Cigna Group abandoned its pursuit of a tie-up with Humana after shareholders balked at a deal that would have created a roughly $140 billion giant in the health-insurance industry.

The companies couldn’t come to agreement on price and other financial terms, according to people familiar with the matter. In the near term, Cigna is turning its focus toward smaller, so-called bolt-on, acquisitions.

Shareholders of Walmart Inc. may have had an inkling of today’s stock selloff if they had been watching the performance of its bonds over the last two weeks.

The bonds have seen net selling even as spreads have tightened, according to data solutions company BondCliQ Media Services.

The same is true for Costco Wholesale Corp. COST, -3.12%,

as the company’s stock fell in sympathy with Walmart on Thursday. That was after Walmart WMT, -8.11%

Chief Executive Doug McMillon said he expects to see a U.S. deflation trend in the coming months.

McMillon was the first retail executive to raise the specter of deflation on an earnings call this season so far.

The comment came after the retail giant posted better-than-expected third-quarter earnings, but offered per-share earnings guidance that was below consensus, sending the stock down more than 7%.

The following charts show what’s been happening with Walmart and Costco bonds in the run-up to today’s numbers.

Bondholders tend to be keenly focused on a company’s underlying financials and closely watched metrics such as cash flow to ensure it can cover interest payments.

That’s because, by buying corporate bonds, they are effectively lending money to a company for a set term and want to be sure they will get their full investment back once they mature. Shareholders tend to be more tuned into daily stock-price movements.

Bonds of Walmart and Costco Wholesale by maturity bucket. Source: BondCliQ Media Services

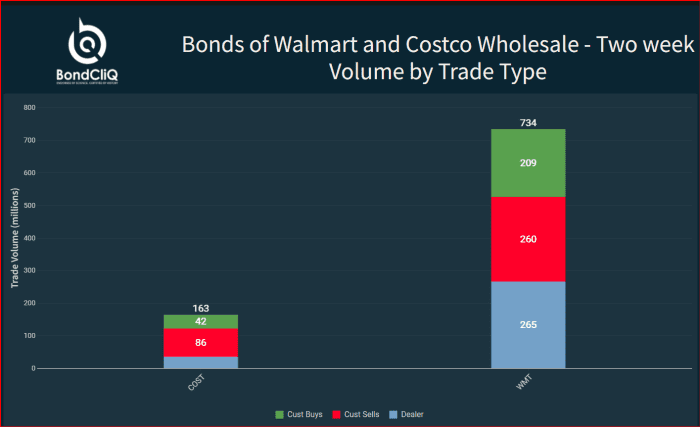

The following chart shows the two-week volume for the bonds by trade type.

Bonds of Walmart and Costco Wholesale — two-week volume by trade type. Source: BondCliQ Media Services

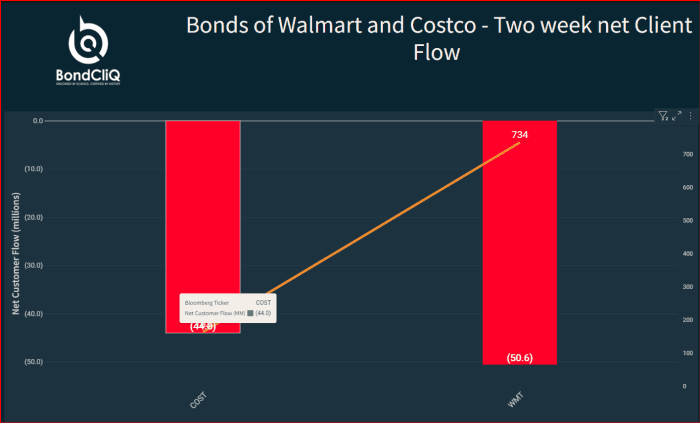

The next chart focuses on two-week client flows, showing net selling for both issuers over the period.

Bonds of Walmart and Costco – two-week net client flow. Source: BondCliQ media Services

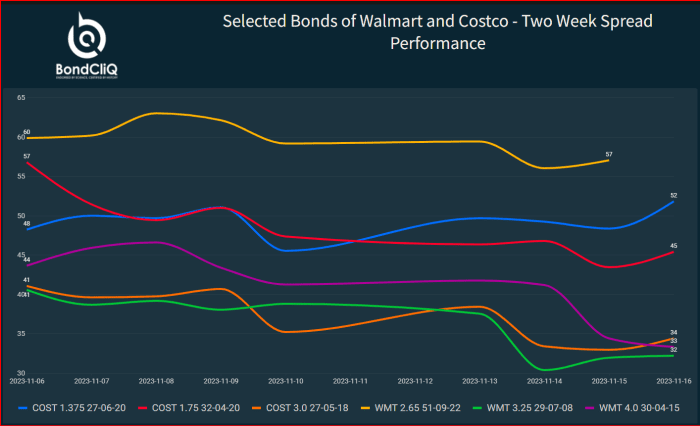

The selling has come as spreads have been tightening, as the next chart illustrates.

