The numbers: The cost of goods and services rose a mild 0.2% in June as inflation eased again, but another measure of prices favored by the Federal Reserve showed somewhat less progress.

Economists polled by The Wall Street Journal had forecast a 0.2% increase in the personal consumption expenditures index.

The increase in prices over the past year slowed to 3% from 3.8% and touched the lowest level since October 2021, the government said Friday.

The so-called core PCE rate of inflation, meanwhile, also rose 0.2% last month. The core rate omits volatile food and energy costs and is viewed by the Fed as a better predictor of future inflation trends.

The rate of core inflation over the past year slowed a bit less to 4.1% from 4.6% in the prior month, but that still puts it at a more than two-year low. It’s still far above the Fed’s 2% target, however.

Big picture: Inflation has slowed a lot this year due to falling energy and food prices, but the cost of living is still rising too fast to mollify the Fed or ease the financial pain of U.S. households.

The Fed is expected to keep interest rates high through next year to bring inflation down closer to its 2% target. The danger is that higher borrowing costs could also slow the economy enough to tip the U.S. into recession.

The latest PCE report is likely to give the Fed more reason for optimism, however.

Looking ahead: “Inflation cooled, but held well above 2%, meaning the Fed can’t declare mission accomplished,” said lead U.S. economist Oren Klatchkin of Oxford Economics.

Market reaction:The Dow Jones Industrial Average DJIA, +0.50%

and S&P 500 SPX, +0.99%

rose in Friday trades. The yield on the 10-year Treasury note TMUBMUSD10Y, 3.953%

slipped 3.96%.

The German economy was stagnant in the second quarter after two periods of decline.

The Federal Statistical Office reported zero quarter-on-quarter change, after a 0.1% drop in the first quarter and a 0.4% drop in the fourth quarter of 2022. Most countries outside the U.S. report GDP on a quarterly, and not annualized, basis.

Consumer spending by private households stabilized in the second quarter of 2023 after the weak winter half-year, it said.

Over the last year, the eurozone’s largest economy dropped by 0.6%.

Sentiment is dark for Germany’s economy, with the key Ifo index of business climate sliding in July to an eight-month low.

The numbers: Home sales inched up for the first time in four months, even as the U.S. housing market continues to deal with a dearth of listings.

Pending home sales rose by 0.3% in June from the previous month, according to the monthly index released Thursday by the National Association of Realtors.

The figure exceeded expectations on Wall Street. Economists were expecting pending home sales to fall 0.5% in June.

Transactions were still down 15.6% from last year.

Pending home sales reflect transactions where a contract has been signed for the sale of an existing home but the sale has not yet closed. Economists view it as an indicator of the direction of existing-home sales in subsequent months.

Big picture: Home sales rose as the housing market contends with excess buyer demand and a shortfall in the supply of homes for sale.

What the real-estate experts said: “The recovery has not taken place, but the housing recession is over,” NAR chief economist Lawrence Yun said. “The presence of multiple offers implies that housing demand is not being satisfied due to lack of supply.”

The NAR also said it expects rates for 30-year mortgages to average 6.4% this year and to fall to 6% in 2024.

The NAR also expects existing-home sales to fall 12.9% in 2023 from the previous year, to 4.38 million, before recovering in 2024 to a rate of 5.06 million.

The group also expects home prices to hold steady this year, falling only slightly by 0.4% to $384,900, before rising 2.6% next year to $395,000.

“The West — the country’s most expensive region — will see reduced prices, while the more affordable Midwest region is likely to see a small positive increase,” Yun added.

The numbers: The U.S. economy grew at the slowest pace in five months in July, a pair of S&P surveys showed, and pointed to weaker conditions later in the year.

The S&P flash U.S. services-sector index fell to 52.4 from 54.4 in the prior month. That’s the lowest reading since February.

Most Americans are employed on the service side of the economy, in areas such as technology, healthcare, finance and hospitality.

The S&P U.S. manufacturing-sector index, meanwhile, rose to 49 from 46.3, but it has been negative for months.

The S&P Global surveys are among the first indicators each month to provide an assessment of the health of the economy. Any number above 50 signals expansion, while numbers below 50 point to contraction.

One caveat: The S&P Global surveys have been more negative this year than other indicators of the U.S. economy.

Key details: New orders, a sign of demand, rose slightly but were relatively soft. Hiring was also the weakest since January.

Prices continued to rise for both raw materials and labor.

“The stickiness of price pressures meanwhile remains a major concern,” said Chris Williamson, chief business economist at S&P Global. “[F]urther falls in the rate of inflation below 3% may prove elusive in the near term.”

Big picture: The large service side of the economy is keeping the U.S. forging ahead, but it might be losing some steam. The Federal Reserve is expected to raise interest rates again this week, and higher borrowing costs have trimmed the sails of the economy.

Manufacturers, for their part, are lagging well behind and arguably are already in a recession of sorts.

Not just in the U.S., either. Manufacturers are struggling even more in Europe and other parts of the world as consumers shift spending to services from goods.

A recession still appears far off, however. A new survey of business economists shows that 71% think a U.S. downturn is at least a year away.

Looking ahead: “July is seeing an unwelcome combination of slower economic growth, weaker job creation, gloomier business confidence and sticky inflation,” Williamson said. “Business optimism about the year-ahead outlook has deteriorated sharply to the lowest seen so far this year.”

Market reaction: The Dow Jones Industrial Average DJIA, +0.52%

and S&P 500 SPX, +0.40%

rose in Monday trades.

Business activity in the eurozone weakened in July, falling further below the level that marks contraction, data from a purchasing managers’ survey showed Monday.

The HCOB Flash Eurozone Composite PMI Output Index–which gauges activity in the manufacturing and services sectors–fell to an eight-month low of 48.9 in July, from a downwardly revised 49.9 in June.

The reading also fell below expectations of economists polled by The Wall Street Journal, who expected the PMI to come in at 49.7.

“The U.S. economy is enjoying ‘a boom in large-scale infrastructure [and] rebounding domestic business investment led by manufacturing.’”

— Morgan Stanley’s Zentner

At least one major investment bank has bought into Bidenomics.

President Joe Biden’s Infrastructure Investment and Jobs Act has seeped into the domestic economy, “driving a boom in large-scale infrastructure,” wrote Ellen Zentner, chief U.S. economist for Morgan Stanley, in a research note out late this week. Plus, she wrote, “manufacturing construction has shown broad strength.”

