KeyCorp is struggling to regain investors’ confidence, as the Cleveland-based lender underperforms other regional banks, its profits drop and the size of its dividend comes into question.

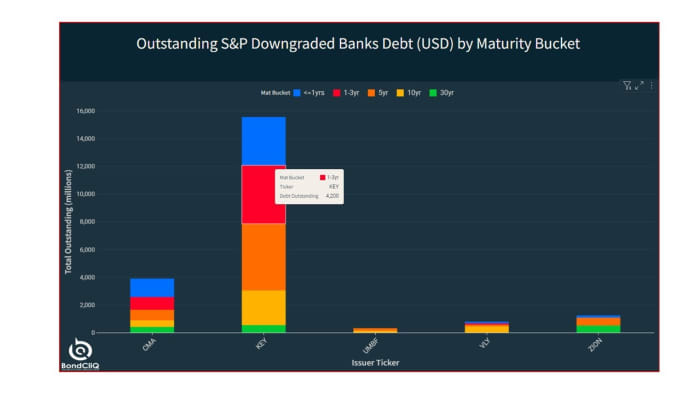

The company’s stock is down 38% this year, a larger drop than other regional banks its size, including Ohio-based competitors Fifth Third Bancorp and Huntington Bancshares. The ratings agency S&P Global downgraded KeyCorp last week, citing its “constrained profitability” compared with other banks its size.

The $195 billion-asset bank’s troubles center around the rapid rise in interest rates over the past year. A sizable chunk of Key’s assets are tied up in securities that the company bought when interest rates were lower — saddling it with lower-yielding assets for several more months and limiting its interest-related revenues.

Key’s interest expenses are climbing, too. The bank is paying more for its deposits — part of the industrywide competition to retain depositors by offering higher interest rates. Higher-cost borrowings that Key assumed this year in larger volumes than its peers are also weighing on the company.

As a result, Key’s guidance on its net interest income — what it earns in interest minus what it pays in interest — has proven to be a disappointment.

“It’s been a very tough year for them,” said Gerard Cassidy, an analyst at RBC Capital Markets, adding that Key’s balance sheet “was not set up for this kind of rate environment.”

KeyBank’s parent company projects that its net interest income will drop 12% to 14% this year — a sharp swing from its projection in April of a 1% to 3% drop, and from earlier forecasts that net interest income would rise. Its noninterest income has also slumped, partly due to a decline in investment banking activity. Overall, Key’s quarterly profits haven’t been this low in years, except for a couple of quarters at the start of the pandemic in 2020.

There is a light at the end of the tunnel, but it may take at least a year to get there. As some of Key’s lower-yielding assets expire, cash will be freed up, and the company should be able to reinvest those funds at higher interest rates.

Key executives have pointed to that coming shift as a factor that will benefit the company — to the tune of $900 million annualized by the first quarter of 2025.

That number is “not immaterial,” Cassidy said. But it’s “tough for shareholders to be patient considering the stock has suffered so much this year,” he added.

Some analysts are particularly pessimistic about Key’s prospects. Alexander Yokum, an analyst at CFRA Research, downgraded the company from a “sell” rating to a “strong sell.”

Key offers a healthy dividend to investors, but Yokum wrote that the dividend is “at risk of getting cut” as the bank prioritizes building up its capital to comply with still-pending rules from the Federal Reserve.

As Key’s profits fall, the amount of earnings going toward its dividend has risen sharply. The dividend payout ratio has “ballooned” to 76%, far higher than the 42% figure at its peers, Yokum wrote.

In a statement, Key said that it’s well capitalized and on strong footing — thanks to a moderate risk profile, a wide range of funding sources and “a diversified deposit base built on earned and enduring trust from our clients.”

“We are a nearly 200-year-old financial institution with safe, sound and strong fundamentals,” the company said. “KeyBank is well positioned to continue supporting all our clients with a full range of financing options while maintaining our moderate risk profile and delivering value to our shareholders.”

