Financial institutions are implementing technology throughout the customer experience, including account opening, servicing and even transactions, but banks also need to know if clients are having problems navigating digital offerings.

That’s where engagement results, client monitoring and customer surveys come in, Debbie Miglaw, head of digital business development at Broadridge Financial Services, tells Bank Automation News on this episode of “The Buzz” podcast.

Banks can access client feedback by using technology to listen, she said, and they can use data to determine how clients are interacting with digital options.

Are clients dropping off at any point of digital account opening? Or is there friction in digital check depositing? Banks are already collecting metrics on their technology use, and they can use that data to measure whether the technology they have releases is successful, Miglaw said.

Listen as Broadridge’s Miglaw discusses how banks can improve the customer experience by leaning on data and insights.

Financial institutions are implementing AI throughout their organizations at a steady pace. However, even with investments made and use cases identified, AI can only accomplish so much without users on board.

“If the businesses [within a bank] don’t care to use it, it’s just not going to change anything,” Inwha Huh, managing director at $1.4 trillion Deutsche Bank, said last month at Sibos.

At Sibos 2023, from left, are: Shelby Austin, Grace Lee, Mike Hughes and Inwha Huh. Photo by Whitney McDonald.

Mike Hughes, global head of custody product development at Citigroup, said: “If you don’t get user adoption [of AI], it’s just a huge waste of time, effort and energy.

Similarly, Scotiabank Chief Data and Analytics Officer Grace Lee cautioned that if AI isn’t integrated into a bank’s infrastructure and culture, “Then we’re going to continue to under-invest. … And that’s a recipe for us to spend another couple of decades without AI fundamentally changing the way we live and work.”

To make the transition to an AI-driven institution, Deutsche Bank has identified three ways to drive the technology in its operations:

1. Pushing adoption: Bank employees who understand how AI will change their day-to-day work lives will want to use the technology.

“The No. 1 thing that comes to mind for me is people,” Huh said. Employees much think differently about AI in order to understand and use it, therefore any adoption effort must go beyond senior management and into middle management and users to be successful.

2. Adjusting the operating model: Banks must undergo fundamental changes to their operating model to benefit from AI, she said. For example, AI must be part of the business structure and client experience from within, rather than an added capability.

“It’s not enough to stick in cool new technology,” Huh said.

3. Reengineering processes: Banks often run proofs of concept that don’t lead to change, however this cannot be the case with AI.

“The process [of] reengineering up front as you embed new and great AI tooling is also critical,” Huh said. “And unless [we] reengineer the way we do stuff. … nothing’s really going to change.”

Silicon Valley Bank’s integration with First Citizens Bank is going “better than expected.” Acquiring Silicon Valley Bank (SVB) in March was an opportunity for First Citizens Bank (FCB) to go beyond traditional banking, Christopher Hollins, head of solution sales and delivery at SVB, a division of First Citizens Bank, told Bank Automation News at […]

Silicon Valley Bank, a division of First Citizens Bank, named Martin Murrell the new head of global payments and Milton Santiago the new head of global digital solutions last month. The pair will bring “the vision and execution needed to enhance SVB’s product suite, bringing inventive and bespoke solutions to our innovation economy clients,” Gagan […]

On the heels of a tumultuous spring that saw three of the four largest bank failures in U.S. history — Silicon Valley Bank and Signature Bank went under in March, followed by First Republic in May — many customers of smaller institutions quickly moved their deposits to “too big to fail” banks — and those financial institutions grew by acquisition, too.

As the banking crisis drags on, pressure is building on financial institutions to find new ways to compete for deposits in the changing market — and customer loyalty is more important than ever.

Despite the rise of digital banking, the brick-and-mortar branch is still a critical component in building customer loyalty. In fact, many conventional banks are putting increased emphasis on their physical branches as the prime differentiator for their services. A survey by Blend found that the vast majority of respondents are multi-channel customers, and the top reason surveyed customers gave for switching banks was actually the inconvenient location of their local branch.

Blurring the digital/physical line

However, the nature of these physical branches is changing. With digital transactions continuing to rise, customers have less of an everyday need to visit their bank and typically only do so to engage in more complex activities like taking out a loan or receiving financial consultations. These interactions are key; the banks that are poised for the greatest success in the coming years will be those that can provide a personalized service that blurs the line between the digital and physical.

Retail banking customer service has the difficult task of serving customers across the gamut of banking needs and across multiple channels. Banks typically employ different software tools for managing accounts, handling loan applications and getting insights into customer income, debt and credit. Furthermore, the platforms used for online services are often different from the ones used by in-branch staff.

When customers are multi-channeled but systems are siloed, service delivery is inevitably hindered. Not only does it take more time and effort to provide offers and recommendations to customers, but it also takes longer for employees to gain proficiency across the platforms. This can translate to less timely and personalized results for customers.

