Food prices grew at a slower pace in June, but economists remain concerned that prices will reach a level where consumers will make dramatic changes in their behavior.

Food prices rose 3% in June compared to a year ago, according to the latest data from the Bureau of Labor Statistics. After a year of price hikes, consumers continued to see food prices rise, but at a slower rate.

Grocery prices were 5.7% higher in June compared to a year ago, and dining out was 7.7% more expensive. That’s significantly lower than the 13.5% peak inflation for grocery prices last August and the 8.8% peak inflation for dining out.

“Overall, there continues to be a similar narrative of extended upward pressure on food prices as we try to discern whether this stress has led to a tipping point where consumers are struggling to buy the foods that they want,” said Jayson Lusk, the head and distinguished professor of Agricultural Economics at Purdue University.

Reported food insecurity across households of different income levels reached 17% in June, the highest level since March 2022, according to the monthly Consumer Food Insights Report from Purdue University. Although it didn’t deviate too much from the normal range — food insecurity hovered at 14% two months ago — Lusk said the increase is concerning given the amount of pressure on more financially vulnerable consumers.

“Reported food insecurity across households of different income levels reached 17% in June, the highest level since March 2022, according to Purdue University. ”

The pandemic-era expansion of the Supplemental Nutrition Assistance Program ended in March, meaning SNAP recipients are now receiving $90 less on average every month, according to the Center on Budget and Policy Priorities, a progressive policy think tank based in Washington, D.C.

The recent rise in food insecurity could be a lag from households adjusting to the policy change, Lusk said. On average, consumers are spending about $120 per week on groceries and $70 per week on dining out or takeout, the report found.

Middle-income households earning $50,000 to $100,000 a year and low-income households earning less than $50,000 a year cut weekly spending on groceries and dining out by about $10 a week, Purdue found. The average weekly grocery expenditure for low-income households was $103 in June; for middle-income households, it was $118. Households earning more than $100,000 a year spent $141 a week on groceries in June.

Around 47% of low-income households — those earning less than $50,000 a year — said they relied on SNAP benefits in May, up from roughly 40% in February, according to a recent Morning Consult report.

For low-income households, rising food insecurity is often coupled with juggling bills such as utilities and rent, which has also led to rising eviction rates in recent months, according to Propel, an app that aims to help low-income Americans improve their financial health. Propel surveys SNAP users on insecurity around food, finance and their housing situation.

Nearly half of the survey respondents said they cannot afford the food they want. “We were unable to pay bills because we had to buy food. We’re about to lose our home,” a South Carolina user named Anna told the Propel survey.

The share of surveyed households that paid their utilities late rose 11% from May to June, and only 27% of respondents paid their utility bills on time and in full, according to Propel’s June survey.

The U.S. Federal Trade Commission’s defeat as it sought to block Microsoft Corp.’s acquisition of videogame maker Activision Blizzard is yet another setback for an increasingly toothless regulator that needs to pick better battles with Big Tech.

“With these 10-year contracts that Microsoft made across the board with so many vendors, Nvidia NVDA, +0.53%,

Nintendo and others, 10 years is a really long time, in my opinion,” said Sarah Hindlian-Bowler, an analyst at Macquarie Equity Research, in an interview Tuesday. “It is long enough to cover the arrival and maturity of the cloud gaming market….She understands that 10 years is a very long long time to make a guarantee of this kind.”

Hindlian-Bowler said that she had been in the minority of Wall Street analysts in not believing the U.S. government would be able to block this deal.

“The assumption that this somehow decreases the market is going to prove to be wildly incorrect,” she said, adding that she does not believe that the U.K.’s Competition and Markets Authority will be able to block the deal either.

The latest upset at the FTC was also not too surprising to other Capitol Hill watchers, especially in the light of other high-profile setbacks by the agency and its once-heralded commissioner, Lina Khan. When she was sworn in as chair of the FTC in mid-2021, Khan was hailed as the sheriff who would rein in Big Tech.

“It’s hard to say I am surprised by the ruling because Khan has had a fairly unsuccessful track record,” said Owen Tedford, a senior research analyst at Beacon Policy Advisors. “The regulators are pushing the boundaries, deals that previously would have gone unchallenged have now gone challenged. And they are breaking precedent because Khan and company have expressed a dislike of settlements.”

“I think that the FTC is in need of some change, in need of some refreshing and in need of doing a much better job of picking their battles,” said Hindlian-Bowler. “This does feel toothless, a lot of the fights they are picking are toothless. And unfortunately, they are missing the real battle. They are missing TikTok, they are missing the real fights where we actually have national security at risk.”

In February, one of the Republican commissioners on the FTC resigned, and wrote an op-ed in the Wall Street Journal accusing Khan of disregarding the rule of law and due process.

Compared to the European Union, which has had far more success implementing regulation to rein in Big Tech, the U.S. is still much weaker. “The EU seems to be having somewhat more success, levying big fines, getting these companies to change,” said Beacon’s Tedford. “The EU has passed these bills, but the U.S., despite these efforts, has not gotten there and is not going to get there for the next two years.”

Money spent by Big Tech to lobby Congress in a huge part of the problem, whereas in Europe, “those lawmakers feel less beholden,” he added.

More than a century ago, President Teddy Roosevelt, known for his “speak softly and carry a big stick” foreign policy, also used his bully pulpit to bust industrial monopolies.

If Khan and her staff want to follow his lead and rein in Big Tech, they need to start picking their future battles more carefully — and carry bigger sticks.

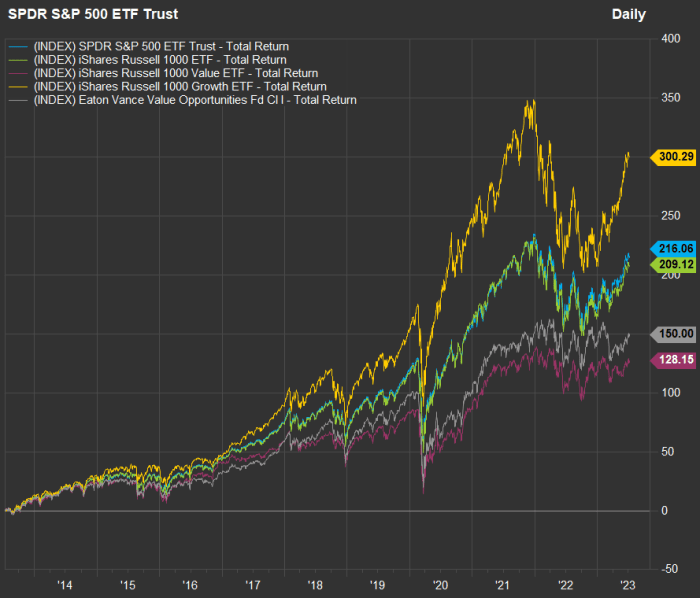

At a time when many investors seem euphoric, others are warning that stock valuations have once again turned frothy. It may pay to take a look back at valuation and performance and consider your own risk tolerance.

