Two years ago, Argentines elected the radical libertarian

Javier Milei as president with a mandate to fix the country’s chronically high inflation.

The odds didn’t look good. Previous presidents had failed to address one of inflation’s root causes: government deficits. Without access to capital markets, Argentina often turned to the central bank to finance its deficits by printing money. Efforts to rein in spending were stymied by resistance in Congress and by the public.

Eurozone manufacturing is showing signs of life again after industrial production jumped unexpectedly in December, further signaling that the recent slump in manufacturing in the bloc may be coming to a close.

Total production rose on 2.6% on month in December, according to figures published Wednesday by European Union statistics…

After a year of mortgage rates near 8%, home buyers are eager for good news. Some forecasters have buoyed their hopes, estimating that the rate on the 30-year mortgage will drop to 6% or lower this year.

“Homebuyers may be feeling like the lower mortgage rates they’ve been promised in 2024 are not materializing,” Lisa Sturtevant, chief economist at Bright MLS, said in a statement. In a recent survey of Americans’ feelings about the housing market, 36% of respondents said they expect mortgage rates to fall in the next 12 months.

While the Fed doesn’t set mortgage rates, it can influence them, just as it influences the overall U.S. economy through monetary policy. But even though the central bank has hit the brakes on tightening monetary policy, with the economy giving off mixed signals of strength and weakness, the timing of anticipated cuts to the benchmark rate remains unclear.

That in turn creates uncertainty about when mortgage rates will drop enough to “unfreeze” the housing market. Home buyers are probably going to have to wait until the Fed acts definitively before they see those lower rates.

The effect of a strong economy

The strength of the U.S. economy is one reason mortgage rates have not yet fallen much, economists say. The job market is still hot, and inflation remains higher than the Fed’s goal, which is why the latest read on inflation, out Feb. 13, will be so closely watched. The fact that rates haven’t fallen this year is “a result of uncertainty about the economy and the timing of the Fed’s rate cuts,” Sturtevant said.

“The strong job market is good news for the spring buying season, as higher household incomes are a necessary component, but it also means that mortgage rates are not likely to drop much further at this point,” Mike Fratantoni, chief economist at the Mortgage Bankers Association, told MarketWatch.

Another reason mortgage rates are still high is that lenders are trying to protect themselves against lower rates in the future, Cris deRitis, deputy chief economist at Moody’s Analytics, told MarketWatch. If rates fall, lenders run the risk that a borrower will pay off a loan early by refinancing. That would limit how much in interest that lender could expect to make.

“In an odd sort of way, then, the expectation that mortgage rates will be lower in the future can lead lenders to increase rates today to compensate for the prepayment risk,” deRitis said.

Lower rates, more competition among buyers

So when can prospective buyers expect mortgage rates to fall significantly?

“Homebuyers should expect mortgage rates to move lower as we head through 2024,” Sturtevant said. While Fannie Mae expects rates to fall below 6% by the end of the year, other economists, like Fratantoni, expect the 30-year rate to finish the last quarter of 2024 at 6.1%.

But even if rates do fall, that won’t necessarily mean buyers will be better able to afford a home, because a drop in rates could heat up competition for homes even as it boosts buyers’ purchasing power.

“There is still very low inventory in the market, and buyers need to act quickly when they find the right home for them,” Sturtevant said.

But it’s worth noting that since 2000, rates on 30-year mortgages have ranged from a high of about 8.62% to a low of 2.81%, averaging about 5% over that span. And compared with the historical average of the 1970s, which was 7.7%, the current rates in the 6% rage are not that high, deRitis noted.

German manufacturing orders jumped unexpectedly in December, driven by bumper aircraft purchases, although excluding larger orders they still fell, reflecting a difficult environment for the sector.

Orders were 8.9% higher than the previous month, German statistics office Destatis said Tuesday, flipping expectations that they would fall 0.5%, according to a consensus of economists polled by The Wall Street Journal.

It reverses many of the losses of previous months, including a 4% decline in October and a 11% dive in July, which were at the time seen as indicative of a manufacturing slump in Germany. On year, orders in December were 2.7% higher than the same month in 2022.

However, the intake was swayed by large-scale orders, in particular of aircraft, likely swelled by Airbus orders, according to Destatis. The airline manufacturer received 807 orders in the month.

For aircraft, ships and trains, incoming orders were more than twice as high in December as November. Metal products and electrical equipment orders also rose by double-digit percentages.

However, in the country’s key car industry, orders fell 15%, while they also dipped in mechanical engineering and in the chemical industry, according to the data. Excluding major purchases, orders fell by 2.2% on month.

Symbolizing Germany’s still-stuttering manufacturing base, orders were 5.9% lower in the whole of 2023 compared with 2022, Destatis said, amid a global slump in demand and tight financing conditions.

Banks are in wait-and-see mode about how quickly net interest margins can be rejuvenated now that Fed Chairman Jerome Powell says three rate reductions are on the table for 2024 — but that the first is unlikely to be in March as the markets had once hoped.

Bloomberg News

A resilient economy and continued strong employment gains could persuade the Federal Reserve to keepinterest rates elevated for longer — stymieing hopes for cuts this spring and keeping pressure on banks’ deposit costs and their collective ability to grow their loan portfolios.

The one-two punch of slower lending and higher funding expenses crimped many banks’ net interest margins and, by extension, fourth-quarter profits. Bankers said during earnings season in January and early this month that theyanticipated more favorable conditions in the year ahead, assuming rates at least start to come down and deposit costs follow suit. Lower rates would also decrease borrowing costs for banks’ customers, opening a door forstronger loan demand and increased income.

The $61 billion-asset Valley National in New York, for example, said its fourth-quarter NIM fell 9 basis points from the prior quarter and plunged 75 basis points from a year earlier to 2.82%.

Valley Chairman and CEO Ira Robbins said on the company’s earnings call that “it’s areally challenging” time. But, with rates poised to decline, “we do anticipate significant margin expansion as we get back to an appropriate environment.”

Last Wednesday, Fed policymakers left their benchmark rate untouched — as they have since last summer — after boosting it at the fastest pace in 40 years between March 2022 and July 2023, to a range of 5.25% and 5.5%. The Fed forced rates higher to curb inflation that soared above 9% in 2022 and reached the highest level of this century. The Fed proved largely successful: The inflation rate fell to 3.4% at the end of last year.

Still, inflation continues to hover well above the Fed’s preferred 2% rate. What’s more, the strength of the job market and continued economic growth could reignite robust consumer spending and price spikes, Fed Chair Jerome Powell cautioned at a news conference.

“We’ve made a lot of progress on inflation,” he said. “We just want to make sure that we do get the job done in a sustainable way.”

Ahead of the Fed meeting last week, futures markets showed a 50% chance of a March rate cut. That is when the Fed meets next. Powell did not rule it out, but said: “I don’t think it’s likely that the committee will reach a level of confidence by the time of the March meeting” to announce a rate reduction.

Then, on Friday of last week, the Labor Department affirmed that the employment picture continues to brighten, following robust gains over the course of 2023. It said employers added 353,000 jobs in January, the biggest gain in a year. Additionally, December’s gain was revised up to 333,000 from a prior reading of 216,000. The unemployment rate in January held steady at 3.7%, close to a four-decade low.

