Fed fund futures traders boosted the likelihood of no further rate hikes by the Federal Reserve in September, November or December on Thursday, a day after a mixed consumer price index report for August was released. After factoring in a 97% probability that the Fed will leave rates unchanged at between 5.25%-5.5%, traders now see a 63.7% likelihood of no action in November and 59.9% chance of the same for December, according to the CME FedWatch Tool. That’s up from 57.4% and 53.8% respectively on Wednesday, despite Thursday’s better-than-expected producer price index and retail sales data for August. Treasury yields swung between advances and declines Thursday morning, with the policy-sensitive 2-year rate hovering at just under 5%.

The Dow posted a back-to-back loss on Wednesday after a gauge of consumer inflation for August rose on the back of higher energy costs, while the S&P 500 and Nasdaq Composite ended with modest gains. The Dow Jones Industrial Average DJIA, -0.20%

shed about 70 points, or 0.2%, ending near 34,565, according to preliminary FactSet data. That marked its second day in a row of declines. The S&P 500 index SPX, +0.12%

added 0.1% and the Nasdaq Composite Index COMP, +0.29%

finished at a 0.3% gain. Both the Dow and S&P 500 struggled for direction earlier Wednesday, with both indexes flipping between small gains and loss as investors considered whether the Federal Reserve will be promoted to increase its policy rate any further this year to tamp down inflation further. Its benchmark rate was increased to a 22-year high in July. The consumer price-index for August showed the yearly rate of inflation climbed to 3.7% from 3.2% in July, and up from a 27-month low of 3% in June.

Inflation is likely to fall below the Federal Reserve’s 2% annual target by late next year, according to David Kelly, chief global strategist at JP Morgan Asset Management.

Consumer prices rose again in August to reach a 3.7% yearly rate, based on Wednesday’s release of the monthly consumer-price index. That marked its biggest jump in 14 months and a higher reading than the recent 3% low set in June (see chart) as the toll of the Fed’s rate hikes kicked in.

U.S. consumer prices rose in August, after touching a recent low of 3% yearly in June, as energy prices shot up.

AllianceBernstein

The catalyst for increased price pressures in August was a roughly 30% surge in energy prices CL00, +1.32%

this quarter, according to Eric Winograd, director of developed market economic research at AllianceBernstein.

West Texas Intermediate Crude, the U.S. benchmark, settled at $88.52 a barrel on Wednesday, as traders focused on supply concerns following decisions by Saudi Arabia and Russia to cut crude supplies through year-end. WTI was trading at a low for the year below $65 a barrel in May.

“I don’t think that today’s upside surprise is sufficient to trigger a rate hike next week and I continue to expect the Fed to stay on hold,” Winograd said, in emailed commentary. “But with inflation sticky and growth resilient, the committee is likely to maintain a clear tightening bias—the dot plot may even continue to reflect expectations of an additional hike later this year.”

Higher gasoline prices, however, also could act as a counterweight to inflation, according to JP Morgan’s Kelly. “Indeed, to the extent that higher gasoline prices cool other consumer spending, the recent energy price surge could contribute to slower growth and lower inflation entering 2024,” Kelly wrote in a Wednesday client note.

“We still believe that, barring some further shock, year-over-year headline consumption deflator inflation will be below the Fed’s 2% target by the fourth quarter of 2024.”

Kelly isn’t expecting the Fed to raise rates again in this cycle.

U.S. stocks ended mixed Wednesday following the CPI update, with the Dow Jones Industrial Average DJIA

down 0.2%, the S&P 500 index SPX

up 0.1% and the Nasdaq Composite Index COMP

up 0.3%, according to FactSet.

But with oil prices well off their lows for 2023, Winograd said further progress on cooling headline inflation is unlikely this year, even though he expects core inflation to gradually decelerate, a process that will “keep the Fed on high alert.”

Investors were evaluating a less-than-straightforward take on U.S. inflation Wednesday, with August’s consumer price index coming in close to or in line with expectations while providing reasons for the Federal Reserve to hike again by year-end.

COMP

were higher, though wavering, in New York afternoon trading as traders weighed the chances of another rate hike in November. Three-month through 1-year T-bill rates were up slightly, though 2- through 30-year Treasury yields slipped. And the ICE U.S. Dollar Index DXY,

which moves according to the market’s expectations for U.S. rates relative to the rest of the world, swung between gains and losses.

Rising gas prices in August had Wall Street anticipating higher headline inflation figures of 0.6% for last month and either 3.6% or 3.7% year-on-year ahead of Wednesday’s session, and on that score August’s CPI report met expectations. The as-expected headline readings appeared to offer some comfort to many investors, even though the monthly gain was the biggest increase in 14 months and the annual rate jumped versus the prior two months.

