The numbers: Total U.S. household net worth rose $5.5 trillion to a record $154.28 trillion in the second quarter, the Federal Reserve said Friday. This is the third straight quarterly increase.

Key details: The gain was boosted by a $2.6 trillion gain in stocks. The value of real estate holdings rose $2.5 trillion in the three months.

Household debt rose at a 2.7% annual rate in the second quarter. Mortgage debt grew at a 2.8% annual rate.

Big picture: The health of the consumer has been a big factor in the surprising strength of the U.S. economy this year. Talk of a recession has vanished and the economy seems to be strengthening as the year progresses.

New York Fed President John Williams on Thursday sounded content with the current level of interest rates, but said he will be watching data closely to make sure the level of rates is high enough to keep inflation moving down.

“We’ve done a lot,” Williams said during a discussion at a conference sponsored by Bloomberg News.

Another big corporate borrowing blitz to kick off September has gotten under way, but this one isn’t looking like the rest.

Instead, the flurry of new bond issues shows how the Federal Reserve’s higher interest rate environment has begun to seep in a year later, by making major companies far more hesitant to tap credit for longer stretches.

The roughly $25 trillion Treasury market first began flashing this telltale sign that a U.S. recession likely lurks on the horizon almost a year ago, according to Bespoke Investment Group.

It was late October of 2022 when the 3-month Treasury yield BX:TMUBMUSD03M first eclipsed the 10-year Treasury yield BX:TMUBMUSD10Y, resulting in an “inversion” of a key part of the yield curve that’s been a reliable predictor of past recessions.

The Federal Reserve’s inflation fight has been particularly brutal for anyone not already a U.S. homeowner before interest rates and mortgage rates rose to 15-year highs.

With mortgage rates around 7.2% to kick off the post–Labor Day period, the difference between the rates on a new 30-year home loan and on all outstanding U.S. mortgage debt (see chart) has not been so wide since the 1980s.

It’s the 1980s again in the U.S. housing market.

Glenmede, FactSet

“Generally, climbing interest rates curb demand and cause housing prices to fall,” Glenmede’s investment strategy team wrote, in a Tuesday client note, but not this time.

Instead, U.S. homes remain in critically low supply after more than a decade of underbuilding, and with most homeowners who already refinanced at low pre-pandemic rates being “reluctant to leave their homes,” wrote Jason Pride, chief of investment strategy and research, and his Glenmede team.

“Until the supply gap is filled by new construction, home prices and building activity are unlikely to decline as meaningfully as they normally would given the headwind from rising rates,” the Glenmede team said.

The Glenmede team, however, does expect more pressure on consumers in the coming months, particularly as student-loan payments resume in October and if the Fed keeps interest rates high for a while, as increasingly expected. The benchmark 10-year Treasury yield BX:TMUBMUSD10Y,

which underpins the U.S. economy, was back on the climb at 4.26% Tuesday.

Meanwhile, shares of home-vacation rental platform Airbnb Inc. ABNB, +7.23%

rose 7.2% on Tuesday, after the Labor Day weekend, and 66.4% higher on the year so far, according to FactSet.

Shares of Invitation Homes Inc. INVH, -0.91%,

which grew out of the last decade’s home-loan foreclosure crisis to become a single-family-rental giant, were up 14.3% on the year, according to FactSet.

Dallas Tanner, CEO of Invitation Homes, said he expected “the rising costs and the burden of homeownership” to continue to benefit his company, in a July earnings call. The company recently bought a portfolio of about 1,900 homes and has been snapping up newly constructed homes. Companies can borrow on Wall Street at much lower rates than individuals.

Stocks closed lower Tuesday, with the Dow Jones Industrial Average DJIA

off 0.5%, and the S&P 500 index SPX

0.4% lower and the Nasdaq Composite Index COMP

down 0.1%, according to FactSet.

Shares of Chinese property developers rose sharply Monday, as more major Chinese cities said over the weekend that they would ease mortgage policies in a bid to shore up the real-estate sector.

The Hang Seng Mainland Properties Index rose 8.2%. Hong Kong-listed Longfor Group Holdings 960, +8.11%

climbed 10% and Seazen Group 1030, +18.30%

jumped 17%. Shanghai-Listed Gemdale 600383, +1.63%

added 4.1% and China Vanke 000002, -0.07%

gained 1.4%.

Major Chinese cities across the country, including Beijing and Shanghai, lowered mortgage requirements for some home buyers late last week, lowering the bar for home purchases.

