The bank said Thursday it will now pay a quarterly dividend of $1.42 per share, an increase of four cents. It also said it plans to buy back up to 30 million of its shares.

The moves came as RBC said it earned $3.95 billion or $2.74 per diluted share for the quarter ended April 30, up from $3.68 billion or $2.60 per diluted share a year earlier, helped in part by record capital markets revenue.

“This quarter, we saw strong growth across diversified revenue streams,” said chief executive Dave McKay on an earnings call.

He said the bank’s capital generation means it has options ahead for growth, including potential acquisitions, even as the bank returns more money to shareholders.

“This enormous capital that we are generating gives us significant strategic flexibility inorganically.”

The bank also has a wide range of growth options within the bank now, including making the most of its $13.5-billion HSBC Canada acquisition.

End of uncertainty for former HSBC employees

The roughly 4,500 employees RBC took on with the acquisition are now free from the uncertainty around the deal, and the barriers it posed to bringing on clients, he said.

“They’ve been on the defence for 18 months, and now we’re on the offence and you can see the excitement in their eyes to get back,” said McKay.

A stock split divides existing shares into smaller pieces. So, if you previously had one share of Nvidia worth $1,000, you would now have 10 shares of Nvidia each worth $100, for an unchanged total value of $1,000. Stock splits are a way for companies to ensure that investors can easily buy and sell single shares.

The massive hype behind Nvidia has resulted in a price-to-earnings ratio of over 55x. By comparison, tech giants Microsoft and Apple currently have ratios of 36x and 29x, respectively. Conventional logic says Nvidia’s growth has to fall back into line at some point—but this sustained period of record earnings is tough to argue with for the moment. Nvidia made 18% more money in Q1 2024 than it did in Q4 2023, and it made a whopping 262% more money than it did in Q1 2023.

Founder and CEO Jensen Huang sounded appropriately upbeat in stating, “The next industrial revolution has begun—companies and countries are partnering with Nvidia … to produce a new commodity: artificial intelligence.”

Nvidia bought back $7.7 billion worth of its shares in Q1 and announced it was increasing its dividend from four cents to 10 cents per share (on a pre-split basis).

Frankly, I think it’s just a matter of time until competitors start to close the gap with Nvidia and some of those juicy profit margins start to shrink. That said, there is a whole lot of money to be made while that process plays out. Clearly, investors are willing to pay a premium for Nvidia’s future earnings.

Target (TGT/NYSE): Earnings per share of $2.03 (versus $2.06 predicted), and revenue of $24.53 billion (versus $24.52 billion estimated).

Macy’s (M/NYSE): Earnings per share of $0.27 (versus $0.15 predicted), and revenue of $4.85 billion (versus $4.86 billion estimated).

Lowe’s (LOW/NYSE): Earnings per share of $3.06 (versus $2.94 predicted), and revenue of $21.36 billion (versus $21.12 billion estimated).

All three of these retail heavy hitters cited a stretched consumer as the main reason for mediocre quarterly earnings reports. Target CEO Brian Cornell explained that low sales numbers reflected “continued soft trends in discretionary categories.” Compared to its rival Walmart, Target has substantially fewer customers coming into its stores to buy groceries, so the consumer shift to necessities appears to be hitting it harder.

Lowe’s CEO Marvin Ellison had similar thoughts on the current retail scene, saying, “Interest rates can go down, but you still need consumer confidence to come up.” Macy’s CFO and COO Adrian Mitchell went so far as to say that its team expects consumers “will remain under pressure for the balance of the year.”

Rainey went on to comment on the state of American consumers. While “wallets are still stretched,” it was also the case that “even the low-income consumer seems to be holding in there pretty well,” he said. He also added that shoppers were still coming to Walmart to buy necessities like food and health-related items, along with less general merchandise (such as home goods and electronics).

Going forward, Walmart is banking for growth on new revenue drivers, such as its subscription program, Walmart+. Global advertising grew 24% in Q1 and will be an interesting supplemental line of business for the company going forward—as it has been for retail rival Amazon.

In less celebratory news, Walmart has plans to streamline its store offerings by shuttering Walmart health clinics in American locations.

Given that consumers continue to cut back on home renovations after the massive COVID reno-boom, it stands to reason that Home Depot shareholders might be in for a bit of a sideways run for a while.

On Monday, the company revealed that while it was reporting its worst revenue miss in two decades, its bottom line was still holding up pretty well. Shares were mostly flat on the week.

For those who haven’t watched Dumb Money or Eat The Rich (excellent airplane flicks btw), GameStop stock is the iconic “meme stock.”

What is a meme stock?

A meme stock is an equity that sees growth instigated by internet memes—usually not based on earnings or value. To sum it up: GameStop is a semi-dying company that appears unlikely to make a profit in the foreseeable future. Consequently, it doesn’t make a lot of sense (according to traditional investing metrics) to pay a high price for GameStop stock. However, speculative bets on where its price could move can quickly make investors money (or make them lose it) quite quickly. Investors who short sell GameStop’s stock are essentially betting that the price will continue to go down. If enough people buy shares of GameStop, those short bets against its share price can cost those investors a ton of money.