As a result Morgan Stanley now projects 1.9% gross domestic product (GDP) growth for the first half of this year. That’s some four times higher than the bank’s previous forecast for the first half of 2023 of 0.5%.

Infrastructure spending signed into law in 2021 marked an early legislative win for a president handed only a slim majority in Congress. It was followed up by another legislative banner for the incumbent: the Inflation Reduction Act, a climate change and healthcare-focused spending bill signed into law about a year ago. Much of the incentives in the laws are tied to domestic manufacturing and require U.S. hiring, sometimes at the expense of less-expensive or readily available goods from abroad.

As a result of these economic lifts, the Morgan Stanley MS, +0.22%

analysts also doubled their original estimate for GDP growth in the fourth quarter, to 1.3% from 0.6%. And they nudged up their forecast for GDP in 2024 by a tenth of a percent, to 1.4%.

“The narrative behind the numbers tells the story of industrial strength in the U.S,” Zentner wrote.

The White House has run with the theme of U.S. brick-and-mortar economic growth in recent weeks, increasingly leveraged by the president and his acolytes as “Bidenomics.” It’s a phrase originally used by Republicans to take a shot at the president, who has been saddled with high inflation and rising interest rates in his first term.

For now, the Biden team co-opted the term as a badge of honor as Biden has tried to tap into economic performance during recent road appearances. That included a speech to a union crowd at a shipyard in Philadelphia this past week.

Bidenomics and Morgan Stanley forecasts aside, wider polling shows that some Americans, likely feeling the lingering sting of inflation, aren’t yet convinced.

A Monmouth University poll released Wednesday showed only three in 10 Americans feel the country is doing a better job recovering economically than the rest of the world since the COVID-19 pandemic. Respondents were split on Biden’s handling of jobs and unemployment, with 47% approving and 48% disapproving of his performance.

The latest CNBC All-America Economic Survey, released Thursday, found that just 37% of respondents approved of Biden’s handling of the economy, while 58% disapproved. Some 20% of Americans agreed that the economy was excellent or good, while 79% said it was just fair or poor, CNBC’s poll found.

Republicans looking to challenge Biden and the Democrats in 2024 care less about Wall Street’s forecasts and more about Main Street’s polling, it would seem.

“Bidenomics is about blind faith in government spending and regulation,” Republican House Speaker Kevin McCarthy said in a statement Friday. “It’s an economic disaster where government causes decades-high inflation, high gas prices RB00, -0.32%,

lower paychecks and crippling uncertainty that leaves America worse off.”

Late on Wednesday, Tesla Inc. TSLA, -1.10%

reported that quarterly sales were up 47% from a year earlier. But the stock tumbled 10% on Thursday.

Tesla’s shares are still up 113% this year. The company is among a group of 13 in the S&P 500 that stand out with high growth expectations for sales, earnings and free cash flow through 2025.

But less than half of analysts polled by FactSet rate Tesla a buy. Emily Bary explains what they are worried about.

Chipotle Mexican Grill is among 14 stocks named by Michael Brush for consideration by investors looking to ride along with long-term improvement of U.S. labor productivity.

AP

The S&P 500 SPX, +0.03%

has returned 19% this year, following its 18% decline in 2022. On the same basis, with dividends reinvested, the benchmark index is still down 2% since the end of 2021.

The Dow Jones Industrial Average DJIA, +0.01%

is up 6% this year. The venerable index has trailed the S&P 500, but its closing level of 35,255.18 on Thursday was only 4% shy of its record close a 36,799.65 on Jan. 4, 2022. Joseph Adinolfi explains Dow Theory, which according to technical analysts is sending a strong bullish signal for the stock market.

Even if you have resisted the idea of a Roth IRA, you may soon be forced to have one

This year if you are age 50 or older and are already maxing-out your contribution to a 401(K), 403(B) or other qualified employer-sponsored tax-deferred retirement plan at $22,500, you can make an additional “catch up” tax deductible contribution of $7,500 for a total of $30,000. But starting in 2024, the catch up contribution will no longer be tax deductible if you earn at least $145,000 a year. You can still make the contribution with after-tax money into a Roth 401(K) account that your plan administrator may already have set up for you.

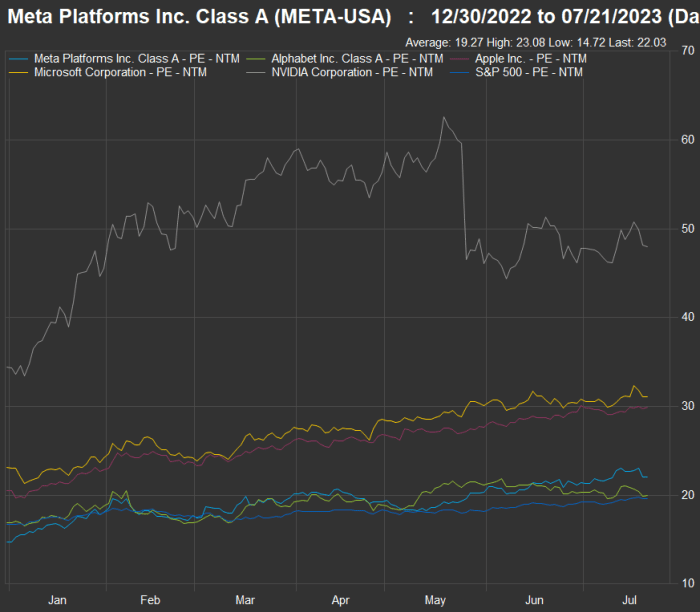

Shares of Meta Platforms Inc. and Alphabet Inc. trade only slightly higher than the S&P 500 on a forward price-to-earnings bases, while Nvidia Corp., Microsoft Corp. and Apple Inc. trade much higher.

FactSet

Leslie Albrecht looks at Meta Platforms Inc. META, -2.73%,

which is Facebook’s holding company and has a hit on its hands with the new Threads social-media platform, and Google holding company Alphabet Inc. GOOGL, +0.69%,

to consider which stock is a better buy.

In The Ratings Game column, MarketWatch reporters track analysts’ thoughts about various stocks. Here’s a sampling of this week’s coverage:

You don’t know every bad factor causing air travel to be nothing but harassment

Getting there is half the fun.