“This nationwide policy measure marks a significant step in stimulating the property sector, as top policymakers become increasingly worried about the collapse of the property sector, the downward spiral, and a rising number of credit risk events among major developers and financial institutions since mid-August,” Nomura analysts said in a note.

Separately, news reports over the weekend saying that property giant Country Garden Holdings 2007, +14.61%

received creditor approval to extend a bond also lifted the mood and supported the company’s shares. Country Garden shares were last up 9.0% at 0.97 Hong Kong dollars (12 U.S. cents).

Year to date, Country Garden’s stock has slumped 64% after the company posted its worst loss since going public 16 years ago and missed $22.5 million in interest payments on its dollar bonds in August.

Despite Chinese authorities’ supportive policies and Country Garden’s bond extension, some analysts warned that the extension could just be a near-term reprieve.

“With the lack of an eventual resolution [for Country Garden],” headwinds linger for the Chinese property sector, IG Asia analysts said in a note.

“Persistent earnings weakness will no doubt drive the sector’s leverage higher,” said S&P Global Ratings credit ratings analyst Oscar Chung.

S&P believes industry leaders and real-estate companies with a diverse business mix such as rental and service incomes can better withstand declining development margins.

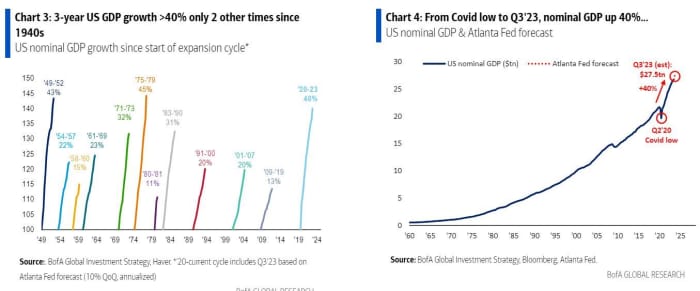

The 10-year Treasury bond is on track for a third year of losses in 2023, something that hasn’t happened in 250 years of U.S. history.

In short, it has never happened, say strategists at Bank of America.

The return for investors putting money in that bond BX:TMUBMUSD10Y

stands at negative 0.3% so far in 2023, after a 17% slump in 2022 and a 3.9% drop in 2021, the bank’s strategists, led by Michael Hartnett, pointed out in a note on Friday.

Here’s a visual on that:

That reflects a “staggering 40% jump in U.S. nominal GDP growth” — factoring in growth and inflation — “since the COVID lows of 2020,” they said, providing this chart:

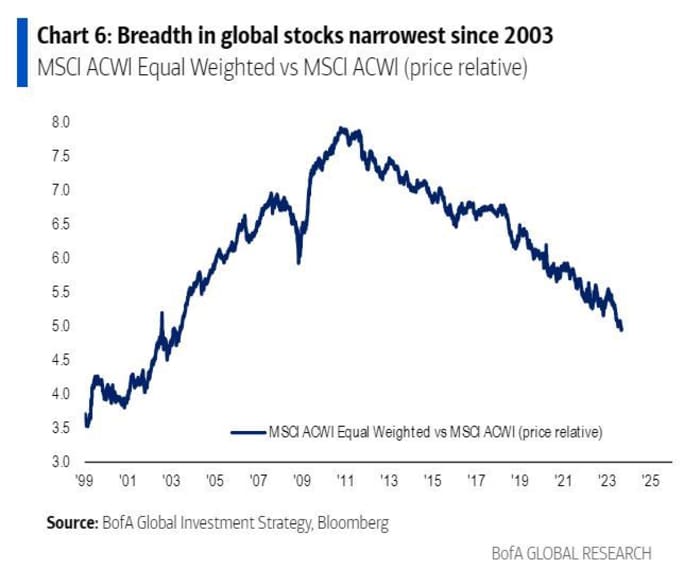

Bond returns have suffered this year as the Federal Reserve has continued its interest-rate-hiking campaign aimed at getting inflation under control. The “big picture in the 2020s vs. the 2010s is lower stock and bond returns, which we would expect to continue given political, geopolitical, social [and] economic trends,” said Hartnett and the team.

SPX,

but the bounce since COVID pandemic restrictions began to be lifted has been very concentrated in U.S. stocks, especially the technology sector, with breadth in global markets “breathtakingly bad,” the analysts said. Breadth refers to the number of stocks actively participating in a rally.

Breadth is the worst since 2003 for the MSCI ACWI, which captures large- and midcap-stock representation across 23 developed markets and 24 emerging ones.

