The U.S. economy could expand at about a 2.2% annual rate in the current quarter, according to a revamped real-time estimate from the New York Federal Reserve released Friday.

According to the weekly New York Fed’s Staff Nowcast, the economy has been on an upward trend since late July.

The regional Fed bank had discontinued the real-time estimate during the pandemic. The New York Fed said the series will now be available weekly.

The New York Fed’s estimate is much lower than the Atlanta Fed’s GDPNow model, which shows growth could expand at a 5.6% annual rate in the current quarter.

Economists say the strength of the economy will be critical going forward in deciding whether the Federal Reserve needs to continue to raise its policy interest rate to cool inflation.

The Fed has been expecting the economy to slow in the second half of the year. Fed officials forecast only 1% growth for 2023. In the first six months of the year, U.S. gross domestic product is averaging about a 2% growth rate.

If the economy reaccelerates, it is likely that inflation will also move higher. Fed officials had been hoping that slower economic growth would continue push down inflation.

Faster growth means “you are probably going to get some inflation numbers that aren’t going to be as good as people were anticipating,” said James Bullard, the former president of St. Louis Fed president and now dean of Purdue’s business school.

“There is some risk that the Fed will have to go a little bit higher” even than the one more interest rate hike that the central bankers have penciled in this year, he said, in a recent CNBC interview.

The first official government estimate of third-quarter growth won’t be released until Oct. 26.

The picture of the health of the economy painted by U.S. GDP statistics can change quickly.

The growth estimates for the first half of the year could be revised at the end of September when the Commerce Department releases benchmark updates to GDP data.

The sharp revisions are one of the reasons why the Fed typically pays more attention to the unemployment rate and the inflation data.

Usually, the announcement of a CEO change at a struggling company brings optimism and maybe even a stock pop. Not for

Walgreens Boots Alliance

Its shares have tumbled since Rosalind Brewer announced on Sept. 1 that she was stepping down. That could present a buying opportunity if the company makes the “right” choice…

Shares of GameStop Corp. rose in extended trading Wednesday after the videogame retailer and original meme stock reported second-quarter results that beat expectations, lifted by international sales gains and what the company described as “a significant software release.”

The company — which over the past few months has made some big leadership changes — reported a net loss of $2.8 million, or 1 cent a share, compared with $108.7 million, or 36 cents a share, in the same quarter last year. Revenue crept higher to $1.16 billion,…

After nearly two years of concerns about a recession, growing optimism about the economy is starting to filter down into Wall Street’s expectations for individual companies’ quarterly results, with analysts growing more upbeat about corporate profit in the months ahead

While expectations for those quarterly results usually trend lower as earnings season arrives, analysts over the past two months have actually nudged their profit forecasts higher for the first time in two years, according to a FactSet report released Friday….

Shares of investment giant Blackstone Inc. and vacation-home rental platform Airbnb Inc. rallied after hours on Friday after both won the nod to join the S&P 500 index SPX

later this month.

The announcement, from S&P Dow Jones Indices, said that the change would take hold before the start of trading on Monday, Sept. 18. The move, among others announced Friday, will “ensure each index is more representative of its market-capitalization range,” according to a release.

Airbnb ABNB, +0.87%

currently has a market value of $83.98 billion, and its shares are up 64.7% so far this year. Blackstone BX, -1.77%,

currently worth $129.29 billion, has seen its stock rise 43.6% year-to-date.

Shares of Airbnb and Blackstone were up 5.7% and 4.8%, respectively, after hours on Friday.

Blackstone and Airbnb will replace Lincoln National Corp. LNC, +2.14%

and Newell Brands Inc. NWL, +1.23%

in the index, S&P Dow Jones Indices said on Friday. In the process, Lincoln and Newell will join the S&P SmallCap 600.

“We’ve established an unparalleled global platform of leading business lines, offering over 70 distinct investment strategies,” Chief Executive Stephen Schwarzman told analysts. “We believe our clients view us as the gold standard in alternative asset management.”

