David Solomon, Chairman & CEO Goldman Sachs, speaking on CNBC’s Squawk Box at the World Economic Forum Annual Meeting in Davos, Switzerland on Jan. 17th, 2024.

Adam Galici | CNBC

Goldman Sachs is scheduled to report first-quarter earnings before the opening bell Monday.

Here’s what Wall Street expects:

Earnings: $8.56 per share, according to LSEG

Revenue: $12.92 billion, according to LSEG

Trading Revenue: Fixed income of $3.64 billion and equities of $2.95 billion, per StreetAccount

Investing Banking Revenue: $1.77 billion, per StreetAccount

Goldman Sachs CEO David Solomon has taken his lumps in the past year, but hope is building for a turnaround.

Dormant capital markets and missteps tied to Solomon’s ill-fated push into retail banking should give way to stronger results this year.

Rivals JPMorgan Chase and Citigroup posted better-than-expected trading results and a rebound in investment banking fees in the first quarter; investors will be disappointed if Goldman doesn’t show similar gains.

Unlike more diversified rivals, Goldman gets most of its revenue from Wall Street activities. That can lead to outsized returns during boom times and underperformance when markets don’t cooperate.

After pivoting away from retail banking, Goldman’s new emphasis for growth has centered on its asset and wealth management division. The business could see gains from buoyant markets at the start of the year, though it also has taken write-downs tied to commercial real estate in the past.

Solomon may also field questions about the latest examples of an exodus in senior managers, including his global treasurer Philip Berlinski and Beth Hammack, co-head of the bank’s global financing group.

On Friday, JPMorgan, Citigroup and Wells Fargo each posted quarterly results that topped estimates.

This story is developing. Please check back for updates.

Ebrahim Poonawala, Band of America Securities head of North American banks research, joins ‘Power Lunch’ to discuss if he saw any concerns from bank earnings, what the bank stocks are reacting to, and more.

Sarat Sethi, DCLA managing partner, joins ‘Power Lunch’ to discuss what the managing partner makes of recent economic performance, what Sethi made of recent bank earnings, and what is changing with equity markets.

Wells Fargo reported better-than-expected earnings results on Friday, but some weakness under the hood is putting a lid on the bank’s stock. Stay the course: Shares should move higher as management continues to shake off regulatory punishments for past misdeeds. Total revenue for the three months ended Mar. 31 ticked up less than 1% over last year, to $20.86 billion, exceeding analysts’ expectations of $20.2 billion, according to LSEG. Adjusted earnings of $1.26 per share was nicely above Wall Street’s consensus estimate of $1.11 per share, LSEG data showed. Note: The $1.26 EPS excludes a 6-cent per share ($284 million hit to net income) negative impact from a Federal Deposit Insurance Corporation (FDIC) special assessment for the rescue of regional banks after last year’s failure of Silicon Valley Bank. This special assessment charge was a 40-cent per share headwind in the fourth quarter of 2023. Wells Fargo Why we own it : We bought Wells Fargo as a turnaround story under CEO Charlie Scharf. He’s been making progress cleaning up the bank’s act and fixing its previously bloated cost structure after a series of misdeeds before his tenure. Scharf has also been working to get the Fed’s $1.95 trillion asset cap lifted and to boost Wells Fargo’s fee-generating revenue streams. Competitors : Bank of America and Citigroup Weight in Club portfolio : 4.76% Most recent buy : Feb. 24, 2022 Initiated : Jan. 8, 2021 Bottom line The results skew positive, even with some key line-item misses. For one, the bank’s overall efficiency ratio was a tad higher than expected. (The ratio is non-interest expense divided by total revenue, the lower the ratio the better the efficiency). However, we expect to see that number come down over time as management continues to address regulatory concerns and makes progress toward the ultimate removal of the asset cap. In addition, the bank’s net interest margin came up short, and therefore net interest income. We aren’t too surprised given that interest rates are a double-edged sword for banks. Higher rates mean higher revenue generation on loans; they also mean higher funding costs (interest payments on deposits) as customers withdraw deposits in search of higher yields elsewhere. None of this is news: We’ve seen this dynamic play out for several quarters already. That said, in general, higher rates are a net positive for Wells Fargo’s bottom line. Many positives outweighed the negatives. For example, non-interest expenses increased this quarter to a level above Street estimates, but non-interest income advanced at a faster rate and ahead of expectations. Likewise, the bank’s tangible book value per share came in a bit soft but was more than offset by better-than-expected return on tangible common equity performance — a key metric that investors take into heavy consideration when determining the appropriate valuation multiple to place on a bank’s stock. Also a plus: The bank’s provisions for credit losses were much lower than expected. That’s especially good considering the concerns many had regarding Wells Fargo’s commercial real estate exposure and increased credit usage by consumers as their pandemic savings diminished. On the post-earnings call with investors, CEO Charles Scharf said: “We continue to see strength in the U.S. economy, spending patterns of consumers using our debit and credit cards remain generally consistent and continued to grow year over year. Consumer credit is performing as we expect, wholesale credit continues to perform well, and our views around commercial real estate have not significantly changed since last quarter.” On the capital return front, we got a big step up in returns to shareholders, with the bank repurchasing $6.1 billion worth of stock (112.5 million shares) in the first quarter. That’s a major increase from the $2.4 billion (51.7 million shares) repurchased in the fourth quarter. Moreover, despite the CET 1 ratio — which compares a bank’s capital against its risk-weighted assets — coming in a tick below expectations, it’s nothing to be concerned about. There’s plenty of excess capital left for management to return to shareholders. Wells Fargo is on the right path to increasing efficiencies, driving ROTCE (return on average tangible common shareholders’ equity) toward management’s goal of 15%, and having its regulator-imposed asset cap removed. As a result, we are increasing our price target on WFC shares to $62 from $60, but maintaining our 2 rating as we look for a better entry point. WFC YTD mountain Wells Fargo YTD Guidance Wells Fargo’s management team maintained its outlook for full-year 2024 net interest income: 7% to 9% lower than the $52.4 billion level achieved in 2023. This implies a range of $47.7 billion to $48.7 billion, a miss versus the $48.8 billion consensus estimate coming into the print. We don’t like a miss on guidance. However, bank interest income estimates depend on interest rates, a factor Wells can’t control. Management said on Tuesday that it’s still early in the year and ultimately “the amount of net interest income we earn will depend on a variety of factors, many of which are uncertain, including deposit balances mix and pricing, the absolute level of interest rates and the shape of the yield curve and loan demand.” Keep in mind that management has been very focused on decreasing the revenue contribution from interest-based revenues, focusing instead on growing the non-interest, fee-based revenues, a move we strongly support as it serves to reduce volatility and reliance on interest rate dynamics that management can’t control. “We’re beginning to see early signs of share and fee growth which will be important as we diversify our revenues and reduce net interest income as a percentage of revenue,” the company said. Full-year non-interest expense guidance was also left unchanged at roughly $52.6 billion. That’s a bit below the $52.95 billion expected, which is a positive. First-quarter results Consumer banking and lending revenue fell nearly 3% year over year to $9.09 billion. Consumer and small business banking (CSBB) revenue fell 4% as the tailwind of higher debit card fees was more than offset by lower deposit balances. Within consumer lending, home lending was flat versus last year and up 3% sequentially. Credit card revenue increased 6% annually and 3% on a sequential basis. Auto loan revenue was down 23% year over year and down 10% sequentially. Personal lending increased 7% from last year but declined 1% sequentially. Commercial banking revenue fell 5% to $3.15 billion. Middle-market banking revenue declined 4% year over year, while asset-based lending and leasing revenue was down 7% annually. Non-interest expenses fell 4% due to a reduction in personnel expenses and efficiency gains. Corporate and investment banking revenue increased nearly 2% to $4.98 billion. Total banking revenue increased 5% year over year, as a 3% decline in lending and a 13% decline in treasury management and payments revenues were more than offset by a 69% increase in investment banking revenues. Commercial real estate revenue fell 7% as the headwind of lower loan balances was only partially offset by increased commercial mortgage-backed securities volumes. Markets revenue was up 2% on the back of a 6% increase in fixed income, currencies, and commodities (FICC) revenue, and a 3% increase in equities revenues. Non-interest expenses increased 5% annually, due to higher operating costs, which were only partially offset by efficiency gains. Wealth and investment management revenue advanced about 2% to $3.74 billion. Net interest income fell 17% year over year as deposits declined due to customers reallocating cash into higher-yielding securities. Non-interest income increased 9% thanks to higher asset-based fees driven by an increase in market valuations. Non-interest expenses were up 6% annually as higher revenue-related compensation was only partially offset by efficiency initiatives. (Jim Cramer’s Charitable Trust is long WFC. See here for a full list of the stocks.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

