Central bankers like to focus on core inflation readings, which strip out food and energy prices, but that doesn’t mean that they, or investors, will be able to ignore a renewed surge in crude-oil prices.

In a Thursday note, DataTrek Research observed that the correlation between energy prices and the core reading of the consumer-price index has returned to levels seen in the 1970s and 1980s. It stands at 0.62 since 2020, compared with an average of 0.68 in those prior decades, and well above its long-run average of 0.31. A reading of 1.0 would mean the measures were moving in perfect lockstep. (See table below.)

DataTrek Research

Core measures of inflation typically strip out volatile items like food and energy. While that often leads to eye-rolling by commentators who note that food and energy make up a big chunk of what consumers spend money on, the logic behind the move holds that such items are less responsive to monetary policy.

Policy makers put more emphasis on the core reading for a better read on what they can influence. The core personal-consumption expenditures, or PCE, index, for example, is often described as the Federal Reserve’s favored inflation indicator.

But that doesn’t mean rising energy or food prices can be ignored. Energy, after all, is an input, and can have an influence on overall prices.

“Recent data says energy prices hold more sway on core inflation than any time since the 1970s/1980s, so rising oil prices are a legitimate concern for both the Fed and capital markets. Food inflation fits the same bill,” said DataTrek co-founder Nicholas Colas in the note.

Oil prices have been on a tear this summer, with the rally accelerating after Saudi Arabia announced earlier this week it would extend a production cut of 1 million barrels a day through the end of the year, with Russia also pledging to extend a supply cut.

West Texas Intermediate crude CL00, +0.48%,

the U.S. benchmark, extended a winning streak to nine days on Wednesday, while Brent crude BRN00, +0.60%,

the global benchmark, rose for a seventh straight day. Both grades ended at 2023 highs Wednesday before pulling back modestly in the Thursday session.

The surge in crude threatens to further drive up fuel prices, including gasoline and diesel.

And rising oil prices this week got a chunk of the blame from investors and analysts for a pickup in Treasury yields as market participants began to pencil in a longer stretch of higher interest rates — or weighed the possibility the Fed may need to deliver more monetary tightening. That’s also contributed to a rise in the U.S. dollar, with the ICE U.S. Dollar Index DXY,

a measure of the currency against a basket of six major rivals, hitting a six-month high.

U.S. stocks have weakened in the face of rising yields, with technology and growth shares, which are particularly rate-sensitive, leading the way lower. The Nasdaq Composite COMP

was on track for a 2% decline so far this holiday-shortened week, while the S&P 500 SPX

has pulled back 1.4% and the Dow Jones Industrial Average DJIA

has lost 1%.

“With oil prices rising again, we got to wondering about the spillover effects of this move on inflation. Will pricier crude derail recent disinflationary trends?” Colas wrote.

Another big corporate borrowing blitz to kick off September has gotten under way, but this one isn’t looking like the rest.

Instead, the flurry of new bond issues shows how the Federal Reserve’s higher interest rate environment has begun to seep in a year later, by making major companies far more hesitant to tap credit for longer stretches.

A McDonald’s restaurant near Times Square, NYC on July 29th, 2023.

Adam Jeffery | CNBC

This report is from today’s CNBC Daily Open, our new, international markets newsletter. CNBC Daily Open brings investors up to speed on everything they need to know, no matter where they are. Like what you see? You can subscribe here.

Stocks sold off U.S. stocks experienced a sell-off and all major indexes closed in the red. Meanwhile, U.S. Treasury yields rose for the second consecutive day. Asia-Pacific markets followed Wall Street lower Thursday. Australia’s S&P/ASX 200 fell 1.29%, leading losses in the region, as trade data for the country came in worse than expected. Japan’s Nikkei 225 slipped 0.64% after eight straight days of gains.

China’s trade isn’t picking up China’s trade activity fell again in August, though not as badly as feared. In U.S. dollar terms, exports fell by 8.8% from a year ago, compared with the 9.2% forecast. Imports dropped 7.3%, less than the 9% decline expected. However, that means imports have fallen every month this year, while exports have dropped monthly since April.

An Apple-Arm agreement Apple has signed an agreement with Arm that “extends beyond 2040,” Arm said in a U.S. Securities and Exchange Commission filing. This suggests Apple has secured access to the Arm architecture, an instruction set that outlines how a chip’s central processor works, for the foreseeable future. That can only boost the excitement around Arm’s upcoming IPO that values it as high as $52 billion.

Inside the Magic Kingdom’s chaos What did a private bathroom, Oogie Boogie and a hippo have to do with the behind-the-scenes chaos between Bob Iger and Bob Chapek at Disney? CNBC’s Alex Sherman spoke with more than 25 people who worked closely with Iger and Chapek between 2020 and 2022, uncovering the inside story of a CEO succession plan gone awry.

[PRO] Taking bites out ofApple China reportedly banned government officials from using Apple’s iPhone and other foreign-branded devices for work. The European Commission also designated Apple as a “gatekeeper” under its new act. Apple shares fell 3.6% yesterday — could the company face even more headwinds ahead? Listen to what the pros are saying about those developments.

And today we found out the services and manufacturing sectors of the U.S. economy have been paying higher prices for inputs in August, according to the prices component of the ISM Services index and its manufacturing counterpart. Moreover, the report showed the services sector growing at a faster-than-expected clip for its eighth consecutive month of expansion and its highest reading since February.

For recession worriers, that sounds like good news. But markets have turned their focus from recession to stubborn inflation and the threat of higher interest rates.

