Wall Street just learned an expensive lesson about betting on Washington.

According to a Wall Street Journal report, UnitedHealth Group lost roughly $60 billion in market value on January 27 after the Centers for Medicare & Medicaid Services proposed 2027 payment rates that would barely budge from current levels.

Analysts had expected increases closer to 5%. Instead, CMS suggested a 0.09% bump. UNH stock plunged 19% in a single session, marking its worst day since April 2025.

For income investors who’ve collected UnitedHealth (UNH) dividends through thick and thin, the question isn’t just about recovering the stock price.

It’s whether that dividend check keeps showing up while the company navigates what could be its roughest period in decades.

UNH is dependent on Medicare for long-term growthGetty Images Heather Diehl ·Getty Images Heather Diehl

Here’s the uncomfortable truth:

UnitedHealth has become heavily dependent on Medicare for revenue growth.

The company’s Medicare revenue is now more than double its private insurance revenue.

That worked great when government rates kept climbing. Now it’s a vulnerability.

CEO Steve Hemsley, who came out of retirement to lead the turnaround after the company fired his predecessor last year, tried to project confidence during Tuesday’s earnings call.

Investors didn’t share his enthusiasm as the stock kept falling.

UnitedHealth now expects 2026 revenue to reach roughly $439 billion, a 2% decline from 2025. That’s the first revenue contraction since 1989, back when hardly anyone had heard of managed care.

That’s worse than the company originally anticipated, driven by fierce competition during the annual enrollment period.

Add in expected losses of 565,000 to 715,000 Medicaid members, plus declines across commercial plans, and you’re looking at total membership dropping by 2.3 million to 2.8 million people.

That’s not all bad news, though. UnitedHealth deliberately walked away from unprofitable business, repricing plans to focus on members it can actually serve sustainably. The strategy prioritizes margin recovery over top-line growth.

“We will need very meaningful benefit reductions and to take a hard look at our geographic and product footprint,” Noel said, according to Reuters.

In other words, seniors should expect fewer extras and potentially higher out-of-pocket costs as insurers scramble to protect margins.

This is where dividend investors need to focus.

UnitedHealth expects to generate at least $18 billion in operating cash flow for 2026.

That works out to roughly 1.1 times net income, down from 1.5 times in 2025 but still healthy enough to cover the dividend.

CFO Wayne DeVeydt said the dividend would “remain well supported by earnings and cash flow” this year.

According to data from Tikr.com, between 2026 and 2030, UNH stock is forecast to expand from:

Revenue from $449 billion to $581.8 billion.

Free cash flow from $19.35 billion to $27.80 billion.

Annual dividend from $8.75 per share to $12.72 per share.

Wall Street expects UnitedHealth’s dividend payout ratio to range around 41% over the next four years, which is not too high. In this period, the dividend yield at cost is expected to increase from 3% to 4.5%.

But here’s the catch investors need to understand: DeVeydt made clear the company won’t return to “historical capital deployment practices” until the second half of 2026. That’s corporate speak for “don’t expect share buybacks anytime soon.”

The dividend itself looks safe based on cash flow projections. But growth in the payout? That could slow to a crawl as the company prioritizes balance sheet repair and navigates a hostile regulatory environment.

For 2026, UnitedHealth projects adjusted earnings per share of greater than $17.75, representing growth of at least 8.6% over 2025’s adjusted EPS of $16.35.

That’s solid, but nowhere near the double-digit earnings growth investors had grown used to.

UnitedHealth faces more than just rate pressure. The WSJ report explained:

The Trump administration has shown little appetite for insurance industry lobbying, despite initial expectations that it would take a friendlier approach.

Federal spending cuts remain a priority, and political hostility toward insurers has only intensified.

Two powerful House committees recently grilled insurance CEOs about care denials, business structures, and profits.

President Trump himself has said he wants to meet with insurers to push for lower pricing.

Meanwhile, CMS administrator Mehmet Oz has positioned himself as a “new sheriff in town” ready to crack down on industry billing practices that have drawn scrutiny.

The final 2027 rates won’t be announced until April, giving the industry time to lobby for improvements. But the early signals suggest the government isn’t in a generous mood.

UnitedHealth’s dividend isn’t in immediate danger. Cash flow remains strong enough to support current payouts, and management has explicitly committed to maintaining the dividend.

But this isn’t a growth story anymore, at least not for the next year or two.

The company needs time to stabilize margins, work through membership declines, and adapt to a tougher regulatory environment.

Dividend growth will likely remain minimal until earnings momentum returns, not until 2027 at the earliest.

For conservative income investors looking for steady, growing dividends, UnitedHealth doesn’t fit that profile right now. The dividend is safe, but it’s unlikely to grow at the historical pace.

For more aggressive investors willing to ride out volatility, the 19% selloff could create value. But you’d need patience to wait for the turnaround to gain traction and comfort with the political and regulatory risks that aren’t going away.

Sometimes the best dividend play is the one you don’t make.

WASHINGTON, Dec 16 (Reuters) – The Trump administration is planning an executive order that would limit dividends, buybacks and executive pay for defense contractors that are over-budget and delayed, according to three sources briefed on the order.

President Donald Trump and the Pentagon have been complaining about the expensive, slow-moving and entrenched nature of the defense industry, promising dramatic changes that would make the production of war equipment more nimble.

Industry groups have been on high alert about the closely held proposal, which is tied to a Treasury Department initiative, two of the sources said.

Reuters could not determine exactly how the order would compel defense firms to enact any restrictions. The sources said the language of the order could still change.

Online political news service Punchbowl was the first to report the potential for financial restrictions on defense firms.

The White House did not immediately return a request for comment.

U.S. Secretary of Defense Pete Hegseth unveiled sweeping changes in November to how the Pentagon purchases weapons, allowing the military to more rapidly acquire technology amid growing global threats, in accordance with an executive order signed by Trump in April.

The Pentagon restructuring will have direct authority over major weapons programs to eliminate bureaucracy. The acquisition chain will run directly from program managers to these portfolio executives to military service branch acquisition leaders, with no intermediate approval layers.

The November reforms target what Pentagon officials call “unacceptably slow” procurement, which they blame on fragmented accountability and misaligned incentives that have hampered the military’s ability to field new technology quickly.

(Reporting by Joey Roulette and Mike Stone; Editing by Chris Reese)

President Donald Trump promised on Monday that his administration will begin issuing $2,000 “tariff dividend” checks to Americans around the middle of 2026, the most specific timetable he has offered yet on a proposal that can’t seem to find a home within a campaign-esque promise, economic argument and political provocation.

“We’re going to be issuing dividends later on, somewhere prior to … probably the middle of next year, a little bit later than that,” Trump told reporters in the Oval Office, according to Axios. The payments, he said, would go to “individuals of moderate income, middle income.”

The commitment marks an escalation from Trump’s earlier, vaguer assertions that tariffs are generating enough money to fund direct payments to American households. But turning the idea into actual checks is far more complicated than his easy-going rhetoric suggests.