Wells Fargo customers use the ATM at a bank branch on August 08, 2023 in San Bruno, California.

Justin Sullivan | Getty Images

Wells Fargo reported better-than-expected earnings results on Friday, but some weakness under the hood is putting a lid on the bank’s stock. Stay the course: Shares should move higher as management continues to shake off regulatory punishments for past misdeeds.

Citigroup on Friday posted first-quarter revenue that topped analysts’ estimates, helped by better-than-expected results in the bank’s investment banking and trading operations.

Here’s how the company performed, compared with estimates from LSEG, formerly known as Refinitiv:

Earnings: $1.86 per share, adjusted, vs. $1.23 expected

Revenue: $21.10 billion vs. $20.4 billion expected

The bank said profit fell 27% from a year earlier to $3.37 billion, or $1.58 a share, on higher expenses and credit costs. Adjusting for the impact of FDIC charges as well as restructuring and other costs, Citi earned $1.86 per share, according to LSEG calculations.

Revenue slipped 2% to $21.10 billion, mostly driven by the impact of selling an overseas business in the year-earlier period.

Investment banking revenue jumped 35% to $903 million in the quarter, driven by rising debt and equity issuance, topping the $805 million StreetAccount estimate.

Fixed income trading revenue fell 10% to $4.2 billion, edging out the $4.14 billion estimate, and equities revenue rose 5% to $1.2 billion, topping the $1.12 billion estimate.

The bank also posted an 8% gain to $4.8 billion in revenue in its Services division, which includes businesses that cater to the banking needs of global corporations, thanks to rising deposits and fees.

Shares of the bank fell nearly 2% Friday.

Citigroup CEO Jane Fraser previously said that her sweeping corporate overhaul would be complete by March, and that the firm would give an update to severance expenses along with first-quarter results.

“Last month marked the end to the organizational simplification we announced in September,” Fraser said in the earnings release. “The result is a cleaner, simpler management structure that fully aligns to and facilitates our strategy.

Last year, Fraser announced plans to simplify the management structure and reduce costs at the third-biggest U.S. bank by assets. The bank on Friday reiterated its medium term targets for returns hitting at least 11% and generating at least $80 billion in revenue this year.

Jamie Dimon, President and CEO of JPMorgan Chase, speaking on CNBC’s “Squawk Box” at the World Economic Forum Annual Meeting in Davos, Switzerland, on Jan. 17, 2024.

Adam Galici | CNBC

JPMorgan Chase is scheduled to report first-quarter earnings before the opening bell Friday.

Here’s what Wall Street expects:

Earnings: $4.11 a share, according to LSEG

Revenue: $41.85 billion, according to LSEG

Net interest income: $23.18 billion, according to StreetAccount

Trading Revenue: Fixed income of $5.19 billion and equities of $2.57 billion, according to StreetAccount

JPMorgan will be watched closely for clues on how banks fared at the start of the year.

While the biggest U.S. bank by assets has navigated the rate environment well since the Federal Reserve began raising rates two years ago, smaller peers have seen their profits squeezed.

The industry has been forced to pay up for deposits as customers shift cash into higher-yielding instruments, squeezing margins. Concern is also mounting over rising losses from commercial loans, especially on office buildings and multifamily dwellings, and higher defaults on credit cards.