Markets are “seemingly adopting a ‘bad news is good news’ view, rallying on weak growth data, and selling off on strong data — amid fears that too strong data will increase the risk of an additional rate hike,” Goldman Sachs’ Chris Hussey wrote in a Wednesday note.

Indeed, as Treasury yields jumped — the 2-year yield breached the 5% level once again — and bets of a rate hike in November increased, stocks were pressured. Rate-sensitive technology stocks were especially affected, with Nvidia and Apple losing more than 3% each. (Apple’s shares were also affected by a Wall Street Journal report that Chinese government agencies have banned staff from using iPhones at work.)

A roaring blaze is dangerous. But more often than not, it’s the embers smoldering in the underbush that cause the most damage — and ignite a wildfire again.

U.S. stocks finished lower Wednesday, with shares of technology companies dropping sharply, as the S&P 500 booked back-to-back losses amid a rise in Treasury yields. The Dow Jones Industrial Average DJIA fell 0.6%, while the S&P 500 SPX dropped 0.7% and the tech-heavy Nasdaq Composite COMP sank 1.1%, according to preliminary data from FactSet. Information technology was the S&P 500’s worst-performing sector on Wednesday with a loss of around 1.4%. In the U.S. bond market, the yield on the 10-year Treasury note rose for a third straight day on Wednesday to 4.289%, according to Dow Jones Market Data.

The roughly $25 trillion Treasury market first began flashing this telltale sign that a U.S. recession likely lurks on the horizon almost a year ago, according to Bespoke Investment Group.

It was late October of 2022 when the 3-month Treasury yield BX:TMUBMUSD03M first eclipsed the 10-year Treasury yield BX:TMUBMUSD10Y, resulting in an “inversion” of a key part of the yield curve that’s been a reliable predictor of past recessions.

The Federal Reserve’s inflation fight has been particularly brutal for anyone not already a U.S. homeowner before interest rates and mortgage rates rose to 15-year highs.

With mortgage rates around 7.2% to kick off the post–Labor Day period, the difference between the rates on a new 30-year home loan and on all outstanding U.S. mortgage debt (see chart) has not been so wide since the 1980s.

It’s the 1980s again in the U.S. housing market.

Glenmede, FactSet

“Generally, climbing interest rates curb demand and cause housing prices to fall,” Glenmede’s investment strategy team wrote, in a Tuesday client note, but not this time.

Instead, U.S. homes remain in critically low supply after more than a decade of underbuilding, and with most homeowners who already refinanced at low pre-pandemic rates being “reluctant to leave their homes,” wrote Jason Pride, chief of investment strategy and research, and his Glenmede team.

“Until the supply gap is filled by new construction, home prices and building activity are unlikely to decline as meaningfully as they normally would given the headwind from rising rates,” the Glenmede team said.

The Glenmede team, however, does expect more pressure on consumers in the coming months, particularly as student-loan payments resume in October and if the Fed keeps interest rates high for a while, as increasingly expected. The benchmark 10-year Treasury yield BX:TMUBMUSD10Y,

which underpins the U.S. economy, was back on the climb at 4.26% Tuesday.

Meanwhile, shares of home-vacation rental platform Airbnb Inc. ABNB, +7.23%

rose 7.2% on Tuesday, after the Labor Day weekend, and 66.4% higher on the year so far, according to FactSet.

Shares of Invitation Homes Inc. INVH, -0.91%,

which grew out of the last decade’s home-loan foreclosure crisis to become a single-family-rental giant, were up 14.3% on the year, according to FactSet.

Dallas Tanner, CEO of Invitation Homes, said he expected “the rising costs and the burden of homeownership” to continue to benefit his company, in a July earnings call. The company recently bought a portfolio of about 1,900 homes and has been snapping up newly constructed homes. Companies can borrow on Wall Street at much lower rates than individuals.

Stocks closed lower Tuesday, with the Dow Jones Industrial Average DJIA

off 0.5%, and the S&P 500 index SPX

0.4% lower and the Nasdaq Composite Index COMP

down 0.1%, according to FactSet.

U.S. stocks closed lower Tuesday after the long Labor Day weekend, as bond yields and oil prices climbed. The Dow Jones Industrial Average DJIA shed about 195 points, or 0.6%, ending near 34,642, according to preliminary FactSet data. The S&P 500 index SPX dropped about 0.4% and the Nasdaq Composite Index COMP fell 0.1%. Investors returned from the long weekend in a less bullish mood on weaker economic data from China and Europe, but also with more clouds on the horizon in oil markets. Oil prices CL00 closed at the highest level since November on Tuesday, after Saudi Arabia and Russia opted to extend oil supply production…

A hiring sign is pictured at a McDonald’s restaurant in Garden Grove, California on July 8, 2022.

Robyn Beck | Afp | Getty Images

This report is from today’s CNBC Daily Open, our new, international markets newsletter. CNBC Daily Open brings investors up to speed on everything they need to know, no matter where they are. Like what you see? You can subscribe here.

More jobs but higher unemployment U.S. nonfarm payrolls for August increased by 187,000, above the 170,000 estimate. However, the unemployment rate jumped from 3.5% last month to 3.8%, the highest since February 2022. Average hourly earnings increased 4.3% year on year, below the forecast of 4.4%. Combined with the downwardly revised figures for June and July, those are clear signs the U.S. jobs market is slowing.