Meanwhile, Airbnb last month said that travelers were seeking longer stays and bigger properties in pricier areas, as the rebound in travel endures despite a tidal wave of inflation last year. The company’s second-quarter results and third-quarter sales forecast topped Wall Street’s estimates.

Meanwhile, S&P 500 member Deere & Co. DE, +1.94%

will replace Walgreens Boots Alliance Inc. WBA, -7.43%

in the S&P 100, S&P Dow Jones Indices said on Friday. That change also takes hold on Sept. 18. S&P Dow Jones Indices said Walgreens “is no longer representative of the megacap market space” but will stay in the S&P 500.

Shares of Deere fell 0.2% after hours. Walgreens stock was up 0.4%.

The U.S. Labor Day holiday will mark another milestone in the marathon to bring workers back to the office, but it won’t be a quick fix for landlords, according to Thomas LaSalvia, head of commercial real estate economics at Moody’s Analytics.

“A lot of companies are saying that after Labor Day, ‘We expect more out of you,” LaSalvia said, referring to days in the office. Still, office attendance, he argues, likely only stages a fuller comeback if a job or promotion is on the line.

That could prove difficult, with Friday’s U.S. jobs report for August expected to show U.S. unemployment at a scant 3.5%, near the lowest levels since the late 1960s, even if hiring has been slowing. The labor market, so far, appears unfazed by the Federal Reserve’s benchmark rate reaching a 22-year high.

It has been a different story for landlords facing a roughly 19% vacancy rate nationally and piles of debt coming due, especially for owners of older Class B and C office buildings with a bleak outlook or properties in cities with wobbling business centers.

As with shopping malls, LaSalvia said it’s largely a problem of oversupply, with many office properties at risk of becoming obsolete as tenants flock to better buildings and locations staging a rebirth. The trend can be traced in leasing data since 2021, with Class A properties in central business districts (blue line) showing a big advantage over less desirable buildings in the heart of cities (orange line).

Return to office isn’t going to save the entire office property market

Moody’s Analytics

“Little by little, we are finding the office isn’t dead,” LaSalvia said, but he also sees more promise in neighborhoods with a new purpose, those catering to hybrid work and communities that bring people together.

Another way to look at the trend is through rents. Manhattan’s Penn Station submarket, with its estimated $13 billion overhaul and neighboring Hudson Yards development, has seen asking rents jump 32% to $74.87 a square foot in the second quarter since the fourth quarter of 2019, according to Moody’s Analytics. That compares with a 2% bump in asking rents in downtown New York City to $61.39 a square foot for the same period.

The push for a return to the office also doesn’t mean a repeat of prepandemic ways. Goldman Sachs analysts estimate that part-time remote work in the U.S. has stabilized around 20%-25%, in a late August report, but that’s still up from 2.6% before the 2020 lockdowns.

Furthermore, the persistence of remote work will likely add another 171 million square feet of vacant U.S. office space through 2029, a period that also will see tenants’ long-term leases expire and many companies opting for less space. The additional vacancies would roughly translate to 57% of Los Angeles roughly 300 million square feet of office space sitting empty.

“The fundamental reason why we had offices in the first place have not completely disintegrated,” LaSalvia said. “But for some of those Class B and C offices, the writing was on the wall before the pandemic.”

U.S. stocks were mixed Thursday, but headed for losses in a tough August for stocks, with the S&P 500 index SPX

off about 1.5% for the month, the Dow Jones Industrial Average DJIA

2.1% lower and the Nasdaq Composite COMP

down 2% in August, according to FactSet.

The numbers: The index of U.S. consumer confidence dipped to 106.1 in August from a revised 114 in the prior month, the Conference Board said Tuesday.

Economists polled by The Wall Street Journal had forecast a modest pullback to 116 from the initial reading of 117, which was the highest level in two years.

The revised July reading was the highest since December 2021.

Key details: Part of the survey that tracks how consumers feel about current economic conditions fell to 114.8 this month from 153 in July.

A gauge that assesses what Americans expect over the next six months dropped to 80.2 from 88. The August reading is just above to 80 level that historically signals a recession within the next year.