Still, Ed Moya, a senior market analyst for the Americas at OANDA Corp. in New York, said “this was a complicated inflation report” and price gains are failing to ease by enough for the central bank to abandon its hawkish stance. Core readings which matter most to Fed policy makers came in a bit above expectations at 0.3% for last month, driven partly by a jump in airline fares, as the annual core rate dipped to 4.3% from 4.7% previously. According to Moya, “inflation will likely still be running well above the Fed’s 2% target for the rest of the year.”

“Today’s uptick in CPI could slightly increase the likelihood of a November interest rate hike and potentially delay the timing of any rate cuts until deeper into 2024,” said Joe Tuckey, head of FX analysis at London-based Argentex Group, a provider of currency risk-management and payment services.

As of Wednesday afternoon, however, August’s CPI wasn’t putting much of a dent in expectations for fed funds futures traders. They see a 97% likelihood of no rate hike next Wednesday, which would keep the fed funds rate at between 5.25%-5.5%, and a more-than-50% chance of the same in November and December, according to the CME Fed Tool. They also continued to price in the likelihood of no rate cuts through the early part of 2024.

While August’s CPI report failed to move the needle in stocks, the dollar, or fed funds futures, there was one corner of the financial market where the data did make more a difference: Traders of derivatives-like instruments known as fixings now foresee five more 3%-plus annual headline CPI readings starting in September, after adjusting their expectations to include January.

If those expectations play out, that would bring the total number of 3%-plus readings to six months, including August’s data, and produce a scenario that investors may not be entirely prepared for — the possibility that headline inflation doesn’t meaningfully budge from current levels soon.

Central bankers care more about less-volatile core readings, but pay attention to headline CPI figures because of their potential to affect household expectations.

“While these numbers do not change our, and the market’s, expectations that the Fed will hold the target fed funds rate unchanged at the September meeting, the slightly stronger number can influence the tone of the press conference and Summary of Economic Projections,” said Greg Wilensky, head of U.S. fixed income at Denver-based Janus Henderson Investors, which manages $322.1 billion in assets.

“We continue to expect some reduction in the number of participants projecting further hikes, but probably not enough to move the median projection of one more rate hike,” Wilensky said in an email. “That said, we believe that we have likely seen the last rate hike for this cycle, as the economic data that the Fed will see over the coming months will keep them on hold and allow the impact of 5.25% of prior hikes to slow the economy and inflation.”

Neuberger Berman, an asset manager with eight decades under its belt, is on the lookout for cracks in credit markets from the Federal Reserve’s rate-hiking campaign.

Erik Knutzen, chief investment officer of multi asset, worries that several factors could be a tipping point for the economy, from an economic slowdown in China to U.S. consumers finally becoming exhausted by higher rates.

Yet Knutzen expects the high-yield, or junk bond, market to serve as the “canary in the coal mine” for broader market volatility, acting as “perhaps the most visible threat, and therefore one we think could be priced in sooner than later.”

The Bloomberg U.S. High Yield Bond Index has returned 6.4% through the end of August, producing one of the year’s highest gains in fixed income, helped along by a “resilient U.S. economy coupled with still-available financial liquidity,” according to the Wells Fargo Investment Institute.

But Knutzen worries that as the high-yield maturity wall draws closer, “the first policy rate cuts get priced further and further out, raising the threat of expensive refinancings.”

Starting next year, some $700 billion of high-yield bonds are set to mature through the end of 2027, with a big slice of the refinancing need coming from companies with riskier credit ratings below the top BB ratings bracket.

The junk-bond maturity wall.

Bloomberg, Wells Fargo Investment Institute, Moody’s Investors Service

The two big U.S. exchange-traded funds linked to junk bonds are the SPDR Bloomberg High Yield Bond ETF JNK

and the iShares iBoxx $ High Yield Corporate Bond ETF HYG,

both up 1.8% and 1.5% on the year through Monday, respectively, while offering dividend yields of more than 5.8%, according to FactSet.

Of note, fixed-income strategists at the Wells Fargo Investment Institute also said they see risks emerging in junk bonds for companies rated B and below, particularly with spread in the sector trading less than 400 basis points above the risk-free Treasury rate since July. Spreads are the premium that investors are paid on bonds to help compensate for default risks.

Top corporate executives appear hopeful that the Federal Reserve will cut rates sooner than later. Fed Chairman Jerome Powell said in Jackson Hole, Wyo., in August that the central bank is prepared to keep its policy rate restrictive for a while to get inflation down to its 2% target.

To that end, Neuberger Berman, which has roughly $443 billion in managed assets, sees several sources of volatility lurking through year’s end, and has a “defensive inclination” in equity and credit, favoring high-quality companies with plenty of free cash flow, high cash balances and less expensive long-term debt.

