Etsy Inc., once known as a quirky marketplace for handmade, artisanal and vintage items, seems to be moving further away from its origins amid a much tougher e-commerce landscape and the impact of AI.

Etsy ETSY, +4.83%

will be marketing to a whole new audience on Sunday, when its first Super Bowl commercial will run. The 30-second ad is quirky; it depicts a generic 19th-century American leader who’s flummoxed over how to reciprocate France’s gift of the Statue of Liberty. With the help of an anachronistic smartphone, he and his team search on Etsy using its new Gift Mode option, and find its “Cheese Lover” category after determining that the French love cheese. Voilà — they decide to send the French some cheese.

The commercial is part of Etsy’s push of a new user interface featuring Gift Mode, which lets shoppers search for gifts for a specific type of person or occasion — combining generative AI and human curation to give gift buyers some unusual options.

But are these moves desperate and costly efforts to try to reach potential new buyers, coming on the heels of Etsy’s plans to lay off 11% of its staff?Or could running a TV ad at the most expensive time of the year actually lead to more sales on the once-fast growing marketplace?

Etsy believes these moves will help the company grow again, and its research shows the average American spends $1,600 a year on gifts. “There is no single market leader and Etsy sees a real opportunity to become the destination for gifting,” Etsy’s Chief Executive Josh Silverman said in a recent blog post.

Etsy is clearly under pressure after seeing its gross merchandise sales more than double in 2020 during the pandemic, when it became a go-to place to buy handmade masks and all kinds of items for the home, from vintage pieces to antiques to castoffs. From personal experience as an Etsy seller, I saw sales at my own small vintage-clothing shop more than double in 2020 and then fall back in 2021, while still remaining higher than in 2019. In the last two years, sales have slowed, and some other sellers have witnessed similar patterns, based on their comments in seller forums.

The number of sellers and buyers on the platform has increased on the same level as gross merchandise sales. But e-commerce competition has also gotten more fierce.

“Our main concern with Etsy is growing competition in the space from new players like Temu,” said Bernstein Research analyst Nikhil Devnani, in an email. Temu and fellow Chinese online retailer Shein have raised a lot of investor jitters, as Etsy’s gross merchandise sales have slipped over the last year and are forecast to fall again in its upcoming fourth-quarter earnings report later this month.

Devnani said a Super Bowl ad could potentially help the marketplace gain visibility, something it has always lacked.

“One dynamic they’ve talked about a lot is that brand awareness/recollection is still low, and this keeps frequency low,” he said, noting that Etsy buyers shop on the site about three times per year, on average. “They want to be more top-of-mind … Super Bowl ads are notoriously expensive of course, but can be impactful/get noticed.”

The company’s big focus on Gift Mode, however, could be a risky strategy. How many times a year do consumers look for gifts? And in a note Devnani wrote in October, before the company’s Gift Mode launch, he said that one of the concerns investors have is that Etsy is too niche. “’How often does someone need something special?’ is the rhetoric we hear most often,” he said. Etsy, then, is counting on buyers returning for other items for themselves.

Etsy CEO Silverman believes buyers will come back again and again to purchase gifts. Naved Khan, a B. Riley Securities analyst, said in a recent note to clients that he believes Gift Mode plays to Etsy’s core strengths, offering “unique goods at reasonable prices” versus the mass-produced products sold on Shein, Temu, Amazon.com Inc. AMZN, +2.71%,

and other sites.

Consumer spending has changed, though. At an investor conference in December, Silverman said that consumers are spending on dining out and traveling, instead of buying things.

But while investors still view Etsy as a niche e-commerce site, some buyers and sellers see it overrun with repetitive, non-relevant ads. Complaints about a decline in search capabilities, reliance on email and chat for support, and constant tech changes are common on seller forums and Facebook groups. AI-generated art offered by newer sellers as a side hustle has also become a thought-provoking, debated issue. And there are complaints about mass-produced items making their way on the site.

Etsy said that in addition to its human and automated efforts, it also relies on community flags to help take down infringing products that are not allowed on its marketplace, and that community members should contact the company when if they see mass-produced items for sale on the site.

It also continues to work on search. On its last earnings call, Silverman said the company was moving beyond relevance to the next frontier of search, one “focused on better identifying the quality of each Etsy listing utilizing humans and [machine-learning] technology, so that from a highly relevant result set we bring the very best of Etsy to the top — personalized to what we understand of your tastes and preferences.”

The pressure could build on the company if its latest moves don’t generate growth. Etsy recently gave a seat on its board to a partner at activist investor Elliott Management, which bought a “sizable” stake in the company in the last few months. Marc Steinberg, who is responsible for public and private investments at Elliott, has also has been on the board at Pinterest PINS, -9.45%

since December 2022.

Elliott Management did not respond to questions. But in a statement last week, Steinberg said he was joining the board because he “believe[s] there is an opportunity for significant value creation.” Some sellers fear that the pressure from investors and Wall Street will lead to Etsy allowing mass-produced products onto the site. In its fall update, Etsy said the number of listings it removed for violating its handmade policy jumped 112% and that it was further accelerating such actions.

Etsy’s stock before the news of Elliott’s stake was down about 18% this year. Its shares are now off about 3.65% this year, after recently having their best day in seven years on the news that Steinberg joined the board.

Etsy is a unique marketplace that for many years had a much better reputation than some of its rivals, like eBay EBAY, +0.98%.

But since going public and answering to Wall Street, the need to provide growth and profits for investors has become much more of a driver. The Super Bowl ad and Gift Mode may bring a broader awareness to Etsy, but will it be the right kind of awareness? Sellers like me hope these new efforts will stave off the continuing fight with the likes of Temu and other vendors of mass-produced products, and help Etsy retain the remaining unique aspects of its marketplace.

Toy maker Mattel Inc. on Wednesday reported fourth-quarter results that missed expectations, with the company saying it plans to cut costs this year while continuing to buy back stock.

The cost cuts would follow layoffs by rival Hasbro Inc. HAS, +1.34%

amid a slowdown in demand for toys. They also come as other companies over the past several weeks have announced layoffs and plans to tighten up expenses, as investors seek out bigger profit margins.

Shares of Mattel MAT, +1.57%

were up 1.5% after hours.

“Looking ahead, we are launching a new cost-savings program focused on profitable growth and expect to improve profitability and continue share repurchases in 2024,” Mattel Chief Financial Officer Anthony DiSilvestro said in the company’s earnings release.

Mattel — known for its Barbie and Hot Wheels toys and, increasingly, its efforts to turn them into content — reported fourth-quarter net income of $147.3 million, or 42 cents a share. That compares with net income of $16.1 million, or 4 cents a share, in the same quarter in 2022.

Adjusted for things like severance, product recalls and changes to deferred tax assets, Mattel earned 29 cents a share. Sales rose 16% to $1.62 billion.

Analysts polled by FactSet expected Mattel to report adjusted earnings per share of 31 cents, on revenue of $1.65 billion.

“Execution on our toy strategy was strong and we made meaningful progress in entertainment across film, television, digital and publishing,” Chief Executive Ynon Kreiz said in the company’s earnings release.

“We ended 2023 with the strongest balance sheet we have had in years, putting us in an excellent position to execute our strategy to grow Mattel’s IP-driven toy business and expand our entertainment offering,” he continued.

Mattel reported earnings after the key holiday-shopping season, and as analysts try to gauge the sales impact from the success of the “Barbie” movie released last summer. Mattel executives have said they want to make more films based on some of its other popular toys, and turn “Barbie” into a film franchise.

However, toy demand has been cooler recently, thanks to two years of inflation-fueled higher prices for goods and necessities. Retailers have taken a cautious approach toward stocking their shelves, after getting caught two years ago with too many toys and electronics that people didn’t want.

The Wall Street Journal reported this month that activist investor Barington Capital had taken a stake in Mattel, adding that Barington believed the company should consider “pursuing strategic alternatives” for its Fisher-Price and American Girl businesses.

Bank of America analysts on Tuesday said Mattel and Hasbro were among the companies that were “most at risk of direct impact” from shipping disruptions in the Red Sea. Yemen-based Houthi fighters opposed to Israel’s war in Gaza have attacked ships in the area, forcing lengthy detours and driving up shipping costs. Mattel, the analysts noted, got around 24% of its total sales from the Europe, Middle East and Africa regions in 2022.