Big picture: The tight labor market had bolstered confidence in June and July. The decline in August reverses all of those gains. The index is still 10.8 points above the recent cycle low in July 2022.

Economists think that higher gasoline prices were behind some of the decline in August. The price of a gallon of unleaded gasoline is up 19.6% from the start of the year and over 2% from last month.

What the Conference Board said: The organization said it still expects a recession before the end of the year.

“Write-in responses showed that consumers were once again preoccupied with rising prices in general, and for groceries and gasoline in particular,” said Dana Peterson, chief economist at The Conference Board.

What are they saying? “The August drop does not definitively end the upward trend in place since last summer, and the expectations index still points to faster growth in real consumption spending. We are not convinced, however, in part because some of the strength in July retail sales was due to boost from Amazon Prime Day, which won’t continue, and because near-real-time indicators of discretionary services spending paint a much less upbeat picture,” said Ian Shepherdson, chief economist at Pantheon Macroeconomics.

Robert Frick, corporate economist with Navy Federal Credit Union, said he didn’t think confidence would rise significantly until inflation falls further.

U.S. stocks so far haven’t fared as well under President Joe Biden as they did in Donald Trump’s single term or in either of Barack Obama’s two terms.

The research team at Wilshire Indexes is pointing that out this month with the chart below, which features the FT Wilshire 5000 XX:W5000FLT,

an index that aims to reflect the performance of the total U.S. stock market.

U.S. stocks haven’t performed as well in Biden’s current term as they did under Obama or Trump.

Wilshire Indexes

Biden and his allies could be worried about how stocks SPX

are doing, and it’s possible his administration will try to help the market somehow in 2024, according to Philip Lawlor, managing director of market research at Wilshire Indexes.

“With the 2024 election in sight, the disparity in cumulative equity return generated so far under the Biden administration compared to the superior return trajectory delivered by the Trump and Obama presidencies could cause some concern,” Lawlor wrote. “Electoral cycle logic points to the Biden administration doing its utmost to ensure that the gap closes next year.”

When asked about the stock market’s struggles earlier this year, one White House official told MarketWatch that the administration wants to see “strong performance,” but he also noted that roughly half of Americans don’t hold stocks and highlighted other economic indicators.

“The markets are going to go up and down. The main measure that the president has about the state of the economy is, how are middle-class families doing?” said Bharat Ramamurti, deputy director of the White House’s National Economic Council.

“Do they have good-paying jobs that allow them to support themselves and their families? Are they seeing their wages go up? Do they feel like they have good opportunities to advance in their career, good opportunities to switch jobs and make more money? Or live in a better neighborhood, or whatever the case may be? By those metrics, we think that the economy is doing very, very well.”

Republican presidential hopefuls made their economic pitches at a debate on Wednesday night in Milwaukee, with Florida Gov. Ron DeSantis, who is currently running second in GOP primary polls, saying the country “must reverse ‘Bidenomics’ so that middle-class families have a chance to succeed again.” Trump, the current frontrunner in the 2024 primary, skipped the debate and instead released an interview just before the event kicked off.

COMP

were higher in choppy trading Friday after Federal Reserve Chair Jerome Powell warned that the central bank may need to raise interest rates even higher to temper a strong U.S. economy and quell inflation, while assuring investors that the Fed would proceed cautiously.

stock plunged on Wednesday as investors kicked around a bevy of bad news. The shoe and sportswear retailer missed expectations for second-quarter sales, slashed its full-year outlook again, and paused its dividend.

Economists don’t much like presidential-campaign seasons. For them, it’s a bit like seeing their manicured gardens getting trampled by schoolchildren having a water-balloon fight.

Robert Brusca, the president of consulting firm FAO Economics, predicted that the political discussion of the U.S. economy in the 2024 campaign would be “a farce.”

Talk of inflation is likely to dominate the Aug. 23 Republican debate, for example.

Republicans, eager to lay the blame for higher prices at the feet of President Joe Biden, are going to make the strongest case they can for that. For them, it is a happy coincidence that inflation started to pick up right when Biden was sworn into office.