The economy advanced at a 3.3% annual rate in the fourth quarter, following growth in the third quarter of 4.9%, according to federal data. The January job gains keep the economy on a solid growth path, economists said.

“The January jobs report was impressively strong” and likely pushes until at least May the first Fed rate cut, said Carl Riccadonna, BNP Paribas’ chief U.S. economist.

In an interview aired Sunday night on CBS’ “60 Minutes,” Powell reiterated his press conference comments and cautioned that a March rate cut is not likely, though three reductions were still on the table for 2024.

Continued bullish employment data, and any reversal in the inflation trajectory, could further delay rate reductions. That could continue to pressure regional and community banks’ deposit expenses and, following hits to profitability in the second half of 2023, extend the bruising further into this year, analysts said.

Cooled inflation “could mean that U.S. policymakers manage to land the economy without too much turbulence — but we’re miles away from knowing that for sure,” said Sophie Lund-Yates, lead equity analyst at Hargreaves Lansdown. “For now, it seems likely the economy has a touch too much wind in its sails for the Federal Reserve to change course.”

That leaves banks in wait-and-see mode.

First Foundation in Dallas, which has facedrecent investor criticism about its early handling of the rising rate environment, is a case in point. It cut 15% of its staff in 2023 to offset the strain of stubbornly high rates. The $13.3 billion-asset bank’s margin pain endured through the fourth quarter.

Its NIM shriveled to 1.36% from 1.66% the prior quarter and 2.45% a year earlier.

For First Foundation, “there’s probably, I would say, upward towards $3 billion of liabilities that would reprice immediately if the Fed were to cut rates, which would be a substantial savings and, frankly, ignite earnings back to where they once were,” President and CEO Scott Kavanaugh said on the bank’s earnings call.

While the bank expects improvement this year should the Fed’s target rate hold steady, Kavanaugh added, “obviously, it won’t be at the same pace as if the Fed were to start cutting.”

Even if the Fed does lower rates multiple times this year, as many banks anticipate, NIM expansion is likely to prove a long, gradual process.

Sandy Spring Bancorp Chairman and CEO Daniel Schrider said during the company’s earnings call that he anticipates three rate cuts in the second half of this year and more in 2025. Should those expectations prove correct, he said the bank’s margin could recover to 2022 levels late in 2025.

The $14 billion-asset bank in Olney, Maryland, said its NIM of 2.45% for the fourth quarter compared to 2.55% for the previous quarter and 3.26% for the final quarter of 2022.

Should the Fed push rates lower, “we expect the margin to bottom out in the first quarter” and “then to rebound in the second quarter and throughout the remainder of the year, by 7 to 10 basis points per quarter. We would also expect the Fed to continue rate cuts throughout 2025, which would allow the margin to move above 3% during the second half of next year.”

Small businesses in sectors like software and manufacturing are panicking over the expiration of a critical tax deduction that they say could lead to mass layoffs and business closures, unless Congress acts quickly to amend the law.

“This is a life-and-death scenario for small software companies,” Michelle Hansen, co-founder of the geocoding company Geocodio, told MarketWatch.

The tax change that Hansen and other software executives are taking issue with was signed into law by President Trump in 2017, as part of a larger tax overhaul that slashed the top corporate tax rate from 35% to 21%.

But in order to satisfy Senate budget rules and pass the law with only Republican votes, the bill could not increase the budget deficit over a 10-year window.

So lawmakers included a provision that, beginning in 2022, drastically reduced how much research-and-development spending a business could deduct from their annual revenue to determine taxable income.

The change penalizes certain industries like software and information technology — where engineer salaries are often classified as R&D expenses — as well as manufacturing and pharmaceuticals IHE.

IntervalZero CEO Jeff Hibbard, whose Massachusetts-based company designs and sells software for installation on precision machines like semiconductor manufacturers, told MarketWatch that he has had to tap into company savings for the past several years in order to avoid laying off engineers.

He said that his firm brings in about $9 million in revenue annually with expenses of $8 million — but 60% of those expenses come in the form of engineer salaries, which can only be deducted from taxable income over a five-year period because the IRS treats it as R&D.

He said that after taxes consumed all his profits in 2022, he had to pay an additional $800,000 to Uncle Sam, and an additional $600,000 for the 2023 tax year.

“We’ve had to do a hiring freeze and postpone projects” in a cutthroat industry where technology progresses rapidly, Hibbard said. “We’ve been in existence for 15 years. For the first 14, we always hired additional people. Now we have a hiring and salary freeze.”

The House of Representatives voted last week 357-70 to restore full expensing for R&D as part of a $79 billion tax package that boosted the child tax credit and extended other business tax breaks.

The bill now heads to the Senate, which already has its hands full debating immigration and national-security issues, and analysts say election-year politics could thwart its passage in 2024.

Henrietta Treyz, director of economic-policy research at Veda Partners, gave just a 10% chance of the bill passing the Senate in a recent note to clients.

“This year’s effort to pass a tax package has been more robust than the effort we saw in 2022 and 2023,” she wrote. Treyz added, however, that “the competing need to pass border reform and Ukraine/Israel aid, and general dysfunction in Washington keep us pessimistic that we’ll see a bipartisan economic-stimulus package come out of Congress this year.”

On top of Republicans not wanting to give President Joe Biden a victory that would provide tax relief for businesses and families, Senate Republicans could decide to drag their feet on the bill in the hope that they’ll retake the chamber next year and can play a bigger role in the process, according to Owen Tedford, policy analyst at Beacon Policy Advisors.

“The critical member to watch is Senator Mike Crapo [of Idaho], the top Republican on the Senate Finance Committee,” Tedford wrote. “Crapo has not outright opposed the bill but has raised policy concerns and has expressed a desire to have a chance to amend it.”

Political considerations may be dictating the bill’s fate in Washington — but some business owners fear they don’t have the wherewithal to wait until next year for the problem to be fixed.

Benjamin Bengfort, co-founder and CEO of Iowa-based software firm Rotational Labs, told MarketWatch that he had to lay off workers last year after his 2022 tax bill rose by 438%.

He noted that even demand for his products has taken a hit because of the change in the law, because his services can count as an R&D expense for his customers, too.

“So it is [between] a rock and a hard place for us, no matter how you look at it,” Bengfort said. “This is an existential threat for software engineering companies.”

While the U.S. stock market has been pricing in a “soft-landing” scenario for the economy, a blowout January jobs report, relatively strong corporate earnings, and Federal Reserve Jerome Powell’s comments during the past week could point to the possibility of “no landing,” where the economy is resilient while inflation stays on target.

Such a scenario could still be positive for U.S. stocks, as long as inflation remains steady, according to Richard Flax, chief investment officer at Moneyfarm. However, if inflation reaccelerates, the Fed may be hesitant to cut its policy interest rate much, which could spell trouble, Flax said in a call.

What the past week tells us

Investors have just gone through the busiest week so far this year for economic data and corporate earnings reports, with stocks ending at or near their record highs.