During a conference in December, Kreiz said he believed in the long-term growth of the toy industry. But he said that after a jump in growth between 2019 and the pandemic, 2023 would likely be tamer.

“We believe 2023 will be back to normal in terms of shopping patterns and consumer behavior,” he said. “And also even inventory at the retail level and at our level is now reverting back to historical norms.”

Walt Disney Co.’s ESPN, Fox Corp. and Warner Bros. Discovery Inc. are teaming to create a joint sports streaming service.

The as-yet unnamed service, which could be available as early as the fall and offer a sort of Hulu model for sports, comes amid an explosion in sports-streaming rights and audiences.

The service would essentially be a skinny bundle of the companies’ linear channels, including ESPN, ESPN2, ESPNU, SECN, ACCN, ESPNEWS, ABC, Fox, FS1, FS2, BTN, TNT, TBS, truTV, as well as the ESPN+ streaming service.

“The launch of this new streaming sports service is a significant moment for Disney DIS, +2.73%

and ESPN, a major win for sports fans, and an important step forward for the media business,” Disney Chief Executive Bob Iger said in a statement late Tuesday. “This means the full suite of ESPN channels will be available to consumers alongside the sports programming of other industry leaders as part of a differentiated sports-centric service.”

Added Warner Bros. WBD,

CEO David Zaslav: “This new sports service exemplifies our ability as an industry to drive innovation and provide consumers with more choice, enjoyment and value and we’re thrilled to deliver it to sports fans.”

Each company will own one-third of the platform, according to Disney, in a deal reminiscent of the original Hulu, which started off as a joint venture between ABC, Fox and NBCUniversal.

The service will have a new brand with an independent management team, and will be available to bundle with Disney+, Hulu and Max subscriptions.

“We’re pumped,” Fox FOX, +0.55%

CEO Lachlan Murdoch said. “We believe the service will provide passionate fans outside of the traditional bundle an array of amazing sports content all in one place.”

More details, including pricing, will be announced later.

Prominently missing from the deal are Comcast Corp. CMCSA, -1.00%,

which owns NBCUniversal and its sports lineup that includes NFL football and the Olympics, and Paramount Global PARA, -0.21%,

which owns CBS — which carries the NFL and college football, among other sports.

The new service will showcase thousands of high-profile sporting events and include all four major sports leagues — the NFL, NBA, MLB and NHL — as well as college football and basketball, golf, tennis, cycling, soccer and UFC.

Shares of Disney were down 1% in extended trading Tuesday, while Fox shares jumped 6% and WBD gained 3%.

McDonald’s Corp.’s stock fell 1.3% in premarket trading on Monday after the fast-food giant missed Wall Street analysts’ estimates for revenue and same-store sales, while citing an impact from war in the Middle East.

The global fast-food giant said it expects “macro challenges” to persist in 2024.

McDonald’s MCD, -0.35%

said its fourth-quarter net income rose by 7% to $2.04 billion, or $2.80 a share, from $1.9 billion, or $2.59 a share, in the year-ago quarter.

McDonald’s said the latest quarter’s results included 15 cents a share in one-time charges.

Breaking those charges out, McDonald’s would have earned $1.95 a share. Analysts expected McDonalds to earn $1.83 a share, according to FactSet data.

Revenue rose 8% to $6.41 billion, short of the FactSet consensus estimate of $6.45 billion.

Fourth-quarter global comparable-store sales increased by 3.4%, including a 4.3% rise in the U.S.. Analysts expected same-store sales growth of 4.7%.

McDonald’s said its comparable sales fell in the Middle East as a reflection of war in the region since Oct. 7.

All other same-stores sales rose in international developmental licensed markets.

Total international developmental licensed markets same-store sales rose by 0.7%, well below the result in the previous quarter, which saw a 10.5% increase.

Looking back at the balance of 2023, McDonald’s said its net income rose by 37% to $8.47 billion.

Revenue jumped by 10% in 2023 to $25.49 billion.

Free cash flow for 2023 increased to $7.25 billion from $5.49 billion.

Before Monday’s moves, McDonald’s stock was up by 10.9% in the past year.

While the U.S. stock market has been pricing in a “soft-landing” scenario for the economy, a blowout January jobs report, relatively strong corporate earnings, and Federal Reserve Jerome Powell’s comments during the past week could point to the possibility of “no landing,” where the economy is resilient while inflation stays on target.

Such a scenario could still be positive for U.S. stocks, as long as inflation remains steady, according to Richard Flax, chief investment officer at Moneyfarm. However, if inflation reaccelerates, the Fed may be hesitant to cut its policy interest rate much, which could spell trouble, Flax said in a call.

What the past week tells us

Investors have just gone through the busiest week so far this year for economic data and corporate earnings reports, with stocks ending at or near their record highs.

The Dow Jones Industrial Average DJIA

finished the week with its nineth record close of 2024, according to Dow Jones Market Data. The S&P 500 index SPX

scored its seventh record close this year on Friday, while the Nasdaq Composite COMP

is about 2.7% lower from its peak.

The Fed kept its policy interest rate unchanged in the range of 5.25% to 5.5% at its Wednesday meeting, as expected. However, in the subsequent press conference, Fed Chair Jerome Powell threw cold water on market expectations that the central bank may start cutting its key interest rate in March, and underscored that they want “greater confidence” in disinflation.

Roger Ferguson, former Fed vice chairman, said Powell introduced “a new kind of risk, the risk of no landing.”

In that scenario, inflation will stop falling, while the economy is strong, Ferguson said in an interview with CNBC on Thursday. However, Ferguson said he doesn’t think it is the likely outcome.

Traders were pricing in a 20.5% likelihood on Friday that the Fed will cut its interest rates in its March meeting, according to the CME FedWatch tool and that’s down from over 46% chance a week ago. The likelihood that the Fed will kick off its rate cutting program in May stood at 58.6% on Friday.

The stronger-than-expected January jobs data released on Friday further eliminates the chance of a rate cut in March, said Flax.

The U.S. economy added a whopping 353,000 new jobs in January while economists polled by The Wall Street Journal had forecast a 185,000 increase in new jobs. Hourly wages rose a sharp 0.6% in January, the biggest increase in almost two years.

The past week has also been heavy with earnings reports, as several tech giants including Microsoft MSFT, +1.84%,

Apple AAPL, -0.54%,

Meta META, +20.32%,

and Amazon AMZN, +7.87%

reported their financial results for the fourth quarter of 2023.

Among the 220 S&P 500 companies that have reported their earnings so far, 68% have beaten estimates, with their earnings exceeding the expectation by a median of 7%, analysts at Fundstrat wrote in a Friday note.

While the reported earnings by big tech companies have been “okay,” the guidance was not, said José Torres, senior economist at Interactive Brokers.

What has been driving the tech stocks’ rally since last year was mostly the prospect of sales from artificial intelligence products, but tech companies are not able to monetize the trend yet, Torres said in a phone interview.

Adding to the headwinds is a comeback of concerns around regional banks.

On Thursday, New York Community Bancorp Inc.’s stock triggered the steepest drop in regional-bank stocks since the collapse of Silicon Valley Bank in March 2023. New York Community Bancorp on Wednesday posted a surprise loss and signaled challenges in the commercial real estate sector with troubled loans.

Meanwhile, the Fed’s bank term funding program, which was launched in March last year to bolster the capacity of the banking system, will expire on March 11.

If the Fed could start cutting its key interest rate in March, it would be “sort of like the ambulance that was going to pick regional banks up and save them,” said Torres. “Now the ambulance is coming in May at the earliest, I think that we’re in a particularly risky period from now to May,” Torres said.

What should investors do

Investors should go risk-off before May, according to Torres. “Last year, goods and commodities helped a lot on the disinflationary front. This year for disinflation to continue, we’re going to need services to start contributing to that. Then we’re going to need to see an increase in the unemployment rate,” Torres said.

He said he prefers U.S. Treasurys with a tenor of four years or shorter, as the long-dated ones may be susceptible to risks around the fiscal deficit and government borrowing. For stocks, he prefers the healthcare, utilities, consumer staples and energy sectors, he said.