Still, large banks are expected to outperform smaller ones this quarter, and expectations for JPMorgan are high. Analysts believe the bank can boost guidance for 2024 net interest income as the Federal Reserve is forced to maintain interest rate levels amid stubborn inflation data.

Analysts will also want to hear what CEO Jamie Dimon has to say about the economy and the industry’s efforts to push back against efforts to cap credit card and overdraft fees.

Wall Street may provide some help this quarter, with investment banking fees for the industry up 11% from a year earlier, according to Dealogic.

Shares of JPMorgan have jumped 15% this year, outperforming the 3.9% gain of the KBW Bank Index.

Sergio Ermotti, CEO of Swiss banking giant UBS, during the group’s annual shareholders meeting in Zurich on May 2, 2013.

Fabrice Coffrini | Afp | Getty Images

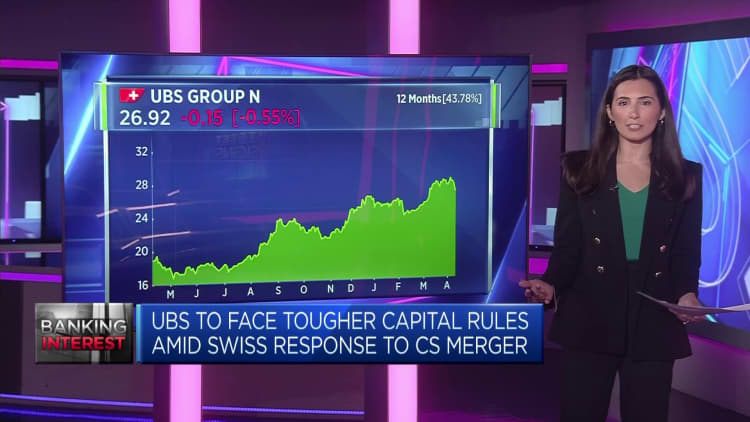

Switzerland’s tough new banking regulations create a “lose-lose situation” for UBS and may limit its potential to challenge Wall Street giants, according to Beat Wittmann, partner at Zurich-based Porta Advisors.

In a 209-page plan published Wednesday, the Swiss government proposed 22 measures aimed at tightening its policing of banks deemed “too big to fail,” a year after authorities were forced to broker the emergency rescue of Credit Suisse by UBS.

The government-backed takeover was the biggest merger of two systemically important banks since the Global Financial Crisis.

At $1.7 trillion, the UBS balance sheet is now double the country’s annual GDP, prompting enhanced scrutiny of the protections surrounding the Swiss banking sector and the broader economy in the wake of the Credit Suisse collapse.

Speaking to CNBC’s “Squawk Box Europe” on Thursday, Wittmann said that the fall of Credit Suisse was “an entirely self-inflicted and predictable failure of government policy, central bank, regulator, and above all [of the] finance minister.”

“Then of course Credit Suisse had a failed, unsustainable business model and an incompetent leadership, and it was all indicated by an ever-falling share price and by the credit spreads throughout [20]22, [which was] completely ignored because there is no institutionalized know-how at the policymaker levels, really, to watch capital markets, which is essential in the case of the banking sector,” he added.

The Wednesday report floated giving additional powers to the Swiss Financial Market Supervisory Authority, applying capital surcharges and fortifying the financial position of subsidiaries — but stopped short of recommending a “blanket increase” in capital requirements.

Wittman suggested the report does nothing to assuage concerns about the ability of politicians and regulators to oversee banks while ensuring their global competitiveness, saying it “creates a lose-lose situation for Switzerland as a financial center and for UBS not to be able to develop its potential.”

He argued that regulatory reform should be prioritized over tightening the screws on the country’s largest banks, if UBS is to capitalize on its newfound scale and finally challenge the likes of Goldman Sachs, JPMorgan, Citigroup and Morgan Stanley — which have similarly sized balance sheets, but trade at s much higher valuation.

“It comes down to the regulatory level playing field. It’s about competences of course and then about the incentives and the regulatory framework, and the regulatory framework like capital requirements is a global level exercise,” Wittmann said.

“It cannot be that Switzerland or any other jurisdiction is imposing very, very different rules and levels there — that doesn’t make any sense, then you cannot really compete.”

In order for UBS to optimize its potential, Wittmann argued that the Swiss regulatory regime should come into line with that in Frankfurt, London and New York, but said that the Wednesday report showed “no will to engage in any relevant reforms” that would protect the Swiss economy and taxpayers, but enable UBS to “catch up to global players and U.S. valuations.”

“The track record of the policymakers in Switzerland is that we had three global systemically relevant banks, and we have now one left, and these cases were the direct result of insufficient regulation and the enforcement of the regulation,” he said.

“FINMA had all the legal backdrop, the instruments in place to address the situation but they didn’t apply it — that’s the point — and now we talk about fines, and that sounds like pennywise and pound foolish to me.”