As for the latest weekly flows into funds, Bank of America reported that $10.3 billion went to stocks, $6.5 billion to cash and $1.7 billion to bonds, with $300 million draining from gold GC00, -0.06%.

The yield on the 10-year Treasury was holding steady on Friday at 4.102% after data showed the U.S. economy generated 187,000 jobs in August, but the unemployment rate rose to 3.8% from 3.5%, and job gains were revised lower for July and June.

The 10-year Treasury bond is on track for a third year of losses in 2023, something that hasn’t happened in 250 years of U.S. history.

In short, it has never happened, say strategists at Bank of America.

The return for investors putting money in that bond BX:TMUBMUSD10Y

stands at negative 0.3% so far in 2023, after a 17% slump in 2022 and a 3.9% drop in 2021, the bank’s strategists, led by Michael Hartnett, pointed out in a note on Friday.

Here’s a visual on that:

That reflects a “staggering 40% jump in U.S. nominal GDP growth” — factoring in growth and inflation — “since the COVID lows of 2020,” they said, providing this chart:

Bond returns have suffered this year as the Federal Reserve has continued its interest-rate-hiking campaign aimed at getting inflation under control. The “big picture in the 2020s vs. the 2010s is lower stock and bond returns, which we would expect to continue given political, geopolitical, social [and] economic trends,” said Hartnett and the team.

SPX,

but the bounce since COVID pandemic restrictions began to be lifted has been very concentrated in U.S. stocks, especially the technology sector, with breadth in global markets “breathtakingly bad,” the analysts said. Breadth refers to the number of stocks actively participating in a rally.

Breadth is the worst since 2003 for the MSCI ACWI, which captures large- and midcap-stock representation across 23 developed markets and 24 emerging ones.

As for the latest weekly flows into funds, Bank of America reported that $10.3 billion went to stocks, $6.5 billion to cash and $1.7 billion to bonds, with $300 million draining from gold GC00, +0.02%.

The yield on the 10-year Treasury was holding steady on Friday at 4.102% after data showed the U.S. economy generated 187,000 jobs in August, but the unemployment rate rose to 3.8% from 3.5%, and job gains were revised lower for July and June.

Shares of investment giant Blackstone Inc. and vacation-home rental platform Airbnb Inc. rallied after hours on Friday after both won the nod to join the S&P 500 index SPX

later this month.

The announcement, from S&P Dow Jones Indices, said that the change would take hold before the start of trading on Monday, Sept. 18. The move, among others announced Friday, will “ensure each index is more representative of its market-capitalization range,” according to a release.

Airbnb ABNB, +0.87%

currently has a market value of $83.98 billion, and its shares are up 64.7% so far this year. Blackstone BX, -1.77%,

currently worth $129.29 billion, has seen its stock rise 43.6% year-to-date.

Shares of Airbnb and Blackstone were up 5.7% and 4.8%, respectively, after hours on Friday.

Blackstone and Airbnb will replace Lincoln National Corp. LNC, +2.14%

and Newell Brands Inc. NWL, +1.23%

in the index, S&P Dow Jones Indices said on Friday. In the process, Lincoln and Newell will join the S&P SmallCap 600.

“We’ve established an unparalleled global platform of leading business lines, offering over 70 distinct investment strategies,” Chief Executive Stephen Schwarzman told analysts. “We believe our clients view us as the gold standard in alternative asset management.”

Meanwhile, Airbnb last month said that travelers were seeking longer stays and bigger properties in pricier areas, as the rebound in travel endures despite a tidal wave of inflation last year. The company’s second-quarter results and third-quarter sales forecast topped Wall Street’s estimates.

Meanwhile, S&P 500 member Deere & Co. DE, +1.94%

will replace Walgreens Boots Alliance Inc. WBA, -7.43%

in the S&P 100, S&P Dow Jones Indices said on Friday. That change also takes hold on Sept. 18. S&P Dow Jones Indices said Walgreens “is no longer representative of the megacap market space” but will stay in the S&P 500.

Shares of Deere fell 0.2% after hours. Walgreens stock was up 0.4%.

The U.S. Labor Day holiday will mark another milestone in the marathon to bring workers back to the office, but it won’t be a quick fix for landlords, according to Thomas LaSalvia, head of commercial real estate economics at Moody’s Analytics.

“A lot of companies are saying that after Labor Day, ‘We expect more out of you,” LaSalvia said, referring to days in the office. Still, office attendance, he argues, likely only stages a fuller comeback if a job or promotion is on the line.

That could prove difficult, with Friday’s U.S. jobs report for August expected to show U.S. unemployment at a scant 3.5%, near the lowest levels since the late 1960s, even if hiring has been slowing. The labor market, so far, appears unfazed by the Federal Reserve’s benchmark rate reaching a 22-year high.