Real estate stocks have become oversold and that has presented an opportunity for investors, according to BMO. In fact, since the group has been a part of the S & P 500 , there have only been a handful of other times where the stocks have performed worse relative to the index on a year-over-year basis, chief investment strategist Brian Belski wrote in a note Tuesday. Real estate is the only S & P 500 sector that is in the red this year, off 6%. “According to our work, this type of abnormal underperformance has typically proved to be an inflection point historically,” Belski said. “[We] believe the sector is poised for a turnaround in the coming months and are recommending that investors use its current weakness as a dip buying opportunity,” he added. .SPLRCR YTD mountain S & P 500 Real Estate Sector year to date BMO identified four other periods of this abnormal underperformance. In the year following such troughs, real estate investment trusts outperformed the S & P 500 by about 17%, on average. Belski thinks the stocks have also been unfairly punished in response to interest rate trends. While historically their relative performance has fared somewhat better during periods of falling interest rates, they have also managed to outperform in a higher rate environment, he said. Fundamentals also appear supportive, according to Belski. “Free cash flow yields for REITs continue to go up, with debt going down,” he said in an interview on ” Squawk on the Street ” on Thursday. “Payouts are going up as well.” Here are some of the REITs BMO rates as outperform. They also pay dividends, so investors can earn some income while they wait for a rebound. Investors can snag a 6.4% dividend yield with Boston Properties . The company develops, owns and manages workspaces across the country, including in New York and San Francisco. Office REITs suffered from the Covid-19 pandemic work-from-home trend and a slow return to the office. However, that is now shifting, Belski pointed out. “Everyone is working. We are coming back to work again,” he told CNBC. “The death of commercial real estate is way, way precluded. I think people predicted that way too early.” Shares are down nearly 13% year to date and have about 27% upside to BMO’s price target. Meanwhile, data center REIT Equinix just saw its stock rally more than 11% on Thursday, fueled by an earnings beat. “The rapidly evolving AI landscape continues to serve as a catalyst for economic expansion, creating immense potential for Equinix as our customers recognize the importance of digital initiatives in driving long-term revenue growth and operational efficiency,” Equinix president and CEO Charles Meyers said in a statement. Shares have lost about 6% so far this year and have about 25% upside to BMO’s price target. It has a 2.3% dividend yield. Ventas is also down about 4% year to date. The company’s portfolio includes senior housing communities, which stand to benefit from the aging population . The last of the baby boomers will turn 65 in 2030 , according to the U.S. Census Bureau. The stock, which yields 3.8%, has roughly 7% upside to BMO’s price target. Lastly, Host Hotels & Resorts , which owns luxury and upper-upscale hotels, has a 4.4% dividend yield and is down nearly 6% so far this year. It also has about 25% upside to BMO’s price target. Earlier this month, the company reported adjusted funds from operations for the first quarter that topped estimates. It also posted a revenue beat and upped its full-year funds-from-operations and revenue guidance.

When countries look to attract the attention of big financial funds, they often attempt to brand themselves in a manner that will bring much-needed foreign investment to their shores. For example, you might see buzzwords such as:

Innovative

Efficient

Attractive

Shareholder-friendly

But given Canada’s stagnating economy, I think it’s appropriate to get excited about this Warren Buffett quote:

“We do not feel uncomfortable in any shape or form putting our money into Canada.”

When Buffett takes the stage at his annual “Woodstock for capitalists” in Omaha each year, the investing world sits up to take notice. So, it was noteworthy to hear his lukewarm notes about Canada, including:

“There are a lot of countries we don’t understand at all. So, Canada, it’s terrific when you’ve got a major economy, not the size of the U.S., but a major economy that you feel confident about operating there. … Obviously, there aren’t as many big companies up there as there are in the United States. There are things we actually can do fairly well that Canada could benefit from Berkshire’s participation.”

He went on to reveal his company’s possible Canadian strategy, saying, “In fact, we’re actually looking at one thing now.” While most other investors are cool on Canadian stocks, it’s interesting to see Buffett warm (again).

Buffett’s last major foray into Canada generated a massive 70% gain in a single year back in 2017 when he invested in Home Capital Group, so he may know a thing or two about making money in the Great White North.

Other highlights from the annual general meeting included (all figures in U.S. dollars):

Buffett’s company, Berkshire Hathaway (BRK.A/NYSE) is currently benefiting from high interest rates, as it sits on a massive cash hoard of $189 billion.

Berkshire sold about $39 billion worth of Apple stock during the quarter. Berkshire remains Apple’s single biggest shareholder with over $135 billion still invested.

In the absence of big deals, Berkshire continues to reward its shareholders by buying back its own shares to the tune of $2.6 billion for the quarter. When asked why he hadn’t used the cash to make big, flashy investments, Buffett responded, “I don’t think anyone sitting at this table has any idea how to use it effectively, and therefore we don’t use it. We only swing at pitches we like.”

Berkshire’s operating profit rocketed up 39% on a year-over-year basis.

Underwriting profits at Buffett’s insurance companies were up 185% year-over-year to $2.6 billion.

Buffett told the audience that he had sold all of Berkshire’s remaining Paramount Global shares and was refreshingly honest in admitting, “It was 100% my decision, and we’ve sold it all and we lost quite a bit of money.”

Buffett wrapped up the annual meeting by saying humbly, “I not only hope you come next year, [but] I hope I come next year.” He later added, “I know a little about actuarial tables,” in reference to his insurance expertise.

This insight was made particularly relevant given the absence of long-time friend and partner Charlie Munger at this year’s event. Munger passed away at age 99 in November 2023.

My number-one investing hero has to be Brandon Beavis. His YouTube videos taught me everything I know about investing. My money hero is Adrian Bar, Canadian in a T-Shirt on YouTube. He taught me how to optimize taxes and keep more money in my pocket. Third, my finance hero is Maxwell Nicholson, the CEO of Blossom. He built an app that shows you what your favourite influencers and friends are investing in, and transparency is truly what Gen Z needs nowadays.

How do you like to spend your free time?

Free time is such a luxury for me. While working two to three jobs from the ages of 19 to 25, I never had free time. I’ve been self-employed for six months now, and I’ve been travelling a lot recently. I also love going on solo dates, taking myself out for breakfasts, dinners, spa treatments and window shopping.

If money were no object, what would you be doing right now?

I would definitely be travelling and doing all the excursions, like swimming with dolphins, scuba diving, ziplining, paragliding and so on.

What was your first memory about money?

Buying snacks at the grocery store. I learned that money allows me to purchase items that I want.

What’s the first thing you remember buying with your own money?

The first thing I bought with my first paycheque was a silver ring at Swarovski. I wanted to buy something that would remind me of my independence and something that would never go out of style.

What was your first job?

I got my first job at age 16, as a sales associate at Old Navy.

What was the biggest money lesson you learned as an adult?