Larry Kudlow, a former top economic adviser to President Donald Trump, put it succinctly. “I have numbers. The consumer-price index is up 16% since February 2021. Groceries are up 19%. Meat and poultry up 19%. New cars up 20%. Used cars up 34%,” Kudlow said in an interview on the Fox Business Network.

Unlike Kudlow, the Federal Reserve doesn’t usually measure inflation over 29 months. Instead, the central bank favors using inflation data that looks at the past 12 months.

By that year-over-year measure, CPI is up 3.2%. Groceries are up 3.6%. Meat and poultry prices are up 0.5%. New-vehicle prices are up 3.5%, but prices of used cars and trucks are actually down 5.6%.

Economists, meanwhile, tend to like even shorter measures, such as the three-month annualized rate. They think the 12-month rate says more about the rate a year ago than it does about what is happening today.

“Looking at year-over-year [data], the only new piece of information is the current month. You are looking at 11 months that you already know,” said Omair Sharif, president and founder of research company Inflation Insights.

Using the shorter metric, headline CPI for the three months ending in July is up 1.9%, while food at home rose 1.1% and meat and poultry is down 4.5%, he said.

Trends have been favorable in recent months, but that might not last. “It’s been a good summer,” Sharif said. “But unfortunately, the winter data won’t be as pleasant.”

What caused the spike in inflation?

Economists tend not to blame one political party or the other for spikes in inflation.

In the 1970s, for example, the culprit was increases in oil prices by the Organization of Petroleum Exporting Countries.

This time, there was no one single factor. While the debate is not yet over, economists tend to focus on the pandemic, the war in Ukraine and the move to end reliance on fossil fuels in order to combat climate change.

Brian Bethune, an economics professor at Boston College, said prices started to rise when the healthcare industry had to adjust to a new, unforeseen risk. There were steep costs to dealing with the deadly coronavirus and developing vaccines.

People working in frontline industries were able to command higher wages. And demand outstripped supply for many things, as shelves were emptied by consumers and supply chains were strained.

Bethune also stressed recent moves toward renewable energy. The best way to explain inflation to your grandmother, he said, is to look at a chart of electricity prices.

Uncredited

The steady increase stems from efforts to move closer to a carbon-free economy, Bethune said. And those prices get passed along “right through the whole cost pressure of the economy,” including the price of refrigerated foods.

Inflation boomed and is now coming off its peak, said Brusca of FAO Economics. Prices are still rising, but not at the same rapid clip. And they won’t roll back to prepandemic levels.

“Consumers are caught in a trap,” he said. “If prices are going to come down, you have got to have deflation.”

Deflation comes with its own unique set of woes. It can make the cost of borrowed money, like mortgages, much more expensive. And it can lead to serious economic weakness.

“All of this is why the Fed targets price stability,” Brusca said.

In a dreary smartphone market, Apple Inc. could do something it’s never done before.

The consumer-electronics giant has a chance to finish the year as the global leader in smartphone shipments for the first time, according to analysts at Counterpoint Research.

Consumers continue to hold on to their smartphones for longer, one reason that the Counterpoint team expects overall shipments to fall 6% this year, to 1.15 billion units. That would be the lowest level in a decade.

“But we’re watching [the fourth quarter] with interest because the iPhone 15 launch is a window for carriers to steal high-value customers,” Jeff Fieldhack, Counterpoint’s North America research director, said in a release.

With a big base of current iPhone 12 owners due for upgrades, “promos are going to be aggressive, leaving Apple in a good spot.”

Counterpoint notes that premium smartphones have been picking up share within the market and called out China as a region where that trend holds true. Apple AAPL, -0.12%

focuses on the premium market and is expected to debut its next lineup of devices, the iPhone 15 family, in September, and sales likely will begin later that month or in early October.

Projections from Counterpoint put Apple the closest its ever been to capturing the top spot. “We’re talking about a spread that’s literally a few days’ worth of sales,” Fieldhack said. “Assuming Apple doesn’t run into production problems like it did last year, it’s really a toss-up at this point.”