How the Federal Reserve will proceed with interest rate policy will be top of mind for investors next week when the latest inflation numbers are reported. That price data comes at a tricky time as markets attempt to maneuver around rising Treasury yields. Stocks rallied on Friday after parts of the March jobs report assured investors the central bank remains on track to cut rates this year. The number of jobs added to the U.S. economy in March blew past expectations, underscoring the labor market’s strength. But average hourly earnings matched forecasts, suggesting the labor market, and the broader economy, aren’t really overheating. Currently, the CME FedWatch Tool shows markets are pricing in three rate cuts this year, starting in June. But Wall Street will gain greater insight next week into what the Fed governors are looking at when March consumer and producer price indexes are released. Investors have mostly shrugged off recent reports suggesting inflation is stickier than anticipated, saying much of the uptick in January , for example, was attributable to seasonal factors. March numbers could confirm for investors whether inflation is indeed heading toward the Fed’s 2% target, or if they need to revisit their base case assumptions for interest rates. A strong inflation reading next week could throw a wrench into this year’s extraordinary equity rally, especially as concern mounts that the market is overbought. IEF YTD mountain Price of iShares 7-10 Year Treasury Bond ETF this year. “A lot of the momentum and breadth from Q4 and Q1 are pretty bullish signposts, but we’re also pretty stretched here in the near term,” said Ross Mayfield, investment strategy analyst at Baird. “Sentiment is bullish, positioning is pretty aggressive. The market continues to take rate cuts out of the picture. And so, I think in the absence of an upside catalyst, a push higher in yields could be a problem for the equity market in the near term.” “I would expect a little more volatility, certainly than we saw in Q1, and potentially a minor correction here,” Mayfield added. On Friday, stock benchmarks registered a losing week amid spiking oil prices and rising Treasury yields. The Dow Jones Industrial Average closed lower by 2.3% on the week, while the S & P 500 and Nasdaq Composite fell by about 1% and 0.8%, respectively. West Texas Intermediate crude oil futures topped $87 a barrel this week, reaching a five-month high. The 10-year Treasury yield hit 4.4% on Friday, up from 4.2% last week. Meanwhile, investor sentiment surveys were looking stretched. .SPX mountain 2023-10-31 The S & P 500 since late October. Near-term pressure Forecasts for next week’s data point to Wall Street expecting continued progress in the fight against inflation. Economists polled by FactSet anticipate the March consumer price index will show prices rising by 0.3% on a monthly basis, less than February’s 0.4% advance. Similarly, the March producer price index is expected to show an increase of 0.5%, according to FactSet consensus estimates. That’s lower than the 0.6% gain in prior month. But some investors remain concerned inflation could pick up in the months ahead of the June Fed meeting, which could alter market expectations for interest rates. Hedge fund manager David Einhorn told CNBC’s Scott Wapner this week he anticipates inflation to reaccelerate , noting he’s made gold, a safe haven asset, a large position in his portfolio. On Friday, Fed Governor Michelle Bowman said that another rate hike , not a cut, could be needed if inflation remains sticky. Others are concerned that recent signals point to a stock market that’s in for a near-term correction. Bespoke Investment Group found that sentiment is at historically high levels, with the bull-bear spread measured by Investors Intelligence and the American Association of Individual Investors in the 96th percentile, measured by data going back to 1997. Historically, high readings means lackluster future returns, Bespoke found. On average, stocks typically fall slightly after the bullish reading, it said. Over the next three months, they average a 1 percentage point gain. Over the next year, they notch an average advance of almost three percentage points. Constructive upside Regardless, many investors remain optimistic that stocks can continue to rise, citing a recent broadening out in the rally and a resilient economy as constructive signals for markets. U.S. Bank’s Tom Hainlin has a 5,520 year-end target on the S & P 500, preferring U.S. equities over non-U.S., and large cap companies over small cap. He anticipates that more stocks participating in the up move will benefit sectors such as materials and energy. “We would say we’re still optimistic about more of a melt up in equity prices,” Hainlin said. “And that’s based on durability of earnings estimates for the year.” Jamie Myers, securities analyst at Laffer Tengler, is also positive on equities. He spies opportunities in dividend growth stocks, saying investors should choose companies that have recently hiked dividends, such as Walmart . The move signals management confidence in future earnings. Next week will also bring the start of the first quarter earnings season. Next Friday, results from the country’s largest banks, from Citigroup to JPMorgan Chase to Wells Fargo , are on deck. Minutes from the most recent Federal Open Market Committee meeting are also due next Wednesday. Week ahead calendar All times ET. Monday April 8 Tuesday April 9 6 a.m. NFIB Small Business Index (March) Wednesday April 10 8:30 a.m. Consumer Price Index (CPI) (March) 8:30 a.m. Hourly Earnings final (March) 8:30 a.m. Average Workweek final (March) 10 a.m. Wholesale Inventories final (February) 2 p.m. Treasury Budget NSA (March) 2 p.m. FOMC Minutes Earnings: Delta Air Lines Thursday April 11 8:30 a.m. Continuing Jobless Claims (3/30) 8:30 a.m. Initial Claims (04/06) 8:30 a.m. Producer Price Index PPI Earnings: CarMax Friday April 12 8:30 a.m. Export Price Index (March) 8:30 a.m. Import Price Index (March) 10 a.m. Michigan Sentiment preliminary (April) Earnings: State Street , Wells Fargo , JPMorgan Chase , Progressive , Citigroup

Mike Mayo, Wells Fargo Securities head of U.S. large-cap bank research, joins ‘Squawk Box’ to discuss the latest market trends, why Citi is his top bank stock pick, and more.

A Citibank branch in the central business district of Singapore on Feb. 12, 2018.

Ore Huiying | Bloomberg | Getty Images

New York Attorney General Letitia James on Tuesday suedCitibank for allegedly failing to protect and reimburse victims of electronic fraud.

The suit claims that Citi does not have strong protections in place to prevent unauthorized account takeovers, misleads victims of fraud and illegally denies reimbursements, according to a release. The attorney general’s office said the alleged failure on Citi’s part has cost New York account holders millions of dollars, and in some cases, their entire life savings.

“Banks are supposed to be the safest place to keep money, yet Citi’s negligence has allowed scammers to steal millions of dollars from hardworking people,” James said in a statement. “Many New Yorkers rely on online banking to pay bills or save for big milestones, and if a bank cannot secure its customers’ accounts, they are failing in their most basic duty.”

Citigroup, the parent company of Citibank, has struggled with risk management and controls in the past. Former executives have said the bank — the product of decades of mergers that created a patchwork of technology systems — underinvested in its infrastructure.That was evident when Citigroup accidentally sent almost $900 million to Revlon’s lenders in 2020.

Later that year, banking regulators fined Citigroup $400 million and ordered the firm to improve its risk management systems. Since taking over in 2021, CEO Jane Fraser has pushed to improve the bank’s technology and appease regulators.

The New York lawsuit includes specific people who had thousands of dollars stolen from their accounts and said the bank did not reimburse them.

In a statement, Citi said the bank “works extremely hard” to prevent threats and assist customers who become victims of fraud.