Select bonds of Walmart and Costco – two-week spread performance. Source: BondCliQ Media Services

Walmart’s numbers come after other retailers this week said they are seeing signs of pushback from their customers, especially when it comes to big-ticket items.

That was the message from Target Corp. TGT, -1.00%

on Wednesday, with that company’s sales number lagging consensus. Chief Executive Brian Cornell the company saw soft industry trends in discretionary categories, as well as higher inventory shrink.

On Tuesday, Home Depot Inc. HD, -0.79%

said its customers were avoiding big-ticket items.

“The third quarter was in line with our expectations – similar to the second quarter, we saw continued customer engagement with smaller projects and experienced pressure in certain big-ticket, discretionary categories,” said Home Depot CEO Ted Decker, during a conference call to discuss the results.

Groupon Inc. shares were tumbling more than 20% in Thursday’s extended session after the discounting marketplace announced a new rights offering and acknowledged “challenged” business conditions.

The company said in a Thursday afternoon release that its board approved an $80 million fully backstopped rights offering to all holders of its common stock. The rights offering will occur through the distribution of nontransferable subscription rights to purchase common stock at a price of $11.30 a share.

Groupon GRPN, -2.73%

also posted third-quarter results, showing revenue down to $126.5 million from $144.4 million a year prior and slightly below the $129.7 million FactSet consensus, which is based on estimates from three analysts.

The company logged a net loss of $41.4 million, or $1.31 a share, compared with a loss of $56.2 million, or $1.86 a share, in the year-earlier period.

“We are turning our focus to delivering projects across product, engineering, sales, marketing and revenue management that we expect will reinvigorate our marketplace and position our business to return to growth,” interim CEO Dusan Senkypl said in a release.

Added Senkypl: “While we did not make as much progress on key projects as I expected and our business continues to be challenged, I am pleased to see sequential improvement in our financial performance, Local Billings return to growth, and our plan to strengthen our liquidity position.”

In addition, co-founder Eric Lefkofsky plans to leave Groupon’s board of directors, according to Thursday’s release. “With a new management team and the announcement of today’s financing strategy, I am confident that Groupon is on the right track to become the ultimate destination for experiences and services,” Lefkofsky said.

Groupon’s stock is up 58% so far this year but off 97% from its 2011 all-time high.

UBS Group issues $3.5 billion in Additional Tier 1 bonds in the first issuance since the acquisition of Credit Suisse.

It is comprised of two tranches of $1.75 billion of 9.25% perpetual notes redeemable at the option of UBS after five years and $1.75 billion of 9.25% perpetual notes redeemable after 10 years.

“Each issue is a direct, unsecured and subordinated obligation of UBS Group AG,” it said.

“The notes provide that, following approval of a minimum amount of conversion capital by UBS Group AG’s shareholders, upon occurrence of a trigger event or a viability event, the notes will be converted into UBS Group AG ordinary shares rather than be subject to write-down,” UBS added.

BP said its third-quarter profit rose, benefiting from higher realized refining margins and oil and gas production, although it missed expectations.

The British oil-and-gas major said Tuesday that it made an underlying replacement cost profit—a metric similar to net income that U.S. oil companies report—of $3.29 billion in the three months to the end of September, up from $2.59 billion in the preceding quarter. This missed an averaged analysts’ forecast compiled by the company of $4.01 billion.

Drugstore chain Rite Aid Corp. filed for bankruptcy Sunday, as it faces billions of dollars of debt related to opioid lawsuits.

In a statement Sunday night, Rite Aid RAD, -16.81%

said it will close some “underperforming” stores and announced Jeffrey Stein as its new chief executive and chief restructuring officer. Interim CEO Elizabeth Burr will remain on the company’s board.

The bankruptcy filing had been expected for months, and the Wall Street Journal reported in August that Rite Aid was more than $3.3 billion in debt, due largely to hundreds of lawsuits related to its distribution of opioid painkillers. The bankruptcy filing stays pending litigation against the company.