U.S. stocks booked gains on Monday after a week of losses, with the S&P 500 index SPX

and Nasdaq Composite Index COMP

scoring their best daily percentage gains in about two weeks. The Dow Jones Industrial Average DJIA

advanced 0.3%.

Recent weakness in the U.S. stock market is likely to persist over the near-term, according to Wall Street’s most bullish strategist, who still thinks the S&P 500 is on a path to a record high this year.

John Stoltzfus, chief investment strategist at Oppenheimer Asset Management Inc., in late July projected the S&P 500 would rise above 4,900 by the end of 2023. That is the highest price target for the large-cap index among 20 Wall Street firms surveyed by MarketWatch in August.

It implies the S&P 500 would rise above its earlier closing record high of 4,796 reached on Jan. 3, 2022 by the end of the year. The path up, however, could get bumpy.

“Bullishness [in the stock market] is relatively high while the Fed remains shy of its inflation target,” said a team of Oppenheimer strategists led by Stoltzfus in a Sunday note. They also said, “we persist in suggesting that investors curb their enthusiasm [in the stock market] for a long rate pause or even a rate cut and instead right-size expectations.”

Expectations that the Federal Reserve is nearing an end to its current interest-rate hiking cycle, as well as optimism around artificial intelligence boosted the U.S. stock market in the first seven months of 2023. However, the rally came to a brief halt in August as investors worried the Fed could be forced to keep rates elevated as a batch of stronger-than-expected economic data and rising oil prices fueled concerns that still-sticky inflation would mean that borrowing costs will stay higher for longer.

Investors should not brush off those pressures, even through the Fed appears to be nearing the end to its current rate-hike cycle, Stoltzfus and his team said. “The stickiness evidenced in food, services, energy and other prices warrants the Fed remaining vigilant along with a potential for one more hike this year and perhaps another next year,” they said.

However, Stoltzfus doesn’t see current headwinds for stocks as something that would prevent the S&P 500 from achieving his team’s new peak target.

Stock-market investors expect this week’s August inflation report to offer more clarity on whether the central bank will continue to ratchet up its fight against inflation. The headline component of the consumer-price index is forecast to accelerate to 0.6% in August from July’s 0.2% gain, while the core measure that strips out volatile food and fuel costs is expected to rise a mild 0.2% from a month earlier, according to a survey of economists by The Wall Street Journal.

Meanwhile, a key Wall Street volatility index also pointed to “some choppiness” in the stock market in the near term to keep investors on their toes, said Stoltzfus. The CBOE Volatility Index VIX,

at a level of 13.82 on Monday, hovered around its 12-month low and traded about 30% below its one-year average level of 19.9, and 37% below its two-year average of 21.88 (see chart below).

Stoltzfus and his team suggest that investors use market weakness to seek out “babies that get thrown out with the bath water” in periods of volatility. They said the S&P 500 Energy Sector XX:SP500.10

looks increasingly attractive as policy makers in the U.S. and abroad strive to contain inflation and manage economic growth.

“We believe that prospects are looking better that the Fed’s success thus far in bringing down the rate of inflation could lead to a [rate] pause next year, thus lessening pressures on economic growth,” the strategists said. An improved economic growth, along with fiscal stimulus from investment in stateside infrastructure projects and stateside chip manufacturing efforts, could contribute to profitability in the energy sector into 2024, the team added.

The Energy Select Sector SPDR Fund XLE,

which is seen as a proxy of the energy sector of the S&P 500, has advanced 3.9% year to date versus a 8.5% increase in the price of the U.S. benchmark West Texas Intermediate crude oil CL00, +0.03%

Oil futures CLV23, +0.03% BRNX23, -0.03%

traded at their highest levels of the year on Monday morning, a week after Russia and Saudi Arabia caught markets off guard with their output cut extension announcements, but they settled modestly lower on Monday afternoon.

Stoltzfus in late July projected the S&P 500 SPX

would rise above its record high by the end of 2023, lifting his year-end price target for the large-cap index to 4,900 from an earlier 4,400 projection from December. It implies a 9.2% advance from where the S&P 500 settled on Monday, at around 4,487.

U.S. stocks finished higher on Monday, boosted by technology shares as Nasdaq Composite COMP

advanced 1.1%. The S&P 500 was up 0.7% and the Dow Jones Industrial Average DJIA

ended 0.3% higher, according to FactSet data.

August was a hot month and it wasn’t just about the weather. Financial markets are now bracing for what’s likely to be a rebound in headline U.S. inflation next week, fueled by higher energy prices.