Electric vehicle moves Tesla shares slid 5% Friday after the company cut prices on its electric vehicles in both the U.S. and China. Meanwhile in Germany, BMW and Mercedes revealed EV concepts, representing their biggest push yet into the EV market. But that might not be enough to stop China’s dominance. Chinese EV companies all delivered enough vehicles in August to keep pace with their third-quarter guidance.

JPMorgan Chase and Jeffrey Epstein JPMorgan Chase notified the U.S. Treasury Department of more than $1 billion in transactions related to “human trafficking” by Jeffrey Epstein, a lawyer for the U.S. Virgin Islands told a federal judge. Those transactions dated back 16 years and were only reported after Epstein was arrested and killed himself in jail in 2019, said Mimi Liu, an attorney for the Virgin Islands.

[PRO]Slow start to September U.S. markets are closed Monday for Labor Day and economic data coming out this week is on the light side. The heavy hitters, like the consumer and producer price indexes, will only be released later in the month. So keep an eye out for these signs that will indicate whether stocks will fall prey to the September seasonality — the month’s historically been the weakest for stocks.

The U.S. economy added more jobs than expected in August, but the overall unemployment rate rose. This may sound counterintuitive since it’s natural to assume an increase in the number of jobs will lead unemployment going down. But there’s a simple explanation for that.

By definition, the unemployment rate is the number of unemployed people (people without a job but are actively looking for one), divided by the labor force (the sum of people both employed and unemployed), expressed as a percentage.

If the unemployment rate goes up, that means the proportion of people looking for a job compared with the total labor force has grown. That’s straightforward enough. For the unemployment rate to go up even as there were 187,000 more jobs in August means there were more people who started looking for a job than people who secured one. The implication: The total labor force grew in August. Indeed, 597,000 people without work experience sought employment last month, according to the report.

A growing labor force is a looser jobs market. That probably contributed to the lower-than-expected wage growth last month. As Bank of America U.S. economist Stephen Juneau wrote, “The broad message here seems to be that we are nearing full employment, with supply and demand coming more into balance.”

That will come as a relief to Federal Reserve officials worried about a hot jobs market contributing to inflation. Investors, too, cheered the jobs report. They think there’s a 93% chance the Fed will keep rates unchanged at its September meeting and a 65.3% chance at its November meeting, according to the CME FedWatch Tool. That’s up from 80% and 44.5% a week ago, respectively.

Major indexes rose in response to the jobs report as well. The S&P 500 climbed 0.18% Friday, giving it a 2.5% increase for the week — its best weekly performance since June. The Dow Jones Industrial Average added 0.33% to close 1.4% higher for the week. The Nasdaq Composite was essentially flat, but ended the week up 3.3%. That was both indexes’ best showing since July.

U.S. markets are closed today, so we’ll have to wait to see if they can sustain this momentum and defy September’s reputation as the worst month for stocks.

A Chipotle restaurant advertises it is hiring in Cambridge, Massachusetts, August 28, 2023.

Brian Snyder | Reuters

This report is from today’s CNBC Daily Open, our new, international markets newsletter. CNBC Daily Open brings investors up to speed on everything they need to know, no matter where they are. Like what you see? You can subscribe here.

More jobs but higher unemployment U.S. nonfarm payrolls for August increased by 187,000, above the 170,000 estimate. However, the unemployment rate jumped from 3.5% last month to 3.8%, the highest since February 2022. Average hourly earnings increased 4.3% year on year, below the forecast of 4.4%. Combined with the downwardly revised figures for June and July, those are clear signs the U.S. jobs market is slowing.

Winning week for markets U.S. stocks cheered the moderate jobs report and mostly inched up Friday, giving major indexes their best week in months. European markets traded mixed. The regional Stoxx 600 closed flat, the U.K.’s FTSE 100 added 0.34% but other major bourses ended the day in the red. For August, the Stoxx 600 lost 2.8%.

Tesla’s price cut hits shares Tesla shares slid 5% after the company cut prices on its electric vehicles in both the U.S. and China. Additionally, the price of Tesla’s Full Self-Driving software, its premium driver assistance option, was reduced by $3,000. CEO Elon Musk previously said the price would only ever go up. Despite the fall, Tesla shares are still up almost 100% this year.

JPMorgan Chase and Jeffrey Epstein JPMorgan Chase notified the U.S. Treasury Department of more than $1 billion in transactions related to “human trafficking” by Jeffrey Epstein, a lawyer for the U.S. Virgin Islands told a federal judge. Those transactions dated back 16 years and were only reported after Epstein was arrested and killed himself in jail in 2019, said Mimi Liu, an attorney for the Virgin Islands.

[PRO]Slow start to September U.S. markets are closed Monday for Labor Day and economic data coming out this week is on the light side. The heavy hitters, like the consumer and producer price indexes, will only be released later in the month. So keep an eye out for these signs that will indicate whether stocks will fall prey to the September seasonality — the month’s historically been the weakest for stocks.

The U.S. economy added more jobs than expected in August, but the overall unemployment rate rose. This may sound counterintuitive since it’s natural to assume an increase in the number of jobs will lead unemployment going down. But there’s a simple explanation for that.

By definition, the unemployment rate is the number of unemployed people (people without a job but are actively looking for one), divided by the labor force (the sum of people both employed and unemployed), expressed as a percentage.

If the unemployment rate goes up, that means the proportion of people looking for a job compared with the total labor force has grown. That’s straightforward enough. For the unemployment rate to go up even as there were 187,000 more jobs in August means there were more people who started looking for a job than people who secured one. The implication: The total labor force grew in August.