A value-based approach that offers lower volatility and good long-term returns can be expected to be less flashy than one focused on the hottest technology stocks. But depending on how much it bothers you when the stock market gyrates, it may be a better way for you to invest. Lower volatility might help you to avoid the type of emotional reaction that can lead to selling into a declining market or attempting to time the market, both of which tend to be losing strategies.

Aaron Dunn is a co-head of the value equity team at Eaton Vance, which is based in Boston and is a unit of Morgan Stanley. During an interview, he explained how he and Brad Galko, who co-heads the team, select stocks for the Eaton Vance Focused Value Opportunities Fund. The fund’s performance benchmark is the Russell 1000 Value Index RLV, +1.08%.

First, let’s take a broad look at how aggregate forward price-to-earnings ratios have moved for exchange-traded funds tracking several broad indexes over the past 10 years:

FactSet

The valuations are lower than their 2020 peaks. But for all but one, the valuations still appear to be high when compared with their 10-year averages:

All of the listed ETFs listed here are trading well above their 10-year average P/E valuations except the iShares Russell 1000 Value ETF, which is only slightly higher. These numbers back the notion that the broad market is expensive and that a value approach may be more reasonable. It is also worth keeping in mind that during 2022, when the SPDR S&P 500 ETF Trust SPY, +0.64%

declined 18.2% and the iShares Russell 1000 ETF IWB, +0.80%

fell 19.2%, the iShares Russell 1000 Value ETF IWD, +1.07%

pulled back 7.7% and the Eaton Vance Focused Value Opportunity Fund’s Class I shares were down only 3.3%, all with dividends reinvested.

If we look at 10-year total returns, the nonvalue indexes, so heavily weighted to the largest technology-oriented companies, have been excellent performers for investors who could remain committed through thick and thin:

For five and 10 years, the growth-oriented approaches have shined. But for three years, which includes the 2022 disruption, the Eaton Vance Value Opportunities Fund has fared best, even outperforming its benchmark.

A selective approach to value

The Eaton Vance Focused Value Opportunity Fund’s Class I EIFVX, +0.92%

shares are rated four stars (out of five) within Morningstar’s Large Value fund category. The fund’s Class A EAFVX, +0.93%

shares are rated three stars. The difference is that the Class I shares, which are typically distributed through investment advisers, have annual expenses of 0.74% of assets under management, while the Class A shares have an expense ratio of 0.99%. You can purchase Class I shares directly through brokerage platforms for a $50 fee.

Dunn said that when selecting stocks for the fund, he and Galko take a bottom-up approach to identify quality companies. The want to see high returns on invested capital (ROIC) over the long term, as well as a “good competitive position” for a company and a strong management team.

They also prefer companies with low debt. “We do not want to buy overlevered companies and be in a situation where we are diluting through equity raises and putting capital at risk,” he said.

Dunn added that he and Galko look closely at free cash flow generation. A company’s free cash flow is its remaining cash flow after capital expenditures. This is money that can be used to fund expansion, acquisitions, dividend increases or share buybacks, or for other corporate purposes.

“Philosophically, what this results in is that we hold up well in markets such as last year’s. And we find upside in stocks trading below intrinsic value,” he said.

“We focus on finding ideas where there is a good skew for upside relative to downside,” he added.

According to Morningstar, the fund’s active share when compared with IWD is high, at 91.45%. Active share is a measure of how much an actively managed fund differs in investment exposure from its benchmark index. If you are paying more for active management than you would to invest in an index fund, active share is something to consider. If it is low, you might be overpaying for a “closet indexer.” You can read about how Morningstar assesses active shares here.

The fund is concentrated, typically holding between 25 and 45 companies.

According to Morningstar’s most recent data, these were the fund’s top 10 holdings (out of 28 stocks) as of May 31:

There is no forward price-to-earnings ratio for Micron Technology Inc. MU, +1.79%,

because the company’s combined EPS for the next 12 months are expected to be negative.

Micron is a company in transition, caught up in diplomatic conflict between the U.S. and China, whose government directed some manufacturers in May to stop purchasing memory chips made by the company. Then again, in June, Micron highlighted its “commitment to China” when announcing a new investment in its plant in Xi’an.

Dunn said downside for Micron’s stock was “mitigated” because of the company’s relatively low debt. He also said that as companies continue to adopt more cloud services and deploy artificial-intelligence technology, demand for memory chips will increase.

While there is no current forward P/E for Micron, the stock always trades at low valuations relative to most other large tech companies. Dunn touted Micron’s strong cash flow and said the stock was “underappreciated” and remained “an interesting play on cloud and AI.”

While it is not among the top 10 holdings listed above, Dunn highlighted Dollar Tree Inc. DLTR, +1.80%

as an example of the type of value stock he favors. The company “was not well run” following its acquisition of Family Dollar in 2015. But he has been impressed with its more recent turnaround efforts, including improvements in how products are shipped to stores, better efficiency and “a lot of work going on with culture, how they operate, how they treat employees [and] adding some shelf space to move more product.”

It is interesting to see NextEra Energy Inc. NEE, +0.67%

among the fund’s largest holdings. This has been quite a strong grower over the past 10 years, with a total return of 346% as the owner of Florida Power & Light has grown along with its customer base and has become a leader in the build-out of solar-power generation.

Dunn said the company is “still growing in the mid-single digits. For a utility company, that is a strong profile.”

When discussing Alphabet Inc. GOOGL, +0.59%,

the fund’s largest holding as of May 31, Dunn said that “it is really an advertising business with other businesses around it” and that its P/E valuation was “not extremely taxing.” He said Alphabet had been “less aggressive with cost cutting” than other technology giants and added that the company’s “targeted search” through Google and other properties, such as YouTube, “probably provides a better return on investment than broadcast advertising, and that really is the key.”

If you’re a retiree and you’re trying to square the circle of rising costs, longer lifespans, more expensive medical care and turbulent markets, don’t be afraid to run the numbers on your biggest investment.

That would be your home — if you own it.