Barclays BARC, +0.18%,

BofA Securities BAC, +0.62%,

and TD Securities expect August’s consumer price index to reflect a 0.6% monthly rise, up from the 0.2% monthly readings seen in July and in June. In addition, they put the annual CPI inflation rate at 3.6% or 3.7% for last month, which compares with the 3.2% and 3% figures reported respectively for the prior two months.

While Federal Reserve policy makers and analysts are loath to read too much into one report, August’s CPI has the potential to disrupt expectations that getting back to the central bank’s 2% target will be easy. Inflation has instead been nudging back up since June, with the likely rebound in August being regarded as primarily driven by the energy sector. What now remains to be seen is how much longer energy prices will remain elevated and whether they’ll begin to feed into narrower measures of inflation that matter most to the Fed.

“We’re going to see a spike in gas prices and other commodity prices driven by supply cuts, which means headline CPI goes back up,” said Alex Pelle, a U.S. economist for Mizuho Securities in New York. Via phone on Friday, Pelle said that prospects for a hotter August CPI report have already been factored in by financial markets, with all three major U.S. stock indexes heading for weekly losses.

How investors react to next Wednesday’s data will likely come down to whether the rebound in headline figures is seen as “a one-off” or something that gets repeated, and “what that means for the bottoming off of inflation,” Pelle said. “The equity market is going to have some trouble in the fourth quarter after a pretty impressive first half. Earnings expectations are still pretty high, but the macro-driven backdrop is challenging.”

Rising energy prices in August have already spilled into the month of September, with gasoline reaching the highest seasonal level in more than a decade this week. Voluntary production cuts by Saudi Arabia and Russia are a major contributing factor curtailing the supply of crude oil into year-end, and Goldman Sachs has warned that oil could climb above $100 a barrel.

In financial markets, there’s one group of traders which is telegraphing that the final mile of the road toward 2% inflation won’t be smooth.

Traders of derivatives-like instruments known as fixings anticipate that the next five CPI reports, including August’s, will produce annual headline inflation rates above 3%. Though policy makers care more about core readings that strip out volatile food and energy prices, they’re aware of how much headline figures can impact the public’s expectations.

Source: Bloomberg. The maturity column reflects the month and year of upcoming CPI reports. The forwards column reflects the year-ago period from which the year-over-year rate is based.

At BofA Securities, U.S. economist Stephen Juneau said August’s CPI won’t necessarily change his firm’s view that inflation is likely to move lower next year and fall back to the Fed’s target without the need for a recession. BofA Securities expects just one more Fed rate hike in November and will maintain that view if August’s CPI report comes in as he expects, Juneau said via phone.

After stripping out volatile food and energy items, BofA Securities, along with Barclays and TD Securities, expects August’s core CPI readings to come in at 0.2% month-over-month — matching June and July’s levels — and to fall to 4.3% on an annual basis.

Based on core measures, August’s report wouldn’t “change the narrative all that much: Everything points to a moderation in price growth,” Pelle said. “There’s a reason why food and energy are typically excluded,” and “we don’t want to put too much stock into one month.”

As of Friday afternoon, all three major U.S. stock indexes were headed higher, with the S&P 500 attempting to snap a three-day losing streak. Dow industrials DJIA,

the S&P 500 SPX

and Nasdaq Composite COMP

were respectively on track for weekly losses of 0.7%, 1.2%, and 1.7%. They’re still up for the year by more than 4%, 16% and 31%.

Meanwhile, Treasury yields turned were little changed on Friday as fed funds futures traders priced in a 93% chance of no action by the Fed at its next policy meeting in less than two weeks, and a more-than-50% likelihood of the same for November and December — which would leave the Fed’s main policy rate target between 5.25%-5.5%.

“There is a risk that investors are too complacent about the inflation report,” said Brian Jacobsen, chief economist at Annex Wealth Management in Elm Grove, Wis. “We might not get to 2% inflation as quickly as many hope.”

The U.S. economy could expand at about a 2.2% annual rate in the current quarter, according to a revamped real-time estimate from the New York Federal Reserve released Friday.

According to the weekly New York Fed’s Staff Nowcast, the economy has been on an upward trend since late July.

The regional Fed bank had discontinued the real-time estimate during the pandemic. The New York Fed said the series will now be available weekly.

The New York Fed’s estimate is much lower than the Atlanta Fed’s GDPNow model, which shows growth could expand at a 5.6% annual rate in the current quarter.

Economists say the strength of the economy will be critical going forward in deciding whether the Federal Reserve needs to continue to raise its policy interest rate to cool inflation.

The Fed has been expecting the economy to slow in the second half of the year. Fed officials forecast only 1% growth for 2023. In the first six months of the year, U.S. gross domestic product is averaging about a 2% growth rate.

If the economy reaccelerates, it is likely that inflation will also move higher. Fed officials had been hoping that slower economic growth would continue push down inflation.