Treasury Secretary Scott Bessent made that clear over the weekend, saying on Fox News that the administration “needs legislation” to distribute any such dividend.

“We will see,” he added. Bessent also implied that the structure could take forms other than a check — for instance, a tax rebate — signaling uncertainty inside the administration about what Trump’s proposal even is.

The math is another obstacle. A $2,000-per-person dividend, even if limited to Americans with low or middle incomes, would cost well over the $200 billion that Trump’s tariffs have brought in. If the checks resembled the COVID-era stimulus structure — which went to adults and children alike— the Committee for a Responsible Federal Budget estimates the price tag could reach $600 billion. That would mean that Trump’s tariffs would be a net $400 billion negative for the U.S. in 2026, based on current projections.

And the future of that revenue is itself uncertain. The Supreme Court is expected to rule within months on whether Trump exceeded his authority when he imposed sweeping tariffs by invoking national emergency powers. So far, both conservative and liberal supreme court justices have seemed skeptical of his arguments. If the Court rules against him, the administration may have to somehow refund billions in collected duties to importers, which would be the opposite of Trump’s promised “dividend.” Trump argues the stakes are existential, claiming a loss could cost the U.S. $3 trillion in refunds and lost investment.

The White House did not immediately respond to Fortune’s request for comment.

Still, Trump continues to present tariffs as an all-purpose economic engine: a way to protect U.S. factories, pressure foreign governments, strengthen the federal budget, and now, finance what he has described as a populist windfall. Trump and the Republican party broadly have been focused on winning voters’ favor back on “affordability” ever since Democrats’ swept elections earlier this month. The President even said on Friday that he would roll back tariffs on beef, coffee, tropical fruits and commodities, even as he continues to insist that tariffs don’t raise prices.

“Affordability is a lie when used by the Dems. It is a complete CON JOB,” he wrote Friday on Truth Social.

WILMINGTON, DEL. (Reuters) -A Texas state judge won’t block Kenvue from paying its scheduled November 26 shareholder dividend, rejecting a request by Texas Attorney General Ken Paxton, a Kenvue lawyer told Reuters on Friday.

(Reporting by Tom Hals in Wilmington, Delaware, Editing by Franklin Paul)

Chalk that up as a win for Canadians. Between the tax-free savings account (TFSA), registered retirement savings plan (RRSP), and first home savings account (FHSA), Canadians have ample room to shelter gains from the Canada Revenue Agency (CRA). These registered accounts offer more flexibility and contribution room than Americans get with comparable 401(k) and Roth IRA plans, and they can go a long way if you use them wisely.

That said, whether from windfalls or diligent saving, some Canadians do manage to max out their registered accounts. Once that happens, and until new room opens up in January, the challenge becomes how to keep more of your investment income and gains from getting taxed in a non-registered account.

Some exchange-traded funds (ETFs) are better than others for this. Here’s a guide to how ETF tax efficiency works in Canada and which types of ETFs work best in taxable accounts.

Compare the best TFSA rates in Canada

The ABCs of ETF taxation

In a nutshell, ETF taxes work a lot like the taxes on stocks or bonds, because most ETFs are just collections of those underlying investments. If you’ve ever received a T3 or T5 slip, the categories will look familiar.

The easiest way to see how it works in practice is to check the ETF provider’s website for a tax breakdown. We’ll walk through an example using the BMO Growth ETF (ZGRO), a globally diversified asset-allocation ETF that holds about 80% equities and 20% fixed income.

If you scroll down to the “Tax & Distributions” section on ZGRO’s fund page, you’ll see a table that breaks down the composition of distributions by year. The most recent data for 2024 shows the ETF paid out $0.467667 per unit in total distributions, made up of several different tax categories:

Eligible dividends ($0.082884): These are typically paid by Canadian companies and benefit from the dividend tax credit, which lowers your effective tax rate.

Other income ($0.047890): This mostly includes interest income from the bonds held in ZGRO. It’s fully taxable at your marginal tax rate, just like salary or rental income.

Capital gains ($0.157617): Often from ETF managers rebalancing the portfolio. While not always avoidable, only 50% of a capital gain is taxable, which softens the tax hit. You will also have to pay these yourself if you sell ETF shares for a capital gain.

Foreign income ($0.169810): This comes from dividends paid by non-Canadian companies in the ETF. It’s also fully taxable as ordinary income. Worse, 15% is typically withheld at source (visible as the “foreign tax paid” line of –$0.018009) and may or may not be recoverable depending on the account type.

Return of capital ($0.027475): This is essentially some of your own money coming back to you. It’s not taxable in the year received, but it lowers your adjusted cost base. That means you’ll eventually pay tax on it when you sell the ETF and realize a capital gain. Used properly, this can smooth out distributions, but it can also inflate yield figures.

All of these get taxed differently, which makes ETFs like ZGRO tricky to manage in a non-registered account. In a TFSA or RRSP, you can ignore this tax complexity because none of it applies. But outside of registered accounts, you’ll need to report this all accurately, which can mean more work at tax time.

ZGRO is still a strong choice overall—it’s diversified, affordable, and well constructed. But for Canadian investors focused on tax efficiency, there are cleaner options. ETFs like ZGRO make the most sense in a registered account where you don’t have to worry about this messy tax mix.

Article Continues Below Advertisement

What’s your goal: capital appreciation or income?

Figuring out which ETFs are more tax-efficient starts with defining your objective. Are you investing for capital appreciation, or are you trying to generate regular income from your portfolio?

If your goal is capital growth and you don’t need to make regular withdrawals, say, for retirement income, the focus should be on ETFs that minimize or avoid distributions. This allows the value of the ETF to grow through share price gains rather than payouts, which can defer your tax burden.

One simple way to do this is to choose growth-focused ETFs. For example, the Invesco NASDAQ 100 ETF (QQC) offers exposure to U.S. tech stocks that typically don’t pay high dividends, since they often reinvest profits into research and development and expansion. QQC’s trailing 12-month yield is just 0.42%, mostly foreign income. That level is low enough to render the tax drag minimal.

If you want to go a step further and avoid distributions altogether, some ETF families are designed specifically to do that. A well-known example is the Global X Canada (formerly Horizons ETFs) suite of corporate class, swap-based ETFs. In simple terms, these ETFs use a different fund structure and derivatives contracts to synthetically replicate exposure to equities while avoiding distributions. This has worked well in practice. You could create a globally diversified equity portfolio using:

HXS: Global X S&P 500 Index Corporate Class ETF

HXT: Global X S&P/TSX 60 Index Corporate Class ETF

HXX: Global X Europe 50 Index Corporate Class ETF

But there are trade-offs. These ETFs have seen their fees rise over time. On top of the management fee, they also charge a swap fee and have higher trading expense ratios than traditional index ETFs. This adds to your cost of holding the fund. And because they rely on swaps, you’re exposed to counterparty risk, which is the chance that the other party to the derivative contract (often a big Canadian bank) fails to deliver on its obligation. That’s unlikely but not impossible.