The omnichannel platform

By combining these discrete internal software tools into a unified, omnichannel platform, banks stand to gain a leg up on competitors through increased customer engagement. Removing complexity from the origination process helps focus bankers on the customer’s goals, rather than on navigating the system and data input. Automated workflows and verification services reduce the time to complete rigorous tasks including credit card applications and approving personal loans, and allow for more timely service and advice to be offered in person at branches.

As a bonus, streamlining with a single, intuitive software tool that can administer tasks typically siloed across multiple programs can also help soften the learning curve for onboarding new employees.

Ultimately, in this competitive era, institutions that master the art of seamless, intuitive and personalized banking experiences will be the ones to thrive through the downturn and beyond.

Nima Ghamsari is co-founder and chief executive of Blend, and chair of its board of directors. He leads the company’s corporate and product strategy, and in 2020 was included in Fortune’s 40 Under 40 list.

Cloud migration projects have become increasingly important for the banking industry, offering benefits that can revolutionize how financial institutions operate. In an era in which digital transformation is reshaping the landscape, it is vital for banks to adapt to stay competitive and meet evolving customer expectations. Cloud migration provides a powerful avenue for achieving these goals, enabling banks to leverage advanced technologies, enhance operational efficiency and deliver superior customer experiences.

The banking sector has traditionally been cautious when adopting new technologies, and cloud migration is no exception. The difference is that cloud migration’s benefits far outweigh its challenges. By understanding these challenges and the crucial role cloud migration plays in the survival of legacy institutions, banking professionals can gain insights into the significance of the cloud and the steps required to navigate this journey successfully.

Rambabu Nalagandla, Lead Solutions Architect at Pilvi Systems Inc.

Challenges in migration for banks

Cloud migration for banks presents myriad challenges that demand meticulous attention and strategic planning. One significant hurdle is the initial reluctance to move to the cloud, which stems from data security and compliance concerns. Banks handle vast amounts of sensitive customer data and ensuring its protection during migration is paramount to maintaining trust and confidence.

Migrating complex legacy systems poses another obstacle. These systems often have intricate interdependencies, making their integration with cloud infrastructure a delicate process. Meticulous restructuring and data mapping are required to ensure a seamless transition without disrupting critical functionalities.

Adhering to regulatory requirements is a vital aspect of cloud migration for banks. Financial institutions are subject to stringent regulations imposed by the Financial Industry Regulatory Authority, the Securities and Exchange Commissionand other regulators. Banks must ensure compliance to avoid potential legal and financial consequences.

Effective data governance and management are fundamental in addressing these requirements. It is essential for banks to implement robust data governance policies to appropriately classify and protect sensitive data. Data encryption, access controls and continuous monitoring are essential to maintain data integrity and confidentiality during and after migration.

Fostering a culture that embraces cloud technologies is also vital. This involves educating employees about the benefits of cloud adoption, providing training to upskill the workforce, and cultivating a cooperative environment to ensure a smooth transition.

Banks can overcome these challenges by collaborating with experienced cloud service providers and employing best practices. A comprehensive risk assessment, thorough security frameworks, and continuous monitoring are vital to effectively address data security and compliance concerns. With a clear focus on regulatory adherence and a forward-looking approach, banks can unlock the benefits of enhanced agility, cost–efficiency, and improved customer experiences through successful cloud migration.

Accelerating migration journey

Establishing a well-defined strategy is crucial to a successful cloud migration journey. Banks should thoroughly assess their infrastructure, applications and data to identify suitable candidates for migration. Categorizing workloads based on complexity, security requirements and business impact helps prioritize migration efforts effectively. A phased migration approach, starting with noncritical workloads, allows banks to gain valuable experience and build confidence before moving to mission-critical applications.

Collaboration with experienced cloud service providers is another essential aspect of accelerating the migration journey. Industry-leading cloud providers like Amazon Web Services (AWS), Google Cloud Platform (GCP) and Microsoft Azure offer tailored solutions for banks. These can simplify the migration process while ensuring adherence to industry standards and regulations.

For instance, AWS provides the AWS for Financial Services competency, which highlights AWS partners with demonstrated expertise in serving the financial industry. This competency offers various solutions, including core systems modernization, data management and security. One service for banks, Amazon Aurora, offers a fully managed and relational database service. Banks can utilize Amazon Aurora to migrate their on-premises databases to the cloud with minimal downtime, benefiting from improved performance, reliability and cost optimization.

GCP also offers the Financial Services industry, providing tailored solutions for financial institutions. GCP’s BigQuery service offers a powerful database that enables banks to analyze vast amounts of data and derive valuable insights for informed decision making.

Azure offers the Azure Financial Services Accelerator, a platform designed to streamline the development of financial solutions. Azure Key Vault facilitates secure key management and encryption, ensuring robust security for sensitive data during migration and beyond.

Estimating migration costs

Accurately estimating cloud migration costs is key to ensuring a cost-effective process. Banks can utilize cloud cost estimator tools provided by AWS, Azure, and GCP to gain insights into potential expenses based on their existing infrastructure and projected workloads. These tools help banks make informed decisions and plan their migration budgets effectively. Banks must consider data storage requirements, application dependencies, network bandwidth, and data transfer fees when estimating costs. AWS, Azure, and GCP offer pricing options, including pay-as-you-go, reserved instances and volume-based discounts.