The biggest money lesson I learned was the importance of putting every single dollar of mine to work. I wish I’d researched all the available investment vehicles, like high-interest savings accounts, the stock market and GICs, when I was 19. I missed out on potential gains because I was unaware that such investment vehicles exist. It was important for me to go through that, because now I love exploring more ways to put my money to work, and now I have a platform to share my findings.

What’s the best money advice you’ve ever received?

Diluted bitumen started flowing through the expanded Trans Mountain Pipeline on Wednesday (even at a brisk walking pace, it’ll take weeks to reach its destination). This is raising hopes that at last Canada’s oil sands producers will be able to narrow the discount paid by a now-larger cohort of refiners for their product. Meanwhile, two of the largest shippers on the pipeline reported first-quarter earnings sans that hoped-for revenue bump.

Oilsands earnings highlights

Two producers released their financials this week.

Cenovus Energy (CVE/TSX): Earnings per share rose to $0.62 (versus $0.54 predicted) on revenues of $13.4 billion.

Canadian Natural Resources (CNQ/TSX): Earnings per share of $1.37 (versus $1.48 predicted) on revenues of $8.244 billion.

Cenovus output and profits both surprised on the upside, and the company further sweetened the pot by hiking its base dividend by 29% and announcing a variable dividend of 13.5¢ a share for this quarter. Production for the quarter exceeded 800,000 barrels of oil equivalent per day. At the same time the company modestly reduced its overall debt level.

Results for Canadian Natural Resources suffered from lower-than-expected production and realized prices, especially on the natural gas side. Output came in at 1.33 million barrels of oil equivalent per day.

Amazon, Apple still magnificent

Two more technology mega-caps reported first-quarter results this week, helping keep the Magnificent 7 bandwagon rolling.

U.S. earnings highlights

All amounts in U.S. dollars

Amazon (AMZN/NASDAQ): Adjusted earnings per share were $0.98, exceeding the consensus estimate of 83¢, while revenue of $143.3 billion outstripped the $142.6 billion predicted.

Apple (AAPL/NASDAQ): Earnings per share hit $1.53 (beating the estimate of $1.50) on revenue of $90.8 (versus expectations of $90.3 billion).

Amazon reported continued strong demand for its Web Services, as corporate customers signed longer-term deals with bigger commitments. Generative artificial intelligence (AI) components added to the overall spend, the company said. Advertising revenue also enjoyed strong growth, although there are signs consumers are turning more cautious with retail spending. Following the earnings release, the stock rose 3% Wednesday morning.

Amazon rival Walmart, meanwhile, opted to close 51 health clinics at U.S. stores and discontinue its virtual health services, the company announced Tuesday. It blamed high operating costs and “a challenging reimbursement environment” for poor profitability in the division first launched in 2020.

Apple’s revenues fell less than expected and earnings surpassed Wall Street estimates. The company also said it would boost its dividend to 25¢ a share and authorize $110 billion worth of share buybacks. Services revenue grew to nearly $24 billion, offsetting declines in sales of iPhones and other devices. Sales fell 8% in Greater China (including Taiwan, Singapore and Hong Kong), but that drop-off was not as severe as analysts anticipated. Apple shares surged nearly 6% before markets opened Friday, and more than a dozen analysts raised their target price on Apple.

Tipping on fast food

There’s no accounting for taste as fast-food purveyors moved in divergent ways in the first quarter; some were squeezed between cost inflation and consumer austerity while others continued to super-size their sales.

Deutsche Bank shares were 6% higher on Thursday afternoon after the German lender reported a 10% rise in first-quarter profit, beating expectations amid an ongoing recovery in its investment banking unit.

Net profit attributable to shareholders was 1.275 billion euros ($1.365 billion) for the period, ahead of an aggregate analyst forecast of 1.23 billion euros for the period, according to LSEG data.

Deutsche Bank said this was its highest first-quarter profit since 2013. It also marks the bank’s 15th straight quarterly profit.

Group revenue rose 1% year-on-year to 7.8 billion euros, which the bank attributed to growth in commissions and fee income, along with strength in fixed income and currencies. The revenue print also came in ahead of an analyst forecast of 7.73 billion euros, according to LSEG.

Revenues at its investment bank increased 13% to 3 billion euros, following a 9% slump through full-year 2023 which had dragged down overall profit. The performance restores the division as Deutsche Bank’s highest-earning unit on growth in financing and credit trading revenue.

Other first-quarter highlights included:

Net inflows of 19 billion euros across the Private Bank and Asset Management divisions.

Credit loss provision was 439 million euros, down from 488 million in the fourth quarter of 2023.

Common equity tier one (CET1) capital ratio — a measure of bank solvency — was 13.4%, compared to 13.6% at the same time last year.

“There’s momentum in the businesses, actually across all four businesses, and we do think it’s sustainable,” Deutsche Bank Chief Financial Officer James von Moltke told CNBC’s Annette Weisbach on Thursday.

“We’re delivering on our commitments on costs and capital returns in the quarter.”

Germany’s biggest lender reported net profit of 1.3 billion euros in the prior quarter and of 1.16 billion euros in the first quarter last year.

In 2023, the bank announced it would cut 3,500 jobs over the coming years, as it targets 2.5 billion euros in operational efficiencies to boost profitability and increase shareholder returns.

Morgan Stanley on Tuesday posted results that topped analysts’ estimates for profit and revenue as wealth management, trading and investment banking exceeded expectations.

Here’s what the company reported:

Earnings: $2.02 a share, vs. $1.66 expected, according to LSEG

Revenue: $15.14 billion, vs. expected $14.41 billion

The bank said first-quarter profit rose 14% from a year earlier to $3.41 billion, or $2.02 a share, helped by rising results at each of its three main divisions. Revenue climbed 4% to $15.14 billion.

Shares of the bank jumped about 2.5%.

Wealth management revenue rose 4.9% to $6.88 billion, topping the StreetAccount estimate by $230 million, as rising markets helped boost fee revenue and offset a decline in interest income.