Another caveat is that, while these ETFs are designed to avoid distributions, they can’t guarantee zero payouts. The distribution frequency is listed as “at the manager’s discretion,” largely because of how fund accounting works. And there’s always the risk that tax law changes could alter how these structures are treated, as has happened in the past.

If you’re investing in a taxable account and want to prioritize tax deferral, these ETFs are worth considering, but go in with your eyes open.

Tax-efficient income funds

Personally, I fall into the camp of just selling ETF shares and paying capital gains tax when I need portfolio withdrawals. But I recognize a lot of investors (especially retirees) have a strong psychological aversion to this. This behaviour is known as mental accounting.

Share prices were up 5% in after-hours trading on Thursday after the strong earnings beat.

Amazon (AMZN/NASDAQ): Earnings per share of $1.43 (versus $0.14 predicted) and revenues of $134.4 billion (versus $131.5 billion predicted).

Amazon Web Services (AWS) remains the golden goose, even though very few of Amazon’s retail customers know it exists. Revenues climbed 19% during the quarter, and totalled $27.4 billion. Amazon’s advertising revenues were another highlighted area of the report, as they were up 19%. Overall operating profits grew 56% year over year to $17.4 billion, mostly credited to the 27,000 jobs cut by the company since 2022.

Founder, executive chairman and former president and CEO of Amazon, Jeff Bezos was in the headlines this week in his role as owner of the Washington Post. He refused to allow the Post’s editorial team to print their endorsement of Kamala Harris for president, and it was met with widespread outrage from Post readers. As of Tuesday, more than 250,000 subscriptions were cancelled as a result.

Fortunately for Bezos, he purchased the Washington Post (one of the world’s premier news brands) for “chump change”—$250 million (roughly a mere 1.2% of his net worth). So, if he drives it into the ground, I don’t think he’ll shed tears.

No doubt co-founder and CEO of Tesla, Elon Musk, is making similar calculations with his luxury purchase two years ago of Twitter (which he rebranded as X). Critics say he has turned the social platform into an echo chamber for Republican presidential candidate Donald Trump. What are the billions for, if a person can’t even enjoy themselves by buying a little media, am I right?(That’s sarcasm.)

So far we’ve yet to see analysis to show Bezos’ editorial decision affecting Amazon’s share price or revenue numbers. Apparently Republicans buy Amazon Prime, too.

Canada’s best dividend stocks

Microsoft, Meta and Google: Predictably incredible earnings

While not having quite as large a market cap as Nvidia and Apple, other mega tech stocks in the U.S. are no slouches. For example, Microsoft is also as valuable as the entirety of Canada’s stock exchanges at $3.2 trillion. Alphabet and Meta clock in at $2.1 trillion and $1.5 trillion respectively. (All figures in this section are in U.S. dollars.)

Other Big Tech stock news highlights

Here’s what these companies announced this week.

Alphabet (GOOGL/NASDAQ): Earnings per share came in at $2.12 (versus $1.51 predicted) on revenues of $88.27 billion (versus $86.30 billion predicted).

Microsoft (MSFT/NASDAQ): Earnings per share of $3.30 (versus $3.10 predicted), and revenues of $65.59 billion (versus $64.51 predicted).

Meta (META/NASDAQ): Earnings per share coming in at $6.03 (versus $5.25 predicted) and revenues of $40.59 billion (versus $40.29 predicted).

All three companies crushed earning estimates across the board. However, shareholders’ reactions to these earnings beats were still muted. Meta shares were down 2.5% in after-hours trading on Wednesday, and it was a similar situation for Microsoft. Alphabet fared better as its shares were up 3%.

It’s hard to put these numbers into the massive context into which they belong, because the world has never seen anything like these companies before. Here are highlights from the earnings calls. (Scroll the chart left to right with your fingers or press shift, as you use scroll wheel on your mouse to read.)

Despite these setbacks, CPKC posted an income gain of 7% year over year. The four categories that made the most impact were grain, energy, plastics and chemicals, and they grew revenues by 11%. CPKC says the shipment of wheat to Mexico from the Canadian and American Prairies over the past 12 months was exactly the type of “synergy win” that it was hoping for when the former Canadian Pacific acquired Kansas City Southern back in 2021. This railway remains the only one to span Canada, the United States and Mexico.

CNR CEO Tracy Robinson commented on the railway’s operational challenges. “Our scheduled operating plan demonstrated its resilience in the third quarter, allowing us to adapt our operations to challenges posed by wildfires and prolonged labor issues,” she said. “Our operations recovered quickly and the railroad is running well. As we close 2024, we will continue to focus on recovering volumes, growth, and ensuring our resources are aligned to demand.”

CNR’s revenues were up 3% year over year; however, increased expenses meant the company’s operating ratio rose 1.1% to 63.1% (indicating that expenses are growing as a share of revenue). The railway announced it was raising its quarterly dividend from $0.79 to $0.845. This raise of nearly 7% is right in line with CNR’s mission to conservatively raise its dividend payouts each year.

Thursday’s revenue miss left some Rogers shareholders shaking their heads.

Rogers earnings highlights

Here’s what the large mobile company reported this week:

Rogers Communications (RCI/TSX): Earnings per share of $1.42 (versus $1.34 predicted) and revenues of $5.13 billion (versus $5.17 predicted).

While solid earnings numbers did take away some of the sting, Rogers’ share price was down 3% on Thursday. Lower-than-expected numbers for new wireless customers were at the root of low revenue growth. The oligopolistic Canadian wireless market remains uncharacteristically competitive as Rogers, Telus and Bell all continue to fight for market share. That competition is hurting profit margins for all three telecommunications giants at the moment. (Unlike in past years, when the three telcos all enjoyed charging some of the highest wireless plan fees in the world.)

One highlight for Rogers was its sports revenue vertical, which was up 11% from last quarter. Rogers has really doubled down on its sports media strategy over the last few years and now owns a controlling share of the:

Toronto Blue Jays in the Major League Baseball league (MLB)

Toronto Maple Leafs in the National Hockey League (NHL)

Toronto Raptors in the National Basketball Association (NBA)

Toronto FC in Major League Soccer (MLS)

Toronto Argonauts in the Canadian Football League (CFL)

SportsNet, a major Canadian sports network

Toronto’s Rogers Centre and Scotiabank Arena venues

Naming rights of sports venues in Edmonton, Toronto and Vancouver

National NHL media rights in Canada

Local media rights to the NHL’s Vancouver Canucks, Calgary Flames and Edmonton Oilers

Partial local media rights to the Maple Leafs and Raptors

Several minor-league franchises and esports (gaming) teams

Despite owning all those household-name sports assets, it’s worth noting that Rogers’ wireless and cable divisions were responsible for close to 90% of revenues, with sports and media making up the rest.

Netflix (NFLX/NASDAQ) shareholders were happy on Thursday, as they saw share prices rise 5% in after-hours trading on the back of another excellent earnings announcement. (All figures in U.S. dollars.) Earnings per share came in at $5.40 (versus $5.12 predicted) and revenues were $9.83 billion (versus $9.77 billion predicted).