It has been a different story for landlords facing a roughly 19% vacancy rate nationally and piles of debt coming due, especially for owners of older Class B and C office buildings with a bleak outlook or properties in cities with wobbling business centers.

As with shopping malls, LaSalvia said it’s largely a problem of oversupply, with many office properties at risk of becoming obsolete as tenants flock to better buildings and locations staging a rebirth. The trend can be traced in leasing data since 2021, with Class A properties in central business districts (blue line) showing a big advantage over less desirable buildings in the heart of cities (orange line).

Return to office isn’t going to save the entire office property market

Moody’s Analytics

“Little by little, we are finding the office isn’t dead,” LaSalvia said, but he also sees more promise in neighborhoods with a new purpose, those catering to hybrid work and communities that bring people together.

Another way to look at the trend is through rents. Manhattan’s Penn Station submarket, with its estimated $13 billion overhaul and neighboring Hudson Yards development, has seen asking rents jump 32% to $74.87 a square foot in the second quarter since the fourth quarter of 2019, according to Moody’s Analytics. That compares with a 2% bump in asking rents in downtown New York City to $61.39 a square foot for the same period.

The push for a return to the office also doesn’t mean a repeat of prepandemic ways. Goldman Sachs analysts estimate that part-time remote work in the U.S. has stabilized around 20%-25%, in a late August report, but that’s still up from 2.6% before the 2020 lockdowns.

Furthermore, the persistence of remote work will likely add another 171 million square feet of vacant U.S. office space through 2029, a period that also will see tenants’ long-term leases expire and many companies opting for less space. The additional vacancies would roughly translate to 57% of Los Angeles roughly 300 million square feet of office space sitting empty.

“The fundamental reason why we had offices in the first place have not completely disintegrated,” LaSalvia said. “But for some of those Class B and C offices, the writing was on the wall before the pandemic.”

U.S. stocks were mixed Thursday, but headed for losses in a tough August for stocks, with the S&P 500 index SPX

off about 1.5% for the month, the Dow Jones Industrial Average DJIA

2.1% lower and the Nasdaq Composite COMP

down 2% in August, according to FactSet.

U.S. stocks scored back-to-back gains on Monday in an attempt to claw back ground in a rough August for equities. The Dow Jones Industrial Average DJIA, +0.62%

rose about 213 points, or 0.6%, ending near 34,560, according to preliminary data from FactSet. The S&P 500 index SPX, +0.63%

closed 0.6% higher and the Nasdaq Composite Index COMP, +0.84%

gained 0.8%. Investors kicked of the final week of August on an upbeat note, while largely focusing on Thursday’s inflation data and Friday’s monthly jobs report to help inform the Federal Reserve’s path on interest rates and its inflation fight. The 10-year Treasury yield TMUBMUSD10Y, 4.203%

eased back to about 4.20% late Monday after its sharp rise a week ago to its highest level since 2007. The Dow still was off about 2.8% so far in August, while the S&P 500 index was 3.4% lower and the Nasdaq was down 4.5%, according to FactSet.

Investors sitting on the sidelines in cash and in money-market funds might consider moving into longer-dated bonds sooner rather than later, according to Saira Malik, chief investment officer at Nuveen.

As look at historical returns shows the broader $55 trillion U.S. bond market typically outperforms short-term Treasurys at the end of past Federal Reserve rate hiking cycles since the 1990s.

The bond market produced an average 5.5% three-month rolling return following the last rate hike (see chart) in the past four Fed hiking cycles, while short-term Treasurys returned 2.1%.

This data includes the three-month rolling average performance of bonds in all Federal Reserve rate-hiking cycles since 1990 (1995, 2000, 2006 and 2018) based on the Bloomberg U.S. Aggregate Bond Index and the Bloomberg U.S. Treasury 1-3 Year Index

Bloomberg, Nuveen

Of note, the magnitude of the bond market’s outperformance faded by 12 months versus short-term positions, when looking at the Bloomberg U.S. Aggregate Bond Index’s performance relative to the Bloomberg U.S. Treasury 1-3 Year Index.

“The broad market typically experienced a strong relief rally immediately after the Fed pause and mostly outperformed the following year,” Malik said, in a Monday client note. “This lends further credence to our view that overallocating to cash or short-term government debt could be a mistake — and that investors may want to start closing their duration underweights.”