Faster growth means “you are probably going to get some inflation numbers that aren’t going to be as good as people were anticipating,” said James Bullard, the former president of St. Louis Fed president and now dean of Purdue’s business school.

“There is some risk that the Fed will have to go a little bit higher” even than the one more interest rate hike that the central bankers have penciled in this year, he said, in a recent CNBC interview.

The first official government estimate of third-quarter growth won’t be released until Oct. 26.

The picture of the health of the economy painted by U.S. GDP statistics can change quickly.

The growth estimates for the first half of the year could be revised at the end of September when the Commerce Department releases benchmark updates to GDP data.

The sharp revisions are one of the reasons why the Fed typically pays more attention to the unemployment rate and the inflation data.

The numbers: Total U.S. household net worth rose $5.5 trillion to a record $154.28 trillion in the second quarter, the Federal Reserve said Friday. This is the third straight quarterly increase.

Key details: The gain was boosted by a $2.6 trillion gain in stocks. The value of real estate holdings rose $2.5 trillion in the three months.

Household debt rose at a 2.7% annual rate in the second quarter. Mortgage debt grew at a 2.8% annual rate.

Big picture: The health of the consumer has been a big factor in the surprising strength of the U.S. economy this year. Talk of a recession has vanished and the economy seems to be strengthening as the year progresses.

New York Fed President John Williams on Thursday sounded content with the current level of interest rates, but said he will be watching data closely to make sure the level of rates is high enough to keep inflation moving down.

“We’ve done a lot,” Williams said during a discussion at a conference sponsored by Bloomberg News.

Central bankers like to focus on core inflation readings, which strip out food and energy prices, but that doesn’t mean that they, or investors, will be able to ignore a renewed surge in crude-oil prices.

In a Thursday note, DataTrek Research observed that the correlation between energy prices and the core reading of the consumer-price index has returned to levels seen in the 1970s and 1980s. It stands at 0.62 since 2020, compared with an average of 0.68 in those prior decades, and well above its long-run average of 0.31. A reading of 1.0 would mean the measures were moving in perfect lockstep. (See table below.)

DataTrek Research

Core measures of inflation typically strip out volatile items like food and energy. While that often leads to eye-rolling by commentators who note that food and energy make up a big chunk of what consumers spend money on, the logic behind the move holds that such items are less responsive to monetary policy.

Policy makers put more emphasis on the core reading for a better read on what they can influence. The core personal-consumption expenditures, or PCE, index, for example, is often described as the Federal Reserve’s favored inflation indicator.

But that doesn’t mean rising energy or food prices can be ignored. Energy, after all, is an input, and can have an influence on overall prices.

“Recent data says energy prices hold more sway on core inflation than any time since the 1970s/1980s, so rising oil prices are a legitimate concern for both the Fed and capital markets. Food inflation fits the same bill,” said DataTrek co-founder Nicholas Colas in the note.

Oil prices have been on a tear this summer, with the rally accelerating after Saudi Arabia announced earlier this week it would extend a production cut of 1 million barrels a day through the end of the year, with Russia also pledging to extend a supply cut.

West Texas Intermediate crude CL00, +0.48%,

the U.S. benchmark, extended a winning streak to nine days on Wednesday, while Brent crude BRN00, +0.60%,

the global benchmark, rose for a seventh straight day. Both grades ended at 2023 highs Wednesday before pulling back modestly in the Thursday session.

The surge in crude threatens to further drive up fuel prices, including gasoline and diesel.

And rising oil prices this week got a chunk of the blame from investors and analysts for a pickup in Treasury yields as market participants began to pencil in a longer stretch of higher interest rates — or weighed the possibility the Fed may need to deliver more monetary tightening. That’s also contributed to a rise in the U.S. dollar, with the ICE U.S. Dollar Index DXY,

a measure of the currency against a basket of six major rivals, hitting a six-month high.

U.S. stocks have weakened in the face of rising yields, with technology and growth shares, which are particularly rate-sensitive, leading the way lower. The Nasdaq Composite COMP

was on track for a 2% decline so far this holiday-shortened week, while the S&P 500 SPX

has pulled back 1.4% and the Dow Jones Industrial Average DJIA

has lost 1%.

“With oil prices rising again, we got to wondering about the spillover effects of this move on inflation. Will pricier crude derail recent disinflationary trends?” Colas wrote.

Another big corporate borrowing blitz to kick off September has gotten under way, but this one isn’t looking like the rest.

Instead, the flurry of new bond issues shows how the Federal Reserve’s higher interest rate environment has begun to seep in a year later, by making major companies far more hesitant to tap credit for longer stretches.