U.S. house prices are now so high that it is almost impossible for seniors not to ask themselves the obvious question: “Should we cash in, invest the money, and rent?”

Right now the average U.S. house price is nearly $360,000. That’s about a third higher than just a few years ago, before the COVID-19 pandemic. The lockdowns, the panic, the stimulus checks and 2.5% mortgage rates have all passed into history. But the sky-high prices remain — for now.

After several years of double-digit percentage increases, apartment-rent growth is falling for only the second time since the 2008 financial crisis. WSJ’s Will Parker joins host J.R. Whalen to discuss.

There is a similar story for seniors. Federal data show that the average U.S. house price is now nearly 17 times the average annual Social Security benefit — an even higher ratio than it was in August 2008, just before Lehman Brothers collapsed. At that juncture, the average house price was 15 times higher.

U.S. National Home Price Index vs. average rent of primary residence in U.S. city, according to the U.S. Bureau of Labor Statistics. Indexed: January 1987=100.

S&P/Case-Shiller

Our simple chart, above, compares average U.S. home prices with average U.S. rents, going back to 1987. (The chart simply shows the ratio, indexed to 100.) The bottom line? House prices are very high at the moment compared with rents — again, prices are about where they were in 2006-07.

And the two must run in tandem over the long term, because the economic value of owning a house is not having to pay rent to live there.

If there are times when, in general, it makes more financial sense for seniors to rent than to own, this has to be one of those.

Seniors who own their own homes may think high interest rates on new mortgages don’t affect them. They most likely either already have a mortgage at a lower, older rate or they’ve paid off their home loan. But if you want to sell, you’ll almost certainly be selling to someone who needs a mortgage.

If borrowing costs drive down real-estate prices, seniors who hold off on selling may miss out on gains they may never see again. After the last housing peak, in 2006, it took a full decade for prices to recover fully. Those who sold when the going was good had the chance to buy lifetime annuities at excellent rates or to invest in stocks and bonds that overall rose about 80% over the same period.

Incidentally, there is also an exchange-traded fund that invests in residential REITs, Armada’s Residential REIT ETF HAUS, -0.53%,

though in addition to single-family homes and apartment-complex operators, about 25% of the fund is invested in companies involved in manufactured-home parks and senior-living facilities.

For each person, the math will be different, and there are a number of questions you need to ask. Where do you want to live? How much would you get if you sold your house? How much would you pay in taxes? How much would it cost to rent the right place? Do you want to leave a property to your heirs? And what would be the costs of moving — both financial and emotional?

The conventional wisdom is that you should own your home in retirement.

“I would advise any and all retirees against renting if at all possible,” says Malcolm Ethridge, a financial planner at CIC Wealth in Rockville, Md. “You need your costs to be as fixed as possible during retirement, to match your income being fixed as well. If you choose to rent, you’re leaving it up to your landlord to determine whether and by how much your No. 1 expense will increase each year. And that makes it very tough to determine how much you are able to allocate toward everything else in your budget for the month.”

A key point here, from federal data, is that nationwide rents have risen year after year, almost without a break, at least since the early 1980s. They even rose during the global financial crisis, with just one 12-month period where they fell — and then by only 0.1%.

“My general advice for clients is that owning a home with no mortgage in retirement is the best scenario, as housing is typically the highest cost we pay monthly,” says Adam Wojtkowski, an adviser at Copper Beech Wealth Management in Mansfield, Mass. “It’s not always the case that it works out this way, but if you can enter retirement with no mortgage, it makes it a lot easier for everything to fall into place, so to speak, when it comes to retirement-income planning.”

“Renting comes with a lot of risk,” says Brian Schmehil, a planner with the Mather Group in Chicago. “If you rent, you are subject to the whims of your landlord, and a high inflationary environment could put pressure on your finances as you get older.”

But it’s not always that simple.

“With housing costs as high as they are now though, renting may be a viable solution, at least for the moment,” says Wojtkowski. “We don’t know what the housing-market trends will be going forward, but if someone is waiting for a housing-market crash before they move, they could very likely be waiting for a long time. We just don’t know.”

“Any decision comes with pros and cons,” says Schmehil. “Selling when your home values are historically high and renting allows you to capture the equity in your home, which is usually a retiree’s largest or second-largest financial asset. These extra funds allow you to spend more money on yourself in retirement without having to worry about doing a reverse mortgage or selling later in retirement, when it may be harder for you to do so.”

Renting also allows you to be more flexible about where you live, for example nearer your children or grandchildren, he adds.

And as any experienced property owner knows, renting also brings another benefit: You no longer have to do as much work around the house.

“Renting is great in that you don’t need to maintain a residence,” says Ann Covington Alsina, a financial planner running her own firm in Annapolis, Md. “If the dishwasher breaks or the roof leaks, the landlord is responsible.”

Wojtkowski agrees, noting that many people no longer want to spend time mowing the lawn or shoveling snow in retirement. “Ultimately, one of the things that I’ve seen most retirees most concerned with is eliminating the general upkeep [and] maintenance of homeownership in retirement,” he says.

Several planners — including Covington Alsina and Wojtkowski — note that one alternative to selling and renting is simply downsizing. This can free up capital, especially when home prices are high, like now, without leaving you exposed to rising rents.

Many baby boomers have been doing exactly that.

Meanwhile, I am reminded of my late friend Vincent Nobile, who — after a long and fruitful life owning homes and raising a family — found himself widowed and alone in his 80s. He rented a small cottage on a New England sound and said how glad he was that he never had to worry about maintaining the roof or the appliances, or fixing the plumbing or the heating, or any one of a thousand other irritations. Or paying property taxes — which go down even more rarely than rents.

When the regular drives to Boston got too onerous, he moved into the city and rented there. And he was glad to do it. The money he had made was all in investments — a lot less hassle both for him and his heirs.

I once asked him if he would prefer to own his own home. He shook his head and laughed.

The goal of many (or most) savers and long-term investors is to achieve financial independence. The combination of building up a nest egg, paying down debt and eventually receiving Social Security payments or another source of retirement income might put you in a comfortable position, but even people who have worked together to achieve financial independence may disagree on what to do after their careers end.

Quentin Fottrell — the Moneyist — heard from one couple who are facing a quandary. They have been financially responsible, but as they near retirement, the wife wishes to be very careful with their combined investment portfolio, while the husband wants to begin spending a significant portion of it. They both make reasonable arguments. Here’s what they should do.

A behavioral study finds a correlation between having one specific type of conversation and taking action to build wealth.