The Dow Jones Industrial Average DJIA

finished the week with its nineth record close of 2024, according to Dow Jones Market Data. The S&P 500 index SPX

scored its seventh record close this year on Friday, while the Nasdaq Composite COMP

is about 2.7% lower from its peak.

The Fed kept its policy interest rate unchanged in the range of 5.25% to 5.5% at its Wednesday meeting, as expected. However, in the subsequent press conference, Fed Chair Jerome Powell threw cold water on market expectations that the central bank may start cutting its key interest rate in March, and underscored that they want “greater confidence” in disinflation.

Roger Ferguson, former Fed vice chairman, said Powell introduced “a new kind of risk, the risk of no landing.”

In that scenario, inflation will stop falling, while the economy is strong, Ferguson said in an interview with CNBC on Thursday. However, Ferguson said he doesn’t think it is the likely outcome.

Traders were pricing in a 20.5% likelihood on Friday that the Fed will cut its interest rates in its March meeting, according to the CME FedWatch tool and that’s down from over 46% chance a week ago. The likelihood that the Fed will kick off its rate cutting program in May stood at 58.6% on Friday.

The stronger-than-expected January jobs data released on Friday further eliminates the chance of a rate cut in March, said Flax.

The U.S. economy added a whopping 353,000 new jobs in January while economists polled by The Wall Street Journal had forecast a 185,000 increase in new jobs. Hourly wages rose a sharp 0.6% in January, the biggest increase in almost two years.

The past week has also been heavy with earnings reports, as several tech giants including Microsoft MSFT, +1.84%,

Apple AAPL, -0.54%,

Meta META, +20.32%,

and Amazon AMZN, +7.87%

reported their financial results for the fourth quarter of 2023.

Among the 220 S&P 500 companies that have reported their earnings so far, 68% have beaten estimates, with their earnings exceeding the expectation by a median of 7%, analysts at Fundstrat wrote in a Friday note.

While the reported earnings by big tech companies have been “okay,” the guidance was not, said José Torres, senior economist at Interactive Brokers.

What has been driving the tech stocks’ rally since last year was mostly the prospect of sales from artificial intelligence products, but tech companies are not able to monetize the trend yet, Torres said in a phone interview.

Adding to the headwinds is a comeback of concerns around regional banks.

On Thursday, New York Community Bancorp Inc.’s stock triggered the steepest drop in regional-bank stocks since the collapse of Silicon Valley Bank in March 2023. New York Community Bancorp on Wednesday posted a surprise loss and signaled challenges in the commercial real estate sector with troubled loans.

Meanwhile, the Fed’s bank term funding program, which was launched in March last year to bolster the capacity of the banking system, will expire on March 11.

If the Fed could start cutting its key interest rate in March, it would be “sort of like the ambulance that was going to pick regional banks up and save them,” said Torres. “Now the ambulance is coming in May at the earliest, I think that we’re in a particularly risky period from now to May,” Torres said.

What should investors do

Investors should go risk-off before May, according to Torres. “Last year, goods and commodities helped a lot on the disinflationary front. This year for disinflation to continue, we’re going to need services to start contributing to that. Then we’re going to need to see an increase in the unemployment rate,” Torres said.

He said he prefers U.S. Treasurys with a tenor of four years or shorter, as the long-dated ones may be susceptible to risks around the fiscal deficit and government borrowing. For stocks, he prefers the healthcare, utilities, consumer staples and energy sectors, he said.

Keith Buchanan, senior portfolio manager at Globalt Investments, is more optimistic. The slowdown in inflation and the relatively strong economic data and earnings “don’t really paint a picture for a risk-off scenario,” he said. “The setup for risk assets still leans towards the bullish expectation,” Buchanan added.

In the week ahead, investors will be watching the ISM services sector data on Monday, the U.S. trade deficit on Wednesday and weekly initial jobless benefit claims numbers on Thursday. Several Fed officials will speak as well, potentially providing more clues on the possible trajectory of rate cuts.

As the U.S. Federal Reserve’s three-year reign in the headlines potentially comes to an end, an analysis of this year’s market themes can offer valuable insights for predicting trends and ensuring attractive returns in 2024.

Beyond the central bank’s actions, pivotal factors shaping the investment landscape this year include fiscal policies, election outcomes, interest rates and earnings prospects.

Throughout 2023, a prominent theme emerged: that equities are influenced by factors beyond monetary policy. That trend is likely to persist.

A decline in interest rates could significantly increase the relative valuations of equities while simultaneously reducing interest expenses, potentially transforming market dynamics. Contrary to consensus estimates, 2023 brought a more robust earnings rebound, leaving analysts optimistic about 2024.

The 2024 U.S. presidential election, meanwhile, introduces a new element of uncertainty with the potential to cast a shadow over the market during much of the coming year.

Choppy trading, modest earnings growth

Anticipating a choppy first half of the year due to sluggish economic growth, we see a better opportunity for cyclicals and small-cap stocks to rebound in the latter part of the year. As uncertainty around the election and recession fears dissipate, a broad rally that includes previously ignored cyclicals and small-caps should help propel the S&P 500 SPX

higher.

Broader macroeconomic conditions support mid-single-digit growth in earnings per share throughout 2024. Factors such as moderate economic expansion, controlled inflation and stable interest rates are expected to provide a conducive environment for companies, enabling them to sustain and potentially improve their earnings performance. We estimate EPS growth of 6.5%. This projected growth aligns with the broader market sentiment indicating a steady upward trajectory in earnings for the upcoming year, fostering investor confidence and supporting valuation expectations across various sectors.

“ If the economy has not been in recession at the time of the first rate cut but enters one within a year, the Dow enters a bear market.”

When it comes to U.S. stock-market performance around rate cuts, the phase of the economic cycle matters. When there has been no recession, lower rates have juiced the markets, with the Dow Jones Industrial Average DJIA

rallying by an average of 23.8% one year later.

If the economy has not been in recession at the time of the first cut but enters one within a year, the Dow has entered a bear market every time, declining by an average of 4.9% one year later. Our base case is a soft landing, but history shows how critical avoiding recession is for the bull market as the Fed prepares to ease policy.

Big on small-caps

This past year has posed a hurdle for small-cap stocks due to the absence of a driving force. These stocks typically perform better as the economy emerges from a recession. While they are currently undervalued, their earnings growth has been notably lacking. If concerns about a recession diminish, a normal yield curve could serve as a potential catalyst for small-cap stocks.

Growth vs. value

The ongoing outperformance of megacap growth stocks that we saw in 2023 might hinge on their ability to sustain superior earnings growth, validating their current valuations. Defensive sectors in the value category, meanwhile, are notably oversold and might exhibit strong performance, particularly toward the latter part of the first quarter. Should concerns about a recession dissipate, cyclical sectors within the value category could outperform, particularly if broader market conditions turn favorable in the latter half of the year.

Handling uncertainty

The Fed’s enduring influence regarding the prospect of a soft landing in 2024 remains a pivotal point in the market’s focus. Considering the themes of the past year and the multifaceted influences on equities beyond monetary policy, investors are advised to navigate through uncertainties stemming from unintended fiscal shifts, upcoming elections and the impact of fluctuating interest rates. While a potentially choppy start to the year is anticipated, it could create opportunities for cyclical and small-cap stocks later in the year.