Keith Buchanan, senior portfolio manager at Globalt Investments, is more optimistic. The slowdown in inflation and the relatively strong economic data and earnings “don’t really paint a picture for a risk-off scenario,” he said. “The setup for risk assets still leans towards the bullish expectation,” Buchanan added.

In the week ahead, investors will be watching the ISM services sector data on Monday, the U.S. trade deficit on Wednesday and weekly initial jobless benefit claims numbers on Thursday. Several Fed officials will speak as well, potentially providing more clues on the possible trajectory of rate cuts.

As the U.S. Federal Reserve’s three-year reign in the headlines potentially comes to an end, an analysis of this year’s market themes can offer valuable insights for predicting trends and ensuring attractive returns in 2024.

Beyond the central bank’s actions, pivotal factors shaping the investment landscape this year include fiscal policies, election outcomes, interest rates and earnings prospects.

Throughout 2023, a prominent theme emerged: that equities are influenced by factors beyond monetary policy. That trend is likely to persist.

A decline in interest rates could significantly increase the relative valuations of equities while simultaneously reducing interest expenses, potentially transforming market dynamics. Contrary to consensus estimates, 2023 brought a more robust earnings rebound, leaving analysts optimistic about 2024.

The 2024 U.S. presidential election, meanwhile, introduces a new element of uncertainty with the potential to cast a shadow over the market during much of the coming year.

Choppy trading, modest earnings growth

Anticipating a choppy first half of the year due to sluggish economic growth, we see a better opportunity for cyclicals and small-cap stocks to rebound in the latter part of the year. As uncertainty around the election and recession fears dissipate, a broad rally that includes previously ignored cyclicals and small-caps should help propel the S&P 500 SPX

higher.

Broader macroeconomic conditions support mid-single-digit growth in earnings per share throughout 2024. Factors such as moderate economic expansion, controlled inflation and stable interest rates are expected to provide a conducive environment for companies, enabling them to sustain and potentially improve their earnings performance. We estimate EPS growth of 6.5%. This projected growth aligns with the broader market sentiment indicating a steady upward trajectory in earnings for the upcoming year, fostering investor confidence and supporting valuation expectations across various sectors.

“ If the economy has not been in recession at the time of the first rate cut but enters one within a year, the Dow enters a bear market.”

When it comes to U.S. stock-market performance around rate cuts, the phase of the economic cycle matters. When there has been no recession, lower rates have juiced the markets, with the Dow Jones Industrial Average DJIA

rallying by an average of 23.8% one year later.

If the economy has not been in recession at the time of the first cut but enters one within a year, the Dow has entered a bear market every time, declining by an average of 4.9% one year later. Our base case is a soft landing, but history shows how critical avoiding recession is for the bull market as the Fed prepares to ease policy.

Big on small-caps

This past year has posed a hurdle for small-cap stocks due to the absence of a driving force. These stocks typically perform better as the economy emerges from a recession. While they are currently undervalued, their earnings growth has been notably lacking. If concerns about a recession diminish, a normal yield curve could serve as a potential catalyst for small-cap stocks.

Growth vs. value

The ongoing outperformance of megacap growth stocks that we saw in 2023 might hinge on their ability to sustain superior earnings growth, validating their current valuations. Defensive sectors in the value category, meanwhile, are notably oversold and might exhibit strong performance, particularly toward the latter part of the first quarter. Should concerns about a recession dissipate, cyclical sectors within the value category could outperform, particularly if broader market conditions turn favorable in the latter half of the year.

Handling uncertainty

The Fed’s enduring influence regarding the prospect of a soft landing in 2024 remains a pivotal point in the market’s focus. Considering the themes of the past year and the multifaceted influences on equities beyond monetary policy, investors are advised to navigate through uncertainties stemming from unintended fiscal shifts, upcoming elections and the impact of fluctuating interest rates. While a potentially choppy start to the year is anticipated, it could create opportunities for cyclical and small-cap stocks later in the year.

Ed Clissold is chief of U.S. strategies at Ned Davis Research.

Mark Zuckerberg delighted Meta shareholders and Wall Street this week with news of the social media giant’s first-ever dividend.

The IRS may also be happy, now that it’s staring at millions in taxes on the Meta stock dividends bound for Zuckerberg’s portfolio.

Zuckerberg, the CEO of Meta Platforms Inc. META, +20.32%,

is poised to make $700 million in dividends yearly. He owns nearly 350 million shares, according to FactSet, and the company will start paying a quarterly dividend of 50 cents a share.

That would yield nearly $167 million in federal taxes yearly, after a qualified-dividend tax of 20% and another 3.8% tax on the investment returns of rich households, two accounting experts said.

California income taxes of 13.3% on the dividends could cost Zuckerberg another $93.1 million, said Andrew Belnap, an accounting professor at the University of Texas at Austin’s McCombs School of Business.

All in, that’s a combined $259.7 million in federal and state taxes annually on the Meta dividends, Belnap estimated.

For context, U.S. taxpayers reported over $285 billion in qualified-dividend income to the IRS though mid-November 2023, according to agency statistics. Nearly 30 million tax returns reported qualified dividends through that time.

Meta said it plans a quarterly cash dividend going forward, with the first such payment in March.

Meta shares soared 20.5% on Friday, ending with a record-high close of $474.99. The Dow Jones Industrial Average DJIA,

S&P 500 SPX

and Nasdaq Composite COMP

all closed higher Friday.

‘Zuck is getting a major break’

Meta announced the dividend payment in its earnings results Thursday, on the same week that Americans began filing their income taxes.

A look at Zuckerberg’s dividends and their tax implications offer a peek at the debate about the varying ways wages and wealth are taxed.

“Zuck is getting a major break,” said Andrew Schmidt, an accounting professor at North Carolina State University’s Poole School of Management who also crunched the numbers for MarketWatch.

Approximately $167 million “seems like a high tax bill,” he said. But if Zuckerberg received the $700 million as a straight salary, Schmidt estimated he’d be looking at a roughly $259 million tax bill on the wages after they were taxed at the top marginal rate of 37%.

For federal and state taxes on the Meta dividends, Zuckerberg would face a combined rate of 37.1%, Belnap noted. “His tax rate on this is actually fairly high,” he said.

The gap in tax rates on income derived from wages and investments “has been a big criticism with U.S. tax policy,” Schmidt said, especially as lawmakers look for ways to come up with more tax revenue.

Regular retail investors enjoy the same preferential rates on capital gains and dividends as the top 1% of taxpayers, Schmidt added. The issue is that those dividends and stock profits are a smaller part of their income while salaries, taxed at higher rates, are a bigger proportion.

Belnap noted that California’s state tax rules don’t provide special treatment to dividends.

Zuckerberg received a $1 base salary in 2022, a figure that hasn’t changed in several years. He is now worth $142 billion, according to the Bloomberg Billionaires Index, making him the fifth-richest person in the world.

Meta did not immediately respond to a request for comment.

Taxes on the Meta dividends will not be something Zuckerberg, or any Meta shareholders big or small, need to deal with until next year’s tax season, Belnap and Schmidt observed.

But as taxpayers amass their 1099-DIV forms on dividend income, IRS figures show that it’s mostly upper-echelon taxpayers reaping the rewards on the preferential rates for qualified dividends.

Households worth at least $1 million accounted for 40% of the approximate $285.3 billion in qualified dividends reported through mid-November, according to agency figures.

For less affluent investors, “it’s usually a nice supplement, but I’d say very few people are living off dividends,” Belnap said.

There’s a common belief that “overbought” is a technical condition for a stock, but in practice it seems to be more of an ability.

Meta Platforms Inc.’s stock META, +20.32%

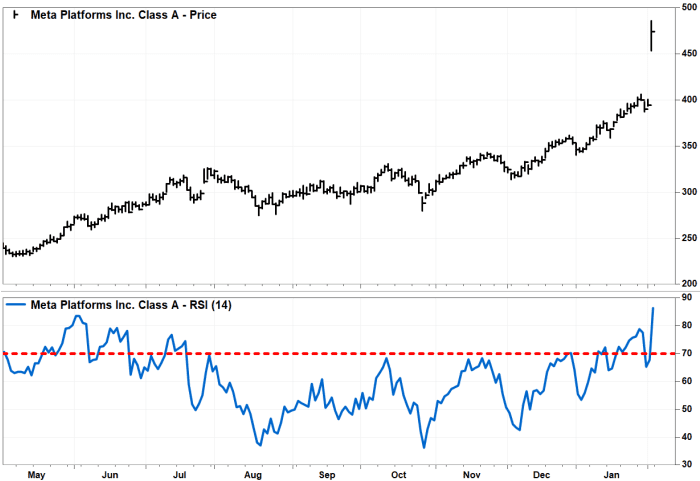

soared so much Friday after a blowout earnings report, that some technical readings have reached levels not seen in 11 years.