“Banks are not required to make customers whole when those customers follow criminals’ instructions and banks can see no indication the customers are being deceived. However, given the industry-wide surge in wire fraud during the last several years, we’ve taken proactive steps to safeguard our clients’ accounts with leading security protocols, intuitive fraud prevention tools, clear insights about the latest scams, and driving client awareness and education,” the company said in a statement. “Our actions have reduced client wire fraud losses significantly, and we remain committed to investing in fraud prevention measures to help our clients secure their accounts against emerging threats.”

James alleged in the lawsuit that Citi must reimburse victims of fraud under the Electronic Fund Transfer Act.

Traders work on the floor of the New York Stock Exchange during afternoon trading on January 17, 2024 in New York City.

Michael M. Santiago | Getty Images News | Getty Images

This report is from today’s CNBC Daily Open, our new, international markets newsletter. CNBC Daily Open brings investors up to speed on everything they need to know, no matter where they are. Like what you see? You can subscribe here.

Dow falls three days The blue-chip Dow Jones Industrial Average fell for the third straight day Wednesday. Wall Street’s other two main indexes also dropped as better-than-expected retail sales data helped lift Treasury yields. In Asia, China stocks hit five-year lows, while Hong Kong stocks rebounded. Sectoral declines were led by mining stocks.

Strong retail sales U.S. retail sales came in higher than expected for the last month of 2023 in a sign that holiday shopping picked up. Retail sales for December increased 0.6% vs. the 0.4% rise expected in a Dow Jones estimate. The rise was driven by clothing, accessories and online shopping.

Dimon in Davos JPMorgan Chase CEO Jamie Dimon was one of the more highly anticipated guests at the World Economic Forum in Davos, Switzerland. Dimon discussed a variety of topics ranging from financial to geopolitical risks. He was also seen praising former U.S. President Donald Trump’s stance on the U.S. economy, immigration and taxes.

Singapore minister face corruption charges Singapore Transport Minister S Iswaran resigned as he faces corruption charges, the first for a cabinet minister in the island country. He pleaded not guilty to 24 charges of obtaining gratification as a public servant, two charges of corruption and one charge of obstructing the course of justice.

[PRO] Citi says how to invest in the next AI boom Citi says it is definitely “not too late” for investors to invest in the “exponential growth” of AI technology. And after Nvidia sparked the AI boom, soaring over 200% last year, the investment bank now names its top plays for 2024.

It’s only the third week of the new year and markets are slowly heading into a cycle of good data being received as bad news — at least from an equity standpoint.

Treasury yields, however, have risen this week boosted by comments from Federal Reserve Governor Christopher Waller on Tuesday. The yield on the benchmark 10-year Treasury note continued to trade higher Wednesday, crossing the 4% mark on the back of better-than-expected U.S. retail sales for December.

The data showed American consumers somewhat loosened their purse strings in the last month of 2023. But for Wall Street, that was hardly any reason to celebrate based on how aggressively markets have been pricing in interest rate cuts by the Federal Reserve.

Waller’s comments on Tuesday at Davos about the U.S. central bank taking its time to cut rates this year, came as a sharp contrast to markets expecting the Fed’s first rate cut of 2024 to come as early as March.

“The Fed was already hammering away on its ‘no rush to cut rates’ message, and today’s stronger-than-expected retail sales won’t give them any reason to change their tune,” said Chris Larkin, managing director of trading and investing for E-Trade from Morgan Stanley.

About 55% of traders tracked by the CME Group’s FedWatch tool expect a 25 basis point rate cut in March, falling from 63% a day earlier.

Traders work on the floor of the New York Stock Exchange during afternoon trading on January 17, 2024 in New York City.

Michael M. Santiago | Getty Images News | Getty Images

This report is from today’s CNBC Daily Open, our new, international markets newsletter. CNBC Daily Open brings investors up to speed on everything they need to know, no matter where they are. Like what you see? You can subscribe here.

Strong retail sales U.S. retail sales came in higher than expected for the last month of 2023 in a sign that holiday shopping picked up. Retail sales for December increased 0.6% vs. the 0.4% rise expected in a Dow Jones estimate. The rise was driven by clothing, accessories and online shopping.

Dimon in Davos JPMorgan Chase CEO Jamie Dimon was one of the more highly anticipated guests at the World Economic Forum in Davos, Switzerland. Dimon discussed a variety of topics ranging from financial to geopolitical risks. He was also seen praising former U.S. President Donald Trump’s stance on the U.S. economy, immigration and taxes.

Apple Watch sales banned in U.S. again The U.S. Court of Appeals for the Federal Circuit reinstated a sales ban on Apple’s watches with blood oxygen sensors. The ban will take effect Thursday, affecting both the Apple Watch Series 9 and Ultra 2 models. The injunction stems from an intellectual property dispute with medical device maker Masimo.

[PRO] Cheap energy stocks The pros say some pockets of the energy market are poised for a jump after taking a beating last year. The energy sector was the second biggest loser on the S&P 500 last year. The CNBC Pro Screener Tool says they could still do well as companies in the sector are cheap and are seen rising over 10% their average price targets.

It’s only the third week of the new year and markets are slowly heading into a cycle of good data being received as bad news — at least from an equity standpoint.

Treasury yields, however, have risen this week boosted by comments from Federal Reserve Governor Christopher Waller on Tuesday. The yield on the benchmark 10-year Treasury note continued to trade higher Wednesday, crossing the 4% mark on the back of better-than-expected U.S. retail sales for December.

The data showed American consumers somewhat loosened their purse strings in the last month of 2023. But for Wall Street, that was hardly any reason to celebrate based on how aggressively markets have been pricing in interest rate cuts by the Federal Reserve.

Waller’s comments on Tuesday at Davos about the U.S. central bank taking its time to cut rates this year, came as a sharp contrast to markets expecting the Fed’s first rate cut of 2024 to come as early as March.

“The Fed was already hammering away on its ‘no rush to cut rates’ message, and today’s stronger-than-expected retail sales won’t give them any reason to change their tune,” said Chris Larkin, managing director of trading and investing for E-Trade from Morgan Stanley.