Samsung Electronics Co. Ltd. 005930, +0.45%

was the market leader in shipments last year, and it held the top spot in the first quarter of this year.

When Nvidia Corp. last reported quarterly results, the chip maker forecast record revenue that was far above anything it had put up before. In response, investors sent the stock into orbit. On Wednesday, the latest round of earnings for the company will be a test of Nvidia’s status as the darling of the AI investment boom, and a test of whether it can deliver on its own lofty expectations.

The results will also be an update of tech demand overall, after businesses tightened their IT budgets following worries about an economic slowdown. But even with Nvidia’s NVDA, -0.10%

stock up more than 200% so far this year and expectations rising just as much, some analysts still say there’s room for shares to go higher, despite supply-side logjams.

Barclays said that Nvidia, whose chips analysts say will help power AI technology in the days to come, has “monopolized the economics of the AI boom, with no clear competitor close behind.” They added that “cloud capex budgets are being funneled towards AI.”

Signs that Nvidia might be falling behind on meeting chip demand have started to emerge. But as businesses rush to mark their territory, or potential territory, in the world of AI, Wedbush analysts have asked whether Nvidia’s results and forecast would even matter, as today’s production constraints turn into tomorrow’s sales.

“We don’t think NVDA results/guidance need to hit the high end of expectations,” Wedbush analyst Matt Bryson said in a research note on Friday.

“With demand for AI training having lifted substantially in the past quarter and with no other silicon supplier now capable of providing part volumes within an order of magnitude of NVDA’s output, we believe any unfilled demand will just be pushed into forward quarters fueling future sales and (earnings per share),” he continued.

Synovus analyst Daniel Morgan was also bullish on Nvidia’s business targeted toward data centers, as those facilities try to integrate generative AI and large language models. And within Nvidia’s gaming segment, he said the company’s new Ada Lovelace graphics-processing unit ecosystem “appears to be seeing a high level of success in retail.”

Still, the longer a stock runs higher, the harder it can fall. And Nvidia’s $1 trillion valuation, Morgan said, “is not for the faint-hearted.”

This week in earnings

Along with Nvidia, China search giant Baidu Inc. BIDU, -3.63%

reports, as the nation’s economic rebound sputters. And if more businesses are still cautious about cloud spending, or shifting spending to AI, the mood could filter through to results from Splunk Inc. SPLK, +0.35%

and Snowflake Inc. SNOW, +0.47%.

Peloton Interactive Inc. PTON, +1.59%,

Workday Inc. WDAY, +0.16%

and Marvell Technology Inc. MRVL, +0.05%

also report.

The call to put on your calendar

Zoom and offices: If even Zoom is calling some of its workers back to the office, what could that possibly mean for its results on Monday and the business of videoconferencing? Zoom Video Communications Inc. ZM, +1.42%

hasn’t been spared from the wave of tech-industry layoffs, and the company is trying to branch out from its pandemic-mainstay video-call platform, and harnessing its technology to handle phone calls and customer contact centers. Benchmark Research analyst Matthew Harrigan, in a note last week, said he still liked Zoom’s prospects, even though he wasn’t expecting “much instant gratification.” “We do expect AI to crystallize as a significant positive for Zoom even as it navigates through customer pushback on using customer data to train AI models off privacy concerns,” he said.

The numbers to watch

Sales, forecasts and inventories from retailers: Last week, Target Corp. TGT, +0.85%

reported what one analyst called “the definition of mixed results,” while another said the results amounted to “Recessionary trends without the recession.” Sales of essentials like groceries, as they have over the past year, helped Walmart Inc.’s WMT, +1.44%

results, but management said that consumers were still feeling the pain from inflation, which for some shoppers over the past year has left little room for much beyond the basics.

In the week ahead, we’ll get results whole bunch of retailers that don’t sell basics — like department stores Macy’s Inc. M, +0.53%

and Kohl’s Corp. KSS, +3.53%

; clothing chains Nordstrom Inc. JWN, +0.47%,

Gap Inc. GPS, +2.17%,

Urban Outfitters Inc. URBN, +2.00%

; shoe retailer Foot Locker Inc. FL, +0.60%

and beauty-products chain Ulta Beauty Inc. ULTA, +1.40%.