Equities trading revenue increased 4.1% to $2.84 billion, $160 million more than expected, fueled by derivatives volumes. Fixed income trading revenue slipped 3.5% to $2.49 billion, but that still topped expectations by $120 million.

Investment banking revenue jumped 16% to $1.45 billion, edging out the $1.40 billion estimate, as increases in debt and equity issuance offset lower fees from acquisitions.

The firm’s smallest division, investment management, was the only major business to underperform expectations. While revenue climbed 6.8% to $1.38 billion, it was below the $1.43 billion StreetAccount estimate.

CEO Ted Pick’s tenure had kicked off on a rocky note, as high interest rates have incentivized the bank’s wealth management customers to move cash into higher-yielding securities. The bank’s shares have declined nearly 7% this year before Tuesday.

But like rivals including Goldman Sachs and JPMorgan Chase, Morgan Stanley was helped by strong trading and investment banking results in the quarter.

Last week, JPMorgan, Wells Fargo and Citigroup each topped expectations for revenue and profit, a streak continued by Goldman on Monday and Bank of America on Tuesday.

Analysts questioned Pick about reports that multiple U.S. regulators are investigating Morgan Stanley for potential shortfalls in how it screens clients for its wealth management division.

“We’ve been focused on our client on-boarding and monitoring processes for a good while,” Pick said Tuesday. “We have been spending time, effort and money for multiple years, and it is ongoing. We’ve been on it and the costs associated with this are largely in the expense run rate.”

Citigroup on Friday posted first-quarter revenue that topped analysts’ estimates, helped by better-than-expected results in the bank’s investment banking and trading operations.

Here’s how the company performed, compared with estimates from LSEG, formerly known as Refinitiv:

Earnings: $1.86 per share, adjusted, vs. $1.23 expected

Revenue: $21.10 billion vs. $20.4 billion expected

The bank said profit fell 27% from a year earlier to $3.37 billion, or $1.58 a share, on higher expenses and credit costs. Adjusting for the impact of FDIC charges as well as restructuring and other costs, Citi earned $1.86 per share, according to LSEG calculations.

Revenue slipped 2% to $21.10 billion, mostly driven by the impact of selling an overseas business in the year-earlier period.

Investment banking revenue jumped 35% to $903 million in the quarter, driven by rising debt and equity issuance, topping the $805 million StreetAccount estimate.

Fixed income trading revenue fell 10% to $4.2 billion, edging out the $4.14 billion estimate, and equities revenue rose 5% to $1.2 billion, topping the $1.12 billion estimate.

The bank also posted an 8% gain to $4.8 billion in revenue in its Services division, which includes businesses that cater to the banking needs of global corporations, thanks to rising deposits and fees.

Shares of the bank fell nearly 2% Friday.

Citigroup CEO Jane Fraser previously said that her sweeping corporate overhaul would be complete by March, and that the firm would give an update to severance expenses along with first-quarter results.

“Last month marked the end to the organizational simplification we announced in September,” Fraser said in the earnings release. “The result is a cleaner, simpler management structure that fully aligns to and facilitates our strategy.

Last year, Fraser announced plans to simplify the management structure and reduce costs at the third-biggest U.S. bank by assets. The bank on Friday reiterated its medium term targets for returns hitting at least 11% and generating at least $80 billion in revenue this year.

The high interest rates over the last few years have led to the explosive growth of cash holdings, including certificates of deposit (like guaranteed investment certificates (GICs) in Canada) and money market funds. Cash holdings in the fourth quarter of 2023 increased by $270 billion to $18 trillion. Despite that relatively small increase, the rise in value of U.S. equities has led to American households to hold more of their wealth in equities than at any point in history (save the dot-com boom in 2000).

There are likely many reasons for this shift, but these factors could likely be the most prominent influences:

It’s just simple math, since U.S. stocks are on such a long “winning streak” post-2008, the value of those assets is going to be worth more relative to other assets.

As companies complete the shift from defined-benefit pension plans to defined-contribution plans, it’s possible more stocks are being purchased at the individual level.

The average investor got smarter thanks to much more accessible information. Consequently, they now understand the long-term wealth-creating potential of owning large companies (both domestically and internationally).

Millennials and older Gen Zers are sticking around in the stock market after being introduced to it during the meme-stock and pandemic world of 2021.

There hasn’t been a brutal bear market for U.S. stocks since 2008. Sure, there were substantial pullbacks at the start of the COVID-19 pandemic, and then again in 2022. But, those were relatively short-lived. When the stocks did come back, they returned in a massive way—thus, rewarding buy-and-hold investors.

A contrarian investor might say this indicates an oversold market. We’re not so sure that’s the case. Given the long-term track record of U.S. stocks, we’d be surprised to see stock allocations fall below 35% of household assets in the foreseeable future. That’s as low as it got during the worst days of the pandemic. There has been a durable paradigm shift in how investors see the stock market from a risk/reward perspective.

Canadian investors aren’t doing so bad either. We hit a record high last quarter for financial assets of $9.74 trillion, and overall net worth reached $16.4 trillion. Financial assets (shorthand for stocks and bonds) increased overall net worth by about half a trillion bucks, while residential real estate was down about $158 billion. Household debt was up 3.4%, but that’s actually the slowest rise in debt since 1990, and the debt-to-income ratio actually fell slightly.

Will new corporations spin off more value?

When big corporations buy new companies or dive into new lines of business they often tout the advantages of integration and synergies. The theory goes that the asset will be more valuable as a cog in the bigger machine. General Electric (GE/NYSE) and 3M (MMM/NYSE) are two of the world’s largest industrial companies and it was interesting to see them move in the opposite direction this week.

In contrast to the bigger-is-better theory, companies can sometimes get too big and be hindered by layers of bureaucracy. In that case, the spin-off idea is put forward, in which a part of the company will be separated into its own entity so it can focus on providing a narrower product or service. The more narrowly-focused company should, in theory, excel as it’s no longer distracted by the tangle of corporate machinery at the parent company.