About 55% of traders tracked by the CME Group’s FedWatch tool expect a 25 basis point rate cut in March, falling from 63% a day earlier.

U.S. Federal Reserve Board Chairman Jerome Powell speaks during a news conference at the headquarters of the Federal Reserve on December 13, 2023 in Washington, DC.

Win Mcnamee | Getty Images

This report is from today’s CNBC Daily Open, our international markets newsletter. CNBC Daily Open brings investors up to speed on everything they need to know, no matter where they are. Like what you see? You can subscribe here.

Markets start week lower U.S. stocks started the shortened week lower on Tuesday as investors closely watched fourth-quarter earnings, while tracking an uptick in Treasury yields after a Federal Reserve official said the central bank’s interest rate cutting cycle could be slower than what Wall Street expected. Stocks in Asia were lower, as Hong Kong led losses after tumbling 3%. China shares also fell after the country missed fourth quarter GDP estimates but met its year-end growth target of 5%.

Slower pace of Fed cuts Federal Reserve Governor Christopher Waller said there will be monetary policy loosening this year but the central bank could do it at a slower pace. “In many previous cycles … the FOMC cut rates reactively and did so quickly and often by large amounts.” For this cycle, he said, “I see no reason to move as quickly or cut as rapidly as in the past.”

China’s growth Official data showed China’s economy grew at a pace of 5.2% in 2023, exceeding Beijing’s 5% growth target for the year by a sliver. For the first time since the summer, China posted youth jobless rates which surged to 14.9% for December. The country temporarily stopped reporting the jobless rate for young people last year, saying it had to reassess its methods. Youth unemployment previously recorded a reading of over 20%.

More Big Bank earnings Goldman Sachs and Morgan Stanley reported earnings on Tuesday, wrapping up results for Wall Street’s biggest six lenders. Morgan Stanley’s fourth quarter revenue topped analysts’ estimates but the bank warned of economic and geopolitical risks. Goldman Sachs exceeded expectations, boosted by higher asset and wealth management revenue.

[PRO] ‘Buy the dip’ Morgan Stanley highlights its key picks in Europe’s technology hardware sector after a “rollercoaster year” in 2023. The investment bank says the sector could recover as excitement grows around themes like artificial intelligence, advanced packaging, silicon carbide and gate-all-around transistors.

Federal Reserve Governor Christopher Waller said there’s “no reason” for the central bank to “move as quickly” in its approach to lower interest rates this year. His comments were in sharp contrast to the aggressive policy loosening that markets are expecting this year.

Traders still see a more than 64% chance of the Fed cutting interest rates by 25 basis points to 5%-5.25% range at its meeting in March, according to the CME Group’s FedWatch tool. Those bets came down substantially from a near 77% chance of rate cuts on Friday, when data showed producer prices unexpected dropped in December.

In Asia hours, China reported its highly anticipated economic growth figures along with an unexpected print on youth unemployment, which the country abruptly stopped reporting since last summer.

Dan Wang, chief economist at Hang Seng Bank told CNBC’s Street Signs Asia she was surprised by the improvement in youth unemployment: “I can see that it is a result of government efforts and not so much improving economic fundamentals.”

China’s economy grew at 5.2% for all of 2023, above the 5% growth target it had set for itself at the beginning of the year. For the fourth quarter, it also grew at a pace of 5.2% — falling short of a Reuters poll expectation of 5.3%.

Artificial intelligence remained a hot topic, with Microsoft CEO Satya Nadella advocating for its uses, noting that more countries are now talking about AI in similar ways.

“I think [a global regulatory approach to AI is] very desirable, because I think we’re now at this point where these are global challenges that require global norms and global standards,” Nadella said.

A trader reacts as a screen displays the Fed rate announcement on the floor of the New York Stock Exchange (NYSE) in New York City, U.S., December 13, 2023.

Brendan Mcdermid | Reuters

This report is from today’s CNBC Daily Open, our international markets newsletter. CNBC Daily Open brings investors up to speed on everything they need to know, no matter where they are. Like what you see? You can subscribe here.

Markets start week lower U.S. stocks started the shortened week lower on Tuesday as investors closely watched fourth-quarter earnings, while tracking an uptick in Treasury yields after a Federal Reserve official said the central bank’s interest rate cutting cycle could be slower than what Wall Street expected. European stocks ended the session lower, with fashion brand Hugo Boss tumbling 9% after lower than expected earnings.

Slower pace of Fed cuts Federal Reserve Governor Christopher Waller said there will be monetary policy loosening this year but the central bank could do it at a slower pace. “In many previous cycles … the FOMC cut rates reactively and did so quickly and often by large amounts.” For this cycle, he said, “I see no reason to move as quickly or cut as rapidly as in the past.”

China’s growth Speaking at the at the World Economic Forum in Davos, Switzerland, Chinese Premier Li Qiang said China’s economy grew by around 5.2% in 2023 — slightly better than the official target of around 5%. It comes as Beijing is set to release official GDP numbers on Wednesday. A Reuters poll also forecasts 5.2% growth for China in 2023. Premier Li also said innovations in technology shouldn’t be used as means to contain or restrict other countries.

More Big Bank earnings Goldman Sachs and Morgan Stanley reported earnings on Tuesday, wrapping up results for Wall Street’s biggest six lenders. Morgan Stanley’s fourth quarter revenue topped analysts’ estimates but the bank warned of economic and geopolitical risks. Goldman Sachs exceeded expectations, boosted by higher asset and wealth management revenue.

[PRO] The hunt for quality stocks Markets have cooled off from the massive gains in the latter part of 2023. Amid this loss of momentum, the pros say investors must look toward quality names. Quality stocks are defined as those that have robust earnings, low debt and a stock price that’s less likely to be impacted by a broad market selloff.

Federal Reserve Governor Christopher Waller said there’s “no reason” for the central bank to “move as quickly” in its approach to lower interest rates this year. His comments were in sharp contrast to the aggressive policy loosening that markets are expecting this year.