Earlier this month, the New York Stock Exchange warned Rite Aid that it was “no longer in compliance” with the exchange’s minimum pricing and valuation standards, and gave it six months for the stock to regain compliance. Rite Aid shares have plunged about 80% year to date.

Rite Aid said Sunday that lenders will provide $3.45 billion in financing for the chain to continue operating through the chapter 11 bankruptcy process.

“With the support of our lenders, we look forward to strengthening our financial foundation, advancing our transformation initiatives and accelerating the execution of our turnaround strategy,” Stein said in a statement. “In doing so, we will be even better able to deliver the healthcare products and services our customers and their families rely on — now and into the future.”

Rite Aid said it would work to minimize the effect of store closures on its customers so there is no disruption of services, and will transfer affected workers to different locations when possible.

Rite Aid has about 2,100 stores and employs around 47,000 people. It has closed more than 200 stores in the past couple of years.

Rite Aid also said it had reached a deal for pharmacy benefit-solutions company MedImpact Healthcare Systems Inc. to acquire its Elixer Solutions business. A price for the transaction was not disclosed.

Drugstore chain Rite Aid Corp. filed for bankruptcy Sunday, as it faces billions of dollars of debt related to opioid lawsuits.

In a statement Sunday night, Rite Aid RAD, -16.81%

said it will close some “underperforming” stores and announced Jeffrey Stein as its new chief executive and chief restructuring officer. Interim CEO Elizabeth Burr will remain on the company’s board.

The bankruptcy filing had been expected for months, and the Wall Street Journal reported in August that Rite Aid was more than $3.3 billion in debt, due largely to hundreds of lawsuits related to its distribution of opioid painkillers. The bankruptcy filing stays pending litigation against the company.

Earlier this month, the New York Stock Exchange warned Rite Aid that it was “no longer in compliance” with the exchange’s minimum pricing and valuation standards, and gave it six months for the stock to regain compliance. Rite Aid shares have plunged about 80% year to date.

Rite Aid said Sunday that lenders will provide $3.45 billion in financing for the chain to continue operating through the chapter 11 bankruptcy process.

“With the support of our lenders, we look forward to strengthening our financial foundation, advancing our transformation initiatives and accelerating the execution of our turnaround strategy,” Stein said in a statement. “In doing so, we will be even better able to deliver the healthcare products and services our customers and their families rely on — now and into the future.”

Rite Aid said it would work to minimize the effect of store closures on its customers so there is no disruption of services, and will transfer affected workers to different locations when possible.

Rite Aid has about 2,100 stores and employs around 47,000 people. It has closed more than 200 stores in the past couple of years.

Rite Aid also said it had reached a deal for pharmacy benefit-solutions company MedImpact Healthcare Systems Inc. to acquire its Elixer Solutions business. A price for the transaction was not disclosed.

U.S. homes may be wildly unaffordable for first-time buyers, but mortgage bonds backed by those same properties could be dirt cheap.

Shocks from the Federal Reserve’s dramatic rate increases have walloped the $8.9 trillion agency mortgage-bond market, the main artery of U.S. housing finance for almost the past two decades.

Spreads, or compensation for investors, have hit historically wide levels, even through the sector is underpinned by home loans that adhere to the stricter government standards set in the wake of the subprime-mortgage crisis.

Bond prices also have tumbled, sinking from a peak above 106 cents on the dollar to below 98, despite guarantees that mean investors will be fully repaid at 100 cents on the dollar.

From $106 to $98 cents, agency mortgage-bond prices are falling.

Bloomberg, Goldman Sachs Global Investment Research

“It’s really, really struggled,” Nick Childs, portfolio manager at Janus Henderson Investors, said of the agency mortgage-bond market during a Thursday talk on the firm’s fixed-income outlook.

Yet Childs and other investors also see big opportunities brewing. While mortgage bonds have gotten cheaper with the sector’s two anchor investors on the sidelines, the stalled housing market should breed scarcity in the bonds, which could help lift the sector out of a roughly two-year slump.

Prices have tumbled since rate shocks hit, but also since the Fed continued winding down its large footprint in the sector by letting bonds it accumulated to help shore up the economy roll off its balance sheet.

“Banks have been not only absent, but selling,” said Childs, who helps oversee the Janus Henderson Mortgage-Backed Securities exchange-traded fund JMBS,

an actively managed $2 billion fund focused on highly rated securities with minimal credit risk.