Reserved instances allow banks to commit to specific virtual machine types for one- or three-year terms, offering substantial discounts compared to pay-as-you-go rates. Azure offers Reserved VM Instances, while AWS provides Amazon EC2 Reserved Instances. GCP offers sustained use discounts, automatically reducing prices for long-running workloads.

Implementing cost optimization strategies like rightsizing instances, auto scaling and serverless computing helps banks reduce expenses while maintaining optimal performance.

Continuous monitoring and optimization post-migration allow banks to identify cost-saving opportunities and adjust cloud resources. By leveraging cost estimator tools, understanding pricing models, and optimizing expenses through reserved instances and volume-based discounts, banks can navigate cloud migration with financial clarity, enhance cost efficiency and achieve long-term success.

The survival of legacy institutions depends on cloud migration. Emphasizing the advantages of enhanced agility, scalability and improved customer experiences, cloud adoption empowers these institutions to maintain competitiveness, adapt to evolving demands and deliver seamless services in the rapidly changing digital landscape. Embracing cloud technologies enables legacy institutions to unlock new possibilities, optimize operations, and ensure long-term success in an increasingly technology-driven world. It is essential for banks to take the leap and embark on their cloud migration journeys for sustained growth and prosperity.

About the Author:

Rambabu Nalagandla is a lead solutions architect at Pilvi Systems Inc., with more than 19 years of experience in the banking and financial services industry. He has successfully guided leading banks through digital transformation, leveraging emerging technologies to drive operational efficiency and enhance customer experiences.

In the rapidly evolving world of banking and financial services, Agile and DevOps methodologies have emerged as essential tools to drive innovation and stay ahead of the competition. These revolutionary approaches to software development and project management have gained significant traction within the industry due to their ability to foster collaboration, accelerate time to market and deliver customer-centric solutions.

The traditional waterfall model of software development is becoming increasingly outdated and unsuitable for several reasons. It follows a linear, sequential approach to development, where each phase must be completed before moving on to the next. This rigid and inflexible structure is ill-suited for the rapidly evolving and dynamic nature of the financial sector. Banks and financial institutions, regardless of size, are investing heavily in Agile and DevOps practices. For example, JP Morgan Chase drives innovation in software development and delivery through these practices.

Unique challenges to address, overcome

The banking industry faces unique challenges when it comes to adopting new methodologies like Agile and DevOps. Financial institutions handle vast amounts of sensitive data and are subject to strict regulations, making it imperative to ensure that the implementation of Agile and DevOps does not compromise data security and privacy.

In the United States, there are different regulations that govern the financial industry, including payment services. One of the key regulations in the U.S. related to payment services is the Electronic Fund Transfer Act (EFTA) and its implementing Regulation E. These regulations provide consumer protection and govern electronic funds transfers, including rules for automated clearinghouse transactions and electronic debit card transactions.

Another challenge is the need for flexibility and adaptability in a constantly evolving financial landscape. Market conditions, customer preferences and advancements in technology can change rapidly, and banks must be agile enough to respond quickly and effectively. The iterative nature of Agile and DevOps practices empowers banks to adapt their products and services in real time, meeting the dynamic and ever-changing demands of the market.

Benefits of Agile, DevOps in banking

Implementing Agile and DevOps in the banking sector yields numerous benefits. Operational efficiency is improved significantly through continuous integration and automation, enabling faster and more frequent software releases. This leads to a reduced time to market for new products and services, helping banks gain a competitive edge.

Industry compliance standards such as EFTA and Regulation E may undergo updates or changes over time. DevOps enables financial institutions to respond rapidly to these regulatory modifications. By using continuous integration and continuous delivery pipelines, banks can quickly deploy changes, ensuring that their electronic fund transfer processes remain compliant.

Customer satisfaction is another area that benefits from Agile and DevOps. These methodologies allow banks to deliver products that align closely with customer needs, preferences and feedback. This customer-centric approach results in enhanced customer experiences and fosters customer retention.

Additionally, the focus on iterative development and continuous improvement promotes innovation. By encouraging experimentation and risk-taking, Agile and DevOps practices enable banks to explore new ideas and technologies, paving the way for groundbreaking innovations in the financial sector.

Overcoming implementation challenges

Implementing Agile and DevOps practices in the banking sector faces a significant hurdle in the cultural shift required to embrace these methodologies fully. Banks may have traditionally operated in a hierarchical and risk-averse manner, which can hinder the adoption of Agile and DevOps principles. It is important for leadership to drive the cultural change by promoting collaboration, experimentation and a learning-oriented environment.

Stakeholder alignment is crucial for successful implementation. All teams and departments must be on board with the Agile and DevOps transformation, from top-level management to frontline employees. Effective communication and buy-in from all stakeholders are vital for the seamless integration of these methodologies.