Ed Clissold is chief of U.S. strategies at Ned Davis Research.

Mark Zuckerberg delighted Meta shareholders and Wall Street this week with news of the social media giant’s first-ever dividend.

The IRS may also be happy, now that it’s staring at millions in taxes on the Meta stock dividends bound for Zuckerberg’s portfolio.

Zuckerberg, the CEO of Meta Platforms Inc. META, +20.32%,

is poised to make $700 million in dividends yearly. He owns nearly 350 million shares, according to FactSet, and the company will start paying a quarterly dividend of 50 cents a share.

That would yield nearly $167 million in federal taxes yearly, after a qualified-dividend tax of 20% and another 3.8% tax on the investment returns of rich households, two accounting experts said.

California income taxes of 13.3% on the dividends could cost Zuckerberg another $93.1 million, said Andrew Belnap, an accounting professor at the University of Texas at Austin’s McCombs School of Business.

All in, that’s a combined $259.7 million in federal and state taxes annually on the Meta dividends, Belnap estimated.

For context, U.S. taxpayers reported over $285 billion in qualified-dividend income to the IRS though mid-November 2023, according to agency statistics. Nearly 30 million tax returns reported qualified dividends through that time.

Meta said it plans a quarterly cash dividend going forward, with the first such payment in March.

Meta shares soared 20.5% on Friday, ending with a record-high close of $474.99. The Dow Jones Industrial Average DJIA,

S&P 500 SPX

and Nasdaq Composite COMP

all closed higher Friday.

‘Zuck is getting a major break’

Meta announced the dividend payment in its earnings results Thursday, on the same week that Americans began filing their income taxes.

A look at Zuckerberg’s dividends and their tax implications offer a peek at the debate about the varying ways wages and wealth are taxed.

“Zuck is getting a major break,” said Andrew Schmidt, an accounting professor at North Carolina State University’s Poole School of Management who also crunched the numbers for MarketWatch.

Approximately $167 million “seems like a high tax bill,” he said. But if Zuckerberg received the $700 million as a straight salary, Schmidt estimated he’d be looking at a roughly $259 million tax bill on the wages after they were taxed at the top marginal rate of 37%.

For federal and state taxes on the Meta dividends, Zuckerberg would face a combined rate of 37.1%, Belnap noted. “His tax rate on this is actually fairly high,” he said.

The gap in tax rates on income derived from wages and investments “has been a big criticism with U.S. tax policy,” Schmidt said, especially as lawmakers look for ways to come up with more tax revenue.

Regular retail investors enjoy the same preferential rates on capital gains and dividends as the top 1% of taxpayers, Schmidt added. The issue is that those dividends and stock profits are a smaller part of their income while salaries, taxed at higher rates, are a bigger proportion.

Belnap noted that California’s state tax rules don’t provide special treatment to dividends.

Zuckerberg received a $1 base salary in 2022, a figure that hasn’t changed in several years. He is now worth $142 billion, according to the Bloomberg Billionaires Index, making him the fifth-richest person in the world.

Meta did not immediately respond to a request for comment.

Taxes on the Meta dividends will not be something Zuckerberg, or any Meta shareholders big or small, need to deal with until next year’s tax season, Belnap and Schmidt observed.

But as taxpayers amass their 1099-DIV forms on dividend income, IRS figures show that it’s mostly upper-echelon taxpayers reaping the rewards on the preferential rates for qualified dividends.

Households worth at least $1 million accounted for 40% of the approximate $285.3 billion in qualified dividends reported through mid-November, according to agency figures.

For less affluent investors, “it’s usually a nice supplement, but I’d say very few people are living off dividends,” Belnap said.

Former President Donald Trump on Friday criticized Federal Reserve Chair Jerome Powell and said he’s playing politics with interest-rate policy.

“It looks to me like he’s trying to lower interest rates for the sake of maybe getting people elected,” Trump said, in an interview on the Fox Business Network.

“I think he’s political,” added Trump, the likely 2024 Republican nominee for president.

Asked if he would reappoint Powell to a third four-year term, Trump replied “no.”

Trump said he has a couple of choices in mind to replace Powell, but wouldn’t say who.

Trump said he thinks lowering interest rates would lead to massive inflation. The conflict in the Middle East is likely to lead to “big inflation” from a spike in oil prices, he added.

“Trump said he thinks lowering interest rates would lead to massive inflation. The conflict in the Middle East is likely to lead to “big inflation” from a spike in oil prices, he added.”

Powell “is not going to be able to do anything,” Trump said.

On Wednesday, Powell said he wasn’t giving a potential third term any thought. Powell’s current term expires in early 2026.

Speculation on a third term “is not something I’m focused on,” Powell said.

“We’re focused on doing our jobs. This year is going to be a highly consequential year for the Fed and monetary policy. We’re, all of us, very buckled down, focused on doing our jobs,” Powell said.

Analysts say that the Fed will be criticized by both parties in the election year.

On Sunday, Powell will appear on the CBS News program “60 Minutes” and will likely face more questions about the election.

Earlier this week, top Democrats on the Senate Banking Committee urged the Fed to cut rates quickly, saying they were too high and hurting the housing market.

“Keeping interest rates high will be detrimental to American workers and their families and do little to bring down prices or promote moderate economic growth,” said Sen. Sherrod Brown, a Democrat from Ohio, and the chairman of the Banking Committee, in a letter to Powell prior to Wednesday’s Fed meeting.

At the meeting on Wednesday, the Fed kept its benchmark interest rate unchanged in a range of 5.25%-5.5%.

Asked about the letter from the Democrats on Wednesday, Powell said Congress has given the Fed the job of stable prices. High inflation hurts people at the lower end of the income spectrum, he added.

“It’s what society has asked us to do is to get inflation down. The tools we use to do it are interest rates,” he said.

The Fed has penciled in three rate cuts for 2024. Powell said that a cut at the Fed’s next meeting in March was unlikely. He said the Fed wants to see more good inflation reports so it can have greater confidence that inflation is coming down to the 2% target.

The Biden administration’s announcement Friday that it’s pausing liquefied natural gas export approvals sparked political backlash, drew cheers from climate activists and stoked uncertainty in energy markets, but is unlikely to see the U.S. give up its title as the world’s top LNG exporter.

The U.S. will delay its decisions on new LNG exports to non-free trade agreement countries, allowing time for the Energy Department to update the underlying analyses for LNG export authorizations, the White House said.

Those analyses are roughly five years old and “no longer adequately account for considerations” such as potential cost increases for American consumers and manufacturers or the “latest assessment of the impact of greenhouse gas emissions,” it said.

The Biden administration likely “realizes the role of LNG in foreign policy, but at the same time it needs to show the Democrat base that it is doing something for climate change,” said Anas Alhajji, an independent energy expert and managing partner at Energy Outlook Advisors, pointing out that the announcement comes during a presidential election year.

“Delaying one project or stopping it may not be a big deal, but it is a problem if it becomes a trend,” he said in emailed commentary.