Getty Images

The U.S. flying scene — from shortages of equipment and labor (and runways) to ill-staffed air-traffic control towers — is a well-known nightmare for U.S. travelers. But there is more to the story. Jeremy Binckes looks into other factors that may surprise you and cause great inconvenience this summer.

The Federal Reserve is expected to raise interest rates again next week

The Federal Open Market Committee will meet next Tuesday and Wednesday, to be immediately followed by a policy announcement. Economists expect the central to raise the federal-funds rate by another quarter point. The question is whether or not this will end the Fed’s inflation-fighting rate cycle.

How much would you pay for 100% downside protection in the stock market?

MarketWatch illustration/iStockphoto

Over the past 30 years, the SPDR S&P 500 ETF Trust SPY,

has returned 1,650%, for an average annual return of 10%, with dividends reinvested, according to FactSet. But it hasn’t been a smooth ride. The ETF, which tracks the benchmark S&P 500, fell 18% last year and 37% during 2008, for example. And there have been even larger declines if the analysis isn’t confined to calendar years.

But can you ride through market declines? Many studies have shown that most investors who try to time the market sell after a decline has started and buy back in well after a recovery is under way, which means their long-term performance can suffer significantly.

In this week’s ETF Wrap column (and emailed newsletter), Isabel Wang describes a new buffered fund that can give you 100% downside protection over a two-year period, in return for a cap on your potential gains in the stock market. Here’s the price you would pay for the protection.

The World Cup games have started

Hannah Wilkinson scored the home team’s first goal against Norway during the first World Cup game in Auckland, New Zealand, on July 20.

Getty Images

The Women’s World Cup began Thursday with an upset victory by New Zealand over Norway.

James Rogers reports on what is expected to be a much easier environment for FIFA and corporate sponsors than that of last year’s Men’s World Cup in Qatar.

U.S. Soccer Federation President Cindy Parlow Cone participated in MarketWatch’s Best New Ideas in Money podcast and spoke about the long-term effort to achieve equal treatment for women soccer players.

More coverage of the World Cup:

Want more from MarketWatch? Sign up for this and other newsletters to get the latest news and advice on personal finance and investing.

Recent economic data indicates the U.S. isn’t in a recession, a top White House economist said Tuesday, as he cited what he called momentum to keep the country out of one.

Jared Bernstein, the chair of the Council of Economic Advisers, told a Washington Post event that indicators like employment and retail sales “are certainly not flashing anything close to recession.”

Former Vice President Mike Pence is taking a long view when it comes to inflation — a very long view that isn’t commonly expressed when debating economic performance.

Pence — well behind former President Donald Trump and Florida Gov. Ron DeSantis in early polling for the Republican nomination — is trying to position himself as the true conservative alternative in the Republican presidential race, and used inflation as a key talking point.

“We’ve got to end this scourge of inflation on families,” he said Monday. “We’re still 16% inflation in the last two and a half years and that also means another issue I’ve been willing to tackle, Larry, is we’ve got to bring common-sense and compassionate reforms to entitlements.”

The Pence campaign told MarketWatch they were comparing June 2023 with Jan. 2021 — when President Joe Biden and Vice President Kamala Harris came into office, for a 16.6% rise.

They also provided a similar comparison for inflation during the Trump/Pence administration — over those four years, prices grew by a smaller 7.7%.

But then, if that’s the new way of calculating things, there’s all sorts of data that also should be compared to 29 months ago.

To name a few: there’s been a 9% increase in jobs compared to 29 months ago, compared to the 2% drop during the Trump administration.

Average hourly earnings compared to 29 months ago have climbed 12%.

Durable-goods orders are up by 23% compared to 29 months ago, and retail sales have grown by 21%.

Comparing inflation now to 29 months ago isn’t wrong, but is misleading when the overwhelming percentage of listeners assume that comparison to be done over 12 months.

It’s an adjustment of inflation data that landed President Biden in hot water last year, when he used month-by-month data — instead of the more commonly used year-over-year data — to say that inflation was zero.

As U.S. inflation continues to cool, stocks are riding a wave of optimism.

During the past week, the S&P 500 SPX, -0.10%

climbed above 4,500 for the first time in more than 15 months, after both the consumer price index and producer price index data showed cooler-than-expected inflation in June.

Some bulls expect an improved economic outlook to send the S&P 500 to an all-time high later this year. The large-cap equities gauge hit a record close of 4,796.56 in January, 2022, according to Dow Jones market data.

In that camp stands Scott Ladner, chief investment officer at Horizon Investments. “This is increasingly looking like an economy that just can’t get knocked off its footing,” said Ladner in a phone interview.

“We see the nominal GDP coming in the 5%to 7% range this year. And earnings are priced at 0% right now. So we think there’s some room for earnings to catch up,” Ladner said.

Meanwhile, the Federal Reserve may be be close to the end of its year-long campaign to raise interest rates to slow the economy and lower inflation and steady or lower borrowing costs add more fuel to the rally, noted Ladner.

The market consensus is that the Fed will raise its interest rate at least one more time before the year concludes. Future funds traders are pricing in an over 95% chance the U.S. central bank will raise its bench mark interest rate in July by 25 basis points to the range of 5.25% to 5.5% and a 23% likelihood that it will deliver one more hike after July, according to CME Fed Watch.

“We might have already seen the peak of interest rates. That’s actually some fuel for multiples to be able to expand,” said Ladner.

Greg Bassuk, chief executive at AXS Investments, echoed the point. “While we do anticipate at least one more rate hike, we think the ending of a two-year track of rate hikes is going to put more certainty into the market and very importantly, have the U.S. economy achieve a soft landing and avoid a recession.”

Adding to the tailwind for risky assets is a weakening U.S. dollar. The ICE U.S. Dollar Index DXY, +0.03%

fell to 99.96 as of 4 pm Eastern on Friday, the lowest close since April 2022, according to Dow Jones market data.

If the Fed is close to being done with increasing its benchmark interest rate, while other central banks are not, it would weigh on the greenback even further, noted Ladner.

Dangers lurking

Still, there are several challenges that may impede stocks from extending their rally.

Raymond Bridges, portfolio manager of the Bridges Capital Tactical ETF BDGS, -0.10%,

said he expects U.S. stocks to end the year lower, citing further tightening of credit conditions.

The Fed’s balance sheet has been shrinking for the past few months, after the central bank again expanded it in March by setting up a new emergency loan program and lending more than $300 billion to provide liquidity when some regional banks failed during the first quarter of the year.