Another pain point for banking and financial institutions is the complexity of legacy systems. Many financial institutions have extensive and intricate legacy IT infrastructures that were not designed to work with Agile and DevOps methodologies. Integrating these methodologies with existing systems and processes can be challenging and may require significant time and effort.

Digital strategy alignment

Agile and DevOps methodologies are inherently aligned with broader digital transformation strategies in the banking industry. Digital transformation aims to leverage technology to enhance operational efficiency, improve customer experiences and drive innovation. By adopting Agile and DevOps, banks can efficiently incorporate emerging technologies like cloud computing and artificial intelligence into their operations and customer-facing solutions.

The synergy between Agile and DevOps and these emerging technologies allows banks to experiment with new digital solutions rapidly and deliver value to customers faster. The continuous feedback and improvement loops fostered by Agile and DevOps are well-suited to optimizing digital transformation initiatives.

In the context of generative AI in banking, DevOps can streamline deployment and maintenance of AI models. DevOps practices enable continuous integration and delivery of AI solutions, allowing banks to quickly respond to changing market needs and iterate on AI models for improved accuracy and efficiency. This seamless integration of generative AI into the development and operations pipeline enhances agility and accelerates the realization of value from AI-driven digital transformation strategies.

The combination of Agile and DevOps methodologies provides a powerful framework for banking and financial institutions to navigate the challenges of the digital age successfully. By addressing industry-specific concerns, leveraging their benefits, overcoming implementation challenges and aligning with broader digital transformation strategies, banks can position themselves at the forefront of innovation and deliver exceptional customer experiences in an increasingly competitive landscape.

Rambabu Nalagandla is a lead solutions architect at Pilvi Systems Inc., with more than 19 years of experience in the banking and financial services industry. He has successfully guided leading banks through digital transformation, leveraging emerging technologies to drive operational efficiency and enhance customer experiences.

Barclays UK has announced the appointment of Lee Counselman as a managing director for technology investment banking. Counselman will focus on strategic M&A and equity work within the software banking team and report to Kristin Roth DeClark, head of technology investment banking, according to an Aug. 14 news release. London-based Barclays has been investing heavily […]

Financial institutions are looking to upgrade their tech stacks to attract customers and drive deposit growth. The approach of strengthening deposits and adding to the client pool follows the spring collapses of Silicon Valley Bank, First Republic Bank, and Signature Bank. “Banks that had good and aggressive digital account opening experiences were able to gobble […]

Credit unions are looking to digital lending marketplace Union Credit to grow their membership, gain national exposure and break into younger demographics. Nationally, the average credit union member is 54 years old while the average consumer in the United States is 37, Barry Kirby, chief revenue officer and co-founder of Santa Rosa, Calif.-based Union Credit, […]

The finance industry has seen a wave of bank mergers this year amid uncertain macroeconomic conditions and a high interest rate environment. First Citizens Bank acquired a part of Silicon Valley Bank, JPMorgan absorbed First Republic Bank, and last month PacWest Bank and Banc of California announced a merger. And more mergers are expected […]

Community banks are turning to technology provider Computer Services Inc. for core processing and FedNow capabilities. In the sales process, the Paducah, Ky.-based CSI is being asked about FedNow rails and onboarding by potential clients as a new selling point for the core processer, Allison Maddock, chief product officer at CSI, told Bank Automation News. […]

There is a general complaint encountered by developers from among open banking participants, even after partner APIs are made available: Adoption isn’t straightforward.

Tvisha Dholakia, co-founder, apibanking.com

We’ve experienced this across hundreds of integration points. Even with the developer assistance toolbox, which includes documentation, software developer kits and sandboxes, and developer self-service consoles, partner integration timelines are intractable. Developer and support teams are overloaded for each integration.

For financial products with complex customer journeys and for BaaS partnerships requiring complex on-boarding, compliance and API integrations, the degree of handholding required is even greater.

More support, higher integration cost

This also impacts open banking accessibility, putting it out of reach for the broader ecosystem. If there is a high cost to a partnership, the benefit becomes a key criterion. As financial institutions become picky about who partners with them, this de-levels the playing field creating a disadvantage for smaller players.

So, what is the right level of integration assistance? How can open banking be made accessible to all?

This is a discussion on how to create integration options for your API consumers. I’ll discuss what the options are and why and when they are meaningful.

A typical partner integration follows these 4 steps:

Chart by openbanking.com

1. Channel front-end: This is the application on which the services powered by the APIs will be made available to the end user. This is where the partner designs its customer journey. However, while the partner has complete control over the branding, look and user experience (UX), this is also where the customer authenticates themself, inputs their personal information, and provides consent to the app to share this via APIs. For designing such a user interface (UI), a partner without adequate experience may require oversight to ensure that the overall customer journey meets the regulatory requirements.