Traders still see a more than 64% chance of the Fed cutting interest rates by 25 basis points to 5%-5.25% range at its meeting in March, according to the CME Group’s FedWatch tool. Those bets came down substantially from a near 77% chance of rate cuts on Friday, when data showed producer prices unexpected dropped in December.

Looking across the Atlantic, the World Economic Forum in Davos saw plenty more discussions on the second day.

Artificial intelligence remained a hot topic, with Microsoft CEO Satya Nadella advocating for its uses, noting that more countries are now talking about AI in similar ways.

“I think [a global regulatory approach to AI is] very desirable, because I think we’re now at this point where these are global challenges that require global norms and global standards,” Nadella said.

(L-R) Brian Moynihan, Chairman and CEO of Bank of America; Jamie Dimon, Chairman and CEO of JPMorgan Chase; and Jane Fraser, CEO of Citigroup; testify during a Senate Banking Committee hearing at the Hart Senate Office Building on December 06, 2023 in Washington, DC.

Win Mcnamee | Getty Images

This report is from today’s CNBC Daily Open, our international markets newsletter. CNBC Daily Open brings investors up to speed on everything they need to know, no matter where they are. Like what you see? You can subscribe here.

Positive inflation signal? An unexpected decline in wholesale prices indicated inflation could be declining for good. The Labor Department’s producer price index fell 0.1% in December, as opposed to a 0.1% rise seen by economists surveyed by Dow Jones. PPI data measures inflation from the producer or manufacturer’s perspective.

Markets rose for the week The blue-chip Dow Jones Industrial Average shed over 100 points on Friday but rose 0.3% for the week. The S&P 500 and the Nasdaq closed the day nearly flat, while also ending higher for the week. Markets digested the start of the earnings season and an unexpected decline in producer prices. In Asia, China stocks erased losses from earlier in the session after the country’s central bank left its medium-term policy loans rate unchanged, while Taiwan stocks gained after election.

China skeptic wins Taiwan elections Taiwan’s Lai Ching-te won the island’s presidential election on Saturday. This was the Democratic Progressive Party’s third straight win. Lai, who is seen as a strong China skeptic, won by more than 40% of the popular vote. He said he was “determined to safeguard Taiwan from threats and intimidation from China.” Beijing dismissed his victory.

[PRO] Goldman Sachs picks unloved stocks Goldman Sachs said Europe’s utilities sector may not have had much action in the last three years, but there could be a potential shift waiting to happen. The investment bank names which European stocks, that have lagged the broader market by nearly 20%, are worthy plays in the industry in 2024.

Fourth-quarter earnings have officially begun with four of Wall Street’s top six banks reporting rather bleak results.

JPMorgan Chase, the biggest U.S. bank by assets, paid a sizeable fee linked to the government seizures associated with regional banking crisis last March, which impacted its earnings.

CEO Jamie Dimon said: “the U.S. economy continues to be resilient, with consumers still spending, and markets currently expect a soft landing.”

But he added that deficit spending and supply chain adjustments “may lead inflation to be stickier and rates to be higher than markets expect.”

Citigroup was also hit by last year’s regional banking crisis but focus was mostly on CEO Jane Fraser’s massive overhaul plan aimed at lifting sentiment around the bank’s financial health and also its stock price.

The third largest U.S. bank by assets said it will slash about 20,000 jobs over the “medium term,” but did not make it immediately clear on the exact duration. Citigroup has lagged its Wall Street peers since the 2008 financial crisis and remains the lowest valued among the top six banks.

Outlook from Wall Street’s biggest lenders was cautious against the backdrop of markets pricing in interest rate cuts by the Federal Reserve as early as March. Lower rates hurt the net interest income generated by banks.

Separately, data showing a decline in wholesale prices came as a positive surprise. It came a day after prices consumers pay for goods and services rose 0.3% in December and were up 3.4% on the year. Still remaining much above the Fed’s 2% target for the year.

“What inflation risks remain in the U.S. economy clearly cannot be sourced to any upward pressure in producers’ costs,” said Kurt Rankin, senior economist at PNC.

“Whether surveying from producers’ intermediate or final demand perspective, there is little to no pricing pressure headed into the U.S. economy from the supply side entering 2024.”

During Asia hours, Taiwan’s election results stole the show. Voters in the island chose the ruling Democratic Progressive Party, or DPP for a third straight presidential term, handing victory to China-skeptic Lai Ching-te.

Lai, who won by more than 40% of the popular vote, said he was “determined to safeguard Taiwan from threats and intimidation from China.”

Traders work on the floor of the New York Stock Exchange (NYSE) in New York, U.S., on Monday, June 27, 2022.

Michael Nagle | Bloomberg | Getty Images

This report is from today’s CNBC Daily Open, our new, international markets newsletter. CNBC Daily Open brings investors up to speed on everything they need to know, no matter where they are. Like what you see? You can subscribe here.

Positive inflation signal? An unexpected decline in wholesale prices indicated inflation could be declining for good. The Labor Department’s producer price index fell 0.1% in December, as opposed to a 0.1% rise seen by economists surveyed by Dow Jones. PPI data measures inflation from the producer or manufacturer’s perspective.

Markets rose for the week The blue-chip Dow Jones Industrial Average shed over 100 points on Friday but closed 0.3% higher for the week. The S&P 500 and the Nasdaq closed the day nearly flat, while also ending higher for the week. Markets digested the start of the earnings season and an unexpected decline in producer prices. European stocks ended higher, but shares of British luxury firm Burberry fell 7% after a profit warning.

China skeptic wins Taiwan elections Taiwan’s Lai Ching-te won the island’s presidential election on Saturday. This was the Democratic Progressive Party’s third straight win. Lai, who is seen as a strong China skeptic, won by more than 40% of the popular vote. He said he was “determined to safeguard Taiwan from threats and intimidation from China.” Beijing dismissed his victory.

[PRO] Buffett’s view on airlines Wall Street legend Warren Buffett will most likely never add airline stocks to his portfolio again. The “Oracle of Omaha” has been swift in unloading $4 billion worth of airline stocks in the pandemic and recently with disappointing profit forecast, more aircraft groundings and midair emergencies, he will not give such stocks a chance again.