GE completed its corporate restructuring last Wednesday, as the former parent company has now been divided into:

GE Vernova (GEV/NYSE): The energy assets of the old GE.

GE Aerospace (GE/NYSE): The old GE market ticker continues on as a pure aerospace company.

GE HealthCare (GEHC/NASDAQ): GEHC was successfully spun off in late 2022, and is up about 57% since it started trading.

GE Aerospace shares finished down 2.42% on their first day of trading, while GE Vernova was down 1.42%.

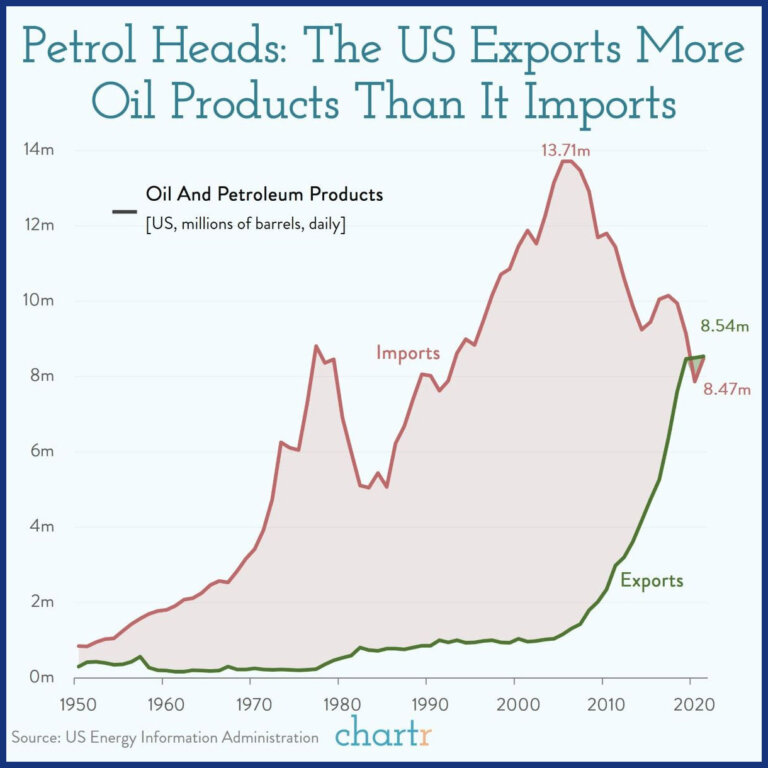

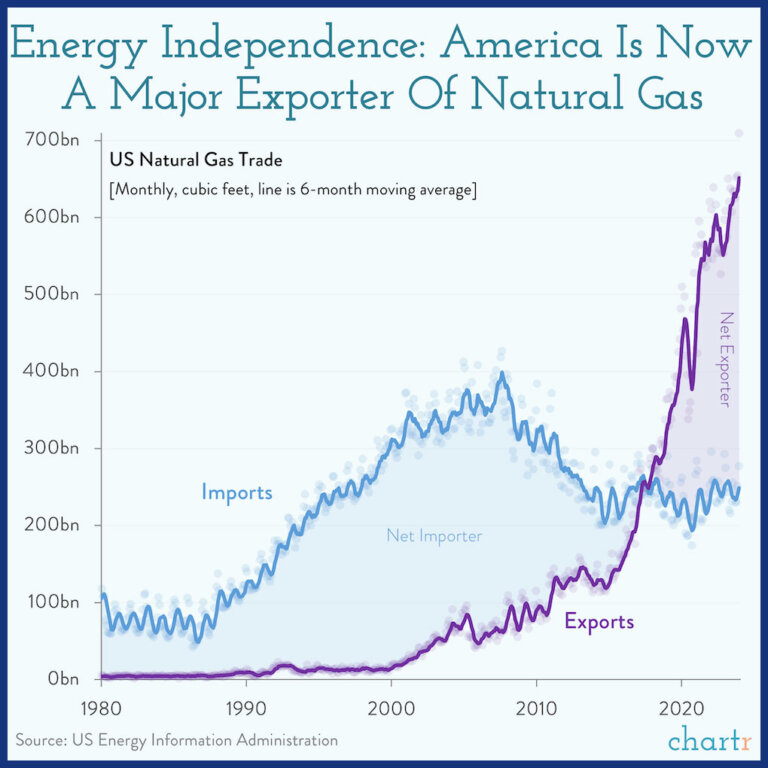

With so much going on in the world, it might have slipped past some Canadian investors that the U.S. fossil fuel industry just hit an interesting milestone. America now has the honour of producing more oil in a single day than any other country in the history of our planet. Yes, even more than Saudi Arabia.

When you consider that the USA has been a massive oil importer for much of the last 70 years, it’s pretty noteworthy that the U.S. exported four million barrels of oil per day last year.

It certainly appears that investors are not shying away from providing capital to American fossil fuel companies. It also means that Canadian efforts to turn away from natural gas (despite our allies essentially begging us for more yet again this week) may not add up to much in the great push against global warming.

The USA is now the world’s largest exporter of natural gas, as well.

Wow, it’s a good thing the Keystone XL pipeline got cancelled, as it appears to have put a stop to all that American fossil fuel business—and at hardly any cost to the Canadian economy either!

Economists would argue that the best way, by far, to reduce the amount of fossil fuel being burned would be to put a tax on it. How popular is that tax on carbon these days anyway?

Clearly, the world has to decide on what sort of level playing field it wants to create in regards to the rules for carbon reduction efforts, as Canada’s attempt to go it alone doesn’t seem to be gaining much traction.

Dividends are after-tax profits a company distributes among its shareholders, typically every quarter, and can be paid in cash or a form of reinvestment.

Heath said a company that pays a high dividend reinvests less of its profit into growth, potentially losing out on opportunities to up its market value. In Canada, stocks with high dividends come from a narrow slice of the stock market—banks, telecoms and utilities.

“Ideally, an investor should consider a combination of stocks with high and low dividends to have a well-diversified portfolio,” he said.