“Those bank term funding programs added a lot of liquidity into the marketplace to stave off a recession, or a credit crunch,” Bridges said. “It was a nice lifeline [for banks], but I think that’s what extended this bear market rally that we’ve had.”

As the Fed’s balance sheet declines to levels seen before March, some banks will have to pay back the emergency loans to the Fed which have a tenor of up to a year, “that’s actually a net liquidity draw,” according to Bridges.

“I see all of that occurring as well as another rate increase. We’re gonna need something to change policy-wise and some blow-out earnings to get a continuation in the [upward] trend in stocks,” Bridges said.

What’s more, if the Fed ends up delivering more interest rate hikes after July, it could significantly undermine the U.S. economy. The Fed’s dot-plot forecast in June showed that officials expected two more rate hikes by the end of the year.

Philip Colmar, managing partner and global strategist at MRB Partners, said while he doesn’t think the credit conditions are tight enough for a recession to hit this year, if the Fed “is forced to do more than another 25 basis point hike before it pauses or if yields were to move meaningfully higher, then maybe we’re getting that catalyst [for a recession] in place.”

Analysts at Capital Economics are even more bearish, saying the U.S. economy is already heading into a mild recession.

“While we do think AI is a transformative technology that will give rise to a much stronger stock market in 2024 and 2025 as investors seek to crystallise its benefits upfront, we are sticking to our forecast that the S&P 500 will drop back a bit in H2 2023 as the US economy flags in the meantime,” John Higgins, Capital Economics’ chief markets economist, wrote in a recent note.

What’s more, while many analysts expect inflation to continue head downward, there might be bumps in the road, with prices rising more than expected for certain months, noted AXS’s Bassuk.

“A lot of factors contribute to the CPI, the PPI. And all it takes is a slight change in any one of these months,” Bassuk said.

U.S. stocks ended the past week higher, with the Dow Jones Industrial Average DJIA, +0.33%

up 2.3%. The S&P 500 SPX, -0.10%

gained 2.4% and the Nasdaq Composite COMP, -0.18%

finished the week 3.3% higher.

For the coming week, investors will be expecting U.S. retail sales data on Tuesday, housing starts numbers on Wednesday, and initial jobless claims data on Thursday.

The numbers: Commercial and industrial loans — a key economic driver — held roughly steady in the week ending July 5, the Federal Reserve said Friday. Loans rose $200 million to $2.754 trillion, the central bank said.

Bank lending has been slowly decelerating, falling for three straight months. C&I loans hit a peak of $2.82 trillion in mid-March, right before the collapse of Silicon Valley Bank.

Uncredited

Key details: Total bank deposits rose by $24.9 million to $17.367 trillion in the same week. Deposits have been shrinking slowly. They peaked at $18. 21 billion in mid-April.

Big picture: In the wake of the collapse of Silicon Valley Bank in March, economists have been watching the data carefully for signs of a credit crunch, as banks have weak balance sheets as a result of the Fed’s swift increases in interest rates since March 2022.

San Francisco Fed President Mary Daly said Monday she hadn’t seen credit tightening that is in excess of normal.

“I do think, from research literature, that this takes a while to show itself, and so I think we are still looking into the fall before we would have a declarative statement to make about the extent of credit tightening and the impact on the economy,” Daly said.

Parts of the financial markets are struggling to adapt to the idea that the Federal Reserve might keep raising interest rates even after this week’s data clearly pointed to decelerating inflation.

Late Thursday, Federal Reserve Gov. Christopher Waller indicated he remains unmoved by June’s consumer price index and that he supports two more rate hikes this year even though monthly core inflation was just 0.2%, or half of what was seen in May.

By Friday morning, parts of fixed-income markets “refused to play along,” with rates on overnight index swaps pricing in “just one more hike, not two — suggesting still that the Fed’s hawks have lost some of their credibility,” said Thierry Wizman, Macquarie’s global FX and currencies strategist.

The bottom line from Waller’s speech is that it’s not solely inflation data that’s driving the Fed’s decisions, complicating the assessments made by traders and investors from here. Policy makers want to make sure that the recent deceleration in inflation feeds through broadly across goods and services sectors, and doesn’t revert back to persistently high core readings, according to the Fed governor. What’s more, “the robust strength of the labor market and the solid overall performance of the U.S. economy gives us room to tighten policy further,” he said.

Some important corners of the financial markets did respond to his remarks, namely the Treasury market. Treasury yields were broadly higher on Friday, with the policy-sensitive 2 year yield TMUBMUSD02Y, 4.733%

jumping off a one-month low, as fed funds futures traders boosted the likelihood of a post-July rate hike by November. Traders now see a 30.1% chance that the fed funds rate target will either get to 5.5%-5.75% or higher in four months — up from a current level of 5%-5.25% and after factoring in a widely expected quarter-of-a-percentage-point hike on July 26.

However, equity investors were largely focused on other things. U.S. stocks DJIA, +0.36%

COMP, -0.34%

mostly reacted to Friday’s batch of good earnings reports from major banks, as well as fresh data from the University of Michigan. Meanwhile, the U.S. Dollar Index DXY, +0.16%,

which typically reacts to changes in U.S. interest-rate expectations, was up by just 0.1% after dropping earlier in the day.

“Inflation coming down has led to market anticipation that the Fed does not have much more tightening to do,” said David Donabedian, chief investment officer of CIBC Private Wealth US, which has $94 billion in assets under management and administration. “And the big banks are looking solid with recent earnings reports. While this might be a short-term swing in sentiment, the market is not fighting the optimism and seems to be pricing in economic nirvana,”

“While we are pleased to see progress on the inflation front, we continue to have concerns about a weakening economy and lower demand that would result to a challenge for corporate earnings,” Donabedian wrote in an email. “There are some economic indicators that look good — like jobs — but these are telling us how the economy is doing yesterday and today. They don’t predict the future.”

As of Friday afternoon, stocks were headed for their fifth day of gains, helped partly by the optimism unleashed from Wednesday’s consumer price report and Thursday’s producer price data. All three major U.S. stock indexes opened higher — brushing aside Waller’s comments — and pared gains only after data from the University of Michigan showed 5-10 year inflation expectations rising this month.