“But we’re moving into an environment where supply continues to dwindle,” he said, given anemic refinancing activity and the dearth of new home loans being originated since 30-year fixed mortgage rates topped 7%.

The bulk of all U.S. mortgage bonds created in the past two decades have come from housing giants Freddie Mac FMCC, +0.66%,

Fannie Mae FNMA, +1.09%

and Ginnie Mae, with government guarantees, making the sector akin to the $25 trillion Treasury market. But unlike investors in Treasurys, investors in mortgage bonds also earn a spread, or extra compensation above the risk-free rate, to help offset its biggest risk: early repayments.

While homeowners typically take out 30-year loans, most also refinanced during the pandemic rush to lock in ultralow rates, instead of continuing to make three decades of payments on more expensive mortgages. If someone refinances, sells or defaults on a home, it leads to repayment uncertainty for bond investors.

“To put this another way, the biggest risk to mortgages is now off the table, yet spreads are at or near historic wides,” said Sam Dunlap, chief investment officer, Angel Oak Capital Advisors, in a new client note.

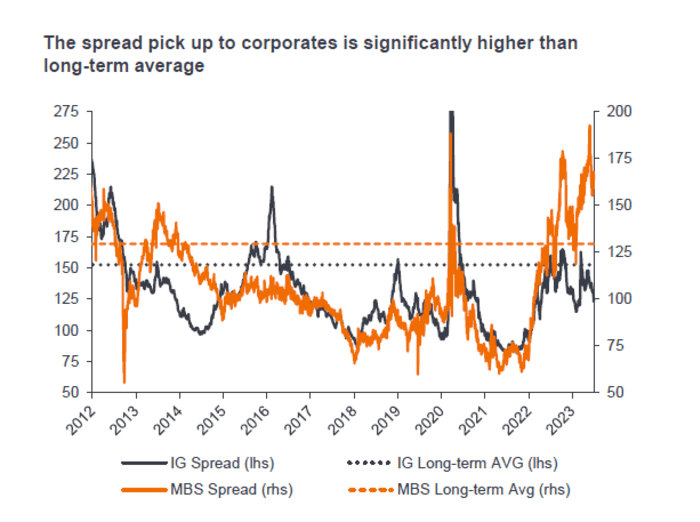

That spread is now far above the long-term average, topping levels offered by relatively low-risk investment-grade corporate bonds.

Agency mortgage bonds are offering far more spread that investment-grade corporate bonds. But these mortgage bonds will fully repay if borrowers default.

Janus Henderson Investors

Agency mortgage bonds typically are included in low-risk bond funds and can be found in exchange-traded funds. While they have been hard hit by the sharp selloff in long-dated Treasury bonds BX:TMUBMUSD10Y

BX:TMUBMUSD30Y,

there has also been hope that the worst of the storm could be nearly over.

Goldman Sachs credit analysts recently said they favored the sector but warned in a weekly client note that it still faces “high rate volatility and a dearth of institutional demand.”

As evidence of the U.S. bond selloff, the popular iShares 20+ Year Treasury Bond ETF TLT

recently sank to its lowest level in more than a decade. It also was on pace for a negative 10% total return on the year so far, according to FactSet. Janus Henderson’s JMBS ETF was on pace for a negative 2.7% total return on the year through Friday.

“Frankly, why they fit portfolios so well is that because the government backs agency mortgages, there is no credit risk,” Childs said. “So if a borrower defaults, you get par back on that. It just comes through as a typical payment.”

Iconic German sandal maker Birkenstock Holdings Ltd.’s stock fell 10% out of the gate in its trading debut Wednesday, signaling that investors remain cautious about new deals and the casual-footwear market remains competitive.

The company’s initial public offering priced at $46 a share late Tuesday, a bit shy of the midpoint of its expected range. The company BIRK, -11.63%

is trading on the New York Stock Exchange under the ticker “BIRK.” Goldman Sachs, JPMorgan and Morgan Stanley were the lead underwriters on the deal.

The deal was expected to prove the latest test for the IPO market, which recently saw three key deals perform strongly on their first day of trade, only to fall back in subsequent sessions.

Chip maker Arm Holdings Ltd. ARM, -1.09% ; Klaviyo KVYO, -3.11%

a digital marketing company; and Instacart, which trades as Maplebear Inc. CART, -7.04%

; all enjoyed strong gains on their first day of trade but pared those in the following sessions. Instacart was quoted at $25.50 on Wednesday, well below its issue price of $30.