A growing labor force is a looser jobs market. That probably contributed to the lower-than-expected wage growth last month. As Bank of America U.S. economist Stephen Juneau wrote, “The broad message here seems to be that we are nearing full employment, with supply and demand coming more into balance.”

That will come as a relief to Federal Reserve officials worried about a hot jobs market contributing to inflation. Investors, too, cheered the jobs report. They think there’s a 93% chance the Fed will keep rates unchanged at its September meeting and a 65.3% chance at its November meeting, according to the CME FedWatch Tool. That’s up from 80% and 44.5% a week ago, respectively.

Major indexes rose in response to the jobs report as well. The S&P 500 climbed 0.18% Friday, giving it a 2.5% increase for the week — its best weekly performance since June. The Dow Jones Industrial Average added 0.33% to close 1.4% higher for the week. The Nasdaq Composite was essentially flat, but ended the week up 3.3%. That was both indexes’ best showing since July.

U.S. markets are closed today, so we’ll have to wait to see if they can sustain this momentum and defy September’s reputation as the worst month for stocks.

— CNBC’s Jeff Cox contributed to this report

Correction: This article has been updated to reflect the correct month of the jobs report.

The 10-year Treasury bond is on track for a third year of losses in 2023, something that hasn’t happened in 250 years of U.S. history.

In short, it has never happened, say strategists at Bank of America.

The return for investors putting money in that bond BX:TMUBMUSD10Y

stands at negative 0.3% so far in 2023, after a 17% slump in 2022 and a 3.9% drop in 2021, the bank’s strategists, led by Michael Hartnett, pointed out in a note on Friday.

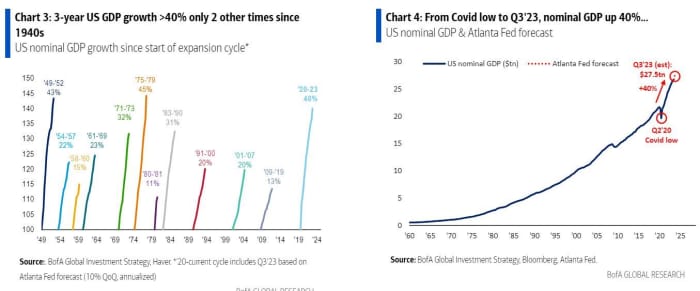

Here’s a visual on that:

That reflects a “staggering 40% jump in U.S. nominal GDP growth” — factoring in growth and inflation — “since the COVID lows of 2020,” they said, providing this chart:

Bond returns have suffered this year as the Federal Reserve has continued its interest-rate-hiking campaign aimed at getting inflation under control. The “big picture in the 2020s vs. the 2010s is lower stock and bond returns, which we would expect to continue given political, geopolitical, social [and] economic trends,” said Hartnett and the team.

SPX,

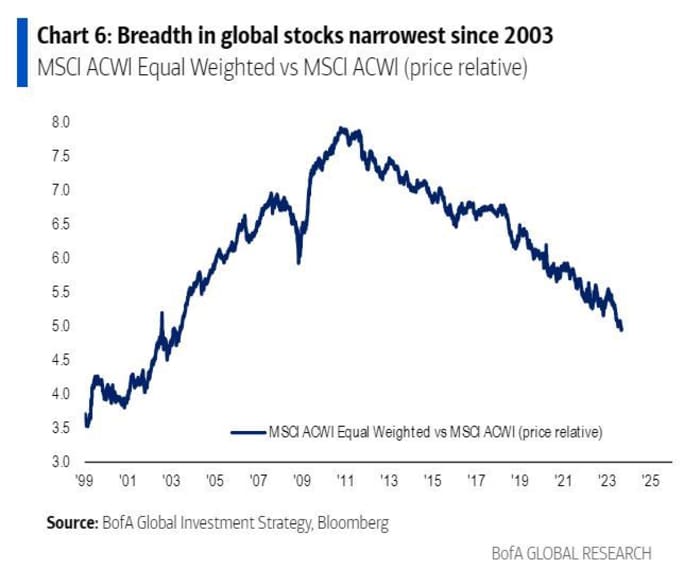

but the bounce since COVID pandemic restrictions began to be lifted has been very concentrated in U.S. stocks, especially the technology sector, with breadth in global markets “breathtakingly bad,” the analysts said. Breadth refers to the number of stocks actively participating in a rally.

Breadth is the worst since 2003 for the MSCI ACWI, which captures large- and midcap-stock representation across 23 developed markets and 24 emerging ones.

As for the latest weekly flows into funds, Bank of America reported that $10.3 billion went to stocks, $6.5 billion to cash and $1.7 billion to bonds, with $300 million draining from gold GC00, -0.06%.

The yield on the 10-year Treasury was holding steady on Friday at 4.102% after data showed the U.S. economy generated 187,000 jobs in August, but the unemployment rate rose to 3.8% from 3.5%, and job gains were revised lower for July and June.

With second-quarter earnings season now largely behind the market, stock investors have been focusing on the latest economic data.

They have, for the most part, been reacting positively to “bad economic news,” or any data that may point to an economic slowdown.

It’s been almost nine months since the trend emerged, as softening economic data and lower inflation may mean the Federal Reserve can stop raising interest rates, said Chris Fasciano, portfolio manager at Commonwealth Financial Network.

Traders in federal-funds futures, as of Friday, are pricing in an over 90% chance that the Fed will hold its policy interest rate unchanged at its September meeting, and a roughly 35% likelihood that the U.S. central bank will raise interest rates by 25 basis points in November.