The stock rocketed 20.9% to close at a record $474.99, to book the third-biggest gain since going public in May 2012. The only bigger rallies were 23.3% on Feb. 2, 2023 and 29.6% on July 25, 2013, which were also after earnings reports.

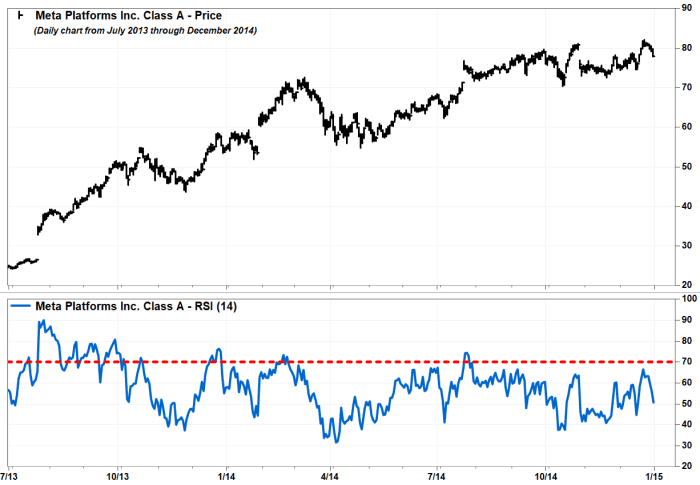

The stock’s Relative Strength Index, which is a momentum indicator that measures the magnitudes of recent gains and losses, climbed to 86.48. That’s the highest level seen since it closed at a record 89.39 on July 30, 2013.

But that shouldn’t scare off Meta bulls.

Many chart watchers believe RSI readings above 70 are signs of “overbought” conditions, which suggests bulls need a breather after running faster and farther than they are used to.

There are also many who believe the ability to become overbought is a sign of underlying strength, since a stock tends to be trending higher when RSI hurdles 70. (Read Constance Brown’s “Technical Analysis for the Trading Professional.”)

For example, the record RSI reading came three days after the record stock-price rally of 29.6% on July 25, 2013. Even though RSI closed at what was then a record of 88.27 after a record price gain on the 25th, the stock continued to rally and become even more overbought.

It was that spike that snapped the stock out of the year-long doldrum that followed the initial public offering, and flipped the long-term narrative on the stock to bullish. (Read “Facebook’s ‘breakaway gap’ is a bullish game changer,” from The Wall Street Journal.)

FactSet, MarketWatch

And while the record RSI readings in July 2013 did lead to a minor short-term pullback, it didn’t stop the stock from embarking on a long-term uptrend, in which RSI made multiple forays above 70.

FactSet, MarketWatch

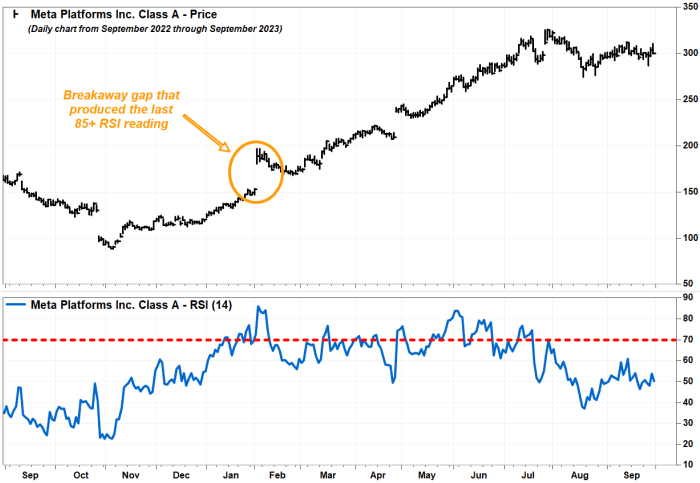

And the last time RSI closed above 85 was Feb. 2, 2023, when it closed at 86.07, also after a blowout earnings report.

And similar to 10 years earlier, that historically high overbought reading helped launch another long-term rally.

FactSet, MarketWatch

So yes, Meta’s stock is now facing historically high overbought conditions. But as many chart watchers like to say, overbought doesn’t mean over.

One thing to consider, however, is that the two prior times RSI spiked above 85 were while the long-term fates of the stock were still in question — the stocks were working on short-term bounces following long-term downtrends.

FactSet, MarketWatch

But Friday’s blast off happened just days after the stock closed at a record high. There was no resistance to hurdle, so rather than a bullish “breakaway gap,” Friday’s jump could be considered more a bullish leap of faith.

Investors bought up shares of Etsy Inc. on Thursday after the online crafts marketplace added to its board of directors a partner of hedge fund Elliott Investment Management L.P., which recently acquired a “sizable” stake in the company.

Etsy ETSY, +9.31%

said Marc Steinberg, who is responsible for public- and private-equity investments at Elliott, has been appointed to the board, effective Feb. 5, and will also join the board’s audit committee.

“Etsy has a highly differentiated position in the e-commerce landscape and a uniquely attractive business model, supported by a distinctive and engaged community,” Steinberg said. “We became a sizable investor in Etsy and I am joining its board because I believe there is an opportunity for significant value creation.”

Etsy’s stock shot up 8% in afternoon trading, to pare earlier gains of as much as 14.2%. The stock was headed for its best one-day gain since it climbed 9.2% on July 11.

Elliott’s stake was acquired in recent months, as the fund’s disclosure of equity holdings through the third quarter did not list Etsy shares.

“Marc’s appointment reflects our ongoing commitment to enhance the perspectives and expertise on the Etsy Board,” said Etsy Chairman Fred Wilson. “We look forward to benefiting from his voice in the boardroom as a seasoned and experienced investor as we continue our journey of creating a leading global e-commerce platform.”

Etsy’s stock has run up 18.6% over the past three months, but has tumbled 48.5% over the past 12 months. That’s compared with the S&P 500 index’s SPX

18.7% rally over the past year.

At an investor conference in December, Chief Executive Josh Silverman said business has slowed since the post-pandemic boom, as people have “had enough of buying things” and are now spending primarily on eating out and travel. Inflation and the loss of government subsidies was also weighing on spending.

Still, Silverman said, Etsy is now about two and a half times bigger than it was before the pandemic, and the company has more active buyers than it did at the peak of the pandemic.

Flutter Entertainment, the parent company of FanDuel, started trading on the New York Stock Exchange for the first time Monday, as the company tries to narrow the valuation gap between it and rivals including DraftKings.

Flutter said Monday that it’s planning to make the New York Stock Exchange its primary listing and will put that to a vote of its shareholders in May. Making the NYSE its home, rather than London, will help it get included in important U.S. indexes, the company said.

Launching Monday with the ticker FLUT, it’s targeting New York as its primary listing late in the second quarter and early in the third quarter.

Having a New York listing will also boost its profile in the U.S., help with recruitment and retention, and access “much deeper” capital markets.

Flutter CEO Peter Jackson spoke with Yahoo Finance about the company after it started trading on Monday. The total addressable U.S. sports betting market is expected to reach $40 billion by 2023 — but Jackson thinks that’s lowballing it. “I expect [$40 billion] will turn out to be conservative, because everything in America turns out bigger than you expect,” he said.

Oil futures popped higher Sunday evening, after a drone attack that killed three U.S. service members in northern Jordan, blamed by the White House on Iran-backed militants, marked a major escalation of tensions in the Middle East.

West Texas Intermediate crude for March delivery CL00, +1.22%

CLH24, +1.22%

was up $1.09, or 1.4%, at $79.10 a barrel on the New York Mercantile Exchange. March Brent crude BRN00, +1.15%

BRNH24, +1.14%,

the global benchmark, gained $1.11, or 1.3%, to trade at $84.66 a barrel on ICE Futures Europe.