Waller’s speech, delivered to the Money Marketeers of New York University, clearly articulates areas that investors may be missing in their assessments of where the Fed could go with rates, analysts said. In his mind, the impacts of policy tightening from last year “are feeding through to market interest rates faster than typically thought.” In addition, Waller said, households and firms appear to be adapting more rapidly to the dramatic, fast pace of interest-rate changes seen since March 2022.

“If one believes the bulk of the effects from last year’s tightening have passed through the economy already, then we can’t expect much more slowing of demand and inflation from that tightening,” Waller said in his prepared comments.

“To me, this means that the policy tightening we have conducted this year has been appropriate and also that more policy tightening will be needed to bring inflation back to our 2 percent target,” he said. “Pausing rate hikes now, because you are waiting for long and variable lags to arrive, may leave you standing on the platform waiting for a train that has already left the station.”

The numbers: The University of Michigan’s gauge of consumer sentiment rose to a preliminary July reading of 72.6 from a June reading of 64.4. It is the largest gain since December 2005. Sentiment is at its highest level since September 2021.

Economists polled by the Wall Street Journal had expected a June reading of 65.5.

However, Americans’ expectations for overall inflation over the next year rose to 3.4% in July from 3.3% in the prior month. Expectations for inflation over the next 5 years ticked up to 3.1% from 3% in June.

Key details: According to the UMich report, a gauge of consumers’ views on current conditions jumped to 77.5 in July from 69 in the prior month, while a barometer of their expectations rose to 69.4 from 61.5.

Big picture: Sentiment is improving as gasoline prices have held steady this summer. Low unemployment is also playing a role.

What are they saying? “The good news is that sentiment has roughly retraced half of its fall from pre-pandemic levels. For most Americans, a modest gain in income is expected. Still, durable goods buying conditions remain far off their recent levels. The rise in confidence seems restrained, and clouds concern about the forecasted economic downturn which continues to linger,” said Scott Murray, economist at Nationwide, in a note to clients.

Federal Reserve Board Gov. Christopher Waller said Thursday he was not swayed by June’s benign consumer inflation data, and said he wants the central bank to go ahead with two more 25-basis-point rate hikes this year.

“I see two more 25-basis-point hikes in the target range over the four remaining meetings this year as necessary to keep inflation moving toward our target,” Waller said in a speech to bond-market experts, known as The Money Marketeers of New York University.

That would bring the Fed’s benchmark rate to a range of 5.5%-5.75%.

Waller said that, while the cooling of CPI data for June was welcome news, “one data points does not make a trend.”

“The report warmed my heart, but I have got to think with my head,” Waller said.

He noted that inflation slowed in the summer of 2021 before rocketing higher.

In his remarks, Waller said he is now more confident that the contagion from the collapse of Silicon Valley Bank in March will not create a significant problem for the economy.

“I see no reason why the first of those two hikes should not occur at our meeting later this month,” he said.

Traders in derivative markets have priced in high odds of a rate hike after the Fed’s meeting in two weeks. But traders have been skeptical the Fed will follow through with a second hike, even before the soft CPI data.

Waller said the timing of the second hike depends on the data.

“If inflation does not continue to show progress and there are no suggestions of a significant slowdown in economic activity, then a second 25-basis-point hike should come sooner rather than later, but that decision is for the future,” he said.

During a question-and-answer session, Waller stressed that September was a “live meeting,” meaning the Fed could hike rates at that time.

Some economists had thought the Fed was moving to an “every-other-meeting” pace of hikes, but Waller said he did not favor such mechanical moves, and that data should be the deciding factor.

Some Fed officials want the central bank to hold rates steady in July, and perhaps through the end of the year, thinking the economy is going to be hit by “lagged” effects from past rate hikes.

Waller said he believes the bulk of the effects from last year’s tightening have passed through the economy already.

“Pausing rates now, because you are waiting for long and variable lags to arrive, may leave you standing on the platform waiting for a train that has already left the station,” he said.

The yield on the 10-year Treasury note TMUBMUSD10Y, 3.786%

has fallen to 3.77% this week after a lower-than-expected gain in jobs in the June report and the cooling of inflation. The yield had hit a recent high of 4.07% ahead of those softer reports.

The U.K. economy contracted in May as industrial output slid on month, a signal that rising interest rates are weighing on economic activity.

The country’s gross domestic product declined 0.1% on month in May, from a 0.2% growth in April, data from the Office for National Statistics showed Thursday.

The reading was a little better than expectations in a poll of economists by The Wall Street Journal, which expected a 0.2% fall.

The decline was driven by industrial production falling 0.6% in May, weaker than the fall of 0.2% in April, with the construction sector falling 0.2% in May, while services-sector output flatlined in the month, according to the data.

The U.K. registered no growth in GDP in the three months to May, when compared with the three months to February, with monthly GDP now estimated to be 0.2% above prepandemic levels in February 2020, the ONS said.

Markets seem to be embracing the notion of a soft landing for the U.S. economy despite inflation remaining above the Federal Reserve’s 2% target.

“Soft landings are not impossible, but they’re pretty improbable,” said Bob Elliott, co-founder, chief executive officer and chief investment officer at Unlimited Funds, in a phone interview. “They’re particularly challenging in an environment where the labor market is tight,” he said, and yet “many investors are sort of enamored with this idea that we could get a soft landing.”

The U.S. stock market was rising Wednesday after fresh data showed inflation rose in June slightly less than expected. Meanwhile, the unemployment rate remains low in the U.S., with wage growth helping to fuel consumer spending in an economy that grew at a revised 2% annualized pace in the first quarter.

“There’s a race going on between the Fed slowing the economy down, and then on the other side, inflation becoming entrenched,” said Elliott. In that race, the Fed has been “one or two steps behind,” he said, ahead of Wednesday’s inflation reading.

The consumer-price index showed U.S. inflation rose 0.2% in June for a year-over-year rate of 3%, according to a report Wednesday from the Bureau of Labor Statistics. Core CPI, which excludes energy and food prices, increased 0.2% last month for a year-over-year rate of 4.8%. The Bureau of Labor Statistics said core inflation’s rise in June marked the smallest monthly increase since August 2021.

“The Fed will see the June CPI report as progress, but they are still very likely to raise the target rate a quarter percent at their decision in July,” Bill Adams, chief economist for Comerica Bank, said in emailed comments Wednesday. “The Fed would rather overtighten and slow the economy more than necessary than under-tighten and risk inflation accelerating when the economy regains momentum.”