Paid memberships also topped expectations, at 282.7 million, compared to the 282.15 million predicted by analysts. Netflix chalked up the increase in viewers to new hit shows such as The Perfect Couple, Nobody Wants This and Tokyo Swindlers, as well as new seasons of favourites Emily in Paris and Cobra Kai. Looking ahead to the next quarter, Netflix is banking on the new season of Squid Game and its foray into the world of live sports. Two National Football League (NFL) games and a massively anticipated boxing bout between Jake Paul and Mike Tyson represent new attractions for the streaming giant.

Photo courtesy of United Airlines

United Airlines shares take to the sky

Tuesday was a massive earnings day for United Airlines (UAL/NASDAQ) as earnings per share came in at $3.33, well outpacing the $3.17 that analysts were predicting. (All figures in U.S. dollars.) Revenues were $14.84 billion (versus $14.78 billion predicted). Shares were up more than 13% on the outperformance and the news that the airline was starting a $1.5-billion share buyback program.

Corporate revenue was up more than 13% year over year, while basic economy seat sales clocked an even more impressive 20% increase. Last week, the company announced new international routes headed to Mongolia, Senegal, Spain, Greenland and more.

The best online brokers in Canada

The inflation dragon has been slain

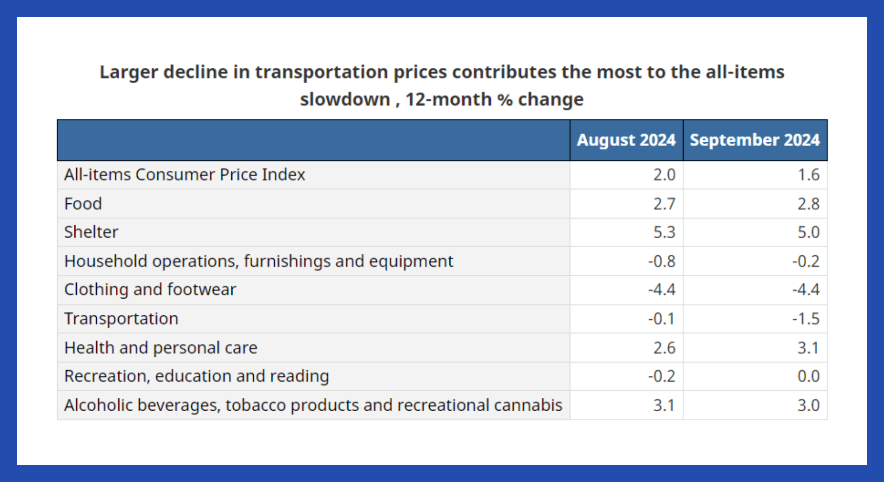

It doesn’t seem that long ago that annualized inflation rates were topping 8%, and there appeared to be no end in sight. Well, the end has arrived. Statistics Canada announced this week that the Consumer Price Index (CPI) annualized inflation rate for September had dropped all the way down to 1.6%. That’s substantially lower than the Bank of Canada’s 2% target.

Led by deflation in clothing and footwear, as well as transportation, the downward trend appears to be widespread. Gasoline was also down 10.7% from this time last year.

Of course, increased shelter costs remain the major concern for many Canadians. Rent increases were up 8.2% year-over-year; while that’s down from August’s figure of 8.9%, it’s still a bitter pill to swallow for many.

Morgan Stanley shares soared to all-time highs Wednesday after third-quarter beats on the bank’s top and bottom lines, with strength seen across the board. Revenue for the three months ended Sept. 30 increased nearly 16% year over year to $15.38 billion, outpacing expectations of $14.4 billion, according to estimates compiled by LSEG. Earnings per share (EPS) jumped over 36% versus the year-ago period to $1.88, exceeding the $1.58 expected, according to LSEG. MS YTD mountain Morgan Stanley YTD Club stock Morgan Stanley was up 7.5%. At one stage it was even higher, punching through our $120 price target. We are setting a new PT of $130 and keeping our wait-for-a-pullback 2 rating in deference to the stock’s hot streak — up over 13% from its July high before the August market swoon and up 33% from its Aug. 5 low. Bottom line This was as clean a quarter as anyone could have asked for. Morgan Stanley outpaced expectations in just about every aspect of each operating division and put up very strong quarterly results in terms of firmwide key performance indicators. Last quarter, when the results weren’t quite what we were looking for, we told members that patience was warranted, and we would likely see dynamics improve in wealth management — a key focus area for investors who want to see the bank’s durable fee-based revenue streams continue to grow. That’s exactly what we saw with Wednesday morning’s release. Investment banking also shined as it did for its rivals, including fellow Club name Wells Fargo , which saw its overall earnings report and commentary on Friday blow the doors off. Wells Fargo stock on Wednesday was trying to extend its winning streak to nine straight sessions. We continue to believe that the improvements we’re seeing at Morgan Stanley in terms of efficiency and disciplined execution will magnify the tailwinds of a resilient U.S. economy and stimulus activity internationally. Commentary Return on tangible common equity (ROTCE) is an important metric in valuing financial institutions, such as determining what multiple to put on tangible book value, which came in at $43.76 per share. Morgan Stanley’s third-quarter ROTCE of 17.5% blew away expectations of 14.8%, according to estimates compiled by Bloomberg. On a year-to-date basis, the bank has realized an 18.2% ROTCE. The common equity tier 1 (CET1) ratio, meanwhile, indicates a financial institution’s ability to return cash to shareholders via buybacks and dividend payments. For that reason, we’re very happy to see that stand at 15.1%. That’s a hair lower than the 15.3% the Street was expecting but not too concerning. Total client assets across wealth management and investment management have now exceeded $7.5 trillion, a nearly $1.4 trillion increase over what we saw a year ago as management continues to execute on its mission of reaching $10 trillion over the long term. The overall efficiency ratio , which is calculated by dividing total non-interest expenses by net revenue — so lower is better — came in well below expectations and declined 300 basis points versus the year-ago period – though importantly did not come at the cost of continued investments in the business. On the call, CFO Sharon Yeshaya noted that in addition to revenue growth, the efficiency ratio improvement was the result of “disciplined prioritization of our controllable spend.” Morgan Stanley repurchased $750 million worth of shares in the third quarter — 8 million shares total — at an average purchase price of $99.94 each, which in light of Wednesday stock price looks like a pretty good move for shareholders. Given its 15.1% CET1 ratio, Morgan Stanley has plenty of excess capital at its disposal to both continue investing in growth and return excess capital to shareholders. Morgan Stanley Why we own it : We own Morgan Stanley for the rebound taking place in IPO and M & A activity along with growth in wealth management, which provides more durable fee-based revenues. We also view the bank’s excess capital as supportive of further shareholder returns via buybacks and dividends while also providing for additional investments in growth. Competitors : Goldman Sachs Weight in Club portfolio : 3.5% Most recent buy : Oct. 18, 2023 Initiated : July 12, 2021 Segments Institutional Securities in the third quarter benefited from strong international performance, with management calling out an acceleration in activity exiting the quarter, indicating the fourth quarter was also off to a strong start. In line with our thesis, CEO Ted Pick noted on the call that “a broadening equity market and evolving interest rate policy are favorable backdrops for our markets businesses.” Morgan Stanley’s large footprint allowed the firm to benefit from “shifting expectations around the size and timing of the Fed’s first rate cut” during the quarter, the change in monetary policy at the Bank of Japan and Chinese stimulus. Investment banking saw a pick-up in equity underwriting due to higher IPO activity and fixed income underwriting increased significantly from a year ago. Wealth management reported record revenue and a record pre-tax profit. Net new assets in the quarter were about $64 billion, well above the $53.5 billion expected and brings year-to-date net new assets to $195 billion, a 5% annualized increase versus where we started the year. Yeshaya said that “year-to-date flows are on pace to exceed last year, supported by an ongoing contribution of assets from advisor-led brokerage accounts to fee-based accounts.” The CFO expects net interest income “to be modestly down from the third quarter results largely on the back of lower rate expectations consistent with the forward curve.” That’s not too much of a concern given the Street has been looking for about $1.73 billion of net interest income in the current quarter. The pre-tax profit margin of 28.3%, a key watch item for investors given the increased focus on fee-based performance, outpaced the 26.8% consensus estimate and represents a very strong sequential increase versus the 26.8% we saw in the prior quarter. Investment management got a boost from higher asset management and related fees, which came on the back of an increase in assets under management. On the call, Yeshaya highlighted the benefits of the prior acquisition of Eaton Vance. (Jim Cramer’s Charitable Trust is long MS, WFC. See here for a full list of the stocks.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

