advisor Network. Moreover, Zoe-Certified Advisors such as Breanna Stott continuously demonstrate leadership qualities within the wealth management industry. Because of this, Breanna was honored as one of this year’s InvestmentNews 40 Under 40.

As a result of its vetting process, Zoe partners with professionals who aspire to create a significant impact and work every day to accomplish it. Individuals who exemplify this include Kevin Disano, Chief Growth Officer at Beacon Pointe Advisors; Gabriel Shahin, Principal and founder at Falcon Wealth Planning, Inc.; and Kara Duckworth, Managing Director of Client Experience at Mercer Advisors. This year, they are all finalists for WealthManagement.com’s Rising Stars award.

“We are pleased to congratulate the vast number of Zoe-Certified Advisors who are finalists for various prestigious wealth management industry awards. These wins for our Partners further validate the high standards of our vetting process and the rigor with which we qualify advisors. Guaranteeing the top 5% ensures that investors who use Zoe’s cost-free services connect only with the best wealth managers,” said Garcia-Amaya, CFA.

Zoe was founded with one mission: to accelerate wealth creation through exceptional client experience and innovative technology. The company’s human experts, alongside powerful technology, remove the friction from the process of finding and hiring a financial advisor. Through Zoe’s Platform, you will connect with Zoe-Certified Financial Advisors across the United States based on your unique financial situation and objectives. Zoe’s thoughtfully curated network of interest-aligned financial advisors includes only the top 5% in the country.

NEW YORK, June 1, 2022 (Newswire.com)

– Zoe, a wealth platform that connects clients with the top five percent of wealth advisors in the country, announced its partnership with GreenUp Wealth Management LLC. After qualifying the firm through a meticulous vetting process, Zoe, recognized as one of Fast Company’s 2022 Most Innovative Companies, admitted GreenUp into their exclusive Advisor Network.

GreenUp Wealth Management LLC was founded with the mission to guide and accompany clients through the journey to a fulfilling financial future. They promise to provide an elite wealth management experience that gives each client a financial guide to make their wealth work for them. The registered investment advisory firm (RIA) manages over $300 million in assets for over 300 clients nationwide.

Each of the advisors in the firm offers a personalized and holistic wealth management experience to clients. They provide financial planning tailored to their unique goals, investment management and income strategies to meet their long-term objectives, and personalized tax, legacy, and estate planning. The firm prioritizes understanding its clients’ values and risk tolerance as a core part of the process. GreenUp wants the client to feel comfortable, knowing that their wealth plan aligns with their values and risk tolerance. The firm ensures the ride (financial planning progress) is as meaningful and enjoyable as the destination (goal accomplishment).

“Wealth management has a whole world of possibilities, and clients would be surprised with all that is possible with their money. We’re confident that GreenUp advisors have the right approach to guide and accompany clients in the journey of discovering the wide range of possibilities that their wealth can bring them,” said Andres Garcia-Amaya, CFA®, Zoe’s Founder and CEO.

While working towards dreams-realization and personal wealth-building, GreenUp promotes a culture where people come first. Transparency, communication, and collaboration are crucial parts of the process. The GreenUp experience encourages clients to ask questions and make sure they understand what is going on throughout the process to ensure alignment and accountability.

“Our partnership with Zoe makes sense because we have shared values and objectives. We both genuinely care about clients and are ready to go above and beyond to help them reach their goals. We are confident that working together is a way to continue transforming the wealth management industry towards personalization and client-centered experiences,” said Tony Schmitt, President & CEO of GreenUp Wealth Management.

About Zoe Zoe was founded with one mission: to accelerate wealth creation through exceptional client experience and innovative technology. The company’s human experts, alongside powerful technology, remove the friction from the process of finding and hiring a financial advisor. Through Zoe’s Platform, you will connect with Zoe-Certified Financial Advisors across the United States based on your unique financial situation and objectives. Zoe’s thoughtfully curated Network of interest-aligned financial advisors includes only the top 5% in the country.

NEW YORK, May 19, 2022 (Newswire.com)

– Zoe, a wealth platform that connects clients with the top five percent of wealth advisors in the country, announced its partnership with Creative Financial Services. Zoe, recognized as one of Fast Company’s 2022 Most Innovative Companies, is known for having a meticulous vetting process to qualify the firms admitted into their exclusive Advisor Network.

