Editor’s Note: Sign up to get this weekly column as a newsletter. We’re looking back at the strongest, smartest opinion takes of the week from CNN and other outlets.

CNN

—

“Can you tell me where we’re headin’?” Bob Dylan asks in his 1978 song “Señor.”

Is it “Lincoln County Road or Armageddon? Seems like I been down this way before. Is there any truth in that, señor?”

Yes, we’ve been here before, at least if you take President Joe Biden at his word. At a fundraiser in New York City Thursday, Biden said, “First time since the Cuban missile crisis, we have a direct threat of the use (of a) nuclear weapon if in fact things continue down the path they are going.” Referring to Russian President Vladimir Putin’s threat to go nuclear in his war with Ukraine, the President observed, “I don’t think there’s any such thing as the ability to easily (use) a tactical nuclear weapon and not end up with Armageddon.”

As historian Julian Zelizer wrote, “Those were unsettling words for a nation to hear from the commander in chief.” Biden referred to “the Cuban missile crisis in October 1962, when the world seemed to teeter on the brink of nuclear war as the US and the Soviet Union faced off over missiles in Cuba.”

“Some planned escape routes from major cities while others stocked up on transistor radios, bottled water and radiation kits for their families. Although nobody knew it at the time, the danger was even greater than most thought as the leaders didn’t have full control of the situation. In the end, diplomacy won out, a deal was reached and disaster was averted.”

Nick Anderson/Tribune Content Agency

But the prospect of annihilating humanity in a nuclear exchange is so great that such brinksmanship should never be allowed to happen again. Surely Presidents Ronald Reagan and Mikhail Gorbachev were right when they agreed in 1985 that “a nuclear war cannot be won and must never be fought.”

US national security officials privately said there was no new intelligence to indicate that Putin is moving to carry out his threat and couldn’t explain why Biden made the extraordinary statement. But its implications were clear, Zelizer argued. “This historic moment in the war between Russia and Ukraine is an important reminder that the US has let nuclear arms control fall from the agenda, and the consequences are dangerous.”

Putin’s back is against the wall as Ukraine continues to retake territory from the Russians. Peter Bergen wrote that Putin is “facing growing criticism from Russians on both the left and the right, who are taking considerable risks given the draconian penalties they can face for speaking out against his ‘special military operation’ in Ukraine.”

“With even his allies expressing concern, and hundreds of thousands of citizens fleeing partial mobilization, an increasingly isolated Putin has once again taken to making rambling speeches offering his distorted view of history.”

One lesson of history is that military defeat endangers dictatorial leaders. “Putin’s gamble may lead to a third dissolution of the Russian empire, which happened first in 1917 as the First World War wound down, and again in 1991 after the fall of the Soviet Union,” Bergen noted. “It could unfold once more as Putin’s dream of seizing Ukraine seems to be coming to an inglorious end.”

It’s striking to recall, as Frida Ghitis did, that “seven months ago, some viewed Putin as something of a genius. That myth has turned to dust. The man who helped suppress uprisings, entered wars and tried to manipulate elections across the planet now looks cornered.”

In Ukraine, “Russia’s trajectory looks like a trail of war crimes, with hundreds of bombed hospitals, schools, civilian convoys, and mass graves filled with Ukrainians. And still Ukraine is pushing ahead, is doing very well in fact, and very possibly winning this war,” wrote Ghitis.

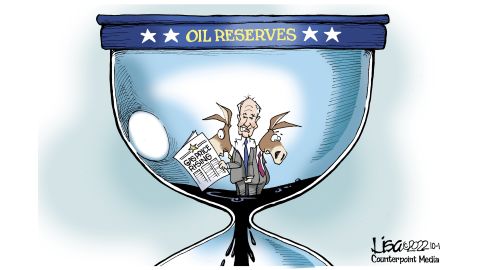

Biden took heat this summer for deciding to meet Saudi Crown Prince Mohammed bin Salman and walking away with little commitment from the Saudis to expand oil production. And then last week, the Saudi regime was instrumental in OPEC+’s decision to actually cut oil production in a move that benefits it and other oil-producing states including Russia.

“So much for cozying up to the Saudis – President Joe Biden’s much-hyped fist bump with Mohammed bin Salman during a trip to the Middle East back in July has turned into something of a slap across the face from the crown prince,” wrote David A. Andelman.

In the US, gasoline prices have started rising after weeks of declines, adding to the burdens Democrats face in trying to hold onto control of Congress in the midterm elections a month from now.

“The OPEC production cutbacks could – indeed, should – backfire for Saudi Arabia and its complicit partners,” wrote Andelman. “There is growing sentiment in Congress to reevaluate America’s wider relationship with Saudi Arabia and especially the vast arms sales to the kingdom.”