Bing Guan | Bloomberg | Getty Images

Morgan Stanley shares soared to all-time highs Wednesday after third-quarter beats on the bank’s top and bottom lines, with strength seen across the board.

For a decade now, big acquisitions by Canadian oil-and-gas producers have mostly been met with distaste by investors. So we’ll take it as a heartening sign how well the markets received Canadian Natural Resources’ (CNQ/TSX) decision to buy the Alberta upstream assets of Chevron Corp. (CVX/NYSE) for USD$6.5 billion in cash. CNQ stock rose 3.7% Monday in the wake of the announcement. Chevron was up 0.7% on a day when oil prices increased.

The assets in question comprise a 20% stake in the Athabasca Oil Sands Project, along with 70% of the Kaybob Duvernay shale play. That should add 122,500 barrels of oil equivalent per day to Canadian Natural Resource’s 2025 output, the company said. It also announced a 7% bump to its quarterly dividend, to 56.25 Canadian cents a share, beginning in January.

Chevron explained the asset sale in terms of freeing up cash for U.S. shale acquisitions as well as targeted positions abroad, such as in Kazakhstan, which it considers to hold better long-term profit potential.

Canada’s best dividend stocks

Nvidia moves up to number 2 in market cap

Reports of the death of the Magnificent 7 tech stocks’ decade-long run are greatly exaggerated, Nvidia (NVDA/Nasdaq) seemed to say this week as its shares rose past $130. (All figures in U.S. dollars.) That pushed its market capitalization ahead of Microsoft Corp. to $3.19 trillion. That leaves only Apple, with a market cap of $3.4 trillion, worth more than the AI-focused chip-maker.

Nvidia’s stock is up 26% in the past month, compared to a 6% advance for the S&P 500. Nvidia has grown tenfold in just two years. The price movement this week appeared to come from a positive report from Super Micro Computer, a provider of advanced server products and services. It found that sales of its liquid cooling products, deployed alongside Nvidia’s graphics processing units (GPUs), would be even stronger than expected this quarter. Analyst estimates of Nvidia’s adjusted EBITDA (earnings before interest, taxes, depreciation and amortization) for the three-month period ended this month is $21.9 billion.

The best online brokers in Canada

Pepsi earnings leave a sour taste

Posting its second straight disappointing set of quarterly results on Tuesday, beverage-and-snack maker PepsiCo lowered its full-year guidance for organic revenue unrelated to acquisitions.

Results were hampered by recalls of the company’s Quaker Foods products, related to potential salmonella contamination. PepsiCo also experienced weak demand in the U.S. and business disruptions in some overseas markets, such as the Middle East. Pepsi’s North American beverage volumes fell 3% year-over-year, mostly due to declines in energy drink sales. Meanwhile, its Frito-Lay division suffered a 1.5% decline.

“After outperforming packaged food categories in previous years, salty and savory snacks have underperformed year-to-date,” executives said in a prepared statement. Overall, PepsiCo revised its 2024 sales growth outlook from the previous 4% to low single digits.

Some experts speculate the real sticking point in negotiations isn’t about wages but protection from automation. The ILA refused to allow its members to work on automated vessels docking at U.S. ports. As a result, American ports are getting more and more inefficient, ranking not only behind ports in China, but also Colombo, Sri Lanka. (The Container Port Performance Index is put together annually by The World Bank and S&P Global Market Intelligence.)

For reference, the highest-rated port in Canada is Halifax, listed at 108th in the world. Halifax’s port efficiency was well behind not only Sri Lanka, but also economic powerhouses like Tripoli, Lebanon. To give further Canadian context, Montreal is 348th, and Vancouver is 356th, which is just ahead of Benghazi, Libya.

Something tells me that negotiating for USD$300,000-per-year dockworkers is not going to help these North American efficiency numbers. The higher salaries get, the more attractive automation strategies will quickly become. Clearly there will be an eventual reckoning. In the meantime, for at least one more important presidential news cycle, dockworkers will be able to extract large wage gains as they hold the broader economy hostage.

Why utilities aren’t “boring”—any more

As income-oriented Canadian investors start to grow less enamoured of high-interest savings accounts and guaranteed investment certificates (GICs), the dividend yields of dependable North American utility stocks should begin to look more attractive. Given how quickly interest rates are likely to fall, it’s clear that there is a stampede of investors heading for the stocks of utility companies.

The iShares U.S. Utilities ETF (IDU/NYSE) is up more than 30% year to date, and the iShares S&P/TSX Capped Utilities Index ETF (XUT/TSX) is up about 15% year to date. (Check out MoneySense’s ETF screener for Canadian investors.)

Most of the time utilities (especially those in sectors regulated by federal and local governments) are perceived as “boring.” Sure, the profits are dependable, but if the government is going to determine how much is paid for electricity or natural gas, then a company’s profit margins are tough to change. The dividend income is dependable. But that’s really the whole sales job in a nutshell.

Lately, however, due to AI’s electricity needs and possible AI-fuelled efficiency increases, utilities have been getting some glowing press. Falling interest rates mean that annual interest costs will drop (utilities often have to borrow a lot of money to complete big projects). Meanwhile, Canadian investors looking for safe cash flow are pouring in. Utility stocks make up about 4% of the S&P/TSX Composite Index. The largest utility companies—such as Fortis, Emera, Hydro-One and Brookfield Infrastructure—are some of Canada’s largest companies.