Many investors have been expecting the Fed to hike its benchmark interest rate by a quarter percentage point at its policy meeting later this month, which would bring it to a targeted range of 5.25% to 5.5%. Federal-funds futures on Wednesday pointed to a 92.4% probability of such a rate hike and a slightly more than 80% chance of the Fed then pausing at its next meeting in September, according to CME FedWatch Tool, at last check.

After the expected increase in July, traders in the fed-funds-futures market were on Wednesday largely expecting the Fed to hold rates steady for the rest of the year.

“The bulls get their wish – CPI print came in better than expectations,” said Rhys Williams, chief strategist at Spouting Rock Asset Management, in emailed comments Wednesday. “We think the danger now is that the Federal Reserve does one too many rate increases and the soft landing turns into something harder.”

In Elliott’s view, both the stock and bond markets lately appeared to be embracing the idea of a soft landing for the economy.

The yield on the two-year Treasury note, which recently has been trading below the Fed’s benchmark rate, tumbled after the CPI report was released Wednesday. Two-year yields TMUBMUSD02Y, 4.758%

were down about 16 basis points around midday Wednesday at 4.73%, according to FactSet data.

“As the Fed has moved interest rates to very restrictive levels thus far, and probably will execute another hike or possibly two from here, we think that patience should be a real virtue in their overall disposition toward ongoing monetary policy,” said Rick Rieder, BlackRock’s CIO of global fixed income and head of the firm’s global allocation investment team, in emailed comments Wednesday. “Today’s CPI report for June displayed notable moderation, which is good news for policy makers, markets and households overall.”

U.S. stocks were up Wednesday afternoon, with the S&P 500 SPX, +0.83%

gaining 0.7% while the Dow Jones Industrial Average DJIA, +0.39%

rose 0.4% and the Nasdaq Composite COMP, +1.15%

advanced 0.9%, according to FactSet data, at last check. The stock-market’s fear gauge, the Cboe Volatility index VIX, -7.28%,

was down more than 7% at 13.8 around midday Wednesday.

U.S. stocks opened higher Wednesday after data showed the rate of inflation in June slowed to the lowest level since early 2021, fueling hopes that the Fed may be close to being done with its interest rate hikes.

How are stocks trading

The Dow Jones Industrial Average DJIA, +0.78%

gained 281 points, or 0.8% to around 34,546

The S&P 500 SPX, +1.03%

added 40 points, or 0.9% to about 4,479

The Nasdaq Composite COMP, +1.36%

rose 158 points, or 1.1% to roughly 13,915

On Tuesday, the Dow Jones Industrial Average rose 317 points, or 0.93%, to 34261, the S&P 500 increased 30 points, or 0.67%, to 4439, and the Nasdaq Composite gained 75 points, or 0.55%, to 13761.

What’s driving markets

Stocks opened higher, while Treasury yields and the dollar were lower after data on Wednesday showed U.S. inflation at its slowest pace in more than two years.

U.S. consumer prices rose a modest 0.2% in June. Economists polled by the Wall Street Journal forecasted an increased of 0.3%. The yearly rate of inflation decelerated to 3% from 4% in the prior month, marking the lowest level since March 2021.

The so-called core rate of inflation that omits food and energy rose a mild 0.2% last month. That’s the smallest increase in almost two years. Wall Street had forecast a 0.3% gain. The annual rate of core inflation decreased to 5% from 5.3% in the prior month.

The markets have been receiving the CPI print “pretty well,” said Brian Katz, chief investment officer at the Colony Group.

The lower-than-expected CPI data is likely to “prolong the uptrend [in stocks] that we’ve been experiencing this year,” Katz in a call. “As long as we are in this environment where disinflation continues and we have reasonable growth, it is a good environment for risk assets,” Katz said.

Inflation in June fell in a majority of the important categories, most notably housing prices, which had been elevated, according to George Mateyo, chief investment officer at Key Private Bank.

“The Fed will embrace this report as validation that their policies are having the desired effect – inflation has fallen while growth has not yet stalled. But it most likely won’t change their mind to raise interest rates later this month,” Mateyo wrote in emailed comment Wednesday.

Fed fund futures traders are still pricing in an over 90% chance that the Fed will raise its benchmark interest rate by 25 basis points in its meeting later this month.

Still, some analysts are optimistic that the Fed may cease its interest rate hikes.

The inflation print in June “is enough on a standalone basis for the market to put in question the Fed’s dot projections of two additional hikes left this year and consequently pull interest rate volatility down,” according to Alexandra Wilson-Elizondo, deputy chief investment officer of multi asset solutions at Goldman Sachs Asset Management.

“Yet despite the disinflationary trends, the level of Fed funds rate has only risen to levels comparable to inflation. This contrasts with previous hiking cycles when the Fed hiked rates well above inflation. Therefore, we continue to expect that US monetary policy will stay restrictive for longer, but after this print the Fed very well may be done,” Wilson-Elizondo wrote in emailed comment.

There will also be a batch of commentary from Fed officials for the market to contend with on Wednesday. Minneapolis Fed President Kashkari will speak at 9:45 a.m.; and Atlanta Fed President Bostic will make comments at 1 p.m.. Also, the Fed Beige Book will be released at 2 p.m.. All times Eastern.

Companies in focus

Shares of ShiftPixy Inc. PIXY, -15.90%

plunged almost 22% Wednesday, after the workforce management software company’s public equity offering valued the stock at a deep discount.

Lucid Group Inc. LCID, -11.02%

shares dropped 5.5% after the company said Wednesday that it delivered 1,404 vehicles during the second quarter, while producing 2,173 vehicles at its Arizona facility.

SunPower Corp. SPWR, +7.82%

shares jumped 6.4% Wednesday after Raymond James analyst Pavel Molchanov upgraded the stock to strong buy from outperform.

The housing market may feel out of whack to home buyers coping with fast-rising home prices and 7% mortgage rates. But like it or not, the housing market is in the pink of health.

Several economic indicators that measure housing activity — from home prices to sentiment surveys — show that home builders and sellers (the few that are out there) are finding strong demand from home buyers.

News of the housing market’s relative health may be welcome to some — like real-estate agents and investors — but it’s becoming a concern for economists. The more buoyant the housing market, economists say, the more likely the U.S. Federal Reserve will unveil another interest-rate hike, which further heightens the risk of a recession.