The roughly $25 trillion Treasury market first began flashing this telltale sign that a U.S. recession likely lurks on the horizon almost a year ago, according to Bespoke Investment Group.

It was late October of 2022 when the 3-month Treasury yield BX:TMUBMUSD03M first eclipsed the 10-year Treasury yield BX:TMUBMUSD10Y, resulting in an “inversion” of a key part of the yield curve that’s been a reliable predictor of past recessions.

The Federal Reserve’s inflation fight has been particularly brutal for anyone not already a U.S. homeowner before interest rates and mortgage rates rose to 15-year highs.

With mortgage rates around 7.2% to kick off the post–Labor Day period, the difference between the rates on a new 30-year home loan and on all outstanding U.S. mortgage debt (see chart) has not been so wide since the 1980s.

It’s the 1980s again in the U.S. housing market.

Glenmede, FactSet

“Generally, climbing interest rates curb demand and cause housing prices to fall,” Glenmede’s investment strategy team wrote, in a Tuesday client note, but not this time.

Instead, U.S. homes remain in critically low supply after more than a decade of underbuilding, and with most homeowners who already refinanced at low pre-pandemic rates being “reluctant to leave their homes,” wrote Jason Pride, chief of investment strategy and research, and his Glenmede team.

“Until the supply gap is filled by new construction, home prices and building activity are unlikely to decline as meaningfully as they normally would given the headwind from rising rates,” the Glenmede team said.

The Glenmede team, however, does expect more pressure on consumers in the coming months, particularly as student-loan payments resume in October and if the Fed keeps interest rates high for a while, as increasingly expected. The benchmark 10-year Treasury yield BX:TMUBMUSD10Y,

which underpins the U.S. economy, was back on the climb at 4.26% Tuesday.

Meanwhile, shares of home-vacation rental platform Airbnb Inc. ABNB, +7.23%

rose 7.2% on Tuesday, after the Labor Day weekend, and 66.4% higher on the year so far, according to FactSet.

Shares of Invitation Homes Inc. INVH, -0.91%,

which grew out of the last decade’s home-loan foreclosure crisis to become a single-family-rental giant, were up 14.3% on the year, according to FactSet.

Dallas Tanner, CEO of Invitation Homes, said he expected “the rising costs and the burden of homeownership” to continue to benefit his company, in a July earnings call. The company recently bought a portfolio of about 1,900 homes and has been snapping up newly constructed homes. Companies can borrow on Wall Street at much lower rates than individuals.

Stocks closed lower Tuesday, with the Dow Jones Industrial Average DJIA

off 0.5%, and the S&P 500 index SPX

0.4% lower and the Nasdaq Composite Index COMP

down 0.1%, according to FactSet.

U.S. stocks closed lower Tuesday after the long Labor Day weekend, as bond yields and oil prices climbed. The Dow Jones Industrial Average DJIA shed about 195 points, or 0.6%, ending near 34,642, according to preliminary FactSet data. The S&P 500 index SPX dropped about 0.4% and the Nasdaq Composite Index COMP fell 0.1%. Investors returned from the long weekend in a less bullish mood on weaker economic data from China and Europe, but also with more clouds on the horizon in oil markets. Oil prices CL00 closed at the highest level since November on Tuesday, after Saudi Arabia and Russia opted to extend oil supply production…

Orders for U.S. manufactured goods fell a sharp 2.1% in July, the Commerce Department said Tuesday. This is the first decline after four straight monthly gains.

Economists surveyed by the Wall Street Journal were expecting a 2.3% fall in July.

Excluding transportation, orders rose 0.8% in July after a 0.3% gain in the prior month.

Economists said that higher interest rates are putting pressure on business equipment spending.

Durable-goods orders fell 5.2 % in July, unrevised from the data that was released on Aug. 24. Non-durable goods orders rose 1.1%.

Orders for nondefense capital goods, excluding aircraft, rose 0.1% in July, also unrevised from prior estimate.

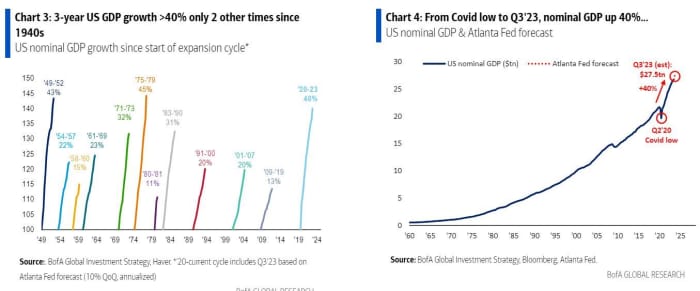

The 10-year Treasury bond is on track for a third year of losses in 2023, something that hasn’t happened in 250 years of U.S. history.