Creative Financial Services (CFS) is a leading female-owned registered investment advisory (RIA) firm headquartered in Colorado Springs, Colorado. Founded in 1999 and led by Jill Isbell, CFP®, CFS was born from the belief that empowering people through knowledge and understanding is the key ingredient to achieving significant financial goals.

CFS’ philosophy is that a robust financial planning process is the best way to create a financially secure life and represents the cornerstone of its services. Advisors at Creative Financial Services use their expertise and experience to develop tailored plans to unlock their clients’ peace of mind. In addition, the firm develops long-term partnerships with its clients through mutual integrity, respect, and a willingness to work together toward a shared objective. Creative Financial Services manages $60 million in assets for over 200 clients with a very personable approach to wealth planning.

“When starting their journey with a wealth planner, clients often focus on the immediate numbers, leading them to lose sight of the bigger picture. Stellar advisors know how to help them see the full picture and understand what it takes to achieve their long-term financial goals. Creative Financial Services’ structured approach to guiding their clients is thorough and effective,” said Andres Garcia-Amaya, CFA®, Zoe’s Founder and CEO. “The firm has been a great addition to our exclusive network. We are proud to partner with the firm’s expert and trustworthy advisors,” he added.

The RIA’s team acknowledges that wealth protection and client understanding are core elements of a financial plan. Once they fully understand their clients’ immediate needs and goals, they present a prudent strategy to protect and grow their wealth. Then, Creative Financial Services advisors have the expertise to make ongoing adjustments as things change in clients’ professional and personal lives. The firm has extensive knowledge in areas that support individuals, families, and business owners. Whether it is retirement, estate, investment, or tax planning, the firm’s unique approach is to create strategies that protect their clients’ needs while planning for the future in a tax-efficient manner.

“We have been working with Zoe for a while now, and our experience has been gratifying. It is fulfilling to meet potential clients who are serious about their financial lives and looking for professional help. We are thrilled to see what the future of our partnership will bring for both of us and additional clients nationwide,” said Jill Isbell, CFP®, Owner and Senior Advisor at Creative Financial Services.

Zoe was founded with one mission: to accelerate wealth creation through exceptional client experience and innovative technology. The company’s human experts, alongside powerful technology, remove the friction from the process of finding and hiring a financial advisor. Through Zoe’s Platform, you will connect with Zoe-Certified Financial Advisors across the United States based on your unique financial situation and objectives. Zoe’s thoughtfully curated Network of interest-aligned financial advisors includes only the top 5% in the country.

LOS ANGELES, April 20, 2022 (Newswire.com)

– WizarPOS, a trailblazer in Android POS and payment systems, announces today its flagship mobile POS, Q2 and Q3, obtained the OmniPay certificate provided by Fiserv, a subsidiary of European Merchant Services (EMS). This authorized certification entails mainstream credit and debit card transactions for omnichannel payments across borders, including online and offline PINs for magnetic stripe, chip, and contactless.

The PIN-on-Glass mobile WizarPOS Q2 has been deployed in North America, South America, Europe, and East Asia, serving varied sectors of catering, retail, mobile merchants, and banking. Its sleek design and mounting flexibility level up the frictionless user experience powered by rigid industry-level security.

In comparison, the portable Android POS WizarPOS Q3, without a thermal printer, supercharges fast, safe, and mobile payments across healthcare, transit, banking, and hospitality industries. It can also be integrated into a vending machine or ticket validator as an embedded payment module supporting contactless bank cards, NFC mobile payments, and QR codes. Combined, the WizarPOS Q2 and Q3 have over 2-million unit shipments on five continents.

Kaishen Zhu, the founder of WizarPOS, commented, “We are excited to achieve the OmniPay certificate, which enables WizarPOS to expand its footprint in Europe and serve more merchants and clients. As usual, the WizarPOS team commits to quality and security at the services of our long-term network partners.”

With a holistic in-house technology stack and three-decade know-how about security and payments, WizarPOS offers a full range of acceptance devices, all of which are Android-based, PCI PTS and EMV certified, and have seamless integration with the Android ecosystem.

About OmniPay and European Merchant Services (EMS)

EMS is a leading European omnichannel payment processor and acquirer based in Amsterdam, The Netherlands. It serves 40,000 clients in 40 countries. Learn more at https://emspay.eu/about-ems.