Much will ultimately depend on the U.S. response and whether Iran takes action aimed at shutting down the Strait of Hormuz, Tariq Zahir, managing member at Tyche Capital Advisors, told MarketWatch on Sunday afternoon.

“We are on the cusp of this escalating, which could seriously impact the flow of crude oil,” he said.

Three U.S. service members were killed and more than two dozen injured in a drone strike on a U.S. base in northeast Jordan, according to U.S. Central Command. They were the first U.S. fatalities in months of attacks on U.S. bases by Iran-backed militias since the start of the Israel-Hamas war in October.

President Joe Biden attributed the Sunday attack to an Iran-backed militia group and said the U.S. “will hold all those responsible to account at a time and in a manner (of) our choosing.” News reports said U.S. officials were still working to conclusively identify the precise group responsible for the attack, but have assessed that one of several Iranian-backed groups is to blame.

Some congressional Republicans called for direct retaliation on Iran.

“We must respond to these repeated attacks by Iran & its proxies by striking directly against Iranian targets & its leadership. The Biden administration’s responses thus far have only invited more attacks. It is time to act swiftly and decisively for the whole world to see,” wrote Sen. Roger Wicker of Mississippi, the senior Republican on the Senate Armed Services Committee, in a post on X.

Oil futures rallied last week to their highest since November, but with gains attributed in part to production outages in the U.S. and more upbeat expectations around economic growth.

“Crude already has the wind to its back, so this will only offer further upside,” Chris Weston, head of research at Australian brokerage Pepperstone told MarketWatch in an email.

With the U.S. election later this year, “Biden needs to strike a balance between increasing aggression that potentially puts U.S. serviceman lives in danger and could potentially raise the cost of living…while also showing a defiant stance that shows his resolve against terror,” Weston said.

Oil prices have seen short-lived rallies around developments in the Middle East since the start of the Israel-Hamas war, but have failed to build in a lasting geopolitical risk premium. West Texas Intermediate crude CL00, +1.22%

CL.1, +1.22%,

the U.S. benchmark, remains around $15 below its 2023 peak in the mid-$90s set in late September. Brent crude BRN00, +1.15%,

the global benchmark, pushed back above $80 a barrel last week.

Attacks by Iran-backed Houthi militants on Red Sea shipping have forced a rerouting of tankers and cargo ships. For crude, that’s had implications for the physical market but hasn’t interrupted the flow of crude from the Middle East.

A move by Iran aimed at closing off the Strait of Hormuz, the world’s biggest oil-transportation chokepoint, remains a top worry.

The strait is a narrow waterway that links the Persian Gulf with the Gulf of Oman and the Arabian Sea. At its narrowest point, the waterway is only 21 miles wide, and the width of the shipping lane in either direction is just two miles, separated by a two-mile buffer zone.

Energy Information Administration

Around 21 million barrels a day of crude moved through the waterway in the first half of 2023, equivalent to around a fifth of daily global consumption, according to the U.S. Energy Information Administration.

The U.S. stock market has largely looked past Middle East tensions, with the S&P 500 SPX

returning to record territory this month, while the Dow Jones Industrial Average DJIA

has also set a series of records.

Dow futures YM00, -0.20%

were off 94 points, or 0.3% as Asian trading got under way, while S&P 500 futures ES00, -0.22%

fell 12 points, or 0.2%, and Nasdaq-100 futures NQ00, -0.24%

lost 0.3%.

Away from oil, there were no signs of a significant surge in demand for instruments that traditionally serve as havens during periods of increased geopolitical tension. Futures on U.S. Treasurys TY00, +0.21%

saw a modest rise of 0.2%, while the U.S. dollar DXY

was little changed versus major rivals and gold futures GC00, +0.41%

ticked up 0.4%.

Escalating Middle East tensions won’t go unnoticed by traders, but probably doesn’t warrant a “solid derisking,” Weston said, particularly with investors facing a barrage of major market events in the week ahead.

For U.S.-focused investors, the week ahead features a Federal Reserve policy meeting, earnings from tech industry heavyweights and a crucial December jobs report.

The Middle East situation “won’t take us too far off the rates, growth track, but we have an eye on whether this escalates,” Weston said.

With a rough 2023 in the rearview mirror, Levi Strauss & Co. this year is trying to tackle its problems with new pants.

That includes pants with lighter-weight denim; pants for women that can be worn as high-rise or low-rise; and even nondenim pants that management, during Levi’s LEVI, +1.27%

earnings call on Thursday, referred to as a “tech pant” for men with “moisture control and 360 mobility.” The company also plans to expand its offerings of Performance Cool pants intended to keep the wearer cool and dry on hotter days.

But as those products roll out, the retailers that account for most of Levi’s sales are still cautious about packing their shelves with new apparel — even though Levi’s executives pointed to slightly better demand from clothing stores during the fourth quarter and holiday period. And as the denim pioneer cuts costs, brings in new leadership and tries to be a bigger e-commerce player, Wall Street will now be digging around for signs of a payoff.

“Ultimately, the market will be looking for evidence new strategies can drive accelerated growth,” Stifel analyst Jim Duffy said in a research note on Thursday.

“We continue to believe in brand vitality and opportunities for extension. With product reflective of new direction arriving in the marketplace across 2024, the proof will be in consumer response,” he continued.

In an interview with MarketWatch on Friday, Duffy said he was optimistic about Levi’s standing as an established brand and stronger demand for its dresses, skirts and other women’s clothing items. But the more products a company rolls out, he suggested, the more it has to invest to make them work — and the more it needs to manage if sales falter.

“The risk, as I see it, is that more categories means more SKUs and more product that is fashion rather than core basic styles, and more investment and inventory that, if it doesn’t translate to the marketplace, could result in higher markdowns,” he said, referring to the stock-keeping units by which retailers track inventory.

Levi’s on Thursday said it would lay off between 10% and 15% of its global corporate staff in the first half of this year, a move intended to save $100 million in costs over that period. The layoffs are part of a two-year plan, called Project FUEL, intended to save money and strengthen the part of Levi’s business that sells directly to consumers via its own e-commerce network and its physical stores, as opposed to third-party retail operations.

The layoff announcement arrived days ahead of Chief Executive Chip Berg’s departure from that role, with Michelle Gass taking over on Jan. 29. As the company tries to be bigger than men’s jeans, Gass, in Levi’s earnings release on Thursday, said she saw an opportunity to grow internationally, make Levi’s own online and bricks-and-mortar sales a greater priority, and turn the brand into a larger “denim apparel lifestyle business.”

Levi’s shares fell after hours Thursday, after the company’s full-year profit forecast came in below expectations. The stock rebounded 1.3% on Friday but is still down 10.3% over the past 12 months.

Still, Levi’s direct-to-consumer sales jumped 11% during the fourth quarter, and accounted for 42% of sales overall. Duffy said that the company has pushed deeper into its direct-sales business because it gives executives greater insight into what consumers want, as well as more control over how it markets and sells its clothing. Cutting out other retailers also widens margins on sales, he noted.

Levi’s operating margins were higher in the fourth quarter. It also declared a dividend of 12 cents per share, payable in cash on Feb. 23.

But sales in Levi’s wholesale segment — the sales it gets from retailers who buy Levi’s product, then sell it to consumers — fell 2%. Better results in the U.S. and Asia were offset by a drop in Europe, the company said.

Retailers have spent the past two years trying to clear unwanted clothes from their stockrooms, and cutting prices in the process, after spiking inflation restricted many shoppers’ appetites to basics.

As Gass prepares to take the reins, she sought to put a positive spin on retail-chain sentiment. “So net-net, overall, as a company, we’re exiting the year on a strong note,” Gass said on the earnings call. “And U.S. wholesale, we’re encouraged. But as it relates to that channel, we’re not declaring victory yet. There’s been a lot of volatility this past year, some in our control, some outside. And so we are taking a cautious approach as we look forward.”

The U.S. dollar has had a relatively strong start to 2024 — but some analysts believe the greenback is still more likely than not to depreciate over the course of this year.

The ICE U.S. Dollar Index DXY,

which tracks the currency against a basket of six major rivals, has climbed about 2.1% so far this year, per Dow Jones Market Data.