In short, it has never happened, say strategists at Bank of America.

The return for investors putting money in that bond BX:TMUBMUSD10Y

stands at negative 0.3% so far in 2023, after a 17% slump in 2022 and a 3.9% drop in 2021, the bank’s strategists, led by Michael Hartnett, pointed out in a note on Friday.

Here’s a visual on that:

That reflects a “staggering 40% jump in U.S. nominal GDP growth” — factoring in growth and inflation — “since the COVID lows of 2020,” they said, providing this chart:

Bond returns have suffered this year as the Federal Reserve has continued its interest-rate-hiking campaign aimed at getting inflation under control. The “big picture in the 2020s vs. the 2010s is lower stock and bond returns, which we would expect to continue given political, geopolitical, social [and] economic trends,” said Hartnett and the team.

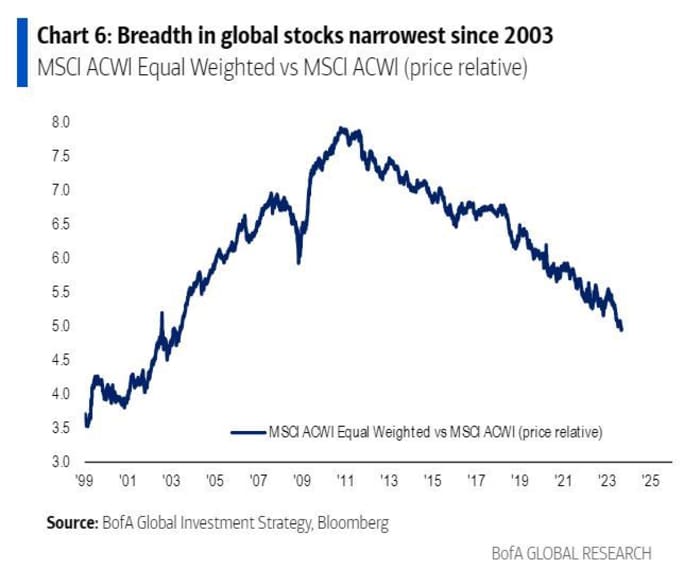

SPX,

but the bounce since COVID pandemic restrictions began to be lifted has been very concentrated in U.S. stocks, especially the technology sector, with breadth in global markets “breathtakingly bad,” the analysts said. Breadth refers to the number of stocks actively participating in a rally.

Breadth is the worst since 2003 for the MSCI ACWI, which captures large- and midcap-stock representation across 23 developed markets and 24 emerging ones.

As for the latest weekly flows into funds, Bank of America reported that $10.3 billion went to stocks, $6.5 billion to cash and $1.7 billion to bonds, with $300 million draining from gold GC00, -0.06%.

The yield on the 10-year Treasury was holding steady on Friday at 4.102% after data showed the U.S. economy generated 187,000 jobs in August, but the unemployment rate rose to 3.8% from 3.5%, and job gains were revised lower for July and June.

The 10-year Treasury bond is on track for a third year of losses in 2023, something that hasn’t happened in 250 years of U.S. history.

In short, it has never happened, say strategists at Bank of America.

The return for investors putting money in that bond BX:TMUBMUSD10Y

stands at negative 0.3% so far in 2023, after a 17% slump in 2022 and a 3.9% drop in 2021, the bank’s strategists, led by Michael Hartnett, pointed out in a note on Friday.

Here’s a visual on that:

That reflects a “staggering 40% jump in U.S. nominal GDP growth” — factoring in growth and inflation — “since the COVID lows of 2020,” they said, providing this chart:

Bond returns have suffered this year as the Federal Reserve has continued its interest-rate-hiking campaign aimed at getting inflation under control. The “big picture in the 2020s vs. the 2010s is lower stock and bond returns, which we would expect to continue given political, geopolitical, social [and] economic trends,” said Hartnett and the team.

SPX,

but the bounce since COVID pandemic restrictions began to be lifted has been very concentrated in U.S. stocks, especially the technology sector, with breadth in global markets “breathtakingly bad,” the analysts said. Breadth refers to the number of stocks actively participating in a rally.

Breadth is the worst since 2003 for the MSCI ACWI, which captures large- and midcap-stock representation across 23 developed markets and 24 emerging ones.

As for the latest weekly flows into funds, Bank of America reported that $10.3 billion went to stocks, $6.5 billion to cash and $1.7 billion to bonds, with $300 million draining from gold GC00, +0.02%.

The yield on the 10-year Treasury was holding steady on Friday at 4.102% after data showed the U.S. economy generated 187,000 jobs in August, but the unemployment rate rose to 3.8% from 3.5%, and job gains were revised lower for July and June.