About WizarPOS

WizarPOS, the trailblazer in Android POS terminal technology, is committed to empowering secure, future-proof, and scalable payment solutions worldwide. Carrying Android DNA without legacies, the WizarPOS team debuted the world’s first wireless POS device under PCI v1.3 in 2005. Designing and enabling Android merchant payment ecosystems from devices, SDK, and TMS to SaaS solutions, WizarPOS has shipped over 2 million units of Android-based payment devices worldwide. Visit www.wizarpos.com for details.

Media contact:

Elaine Lai Director of Marketing & PR elaine@wizarpos.com Phone: +1 818 856 0834

LOS ANGELES, January 19, 2022 (Newswire.com)

– WizarPOS, a leading global provider of Android POS and payment systems, became a member of the White Label Alliance, an organization facilitating an open framework for operator-run white-label payment systems. This new membership acclaims WizarPOS’ dedication to Android payment technologies, which has been the two-decade legacy of the Android-only POS vendors in the market.

Kaishen Zhu, the founder of WizarPOS, remarked, “We are proud to turbocharge the interoperability with other industry-recognized founding members within WLA. The WizarPOS team has been an active member of the GlobalPlatform Device Committee and Small Terminal Interoperable Platform (STIP) since 2005. We endorse the value of the open platform approach and how all stakeholders in the ecosystem can benefit from the standardization and how the total cost of the ownership could be optimized. We are so happy to see that WLA shares the same values with us and enables the economy to flourish with flexibility and easy scaling.”

With a full in-house technology stack and two-decade know-how in security and payments, WizarPOS offers a full range of acceptance devices, all of which are Android-based, PCI PTS and EMV certified, and have seamless integration with the Android ecosystem.

About the White Label Alliance

The White Label Alliance (WLA) is a member-driven association designed to shape an open, comprehensive set of component frameworks for ready-to-deploy and interoperable payment solutions. The WLA founding members consist of Giesecke+Devrient, Idemia, and NXP. Learn more about the White Label Alliance at https://wla-payment.org/.

About WizarPOS

WizarPOS, the trailblazer in Android POS terminal technology, is committed to empowering secure, future-proof, and scalable payment solutions worldwide. Carrying open platform DNA without legacies, the WizarPOS team debuted the world’s first wireless POS device under PCI v1.3 in 2005. Designing and enabling Android merchant payment ecosystems from devices, SDK, and TMS to SaaS solutions, WizarPOS has shipped over 2 million Android POS worldwide within five years. Visit www.wizarpos.com for more information.

MANILA, Philippines, June 20, 2020 (Newswire.com)

– Amid the global economic slowdown, Singapore-based debt management company Collectius embraces the innovative data-driven solutions provided by TransUnion to further strengthen its business operations in the Philippines. In its recent subscription to said services, Collectius was able to detect that as much as 46% of 318,000 consumers who had collection accounts have low to medium risk scores, which translates to high rates of recovery.

A trusted credit management servicing company employing fintech and innovation, Collectius continues to build its position as the preferred debt purchaser of consumer non-performing loans (NPLs) in the ASEAN region.

“With TransUnion, we become more intelligent. We have more accurate data, meaning our system can use the most effective strategy to support our customers to become debt-free again, adapting installment payment solutions to their capacity,” said Gustav Eriksson, Collectius Group founder and CEO.

Customers who have then successfully paid their obligations are given proof of settlement, and no further collections of the same may be executed. Their data is also updated with TransUnion, improving their credit score and bettering their chances of acquiring financial services such as loans from banks or other financial institutions so they can achieve their financial goals.

“TransUnion’s stringent data-quality standards and auditing processes ensure efficiency and effectiveness, providing businesses with a better understanding of consumers. This ultimately helps them make more informed decisions on who to trust,” said Pia Arellano, TransUnion Philippines president and CEO.

Gold Standard in Collection

The threat of COVID-19 notwithstanding, news of harassment and privacy breaches by online lending apps in the exercise of their collection policies maimed the industry. Whilst government agencies have ordered the shutdown of several of these apps, industry expert Collectius employs what it calls the “Collectius way of collections” — one that is rooted in good morals, compliance with local and international regulations, and a personalized approach.

Collectius ensures they end up more financially literate than before, gaining knowledge about the accumulation of interest and the different fees and structures that banks and creditors add as a result of an NPL, and fully grasp the advantages of becoming debt-free in the end. In the same way, TransUnion also champions responsible borrowing among consumers.