Getty Images

Doing this even once might help encourage you or someone you know to begin saving and investing for the long term.

The ‘Magnificent Seven’ stocks may not remain at the top

Salesforce is among the companies passing a Goldman Sachs screen for growth of sales and earnings.

Getty Images

Even an index that includes hundreds of stocks can be heavily concentrated. Large technology-oriented companies have led this year’s 16% rebound for the S&P 500 SPX, -0.29%,

following last year’s 18% decline (both with dividends reinvested). But the index is weighted by market capitalization, which means the “Magnificent Seven” — Apple Inc. AAPL, -0.59%,

Microsoft Corp. MSFT, -1.19%,

two common share classes of Alphabet Inc. GOOGL, -0.52%

In the Need to Know column, Barbara Kollmeyer lists companies that might turn out to be among the next Magnificent Seven, based on a Goldman Sachs screen.

Getting back to the current Magnificent Seven, you may be surprised to see which of the stocks is cheapest — by far — per one commonly used valuation metric.

Meta’s Threads app has signed up as many as 50 million users in its first two days of operation, some reports say.

AFP via Getty Images

Meta rolled out its new Threads service on Wednesday to compete directly with Twitter and has already signed up 50 million users, according to some reports.

U.S. shoppers have been taking it slow during a period of high inflation, but the overall economy has been stronger than expected even as the Federal Reserve continues tightening its monetary policy.

Lukas I. Alpert writes the Financial Crime column. Have you ever wondered how you might steal a lot of cash from a company that is likely to have rather tight accounting controls in place? This week Alpert explains how the manager of an Amazon warehouse managed to scale the heights of criminal achievement to collect $10 million — and a 16-year jail sentence.

Micron Technology Inc. could be approaching a big new semiconductor cycle as it predicts a huge boost from artificial intelligence, but there could be a roadblock in the path.

Micron MU, +0.42% reported a third-quarter loss and a 57% drop in revenue Wednesday, after the chip industry’s oversupply hit the memory-chip maker hard. On the bright side, Micron Chief Executive Sanjay Mehrotra said he believed the memory industry “had passed its trough” and that the company’s margins should improve as the supply-demand balance is gradually restored.

Another big issue for the stock right now, though, is China’s decision to recommend that “operators of critical information infrastructure in China should stop purchasing Micron products.” Mehrotra told analysts on the company’s conference call that the decision will impact about 50% of its products sold in China.

“We currently estimate that approximately half of that China-headquartered customer revenue, which equates to a low double-digit percentage of Micron’s worldwide revenue, is at risk of being impacted,” Mehrotra said on the call. “This significant headwind is impacting our outlook and slowing our recovery.”

He said Micron will work with its long-term customers who are not impacted by China’s decision, and hopefully will increase its share with those customers.

On the plus side, Micron expects to see a substantial boost to its memory business as a result of companies gearing up to run generative AI on their own servers or clouds. “Generative AI [is] becoming a big opportunity and we look at it for 2024 as a big year for AI and for memory and storage, and Micron will be well-positioned,” in the data center with its products, Mehrotra said. He added that it is “very, very early innings for AI,” which is really pervasive. “It’s everywhere.”

He said it will be in both cloud and enterprise server applications, and due to confidentiality of data, enterprises will be building their own large language models, adding that the DRAM (dynamic random access memory) content required for AI in servers is driving higher demand for memory and storage in servers. In super cluster configurations, for example, the DRAM content can be as much as 100 times higher.

Investors appeared to maintain some caution about when the AI impact will kick in, even as some analysts have forecast that AI demand will lead to a general supercycle for many hardware companies. Micron’s shares see-sawed in after-hours trading Wednesday, ending the extended session up about 3%.

In a note ahead of the company’s earnings, Raymond James analyst Srini Pajjuri said that the impact from China “should be short-lived given the commodity nature of Micron’s products.”

Right now, it’s too early to say how long China may be a drag for Micron, but if Mehrotra is right, investors should take heart that the company is going to be another beneficiary of the coming AI boom.

Financial disruptions in 2008 contributed to the deep economic downturn that came to be known as the Great Recession. Could recent bank failures similarly lead to a broad U.S. recession?

The $532 billion of assets of the three banks that failed in March and April 2023 exceed the inflation-adjusted value of $526 billion of assets of the 25 banks that failed in 2008. Yet the current situation differs in many ways from the underlying economic circumstances at the outset of the Great Recession.

Still, that experience, as well as others, show how financial distress can lead to macroeconomic weakness which then contributes to further financial distress, resulting in a downward spiral during which credit becomes tight, investment is curtailed and growth stalls.

Bank distress can have adverse consequences for borrowers and the broader economy. One source of recent U.S. bank vulnerabilities is the rapid increase in interest rates. Banks take in deposits that can be withdrawn in the short term and use them to make loans and invest in securities at interest rates that are fixed for some time.

As interest rates rise, the value of banks’ existing portfolio decreases as new investments at higher rates are more attractive. By one estimate, the U.S. banking system’s market value of assets is $2.2 trillion lower than suggested by their book value of assets accounting for loan portfolios held to maturity.

These book losses are realized if banks have to sell those assets to cover withdrawals from depositors. At the same time banks face challenges in maintaining deposit levels, depositors are less willing to place their money in low-return checking and savings accounts as higher-interest opportunities become increasingly available.

Banks that failed in 2023 have had specific weaknesses that made them particularly vulnerable. Silicon Valley Bank (SVB), for example, was particularly exposed to risk from rising interest rates as it had heavily invested in longer-term government bonds which lost market value as interest rates rose and its management failed to hedge against this risk.

SVB was also especially vulnerable to a run by depositors because over 90% of the value of its deposits exceeded the $250,000 amount guaranteed by the Federal through the Federal Deposit Insurance Corporation (FDIC). Depositors holding accounts in excess of this guaranteed amount, both individuals and companies (whose accounts were used for making payroll, among other reasons) are only partially protected in case of bank failure so they have an incentive to withdraw funds at the first sign of trouble.

Moreover, depositors were connected to each other through business and social groups, so news traveled quickly seeding the conditions for a classic bank run at Twitter speed. Signature Bank also had about 90% of its assets uninsured and its portfolio was heavily concentrated in crypto deposits. Both banks grew rapidly with inadequate risk and liquidity management practices in place and, while regulators had raised concerns about these risks, they had not taken more forceful actions to address them, according to a GAO report. Meanwhile, First Republic Bank, catered to wealthy depositors and for this reason also had a high share of uninsured deposits that made it more vulnerable to a bank run as its bond assets lost value amidst rising interest rates.