Contribute to RRSP, save on taxes

“There’s a lot of taxpayers, investment advisers and accountants who really promote the concept of putting as much into your (registered retirement savings plan) as you absolutely can,” said Heath.

As a financial planner, he thinks the contrary. Heath says using RRSP contributions to get the biggest tax refund possible is not necessarily the best approach for people in low tax brackets and can hurt them in the long run when they withdraw those savings at a higher tax bracket in retirement.

“Sometimes, it’s OK to pay a little bit of tax, as long as you’re paying at a low tax rate,” he said.

It can be wise to use the low tax bracket by taking RRSP withdrawals early in retirement, even though it might feel good to withdraw only from your TFSA or non-registered savings and keep your taxable income low.

Canadians dreading their spring and summer mortgage renewals got some good news this week, as Canada’s annualized inflation rate dropped to 2.8%.

The Statistics Canada report stated that the slower growth of cell phone service fees, groceries, and internet bills were key reasons why the consumer price index (CPI) number came in significantly lower than the 3.1% economists had reported.

The main takeaways from Tuesday’s StatCan report are:

Rent and mortgage costs are still the main drivers of inflation. Excluding shelter costs, the CPI is up only 1.3% from a year ago.

Gas prices rose 4% in February from January, and were a major reason for the 3.1% economist inflation predictions. If prices return to a decline (as has been the trend), it would continue to be disinflationary.

Notably, cell phone plans were down an astounding 26.5% from last February.

While grocery prices have risen by 22% over the past three years, it appears we’re finally reaching an equilibrium. February was the first time in two years that grocery CPI was lower than overall CPI headline.

Restaurant meals, property taxes and electricity were outliers above the 3% CPI mark.

The preferred metrics of core inflation for the Bank of Canada (BoC) are also subsiding, and are down to 2.2% annualized over the last three months.

If we use interest-rate swaps to judge the likelihood of an interest rate cut, there is roughly an 80% chance (up from 50% before the CPI numbers came in), that the BoC will cut rates in June. (Interest rate swaps are basically a way for the free market to speculate or bet on what interest rates will be at a specific point in time.)

In a related note, as the chances of interest-rate cuts increase, the value of the Canadian Dollar falls. The CAD hit a 3-month low on Tuesday. Overall, that’s good news for mortgage holders, bad news for USD-paying snowbirds.

By comparison, Japan raised its interest rates for the first time in 17 years this week, ending the world’s last negative interest rate policy. The Eurozone also released its inflation data this week, and in a pattern quite similar to Canada’s, it also surprised to the downside, as inflation fell to 2.8% from 3.1%.

This week, both the U.S. Federal Reserve and the Bank of Canada reiterated plans for rate cuts later in the year. Here’s how mortgage rates are responding.

powered by

Soft earnings for Power Corp and Alimentation Couche-Tard

It wasn’t exactly a banner week for Canadian heavyweights Power Corp and Alimentation Couche-Tard.

Canadian earnings highlights of the week

While Power Corp reports in CAD, Couche-Tard reports in USD.

Power Corporation of Canada (POW/TSX): Earnings per share of $0.89 (versus $1.08 predicted). Revenue for the quarter was not provided by Power Corp at press time.

Alimentation Couche-Tard (ATD/TSX): Earnings per share of USD$0.65 (versus USD$0.84 predicted). Revenue of USD$19.62 billion (versus USD$20.85 predicted).

Shares of Couche-Tard were down 4.2% on Thursday after its earnings release. ATD president and CEO Brian Hannasch stated that the lower-than-expected earnings were primarily due to lowered customer traffic and decreased gross fuel margin in the US. He went on to talk about how the integration of the TotalEnergies acquisition is going smoothly and that the company is excited about adding four new countries and 2,175 stores to Couche-Tard’s network of convenience stores.

Power Corp shares didn’t suffer quite the same fate as Couch-Tard, as they were up 1.4% on Thursday, despite the significant earnings miss. It appears that a 7.1% dividend increase was enough to quell any fears that the company was underperforming its current valuation.

Business textbooks are always teaching the Japanese business concepts of Kaizen, Kanban, Andon and just-in-time production. But despite this, the actual market valuations of Japanese businesses have been falling behind for a long time now (basically my entire life).

What some investors fail to understand about this historical anomaly is just how massively overvalued the vast majority of companies were in Japan in 1989. It’s as if Japan’s entire stock market had Tesla- or Nvidia-level expectations of world domination.

From 1956 to 1986, land prices in Japan increased by 5,000%, even though consumer prices only doubled in that time.

At the market peak, the grounds on the Imperial Palace were estimated to be worth more than the entire real estate value of California or Canada.

In 1989, the price-to-earnings (P/E) ratio on the Nikkei was 60x trailing 12-month earnings.

Japan made up 15% of world stock market capitalization in 1980. By 1989, it represented 42% of global equity markets.

From 1970 to 1989, Japanese large-cap companies were up more than 22% per year. Small caps were up closer to 30% per year. That’s incredible growth for a 20-year period.

Japan was trading at a CAPE ratio (cyclically adjusted P/E, which uses 10 years of inflation-adjusted earnings in its calculation) of nearly 100 times, which is more than double what the U.S. was trading at during the height of the dotcom bubble.

So, in regard to the constant naysayers who want to compare the “lost decades” of the Japanese stock market to current market conditions, we can only say there is no data to support this level of pessimism. In other words, there are market bubbles, and then there’s the Japanese bubble.

As usual, celebrated investor and CEO of Berkshire Hathaway, Warren Buffett was a bit ahead of the curve on this one. He’s been buying up Japanese assets for several years. Buffett was quoted by CNBC back in 2023 as saying, “We couldn’t feel better about the investment [in Japan].”

It’s also worth noting that even Japanese stocks win “in the long run.”

If you put $1 a day into Japanese stocks starting in 1980 (~$10,500 in total), you’d have over $17,000 today (thanks to recent all-time highs).

