[ad_1]

We’re building more houses—and prices are down!

On Monday, the Canada Mortgage and Housing Corporation announced housing starts rose from 241,111 units in April to 264,506 units in May: good for a 10% increase. The pace was highest in Montreal, where starts were up 104%, and in Toronto, they were notably up 47%. That’s a pretty good clip, considering how high interest rates are at the moment.

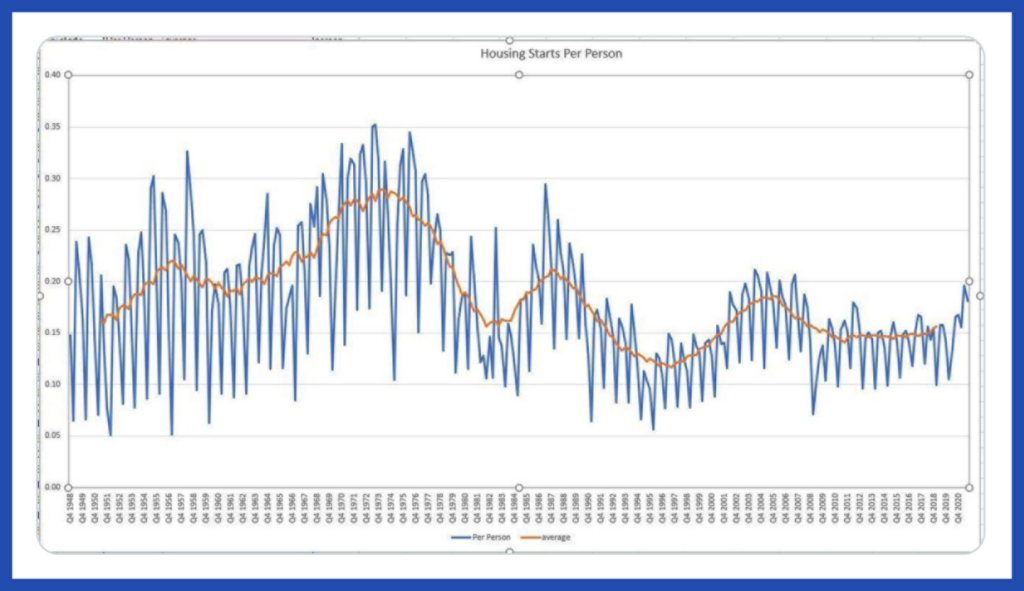

While it would be statistically correct to say that this level of housing starts is near historically high levels, that doesn’t quite tell the whole story.

To get a more accurate historical perspective, we should consider the housing starts per capita over the years. After all, Canada’s higher population should mean more capital, carpenters, electricians and other factors of production that go into housing creation, right?

Perhaps we’re moving in the right direction, but we’ll need a major uptick in housing starts before we have proportionately the same housing creation numbers as we did back in the heyday of the 1970s. Many young Canadians are hoping recent government incentives will spur more housing development sooner rather than later.

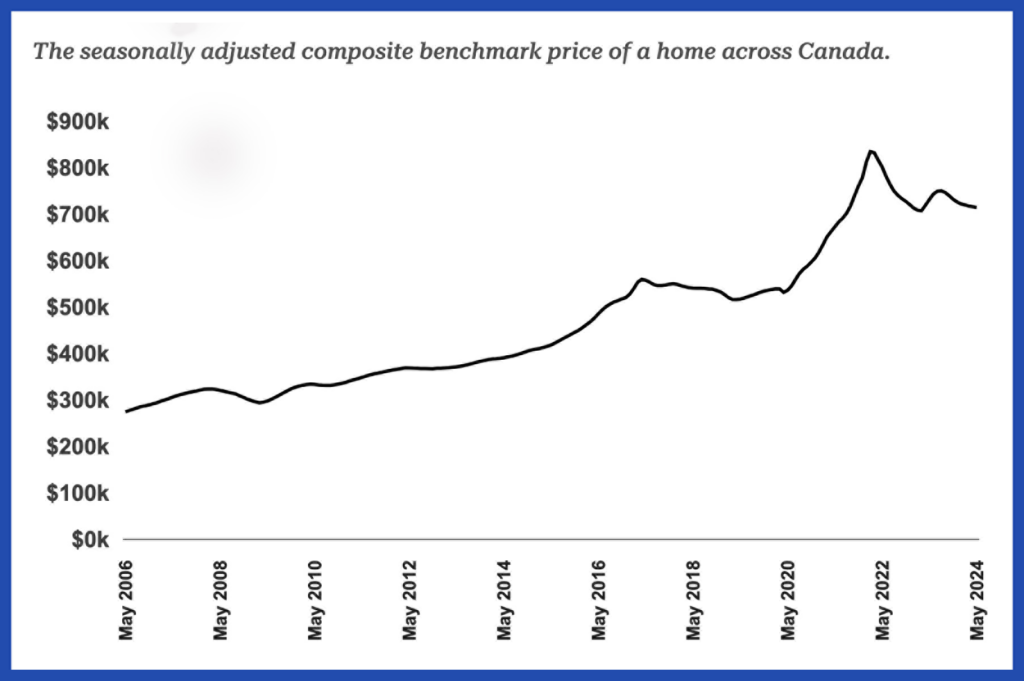

While there is more housing supply on the way, it appears that high interest rates continue to affect the current market. This week, the Canadian Real Estate Association released data that revealed total Canadian home sales were down nearly 6% in May on a year-over-year basis. The average home price slipped to $699,117, down 4% from May 2023 and about 14.4% from its peak in February 2022.

While the small interest rate cut earlier this month may spark some renewed appetite in the real estate market, it’s notable that the number of newly listed properties has jumped 28.4% from this time last year. As more mortgage renewals start to come up, it will be interesting to see which force is stronger: the increase in demand as mortgage rates decrease, or the continued softening of the market as more folks are forced to list houses they can no longer afford (as well as more new units being added).

What does the average Canadian buy?

Each month, Statistics Canada produces an inflation report based on the consumer price index (CPI), a representative “basket” of goods and services across eight categories (food, shelter, transportation, etc.) whose prices are tracked over time. Most of us simply accept that the CPI is a good measurement to go by, while others think it’s out of touch with reality. This week, the CPI got its annual update, after the Statistics Canada team looked at how average consumer preferences have changed over the last 12 months.

The CPI can’t stay the same from year to year because what we buy changes significantly over time. Consequently, measuring inflation with exactly the same goods from years ago doesn’t make much sense. For example, compact discs and videocassettes would have been part of the CPI basket back in my childhood—probably not so much today. Here are some of the more notable changes:

[ad_2]

Kyle Prevost

Source link