Commercial banks reduce lending when their deposits fall or when they otherwise cannot meet regulatory requirements. Deposits represent an important source of banks’ ability to lend. As a bank’s deposits decrease, it has less resources available for lending since other sources of funds are not as easily obtained.

A bank may also cut lending in an effort to satisfy regulations such as meeting or exceeding the Capital Adequacy Ratio. Regulators require banks to have enough capital on reserve to handle a certain amount of loan losses. The Capital Adequacy Ratio decreases when loans fail and the bank sees its loan loss reserves decline. The bank can then increase its Capital Adequacy Ratio by using funds that would otherwise be devoted to commercial loans or by shifting from loans to other assets that are less risky (such as government securities).

There is evidence that this effect contributed to the cutback in bank lending in New England in the 1990-1991 U.S. recession when there was a collapse in that region’s real estate market. A bank may choose to reduce lending if there are concerns about solvency even if it is not yet hitting up against the formal capital adequacy ratio requirement.

A credit crunch occurs when borrowers who would otherwise receive loans are precluded from doing so because of a restriction on the supply of loans by banks. But a reduction in bank lending could also reflect a decrease in borrowers’ demand for loans.

Researchers have used a variety of methods to identify when there is a credit crunch rather than just a lower demand for loans. For example, a credit crunch could be identified through looking for differential borrowing, employment, and performance patterns by bank-dependent companies as compared to those that have access to financing through bond or equity markets. Bank-dependent companies are typically smaller than those that have access to other types of financing.

Credit crunches due to bank distress can undermine investment and economic growth. An early and influential analysis by Ben Bernanke, who went on to chair the Federal Reserve and served during the 2008 Great Financial Crisis, analyzed the effects of bank failures during the Great Depression. He found that bank failures had a particularly strong effect in reducing the amount of borrowing by households, farmers, and small businesses in that period, which contributed to the severity and duration of the Great Depression.

The U.S. banking system has been made more resilient since that time, but there is still evidence of the effect of a credit crunch on regional U.S. economies. The April 2023 IMF Global Financial Stability Report argued that a credit crunch in the United States could reduce lending by 1%, which would lower GDP growth by almost 0.5 percentage points.

Michael Klein is the executive editor of EconoFact. He is the William L. Clayton Professor of International Economic Affairs at The Fletcher School at Tufts University.

As we enter artificial intelligence’s brave new world, humans have naturally come to fear what the future holds. Do computers like HAL from 2001: A Space Odyssey pose an existential threat? Or in an incident not from Hollywood fiction, an Air Force official’s recent remarks implying that a drone had autonomously changed course and killed its operator, only to be later declared a hypothetical, certainly raised alarm.

Closer to home for most of us, the release of large language models like ChatGPT have renewed worries about automation, reminiscent of earlier fears about mechanization. AI has advanced far beyond rote data-storage tasks and can even pass the bar exam, or write news, or research papers, leading to fears of massive white-collar unemployment.

But, as new research looking at data of job churn over the past two decades finds, the impact of automation on workers and industries is, in fact, pretty hard to predict given the complexity of the labor market, requiring carefully crafted policies that take these nuances into account.

First, changes in exposure to automation are not intuitive: they do not easily mesh with “blue-collar” and “white-collar” jobs, as typically defined. Instead, automation is more closely linked to the tasks and characteristics of each job, such as repetitiveness and face-to-face interactions. That translates to the three most automation-exposed jobs: office and administrative support, production, and business and financial operations occupations.

Meanwhile, the three least automation-exposed jobs are in personal care; installation, maintenance and repair occupations; and teaching. In other words, even with the Internet of Things controlling your HVAC system, it cannot fix itself when it needs new refrigerant, but its smart-panel interface can help the technician diagnose the problem remotely quickly and know what equipment to bring for a repair. But back-end accountants in that company may not fare as well in the AI jobs sweepstakes.

While automation can displace workers, history suggests that new technology also tends to boost productivity and create new jobs. Consider the automobile: while horses and buggies are outdated, we still need humans to drive (at least until autonomous vehicles come to full fruition), and the assembly line helped automate manufacturing with entire new classes of jobs created for every part of a car and all its electronic systems, with almost 1 million U.S. workers in auto manufacturing today.

But automation has continued in the auto industry over the decades, with robots helping to make hard and heavy physical labor tasks easier, without fully displacing workers. So there is a push-pull with automation, and the relative sizes of these countervailing effects remains an area of active scholarly debate.

“ It is rare for an entire job class to disappear overnight; changes mainly take place over generations ”

Second, it is rare for an entire job class to disappear overnight; changes mainly take place over generations. The research shows that newer generations of workers, perhaps deterred by the job insecurity observed in earlier generations and lured by high wages in the technology sector, are less inclined to enter automation-prone jobs than those before them. However, after embarking down those career paths, workers tend to stay in their fields, even if the prospects of automation loom large, likely because reskilling is time-consuming and expensive. It is relatively easy for recent high school graduates to opt for tech-centric college degrees like computer science, but learning new skills like coding is more difficult for mid-career professionals in automation-susceptible fields like manufacturing.

Adjustments to automation can be slow on the business side as well. Incorporating automated technology takes time because modern production tasks tend to be so intertwined that automating one part of a business can affect all other operations. For example, when AT&T, once the country’s largest firm, began replacing telephone operators with mechanical switchboards, they found that operators had become central to the complex production system that grew around them, which is why there are fewer operators today, but some still exist.

Third, the research found that the share of workers in highly automation-exposed occupations tends to be clustered, ranging from about 25% to 36% across commuting zones. The least-exposed areas in the U.S. are across the Mountain West, thanks to the area’s high shares of workers in management, retail sales and construction (which hasn’t had much automation or productivity improvement in decades but additive manufacturing may be a game-changer), as well as those on the East and West coasts, with their more innovative finance and tech industries.

On the other hand, those most exposed to automation tend to be located in the Great Plains and Rust Belt, namely due to agriculture. In spite of the fact that U.S. agriculture has been exposed to automation for over a century (more efficient machines and advances in biotechnology), it has become even more technology-driven recently, making ag workers more likely to be impacted by automation.