2. Data security compliance: In addition to consent, there are compliance requirements that govern how and what customer data should be captured, transmitted, shared and stored. In an open banking partnership, this compliance may also be the responsibility of all ecosystem partners involved in the integration, and the integrating partner needs to ensure that its application and connectors meet the requirements.

3. API service orchestration: In a typical multi-API journey, the APIs need to be stitched together to create the journey. This may entail a session management and authority; message encryption and decryption; third party handoffs; and logic-built into a middleware layer, which may likely be development-intensive, depending on the complexity of the journey.

4. API integration: For each API required for the journey, the partner application must consume the API; this means it must be on-boarded and complete the configuration requirements, complete the development to call the required methods and consume the responses.

Not all partners in the integration may have the capability for all four steps. For example, there may be incumbents from a nonfinancial industry who want to partner with a bank for co-branded lending or a card offering for its customers, but don’t meet the PCI-DSS compliance requirements.

This means there will need to be significant investment from the partner to become compliant or that a sub-par customer experience design will result. Also, there may be smaller fintechs without the developer capacity for the orchestration effort required. Hence, they may need to stretch beyond their reach to make the partnership happen.

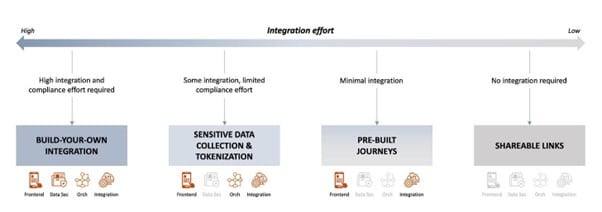

Integration effort is variable

How can we best reduce the integration effort?

The nuance this question misses is that different types of partners have very different needs. There are players who want complete control over their customers’ experience, and want to “look under the hood” and tinker with the parts, nuts and bolts. There are players who want control, but do not want to take on the burden of compliance. And there are players who only want the BaaS partnership to complete their digital offerings, but don’t want to invest in any additional development.

Democratizing API integration: 4

Chart by openbanking.com

The starting point is, of course, understanding partner archetypes and partner requirements from the integration. The platform solution design follows these four needs.

1. Build-your-own integrations: Making raw materials and tools available

This integration option is analogous to starting from basic raw materials, or ingredients, and is for those that know exactly what they want and how to achieve it. The key platform offerings are the APIs and a complete developer experience toolbox. If you’re curious about what that means from an API banking context, we have apiece about that.

The kind of integrating partners who are likely to use the build-your-own option are those with offerings closely adjacent to banking, and that have done this before.

2. Integration with managed data compliance: All raw materials and tools, with compliance crutches

With this option, also, the integration partner has all the raw materials to completely control the experience, but without the overhead of compliance, especially related to sensitive data.

With the help of cross-domain UI components, tokenization, collection and storage of data can be handled entirely at the bank end, while the partner only has to embed these components into its front-end.

This option is especially helpful for those integrating partners that want to control the experience, but to whom financial services is not a core offering, and so compliance is an unnecessary overhead which they are happy to avoid.

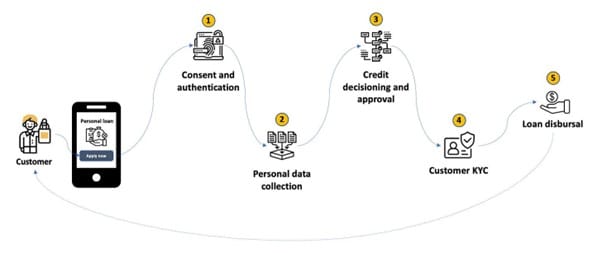

3. Pre-built journeys

Offering pre-built journeys allows a partner to focus only on the front-end experience, while the entire API orchestration and compliance is handled in a middleware layer and abstracted away for the integrating partners.

For a typical banking service, designing an API-first journey means working with a number of separate endpoints and stitching the services together. For instance, a simple loan origination journey for a customer may look like this: (simplified for illustration)

Chart by openbanking.com

This journey requires five services from the bank: customer authentication and consent, customer personal data collection, credit decisioning and approval, KYC and loan disbursal.

Stitching these services together to create a single end-to-end digital experience for a customer may call for a thick middleware with a database and caching, data tokenization and encryption, session management, handoffs across services and other related orchestration.

To enable partners to deliver this journey without the need for orchestration, this layer can be moved to a platform on the bank side and offered as an integration solution to the partners. The partner now only needs to integrate with the platform, and build its UI and UX.

Such a solution, of course, helps drastically cut down development time for the integration and is especially compelling for smaller players and channel sales partners that want to offer banking products or services to their customers.

4. Pre-built UI or shareable links

No integration required, but with directly embeddable, customizable UIs, partners can offer the relevant banking functionality or services with minimal effort. This is equivalent to a contextual redirect and is extremely useful for cases where the partner wants to avail itself of only minimal open banking services and does not want to go through the entire on-boarding, configuration and integration processes required for all other integration options.