Those retailers will report as prices for some things start to come down, or at least not rise as fast, and as some economists overcome their recession fears. But remarks from executives could offer some sense of the impact from higher borrowing costs and the return of student loan payments, and how much they’ll be able to bank on the back-to-school season and wealthier — and more carefree — consumers.

Dollar-store Dollar Tree Inc. DLTR, +0.44%

will also report results, as low-income consumers suffer more under inflation and deal with the end of pandemic-era supplemental food assistance. Off-price retailer Burlington Stores Inc. BURL, +1.43%

reports as well, after Ross Stores Inc. ROST, +5.01%

Chief Executive Barbara Rentler said that while its low- and moderate-income shoppers were still hurting, shoppers overall “responded well to our improved value offerings throughout our stores.”

The majority of second-quarter earnings season is over, with a handful of major technology and retail names left to report this week. Economists will be focused on any news from an annual gathering of monetary policy thinkers and practitioners in Jackson Hole, Wyoming.

The so-called Magnificent Seven grouping of technology stocks lost some of its luster this week after four of the seven moved into correction territory, meaning their stocks have fallen at least 10% from their recent peaks.

The corporate-bond market, in contrast, seems to like all seven names.

One caveat: Tesla has no outstanding bonds. In the past, the electric-car maker issued convertible bonds, but they have all been converted into equity.

The group is credited with helping drive the stock market’s gains in the first half of the year, driven by excitement about artificial intelligence. But the rally has stalled in recent weeks as investors have fretted over the potential for U.S. interest-rate increases, surging Treasury yields and China worries, with property developer Evergrande filing for U.S. bankruptcy protection late Thursday.

On Thursday, Meta followed Apple, Microsoft and Nvidia into correction territory, as MarketWatch’s Emily Bary reported. Tesla, meanwhile, is in a bear market, meaning it’s down more than 20% from its recent peak.

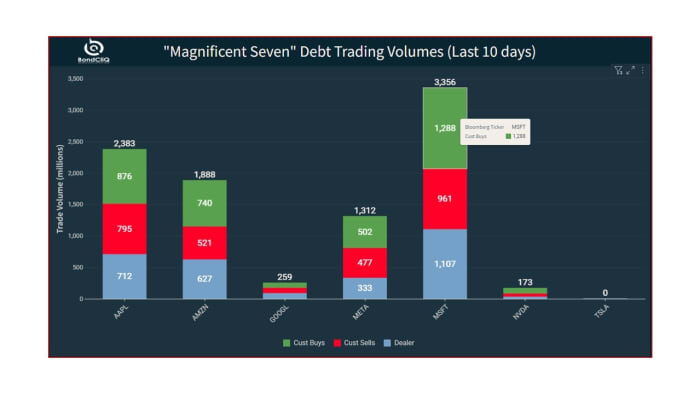

The following series of charts from data-solutions provider BondCliQ Media Services show how many bonds each company has issued by maturity and how they have traded as the stocks have pulled back.

The first chart shows that Microsoft has by far the most bonds, mostly in the 30-year bucket. The software and cloud giant has more than $50 billion in long-term debt, according to its 2023 10-K filing with the Securities and Exchange Commission.

Outstanding Magnificent Seven debt by maturity bucket.

Source: BondCliQ Media Services

This chart shows trading volumes over the last 10 days, divided by trade type. The green shows customer buying, while the red is customer selling. The blue shows dealer-to-dealer flows. Microsoft, for example, has seen almost $1.3 billion in customer buying from dealers in the last 10 days and $960 million in customer sales to dealers.