This is true despite Japan experiencing one of the worst equity market returns in history during this time period. pic.twitter.com/2t8SG9xJfV

As Nick Maggiulli, author of Just Keep Buying (Harriman House, 2022), says in the above tweet, if you had started investing in the Nikkei 225 in 1980 (in the run-up to the Japanese bubble), you’d still have a real annual return of 3.5% today (inclusive of dividends).

Carlson also points out that if you invested in a Japanese stock index back in the early 1970s, your returns would still be about 9% a year, despite the biggest bubble of all time bursting in the middle. It’s just that all future returns were pulled forward due to manic speculation—and investors have been waiting for companies to “grow into their valuations” ever since. After waiting a long time for the earnings growth spurt to kick in, it appears the valuation shoes finally fit.

Of course, no such Japanese index fund existed at the time. Today, Canadian investors can efficiently get Japanese exposure through exchange-traded funds (ETFs), such as the iShares Japan Fundamental Index ETF (CJP) or the BMO Japan Index ETF (ZJPN).

Traders work on the floor at the New York Stock Exchange (NYSE) in New York City, U.S., March 5, 2024.

Brendan Mcdermid | Reuters

LONDON — Global dividend payouts to shareholders hit a record $1.66 trillion in 2023, according to a new report by British asset manager Janus Henderson.

The Global Dividend Index report, published Wednesday, said payouts rose by 5% year-on-year on an underlying basis, with the fourth quarter showing a 7.2% rise from the previous three months.

The underlying figure adjusts for the impact of exchange rates, one-off special dividends and technical factors related to dividend calendars, along with changes to the index.

The banking sector contributed almost half of the world’s total dividend growth, delivering record payouts as high interest rates boosted lenders’ margins, the report found.

Last year, major banks including JPMorgan Chase, Wells Fargo and Morgan Stanley announced plans to raise their quarterly dividends after clearing the Federal Reserve’s annual stress test, which dictates how much capital banks can return to shareholders.

“In addition, lingering post-pandemic catch-up effects meant payouts were fully restored, most notably at HSBC,” Janus Henderson’s report added.

“Emerging market banks made a particularly strong contribution to the increase, though those in China did not participate in the banking-sector’s dividend boom.”

However, the positive impact from banking dividends was “almost entirely offset by cuts from the mining sector,” according to Janus Henderson.

The report noted that large dividend cuts by some major companies such as BHP, Petrobras, Rio Tinto, Intel and AT&T diluted the global underlying growth rate for the year by two percentage points, masking significant broad-based growth in many parts of the world.

Right now, the U.S. economy is strong. There is no reason to cut interest rates. In my view, this is a win-win situation. If the economy were to falter quickly, the Federal Reserve would cut rates to help businesses. If the economy continues to grow at 3% to 4%—which is the current prediction for the first quarter of 2024 in the U.S.—the central bank won’t have to act. In both cases, the stock market will go up. We’ll see on March 28, when the U.S. Bureau of Economic Analysis will announce the U.S. 2023 Q4 GDP.

Bitcoin is skyrocketing thanks to the SEC

Wow. Just wow. For a brief moment on March 5, 2024, bitcoin recently hit an all-time high slightly above USD$69,200, beating its previous peak of USD$69,010 in November 2021. The cryptocurrency has been rising since October 2023, but prices really started to surge in January after the U.S. Securities and Exchange Commission (SEC) approved bitcoin exchange-traded funds (ETFs). American retail investors have been waiting a long time for a way to invest in cryptocurrency without having to own the digital tokens themselves. Now they can choose from 10 bitcoin ETFs, including funds from investment giants BlackRock and Fidelity. Collectively, the new bitcoin ETFs have already attracted billions of dollars. An ethereum ETF is likely around the corner. (Canadian investors already had access to bitcoin ETFs—Purpose Investment’s bitcoin ETF launched in February 2021, and at least three ethereum ETFs were launched by various Canadian firms a few months later.)

For me, this is an asset class that is still speculative. I’m not alone. Executives from Vanguard say they are not offering crypto products because they don’t see an “enduring” role for them in long-term portfolios. SEC chair Gary Gensler made a point of saying the approval of bitcoin ETFs was not an endorsement, and that he views crypto as a “speculative, volatile asset.”

Right now, there is no government body or country backing digital currencies—at least, not yet. Until this happens, I don’t know where they fit into the economy. My view: At this point, crypto represents too much risk for most investors. It’s certainly not a core holding for the investors I work with.

Gold also has been rising of late, and I met with David Garofalo of Gold Royalty Corp. about the rise of gold on March 6, 2024.

TSX significantly underperforming the S&P 500

The TSX Composite Index is up just 5% year over year compared to nearly 30% for the S&P 500. Why has the TSX fallen short? Primarily because of which economic sectors it focuses on. Specifically, there is a lack of high-growth technology stocks in Canada. The majority of the TSX is made up of banking, oil and gold stocks. For a while now, banking has been flat at best. Oil stocks have dropped in price. Even though gold is at an all-time high, gold stocks have not fared as well. Meanwhile, 40% of the companies on the S&P 500 are in the technology sector, which led to its strong performance. BMO senior economist Robert Kavcic points out that just “five [tech companies]—Nvidia, Microsoft, Amazon, Meta and Apple—have alone accounted for almost half of the net 1,200 point increase in the S&P 500 over the past year.” More than half the companies on the Nasdaq are also technology stocks. Even the Dow Jones Industrial Average has a growing number of technology stocks, including Apple, Salesforce and Amazon.

The TSX did very well during the China-driven metals super-cycle, when that country was buying up all the copper, aluminum and iron ore it could to build infrastructure. Those days are over. China’s economy is slowing, and that’s impacting Canadian companies and the TSX.

Canada’s economy is the secondary reason the TSX isn’t doing as well as U.S. indexes. Canadian GDP grew by 1% over the last year, while U.S. GDP grew by 3.2%. As a result, Canada is not as attractive to foreign investment as the U.S. We discussed the TSX’s underperformance on the Allan Small Financial Show.