“While a collection account in one’s credit report negatively affects his credit score, it’s not a dead end. Apart from gaining back your credibility with financial institutions, settling obligations also helps the economy especially during trying times like this,” Arellano concluded.

Menchel serves as director of one of the NADP’s first New York City chapters, one of over 30 NADP chapters nationwide.

Press Release –

updated: Oct 15, 2019

NEW YORK, October 15, 2019 (Newswire.com)

– Ivy Menchel, Certified Divorce Financial Analyst (CDFA®) and the president and founder of Family Wealth Planning Partners, is celebrating her second anniversary as director of one of the National Association of Divorce Professionals (NADP)’s first New York City chapters. Menchel was chosen by the NADP because of her numerous career accomplishments, industry and community involvement, and leadership abilities.

“It has been inspiring and motivating to regularly meet with these talented professionals who are committed to improving the divorce experience for clients going through this emotional process,” Menchel said. “It’s an honor to have had a positive impact on the members of our chapter.”

The NADP is an invitation-only networking and educational organization for professionals whose work involves helping clients going through a divorce. The NADP thoroughly vets professionals before offering membership. Only select members are chosen for leadership positions in one of the organizations more than 30 chapters nationwide. Chapters meet monthly to network and learn more about topics that affect members’ divorcing clients.

“We are proud to have such highly regarded professionals like Ivy in the NADP,” said Vicky Townsend, CEO and co-founder of the NADP. “Under her leadership and commitment, her chapter is making a very positive impact on divorcing families in New York City and beyond. We couldn’t ask for a more qualified and dedicated leader.”

With over 25 years of experience in financial services, Menchel focuses her practice on helping divorcing clients, along with their attorneys and mediators, make sound financial decisions as they transition into the next phase of their lives. In addition to her work as a CDFA, she is also a Certified Financial Planner (CFP®) and Certified Business Exit Consultant (CBEC®), making her one of the few professionals in her field to hold all three certifications.

Beyond her private practice, Menchel is widely regarded as a thought leader in her field. Among other works, she authored the workbook “Define Your Wealth” and co-authored the e-book “Navigating Your Divorce: Legal, Financial and Emotional Basics.” Menchel is also a prominent member of several professional organizations including the Association of Divorce Financial Planners, the Family Divorce and Mediation Council of Greater New York, and many others.

After two successful years leading her chapter, Menchel looks forward to making her third even better. “I’m looking forward to continuing to grow our practices, educate one another, and improve the divorce process to better support our clients,” she said.

About the NADP: The National Association of Divorce Professionals is an invitation-only organization that unifies highly vetted professionals who serve clients going through all stages of divorce. The NADP is committed to making a positive impact on the divorce process through strategic alliances, divorce-centered education, and comprehensive professional development. Please visit www.thenadp.com for more information.

Media Contact: Vicky Townsend vicky@thenadp.com 888-624-7365

Delinquency and Defaults Remain at or Near Historic Lows, According to 12th Edition of MeasureOne Report

Press Release –

updated: Jun 18, 2019

SAN FRANCISCO, June 18, 2019 (Newswire.com)

– MeasureOne, a leading provider of data and analytics serving the $1.59 trillion-dollar student loan market, today released the 12th edition of its Private Student Loan Report. The latest report again affirms that students and families continue to responsibly use private student loans to cover college costs. In fact, 98% of families are successfully managing payments and less than 2% default, annually.

Private student loans, which are fully underwritten to assess creditworthiness and ability to repay, make up approximately 7.7% of total student loans outstanding as of Q1 2019. The remaining 92.3% of the $1.59 trillion in student loans are federal loans owned and managed by the Department of Education.

The MeasureOne Private Student Loan Report reflects data as of end-Q1 2019 for private student loans and does not include federal student loan data. As of the end of Q1 2019, the report found:

Private student loan originations in AYTD 2018/19 (Q3 2018 to Q1 2019 only) was $8.35 billion, up 11.96% year-over-year.

Early-stage delinquency (30 to 89 days past due) rate was 2.48% of loan balances in repayment; the late-stage delinquency (90+ days past due) rate was 1.50%.

Annualized defaults were 1.84% of loan balances in repayment. Loans in forbearance were 2.18%.

The total outstanding balance for private student loans represented in the MeasureOne Report was $66.07 billion (including in-school loans but excluding consolidation, refinance and parent loans).