As recently as late December, traders were pricing a likelihood as high as 90% for a rate cut in March — but those chances have since fallen to around 46% as of Friday, according to the CME FedWatch Tool. Meanwhile, the total amount of rate cuts priced in for this year, which reached as high as 170 basis points in mid-January, has now slipped to around 135 to 150 basis points.

However, the greenback is likely to see depreciation throughout the rest of this year, analysts at the investment bank wrote in a Thursday note, adding that much of the retreat would likely happen in the second half of 2024.

The BofA analysts said expect no recession this year and anticipate that the Federal Reserve will start cutting its key policy rate in March. Such a scenario is negative for the dollar, as the Fed’s easing would likely support risk assets with U.S. economic growth remaining resilient, according to the analysts.

Based on historical data, the ICE U.S. Dollar Index’s performance has been mixed from the onset of the Fed’s first rate cut over the past six cycles, and has been relatively flat on average over the following quarters, the analysts said.

“This is due in large part to the USD’s perceived ‘safe haven’ status and its negative correlation to risk, as cutting cycles have often been associated with recessions,” they wrote.

Jonathan Petersen, senior market economist at Capital Economics, echoed that point in a Thursday note. He expects the dollar to face headwinds from strong risk appetite in global markets and falling bond yields in the U.S. over the course of the year, and anticipates the greenback will remain rangebound against most major currencies for most of 2024.

The Biden administration’s announcement Friday that it’s pausing liquefied natural gas export approvals sparked political backlash, drew cheers from climate activists and stoked uncertainty in energy markets, but is unlikely to see the U.S. give up its title as the world’s top LNG exporter.

The U.S. will delay its decisions on new LNG exports to non-free trade agreement countries, allowing time for the Energy Department to update the underlying analyses for LNG export authorizations, the White House said.

Those analyses are roughly five years old and “no longer adequately account for considerations” such as potential cost increases for American consumers and manufacturers or the “latest assessment of the impact of greenhouse gas emissions,” it said.

The Biden administration likely “realizes the role of LNG in foreign policy, but at the same time it needs to show the Democrat base that it is doing something for climate change,” said Anas Alhajji, an independent energy expert and managing partner at Energy Outlook Advisors, pointing out that the announcement comes during a presidential election year.

“Delaying one project or stopping it may not be a big deal, but it is a problem if it becomes a trend,” he said in emailed commentary.

Environmental groups, which have pushed for action, cheered the decision.

The 12 impacted projects in the U.S. “would spew out as much climate-warming pollution as 223 coal plants per year, and they present explosion risks to the communities where they’re located and emit other health-harming chemicals,” the Sierra Club, an environmental group, said in a statement welcoming the decision.

Top exporter

The announcement is particularly important for a nation that became the world’s biggest LNG exporter in the span of less than a decade.

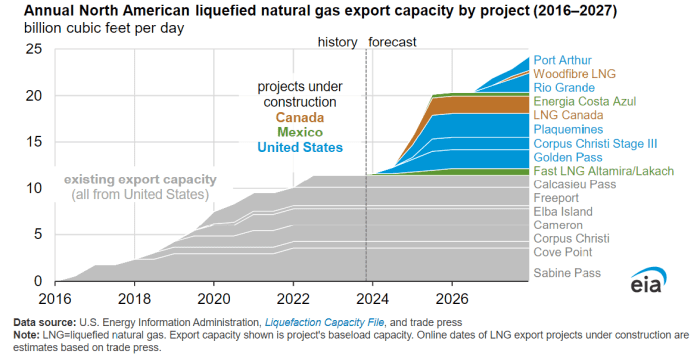

The U.S. became the world’s largest LNG exporter during the first half of 2022 on the back of increases in LNG export capacity, international natural gas and LNG prices, and global demand, particularly in Europe, according to the Energy Information Administration.

The country’s exports of LNG climbed to a fresh record in November 2023, with the EIA reporting domestic exports of 386.2 billion cubic feet, up from 384.4 bcf a month earlier. Exports in December 2016 were at just 41.8 bcf.

U.S. LNG exports soared after 2016.

EIA

With 90% of U.S. LNG going to non-free trade agreement destinations, withholding licensing effectively “halts project development,” John Miller, managing director, ESG and sustainability policy at TD Cowen wrote in a Friday note.

Equities

LNG equities with operating facilities likely won’t benefit from the administration’s announcement, at least not immediately, until the impacts of this pause in export approvals to non-FTA countries becomes more clear, Jason Gabelman, director, sustainability & energy transition at TD Cowen said.

U.S. companies with government approvals that have not been sanctioned, “could have a higher probability of moving forward this year, albeit modestly” as offtakers may be hesitant to sign up to new U.S. projects with LNG development getting “politicized,” he said. Among those, he pointed out approvals for proposed liquefaction units at NextDecade Corp.’s NEXT, +2.30%

Rio Grande LNG export facility project in Brownsville, Texas.

At the same time, it would not be a surprise if U.S. LNG companies pursuing growth that do not yet have non-FTA approval see downside pressure, said Gabelman.

LNG projects take around 4 years to build and any delays to project sanctions today will take “multiple years to manifest in the market,” he said.

Still, the U.S. announcement “introduces the risk of more stringent oversight that could limit new U.S. capacity” more than four years out, Gabelman said.

Companies that supply equipment to LNG liquefaction projects include Baker Hughes Co. BKR, +0.59%

and Chart Industries Inc. GTLS, -7.54%,

said Marc Bianchi, a senior energy analyst at TD Cowen.

Any slowing of approval would create “overhand on order growth,” he said.

Climate change

The White House said Friday that its decision will not impact the ability of the U.S. to continue supplying LNG to its allies in the near term but also acknowledged environmental concerns.

“I think we’ve got to be clear eyed about the challenges that we face. The climate crisis is an existential crisis, and we’ve got to be, I think, really forward leaning into making sure that we’re taking that head on,” said Ali Zaidi, the White House national climate adviser, told reporters Friday.

He added that given the number of approvals already completed, the number of projects under construction are set to double existing capacity with approvals beyond that set to double capacity yet again.

“So there’s a long runway here, and we’re taking a step back and thinking, OK, let’s take a hard look before that runway continues to build out,” he said.

Rob Thummel, senior portfolio manager at Tortoise, argued that U.S. LNG exports actually reduce global carbon emissions as natural gas typically “displaces coal to generate electricity in countries such as China and India.”

They also improve global energy security as U.S. natural gas is becoming Europe’s primary energy supplier, replacing Russia, he said.

In a statement Friday, Sen. Joe Manchin, a West Virginia Democrat and chairman of the U.S. Senate Energy and Natural Resources Committee, said that if the Biden administration has facts to prove that additional LNG export capacity would hurt Americans, it needs to make that information public. But if the pause is “another political ploy to pander to keep-it-in-the-ground climate activists,” he said he would “do everything in my power to end this pause immediately.

Manchin plans to hold a hearing on the decision in the coming weeks.

Market impact

The U.S. decision to delay new LNG export permits is unlikely to have an impact on domestic natural-gas supplies or prices, said Energy Outlook Advisors’ Alhajji.

LNG prices and the rate at which new LNG export terminals can be constructed help determine LNG export volumes, the EIA said, and higher LNG exports can result in upward pressure on U.S. natural-gas prices, while lower U.S. LNG exports can pressure prices.

On Friday, natural gas for February delivery NG00, +0.23%

NGG24, +0.26%

settled at $2.71 per million British thermal units, up 7.7% for the week.

Meanwhile, the U.S. is likely to keep its position as the world’s top LNG exporter, according to Tortoise’s Thummel.

The U.S. is the currently the largest LNG exporter at almost 12 bcf per day, with Qatar coming in second, he said.

Qatar is expanding its LNG export capacity and is expected to have the ability to export almost 20 bcf per day by 2028, he said. The EIA reported recently that Qatar has averaged 10.3 bcf per day in exports during the last 10 years.

That would mark sizable growth. But the EIA reported in November that LNG export capacity from North America is likely to more than double from around 11.4 bcf per day to 24.3 bcf per day by the end of 2027.

The EIA said North America’s LNG export capacity is likely to more than double by 2027.

EIA

Given expected growth in U.S. LNG export capacity, the U.S. is likely to “remain the largest exporter of LNG in the world” despite the U.S. announcement, said Thummel.