New York Community Bank said Thursday it lost 7% of its deposits in the turbulent month before announcing a $1 billion-plus capital injection from investors led by former Treasury Secretary Steven Mnuchin’s Liberty Strategic Capital.

The bank had $77.2 billion in deposits as of March 5, NYCB said in an investor presentation tied to the capital raise. That was down from $83 billion it had as of Feb. 5, the day before Moody’s Investors Service cut the bank’s credit ratings to junk.

NYCB also said it’s slashing its quarterly dividend for the second time this year, to 1 cent per share from 5 cents, an 80% drop. The bank paid a 17-cent dividend until reporting a surprise fourth-quarter loss that kicked off a negative news cycle for the Long Island-based lender.

Before announcing a crucial lifeline Wednesday from a group of private equity investors led by Mnuchin’s Liberty Strategic Capital, NYCB’s stock was in a tailspin over concerns about the bank’s loan book and deposit base. In a little more than a month, the bank changed its CEO twice, saw two rounds of rating agency downgrades and announced deepening losses.

At its nadir, NYCB’s stock sank below $2 per share Wednesday, down more than 40%, before ultimately rebounding and ending the day higher. The shares climbed 10% in Thursday morning trading.

The capital injection announced Wednesday has raised hopes that the bank now has enough time to resolve lingering questions about its exposure to New York-area multifamily apartment loans, as well as the “material weaknesses” around loan review that the bank disclosed last week.

Mnuchin told CNBC in an interview Thursday that he started looking at NYCB “a long time ago.”

“The issue was really around perceived risks in the loans, and with putting billion dollars of capital into the balance sheet, it really strengthens the franchise and whatever issues there are in the loans we’ll be able to work through,” Mnuchin told CNBC’s “Squawk on the Street.”

“I think there’s a great opportunity to turn this into a very attractive regional commercial bank,” he added.

Mnuchin said that he did “extensive diligence” on NYCB’s loan portfolio and that the “biggest problem” he found was its New York office loans, though he expected the bank to build reserves over time.

“I don’t see the New York office working out or getting better in the future,” Mnuchin said.

Incoming CEO Joseph Otting, a former comptroller of the currency, told analysts Thursday that the bank would look to strengthen its capital and liquidity levels and reduce its concentration in commercial real estate loans.

NYCB will likely have to sell assets as well as build reserves and take write-downs, according to Piper Sander analysts led by Mark Fitzgibbon.

The bank, which has $116 billion in assets, is evaluating whether it should reduce assets to below the key $100 billion threshold that brings added regulatory scrutiny on capital and risk management, executives said Thursday.

When asked by an analyst about the feared exit of deposits after ratings agency downgrades, NYCB Chairman Alessandro DiNello said the bank got “waivers” that allowed it to keep custodial accounts that otherwise may have fled.

“Now I think given this capital raise, we’re hopeful that that relationship continues to be the way it is,” DiNello said.

While news of the Mnuchin investment is good for regional banks overall, Wells Fargo analyst Mike Mayo cautioned that the cycle for commercial real estate losses was just beginning as loans come due this year and next, which will probably cause more problems for lenders.

— CNBC’s Laya Neelakandan and Ritika Shah contributed to this report.

Correction: New York Community Bank announced an investment from a group of private equity investors on Wednesday. An earlier version of this story misstated the day.

Nvidia doesn’t have much room left for multiple expansion when it comes to an increased share price for the stock. After accounting for its incredible earnings day, Nvidia is still trading at a P/E ratio of 66x. Even fellow tech heavyweights Microsoft and Apple are only at 36x and 28x respectively. Consequently, if Nvidia continues its incredible bull run, one would have to believe that the demand for chips will continue to skyrocket and that Nvidia will be able to hold off competitors like AMD and Intel. —K.P.

RRSPs are not a scam or a rip-off

With the deadline to contribute to registered retirement savings plan (RRSP) officially passed as of February 29, we wanted to quickly address the becoming prominent idea that RRSPs are some sort of scam.

We’ve noticed an increasing number of inquiries from friends and family over the last few years that go something along the lines of, “RRSPs are just a rip-off because you have to pay tax on them anyway.”

Since you’re reading a column called “Making sense of the markets,” you’re probably aware that RRSPs are not in fact an asset. The fact that some Canadians don’t understand is shocking. It’s important to understand precisely what RRSPs are.

RRSPs are a type of investment account—one that’s registered. It’s a place where you can hold investments, and it has powers that protect investments from taxation. If you think you’re purchasing RRSPs as an asset, then you might have gone to a bad wealth management company. A good financial advisor helps you understand what asset you were investing in. A bad financial advisor will be vague by using phrases such as “invest in RRSPs.” Investment information is often murky so money can be put into whatever high-fee investments (such as mutual funds) they wanted to sell that day. (Need an advisor? Check out MoneySense’s Find A Qualified Advisor tool.)

Of course, an RRSP doesn’t avoid taxes entirely. It defers tax on the contributed amount from when you relatively earn a lot of money (while working) to when you earn less money (when retired). If you get a tax refund when you contribute or owe less taxes when you contributed to a RRSP, that’s essentially the government saying, “Since you contributed to your RRSP, your taxable income this year is not as high as it would’ve been. So you don’t owe us that money now. Oh, and if you have children, we’ll likely increase your Child Care Benefit cheque, as well.”

If you get a refund, then invest it and let all of that money compound in low-fee investments for the next several decades, you’re very likely to be happy with the results. But those people who say “RRSPs are scams” are usually salespeople pedalling life insurance for higher commissions.

Yes, for some Canadians investing within a tax-free savings account (TFSA), it means they could come out ahead of investing within an RRSP. Yet, for the vast majority of Canadians, they could end up in a pretty similar place. Don’t forget, if you invest inside a TFSA, you don’t get that tax refund to stuff right back into your investment account—you’re contributing after-tax income. When deciding on a TFSA or an RRSP, you would need to know exactly how much income you and your spouse will have when you retire.