Some of the same income-oriented investors who like utility stocks may also be interested in two new exchange-traded funds (ETFs) that J.P. Morgan Asset Management Canada just launched. The JPMorgan US Equity Premium Income Active ETF (JEPI/TSX) and the JPMorgan Nasdaq Equity Premium Income Active ETF (JEPQ) use options strategies to “juice” the income already provided by higher-dividend-yielding stocks.

The Chinese government commands the economy to grow

Many people like to sort countries’ economies as either communist, socialist, capitalist or free markets. But these days, every country has some version of a mixed economy. The practical implementation of fiscal and monetary policy is becoming increasingly more grey than our old black-and-white economics textbooks would have us believe. Yet, even within the grey, China’s approach for its economic system is uniquely difficult to define.

Back in 1962, when asked about building a socialist market economy, future China leader Deng Xiaoping famously said, “It doesn’t matter whether the cat is black or white, so long as it catches mice.”

Well, the current China leaders have let the fiscal and monetary cats out of the bag, and they’re hoping those cats are hungry.

We wrote about China’s housing problems about a year ago, warning about rising deflation fears. These issues seem to have gotten worse, and the biggest news in world markets this week was that China’s government decided enough was enough. And in a “command” economy (which is probably the most accurate way to describe its approach), the government has a very high degree of control over economic levers. Consequently, markets reacted swiftly and positively to this news.

Here are the highlights of the multi-pronged fiscal and monetary stimulus that the Chinese government has decided to implement:

Banks cut the amount of cash they need in reserve (this is known as the reservation requirement ratio) by 0.50%. This will incentivize banks to lend more money (basically “creating” 1 trillion yuan, USD$142 billion).

The People’s Bank of China (PBOC) Governor Pan Gongsheng said another cut may come later in 2024.

Interest rates for mortgages and minimum down payments on homes were cut.

A USD$71 billion fund was created for buying Chinese stocks.

That last point is pretty interesting to me. Here you have a supposedly communist government essentially creating a big pot of money to spend within a free stock market. The fund is to directly purchase stocks, as well as providing cash to Chinese companies to execute stock buybacks. Good luck defining that action in traditional economic terms.

The idea is to give investors and consumers faith that they should go out there and buy or invest in China’s expanding economy. Clearly something major had to be done to jolt Chinese consumers out of their malaise.

Early reports are speculating that the Chinese gross domestic product (GDP) could fail to rise by less than the 5% target set by the government. If so, we’re about to see what happens when the commander(s) behind a command economy decide that the GDP will rise no matter what.

Invesco AAA CLO Floating Rate Note ETF (BATS:ICLO – Get Free Report) declared a dividend on Friday, September 20th, NASDAQ reports. Shareholders of record on Monday, September 23rd will be given a dividend of 0.1614 per share on Friday, September 27th. The ex-dividend date is Monday, September 23rd. This is an increase from Invesco AAA CLO Floating Rate Note ETF’s previous dividend of $0.15.

ICLO stock traded up $0.02 during mid-day trading on Friday, reaching $25.77. 67,338 shares of the company traded hands. The company has a fifty day simple moving average of $25.68 and a 200 day simple moving average of $25.67.

The Invesco Aaa Clo Floating Rate Note ETF (ICLO) is an exchange-traded fund that mostly invests in investment grade fixed income. The fund is actively managed to invest in USD-denominated floating rate CLOs that are rated AAA or equivalent. ICLO was launched on Dec 9, 2022 and is managed by Invesco.

Read More

Receive News & Ratings for Invesco AAA CLO Floating Rate Note ETF Daily – Enter your email address below to receive a concise daily summary of the latest news and analysts’ ratings for Invesco AAA CLO Floating Rate Note ETF and related companies with MarketBeat.com’s FREE daily email newsletter.

U.S. Fed cuts rates for the first time in four years

The U.S. dollar remains the most important currency in the world, and the American economy is arguably the most important financial system as well. Consequently, when the U.S. Federal Reserve makes a big announcement, it creates an economic wave that ripples everywhere. That’s why Wednesday’s decision to cut the key overnight borrowing rate by 0.50% is a very big deal.

Many speculated the U.S. Fed would begin cutting rates this week, but it was generally thought it would go with a 0.25% drop to begin an interest rate-cut cycle. The 50 basis points cut lowers the federal funds rate range 4.75% to 5%.

The U.S. Fed announced in a statement: “The Committee has gained greater confidence that inflation is moving sustainably toward 2%, and judges that the risks to achieving its employment and inflation goals are roughly in balance.”

Federal Reserve Chair Jerome Powell said, “We’re trying to achieve a situation where we restore price stability without the kind of painful increase in unemployment that has come sometimes with this inflation. That’s what we’re trying to do, and I think you could take today’s action as a sign of our strong commitment to achieve that goal.”

Immediately after the news of the U.S.’s first interest rate cuts in four years, major stock market indices responded with a brief jump on Wednesday. But they ended the day nearly flat. That seemed to be a bit of a delayed reaction from investors, as the Bulls returned Thursday with Nasdaq soaring 2.5% and the Dow leaping 1.3% to pass 42,000 for the first time ever.

Notably, former U.S. President Donald J. Trump continued to criticize the monetary decisions made by the U.S. Federal Reserve. This despite centuries of financial wisdom telling us that politicians getting involved in short-term monetary policy is a bad idea. (See: Turkey – Erdoğan, Tayyip.) At bitcoin bar PubKey on Wednesday, Trump said, “The economy would be very bad, or they’re playing politics.”

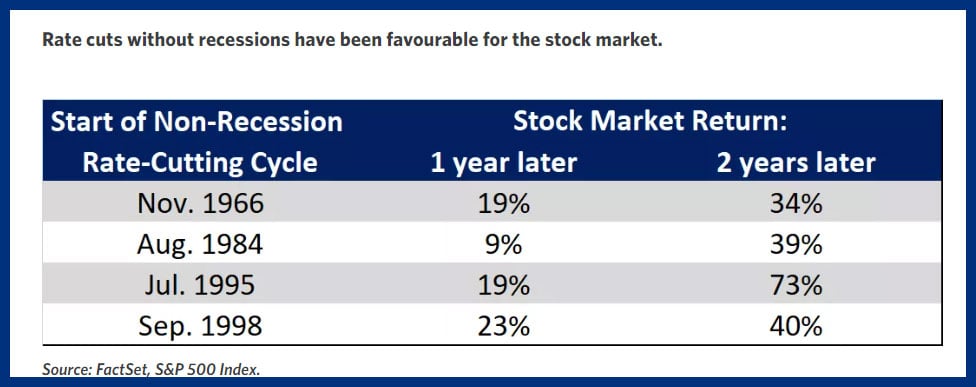

The larger-than-expected rate cut left some commentators questioning if this action would spook the markets. But, if the U.S. Fed manages to thread the needle and cut rates without a recession, it could be a good thing. The historical precedents are very positive for shareholders.

This large rate cut helps ease pressures on emerging markets that borrowed in U.S. dollars. And, it takes some of the pressure off other central banks around the world that didn’t want to see their currencies devalued too much relative to the mighty USD.

Tuesday’s earnings call was the best day that Oracle shareholders have seen in a while.

Oracle earnings highlights

All figures in U.S. currency in this section.