As Intel Corp.’s stock plunged to its biggest one-day drop in about three and a half years, analysts had some harsh words for the chip maker.

“How many times can you push the reset button?” Bernstein’s Stacy Rasgon asked in a note to clients.

While he thought many investors were bracing for the company to miss on its first-quarter forecast, the outlook came in “extremely weak and clearly worse than feared.” Intel INTC, -11.91%

expects $12.7 billion in revenue at the midpoint, while analysts had been looking for $14.3 billion.

“After yet another major reset this story probably just shifted to 2026 at the earliest for the bulls, and there is a lot of meat for the bears to sink their teeth into in the meantime,” Rasgon wrote, while sticking with his market-perform rating and $42 target price.

Baird’s Tristan Gerra highlighted challenges for Intel’s data-center and artificial-intelligence unit, which is “on track for a third consecutive year of revenue declines,” while his own revenue forecast implies a 14-year low.

Gaudi, the company’s accelerator chip for artificial-intelligence applications, “does not seem enough to lift [data-center] revenue, while gross margin will be impacted by higher depreciation inclusive of an expected U.S. Chip Act credit,” Gerra continued.

He also expressed some concerns about the company’s broader road ahead.

“Can top-line growth in future years be sufficient to fund continued node migration?” Gerra said. “Many hurdles remain, notably ramping units from this year’s small base (small baseline for Intel 4 makes it more challenging to yield at the next node), while [the Intel Foundry Service] revenue ramp entirely depends on future node execution including yield and performance.”

Gerra has a neutral rating and $40 target price on Intel’s stock.

Shares fell 11.9% in Friday trading, making for their worst single-day percentage decline since July 24, 2020, when they fell 16.2%, according to Dow Jones Market Data.

Needham’s N. Quinn Bolton, meanwhile, downgraded the stock to hold from buy in the wake of Thursday afternoon’s report, calling the earnings reset “unexpected.”

“In addition to an overall worsening risk-reward, Intel’s core [data-center] business is challenged by a shift to accelerated computing architectures and direct competition from AMD and ARM,” he wrote. “We expect AI to remain the spending priority in the data center for the next several quarters. To that end, dollars will continue moving away from Intel’s core competency.”

Rosenblatt’s Hans Mosesmann took a similar view as he argued that Intel’s sales outlook is “contrary to the uber bullish messaging to the Street and is consistent with share losses to AMD, a lack of any perceivable AI growth vector that moves any dial, and points to another, yes another, transitional year.”

Artificial intelligence “seems like everywhere except at Intel,” he continued, noting that his stance on the stock “has not changed for many years.” Mosesmann continues to rate it at sell.

Raymond James analyst Srini Pajjuri, however, was more upbeat about Intel’s ability to capitalize on AI. “While Intel won’t likely get much credit for AI in the near term, we are encouraged by the growing pipeline for Gaudi accelerators ($2b+) and expect meaningful revenue contribution” in the second half of 2024, he wrote, while sticking with his outperform call but cutting his target price to $52 from $54.

The notion that the Federal Reserve will soon slow, or perhaps even end, its program of quantitative tightening is increasingly being talked about on Wall Street like a foregone conclusion.

But while investors wait to hear more on the subject from Fed Chair Jerome Powell during next week’s post-meeting press conference, they could be forgiven for asking themselves some questions.

What might an imminent taper of the Fed’s balance-sheet runoff look like? Why has it suddenly become so urgent? What might it mean for the six or so interest-rate cuts investors are expecting from the Fed this year, as well as for markets more broadly?

We aim to answer these questions below.

What inspired talk of tapering QT?

It wasn’t until the minutes from the Federal Reserve’s December policy meeting were published earlier this month that investors started to take the notion of the Fed declaring “mission accomplished” on QT seriously.

The minutes revealed that a number of senior Fed officials felt it was nearly time to “begin to discuss” the technical factors that would govern the Fed’s decision to slow the runoff of maturing bonds from its balance sheet.

Shortly after the minutes’ release, several senior Fed officials came forward to discuss the importance of ending the balance-sheet runoff. Dallas Fed President Lorie Logan, the first senior Fed official to expand on what was noted in the minutes, said earlier this month that the Fed should start to slow the pace of its balance-sheet shrinkage once assets locked up in the Fed’s reverse-repo facility fell below a certain level.

According to Logan, senior Fed officials had been unsettled by the drain of $2 trillion in assets from the RRP facility last year.

But there was another issue that was also likely bothering monetary policymakers heading into the Fed’s December meeting.

Sudden spikes in overnight repo rates late last year drew uncomfortable comparisons to the repo-market crisis of September 2019, which foreshadowed the end of the Fed’s previous attempt at tapering its balance sheet, according to TS Lombard’s Steve Blitz.

What is the Fed’s ‘lowest comfortable level of reserves’?

A re-run of the repo-market crisis of 2019 is what the Fed is presumably trying to avoid. Economists are so concerned the central bank might accidentally bump up against the lower bound for reserves in the banking system, that they have come up with a name for the concept: They’re calling it the “lowest comfortable level of reserves.”

According to this idea, strain in overnight-financing markets should emerge once reserves in the banking system retreat below a certain threshold. This would, in turn, likely force the central bank to scale back or even reverse quantitative tightening immediately, according to several economists.

In order to avoid such a risk, Jefferies economist Thomas Simons said in a note to clients earlier this month that he expects the Fed will announce plans to start tapering QT after its March meeting.

Across Wall Street, most economists expect the Fed will begin by tapering the pace at which Treasurys are redeemed from its balance sheet — perhaps cutting it in half to start, from $60 billion a month to $30 billion a month. Reducing the pace at which mortgage-backed securities are running off won’t matter as much until prepayments begin to climb.

Going even further, economists at Evercore ISI said in a report shared with MarketWatch earlier this week that they expect the tapering to begin around the middle of 2024 and continue potentially through 2025, until the Fed has succeeded in reducing the size of its balance sheet to about $7 trillion.

The balance sheet presently stands at $7.7 trillion, according to data published by the Fed. It peaked at nearly $9 trillion in April 2022.

However, one key issue may complicate the Fed’s efforts to ascertain the “LCLoR.” According to Jefferies’ Simons, the amount of banking-system reserves counted as liabilities on the Fed’s balance sheet has been more or less steady since the Fed started its latest round of balance-sheet tapering. It stood at roughly $3.3 trillion recently, according to Fed data cited by Jefferies.

Why stop at $7 trillion if bank reserves haven’t been all that heavily impacted by QT anyway? It’s probably worth noting that, whatever happens, nobody on Wall Street expects the Fed would attempt to shrink the size of its balance sheet back toward pre-crisis levels, when the amount of bonds on its balance sheet was miniscule compared to today.

Why? Because there is simply too much debt sloshing around the global financial system to justify such a withdrawal of support, according to Steven Ricchiuto, chief economist at Mizuho Americas.

“The Fed is not in a position to remove all that extra liquidity because now the system needs it just to function,” Ricchiuto said.

What does this mean for markets?

Because quantitative tightening is a hawkish policy stance, its rolling back should be bullish for stocks and bonds. But there are other considerations that could impact the outcome, market strategists said.

Not only would a reduction in the pace of the Fed’s monthly runoff introduce a fresh dovish tilt to the Fed’s monetary policy, but by reducing the amount of bonds it allows to roll off its balance sheet every month, the Fed would become more active in the Treasury market, said James St. Aubin, chief investment officer at Sierra Investment Management, during an interview.

There are also a few contextual factors that could impact how the equity market reacts. For example, as St. Aubin pointed out, context is equally as important as the nature of the decision itself. Should the Fed decide to end QT abruptly because the U.S. economy is sliding into a recession, then the decision could hurt stocks.

Another issue, raised by a different market strategist, is the notion that the Fed could decide to start tapering QT in lieu of cutting interest rates — or at least in lieu of cutting them as quickly as investors expect. This could buy the central bank more time to press its battle against inflation while mitigating the risks that it could hurt the economy by keeping policy uncomfortably tight for too long, economists said.

Ben Jeffery, U.S. interest-rate strategist at BMO, said in a recent note to clients that, based on Logan’s comments from earlier this month, he would lean toward this being the most likely scenario. Additionally, he said, tapering QT could potentially impact the Treasury’s refunding announcement due in May.