Individuals can gain exposure to Wall Street bond indexes through related exchange-traded funds, including the iShares Core U.S. Aggregate Bond ETF AGG

and the SPDR Bloomberg 1-3 Year U.S. Treasury Bond UCITS ETF UK:TSY3

for short-term Treasury exposure.

Fed Chairman Jerome Powell signaled on Friday that additional rate hikes might be needed to keep the U.S. cost of living in retreat, even though rates already sit at a 22-year high and inflation has fallen sharply in the past year, while speaking at the annual Jackson Hole gathering in Wyoming. He also reiterated a vow to keep rates at a restrictive level for a while to keep inflation in check.

Malik pointed to cooling housing inflation as a positive sign on the inflation front. Home buyers have pulling back as the benchmark 30-year mortgage rate hit an average of 7.31%, the highest levels since 2000.

She also expects U.S. economic growth to slow and a “partial retracing” of the 10-year Treasury yield BX:TMUBMUSD10Y,

following its surge in recent weeks.

“Historically, the 10-year yield has peaked within the last few months of the final rate hike in a tightening cycle. We expect this hike will occur at either the September or November Fed meeting, and that the 10-year yield will decline through year-end.” Yields and debt prices move opposite each other.

Stocks were higher Monday, with the Dow Jones Industrial Average DJIA

up 0.5%, the S&P 500 index SPX

0.3% higher and the Nasdaq Composite Index COMP

up 0.4%, according to FactSet.

Federal Reserve Chair Jerome Powell set a high bar for additional interest-rate hikes, economists said Sunday in their commentary on all the talk at the U.S. central bank’s summer retreat in Jackson Hole, Wyo.

Michael Feroli, chief U.S. economist for JPMorgan Chase, said that the Fed chair certainly did not give a clear signal that more tightening was coming soon. He noted that Powell stressed the Fed would “proceed carefully” and balance the risks of tightening too much or too little.

“We remain comfortable in our view that the FOMC will stay on hold for the next several meetings,” Feroli said.

The caveat to this forecast is if inflation surprises to the upside or the labor market does not continue to soften.

Ian Shepherdson, chief economist at Pantheon, said that Powell’s speech seemed hawkish to some, particularly because the Fed chair made threats to hike again.

But Shepherdson said he thought the Fed “is likely done.”

“Behind the caveats, Mr. Powell’s speech fundamentally was optimistic, though cautious,” Shepherdson said.

Boston Fed President Susan Collins also emphasized patience in an interview with MarketWatch on the sidelines of the Jackson Hole summit.

Other regional Fed officials who spoke “hinted that further action may be needed, but also observed that inflation is moving in the right direction and that the surge in yields would help cool down the economy,” said Krishna Guha, vice chairman of Evercore ISI, in a note to clients.

Traders in derivative markets expect a rate hike in November, but it is a close call, with the odds just above 50%.

The first test of the careful and patient Fed will come this coming Friday, when the government will release the August employment report.

Economists surveyed by the Wall Street Journal expect the U.S. economy added 165,000 jobs in the month. That would be the weakest job growth since December 2020.

In his speech on Friday, Powell emphasized that evidence that the labor market was not softening could “call for a monetary policy response.”

Economists at Deutsche Bank think an upside surprise in the employment data could provide enough discomfort for the Fed, and raise expectations for further tightening.

Guha of Evercore said he detected a careful effort by the officials not to surprise markets.

The exception to this rule might have been Bundesbank President Joachim Nagel, who said in a television interview that it was too early for the ECB to think about a rate-hike pause.

Chinese regulators eased the nation’s mortgage requirements to let more home buyers enjoy favorable mortgage conditions that were previously limited to first-time home purchasers, the state-run Xinhua News Agency said on Friday.

China’s central bank, the Ministry of Housing and Urban-Rural Development and the National Financial Regulatory Administration jointly eased the requirements for home buyers who have already purchased homes to boost property sales as the real-estate slump continued, according to Xinhua.

Home buyers who don’t have family members with houses registered under their names can enjoy favorable terms that were previously limited to people buying their first homes, according to Xinhua.

First-home buyers are normally given cheaper mortgage rates than other buyers who have at least one apartment. First-home buyers are also required to make smaller down payments, as low as 20% of the total property value.

Write to Singapore editors at singaporeeditors@dowjones.com

Credit Suisse said it has abandoned its plan to launch an initial public offering for its Credit Suisse 1a Immo PK real-estate fund due to low trading volumes for listed Swiss real-estate funds.

The Swiss bank–now part of UBS Group–said Thursday that Credit Suisse Funds decided not to carry out the IPO, which had been planned for the fourth quarter of 2023, and that this will allow the newly formed real-estate unit within UBS Asset Management to coordinate its offer of real-estate investment services.