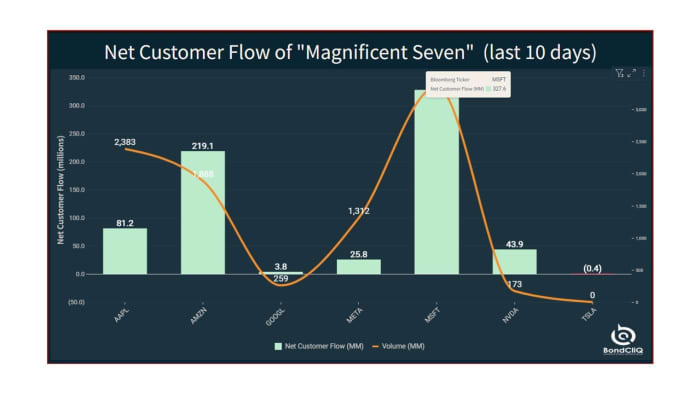

This chart shows that every name in the group has enjoyed better net buying in the last 10 days, with Microsoft leading the way.

Net customer flow of Magnificent Seven debt (last 10 days).

Source: BondCliQ Media Services

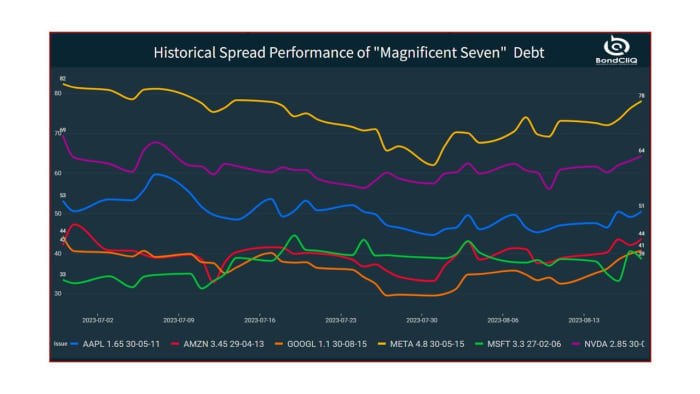

This chart shows spread performance over the last 50 days for an intermediate-term bond from each of the seven issuers. Most have tightened or remained steady over the period.

Historical spread performance of Magnificent Seven debt.

Apple’s stock entered correction Wednesday upon falling more than 10% from its July 31 peak of $196.45. The company sells mainly discretionary products, and right now “consumers are still being pinched” and thinking more carefully about where they spend their money, according to Matt Stucky, senior portfolio manager for equities at Northwestern Mutual Wealth Management.

Investors were jolted by a stronger-than-expected retail sales report on Tuesday, which underscores the dual-edged sword now facing markets.

July’s 0.7% surge in retail sales is helping to bolster the view that a resilient U.S. economy can avoid a recession, despite more than a year of rate hikes by the Federal Reserve. However, the data also serves as another piece of information that some policy makers can use to support even more hikes in the final four months of this year, and left the benchmark 10-year Treasury yield…

The thing that will make companies lower prices is if consumers stop complaining about paying more for the things they need and want, and actually start refusing to buy them.

As the U.S. corporate earnings-reporting season progresses, with earnings from major retailers Walmart Inc. WMT, +0.59%,

Target Corp. TGT, +0.10%

and Home Depot Inc. HD, +0.52%

on tap next week, investors can get a ground-floor view of how consumer demand may have been hurt, or not, by higher prices, and what the companies plan to do, or not do, about it.

This dynamic of how consumers adjust their spending habits when prices change is referred to by economists as the price elasticity of demand.

“ For companies to cut prices, ‘you have to have the consumer go on strike, and they’re not there yet.’”

— Jamie Cox, Harris Financial Group

Those who trust companies will choose to ratchet down prices on their own, or at least not raise them because the rise in input costs has been slowing, haven’t been listening to what the many companies have told analysts on their post-earnings-report conference calls.

Kraft Heinz Co. KHC, +0.47%

acknowledged after its second-quarter report that its relatively higher prices have hurt demand, but not by enough for the food and condiments company to consider cutting prices.

Colgate-Palmolive Co. CL, +0.81%

said it will continue to raise prices, even as inflation slows and selling volume declines, as the consumer-products company continues to be laser focused on boosting margins and profits.