Bringing it all together

While it is certainly possible to continue to grow partnerships by offering customizations and assistance to each integration, for achieving a rapid scale-up in open banking ecosystem partnerships, there is a need for a platform that standardizes these concerns and cuts across developer experience and integration needs.

Tvisha Dholakia is the co-founder of London-basedapibanking.com, which looks tobuild the tech infrastructure to remove friction at the point of integration in open banking.

In one week in April, Metro Credit Union received more than 450 fraudulent account opening applications.

Using manual processes, fraud and digital teams at the Boston-based, $3 billion credit union worked overtime to fend off a series of attacks that Chief Operating Officer Traci Michel believed was enabled by generative AI tools.

Photo by CanStock

“We’re getting it from all sides,” Michel told Bank Automation News. “When you see that type of volume coming into a platform, you have to imagine that there’s some type of computer-generated frequency that’s happening behind the scenes.”

Through informal conversations with colleagues at other financial institutions, Michel discovered that her peers were falling victim to the same attacks.Seventy percent of financial institutions reported losses of over $500,000 to fraud in 2022, according toAlloy’s State of Fraud Benchmark Report.

“The pattern was extremely similar,” she said. “[But] we didn’t have a tool that would help us try to interface and understand whether we were the only financial institution.”

Solutions for smaller FIs

Facing scaling fraud operations, Metro Credit Union turned to anti-fraud platform FiVerity, one of several companies using data collected from a group of member institutions to build records of blacklisted accounts and concerning patterns.

FiVerity opened its Digital Fraud Network in June to more than 100 small and medium-sized businesses for free, according to a release. Other clients include Grasshopper Bank, BHG Financial, and Digital Federal Credit Union.

“Some of the other vendors are going after the larger institutions,” FiVerity Chief Executive Greg Woolf told BAN. “Our focus has really been on the community banks and credit unions, and some of the smaller fintechs… who typically don’t get access to this level of technology.”

FiVerity also launched its Anti-Fraud Collaboration Platform in June, building on its existing network to offer new features to members, according to a release.

The Boston-based company, which raised $4 million in seed funding in April, uses machine learning and data from its members to draw insights and identify fraudulent users in real time, according to its website. Features of its Anti-Fraud Collaboration Platform include an explanation of its risk scoring system that enables customers to see why specific accounts were flagged, Woolf said.

It’s “providing a fraud score, but also providing transparency,” he said. It could be that “the Social [Security number] was used by somebody else, or another institution reported this address was linked to a crime rate… or other elements that could come off the dark web.”

FiVerity has worked with federal regulators, including the Federal Reserve and the Financial Crimes Enforcement Network, that have supported collaboration and promoted equity by encouraging service offerings to smaller FIs, Woolf said.

But bringing together FIs of a similar size and in the same region is also practical, as these institutions often face similar fraud threats, according to Woolf, who referenced an incident in which fraudsters in Maine targeted every financial institution with a branch on the main street of a single town.

“There’s a natural clustering, and that actually helps our models be more effective,” Woolf said, noting a 45% improvement over previous models by focusing on a specific demographic of FIs.

Metro Credit Union hopes that as more FIs join FiVerity’s consortium, the collaboration will help every member fight fraud.

“We’re very excited about the expansion on the client side, because it’s strength in numbers for us,” Metro’s Michel said. “The more financial institutions that are participating into the network and feeding their fraudulent application information, the more we can all benefit.”

A crowded market

Meanwhile, other fintechs have recently announced their own consortiums catering to larger clients.

Anti-fraud fintech Sardine announced its coalition, SardineX, in June to bring together major players from multiple verticals in a similar data-sharing arrangement.

“The way we are going to solve fraud in financial services is to share it across financial services,” SardineX President RaviLoganathan told BAN,adding that the company believes the industry should“not have the silos for fraud data sharing only for banks, and fraud data sharing only for fintechs.”

SardineX’s founding members include card issuer Visa, Williamsburg, Va.-based Chesapeake Bank and cryptocurrency platform Blockchain.com, according to its website.

The week before the Sardine announcement, data transfer fintech Plaid announced its consortium, Plaid Beacon, which focuses on building an after-the-fact fraud database rather than providing real-time insights. Founding members include credit card payment company Tally, buy-now, pay-later provider Uplift and Veridian Credit Union.

With more players entering the market, Metro’s Michel believes competing consortiums may need to work together to offer the best results for members.

“Competition just bears out that there will be multiple providers in the market,” she said, adding that she hopes to see “common data frameworks” used by Fis in the future.

AMOCO Federal Credit Union is identifying internal processes that will benefit from workflow automation built by software company IMM.

The $1.5 billion credit union has used IMM for e-signature and electronic documentation for more than 19 years, Nathan Ashworth, senior vice president of technology at AMOCO, told Bank Automation News. “Outside of a really elementary approach to just archiving documents consistently after they’re signed, we haven’t been using the platform.”

Now the Texas City, Texas-based credit union is creating a “buffet of workflows,” he said. “It’s in our hands, identifying the use cases, building, testing the workflows and rolling them out to train staff how to use them.”