A fall in trading volumes on the market for listed Swiss real-estate funds would likely have meant higher volatility in the event of a listing, Credit Suisse said.

The bank last year postponed the IPO of the fund, citing market conditions and the high volatility.

Write to Adria Calatayud at adria.calatayud@dowjones.com

The numbers: Mortgage rates rose for the fourth week in a row to the highest level since 2000, as the economy continues to show strength.

Rates surged as the U.S. economy continued to show signs of resilience, which signal to the market that the U.S. Federal Reserve may not be done with rate increases.

The 30-year was averaging at 7.31%, which in part dampened demand for home-purchase mortgages to the lowest level since April 1995.

Demand for both purchases and refinancing fell. That overall pushed down the market composite index, a measure of mortgage application volume, the Mortgage Bankers Association (M.B.A.) said on Wednesday.

The market index fell 4.2% to 184.8 for the week that ended Aug. 18, relative to a week earlier. A year ago, the index stood at 270.1.

Key details: High mortgage rates are weighing on home buyers’ budgets due to an increase in borrowing costs. Many buyers fled the market as a result of rates rising over the last week. The purchase index, which measures mortgage applications for the purchase of a home, fell 5% from last week.

Rates hold little allure for homeowners hoping to refinance. The refinance index fell 2.8%.

Rates rose across the board.

The average contract rate for the 30-year mortgage for homes sold for $726,200 or less was 7.31% for the week ending August 18. That’s up from 7.16% the week before, the M.B.A. said. The 30-year is at the highest level since December 2000.

The rate for jumbo loans, or the 30-year mortgage for homes sold for over $726,200, was 7.27%, up from 7.11% the previous week.

The average rate for a 30-year mortgage backed by the Federal Housing Administration rose to 7.09% from 6.93%.

The 15-year rose to 6.72%, up from last week’s 6.57%.

The rate for adjustable-rate mortgages rose to 6.5% from last week’s 6.2%. The share of adjustable-rate mortgages rose to 7.6%, the highest level in five months.

The big picture: The housing market continues to be hammered by good economic news, which is pushing rates up and depressing home sales. Higher rates also discourage homeowners from selling, as their purchasing power erodes when they look for homes to buy.

As a result, both home-buying demand and supply of home listings continues to fall, bringing the market to a standstill. Until the economy shows signs of slowing, it’s likely that the housing market will remain in the doldrums.

What the M.B.A. said: “Applications for home purchase mortgages dropped to their lowest level since April 1995, as home buyers withdrew from the market due to the elevated rate environment and the erosion of purchasing power,” Joel Kan, deputy chief economist and vice president at the M.B.A., said in a statement.

Kan added that there was an uptick in people using adjustable-rate mortgages. “Some home buyers are looking to lower their monthly payments by accepting some interest rate risk after the initial fixed period,” he said.

Market reaction: The yield on the 10-year Treasury note BX:TMUBMUSD10Y

was above 4.3% in early morning trading Wednesday.

U.S. banks and regional banks fell across the board on Tuesday, after S&P Global Ratings downgraded five smaller players after a review of risk related to funding, liquidity and asset quality with a focus on office commercial real estate.

Adding to the gloom, Republic First Bancorp. Inc.’s stock FRBK, -41.90%

tanked by 39%, after Nasdaq told the company that its stock would be delisted on Wednesday, after it failed to file its annual report in time.

S&P’s move comes just days after Fitch Ratings analyst Christopher Wolfe reduced his operating environment score for U.S. banks to aa- from aa due to the unknown path of interest rate hikes and regulatory changes facing the sector.

And Moody’s Investors Service just two weeks ago upset investors when it downgraded some lenders and said it was reviewing ratings on bigger banks, including Bank of New York Mellon BK, -1.71%,

State Street STT, -1.59%

and Northern Trust NTRS, -1.73%.

The S&P 500 Financials Sector has fallen for seven consecutive days, and is on pace for its longest losing streak since April 7, 2022, when it also fell for seven straight trading days.

Individual bank names are also performing poorly, with Goldman Sachs Group Inc. GS, -0.94%

and Citigroup Inc. C, -1.68%

down for 10 of the past 11 days and Charles Schwab Corp. SCHW, -4.84%

down 11 straight days.

Goldman alone has fallen for seven straight days for a total loss of 6.3%. It’s the longest losing streak since Feb. 28, 2020, when it also fell for seven straight days as the pandemic was taking hold.