Oracle (ORCL/NYSE): Earnings per share came in at $1.39 (versus $1.32 predicted), and revenues of $13.31 billion (versus $13.23 billion predicted).

Share prices rose more than 13% after the tech giant showed profits that were up nearly 20% from last year. Revenues across the company’s cloud services division continue to increase. And CEO Safra Catz said, “I will say that demand is still outstripping supply. But I can live with that.”

Founder Larry Ellison (who recently passed Mark Zuckerberg to become the second richest person in the world) excitedly predicted that Oracle would one day operate more than 2,000 data centres, which is up from the 162 today. The current project that he highlighted is a massive data centre that will use three modular nuclear reactors to produce the needed gigawatts of electricity.

In other U.S. stock market news, Trump Media and Technology Group (DJT/NASDAQ) investors face a big decision this week. The stock plummeted from highs of $66 per share on March 27, to $16.56 after the debate on Wednesday. Don’t say we didn’t warn you.

That’s not the worst news for DJT investors though. Next week, a potentially crippling event occurs: the entity that owns 57% of the shares can sell the stock for the first time. If it were to sell all its shares (in order to get as much money as possible out of a business venture that loses millions of dollars every month), the share price would tank.

What is the “entity”? It’s actually a question of who not what: Donald Trump.

Even at reduced share price levels, Trump’s slice of Truth Social is worth about $1.9 billion. It’s not like he needs money for pressing issues or anything like that…

Dell and Palantir kick American Airlines and Etsy out of the S&P 500

In other big events to look forward to, September 23 will see major U.S. market indices experience a reweighting. Given that trillions of dollars are now passively invested into indice-based index funds, whether your company is a member of a specific index or not can make a big difference in its share price. That said, these indice moves are largely anticipated by the market, so a lot of the value movement has already been priced in.

For the third straight month, the Bank of Canada (BoC) decided to cut interest rates. The quarter-point cut takes the Bank’s key interest rate down to 4.25%.

The news that’s perhaps bigger than the widely anticipated rate cut was how aggressive BoC governor Tiff Macklem sounded in his prepared remarks. Macklem stated, “If we need to take a bigger step, we’re prepared to take a bigger step.” That sentence will be focused on by financial markets looking to price in larger potential cuts in the months to come. As of Thursday, financial markets were predicting a 93% probability that October would see another 0.25% rate cut. Several economists believe interest rates would fall to around 3% by next summer.

While describing a potential soft landing to the bumpy pandemic-fuelled inflation flight we’ve been on, Macklem stated, “The runway’s in sight, but we have not landed it yet.” It appears that the real debate is no longer if the BoC should cut interest rates, but instead, how quickly it should cut them, and whether a 0.50% cut may be in the cards sooner rather than later.

With unemployment rates increasing, it follows that the inflation rate of labour-intensive services should continue to fall. Lower variable-rate mortgage interest payments will automatically have a deflationary impact on shelter costs across Canada as well.

Last week we wrote about the Alimentation Couche-Tard (ATD/TSX) proposed buyout of 7-Eleven parent company Seven & i Holdings Co. If the buyout goes through, ATD would go from being Canada’s 14th-largest company to being in the running for third-largest company. That’s a big if: on Friday morning, just hours before we went to press, Seven & i said it is rejecting ATD’s $38.5-billion cash bid on the grounds it was not in the best interests of shareholders and was likely to face major anti-trust challenges in the U.S. (All figures in this section are in U.S. dollars.)

It’s interesting to note that 7-Eleven has been much better at running convenience stores in Japan (where it has a 38% profit margin) versus outside of Japan (where it has a 4% margin). That’s partly due to the fact that locations outside of Japan sell a large amount of low-margin gasoline. Couche-Tard, however, has been able to unlock margins in the 8% range in similar gasoline-dominated locations, indicating substantial room for growth. With 7-Eleven’s overall returns falling far behind its Japanese benchmark index over the last eight years, there is clearly a business case to be made to current shareholders.

The political dimensions to the acquisition are much harder to quantify than the business case. While Japan did change its laws to become more foreign-acquisition-friendly in 2023, it still classifies companies as “core,” “non-core” and “protected,” under the Foreign Exchange and Foreign Trade Act. Logically, it seems that a convenience-store company would fit the textbook definition of “non-core.” However, Seven & i Holdings has asked the government to change the classification of its corporation to “core” or “protected.” That would effectively kill any wholesale acquisition opportunities.

There is also an American legal aspect to the deal. The Federal Trade Commission (FTC) would have to rule on whether ATD’s resulting U.S. market share of 13% would be too dominant. Barry Schwartz, chief investment officer and portfolio manager at Baskin Wealth Management, speculated that the most likely outcome might be a sale of 7-Eleven’s overseas assets to ATD, with the company holding on to its Japan-based assets.

Because I grew up in near Winnipeg, the Slurpee Capital of the World, I thought I knew everything the 7-Eleven universe had to offer. Then, I visited Japan and Thailand last year. I realized that I hadn’t seen anything yet. (All figures in U.S. dollars in this section.)

In much of Thailand and Japan (among other places in Asia), the convenience store is a daily touchstone stop. In Tokyo, there are more than 3,000 7-Eleven stores, a large part of the country’s 56,000-plus convenience store locations. While 7-Eleven was a big part of my childhood, it pales in comparison to the role it plays within many Asian communities.

So, it quickly caught my attention when Canadian corporate darling Alimentation Couche-Tard (ATD/TSX) announced it was making a friendly takeover bid for Tokyo-based Seven & I Holdings Co (SVNDY/NIKKEI). The possible deal is historic for many reasons.

The acquisition of Seven & I Holdings Co is the largest-ever Japanese target of a foreign buyer.

It’s the first test of new 2023 takeover rules by Japan’s Ministry of Economy, Trade and Industry (METI), designed to make foreign acquisitions more welcoming and Japanese companies more internationally competitive.

It would likely top Enbridge’s $28 billion acquisition of Spectra Energy Corp back in 2016, to become Canada’s largest-ever corporate takeover.

It would combine Couche-Tarde’s convenience store empire of 16,700 stores in 31 countries, with 7-Eleven’s 85,800 stores in 19 countries.

By combining ATD’s and 7-Eleven’s U.S. market share, Couche-Tard would control more than 12% of the U.S. convenience store market, with the closest competitor being Casey’s General Stores at only 1.7%.

It’s a massive bite to take for ATD, currently valued at about $56 billion, since 7-Eleven is currently worth about $38 billion.

The potential acquisition is so large that many analysts believe ATD would have to raise $18 billion in new equity to complete the deal. That would be the biggest stock offering in Canada by a wide margin. It would also be in addition to the $2 billion in cash on hand ATD has, and its ability to borrow about $20 billion. There’s speculation that Canadian pension plans would be a key source of capital in order to get a deal done.

Neither company disclosed the precise terms of the deal, but Couche-Tard described the offer as “friendly, non-binding.” That’s a key differentiator from a “hostile takeover.” (A hostile takeover is when a company tries to purchase more than half of another company’s shares on the free market against the wishes of the targeted company’s management, thus taking over operational control.)