And while PepsiCo Inc. PEP, +0.16%

was worried that elasticities would increase, given how its lower-income customers were being particularly pressured by inflation, the beverage and snack giant reported strong results as it witnessed “better elasticities” in most of the markets in which it operated.

“Obviously, there is still carryover pricing, and I don’t think we’ll do anything different than our normal cycles on pricing in the balance of the year,” PepsiCo Chief Financial Officer Hugh Johnston told analysts, according to an AlphaSense transcript.

Basically, as MarketWatch has reported, so-called greedflation is alive and well.

Jamie Cox, managing partner for Harris Financial Group, said as long as the job market stays strong, as it is now, corporate greed will continue to pay off.

“If something is more expensive, and you have a job, you’ll complain about it, but you won’t substitute it for something cheaper,” Cox said. For companies to cut prices, “you have to have the consumer go on strike, and they’re not there yet,” Cox added.

“ ‘At some point, people are going to say, “All right — enough.” ’ ”

— Paul Nolte, Murphy & Sylvest Wealth Management

The reason elasticity is so important in the current environment is that, as long as consumers continue to pay the higher prices companies are charging, inflation will remain stubbornly high, making it, in turn, more likely that the Federal Reserve will continue to raise interest rates or, at the very least, not lower them.

But the longer interest rates stay high enough to crimp economic growth, the more likely the stock market will reverse lower as recession fears rise.

“At some point, people are going to say, ‘All right — enough,’ ” said Paul Nolte, senior wealth manager and market strategist at Murphy & Sylvest Wealth Management. “But we just haven’t seen that yet.”

What is elasticity?

Economists use the term “price elasticity of demand” to refer to the way in which consumers adjust their spending habits when prices change.

“Elasticity tries to measure how much more producers will want to produce if prices rise, and how much more consumers will want to buy if prices fall,” explained Bill Adams, chief economist at Comerica.

Elasticity often depends on the type of product a company sells.

For example, consumer-discretionary-goods companies that sell products and services that people want will often experience greater price elasticity than consumer-staples companies that sell things that people need, such as groceries and prescription drugs.

But even for needs, consumers often still have a choice, as less expensive generic, or private-label, alternatives may be available.

Andre Schulten, chief financial officer of consumer-staples maker Procter & Gamble Co. PG, +0.58%,

which recently beat earnings expectations as it continued to raise prices, telling analysts that, while there was “some trading into private label,” the overall market share of private-label products was unchanged for the year.

As Harris Financial’s Cox said, consumers may be complaining about higher prices, but they aren’t yet desperate enough to stop buying.

The Federal Reserve’s latest Beige Book economic survey stated that business contacts in some districts had observed a “reluctance” to raise prices as consumers appeared to have grown more sensitive to prices, but other districts reported “solid demand” allowed companies to maintain prices and profitability.

That’s likely why companies and analysts have become less concerned about price elasticity. Based on a FactSet analysis, mentions of the word “elasticity” in press releases and conference calls of S&P 500 companies SPX

increased as inflation and interest rates started surging in early 2022 through the end of the year.

Mentions of the word elasticity in earnings press releases and conference-call transcripts of S&P 500 companies.

FactSet

As the chart shows, “elasticity” popped up in more than 55% of earnings releases and conference calls in mid-2022, but with the second-quarter 2023 earnings-reporting season more than half over, mentions had dropped to about 20%.

Perhaps that will pick up, as retailers, especially those catering to lower-income customers — recall the PepsiCo comment — assess the demand impact of continued price increases.

Meanwhile, the branded-foods company Conagra Brands Inc. CAG, +0.71%,

whose wide-ranging food brands including Birds Eye, Duncan Hines, Hunt’s, Orville Redenbacher’s and Slim Jim, were starting to see the emergence of a different dynamic.

Chief Executive Sean Connolly said consumers were shifting behavior in some categories as prices remained high. Rather than trade down to lower-priced alternatives, he noticed some consumers buying fewer items overall, “more of a hunkering down than a trading down.”

That’s exactly the kind of consumer behavior that is needed, if companies are to stop feeding into the greedflation phenomenon and to start pulling back on prices.