Environmental groups, which have pushed for action, cheered the decision.

The 12 impacted projects in the U.S. “would spew out as much climate-warming pollution as 223 coal plants per year, and they present explosion risks to the communities where they’re located and emit other health-harming chemicals,” the Sierra Club, an environmental group, said in a statement welcoming the decision.

Top exporter

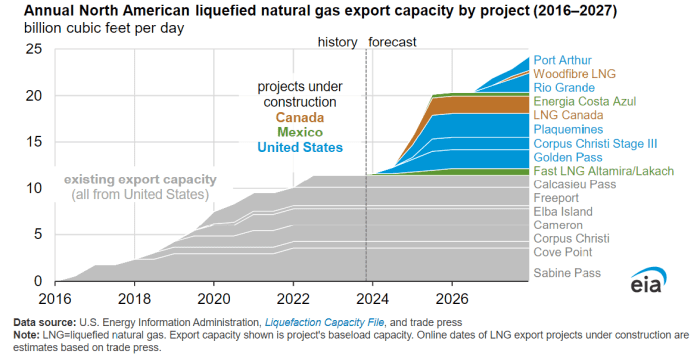

The announcement is particularly important for a nation that became the world’s biggest LNG exporter in the span of less than a decade.

The U.S. became the world’s largest LNG exporter during the first half of 2022 on the back of increases in LNG export capacity, international natural gas and LNG prices, and global demand, particularly in Europe, according to the Energy Information Administration.

The country’s exports of LNG climbed to a fresh record in November 2023, with the EIA reporting domestic exports of 386.2 billion cubic feet, up from 384.4 bcf a month earlier. Exports in December 2016 were at just 41.8 bcf.

U.S. LNG exports soared after 2016.

EIA

With 90% of U.S. LNG going to non-free trade agreement destinations, withholding licensing effectively “halts project development,” John Miller, managing director, ESG and sustainability policy at TD Cowen wrote in a Friday note.

Equities

LNG equities with operating facilities likely won’t benefit from the administration’s announcement, at least not immediately, until the impacts of this pause in export approvals to non-FTA countries becomes more clear, Jason Gabelman, director, sustainability & energy transition at TD Cowen said.

U.S. companies with government approvals that have not been sanctioned, “could have a higher probability of moving forward this year, albeit modestly” as offtakers may be hesitant to sign up to new U.S. projects with LNG development getting “politicized,” he said. Among those, he pointed out approvals for proposed liquefaction units at NextDecade Corp.’s NEXT, +2.30%

Rio Grande LNG export facility project in Brownsville, Texas.

At the same time, it would not be a surprise if U.S. LNG companies pursuing growth that do not yet have non-FTA approval see downside pressure, said Gabelman.

LNG projects take around 4 years to build and any delays to project sanctions today will take “multiple years to manifest in the market,” he said.

Still, the U.S. announcement “introduces the risk of more stringent oversight that could limit new U.S. capacity” more than four years out, Gabelman said.

Companies that supply equipment to LNG liquefaction projects include Baker Hughes Co. BKR, +0.59%

and Chart Industries Inc. GTLS, -7.54%,

said Marc Bianchi, a senior energy analyst at TD Cowen.

Any slowing of approval would create “overhand on order growth,” he said.

Climate change

The White House said Friday that its decision will not impact the ability of the U.S. to continue supplying LNG to its allies in the near term but also acknowledged environmental concerns.

“I think we’ve got to be clear eyed about the challenges that we face. The climate crisis is an existential crisis, and we’ve got to be, I think, really forward leaning into making sure that we’re taking that head on,” said Ali Zaidi, the White House national climate adviser, told reporters Friday.

He added that given the number of approvals already completed, the number of projects under construction are set to double existing capacity with approvals beyond that set to double capacity yet again.

“So there’s a long runway here, and we’re taking a step back and thinking, OK, let’s take a hard look before that runway continues to build out,” he said.

Rob Thummel, senior portfolio manager at Tortoise, argued that U.S. LNG exports actually reduce global carbon emissions as natural gas typically “displaces coal to generate electricity in countries such as China and India.”

They also improve global energy security as U.S. natural gas is becoming Europe’s primary energy supplier, replacing Russia, he said.

In a statement Friday, Sen. Joe Manchin, a West Virginia Democrat and chairman of the U.S. Senate Energy and Natural Resources Committee, said that if the Biden administration has facts to prove that additional LNG export capacity would hurt Americans, it needs to make that information public. But if the pause is “another political ploy to pander to keep-it-in-the-ground climate activists,” he said he would “do everything in my power to end this pause immediately.

Manchin plans to hold a hearing on the decision in the coming weeks.

Market impact

The U.S. decision to delay new LNG export permits is unlikely to have an impact on domestic natural-gas supplies or prices, said Energy Outlook Advisors’ Alhajji.

LNG prices and the rate at which new LNG export terminals can be constructed help determine LNG export volumes, the EIA said, and higher LNG exports can result in upward pressure on U.S. natural-gas prices, while lower U.S. LNG exports can pressure prices.

On Friday, natural gas for February delivery NG00, +0.23%

NGG24, +0.26%

settled at $2.71 per million British thermal units, up 7.7% for the week.

Meanwhile, the U.S. is likely to keep its position as the world’s top LNG exporter, according to Tortoise’s Thummel.

The U.S. is the currently the largest LNG exporter at almost 12 bcf per day, with Qatar coming in second, he said.

Qatar is expanding its LNG export capacity and is expected to have the ability to export almost 20 bcf per day by 2028, he said. The EIA reported recently that Qatar has averaged 10.3 bcf per day in exports during the last 10 years.

That would mark sizable growth. But the EIA reported in November that LNG export capacity from North America is likely to more than double from around 11.4 bcf per day to 24.3 bcf per day by the end of 2027.

The EIA said North America’s LNG export capacity is likely to more than double by 2027.

EIA

Given expected growth in U.S. LNG export capacity, the U.S. is likely to “remain the largest exporter of LNG in the world” despite the U.S. announcement, said Thummel.

The notion that the Federal Reserve will soon slow, or perhaps even end, its program of quantitative tightening is increasingly being talked about on Wall Street like a foregone conclusion.

But while investors wait to hear more on the subject from Fed Chair Jerome Powell during next week’s post-meeting press conference, they could be forgiven for asking themselves some questions.

What might an imminent taper of the Fed’s balance-sheet runoff look like? Why has it suddenly become so urgent? What might it mean for the six or so interest-rate cuts investors are expecting from the Fed this year, as well as for markets more broadly?

We aim to answer these questions below.

What inspired talk of tapering QT?

It wasn’t until the minutes from the Federal Reserve’s December policy meeting were published earlier this month that investors started to take the notion of the Fed declaring “mission accomplished” on QT seriously.

The minutes revealed that a number of senior Fed officials felt it was nearly time to “begin to discuss” the technical factors that would govern the Fed’s decision to slow the runoff of maturing bonds from its balance sheet.

