Want more stock market and economic analysis from Phil Rosen directly in your inbox? Subscribe to Opening Bell Daily’s newsletter.

In the Brave New World of AI dealmaking, the same few names keep showing on up every side of the ledger.

Let’s take stock for a moment:

- Nvidia supplies the chips that power OpenAI

- OpenAI buys computing power from Oracle and CoreWeave

- Oracle finances those purchases partly through its own vendors, which includes Nvidia

- Nvidia has separately committed $100 billion to invest in OpenAI

- Microsoft is both OpenAI’s biggest shareholder and one of its largest customers

- AMD issued OpenAI $34 billion in warrants in exchange for deploying its chips

I can’t be the only one confused by this seemingly closed web of contracts, capital pledges, and cross-ownership.

It’s as if the entire AI sector could be placed on a single, sprawling balance sheet — one that makes oodles of money for all parties involved, of course.

In a note to clients this week, Morgan Stanley strategists said this “circularity” is becoming one of the defining features of the AI era — suppliers double as customers, investors and creditors, while the source of dollars get harder to trace.

“The key players in the AI space are becoming increasingly interwoven, with suppliers funding customers, rising customer concentration, revenue sharing between customer and vendor, take-or-pay contracts, and vendor repurchase agreements,” the strategists said.

By their tally, suppliers are funding customer operations through equity stakes and creative financing.

That setup, in turn, allows other vendors selling to the same customer to take on more debt, since their buyer’s balance sheet has been reinforced.

The AI economy, in other words, operates as its own feedback loop.

Each deal bolsters the next one. For example:

- Nvidia rents cloud capacity from CoreWeave

- CoreWeave rents to Microsoft

- Microsoft licenses OpenAI software that ultimately runs on Nvidia hardware

The result, according to Morgan Stanley, is that most investors won’t understand the complete risks and rewards of the interconnected system.

To be clear, opacity doesn’t necessarily mean more or less risk.

It could simply be a consequence of rapid scale and the sense of urgency surrounding the current arms race.

After all, the biggest companies in the world are working hard to build new products and infrastructure to meet unprecedented demand that’s only expected to rise.

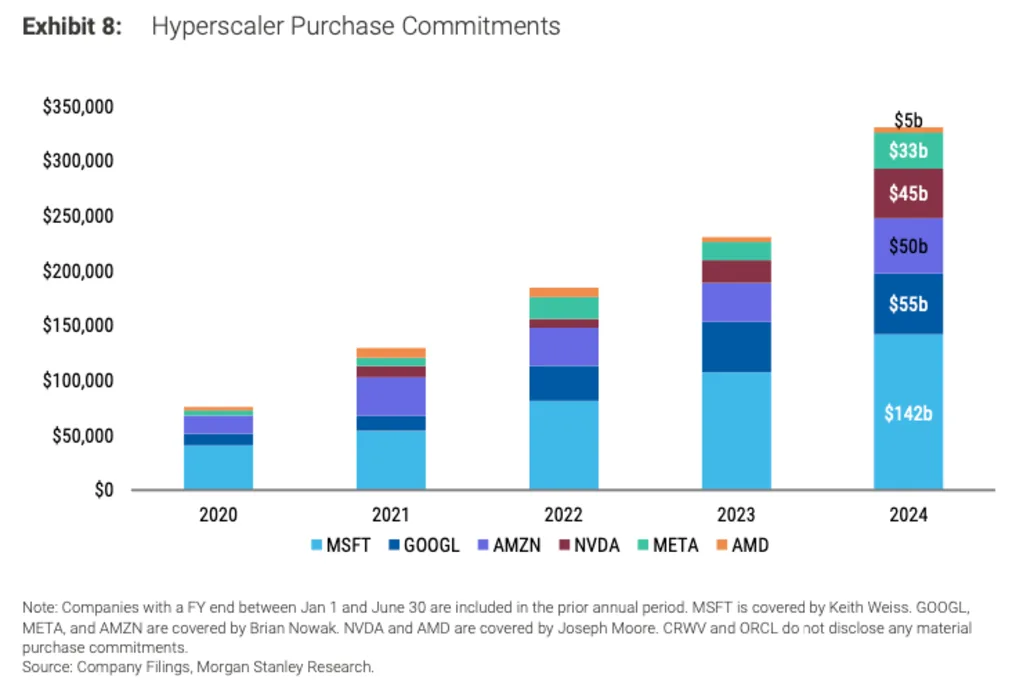

Hyperscalers’ combined purchase and lease commitments have now climbed toward an eye-watering $670 billion.

“If AI demand accelerates, this would be a strategic advantage,” Morgan Stanley strategists said. “But if growth lags, it could expose their customers to capital outlays that will not have returns.”

One useful way to think about the AI economy is not as a bubble inflated by speculation, but as a self-sustaining engine that can’t afford to let itself slow down. The entire network compounds on reciprocal investments, where each new deal drives the demand, funding and justification for the next.

Unlike the vertical integration of the internet era, Big Tech today appears to be pushing for some sort of horizontal entanglement.

Phil Rosen

Source link