Higher oil prices come on top of Europe’s emerging energy crisis, with Russia sharply reducing its export of natural gas to the continent. As a result, Germany is among the nations that have instituted tough new curbs on energy use, wrote Paul Hockenos.

“Step into my Berlin office today and you’ll find everybody is wearing sweaters – I wear two, with wool socks and occasionally a scarf. … At home, my little family has sworn off baths (swift showers please), and lights are on only in the rooms we’re occupying. We’ve invested in a wool curtain inside our apartment’s front door to keep out the draft.”

“My friend Bill … hasn’t turned his heating on yet this year – no one I know has – and wears a sweater at home. He also has a new method of showering: one minute under warm water, turns it off, lathers up, and then rinses off.”

“Timing is everything,” said Garrett Hedlund in the 2011 song of that name.

“When the stars line up

And you catch a break

People think you’re lucky

But you know it’s grace…”

It works in reverse too. Just ask Linda Stewart, a New Mexico educator in her 60s who decided to retire one year into the pandemic lockdown. “Finances would be a little tight for a while, but some outside projects would supplement my income, so I felt confident I would be able to handle it,” she wrote in a new CNN Opinion series, “America’s Future Starts Now,” which explores the key issues in the midterm campaigns.

But, Stewart added, “by the end of the second year of lockdown, inflation started taking a toll and money was getting uncomfortably tight. Soon I was in the red each month, just trying to keep up. The usual suspects were groceries and gas, which meant cutting back on some of the more expensive food items and cooking meals at home.”

“I stopped driving for anything other than essentials. And with the continuing drought here in the Southwest, utility bills went through the ceiling. I cut back on watering my garden and turned the furnace down a few degrees in the winter and the air conditioning up a few in the summer. I switched to washing clothes mostly in cold water and only running the dishwasher once a week.”

The economy is the issue Americans are most concerned about, and there are no quick, easy solutions to the inflation spike. The second part of CNN Opinion’s new series was a roundup of views on how to help people cope with higher costs.

Scott Stantis/Tribune Content Agency

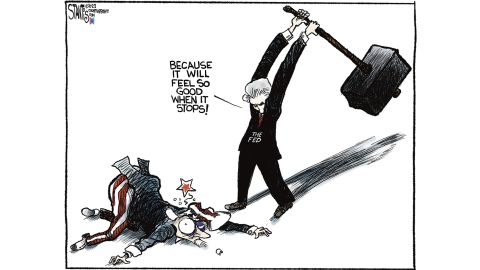

The Federal Reserve Bank is raising interest rates at a rapid pace to conquer inflation. The “tight labor market – and the rapid wage growth it has spurred – is causing inflation to become more entrenched,” wrote economist Gad Levanon for CNN Business Perspectives. To curb the rise in prices, “the Federal Reserve is likely to drive the economy into a recession in 2023, crushing continued job growth.”

Dana Summers/Tribune Content Agency

At least 131 people have died due to Hurricane Ian. Why was it so deadly?

The storm’s course veered south as it approached Florida and rapidly intensified, Cara Cuite and Rebecca Morss noted. “Emergency managers typically need at least 48 hours to successfully evacuate areas of southwest Florida. However, voluntary evacuation orders for Lee County were issued less than 48 hours prior to landfall, and for some areas were made mandatory just 24 hours before the storm came ashore. This was less than the amount of time outlined in Lee County’s own emergency management plan.”

“While the lack of sufficient time to evacuate was cited by some as a reason why they stayed behind, there are other factors that may also have suppressed evacuations in some of the hardest hit areas.” Few people are aware of their evacuation zone, and some websites carrying that information crashed in the leadup to the storm’s arrival, Cuite and Morss wrote.

“People need time to decide what to do, pack belongings, find a place to go and arrange how to get there, often in the midst of heavy traffic and other complications and obstacles.” Other factors: “In addition to a false sense of security from prior near-misses among some residents, others who were in the areas of Florida hardest hit by Hurricane Ian may not have had any personal experience with such powerful storms. This is likely true for the millions of people who have moved to Florida over the past few decades…”

For more:

Adam H. Sobel: Where the hurricane risk is growing

Geoff Duncan, a Republican and the current lieutenant governor of Georgia, is unsure about Herschel Walker’s prospects in the upcoming election. The Republican Senate candidate has denied reports alleging he paid for a girlfriend’s abortion in 2009.