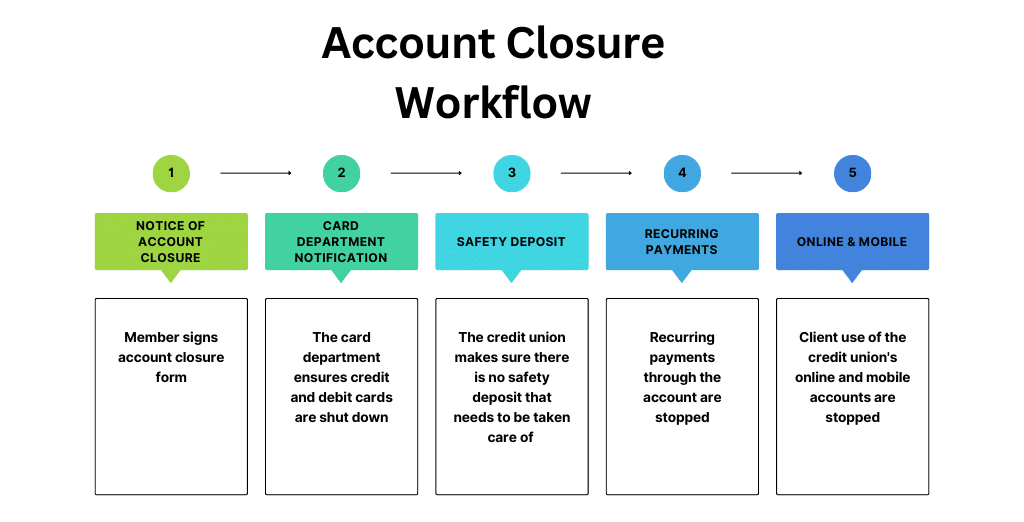

The first areas AMOCO selected for automated workflow projects include death on account processes, account closures and client information updates, Ashworth said.

For example, closing an account requires several tasks, he said. The credit union needs to make sure credit bureau reporting is updated correctly if a loan is being closed; debit cards must be closed, recurring payments must be stopped; and web and mobile pieces of the operation must be addressed.

Those tasks were traditionally the responsibility of administrative employees, but now “we’ve created an account closure workflow,” that is automated, Ashworth said.

AMOCO FCU’s automated account closure workflow

The workflow “goes department by department through that flow, making sure that no step gets missed.”

The credit union continues to vet processes in need of workflow automation, specifically those “in which we need that workflow and control and approval process built in,” he said. The credit union expects to be up and running with workflow automations in the fourth quarter.

Digitizing credit unions

AMOCO FCU joins the wave of credit unions that have invested in workflow automation.

United Bank of Michigan, for one, selected IMM for eSign capabilities within its client onboarding process, Eric Soya, vice president of branch operations at United Bank of Michigan, previously told BAN. Through IMM, the bank built a workflow process and document process for onboarding.

Similarly, Minnesota-based Sunrise Banks looked to document automation amid the payment protection program to enhance its ability to process high volumes of forgiveness applications, Chris Albrecht, senior vice president and director of Small Business Administration lending at Sunrise Banks, previously told BAN.

Accessing fintech tools

As credit unions look to IMM for workflow automation, they are now able to leverage that software’s capabilities as well as that of two more fintechs with Kinective, a fintech group that in June was formed when IMM, CFM and NXTsoft merged, Kinective Chief Executive Stephen Baker told BAN.

Now, bank clients are able to go to the single vendor for several solutions, Baker said, noting that IMM offers document automation, CFM presents branch modernization, and NXTsoft is an API connectivity provider.

Banks look for “efficiency, they want to limit errors, they want to maintain compliance and they want to offer new lines of businesses to help their revenue,” Baker said.

AMOCO has a standing relationship with both IMM and CFM, Ashworth told BAN. Bringing together IMM’s document workflow with CFM’s branch efficiency. “It’s got a lot of potential,” he said.

The question, Baker said, is: “How can we take these two technologies and build a front-to-back cohesive approach to get the most out of both technologies?”

For existing IMM, CFM and NXTsoft clients, Kinective brings a new menu of offerings, Baker said. For now, the tech providers will operate under their established names; however, Kinective is working to bring business units and support teams together under one operation.

Citizens Bank aims to retrain its workforce as it explores use cases of generative AI within contact center systems, advising and coding.

Photographer: Scott Eisen/Bloomberg

As the $222 billion bank invests in AI, it is looking to its workforce to execute its initiatives rather than looking outward, Beth Johnson, chief experience officer at Citizens Bank, told Bank Automation News.

“If we can give [our team] better tools to answer questions faster, if we can train them faster, make them more efficient,” that would add value to the bank’s operations, Johnson said.

For example, within branches, thebank aims to train its workers to provide advice in addition to working as a teller, Michael Ruttledge, chief information officer at Citizens Bank, told BAN.