Birkenstock clearly has its fans, as its customers are brand loyal, with 70% of existing U.S. consumers, for example, purchasing at least two pairs of its shoes, according to its filing documents.

A survey found 86% of recent purchasers said they wanted to buy again, while 40% said they did not even consider another brand while buying.

But as Kyle Rodda, Senior Market AnalystatCapital.com, said the Birkenstock deal was to be a good measure of broader market sentiment and sentiment toward consumer-sensitive stocks.

“It might tell us, too, whether cashed-up millennials like to buy the stocks of products they commonly find on the bottom shelf of their wardrobes,” he said in emailed comments.

The valuation of around $8.6 billion also looks rich, he said. Based on the company’s latest revenue release, the stock’s price-to-sales ratio is above 6, “which is at the higher end of comparable consumer discretionary companies on Wall Street.

“In a higher interest rate environment, these multiples may be hard to sustain in the short term, especially if consumer spending slows as expected next year as interest rate hikes bite households,” Rodda said.

David Trainer, Chief Executive of independent equity research company New Constructs, said ahead of the deal that the valuation was far too high, noting that it was higher than peers such as Skechers USA Inc. SKX, -0.67%,

Crocs Inc. CROX, -0.12%

and Steve Madden Ltd. SHOO, +0.60%.

“Even more shockingly, the only footwear companies with a larger market cap are Nike Inc. NKE, +0.80%

and Deckers Outdoor DECK, -0.07%,

” he said, referring to the maker of Uggs.

“While Birkenstock is profitable, we think it is fair to say that the $8.7 billion valuation mark is too high, especially for a company that was valued at just $4.3 billion in early 2021. Not a whole lot has changed since then,” Trainer said in a report.

“We don’t doubt that Birkenstock has strong brand equity and produces stylish sandals, but there is really no reason for this company to be public,” said Trainer. “We don’t think investors should expect to make any money by buying this IPO.”

The Renaissance IPO exchange-traded fund IPO

has gained 29% in the year to date, while the S&P 500 SPX

has gained 13%.

Iconic German sandal maker Birkenstock priced its initial public offering at $46 a share late Tuesday, a bit shy of the midpoint of its expected range, as investors remain cautious about new public debuts and the casual-footwear market remains competitive.

With that pricing, Birkenstock would fetch a valuation of around $8.6 billion. The company did not immediately respond to a request for comment.

Birkenstock had expected to sell more than 32 million shares at an IPO price of between $44 and $49 a share. The company is expected to start trading on the New York Stock Exchange on Wednesday under the ticker “BIRK.” Goldman Sachs, JPMorgan and Morgan Stanley are the lead underwriters.

The roughly 250-year-old company would make its debut as other large shoe makers, such as Nike Inc. NKE, +0.76%

and Adidas ADDYY, +1.44%,

try to capitalize on a broader consumer shift toward more casual sneakers and attire. Birkenstock, which unlike many IPOs is profitable, describes itself as a company that has been welcomed across a variety of scenes over the decades — hippies in the 1970s, environmentalists in the ’80s and, in the ’90s, women inspired by the feminism movement looking for relief from high heels.

“Today, consumers turn to Birkenstock in their search for healthy, high-quality products and as a rejection of formal dress culture,” the company said in its IPO filing.

More recently, Birkenstock’s Boston clogs have enjoyed a rebound in popularity. The “Barbie” movie, which features the sandal, has also spurred greater interest. And the company, which depends on the Americas and Europe for a lot of its sales, has been investing more in e-commerce.

Still, Birkenstock faces “material indebtedness,” and “material weaknesses” in its financial controls, according to its IPO filing. And its debut would follow some shakier performances from other recent IPOs, like Maplebear Inc. CART, +9.16%,

better known as the online grocery delivery service Instacart, and chip designer Arm Holdings ARM, +2.69%.

Shares of those companies are down since their debuts.

Renaissance Capital Founder and CEO Bill Smith said Birkenstock was hoping to appeal to investors based on a “combination of profitability and growth, along with widespread brand recognition.”

“We don’t doubt that Birkenstock has strong brand equity and produces stylish sandals, but there is really no reason for this company to be public,” he said. “We do not think investors should expect to make any money by buying this IPO.”

stock plummeted earlier this week after

announcing plans to raise more capital and one analyst understands why. It was one of the reasons he downgraded the stock.