Shortly after the minutes’ release, several senior Fed officials came forward to discuss the importance of ending the balance-sheet runoff. Dallas Fed President Lorie Logan, the first senior Fed official to expand on what was noted in the minutes, said earlier this month that the Fed should start to slow the pace of its balance-sheet shrinkage once assets locked up in the Fed’s reverse-repo facility fell below a certain level.

According to Logan, senior Fed officials had been unsettled by the drain of $2 trillion in assets from the RRP facility last year.

But there was another issue that was also likely bothering monetary policymakers heading into the Fed’s December meeting.

Sudden spikes in overnight repo rates late last year drew uncomfortable comparisons to the repo-market crisis of September 2019, which foreshadowed the end of the Fed’s previous attempt at tapering its balance sheet, according to TS Lombard’s Steve Blitz.

What is the Fed’s ‘lowest comfortable level of reserves’?

A re-run of the repo-market crisis of 2019 is what the Fed is presumably trying to avoid. Economists are so concerned the central bank might accidentally bump up against the lower bound for reserves in the banking system, that they have come up with a name for the concept: They’re calling it the “lowest comfortable level of reserves.”

According to this idea, strain in overnight-financing markets should emerge once reserves in the banking system retreat below a certain threshold. This would, in turn, likely force the central bank to scale back or even reverse quantitative tightening immediately, according to several economists.

In order to avoid such a risk, Jefferies economist Thomas Simons said in a note to clients earlier this month that he expects the Fed will announce plans to start tapering QT after its March meeting.

Across Wall Street, most economists expect the Fed will begin by tapering the pace at which Treasurys are redeemed from its balance sheet — perhaps cutting it in half to start, from $60 billion a month to $30 billion a month. Reducing the pace at which mortgage-backed securities are running off won’t matter as much until prepayments begin to climb.

Going even further, economists at Evercore ISI said in a report shared with MarketWatch earlier this week that they expect the tapering to begin around the middle of 2024 and continue potentially through 2025, until the Fed has succeeded in reducing the size of its balance sheet to about $7 trillion.

The balance sheet presently stands at $7.7 trillion, according to data published by the Fed. It peaked at nearly $9 trillion in April 2022.

However, one key issue may complicate the Fed’s efforts to ascertain the “LCLoR.” According to Jefferies’ Simons, the amount of banking-system reserves counted as liabilities on the Fed’s balance sheet has been more or less steady since the Fed started its latest round of balance-sheet tapering. It stood at roughly $3.3 trillion recently, according to Fed data cited by Jefferies.

Why stop at $7 trillion if bank reserves haven’t been all that heavily impacted by QT anyway? It’s probably worth noting that, whatever happens, nobody on Wall Street expects the Fed would attempt to shrink the size of its balance sheet back toward pre-crisis levels, when the amount of bonds on its balance sheet was miniscule compared to today.

Why? Because there is simply too much debt sloshing around the global financial system to justify such a withdrawal of support, according to Steven Ricchiuto, chief economist at Mizuho Americas.

“The Fed is not in a position to remove all that extra liquidity because now the system needs it just to function,” Ricchiuto said.

What does this mean for markets?

Because quantitative tightening is a hawkish policy stance, its rolling back should be bullish for stocks and bonds. But there are other considerations that could impact the outcome, market strategists said.

Not only would a reduction in the pace of the Fed’s monthly runoff introduce a fresh dovish tilt to the Fed’s monetary policy, but by reducing the amount of bonds it allows to roll off its balance sheet every month, the Fed would become more active in the Treasury market, said James St. Aubin, chief investment officer at Sierra Investment Management, during an interview.

There are also a few contextual factors that could impact how the equity market reacts. For example, as St. Aubin pointed out, context is equally as important as the nature of the decision itself. Should the Fed decide to end QT abruptly because the U.S. economy is sliding into a recession, then the decision could hurt stocks.

Another issue, raised by a different market strategist, is the notion that the Fed could decide to start tapering QT in lieu of cutting interest rates — or at least in lieu of cutting them as quickly as investors expect. This could buy the central bank more time to press its battle against inflation while mitigating the risks that it could hurt the economy by keeping policy uncomfortably tight for too long, economists said.

Ben Jeffery, U.S. interest-rate strategist at BMO, said in a recent note to clients that, based on Logan’s comments from earlier this month, he would lean toward this being the most likely scenario. Additionally, he said, tapering QT could potentially impact the Treasury’s refunding announcement due in May.

Jeffery calculated that the Fed tapering QT by $20 billion beginning in April would save the Treasury from issuing nearly $250 billion in bonds compared to if the Fed had continued with its balance-sheet runoff apace.

This should lead to lower Treasury yields, all else being equal. And lower long-dated Treasury yields are typically seen as beneficial for stocks, according to Callie Cox, a U.S. equity strategist at eToro.

Although, once again, the outcome for markets would likely depend on the specific context.

“Higher yields probably aren’t a good thing for stock investors these days, but in particular environments, higher yields and less Fed intervention could hint that the economy is healing,” Cox said.

Retail sales fell more sharply than expected in the U.K. in December, offering little succor to a listless economy at the end of the year.

Total trade volumes were 3.2% lower than a month earlier, according to figures published Friday by the Office for National Statistics.

This was worse than the slight dip expected, according to a Wall Street Journal poll of economists. It reverses rising sales in November, boosted by Black Friday promotions as well as lower inflation. Retailers reported that many shoppers stocked up on Christmas food and gifts in November, weighing on December’s spending.

For the quarter as a whole, retail sales were 0.9% lower than the previous three months, and will have a negative contribution to wider economic growth over the period, the ONS said.

Write to Joshua Kirby at joshua.kirby@wsj.com; @joshualeokirby

TOKYO (AP) — Asian shares slid Wednesday after a decline overnight on Wall Street and disappointing China growth data, while Tokyo’s main benchmark momentarily hit another 30-year high.

Japan’s benchmark Nikkei 225 NIY00, -0.95%

reached a session high of 36,239.22, but reverted lower, last down 0.3% to 35,477. The Nikkei has been hitting new 34-year highs, or the best since February 1990 during the so-called financial bubble. Buying focused on semiconductor-related shares, and a cheap yen helped boost exporter issues.

Hong Kong’s Hang Seng HK:HSCI

tumbled 4% to 15,220.72, with losses building after data showed China hitting its economic growth target of 5.2% for 2023, surpassing government expectations, but short of the 5.3% some analysts expected. The Shanghai Composite CN:SHCOMP

shed 2% to 2,833.62.

Australia’s S&P/ASX 200 AU:ASX10000

slipped 0.2% to 7,401.30. South Korea’s Kospi KR:180721

dropped 2.4% to 2,435.90.

Investors were keeping their eyes on upcoming earnings reports, as well as potential moves by the world’s central banks, to gauge their next moves. Wall Street slipped in a lackluster return to trading following a three-day holiday weekend.

The S&P 500 SPX

fell 17.85 points, or 0.4%, to 4,765.98. The Dow Jones Industrial Average DJIA

dropped 231.86, or 0.6%, to 37,361.12, and the Nasdaq COMP

sank 28.41, or 0.2%, to 14,944.35.