“The October surprise,” Duncan wrote, “has upended the political landscape, throwing one of the nation’s closest midterm races into turmoil five weeks before Election Day, but it never had to be this way. Just as there should not be two Democrats representing a center-right state like Georgia in the US Senate, the Republican Party should not have found its chance of regaining a Senate majority hanging on an untested and unproven first-time candidate.”

“Walker won his Senate primary not because of his political chops or policy proposals. He trounced his opponents because of his performance on the football field 40 years ago and his friendship with former President Donald Trump – neither of which are guaranteed tickets to victory anymore.”

Drew Sheneman/Tribune Content Agency

For more on politics:

SE Cupp: Herschel Walker’s ‘October Surprise’ won’t matter

Tim Kane: What the Biden administration is getting wrong on immigration

Nicole Hemmer: The Onion is right about the future of democracy

Dean Obeidallah: The single-minded goal of Trump-loving Republicans

Organic chemistry is a famously difficult course and a traditional prerequisite for students who want to go on to medical school. Maitland Jones Jr., a master of the field and textbook author, taught the course at NYU – until 82 of the 350 students taking it “signed a petition because, they said, their low scores demonstrated that his class was too hard,” Jill Filipovic noted.

Then the university fired him.

An NYU spokesman “told the (New York) Times in defense of their decision to terminate Jones’s contract that the professor had been the target of complaints about ‘dismissiveness, unresponsiveness, condescension and opacity about grading.’ It’s worth noting that according to the Times, students expressed surprise that Jones was fired, which their petition did not call for.”

Some of the student complaints may have been valid, noted Filipovic, but she added that the case “raises important questions, chief among them how much power students, who universities seem to increasingly think of as consumers (and some of whom think of themselves that way), should have in the hiring, retention and firing of professors…”

“There are real consequences … to making higher education primarily palatable to those paying tuition bills – particularly when it comes to courses like organic chemistry, which are intended to be difficult. Future medical students do in fact need a rigorous science background in order to be successful doctors someday. Whether or not Jones was an effective teacher for aspiring medical students is up for debate, but in firing him, NYU is effectively dodging questions about the line between academic rigor and student well-being with potentially life-and-death matters at stake.”

Alessandro Garofalo/Reuters

The Securities and Exchange Commission fined Kim Kardashian nearly $1.3 million for failing to disclose she was paid to promote a crypto asset, EthereumMax, noted Emily Parker.

“This case reflects a much larger problem in the crypto industry: Celebrities are using their influence to promote cryptocurrencies, a notoriously complex and risky asset class, which can lead people to invest in coins or projects that they may not understand,” Parker observed.

“New coins and projects are constantly popping up, sometimes without sufficient warnings about the risks of investing … In such a fast-changing and confusing market, how do you distinguish winners from losers? It’s easy to imagine how a confident tweet by a celebrity could have a significant impact on a new investor.”

In agreeing to the fine, Kardashian “did a favor for the cryptocurrency industry. Such a high-profile example could cause other celebrities to think twice before shilling a token on social media.”

Bill Bramhall/Tribune Content Agency

Alejandro Mayorkas: The security risk Congress needs to take seriously

Danae Wolfe: Stomping alone won’t wipe out the spotted lanternfly

Victoire Ingabire Umuhoza: Inside the prison where sunlight ceases to exist

Jeremi Suri and William Inboden: A generation of the world’s best leaders has died

Sara Stewart: ‘Dahmer’ debate is finally saying the quiet part about true crime out loud

Elisa Massimino: It’s time to shut down Guantanamo

Pete Brown: What ‘fancy a pint?’ really means

AND…

Rich Fury/Getty Images/FILE`

Until recently, the late-night television formula ruled, as Bill Carter noted. “On the air after 11 p.m. with a charismatic host, some comedy, a desk, a guest or two, maybe a band and then ‘Good night, everybody!’” Late-night shows seemed to be holding their own despite the rise of cord-cutting and the move to streaming.

But that’s changing, as Trevor Noah’s decision to give up hosting “The Daily Show” suggested. Carter wrote, “What many people watch now is not television: It’s whatever-vision, entertainment by any means on any device. What’s on late night is now often seen on subscriptions – and not late at night.”

Noah is leaving on a high note “after a seven-year run, marked by an impressive body of comedy work and growing acclaim,” Carter observed. In succeeding Jon Stewart as the show’s host, Noah “had a different beat in his head from the start. He wanted to refashion the show with a wider comedy vision, one looking more out at the world, instead of purely in at the United States, all informed by Noah’s South African-born global perspective.”

“It was a wise choice. Following Stewart was always going to be a potentially crippling challenge. Noah took it on and remade the show to his own specifications. One major sign of that was how strikingly diverse the show became.”