So will the robots take over your job soon? More likely, they will make our jobs easier and more efficient. Trying to slow the adoption of technology is both futile and counterproductive: taxing or overregulating tech adoption may backfire, especially given global competitiveness and other countries who may not pause. While the advent of a new era of automation is likely to be both gradually incorporated and result in complements to human labor rather than full replacement, thoughtful policies can help disrupted workers transition to new and better opportunities, ensuring we can harness the transformative power of automation and foster a future of work that benefits all.

Eric Carlson is associate economist at the Economic Innovation Group; DJ Nordquist is EIG’s executive vice president.

Is America going into a recession or not? That depends on who you ask—and how old they are.

Consumer households from their 20s to their 50s are now spending sharply less on their credit and debit cards than they were a year ago reports Bank of America, after crunching the numbers on its customers.

“Regression to the mean” is a powerful force in the financial markets, so it was a good bet that the 60:40 portfolio would have a much better year in 2023 than in 2022.

But not as good a year as it has had so far. That’s important to point out, lest retirees start believing that returns like we’re seeing this year are the norm. They’re not.

The 60:40 portfolio, a default option for many retirees and near-retirees, lost 23.4% last year, assuming the 60% equity portion was invested in the Vanguard Total Stock Market ETF VTI, +1.65%

and the 40% bond portion in the Vanguard Long-Term Treasury ETF VGLT, -0.94%.

That was the worst calendar-year return for the portfolio since the Great Depression.

Through the end of May this year, in contrast, this portfolio rose at an annualized pace of 17.6%. That is more than double the average return since 1793 of 7.7% annualized for an annually rebalanced portfolio (according to data compiled by Edward McQuarrie of Santa Clara University).

Regression to the mean deserves only a minority of the credit for this reversal. That’s because there’s no guarantee that, following a year with as big a loss as 2022’s, the portfolio would produce a gain this year. Strictly speaking, in fact, all that regression to the mean implies for the 60:40 portfolio is that its return this year would be closer to its long-term average than last year’s. A wide range of possible returns are consistent with this implication, of course, including a loss—just so long as that loss is significantly less than 2022’s.

Rather than thanking mean regression, retirees therefore should thank their lucky stars that the 60:40 portfolio’s year-to-date return is coming in at the upper end of this possible range.

But I need not remind you that luck is not a strategy.

It’s also important to remember that regression to the mean cuts both ways. Assuming that the 60:40 portfolio continues performing for all of 2023 at its year-to-date pace, mean regression would imply a smaller return in 2024. That smaller return could still be a gain, of course, but it also could be a loss.

In any case, it’s worth emphasizing that the 60:40 portfolio is a long-term bet, not a market timing tool. As you can see from the accompanying chart, this portfolio’s most recent trailing 20-year annualized return is almost precisely on top of its two-century average of 7.7% annualized. So no regression to the mean is implied when projecting the portfolio’s long-term future return.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at mark@hulbertratings.com.

If there were no tax cheats in America, there would be no Social Security crisis. Benefits could be paid, and payroll taxes kept the same, for the next 75 years.

That’s not me talking. That’s math. It comes from the number crunchers at the Social Security Administration and the Internal Revenue Service.

And it explains why those of us who support Social Security should be pounding the table in outrage over one clause of the Biden-McCarthy debt ceiling deal: The part where the president has to retreat from his crackdown on tax cheats just so McCarthy and the House Republicans would agree to prevent America defaulting on its debts.

It’s just two years since the administration got into law an extra $80 billion for the IRS to beef up enforcement. That was supposed to include hiring an estimated 87,000 IRS agents.

OK, so nobody likes paying taxes and nobody likes the IRS. Cue the inevitable critiques of an IRS tax “army,” and so on. But this isn’t about whether taxes should be higher or lower. It’s about whether everyone should pay the taxes that they owe.

After all, if we’re going to cut taxes, shouldn’t they apply to those of us who obey the laws as well as those who don’t? Or do we just support the “Tax Cuts for Criminals” Act?

Why would any voter rally around a platform of “I stand with tax cheats?”

If this seems abstract, consider the context and how it affects you and your retirement — and the retirements of everyone you know.

Social Security is now running at an $80 billion annual deficit. That’s the amount benefits are expected to exceed payroll taxes this year. (So say the Social Security Administration’s trustees.)

Next year, that deficit is expected to top $150 billion. By 2026, we’re looking at $200 billion and rising. The trust fund will run out of cash by 2034, and without extra payroll taxes will have to slash benefits by a fifth or more.

Over the next 75 years, says the Congressional Budget Office, the entire funding gap for the program will average about 1.7% of gross domestic product per year.

Meanwhile, how much are tax cheats stealing from the rest of us? A multiple of that.

But it still worked out at around 12% of all the taxes people were supposed to pay (including payroll taxes). And around 2.3% of GDP.

Over the next 10 years, based on similar ratios to GDP, that would come to another $3.3 billion.

Sure, Social Security’s trust fund is theoretically separate from the rest of Uncle Sam’s finances. But that’s an accounting issue: A distinction without a difference.

Some people want to cut benefits. Others want to raise the retirement age, which also means cutting benefits. Others want to raise taxes on benefits — which also means cutting benefits. Others want to hike payroll taxes, either on all of us or (initially) only on very high earners.

But if investing some of the trust fund in stocks is a no-brainer, so, too, is insisting everyone obey the law and pay the taxes they actually owe each year. I mean, shouldn’t we do that before we think about raising taxes even further on those who abide by the law?

How could anyone object? Any party that believes in law and order would support enforcing, er, law and order on tax evasion. And any party of fiscal conservatism would support measures, like tax enforcement, to narrow the deficit.

And, actually, any party that truly supported lower taxes for all would be tough on tax evasion: It is precisely this $500 billion in evasion by a small, scofflaw minority that forces the rest of us to pay more. We have, quite literally, a tax on obeying the law.

Social Security has been a vital safety net for retirees, disabled individuals, and surviving family members for decades. However, the program is facing financial challenges that may necessitate changes in the coming years. Let’s explore three potential ways Social Security benefits could change in the future.

Adjustments to the full retirement age

One possible change could involve adjusting the full retirement age (FRA), which is the age at which individuals can receive full Social Security benefits. Currently set at 67 for those born in 1960 or later, some experts argue that increasing the full retirement age could help address the program’s funding shortfall. However, this change could mean longer working lives for future retirees and careful consideration of how it impacts individuals with physically demanding jobs or limited job opportunities later in life.

This change would also result in a smaller benefit for the earliest filers at age 62, since the reductions are based on the amount of time between your filing age and the Full Retirement Age. If the FRA is increased to 68, for example, filing at age 62 would result in a benefit that is only 65% of your Full Retirement Age benefit amount.