The Federal Reserve can probably end its inflation fight now that the U.S. labor market is cooling after generating a historic 26 million jobs in roughly the past three years, according to BlackRock’s Rick Rieder.

“In fact, 26 million jobs is like adding an economy the size of Australia or Taiwan (including every man, woman, and child),” said Rieder, BlackRock’s chief investment officer in global fixed income, in emailed commentary following Friday’s monthly jobs report for August.

The August nonfarm-payrolls report showed the U.S. adding 187,000 jobs, slightly more than had been forecast, but also pointing to an uptick in the unemployment rate to 3.8% from 3.5%.

“Remarkably, 22 million people were hired between May 2020 and April 2022, and 11 million were added to the workforce from June 2021 to May 2023, as the economy has opened up massive amounts of roles for fulfillment,” said Rieder.

He expects wage pressures to ease, he said, and thinks the “economy may now have fulfilled many of its needs,” which should make the Fed feel more confident in “the permanence of lower levels of inflation,” so that it can slow or stop its interest-rate rises by year-end.

Hiring in the U.S. has slowed, except in education and in healthcare services, when looking at private payrolls based on a three-month moving average.

Payrolls are slowing in many sectors, expect education and healthcare

Rieder of BlackRock, one of the world’s largest asset managers with $2.7 trillion in assets under management, said he thinks a Fed pause or outright end to rate hikes could calm markets, even if the Fed, as BlackRock expects, keeps rates high for a time.

U.S. closed mostly higher Friday ahead of the Labor Day holiday weekend, with the Dow Jones Industrial Average DJIA

up 0.3%, the S&P 500 index SPX

up 0.2% and the Nasdaq Composite Index COMP

0.02% lower, according to FactSet.

The 10-year Treasury yield BX:TMUBMUSD10Y

was at 4.173%, after hitting its highest level since 2007 in late August, adding to volatility that has wiped out earlier yearly gains in the roughly $25 trillion Treasury market.

The U.S. Labor Day holiday will mark another milestone in the marathon to bring workers back to the office, but it won’t be a quick fix for landlords, according to Thomas LaSalvia, head of commercial real estate economics at Moody’s Analytics.

“A lot of companies are saying that after Labor Day, ‘We expect more out of you,” LaSalvia said, referring to days in the office. Still, office attendance, he argues, likely only stages a fuller comeback if a job or promotion is on the line.

That could prove difficult, with Friday’s U.S. jobs report for August expected to show U.S. unemployment at a scant 3.5%, near the lowest levels since the late 1960s, even if hiring has been slowing. The labor market, so far, appears unfazed by the Federal Reserve’s benchmark rate reaching a 22-year high.

It has been a different story for landlords facing a roughly 19% vacancy rate nationally and piles of debt coming due, especially for owners of older Class B and C office buildings with a bleak outlook or properties in cities with wobbling business centers.

As with shopping malls, LaSalvia said it’s largely a problem of oversupply, with many office properties at risk of becoming obsolete as tenants flock to better buildings and locations staging a rebirth. The trend can be traced in leasing data since 2021, with Class A properties in central business districts (blue line) showing a big advantage over less desirable buildings in the heart of cities (orange line).

Return to office isn’t going to save the entire office property market

Moody’s Analytics

“Little by little, we are finding the office isn’t dead,” LaSalvia said, but he also sees more promise in neighborhoods with a new purpose, those catering to hybrid work and communities that bring people together.

Another way to look at the trend is through rents. Manhattan’s Penn Station submarket, with its estimated $13 billion overhaul and neighboring Hudson Yards development, has seen asking rents jump 32% to $74.87 a square foot in the second quarter since the fourth quarter of 2019, according to Moody’s Analytics. That compares with a 2% bump in asking rents in downtown New York City to $61.39 a square foot for the same period.

The push for a return to the office also doesn’t mean a repeat of prepandemic ways. Goldman Sachs analysts estimate that part-time remote work in the U.S. has stabilized around 20%-25%, in a late August report, but that’s still up from 2.6% before the 2020 lockdowns.

Furthermore, the persistence of remote work will likely add another 171 million square feet of vacant U.S. office space through 2029, a period that also will see tenants’ long-term leases expire and many companies opting for less space. The additional vacancies would roughly translate to 57% of Los Angeles roughly 300 million square feet of office space sitting empty.

“The fundamental reason why we had offices in the first place have not completely disintegrated,” LaSalvia said. “But for some of those Class B and C offices, the writing was on the wall before the pandemic.”

U.S. stocks were mixed Thursday, but headed for losses in a tough August for stocks, with the S&P 500 index SPX

off about 1.5% for the month, the Dow Jones Industrial Average DJIA

2.1% lower and the Nasdaq Composite COMP

down 2% in August, according to FactSet.