“‘The housing market has started to recover, and this is a problem for the Fed because more demand for housing will boost home prices and rents.’”

— Torsten Slok, chief economist at Apollo

“The housing market has started to recover, and this is a problem for the Fed because more demand for housing will boost home prices and rents,” Torsten Slok, chief economist at Apollo, wrote in a note in May. And housing is a big part of how the government measures inflation, he added. This will make it more difficult to reduce inflation from 5% to the Fed’s 2% inflation target, he said.

If the Fed launches another rate hike, it would push mortgage rates, which are already in the 7% range, to go even higher.

“The housing market is in a very — if fragile — recovery,” Mike Simonsen, founder and president of real-estate analytics firm Altos Research, told MarketWatch.

“There appears to be more demand than available supply for homes, especially in the real-estate market,” he explained, which is keeping home prices high, but that doesn’t mean demand could evaporate if the current situation changes. Recall when rates doubled from pandemic-era lows in 2021 to 7% last year, which zapped home-buying momentum.

House hunters have adjusted their expectations. But if rates were to jump from 7% today to even higher levels, “I would not be at all surprised if homebuyers stopped abruptly again,” Simonsen said, stating his thesis for the fragility of the sector. Americans broadly expect rates to go over 8%, according to a March survey by the New York Federal Reserve.

MarketWatch looked at three housing-market indicators — and the picture looks rosier than ever:

Active listings are down — blame interest rates

Redfin’s deputy chief economist, Taylor Marr, said his go-to indicator was active listings.

Active listings are down this spring, compared to the previous year, according to the company’s data. At the end of June, the number of homes listed for sale on the market was down 8.1% over the prior year.

“It really captures that supply is pulling back significantly relative to demand,” Marr said.

Redfin data says that active listings of homes are down.

As a result, the housing market is seeing an excess of demand and not enough supply, which has led to a resurgence of bidding wars in some parts of the U.S.

While this metric is showing signs of the housing market returning to life and heating up amid a shortage of houses for sale, Marr said he’s not yet ready to call it a recovery. “It’s hard to declare completely the bottom of the housing market,” he said.

Still battle-scarred by the housing crash of the Great Recession, Marr said economists “might be hesitant” to say that the housing market is in recovery mode. “We still have a lot of uncertainty with the economy ahead,” he added. “If the economy really takes a turn three or four months from now for whatever reason, it could certainly bring the housing market back lower than it was even last November,” he added.

The price gap between new and existing homes

With a major shortage of resale homes, new-home sales have been taking off.

Home builders, understandably, are thrilled about the inventory shortage.

The National Association of Home Builders measures builders’ sentiment in a monthly index, and that indicator has been very cheery of late. In June, the index turned positive for the first time in nearly a year. Builders were scaling back price reductions; they were happy about current sales conditions as well as sales over the next six months, the NAHB said.

“A bottom is forming for single-family home building as builder sentiment continues to gradually rise from the beginning of the year,” said Rob Dietz, chief economist of the NAHB.

One of the major U.S. home builders, Lennar, also offered some commentary on its second-quarter earnings call last month. The company’s executive chairman, Stuart Miller, said that “the market and the economy will remain constructive for home builders as pent-up demand continues to come to market and consume affordable offerings.”

Miller also doesn’t expect the supply issue to be fixed anytime soon: “We believe that the supply constraint will continue to limit available inventory and maintain supply-demand balance,” he said on the call. “The core elements of the supply shortage will not resolve in the near term as the almost 15-year production deficit will take years to resolve.”

Home-builder confidence, as a result, is signaling high optimism about the future of the housing market, and a return to normalcy.

Builders have ramped up building new single-family and multi-family homes.

Ali Wolf, chief economist at Zonda, looks at how prices of new homes trend relative to resale homes as a key indicator of the health of the housing market. Her conclusion? Housing industry professionals involved in the construction and sale of new homes are out of a recession, given the robust demand.

In fact, demand has been so strong that new homes — generally considered to be more expensive than resales — have become more affordable in home buyers’ eyes given the competition in the existing home space.

Typically, new homes are 20% more expensive than resales, Wolf said. And today? That spread has fallen to 4%.

So what’s going on? Builders are not necessarily slashing prices. Instead, existing home prices have risen as homeowners are reluctant to sell.

That’s a good deal for buyers. New homes, Wolf said, are traditionally considered a “luxury good.” They’re brand new, and buyers can often customize them. They also require less maintenance than older homes.

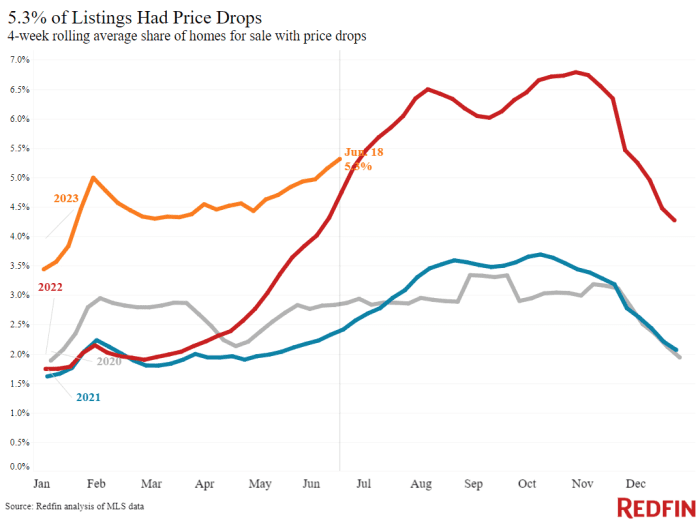

Sellers are holding out on cutting prices

Simonsen, who leads Altos Research, said price cuts were his go-to indicator to gauge the health of the real-estate market. Specifically, price cuts formed a proxy for demand, he explained.

“When the houses are on the market, if there are no buyers for the current houses that are listed, people start taking price cuts,” Simonsen said.

And to be clear, price cuts jumped last year, when rates jumped, he added.

But that dynamic has since changed, as seen in the chart below. “There are currently fewer price reductions now than in 2018 or 2019,” Simonsen said.

Data from Redfin says that homeowners aren’t cutting prices on their homes when selling, possibly due to strong interest from buyers.

And for those of you holding out for home prices to crash? Keep waiting, Simonsen said.