Spirit Airlines SAVE, -47.09%

lost 47.1% after a U.S. judge blocked its takeover by JetBlue Airways JBLU, +4.91%

on concerns it would mean higher airfares for flyers. JetBlue rose 4.9%.

Stocks of banks were mixed, meanwhile, as earnings reporting season ramps up for the final three months of 2023. Morgan Stanley MS, -4.16%

sank 4.2% after it said a legal matter and a special assessment knocked $535 million off its pretax earnings, while Goldman Sachs GS, +0.71%

edged 0.7% higher after reporting results that topped Wall Street’s forecasts.

Companies across the S&P 500 are likely to report meager growth in profits for the fourth quarter from a year earlier, if any, if Wall Street analysts’ forecasts are to be believed. Earnings have been under pressure for more than a year because of rising costs amid high inflation.

But optimism is higher for 2024, where analysts are forecasting a strong 11.8% growth in earnings per share for S&P 500 companies, according to FactSet. That, plus expectations for several cuts to interest rates by the Federal Reserve this year, have helped the S&P 500 rally to 10 winning weeks in the last 11. The index remains within 0.6% of its all-time high set two years ago.

Treasury yields BX:TMUBMUSD10Y

have already sunk on expectations for upcoming cuts to interest rates, which traders believe could begin as early as March. It’s a sharp turnaround from the past couple years, when the Federal Reserve was hiking rates drastically in hopes of getting high inflation under control.

Easier rates and yields relax the pressure on the economy and financial system, while also boosting prices for investments. And for the past six months, interest rates have been the main force moving the stock market, according to Michael Wilson, strategist at Morgan Stanley.

He sees that dynamic continuing in the near term, with the “bond market still in charge.”

For now, traders are penciling in many more cuts to rates through 2024 than the Fed itself has indicated. That raises the potential for big market swings around each speech by a Fed official or economic report.

On Wall Street, Boeing fell to one of the market’s sharper losses as worries continue about troubles for its 737 Max 9 aircraft following the recent in-flight blowout of an Alaska Air ALK, -2.13%

jet. Boeing BA, -7.89%

lost 7.9%.

In energy trading, benchmark U.S. crude CL00, -1.55%

lost 90 cents to $71.75 a barrel. Brent crude BRN00, -1.37%,

the international standard, fell 78 cents to $77.68 a barrel.

In currency trading, the U.S. dollar USDJPY, +0.44%

rose to 147.90 Japanese yen from 147.09 yen. The euro EURUSD, -0.10%

cost $1.0868, down from $1.0880.

Industrial output in the eurozone contracted for the third month in a row November, reflecting the continued downturn in the sector.

Total production fell 0.3% on month in November, according to figures published Monday by European Union statistics agency Eurostat, after a 0.7% decline recorded in October. It matched expectations of economists polled by The Wall Street Journal.

Durable consumer goods led the decline, with output falling 2.0%. Production of intermediate goods declined 0.6% while for capital goods it tumbled 0.8%. Energy production, however, recorded a rise in output of 0.9%.

However, there has been evidence that recent struggles in the industrial sector in the eurozone could be bottoming out. A key survey of purchasing manufacturers said sentiment rose in December in the manufacturing industry.

Among larger eurozone nations, output dipped on month by 0.3% in Germany and 1.5% in Italy, but expanded by 0.5% in France and 1.1% in Spain.

U.S. stock indexes were edging higher on Wednesday with technology stocks looking to extend gains ahead of the December inflation report, which is expected to shed more direct light on when the Federal Reserve could dial back its two-year-long effort to tighten monetary policy and cool the economy.

The Dow Jones Industrial Average DJIA

was up 38 points, or 0.1%, to 37,562

The Nasdaq Composite COMP

gained 43 points, or 0.3%, to 14,901.

On Tuesday, the Dow industrials fell 0.4%, to 37,525, while the S&P 500 declined 0.2%, to 4,757, and the Nasdaq Composite gained less than 0.1%, to 14,858.

What’s driving markets

Inflation and its impact on bond markets and the Federal Reserve’s monetary-policy trajectory are the primary focus for markets this week as investors remain on hold ahead of Thursday’s December inflation reading and high-profile corporate earnings reports on Friday, when some of the big banks will kick off the fourth-quarter 2023 earnings season.

The S&P 500 sits less than 0.7% shy of its record high of 4796.6 touched a little over two years ago, after rallying strongly in the last few months primarily on hopes that easing inflation will allow the Fed to lower interest rates sooner and faster than the markets previously anticipated.

The yield on the 10-year Treasury BX:TMUBMUSD10Y,

the benchmark for borrowing costs, has fallen from 5% in October to 4.014% on Wednesday.

But for this bullish narrative to play out, inflation must be seen continuing to fall back to the central bank’s 2% target. That’s why great importance is therefore being placed on the consumer-price index for December, which will be published at 8:30 a.m. Eastern on Thursday.

Economists forecast that annual headline CPI inflation inched up to 3.2% last month from 3.1% in November. The core reading, which strips out more volatile items like food and energy, is expected to fall from 4% to 3.8%.

Adam Phillips, director of portfolio strategy at EP Wealth Advisors, said the CPI report may give investors enough confidence that the disinflation is likely to continue, even if the price levels are “still a very long way from anything that is considered healthy.”

However, he cautioned that the economy has “certain factors” that are beyond the Fed’s control, such as the volatility in supply chains and growing geopolitical risks, as well as a potential resurgence in inflation, he told MarketWatch via phone on Wednesday.

“[E]quities have remained broadly range-bound since just before Christmas, with little to push them in either direction,” said Jim Reid, strategist at Deutsche Bank.

“That might change soon, since we’ve got the U.S. CPI print tomorrow, and then the start of earnings season on Friday, but for now at least, there’s been few headlines for investors to latch onto, just a bit of indigestion after over exuberance before New Year left markets with a little bit of an extended hangover,” Reid added.

In U.S. economic data, the wholesale inventories declined 0.2% in November, in line with Wall Street expectations, as manufacturers continue to juggle with a fragile economy, according to the Commerce Department.

New York Fed President John Williams will speak in White Plains, N.Y., at 3:15 p.m. Eastern time.

Companies in focus

Shares of Boeing Co. BA, +1.53%

edged up 1.5% on Wednesday after chief executive David Calhoun on Tuesday told employees the jet maker needed to acknowledge its mistakes after a panel blew off a 737 Max 9 jet flown by Alaska Airlines days earlier, and approach the matter with “complete transparency.” Shares have fallen nearly 8% this week.

The former bond king doesn’t like the fixed-income security that’s the lynchpin of the financial world.

Bill Gross, the retired fund manager and co-founder of Pacific Investment Management, took to the social-media service X to say that the 10-year Treasury BX:TMUBMUSD10Y

is “overvalued” with a yield of 4%. Yields move in the opposite direction to prices.

Through Monday, the yield on the 10-year Treasury has fallen 99 basis points from its late October peak.

He said the 10-year Treasury inflation-protected yield at 1.80% is the better choice. “If you need to buy bonds. I don’t,” said Gross.