The data support the narrative of a gradual slowdown in the labor market, but there are no signs that the economy is weakening significantly, according to Richard Flax, chief investment officer at Moneyfarm.

“The economic data has not been bad. It is just softening. If you saw really bad economic data, that wouldn’t be taken particularly positively,” Flax said.

Meanwhile, “what we’re experiencing is a rolling recession,” said Jamie Cox, managing partner at Harris Financial Group. “Recession activity actually goes from sector to sector, but it doesn’t translate into this big broad-based decline.”

However, if investors see a significant decline in the housing and labor markets, that could change the narrative, Cox noted.

To break the cycle in which bad economic news is good news for stocks, economic data have to be much worse than now, indicating more damage from high interest rates, noted Flax.

The trend may also reverse if there is a “meaningful downgrade” of corporate earnings expectations, said Flax. “I think you need to see it when macro data translates into weakened profitability.”

Investors should also be alert of the possibility that inflation may accelerate again, according to David Merrell, founder and managing member at TBH Advisors.

Data showed that the personal consumption expenditures price index rose a mild 0.2% in July, but the yearly inflation rate crept up to 3.3% from 3%, the government said Thursday.

“Inflation overall has been trending down nicely. But if it starts to kick back up, that could mean bad news becomes bad news now,” said Merrell.

If investors start to treat bad economic news as bad news for the stock market, it could put pressure on the 2023 stock-market rally, with the S&P 500 SPX

up 17.6% since the start of the year and the Nasdaq Composite COMP

up 34%.

In the past week, the Dow Jones Industrial Average DJIA

climbed 1.4%, the S&P 500 advanced 2.5% and the Nasdaq gained 3.2%, according to Dow Jones Market Data. The S&P 500 posted its biggest weekly gain since the week ending June 16.

This week, investors will be expecting data on the July U.S. international trade deficit and the ISM services sector activity for August on Tuesday, weekly initial jobless benefit claims data on Thursday, and the July wholesale inventories data on Friday. They will also tune into the speeches of a number of Fed speakers, looking for clues on whether the central bank is ready to be done with its rates hikes.

The 10-year Treasury bond is on track for a third year of losses in 2023, something that hasn’t happened in 250 years of U.S. history.

In short, it has never happened, say strategists at Bank of America.

The return for investors putting money in that bond BX:TMUBMUSD10Y

stands at negative 0.3% so far in 2023, after a 17% slump in 2022 and a 3.9% drop in 2021, the bank’s strategists, led by Michael Hartnett, pointed out in a note on Friday.

Here’s a visual on that:

That reflects a “staggering 40% jump in U.S. nominal GDP growth” — factoring in growth and inflation — “since the COVID lows of 2020,” they said, providing this chart:

Bond returns have suffered this year as the Federal Reserve has continued its interest-rate-hiking campaign aimed at getting inflation under control. The “big picture in the 2020s vs. the 2010s is lower stock and bond returns, which we would expect to continue given political, geopolitical, social [and] economic trends,” said Hartnett and the team.

SPX,

but the bounce since COVID pandemic restrictions began to be lifted has been very concentrated in U.S. stocks, especially the technology sector, with breadth in global markets “breathtakingly bad,” the analysts said. Breadth refers to the number of stocks actively participating in a rally.

Breadth is the worst since 2003 for the MSCI ACWI, which captures large- and midcap-stock representation across 23 developed markets and 24 emerging ones.

As for the latest weekly flows into funds, Bank of America reported that $10.3 billion went to stocks, $6.5 billion to cash and $1.7 billion to bonds, with $300 million draining from gold GC00, +0.02%.

The yield on the 10-year Treasury was holding steady on Friday at 4.102% after data showed the U.S. economy generated 187,000 jobs in August, but the unemployment rate rose to 3.8% from 3.5%, and job gains were revised lower for July and June.

This copy is for your personal, non-commercial use only. To order presentation-ready copies for distribution to your colleagues, clients or customers visit http://www.djreprints.com.

U.S. lawmakers are due to get back to work Tuesday on Capitol Hill, and there are growing expectations that one fruit of their labors will be a partial government shutdown.

“My guess is that we will have a lot of screaming and shouting, and we’ll end up shutting down the government, and a lot of people will be inconvenienced or hurt as a result of doing that, but we’ll do it,” said Republican Sen. Mitt Romney of Utah in an interview with a TV station in his home state.

“And by the way, we’ll shut down government, and then we’ll open it. It’s not like that means that we win. No, no. We just shut it down to show that we’re fighting and making noise.”

Investors should view the shutdown as largely noise, according to a number of analysts in Washington, D.C., who track lawmakers’ moves for Wall Street.

“The stakes here are significantly lower than they were back in June, when we were facing default,” said Ed Mills, Washington policy analyst for Raymond James, referring to lawmakers’ efforts to reach a deal on raising the U.S. debt ceiling in order to avoid a market-shaking default.

“For the most part, this is a 1 or 2 on a scale of 1 to 10 in terms of concern,” Mills told MarketWatch, adding that a U.S. default, on the other hand, would have registered as a 10 on that scale.

There have been six government shutdowns since 1978 that lasted five days or more, and the S&P 500 stock index SPX

gained in the four most recent shutdowns. Brian Gardner, chief Washington policy strategist at Stifel, emphasized that history in a note to clients.

“Headlines regarding a potential budget impasse will grow and there could be a whiff of panic in the air, but investors should take all of this in stride. Markets tend to ignore the impact of a government shutdown,” Gardner wrote, as he offered the chart shown below.