Jeffery calculated that the Fed tapering QT by $20 billion beginning in April would save the Treasury from issuing nearly $250 billion in bonds compared to if the Fed had continued with its balance-sheet runoff apace.

This should lead to lower Treasury yields, all else being equal. And lower long-dated Treasury yields are typically seen as beneficial for stocks, according to Callie Cox, a U.S. equity strategist at eToro.

Although, once again, the outcome for markets would likely depend on the specific context.

“Higher yields probably aren’t a good thing for stock investors these days, but in particular environments, higher yields and less Fed intervention could hint that the economy is healing,” Cox said.

JetBlue Airways Corp. and Spirit Airlines Inc. said late Friday that they have appealed a court ruling that earlier this week blocked their planned merger.

JetBlue JBLU, -1.19%

and Spirit SAVE, +17.19%

announced the appeal in a terse press release that provided no more details, adding only that the process is “consistent with the requirements of the merger agreement.”

Wall Street was split on whether the airlines would be legally obliged to appeal the Tuesday ruling, which sided with the Justice Department in saying that a merger between low-cost JetBlue and ultra-low-cost Spirit would hurt competition.

Shares of Spirit rallied 12% after hours Friday, while JetBlue shares fell nearly 2%. Analysts at JP Morgan said this week that the ruling freed JetBlue from a “costly merger.”

The likelihood of Spirit attracting a new merger or takeover bid is considered low without a debt restructuring. Frontier Group Holdings Inc. ULCC, -2.13%

and JetBlue competed for Spirit in 2022, with Frontier ultimately bowing out in July of that year.

Raymond James analyst Savanthi Syth said in a note earlier Friday that it was “clear to us that Spirit is pressing JetBlue to appeal the antitrust ruling, but we continue to believe the chances of success are low.”

Syth has estimated that an appeal would take some four to five months.

Shares of Spirit have lost 67% in the past 12 months, while shares of JetBlue are down 41%. The U.S. Global Jets ETF JETS

has lost 9% in the same period. Those losses contrast with gains of 24% for the S&P 500 index SPX.

Distressed-debt giant Oaktree Capital sees big opportunities in credit unfolding over the next few years as a wall of debt comes due.

Oaktree’s incoming co-chief executives Armen Panossian, head of performing credit, and Bob O’Leary, portfolio manager for global opportunities, see a roughly $13 trillion market that will be ripe for the picking.

Within that realm is high-yield bonds, BBB-rated bonds, leveraged loans and private credit — four areas of the market that have only mushroomed from their nearly $3 trillion size right before the 2007-2008 global financial crisis.

“Clearly, the most acute area of risk right now is commercial real estate,” the co-CEOs said in a Wednesday client note. “That’s because the maturity wall is already upon us and it’s not going to abate for several years.”

More than $1 trillion of commercial real-estate loans are set to come due in 2024 and 2025, according to the Mortgage Bankers Association.

A retreat in the benchmark 10-year Treasury yield BX:TMUBMUSD10Y,

to about 4.1% on Wednesday from a 5% peak in October, has provided some relief even though many borrowers likely will still struggle to refinance.

“There’s a need for capital, especially for office properties where there are vacancies, rental growth hasn’t materialized, or the rate of borrowing has gone up materially over the last three years. This capital may or may not be readily available, and for certain types of office properties, it absolutely isn’t available,” the Oaktree team said.

With that backdrop, the firm expects to dust off its playbook from the financial crisis and acquire portfolios of commercial real-estate loans from banks, but also plans to participate in “credit-risk transfer” deals that help lenders reduce exposure.

Oaktree also sees opportunities brewing in private credit, as well as in high-yield and leveraged loans, where “several hundred” of the estimated 1,500 companies that have issued such debt are likely “to be just fine” even if defaults rise, they said.

Another area to watch will be the roughly $26 trillion Treasury market, where Oaktree has some concerns “about where the 10-year Treasury yield goes from here” — given not only the U.S. budget deficit and the deluge of supply that investors face, but also how foreign buyers, once the “largest owners in prior years, may be tapped out.”

COMP

fell Wednesday after strong retail-sales data for December pointed to a resilient U.S. economy, despite the Federal Reserve having kept its policy rate at a 22-year high since July.

TOKYO (AP) — Asian shares slid Wednesday after a decline overnight on Wall Street and disappointing China growth data, while Tokyo’s main benchmark momentarily hit another 30-year high.

Japan’s benchmark Nikkei 225 NIY00, -0.95%

reached a session high of 36,239.22, but reverted lower, last down 0.3% to 35,477. The Nikkei has been hitting new 34-year highs, or the best since February 1990 during the so-called financial bubble. Buying focused on semiconductor-related shares, and a cheap yen helped boost exporter issues.

Hong Kong’s Hang Seng HK:HSCI

tumbled 4% to 15,220.72, with losses building after data showed China hitting its economic growth target of 5.2% for 2023, surpassing government expectations, but short of the 5.3% some analysts expected. The Shanghai Composite CN:SHCOMP

shed 2% to 2,833.62.

Australia’s S&P/ASX 200 AU:ASX10000

slipped 0.2% to 7,401.30. South Korea’s Kospi KR:180721

dropped 2.4% to 2,435.90.

Investors were keeping their eyes on upcoming earnings reports, as well as potential moves by the world’s central banks, to gauge their next moves. Wall Street slipped in a lackluster return to trading following a three-day holiday weekend.

The S&P 500 SPX

fell 17.85 points, or 0.4%, to 4,765.98. The Dow Jones Industrial Average DJIA

dropped 231.86, or 0.6%, to 37,361.12, and the Nasdaq COMP

sank 28.41, or 0.2%, to 14,944.35.

Spirit Airlines SAVE, -47.09%

lost 47.1% after a U.S. judge blocked its takeover by JetBlue Airways JBLU, +4.91%

on concerns it would mean higher airfares for flyers. JetBlue rose 4.9%.

Stocks of banks were mixed, meanwhile, as earnings reporting season ramps up for the final three months of 2023. Morgan Stanley MS, -4.16%

sank 4.2% after it said a legal matter and a special assessment knocked $535 million off its pretax earnings, while Goldman Sachs GS, +0.71%

edged 0.7% higher after reporting results that topped Wall Street’s forecasts.

Companies across the S&P 500 are likely to report meager growth in profits for the fourth quarter from a year earlier, if any, if Wall Street analysts’ forecasts are to be believed. Earnings have been under pressure for more than a year because of rising costs amid high inflation.

But optimism is higher for 2024, where analysts are forecasting a strong 11.8% growth in earnings per share for S&P 500 companies, according to FactSet. That, plus expectations for several cuts to interest rates by the Federal Reserve this year, have helped the S&P 500 rally to 10 winning weeks in the last 11. The index remains within 0.6% of its all-time high set two years ago.

Treasury yields BX:TMUBMUSD10Y

have already sunk on expectations for upcoming cuts to interest rates, which traders believe could begin as early as March. It’s a sharp turnaround from the past couple years, when the Federal Reserve was hiking rates drastically in hopes of getting high inflation under control.

Easier rates and yields relax the pressure on the economy and financial system, while also boosting prices for investments. And for the past six months, interest rates have been the main force moving the stock market, according to Michael Wilson, strategist at Morgan Stanley.

He sees that dynamic continuing in the near term, with the “bond market still in charge.”

For now, traders are penciling in many more cuts to rates through 2024 than the Fed itself has indicated. That raises the potential for big market swings around each speech by a Fed official or economic report.

On Wall Street, Boeing fell to one of the market’s sharper losses as worries continue about troubles for its 737 Max 9 aircraft following the recent in-flight blowout of an Alaska Air ALK, -2.13%

jet. Boeing BA, -7.89%

lost 7.9%.

In energy trading, benchmark U.S. crude CL00, -1.55%

lost 90 cents to $71.75 a barrel. Brent crude BRN00, -1.37%,

the international standard, fell 78 cents to $77.68 a barrel.

In currency trading, the U.S. dollar USDJPY, +0.44%

rose to 147.90 Japanese yen from 147.09 yen. The euro EURUSD, -0.10%

cost $1.0868, down from $1.0880.