Gross also continued to talk of his idea to go long 2-year bonds BX:TMUBMUSD02Y

while shorting the 10-year. “Stick with the return to a positive 10 year/2 year yield curve. Earns carry while you wait,” he said. In previous posts, he talked of making such trades via Treasury futures contracts.

Gross said he was taking a bow for his recommendation of regional bank stocks six months ago and mortgage REITs in December. The SPDR S&P Regional Banking ETF KRE

has climbed 49% from its May 4 low, and the iShares Mortgage Real Estate ETF REM

has gained 21% from its late October low. Gross in November highlighted Annaly Capital Management NLY, +2.62%

and AGNC Investment Corp. AGNC, +3.75%

as mortgage REITs he likes for 2024.

Gross said he still likes Capri Holdings CPRI, -0.39%

as a merger arbitrage target. Tapestry TPR, +2.04%

in August agreed to buy Capri for $57 per share, and on Monday, Capri closed at $50.49.

Stock investors have gotten off to a wobbly start to the new year, hobbled by shifting expectations on the timing and extent of Federal Reserve interest-rate cuts in 2024.

All three major U.S. stock indexes snapped a nine-week winning streak on Friday, after unexpectedly strong December job gains prompted traders to briefly pull back on the chances of a March rate cut. The S&P 500 SPX

and Nasdaq Composite COMP

also failed to stage a Santa Claus Rally from the five final trading days of 2023 through the first two sessions of 2024, as questions grew about the market’s multiple rate-cuts view.

It all adds up to a glimpse of what might be in store for investors in the year ahead. Already, the so-called “January effect,” or theory that stocks tend to rise by more now than any other month, could be put to the test by headwinds that include stalling progress on inflation. Inflation’s downward trend in recent months had given traders and investors hope that as many as six or seven quarter-percentage-point rate cuts from the Federal Reserve could be delivered in 2024, starting in March.

Over the first handful of days in the new year, however, reality has started to sink in. For one thing, multiple rate cuts tend to be more commonly associated with recessions and not soft landings for the economy.

Moreover, the idea that the Fed could follow through with as many rate cuts as envisioned by traders would significantly increase the probability that policymakers lose their battle against inflation, according to Mike Sanders, head of fixed income at Wisconsin-based Madison Investments, which manages $23 billion in assets. That’s because six or more rate cuts would loosen financial conditions by too much, and boost the risk of another bout of inflation that forces officials to hike again, he said.

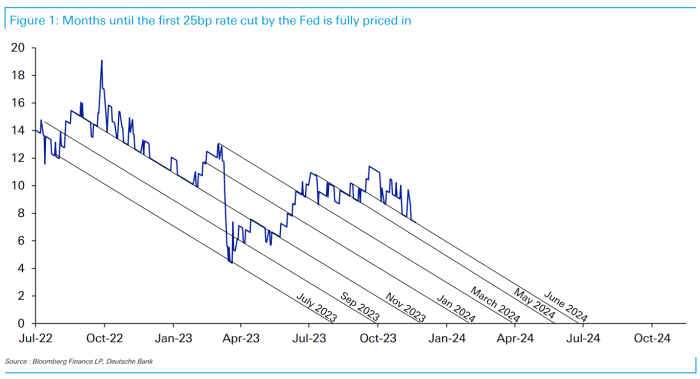

Minutes of the Fed’s Dec. 12-13 meeting show that policymakers were uncertain about their forecasts for rate cuts this year and failed to rule out the possibility of further rate hikes. Nonetheless, fed funds futures traders continued to cling to expectations for a big decline in borrowing costs, with the greatest likelihood now coalescing around five or six quarter-point rate cuts that total 125 or 150 basis points of easing by year-end. That’s roughly twice as much as what policymakers penciled in last month, when they voted to keep interest rates at a 22-year high of 5.25% to 5.5%.

Source: CME FedWatch Tool, as of Jan. 5.

Uncertainty over the path of U.S. interest rates could leave investors flat-footed once again, and damp the optimism that sent all three major stock indexes in 2023 to their best annual performances of the prior two to three years. In November, analysts at Deutsche Bank AG DB, +0.81%

counted seven times since 2021 in which markets expected the Fed to make a dovish pivot, only to be wrong.

Sources: Bloomberg, Deutsche Bank. Chart is as of Nov. 20, 2023.

Financial markets have been operating with “sky-high expectations” for 2024 rate cuts, but the only way to substantiate six cuts this year is with an “abrupt and sharp downturn in the economy,” said Todd Thompson, managing director and portfolio co-manager at Reams Asset Management in Indianapolis, which oversees $27 billion.

Heading into 2024, euphoria over the prospect of lower borrowing costs produced what Thompson calls “an alarming, everything rally,” which he says leaves equities and high-yield corporate debt vulnerable to pullbacks between now and the next six months. Beyond that period, however, “the trend is likely to be lower rates as the economy finally succumbs to tightening conditions at the same time inflation continues to recede.”

The coming week brings the next major U.S. inflation update, with December’s consumer price index report released on Thursday. The annual headline rate of inflation from CPI has slowed to 3.1% in November from a peak of 9.1% in June 2022. In addition, the core rate from the Fed’s favorite inflation gauge, known as the PCE, has eased to 3.2% year-on-year in November from a 4.2% annual rate in July.

The Fed needs to keep interest rates higher because of all the uncertainty around inflation’s most likely path forward, and the U.S. labor market “won’t degrade fast enough in the first quarter to justify a first rate cut in March,” according to Sanders of Madison Investments.

Rate-cut expectations are “going to be the issue for 2024, and a lot of it is going to be revolving around inflation getting back to that 2% target,” Sanders said via phone. “We think somewhere between 75 and 125 basis points of rate cuts make sense, and that the first move is more of a June-type of event. We don’t think it makes sense to have a March rate cut unless the labor market falls off a cliff.”

History shows that Treasury yields tend to fall in the months leading up to the first rate cut of a Fed easing cycle. However, that isn’t happening right now. Yields on government debt have been on an upward trend since the end of December, with 2- BX:TMUBMUSD02Y,

10- BX:TMUBMUSD10Y,

and 30-year yields BX:TMUBMUSD30Y

ending Friday at their highest levels in more than two to three weeks.

While financial markets generally tend to be efficient processors of information, they “haven’t been very accurate in terms of pricing in rate cuts” this time, said Lawrence Gillum, the Charlotte, North Carolina-based chief fixed-income strategist for broker-dealer for LPL Financial. He said the big risk for 2024 is if financial conditions ease too much and the Fed declares victory on inflation too soon, which could reignite price pressures in a manner reminiscent of the 1970s period under former Fed Chairman Arthur Burns.

“We think rate-cut expectations have gone too far too fast, and that the backup in yields we are seeing right now is the market acknowledging that maybe rate cuts are not going to be as aggressive as what was priced in,” Gillum said via phone.

December’s CPI report on Thursday is the data highlight of the week ahead.

On Monday, consumer-credit data for November is set to be released, followed the next day by trade-deficit figures for the same month.

Wednesday brings the wholesale-inventories report for November and remarks by New York Fed President John Williams.

Initial weekly jobless claims are released on Thursday. On Friday, the producer price index for December comes out.