There have been six shutdowns since 1978 that lasted five days or more. Here’s how stocks handled them.

Stifel’s Gardner said that while past shutdowns suggest that investors should not panic, there still is some damage.

“There will be extensive media coverage of closed entrances at national parks and other government facilities. Government salaries will not be paid on time which is, certainly, a hardship for some families,” he wrote. At the same time, he emphasized that “much of the country will operate as usual,” including the military ITA

and air traffic controllers — and missed paychecks will come through once the shutdown ends.

“From a market perspective, the biggest concern relating to a government shutdown is that it could delay official government data reports at a pivotal time for the Federal Reserve,” said BTIG’s Issac Boltansky and Isabel Bandoroff in a note.

The BTIG analysts said they expect a shutdown will occur but it should be a “nonevent for markets” overall, because it “would have no impact on debt payments and any missed activity would be settled on the other side of reopening.”

There could be a greater-than-anticipated impact on stocks DJIA

COMP

if the shutdown lasts for a longer time than expected, and if the deal to end the shutdown features unexpectedly large cuts to spending along with significant repeals of Democrats’ Inflation Reduction Act, according to Mills, the Raymond James analyst.

“The most likely scenario is that it’s days, not weeks,” he said, regarding the length of any shutdown. He also noted it could hit consumer confidence and disrupt the initial-public-offering process for some companies.

What’s likely to happen on Capitol Hill

Only one chamber of Congress is returning to Washington on Tuesday, the day following Labor Day, after an August recess — the Senate. The House of Representatives is slated to resume its work on Capitol Hill a week later, on Sept. 12.

Ahead of their returns, the Biden White House’s budget office has pushed for passage of a short-term funding measure to avoid a partial federal government shutdown on Oct. 1, when the government’s 2024 fiscal year starts.

Such a measure is known as a continuing resolution, or CR, and they’re often used as the House and Senate work to agree on a dozen appropriations bills that would fund government operations for a full fiscal year.

The debt-ceiling deal negotiated between House Speaker Kevin McCarthy and President Joe Biden set spending levels over the next two years, keeping nonmilitary spending for 2024 the same as 2023 levels. But House Republicans have adopted spending targets for the coming fiscal year at levels below the McCarthy-Biden agreement.

“The thing that Kevin McCarthy is trying to tell his caucus is that we probably need to have a short-term CR, so that the House can finish its work on appropriations bills and establish the best negotiating position,” Mills said.

The House Freedom Caucus, a hardline GOP group known for causing headaches for the chamber’s leaders, has voiced concerns. It said in an Aug. 21 statement that its members want to rein in outlays and will oppose any spending measure that doesn’t include a House-passed bill focused on security at the U.S. southern border. In addition, the group said any spending measure must address the “unprecedented weaponization” of the Justice Department and the FBI, as well as end “woke policies in the Pentagon.”

The most likely path forward is the GOP-run House passes a short-term funding measure that incorporates House Freedom Caucus goals, and then there’s a showdown with the Democratic-controlled Senate over those policy riders, with a short-lived shutdown potentially taking place, Mills said.

The Raymond James analyst said the most likely deal is a budget that’s in line with what was negotiated as part of the debt-limit deal. He also expects supplemental measures that provide relief for areas hit by Hurricane Idalia and the Maui wildfires, as well as some funding for Ukraine as it continues its fight against Russia’s invasion.

“For investors, they have seen McCarthy go up to the brink, go through a tough situation and be able to pull a rabbit out of it,” Mills said, referring to his January battle to become House speaker and the spring’s debt-limit talks. And they’ve “gone through government shutdowns in the past, mostly with very minimal market reaction,” he added.

U.S. exchange-traded funds that invest in Chinese stocks notched their best day in a month after China ramped up its efforts to support the country’s flagging currency as investors’ concerns over the economic weakness persist.

The Invesco Golden Dragon China ETF PGJ,

which tracks the American depositary shares of companies based in China, rose 3% on Friday, while the KraneShares CSI China Internet ETF KWEB,

which offers exposure to Chinese software and information technology stocks, gained 3.5%. The iShares MSCI China ETF MCHI

advanced nearly 2.2% and the SPDR S&P China ETF GXC

surged 2%, according to FactSet data.

The iShares MSCI China ETF and the KraneShares CSI China Internet ETF booked their biggest daily percentage advance since August 3, according to FactSet data.

Based on about $822 billion foreign-exchange deposits in July, the 200-basis-point cut in the reserve requirement ratio could release about $16 billion, which will improve the supply of the U.S. dollar onshore, and could move spot USDCNY lower, said strategists at Citigroup led by Johanna Chua, chief Asia economist.

“In a broader picture, this can be also seen as part the current round of accelerated policy rollout which works more directly on asset markets. If the accelerated pace [of policy rollout] continues, it may help stabilize sentiment to some extent and prevent outsized bearish moves on China risk assets including the RMB FX,” they wrote in a Friday note.

The onshore yuan USDCNY,

weakened around 1.7% against the dollar in August, extending its losses for the year to nearly 5%, according to FactSet data. The offshore yuan USDCNH, -0.03%

was trading at 7.27 per dollar Friday afternoon.

Friday’s change to reserve requirement ratio came a day after Chinese authorities announced that homebuyers’ minimum down payment will be reduced to 20% for first-time home purchases, and 30% for second-home purchases nationwide, according to a joint statement from the People’s Bank of China and National Administration of Financial Regulation late Thursday.

Currently, homebuyers in largest cities such as Beijing and Shanghai have a 30% down payment ratio for first homes, and 40% or more for second homes.