In addition, unless the maximum filing age is adjusted, Delayed Retirement Credits (DRCs) would also be limited under such a scenario. Currently when your FRA is 67 you have the opportunity to increase your benefit by 24% (8% per year for DRCs), but if the FRA is 68, the increase would only be 16% at maximum.

Means-testing benefits

Another potential change is means-testing Social Security benefits. Means-testing would involve adjusting benefit amounts based on an individual’s income or assets. Supporters argue that this would ensure benefits are targeted to those who need them most, potentially reducing the strain on the program’s finances. However, critics express concerns about the potential impact on middle-income earners who have paid into the system throughout their working lives and rely on Social Security as a significant part of their retirement income.

An interesting concept I’ve recently seen bandied about involves a trade-off between Social Security benefits and Required Minimum Distributions (RMDs) from retirement plans. Essentially an individual could forgo Social Security benefits (at least partially if not fully) in exchange for looser restrictions on RMDs – allowing for further deferral of taxation on retirement accounts.

Benefit reductions

In order to sustain the Social Security program, benefit reductions might be considered. This could involve various approaches such as adjusting the formula used to calculate benefits or implementing a scaling factor to reduce benefit amounts. While benefit reductions would aim to preserve the long-term viability of Social Security, they could pose challenges for retirees who rely heavily on those benefits to cover essential living expenses.

Most benefit reduction proposals in the pipeline are in concert with expanding the tax base, while at the same time limiting benefits to the upper echelons of earnings levels. In these cases the taxable wage base is either expanded or removed altogether, and the amounts above the current wage base are credited for benefits at a minuscule rate.

It’s important to note that any changes to Social Security benefits would likely be accompanied by broader discussions and careful consideration from policy makers. The goal would be to strike a balance between ensuring the program’s financial stability and protecting the well-being of current and future retirees.

As an individual planning for retirement, it’s crucial to stay informed about potential changes to Social Security benefits. Keeping track of legislative proposals and staying engaged in the conversation can help you adapt your retirement plans accordingly. Consider consulting with a financial adviser who specializes in retirement planning to assess the potential impact on your retirement income and explore other strategies to supplement your savings.

Social Security benefits may undergo changes in the future as policy makers grapple with the program’s financial challenges. Adjustments to the full retirement age, means-testing benefits, and benefit reductions are among the potential changes that could be considered. By staying informed and seeking professional guidance, you can navigate these potential changes and make informed decisions to secure your financial well-being during retirement.

Things move quickly in the world of artificial intelligence. It is easy to sit back and complain about developments that could be disruptive, but sometimes investors are best served by putting emotions aside and observing new developments and how they affect markets. Could AI developments and related trends make you a lot of money?

Below is a new screen showing a group of AI-oriented companies expected to increase their sales most rapidly through 2025, based on consensus estimates among analysts polled by FactSet. Then we show expected revenue growth rates for the largest AI-oriented companies in the screen.

Over the long haul, many businesses might perform more efficiently by employing AI. Maybe this technology can create an economic revolution similar to the one that moved the majority of the working population away from agricultural labor during the 19th and 20th centuries.

Back in February, we screened 96 stocks held by five exchange-traded funds focused on AI and related industries and listed the 20 that analysts thought would rise the most over the following 12 months.

Three months is a long time for AI, and the shakeout hasn’t even started.

There is no way to predict how politicians will react to perceived or real threats of AI and machine learning. And the largest U.S. tech players are doing everything they can to employ the new technology and remain dominant. But that doesn’t mean they will grow more quickly than smaller AI-focused players.

A new AI stock screen

Once again we will begin a screen with these five ETFs:

The Global X Robotics & Artificial Intelligence ETF BOTZ, +0.97%

BOTZ was established 2016 and has $1.8 billion in assets under management. The fund tracks an index of companies listed in developed markets that are expected to benefit from the increased utilization of robotics and AI. There are 44 stocks in the BOTZ portfolio, which is weighted by market capitalization and rebalanced once a year. Its largest holding is Intuitive Surgical Inc. ISRG, +0.53%,

which makes up 10% of the portfolio, followed by Nvidia Corp. NVDA, +3.30%

at 9.4%.

The iShares Robotics and Artificial Intelligence Multisector ETF IRBO, +1.64%

holds 116 stocks that are equal-weighted, as it tracks a global index of companies that derive at east 50% of revenue from robotics or AI, or have significant exposure to related industries. This ETF was launched in 2018 and has $304 million in assets.

The $246 million First Trust Nasdaq Artificial Intelligence & Robotics ETF ROBT, +1.83%

has 107 stocks in its portfolio, with a modified weighting based on how directly companies are involved in AI or robotics. It was established in 2018.

The Robo Global Artificial Intelligence ETF THNQ, +1.81%

has $26 million in assets and was established in 2020. I holds 69 stocks and isn’t concentrated. It uses a scoring system to weight its holdings by percentage of revenue derived from AI, with holdings also subject to minimum market capitalization and liquidity requirements.

The newest ETF on this list is the WisdomTree Artificial Intelligence and Innovation Fund WTAI, +2.42%,

which was established in December and has $13 million in assets and holds 73 stocks in an equal-weighted portfolio. According to FactSet, stocks are handpicked and selected companies “generate at least 50% of their revenue from AI and innovation activities, including those related to software, semiconductors, hardware technology, machine learning and innovative products.”

Altogether and removing duplicates, the five ETFs hold 270 stocks of companies in 23 countries. We first narrowed the list to 197 covered by at least nine analysts and for which consensus sales estimates are available through calendar 2025. We used calendar-year estimates because some companies have fiscal years that don’t match the calendar.

Here are the 20 screened AI-related companies expected by analysts to have the highest compound annual growth rates (CAGR) for sales from 2023 through 2025. Sales estimates are in millions of U.S. dollars. The list also shows which of the above five ETFs holds each stocks.

Click the tickers for more about each company or ETF.

Click here for Tomi Kilgore’s detailed guide to the wealth of information for free on the MarketWatch quote pages.

We have screened for expected revenue growth, rather than for earnings or cash flow, because in a newer tech-oriented business area, investors are most likely to consider the top line as companies sacrifice profits to build market share.

It is important to do your own research if you consider purchasing any individual stock, to form your own opinion about a company’s ability to remain competitive over the long term. Starting from the top of the list, BioXcel Therapeutics Inc. BTAI, -2.47%

is expected to show exponential sales growth, but that is from a low expected baseline this year.