Undergraduate loans accounted for 89.45% and graduate loans 10.55% of loans originated in AYTD 2018/19.

“Our bi-annual report shows that students and families continue to use private student loans responsibly to cover the costs of college,” said Dan Feshbach, CEO for MeasureOne. “That’s particularly encouraging given recent media interest in the student debt issue. What’s often lost in the headlines is that private student loans are being managed successfully. In fact, private student loan portfolios are near historic lows for delinquencies and defaults.”

This bi-annual report includes continuous contributions from the MeasureOne Private Student Loan Consortium, a data cooperative of the six largest student loan lenders and holders: Citizens Bank, N.A., Discover Bank, Navient, PNC Bank, N.A., Sallie Mae Bank and Wells Fargo Bank, N.A.

In addition to the original six largest student lenders, the Q1 2019 report includes the following thirteen contributors: College Ave Student Loans, Navy Federal Credit Union and 11 members from the Education Finance Council. In total, these 19 data contributors represent 63.35% of the private student loans outstanding in the U.S.

The full MeasureOne Private Student Loan Report is available for download at https://www.measureone.com (see Research Section)

About MeasureOne

MeasureOne, founded in San Francisco with offices in Dallas, TX, specializes in data and analytics serving the $1.59 trillion-dollar student loan market, the second largest form of consumer credit in the U.S. The company developed the first and only Private Student Loan Consortium, a data cooperative of the nation’s largest lenders and holders of private student loans. MeasureOne evaluates academic and loan performance data to increase understanding of consumer lending, academic success, and employment opportunities. For more information about MeasureOne, visit www.measureone.com.

SAN FRANCISCO, December 20, 2018 (Newswire.com)

– Students and families are responsibly using private student loans to cover college costs with close to 98 percent successfully managing payments according to the 11th edition of MeasureOne’s Private Student Loan Report.

Private student loans, which are made based on a robust assessment of creditworthiness and ability to repay, make up approximately 7.6 percent of total student loans outstanding as of Q3 2018. The remaining 92.4 percent of the $1.56 trillion in student loans are federal loans owned and managed by the Department of Education.

The MeasureOne Private Student Loan Report reflects data as of end-Q3 2018 for private student loans and does not include federal student loan data.

As of the end of Q3 2018, the report found:

Early-stage delinquency (30 to 89 days past due) rate was 2.73 percent of loan balances in repayment; the late-stage delinquency (90+ days past due) rate was 1.75 percent.

Annualized defaults were 2.19 percent of loan balances in repayment. Loans in forbearance were 2.39 percent.

Private student loan originations in AYTD 2018/19 (Q3 2018 only) was $3.65 billion, up 11.23% year-over-year.

The total outstanding balance for private student loans represented in the MeasureOne Report was $66.28 billion.

On new originations, undergraduate loans accounted for 87.85 percent and graduate loans 12.15 percent of loans originated in AY 2017/18. The ratios for AYTD 2018/19 were 89.80 percent and 10.20 percent respectively.

“The MeasureOne Private Student Loan Report continues to confirm the stability and health of the private student loan market,” said Dan Feshbach, CEO for MeasureOne. “The growth in originations along with low delinquency and defaults and judicious use of forbearance show that students and families are sensibly using private student loans to cover higher education costs.”

This semi-annual report includes continuous contributions from the MeasureOne Private Student Loan Consortium, a data cooperative of the six largest student loan lenders and holders: Citizens Bank, N.A., Discover Bank, Navient, PNC Bank, N.A., Sallie Mae Bank and Wells Fargo Bank, N.A.

The most recent report includes more performance data than ever before. In addition to the original six Consortium members, the Q3 2018 report includes the following eleven contributors: College Ave Student Loans, Navy Federal Credit Union and 9 members from the Education Finance Council. In total, these 17 data contributors represent 62.14 percent of the private student loans outstanding in the U.S.

MeasureOne, founded in San Francisco with offices in Dallas, TX, specializes in data and analytics serving the $1.56 trillion-dollar student loan market, the second largest form of consumer credit in the U.S. The company developed the first and only Private Student Loan Consortium, a data cooperative of the nation’s largest lenders and holders of private student loans. MeasureOne evaluates academic and loan performance data to increase understanding of consumer lending, academic success, and employment opportunities. For more information about MeasureOne, visit www.measureone.com.