Separately, big banks, such as Industrial & Commercial Bank of China 601398, -1.08%

and Bank of China 601988, -1.07%,

have said they would cut their one-year yuan deposit rate by 10 basis points to 1.55% and their two-year yuan deposit rate by 20 basis points to 1.85%. The banks also plan to cut mortgage rates to boost consumption and aid the troubled property sector.

The broader U.S. stock market finished mostly higher on Friday as traders weighed the latest jobs report to conclude the final trading day before the Labor Day holiday weekend. The S&P 500 SPX

was up 0.2%, while the Dow Jones Industrial Average DJIA

advanced 0.3% but the Nasdaq Composite COMP

ended nearly flat.

The Federal Reserve can probably end its inflation fight now that the U.S. labor market is cooling after generating a historic 26 million jobs in roughly the past three years, according to BlackRock’s Rick Rieder.

“In fact, 26 million jobs is like adding an economy the size of Australia or Taiwan (including every man, woman, and child),” said Rieder, BlackRock’s chief investment officer in global fixed income, in emailed commentary following Friday’s monthly jobs report for August.

The August nonfarm-payrolls report showed the U.S. adding 187,000 jobs, slightly more than had been forecast, but also pointing to an uptick in the unemployment rate to 3.8% from 3.5%.

“Remarkably, 22 million people were hired between May 2020 and April 2022, and 11 million were added to the workforce from June 2021 to May 2023, as the economy has opened up massive amounts of roles for fulfillment,” said Rieder.

He expects wage pressures to ease, he said, and thinks the “economy may now have fulfilled many of its needs,” which should make the Fed feel more confident in “the permanence of lower levels of inflation,” so that it can slow or stop its interest-rate rises by year-end.

Hiring in the U.S. has slowed, except in education and in healthcare services, when looking at private payrolls based on a three-month moving average.

Payrolls are slowing in many sectors, expect education and healthcare

Rieder of BlackRock, one of the world’s largest asset managers with $2.7 trillion in assets under management, said he thinks a Fed pause or outright end to rate hikes could calm markets, even if the Fed, as BlackRock expects, keeps rates high for a time.

U.S. closed mostly higher Friday ahead of the Labor Day holiday weekend, with the Dow Jones Industrial Average DJIA

up 0.3%, the S&P 500 index SPX

up 0.2% and the Nasdaq Composite Index COMP

0.02% lower, according to FactSet.

The 10-year Treasury yield BX:TMUBMUSD10Y

was at 4.173%, after hitting its highest level since 2007 in late August, adding to volatility that has wiped out earlier yearly gains in the roughly $25 trillion Treasury market.

U.S. stock futures pointed higher on Friday, ahead of data that could show a slowing pace of hiring, which would reassure investors that the Federal Reserve won’t take interest rates much higher.

What’s happening

Dow Jones Industrial Average futures YM00, +0.39%

rose 78 points, or 0.2%, to 34869.

S&P 500 futures ES00, +0.34%

gained 9 points, or 0.2%, to 4525.

Nasdaq 100 futures NQ00, +0.17%

increased 12 points, or 0.1%, to 15551.

On Thursday, the Dow Jones Industrial Average DJIA

fell 168 points, or 0.48%, to 34722, the S&P 500 SPX

declined 7 points, or 0.16%, to 4508, while the Nasdaq Composite COMP

gained 16 points, or 0.11%, to 14035.

What’s driving

Ahead of Friday’s barrage of heavy-hitting economic data, U.S. stocks saw modest pressure, as inflation data was largely benign but jobless claims dented an emerging picture of an economic slowdown. Dollar General’s DG, -12.15%

profit warning, however, pointed to a consumer under pressure.

Friday will see the release of nonfarm payrolls data at 8:30 a.m. Eastern, with expectations that 170,000 jobs were created in August. That would be the weakest showing since Dec. 2020, a month that saw 268,000 jobs lost.

“There have been indicators that the U.S. jobs market is finally starting to lose some of its tightness, and if the NFP print confirms this trend, it will be one less thing for the FOMC to worry about given labor market resilience has long been a source of inflationary pressure,” said Tim Waterer, chief market analyst at KCM Trade.

There’s also the Institute for Supply Management’s manufacturing index, as well as monthly auto sales, that will get released. Thursday’s after hours releases saw mixed responses, with Dell Technologies DELL, +0.99%

stock rallying but Broadcom shares AVGO, +3.43%

wilting after results.

In China, August Caixin manufacturing PMI came in above expectations, rising to 51, a level that indicates improving conditions, as the country also lowered down-payment requirements on homes. The Hong Kong market was shut over storm-related concerns.

The U.S. Labor Day holiday will mark another milestone in the marathon to bring workers back to the office, but it won’t be a quick fix for landlords, according to Thomas LaSalvia, head of commercial real estate economics at Moody’s Analytics.

“A lot of companies are saying that after Labor Day, ‘We expect more out of you,” LaSalvia said, referring to days in the office. Still, office attendance, he argues, likely only stages a fuller comeback if a job or promotion is on the line.

That could prove difficult, with Friday’s U.S. jobs report for August expected to show U.S. unemployment at a scant 3.5%, near the lowest levels since the late 1960s, even if hiring has been slowing. The labor market, so far, appears unfazed by the Federal Reserve’s benchmark rate reaching a 22-year high.

It has been a different story for landlords facing a roughly 19% vacancy rate nationally and piles of debt coming due, especially for owners of older Class B and C office buildings with a bleak outlook or properties in cities with wobbling business centers.