“We’ve also taken some folks out of the branch, and we’re training them as engineers,” Ruttledge said. “We have got an academy program where we take people who are non-tech but have the aptitude and the skill to be able to learn that and grow that.”

The bank also looks to train employees who have a computer science or data science degree but did not go into that field, he said.

AI’s impact on the workforce

While a recent Challenger, Gray and Christmas report stated that nearly 4,000 jobs were eliminated in May 2023 due to increasing use of AI in companies, experts believe it’s too early to say how AI will affect the job market.

“Technology is going to increase the productivity of the banks and the workforce at the same time, and when we see change, there’s always incredible increase in the amount of work they have to do to actually roll out change,”Carlo Giovine, a partner at QuantumBlack, McKinsey & Co.’s artificial intelligence arm, told BAN.

The increased productivity can allow banks to double down on customer experience or enter new businesses, Giovine said.

“I think the next year will be mostly experimenting with technology, updating risk frameworks and then adding guardrails to essentially prevent misuse, prevent audit risks that we know these models are capable of,” he said. “I don’t expect dramatic changes, but then, as it’s become more mainstream, and is more proven and safer, we may see banks taking different stances.”

Northwest Bank has improved its customer acquisition and retention through personalized, automated marketing and digital offerings since implementing data-driven marketing agency Deluxe in 2021. The $14 billion bank launched Deluxe’s Life Event Trigger Program last year and posted program outperformance at 112% of the target, checking balances also outperformed at 118% of the target and […]

Bank of America this week launched its Breakthrough Lab accelerator program for startups to network and gain access to technology support their companies need to scale. The six-month mentorship program follows two previous pilot programs the bank hosted in 2021 and 2022, according to a Bank of America release. “We received fantastic feedback from the […]

Financial institutions must consider personnel, physical security and technical security when safeguarding their data and operations against cybercrimes. “You must look at all three as a combined piece, especially if you think about that personnel piece in a hybrid environment,” Sue Gordon, former Principal Deputy Director of National Intelligence, said at the recent CBA Live event in Las Vegas. “How […]

KeyBank Executive Vice President of Payments Brandon Nowac is focused on delivering tech-forward automation solutions to the bank’s third-party fintech partners and forming additional partnerships in the year ahead.

BAN caught up with Nowac to discuss KeyBank’s use of technology to mitigate fraud, preparation for the launch of new real-time payment rail FedNow and new technology the bank foresees in the payment space. What follows is an edited version of that conversation.

Bank Automation News: What tech has KeyBank been working on in the payment space?

Brandon Nowac, Executive Vice President of Payments, KeyBank

Brandon Nowac: A lot of times we’re delivering these highly technical, software-first solutions to our customers through our team, but we’re doing it through partnerships and from our API suite that our clients can consume, all the way to the work we’re doing in card acceptance to be able to digitize that whole experience.

Adjacent to it, we acquired XUP and their digital onboarding capabilities. When you think about embedded banking, we can digitize that onboarding experience for that end customer to accept credit card payments online. That’s a digital technology investment but adjacent to core payments on the onboarding side of the equation.

BAN: What technologies stand out in the payments space now?

BN: We do have three power industry verticals in areas of commercial real estate, technology companies and then health care. When we look at technology companies, it’s really the trend of how many new technology businesses’ software-first platforms are coming into the market every year and many times they’re built on user experience workflow management, but there’s a payment somewhere in there. It could be receivable or payable, and that’s where our strategy around tech companies is to help them make or receive payment in their native software that then customers are using.

BAN: How is KeyBank reducing payment fraud through technology?

BN: We are very focused on continuing to present ideas to our clients on ways to mitigate and manage fraud. We’ve been heavily invested in payment gateway partnerships, and one of the gateway partnerships we have is very much focused on fraud and risk management. That’s just an example of where, even in a digital experience, you can work with our team and we’ll use a partnership like a gateway to overlay tools to be able to mitigate fraud in something like card acceptance or merchant acquiring.

BAN: How is KeyBank preparing for the launch of FedNow?

BN: We are live with real-time payments, and we’ve seen good success particularly in some of our industry teams where there’s a product market fit for real-time payments. Although I wouldn’t say its broad adoption at this point, it’s a good conversation with almost every one of our commercial clients. It’s been adopted in certain industries more specifically, and then on our product roadmap, we have investments going into FedNow now as well.

BAN: How would you categorize your leadership style?

BN: I fundamentally believe the most successful businesses have ecosystem leaders, which means you’re well beyond the four walls of a bank, but you’re able to culturally align and then you can align to the ecosystem that you live within.

When we think about our platform of solutions that we bring to an end customer, there’s a massive ecosystem behind the scenes that’s enabling that product or service to be utilized by our client and that could be a network like Mastercard, Visa, American Express, Discover Card, or that could be a core processor, like a Fiserv or others. … I believe in trying to instill in my team [it’s important to be] going beyond being an effective enterprise leader to [becoming] an ecosystem leader.