What about the largest AI-related companies held by these ETFs?

Here are the largest 20 companies in the screen by market capitalization, ranked by expected sales CAGR from 2022 through 2025. Once again the sales estimates are in millions of U.S. dollars, but the market caps are in billions.

When investors think of technology stocks, they might automatically gravitate toward “the next big thing,” or to the giant companies that dominate the S&P 500 SPX, -0.40%.

But Robert Stimson, chief investment officer of Oak Associates Funds, makes a case for diversification through exposure to smaller innovators which he believes are “overlooked in this environment.”

The River Oak Discovery Fund RIVSX, +0.98%

invests in tech-oriented companies with market capitalizations of $5 billion or less, with an average of about $2 billion. It has a five-star rating, the highest, from Morningstar, despite having what the investment information firm considers “above average” annual expenses of 1.19% of assets under management. The fund is ranked in the 6th percentile among 546 funds in Morningstar’s “Small Blend” category for five-year performance and in the 13th percentile among 374 funds for 10-year performance. The performance comparisons are net of expenses.

The Black Oak Emerging Technologies Fund BOGSX, +1.54%

has more of a midcap focus, with some small-cap stocks and follows a similar strategy to that of RIVSX. But with no restriction on the size of companies this fund invests in, “we don’t have to sell stocks,” Stimpson said. So long-term holdings of this fund include Apple Inc. AAPL, -0.05%

and Salesforce.com Inc. CRM, +0.69%.

This fund is rated three stars within Morningstar’s “Technology” category and has a lower expense ratio of 1.03%.

Both funds are concentrated. The River Oak Discovery Fund held 34 stocks and the Black Oak Emerging Technologies Fund held 35 stocks as of March 31. Lists of both funds’ largest holdings are below.

During an Interview, Stimpson, who co-manages both funds, said that when investing in the small-cap technology space, he and colleagues identify companies that are “focused on niches.

“I want a company that knows who they are, what they do and do it well, rather than a small company trying to growing into the next Microsoft, Google or Salesforce,” he said.

Stimpson said Oak Associates pays close attention to what corporate management teams say during earnings calls and in presentations, preferring comments related to improving sales and operations with a market niche, rather than expressions of grand visions for exponential growth.

That type of narrow focus can support higher valuations over time, Stimpson said. “They have better execution, a better ability to fend-off competition and they are quality acquisition candidates.”

“ “I caution everyone that until there is revenue, earnings and a product, the hype can be more dangerous than an opportunity.” ”

— Robert Stimpson, chief investment officer at Oak Funds, when discussing AI and ChatGPT.

All of those factors can be important to investors, considering how easily tech giants such as Microsoft Corp. MSFT, +1.00%

or Google holding company Alphabet Inc. GOOGL, +2.89%

GOOG, +2.88%

can begin to compete with smaller innovative companies because they can afford to make such large investments, he said.

Simpson went further, saying that when running screens for “quality” metrics, such as improving free cash flow yields, the Oak Associates team also looks for “shareholder friendly practices.” For example, a company may be repurchasing shares. But are the buybacks lowering the share count significantly (which boosts earnings per share) or are they merely mitigating the dilution caused by the shoveling of new shares to executives as part of their compensation?

Finally, Simpson cautioned investors not to get caught up in tech-focused hype.

“When I talk to our clients, I get questions about AI and ChatGPT and how to play it. People get focused on a new great tech innovation,” he said. “You can replace ChatGPT with bitcoin, metaverse or 3-D printing.”

“I caution everyone that until there is revenue, earnings and a product, the hype can be more dangerous than an opportunity.”

Two examples

These companies are held by theRiver Oak Discovery Fund and the Black Oak Emerging Technologies Fund.

Cirrus Logic Inc. CRUS, -2.37%

is the largest holding of the River Oak Discovery Fund. Stimpson calls the company “a derivative play on the success of Apple.”

“They are focused on the chips that go into mobile and [vehicles],” as well as the needs of their customers, including Apple, “rather than problem areas of the chip sector, such as memory or PCs. They are not talking about chips for AI, for example,” Stimpson said.

Cirrus focuses on systems and related software used in audio systems..

Kulicke & Soffa Industries Inc. KLIC, +1.92%

makes equipment, tools and related software used by a variety of manufacturers of computer chips and integrated electronic devices.

Stimpson likes the company as a long-term play on the worldwide disruption in semiconductor manufacturing and supply, in the wake of the Covid-19 pandemic. “All chip companies learned that any supply disruption in Southeast Asia is a problem. Over time, the opportunities for semiconductor equipment makers are very good. There will be more plants in more locations, so more equipment,” he said.

He said KLICK was in a “protected” position, with returns on equity of about 20% and free cash flow yields of about 10%.

Top holdings of the funds

Here are the largest 10 holdings of the River Oak Discovery Fund as of March 31:

Short sellers see major trouble ahead for the U.S. economy and the stock market. We ignore that at our peril.

You might dismiss the short sellers’ bearishness because—by definition—they bet on lower prices and therefore are predisposed to seeing the glass as half empty. Actually, however, short sellers’ collective bearishness fluctuates widely over time. And right now they are more bearish than they’ve been in a long time.

When it comes to investing, some people don’t think in terms of thousands of dollars, tens of thousands, or even millions.

They think in hundreds of millions, or even billions. They have so much money they actually set up a private company, known as a “family office,” to manage all the loot.

Oil demand is likely to hold up longer than many people expect during the anticipated transition to electric vehicles. And changes in the industry point to oilfield services companies as good long-term growth investments as offshore production ramps up.

Below is a list of oil producers and related companies favored by two analysts who have followed the industry for decades.

The stock market, as measured by the S&P 500 Index SPX, has struggled to maintain the rally that began in mid-March, and now we are getting new sell signals from some of our internal indicators.

SPX was turned back by resistance near 4200 for the third time since last August. That is an extremely strong resistance area now. Moreover, there is further resistance at 4300. On the downside for SPX, there is technically support at 3970, where the small gaps exist on the SPX chart. A close below 3950 would be extremely bearish and…

David Rosenberg honestly doesn’t want to be bearish on stocks or bash the Federal Reserve. The veteran market strategist will get no satisfaction if he’s right about Americans having to slog through recession and consequently endure deflation, job losses and a wallop to the stock market.

“As I play the role of economic detective, I can see the smoking gun,” says Rosenberg, a former chief North American economist at Merrill Lynch and now president of Toronto-based Rosenberg Research.