Fourth-quarter earnings have officially begun with four of Wall Street’s top six banks reporting rather bleak results.

JPMorgan Chase, the biggest U.S. bank by assets, paid a sizeable fee linked to the government seizures associated with regional banking crisis last March, which impacted its earnings.

CEO Jamie Dimon said: “the U.S. economy continues to be resilient, with consumers still spending, and markets currently expect a soft landing.”

But he added that deficit spending and supply chain adjustments “may lead inflation to be stickier and rates to be higher than markets expect.”

Citigroup was also hit by last year’s regional banking crisis but focus was mostly on CEO Jane Fraser’s massive overhaul plan aimed at lifting sentiment around the bank’s financial health and also its stock price.

The third largest U.S. bank by assets said it will slash about 20,000 jobs over the “medium term,” but did not make it immediately clear on the exact duration. Citigroup has lagged its Wall Street peers since the 2008 financial crisis and remains the lowest valued among the top six banks.

Outlook from Wall Street’s biggest lenders was cautious against the backdrop of markets pricing in interest rate cuts by the Federal Reserve as early as March. Lower rates hurt the net interest income generated by banks.

Separately, data showing a decline in wholesale prices came as a positive surprise. It came a day after prices consumers pay for goods and services rose 0.3% in December and were up 3.4% on the year. Still remaining much above the Fed’s 2% target for the year.

“What inflation risks remain in the U.S. economy clearly cannot be sourced to any upward pressure in producers’ costs,” said Kurt Rankin, senior economist at PNC.

“Whether surveying from producers’ intermediate or final demand perspective, there is little to no pricing pressure headed into the U.S. economy from the supply side entering 2024.”

CNBC’s Leslie Picker and Gerard Cassidy, RBC Capital Markets Head of U.S. Bank Equity Strategy, join ‘Closing Bell Overtime’ to talk the recent slate of bank earnings and what they tell us about the sector.

Citigroup CEO Jane Fraser at the World Economic Forum in Davos, Switzerland, on Jan. 17, 2023.

Adam Galica | CNBC

Citigroup said it was cutting 10% of its workforce in a bid to help boost the embattled bank’s results and stock price.

About 20,000 employees will be let go over the “medium term,” New York-based Citigroup said Friday in a slideshow tied to fourth-quarter earnings. While it wasn’t immediately clear how long that is, the bank has previously used that term to denote a three- to five-year period.

Citigroup had roughly 200,000 workers at the end of 2023, excluding Mexican operations that are in the process of being spun out, according to the presentation.

Citigroup CEO Jane Fraser announced a sweeping overhaul of the third-largest U.S. bank by assets in September. The company has been left behind by peers since the 2008 financial crisis as Fraser’s predecessors couldn’t get a handle on expenses and is the lowest valued among the six biggest U.S. banks.

In November, CNBC reported that managers and consultants involved in the effort — known internally by the code name “Project Bora Bora” — discussed job cuts of 10% in several major businesses.

The company has since executed several waves of layoffs, beginning with the top layers of the bank, with another round of cuts set for Jan. 22, according to a person familiar with the matter. A Citigroup spokeswoman declined to comment.

American banks have been trimming jobs all throughout the past year, led by Wells Fargo and Goldman Sachs, to lower costs amid stagnant revenue. Citigroup had been a notable outlier, maintaining staffing levels at around 240,000 for all of 2023, including its Mexico operations.

Citigroup said Friday it booked a $780 million charge in the fourth quarter tied to Fraser’s restructuring project, and that it may post another $1 billion in severance and other expenses in 2024. The moves could help trim up to $2.5 billion in costs over time, the bank said.

In a footnote to its presentation, Citigroup said the 20,000 job cuts could be “slightly lower” if it chooses to use internal resources rather than outsource functions.

Given the outlook for thousands of more job cuts over the next few years, some Citigroup employees are using vacation time or mental health leave to search for their next position, said the person familiar with the matter, who declined to be identified speaking about personnel matters.

“People are looking aggressively,” the person said. “I know senior VPs who are on vacation now, but they’re never coming back.”

Citigroup on Friday posted a $1.8 billion fourth-quarter loss after booking several large charges tied to overseas risks, last year’s regional banking crisis and CEO Jane Fraser’s corporate overhaul.

All told, the charges — so massive the bank preannounced their effect this week — hit quarterly earnings by $4.66 billion, or $2 per share, Citigroup said. Excluding their effect, earnings would’ve been 84 cents a share, the bank said.

Here’s what the company reported versus what Wall Street analysts surveyed by LSEG, formerly known as Refinitiv, expected:

Earnings: 84 cents a share, adjusted, may not compare with 81 cents, expected.

Revenue: $17.44 billion vs. $18.74 billion expected.

Fraser called her company’s performance “very disappointing” because of the charges but said Citigroup had made “substantial progress” simplifying the bank last year.

The CEO announced plans for a sweeping corporate reorganization in September after previous efforts failed to boost the bank’s results and share price. On Friday, Citi said it expects to cut its headcount by 20,000 and post up to $1 billion in severance costs over the medium term.

Citigroup previously said it would exit municipal bond and distressed debt trading operations as part of the streamlining exercise. Earlier this week, the company said it booked bigger charges in the quarter than previously disclosed by Chief Financial Officer Mark Mason.

Citigroup revenue slipped 3% to $17.44 billion in the quarter, though the bank said revenue rose 2% after excluding the effect of divestitures and charges tied to exposure to Argentina. Despite the noise, Citi’s institutional services operations, U.S. personal banking and investment banking performed well, according to the bank.

“Citigroup’s earnings looked awful with a big loss of $1.8 billion, but the bank’s underlying business showed resilience,” Octavio Marenzi, CEO of consulting firm Opimas LLC, said in an email. Fraser will be under mounting pressure to deliver results this year, he added.

Shares of Citigroup rose 2% during premarket trading.