The KBW Nasdaq Regional Banking Index KBWR

is down for 11 straight days. and the KBW Nasdaq Bank Index BKX

is down for seven straight days.

S&P downgraded Associated Banc. Corp. ASB, -4.20%,

Comerica Inc. CMA, -3.82%,

KeyCorp KEY, -3.58%,

UMB Financial Corp. UMBF, -2.42% % and Valley National Bancorp. VLY, -4.19%

by one notch and said the outlook on all five is stable.

The rating agency affirmed ratings on Zions Bancorp ZION, -4.17%

and maintained a negative outlook, meaning it could downgrade them again in the near-term. And it affirmed ratings and a stable outlook on Synovus Financial Corp. SNV, -3.37%

and Truist Financial Corp. TFC, -1.36%

“We reviewed these 10 banks because we identified them as having potential risks in multiple areas that could make them less resilient than similarly rated peers ,” S&P said in a statement.

“For instance, some that have seen greater deterioration in funding—-as indicated by sharply higher costs or substantial dependence on wholesale funding and brokered deposits—-may also have below-peer profitability, high unrealized losses on their assets, or meaningful exposure to CRE.”

The steep rise in interest rates orchestrated by the Federal Reserve over the past year has raised deposit costs as banks are now competing for savers seeking higher returns and that’s forced some to pay up on deposits and discourage their clients from heading to other institutions and instruments.

However, S&P said about 90% of the banks it rates have stable outlooks and just 10% have negative ones. None have positive outlooks.

The widespread stable outlooks shows that stability in the U.S. banking sector has improved significantly in recent months.

S&P is expecting FDIC-backed banks in aggregate to earn a relatively healthy ROE of about 11% in 2023.

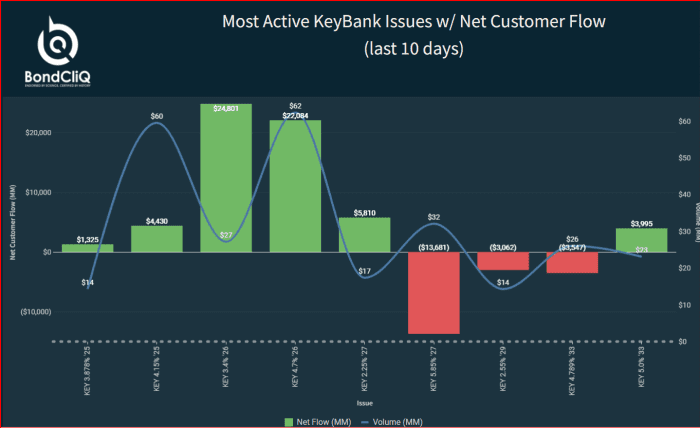

KeyCorp. and Comerica both fell more than 3% on the news. Of the two, KeyCorp. has more outstanding debt and its 10-year bonds widened by about 5 to 10 basis points, according to data solutions provider BondCliq Media Services.

As the following chart shows, the bonds have seen better selling on Wednesday with buyers emerging around midmorning.

KeyBank net customer flow (intraday). Source: BondCliQ Media Services

The next chart shows customer flow over the last 10 days.

Most active KeyBank issues with net customer flow (last 10 days). Source: BondCliQ Media Services

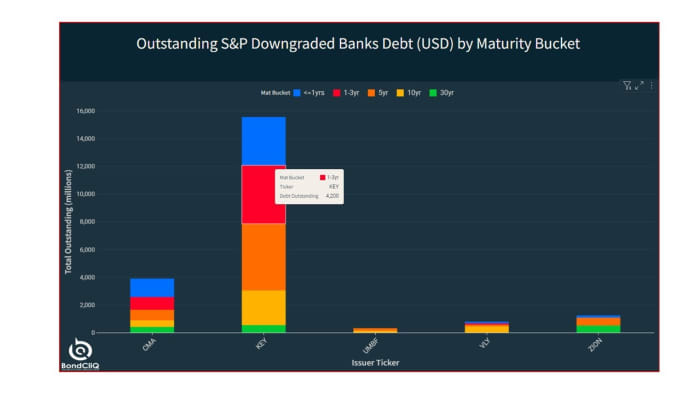

The next chart shows the outstanding debt of the downgraded banks, with KeyCorp. clearly the leader with almost $16 billion of bonds.