Asked last month about a potential dividend cut, KeyCorp CEO Chris Gorman said that he was “confident” the company could sustain the payouts. The company is clearly “under-earning” thanks to its balance sheet positioning, Gorman told analysts at the time.

But Key is also building capital and paring down its balance sheet, and executives expect the current difficulties with respect to net interest income to reverse themselves in the next couple of years, Gorman said.

Plus, Key’s loan book remains healthy, according to Gorman, who said that it should perform well even if a recession hits.

Analysts agree that credit quality is a major bright spot for Key, which in the years after the 2008 financial crisis cut back on risk-taking in its loan portfolio.

Key’s sharper focus on credit risk has led to reduced exposure to the office sector — a segment that’s drawn concern from investors as sluggish return-to-office trends spark worries that urban office loans will deteriorate.

Less than 1% of Key’s loans are office-related. At Key’s peers, that figure is a median of 3%, the company noted in an investor presentation.

Key’s credit quality “remains excellent, and its exposure to higher-risk loan categories is low,” S&P wrote in its report downgrading the bank. The ratings firm also pointed to Key’s “diversified deposit base” as a source of stability.

But S&P also noted that higher interest rates “will continue to pressure profitability for longer and to a greater degree at Key” than at its peer banks.

One reason that Key is in this predicament: its investment and hedging strategies. When interest rates were lower, the bank deployed some of its spare cash on securities.

Those securities are paying some interest, but far less than they would have if Key had either bought them at today’s rates or stuck its cash at the Fed. The central bank now pays upwards of 5.25% for the cash banks that place there — a far higher rate than the 1.74% yield that KeyCorp is earning on its available-for-sale securities.

The securities aren’t ultra-long term, so they’re starting to roll off Key’s balance sheet and opening the door for the bank to reinvest its money at higher rates. Interest rate swaps that Key bought to protect itself against changes in rates are also expiring over the next two years, which will provide yet another boost.

When Key reaches those inflection points, the company should look stronger than its peers, said Scott Siefers, an analyst at Piper Sandler. Right now, Key’s biggest challenge is convincing investors that its net interest income is “indeed finding a bottom and will regain momentum,” Siefers said.

“They’ll make it through, but this is not a thing where they wake up Monday or Tuesday and this is resolved,” Siefers said.

The bank’s securities portfolio has also soured investors for another reason — the “unrealized” losses that accumulated as its low-yielding securities lost value in a high-interest-rate world.

At the end of the second quarter, Key’s securities were worth roughly 13% less than what the bank paid for them, according to regulatory data.

The company sticks most of its investments into the “available-for-sale” accounting bucket, a strategy that some analysts say is wise because it gives Key more flexibility than classifying them as “held-to-maturity” would. If banks sell any chunk of bonds they had planned to hold to maturity, they generally need to absorb losses on the whole portfolio — a penalty that doesn’t apply to selling available-for-sale securities.

But Key is also a “bit unlucky,” given pending changes from the Fed, said CFRA’s Yokum. The regulators’ recent overhaul of rules for large and regional banks — following the failure of Silicon Valley Bank and First Republic Bank — removes a provision that allowed Key and other banks its size to opt out of quarterly swings in their capital tied to gains or losses on its bond portfolios.

Megabanks are required to factor in unrealized gains and losses on their available-for-sale securities each quarter, but regional banks are currently shielded from those quarter-by-quarter swings. The Fed’s changes will be phased in, limiting the impact of the change for Key. The end date for some of its securities is also approaching, helping soften the capital blow further since unrealized losses evaporate if securities are held until they mature.

But some investors are taking a wait-and-see approach on certain banks, and have moved to stocks they view as safer bets.

“Key has its work cut out for it, and this will be a long road,” Siefers said. But the company has a “plan in place, and now it comes down to execution,” he added.

Allissa Kline contributed to this report.