SmileDirectClub Inc. shares plummeted in the extended session Friday after the company said it had voluntarily filed for Chapter 11 bankruptcy protection as founders seek to recapitalize the teeth-straightening business.

SmileDirectClub shares SDC, which had been halted while up 0.9% in after-hours trading pending news, promptly dropped as much as 85% when trading in the stock reopened.

Klaviyo Inc. is reportedly raising the target of its upcoming initial public offering to more than $550 million.

Bloomberg News reported late Sunday that Klaviyo has decided to raise the target range for its shares to $27 to $29, up from its previously stated range of $25 to $27 a share. At the top of that new range, the IPO would raise $557 million, with the company valued at about $8.7 billion, according to Bloomberg.

Ford Motor Co.’s and General Motors Co.’s stocks were higher Friday as workers kicked off a strike, but their bonds have been under selling pressure for some time.

Nearly 13,000 U.S. auto workers went on strike early Friday after the three automakers and the UAW failed to reach an agreement before their national contract expired just before midnight.

The union has opted for targeted strikes, so workers at a Ford F, -0.04%

plant in Michigan and a GM GM, +0.83%

plant in Missouri were first to down tools, along with workers at a Stellantis N.V. STLA, +2.12%

plant in Ohio.

UAW President Shawn Fain has said others could join later and asked all 150,000 members to be ready if and when they’re called to strike.

The strike at all three U.S. carmakers is a break with tradition, as the union for many years has elected to center strike efforts at one company to protect its strike fund and picket-line firepower.

Ford’s stock was last up 0.5%, while GM was up 1.4%.

But as the following charts from data solutions company BondCliQ Media Services shows, the bonds have seen far more selling than buying over the last 10 days. Bondholders are often viewed as “smarter” than shareholders, because they tend to be laser-focused on a company’s financials and cash flows, to ensure they will be repaid their principal when bonds mature.

Net customer flow of Ford and GM bonds (last 10 days). Source: BondCliQ Media Sources

The next chart shows that Ford has seen more selling than GM.

Ford and GM’s debt trading volumes (last 10 days). Source: BondCliQ Media Services

Most-active Ford issues with net customer flow (last 10 days). Source: BondCliQ Media Services

Most-active General Motors issue with net customer flow (last 10 days). Source: BondCliQ Media Services

Stellantis, meanwhile, was seeing strong buying of its U.S. dollar-denominated bonds. The company, the former Fiat Chrysler, has far less debt than Ford and GM.

Stellantis has about $26.5 billion of total debt, according to FactSet data, about $19.7 billion of which is in bonds.

Ford has $143 billion of debt and $124 billion of bonds. GM has $118 billion of debt, with about $107 billion in bonds, according to FactSet.

Most active Stellantis NV issues (USD) with net customer flow (last 10 days). Source: BondCliQ Media Services

“It seems likely the UAW will try to ratchet up pressure on the automakers over time by shifting the strike to more impactful plants and adding more plants to the strike,” Stephen Brown, a senior director at Fitch, said in emailed comments. “The impact on the automakers of striking individual plants could be similar to the semiconductor-induced disruptions that we saw over the past few years.”

Fitch had already incorporated the potential impact of strikes in its recent decision to upgrade its ratings of Ford and GM, he said. The agency moved Ford to BBB- from BB+, moving it back into investment trade from speculative, or “junk,” status.

“Ford, GM and Stellantis all have robust liquidity positions that will help them to withstand a potentially drawn-out period of production disruption. Based on June 30 figures, we estimate Ford has over $50 billion of cash and credit facility capacity, while GM has nearly $40 billion,” said Brown.

Stellantis stock was up 2.2% Friday and has gained 36% in the year to date, outperforming GM’s 1.2% gain and Ford’s 9.0% gain. The S&P 500 SPX

has gained 17% in the same time frame.

priced its initial public offering at $51 a share. That’s at the top of the expected range of $47 to $51, giving the chip design company a valuation of $54.5 billion on a f…

Arm Holding Ltd. priced its initial public offering at the high end of its expected range late Wednesday following intense interest.

The British chip-design company priced shares at $51, raising $4.87 billion, following earlier reports that Arm would be pricing its IPO at $52 a share. A source close to the deal confirmed to MarketWatch that $52 had been the expected price, but that it was reduced to $51. That puts the chip designer at just over a $52 billion valuation. Recently, Arm had stated a targeted range of $47 to $51.