Outstanding S&P downgraded banks debt USD by maturity bucket. Source: BondCliQ Media Services

Stocks closed mostly lower Friday, capping off a bruising week of losses as Treasury yields jumped and China’s mounting property woes gripped investors. The Dow Jones Industrial Average DJIA, +0.07%

rose about 27 points, or 0.1%, ending near 34,501, according to preliminary FactSet data. The S&P 500 index SPX, -0.01%

was nearly flat at 4,370 and the Nasdaq Composite Index COMP, -0.20%

shed 0.2%, despite briefly turning positive late in the session. It still was a tough week for equities, with the Dow booking a 2.2% loss, the S&P 500 index a 2.1% decline and the Nasdaq a 2.6%. The Nasdaq also posted its biggest 3-week decline since December 2022, according to Dow Jones Market Data. Yields on the 10-year Treasury rose for a 5th week in the row, with the benchmark TMUBMUSD10Y, 4.252%

rate briefly touching its highest level since November 2007, before settling back at 4.251% on Friday. China Evergrande’s EGRNF, Chapter 15 bankruptcy filing in New York late Thursday kept focus on the wobbling property market in the world’s second-largest economy. Earlier in the week, Country Garden Group missed a dollar-denominated debt payment. Next week investors will be focused on Federal Reserve Chairman Jerome Powell’s speech on Friday at the Jackson Hole economic summit for hints to whether the central bank is likely done hiking rates in this cycle. The Fed’s policy rate sits at its highest level in 22 years.

While negative returns might stir bad memories of last year’s shocking losses for bonds, stocks and nearly everything else, investors holding Treasury debt issued at 2023’s higher yields might want to sit back and take stock.

“This is the top thing we hear,” said Ryan Murphy, director of fixed-income business development at Capital Group, of evaporating returns in what’s been a tough August. “You saw the worst bond market in 40 years last year. Investors, they are tired, and feel beaten up.”

Murphy’s message to clients is this: “In bonds, you earn the money over time.” And those dwindling bond returns since January? “Approach it with a deep breath, and know this is going to work out in the end.”

Capital Group’s laid-back style and lack of “a star CEO” earned it recognition by Institutional Investor in March as “a new bond leader” without a king, in large part because it attracted $100 billion in funds over the past five years, or twice the total of its peers.

Recent volatility in interest rates again zapped yearly gains in many bond funds, as Fed officials continued to warn that a roaring labor market and robust spending could keep inflation from receding to the central bank’s 2% annual target.

The spike in long-term bond yields makes older, lower-yielding securities look comparatively less attractive. That’s reflected in the yearly return on a key Bloomberg U.S. government bond and note index, which turned negative for the first time since March (see chart), when several regional banks failed, stoking fears of a broader banking crisis.

Returns on U.S. government bonds turn negative for the year.

FactSet

However, a look back at August 2022 shows the 10-year Treasury yield starting around 2.6%, according to FactSet.

By contrast, Treasury bill yields BX:TMUBMUSD06M

neared 5.5% on Thursday, or “north of anything we’ve seen over the past 15 years,” Murphy said. And for investors looking to lock in longer-term yields, the 10-year Treasury rate BX:TMUBMUSD10Y

touched 4.307% on Thursday, its highest level since November 2007, according to Dow Jones Market Data.

“It’s becoming more expensive for the government and companies to finance debt because of the rapid climb in rates,” Murphy said of the drag of higher long-term interest rates.

On the flip side, it’s also been one of the best stretches for lenders and bond investors in terms of getting paid to act as creditors since the 2007-2008 global financial crisis, but without a U.S. recession — or at least not yet.

What’s also different from last year is that the Fed already jacked up interest rates to a 22-year high of 5.25%-5.5% in July, and has signaled it’s likely nearly finished with hikes in this cycle.

Record cash on the sidelines

Murphy pointed to a mountain of cash on the sidelines, in the form of assets in money-market funds, as another potential stabilizer for markets.

Assets in money-market funds hit a record $5.57 trillion for the week ending Wednesday, according to data from the Investment Company Institute.

“What’s really interesting is that there’s been two bursts of investors going into money-market funds. There was a big shift right at the onset of COVID, and another burst over the past 12-18 months since the beginning of the rate-hiking cycle,” Murphy said.

Looking back to 2008, he pointed to a similar buildup in money-market assets, and a roughly $1.1 trillion wall of cash subsequently leaving the sector, as financial assets began to recover in the wake of the financial crisis.

“What we did see, while not all of it, was a healthy amount went back into fixed-income in the following years,” Murphy said.

Stocks closed lower Thursday and were headed for another week of losses, with the Dow Jones Industrial Average DJIA

2.3% lower on the week so far, the S&P 500 index SPX

down 2.1% and the Nasdaq Composite Index off 2.4%, according to FactSet.