This move is not totally out of the blue for ATD, as the company has taken big acquisitional swings before. The Quebec-based operator has a long history of successfully integrating new acquisitions. Its attempt three years ago to purchase French grocery chain Carrefour for $25 billion was scuttled at the last minute by the French Finance Minister citing food security issues. Similar protectionist governmental instincts could prevent this massive deal from getting done.

That said, Couche-Tard has been circling (Circle K-ing?) 7-Eleven for over two years now. Perhaps it believes it has what it takes to navigate the new Japanese corporate legal waters and get the deal done.

While there will likely be some nervous customers of 7-Eleven (nobody wants to see change at their favourite corner store), Seven & I Holdings’ shareholders must be happy. Shares were up 22% upon announcement of the proposed acquisition.

1900 vs. 2023 stock markets

It’s always worth keeping the long run in mind when thinking about trends and market forces. When we consider just what an incredible run the U.S. stock market has achieved over the last few years, it’s important to remember that it’s unlikely to continue that outperformance forevermore.

Utilities – a staple of retirees’ portfolios for their steady dividends – are emerging as a hot corner of the market in 2024, and UBS is highlighting the group as a “most preferred” sector in August. Publicly-traded utility stocks have surged nearly 19% in 2024, behind only information technology and communications services as investors look to utilities as another way to play the artificial intelligence trend. What’s more, their dividend yields will grow more attractive if Treasury yields fall, and their borrowing costs will grow less burdensome if the Fed cuts interest rates, as is widely expected. .GSPU YTD mountain The S & P 500 Utilities Sector in 2024 In the third quarter, utilities have stood out, climbing 10%, through Friday. That compares to a 0.5% advance from tech and a decline of more than 2% for communications services. Electricity demand is expected to grow as much as 20% by 2030, with AI data centers adding an estimated 323 terawatt hours of power demand by then, according to an April analysis from Wells Fargo. To play the trend, UBS strategist James Dobson called out NextEra Energy as a “top pick” among utilities, according to a report last week from the bank’s Chief Investment Office, Global Wealth Management. Shares of NextEra, parent of Florida Power & Light and NextEra Energy Resources, are up 31% in 2024 and yield 2.6%. “With distinct competitive advantages in renewable development in the U.S. and an attractive valuation, we believe NEE can outperform the sector over the next 12 months,” Dobson wrote. He noted that the company is “exceedingly well positioned” to benefit from rising demand for power related to AI data centers, reshoring and electrification. Indeed, NextEra Energy Resources, which operates wind and solar projects, added more than 3,000 megawatts of new renewable power and storage projects to its backlog in the second quarter, including agreements with Google to provide 860 megawatts to data centers, NextEra CEO John Ketchum said on a July 24 earnings call. UBS isn’t alone in recommending NextEra Energy. Sixteen of the 23 analysts covering the stock rate it a buy or strong buy, according to LSEG, but consensus price targets see only about 3% upside from current levels. Dobson and his team dropped Vistra , which provides power in Texas, from the firm’s “top picks” list, although it continues to be labeled “most preferred.” Shares of Vistra have rocketed nearly 123% in 2024, but they’re about flat in the third quarter. The company offers a modest dividend yield of 1%. “As an independent power producer, VST has fewer defensive attributes relative to other regulated utilities in the sector,” UBS noted in its report. Independent power producers aren’t public utilities, so they are less regulated. Rather, they generate power to sell to other customers, including other utilities and end users. Nevertheless, the stock is highly favored on Wall Street, with roughly 92% of the analysts covering Vistra rating it a buy or strong buy, according to LSEG. Analyst consensus price targets are calling for nearly 29% upside from current prices.

On Tuesday, Statistics Canada stated that the Consumer Price Index (CPI) measured inflation of 2.5% for July. That’s down from 2.7% in June, and is the lowest inflation rate recorded since 2021.

Deceleration in headline inflation led by shelter component , 12-month % change

CPI basket items

June 2024

July 2024

All-items Consumer Price Index

2.7%

2.5%

Food

2.8%

2.7%

Shelter

6.2%

5.7%

Household operations, furnishings and equipment

-0.9%

-0.1%

Clothing and footwear

-3.1%

-2.7%

Transportation

2%

2%

Health and personal care

3.0%

2.9%

Recreation, education and reading

0.6%

-0.2%

Alcoholic beverages, tobacco products and recreational cannabis

In fact, if you take shelter out of the equation, we’re getting close to zero inflation. And that’s significant for two reasons:

The shelter-inflation rate (primarily a measurement of rent and mortgage expenses) did come down substantially between June and July.

As the Bank of Canada (BoC) cuts interest rates, the inflation component of the CPI will inevitably go down as Canadians will have access to mortgages with lower rates.

Notably, passenger vehicle prices were down 1.4% in July. Clothing and footwear was also down by 2.7%. Food and gas were up by 2.7% and 1.9% respectively. British Columbia and New Brunswick had the highest inflation rate growth, while Manitoba and Saksatchewan had the lowest.

It’s pretty clear there’s no longer an overall inflation crisis in Canada. It’s now simply a home affordability issue at this point. Economists were widely predicting that this continuing trend of a downward inflation rate would clear the way for continued interest-rate cuts in the coming months. Money markets are now predicting a 0.25% cut minimum on September 4, with a 4% probability that the cut will be 0.50%. Looking further down the road, those same markets are predicting there is a 76% chance we will see a 2% decrease by October of 2025.

Target Corporation posted a big earnings beat on Wednesday and shareholders saw its shares increase in value by 11.20%. The Minneapolis-based discount retailer is the seventh-largest in the U.S.

Retail earnings highlights

All numbers are in U.S. dollars.

Target (TGT/NYSE): Earnings per share of $2.57 (versus $2.18 predicted). Revenue of $25.45 billion (versus $25.21 billion estimate).

Lowe’s Companies (LOW/NYSE): Earnings per share of $4.10 (versus $3.97 predicted), and revenues of $23.59 billion (versus $23.91 billion predicted).

Same-store sales for Target grew 3% last quarter, after five straight quarters of declining sales. More purchases of discretionary items like clothing were responsible for the positive reversal to the declining sales trend.

Target’s COO Michael Fiddelke had a very cautious tone, though. “While we’ve been pleased with our performance so far this year, our view of the consumer remains largely the same. The range of possibilities and the macroeconomic backdrop in consumer data and in our business remains unusually high.” And Target CEO Brian Cornell cited price reductions and a value-seeking consumer as reasons for increased foot traffic in the quarter.

It was very much a mediocre earnings report for Lowes, though, as it beat earnings expectations decisively but cut its full-year forecast. Shares were down by about 1% on Tuesday after the earnings announcement.

Lowe’s CEO Marvin Ellison said consumers were waiting for cuts in interest rates before taking on large home improvement projects. Because 90% of Lowes’ customers are homeowners (as opposed to contractors), they are particularly sensitive to movements in interest rates, he shared. Same-store sales were down 5.1% year over year.