“There’s nothing in the data that shows prices crash,” he said. Even if a recession hits at the end of the year, which results in more job layoffs, demand for home-buying falling, and an increase in foreclosures and distress, that’s still a few years from now, he added.

“There’s no signal of home prices crashing anywhere,” Simonsen added.

If you’re a retiree and you’re trying to square the circle of rising costs, longer lifespans, more expensive medical care and turbulent markets, don’t be afraid to run the numbers on your biggest investment.

That would be your home — if you own it.

U.S. house prices are now so high that it is almost impossible for seniors not to ask themselves the obvious question: “Should we cash in, invest the money, and rent?”

Right now the average U.S. house price is nearly $360,000. That’s about a third higher than just a few years ago, before the COVID-19 pandemic. The lockdowns, the panic, the stimulus checks and 2.5% mortgage rates have all passed into history. But the sky-high prices remain — for now.

After several years of double-digit percentage increases, apartment-rent growth is falling for only the second time since the 2008 financial crisis. WSJ’s Will Parker joins host J.R. Whalen to discuss.

There is a similar story for seniors. Federal data show that the average U.S. house price is now nearly 17 times the average annual Social Security benefit — an even higher ratio than it was in August 2008, just before Lehman Brothers collapsed. At that juncture, the average house price was 15 times higher.

U.S. National Home Price Index vs. average rent of primary residence in U.S. city, according to the U.S. Bureau of Labor Statistics. Indexed: January 1987=100.

S&P/Case-Shiller

Our simple chart, above, compares average U.S. home prices with average U.S. rents, going back to 1987. (The chart simply shows the ratio, indexed to 100.) The bottom line? House prices are very high at the moment compared with rents — again, prices are about where they were in 2006-07.

And the two must run in tandem over the long term, because the economic value of owning a house is not having to pay rent to live there.

If there are times when, in general, it makes more financial sense for seniors to rent than to own, this has to be one of those.

Seniors who own their own homes may think high interest rates on new mortgages don’t affect them. They most likely either already have a mortgage at a lower, older rate or they’ve paid off their home loan. But if you want to sell, you’ll almost certainly be selling to someone who needs a mortgage.

If borrowing costs drive down real-estate prices, seniors who hold off on selling may miss out on gains they may never see again. After the last housing peak, in 2006, it took a full decade for prices to recover fully. Those who sold when the going was good had the chance to buy lifetime annuities at excellent rates or to invest in stocks and bonds that overall rose about 80% over the same period.

Incidentally, there is also an exchange-traded fund that invests in residential REITs, Armada’s Residential REIT ETF HAUS, -0.53%,

though in addition to single-family homes and apartment-complex operators, about 25% of the fund is invested in companies involved in manufactured-home parks and senior-living facilities.

For each person, the math will be different, and there are a number of questions you need to ask. Where do you want to live? How much would you get if you sold your house? How much would you pay in taxes? How much would it cost to rent the right place? Do you want to leave a property to your heirs? And what would be the costs of moving — both financial and emotional?

The conventional wisdom is that you should own your home in retirement.

“I would advise any and all retirees against renting if at all possible,” says Malcolm Ethridge, a financial planner at CIC Wealth in Rockville, Md. “You need your costs to be as fixed as possible during retirement, to match your income being fixed as well. If you choose to rent, you’re leaving it up to your landlord to determine whether and by how much your No. 1 expense will increase each year. And that makes it very tough to determine how much you are able to allocate toward everything else in your budget for the month.”

A key point here, from federal data, is that nationwide rents have risen year after year, almost without a break, at least since the early 1980s. They even rose during the global financial crisis, with just one 12-month period where they fell — and then by only 0.1%.

“My general advice for clients is that owning a home with no mortgage in retirement is the best scenario, as housing is typically the highest cost we pay monthly,” says Adam Wojtkowski, an adviser at Copper Beech Wealth Management in Mansfield, Mass. “It’s not always the case that it works out this way, but if you can enter retirement with no mortgage, it makes it a lot easier for everything to fall into place, so to speak, when it comes to retirement-income planning.”

“Renting comes with a lot of risk,” says Brian Schmehil, a planner with the Mather Group in Chicago. “If you rent, you are subject to the whims of your landlord, and a high inflationary environment could put pressure on your finances as you get older.”

But it’s not always that simple.

“With housing costs as high as they are now though, renting may be a viable solution, at least for the moment,” says Wojtkowski. “We don’t know what the housing-market trends will be going forward, but if someone is waiting for a housing-market crash before they move, they could very likely be waiting for a long time. We just don’t know.”

“Any decision comes with pros and cons,” says Schmehil. “Selling when your home values are historically high and renting allows you to capture the equity in your home, which is usually a retiree’s largest or second-largest financial asset. These extra funds allow you to spend more money on yourself in retirement without having to worry about doing a reverse mortgage or selling later in retirement, when it may be harder for you to do so.”

Renting also allows you to be more flexible about where you live, for example nearer your children or grandchildren, he adds.

And as any experienced property owner knows, renting also brings another benefit: You no longer have to do as much work around the house.

“Renting is great in that you don’t need to maintain a residence,” says Ann Covington Alsina, a financial planner running her own firm in Annapolis, Md. “If the dishwasher breaks or the roof leaks, the landlord is responsible.”

Wojtkowski agrees, noting that many people no longer want to spend time mowing the lawn or shoveling snow in retirement. “Ultimately, one of the things that I’ve seen most retirees most concerned with is eliminating the general upkeep [and] maintenance of homeownership in retirement,” he says.

Several planners — including Covington Alsina and Wojtkowski — note that one alternative to selling and renting is simply downsizing. This can free up capital, especially when home prices are high, like now, without leaving you exposed to rising rents.

Many baby boomers have been doing exactly that.

Meanwhile, I am reminded of my late friend Vincent Nobile, who — after a long and fruitful life owning homes and raising a family — found himself widowed and alone in his 80s. He rented a small cottage on a New England sound and said how glad he was that he never had to worry about maintaining the roof or the appliances, or fixing the plumbing or the heating, or any one of a thousand other irritations. Or paying property taxes — which go down even more rarely than rents.

When the regular drives to Boston got too onerous, he moved into the city and rented there. And he was glad to do it. The money he had made was all in investments — a lot less hassle both for him and his heirs.

I once asked him if he would prefer to own his own home. He shook his head and laughed.