As with shopping malls, LaSalvia said it’s largely a problem of oversupply, with many office properties at risk of becoming obsolete as tenants flock to better buildings and locations staging a rebirth. The trend can be traced in leasing data since 2021, with Class A properties in central business districts (blue line) showing a big advantage over less desirable buildings in the heart of cities (orange line).

Return to office isn’t going to save the entire office property market

Moody’s Analytics

“Little by little, we are finding the office isn’t dead,” LaSalvia said, but he also sees more promise in neighborhoods with a new purpose, those catering to hybrid work and communities that bring people together.

Another way to look at the trend is through rents. Manhattan’s Penn Station submarket, with its estimated $13 billion overhaul and neighboring Hudson Yards development, has seen asking rents jump 32% to $74.87 a square foot in the second quarter since the fourth quarter of 2019, according to Moody’s Analytics. That compares with a 2% bump in asking rents in downtown New York City to $61.39 a square foot for the same period.

The push for a return to the office also doesn’t mean a repeat of prepandemic ways. Goldman Sachs analysts estimate that part-time remote work in the U.S. has stabilized around 20%-25%, in a late August report, but that’s still up from 2.6% before the 2020 lockdowns.

Furthermore, the persistence of remote work will likely add another 171 million square feet of vacant U.S. office space through 2029, a period that also will see tenants’ long-term leases expire and many companies opting for less space. The additional vacancies would roughly translate to 57% of Los Angeles roughly 300 million square feet of office space sitting empty.

“The fundamental reason why we had offices in the first place have not completely disintegrated,” LaSalvia said. “But for some of those Class B and C offices, the writing was on the wall before the pandemic.”

U.S. stocks were mixed Thursday, but headed for losses in a tough August for stocks, with the S&P 500 index SPX

off about 1.5% for the month, the Dow Jones Industrial Average DJIA

2.1% lower and the Nasdaq Composite COMP

down 2% in August, according to FactSet.

A help wanted sign on a storefront in Ocean City, New Jersey, US, on Friday, Aug. 18, 2023. Surveys suggest that despite cooling inflation and jobs gains, Americans remain deeply skeptical of the president’s handling of the post-pandemic economy. Photographer: Al Drago/Bloomberg via Getty Images

Al Drago | Bloomberg | Getty Images

This report is from today’s CNBC Daily Open, our new, international markets newsletter. CNBC Daily Open brings investors up to speed on everything they need to know, no matter where they are. Like what you see? You can subscribe here.

Job creation slowed Job growth in the U.S. slowed to 177,000 in August, according to payroll company ADP. That’s fewer than economists’ expectation of 200,000 — which is itself already much lower than July’s downwardly revised 371,000. It’s a sign the effects of high interest rate are starting to be felt, giving traders hope the Federal Reserve might pause hikes.

Markets regain ground U.S. stocks rallied Wednesday on the back of weaker-than-expected economic data, giving the S&P 500 a four-day winning streak. Asia-Pacific markets traded mixed Thursday. Japan’s Nikkei 225 rose around 1% as data showed retail sales for July jumping 6.8% year on year, sharply higher than the expected 5.4%. But China’s Shanghai Composite lost 0.5% as economic data disappointed again.

Mixed signs in China China’s factory activity in August shrank for the fifth straight month, but at a slower pace than July. Non-manufacturing activity expanded for the month, but dipped to its lowest level this year. Meanwhile, retail sales in August experienced a marked increase compared with July, according to the China Beige Book’s survey of Chinese businesses.

[PRO]China plus three Amid a prolonged downturn in China’s economy, investors are growing bearish on the stock market. But this could be an opportunity for investors to put their money into other Asian markets, analysts say. Here are the three Asian markets analysts recommend — and the best ways to play them.

Markets last week were gripped by the fear that interest rates will remain high — or go even higher than they already are — in the face of an unyieldingly strong economy and stubborn inflation. (Recall how the 10-year Treasury yield, which typically reflects rate expectations, hit a 16-year high last week.)

Those worries dissipated somewhat Wednesday.

New data showed that economic growth, while still hot enough to suggest a soft landing, was not quite as scorching as previously thought. Second-quarter gross domestic product the U.S. was revised downwards from 2.4% to 2.1% on an annualized basis.

Moreover, job creation for August was lower than expected. In another encouraging sign that inflation might be moderating, pay growth for workers slowed, regardless of whether they changed jobs or stayed in their current positions, according to ADP.

“This month’s numbers are consistent with the pace of job creation before the pandemic,” Nela Richardson, chief economist at ADP, said in a press release. “After two years of exceptional gains tied to the recovery, we’re moving toward more sustainable growth in pay and employment as the economic effects of the pandemic recede.”

In sum, there’s hope the Federal Reserve might loosen its grip on monetary policy, based on the weaker-than-expected economic data. Markets cheered the news.

The S&P 500 rose 0.38%. It might seem a small figure, but it’s statistically significant for a few reasons: One, it gives the index a four-day winning streak; two, it helped the index close above 4,500, breaking a key psychological barrier; three, it helped to trim August’s losses to around 1.6%, down from an intraday low of 5.53% on August 18. The Dow Jones Industrial Average inched up 0.11% and the Nasdaq Composite climbed 0.54%.

For tomorrow, look out for the personal consumption expenditures index, which measures how much consumers spent in July. If inflation numbers come in soft, then that completes the trifecta of data — economic growth, jobs and inflation — that the Fed wants to see slow down. Then markets can probably heave a sigh of relief, for now.