Data from the Federal Reserve shows that the so-called K-shaped economy in America is alive and well, with low- and middle-income households falling further behind as the richest Americans pull away.

The top 1% of households owned 31.7% of all U.S. wealth in the third quarter of 2025, the highest share on record since the Federal Reserve began tracking household wealth in 1989. That share has increased even as wealth growth for the rest of the population has stalled or slowed, the data shows.

Collectively, the wealthiest 1% held about $55 trillion in assets in the third quarter of 2025 — roughly equal to the wealth held by the bottom 90% of Americans combined.

“Household wealth is highly concentrated and becoming steadily more concentrated,” Mark Zandi, chief economist at financial research firm Moody’s Analytics, told CBS News.

The latest snapshot of wealth inequality comes as billionaire fortunes continue to grow rapidly, both in the U.S. and abroad. An Oxfam International report released this week found that billionaire wealth in 2025 increased three times faster than the average annual rate over the previous five years.

The world’s richest person is Tesla CEO Elon Musk, whose net worth stands at $668 billion, according to the Bloomberg Billionaires Index.

What’s driving the growing divide

Widening wealth inequality isn’t new to the U.S., with the trend reaching back decades. However, the gap between the rich and the poor has become more skewed since the pandemic, according to Zandi.

Consumer spending patterns underscore those disparities. In the second quarter of 2025, the top 10% of income earners accounted for nearly half of all U.S. consumer spending, according to Zandi’s analysis of Federal Reserve data.

The growing divide is being driven in part by surging stock prices, Zandi said.

The stock market posted strong gains last year, thanks in large part to investments in artificial intelligence. Wealthier households tend to benefit most from bull markets because a larger share of their wealth is invested in stocks and other securities.

According to Gallup, 87% of Americans who own stocks are adults living in households earning $100,000 or more.

Middle-income households, on the other hand, tend to have their wealth tied up in their homes, and house price growth has been slowing, Zandi added. Lower-income Americans are struggling with higher debt loads, he said.

Uneven wage growth is also contributing to the divide. Higher-income Americans have seen their wages grow at a stronger clip than other income groups. Bank of America data shows that higher-income households’ wage growth grew at 3% rate in December 2025, compared to 1.5% and 1.1% for middle- and low-income households.

The “K-shaped” economy, widely touted in the financial press, is the latest expression of wealth inequality. The U.S. economy is experiencing a growing gap between the highest earners and the richest corporations, who are spending and expanding their wealth, and the lowest-income households and mom-and-pop companies, who struggle to pay their bills day to day.

Following the second short-term interest rate cut on Oct. 29, Federal Reserve Chairman Jerome Powell said, “A further reduction in the policy rate at the December meeting is not a forgone conclusion — far from it.”

He cited the Fed’s ongoing concerns regarding inflation, employment, rising defaults in subprime credit, layoffs, and a “bifurcated economy.”

“If you listen to the earnings calls or the reports of big, public, consumer-facing companies, many, many of them are saying that there’s a bifurcated economy there and that consumers at the lower end are struggling and buying less and shifting to lower cost products, but that at the top, people are spending at the higher income and wealth,” Powell said.

That, in a nutshell, is the K-shaped economy.

Can a divided U.S. economy avoid a recession? And how can an economy that’s running hot on one end and cold on the other meet the needs of the millions in the middle?

The K-shaped economy is characterized by robust growth, expanding wealth, and a vibrant economy in the arms at the top of the K.

The legs of the K are where lower-income earners and small businesses continue to struggle.

Cristian deRitis, senior director and deputy chief economist at Moody’s Analytics, said the separation between the two is growing.

“The top 10% of households by income account for about half of all the spending in the U.S. economy, so it’s kind of illustrating the inequality, not only of income, but of spending that’s going on in the economy,” deRitis told Yahoo Finance.

In 2019, the share of spending by the top 10% households was 44.6%. However, the wealth gap goes beyond consumer spending.

“When we think about businesses and the stock market or we think about the labor market, some industries are hiring, others are laying off,” deRitis added. “So, I see that K-shape not only in the consumer — I think that’s where it gets a lot of attention — but it’s actually in a lot of different parts of the economy where you can see that kind of bifurcation of activity.”

DeRitis believes the widening separation between the haves and have-nots goes back to the stimulus relief of the pandemic.

“Households at the bottom in particular got quite a bit of support that helped them to get their finances back in order,” deRitis said. “Delinquency rates went way down. But now that money has run out because inflation has been high, the labor market is slowing — so you don’t have as much wage growth.”

Meanwhile, the top of the K, the wealthiest households and corporations, have benefitted from a rising stock market and asset price appreciation, including housing and crypto.

While the stock market has set record highs recently, it has been on the backs of the largest companies. This is adding to the riches of the very wealthy, who have the biggest individual stake in equities.

During Ford’s Ford (F) latest earnings call, the company highlighted profit driven by its top-of-the-line models, including the F-150, Bronco, Explorer, and Expedition. “The all-new Expedition is red-hot, gaining over three points of segment share, with 75% of customers choosing high-end trims like Tremor,” the company said.

Delta Air Lines’ (DAL) premium-priced seating and iPhone 17 Pro smartphones that top $1,000 are other examples.

Chipotle (CMG) cut its full-year sales outlook for the third straight quarter, with CEO Scott Boatwright citing “persistent macroeconomic pressures” and poorer customers who aren’t eating there as often.

In an analysis, Torsten Sløk, chief economist for Apollo, reveals that earnings expectations for 2026 have soared for the Magnificent 7 stocks and declined for the rest of the S&P 500 (^GSPC). (Disclosure: Yahoo Finance is owned by Apollo Global Management.)

Anthony Chan, a former economist for the Federal Reserve and JPMorgan Chase, told Yahoo Finance that a K-shaped economic recovery is the latest incarnation of wealth inequality.

“It is showing you that inequality is becoming so bad that it’s now impacting how the economy proceeds. All you have to do is look at the anecdotal evidence on food pantries. They’re getting more and more people visiting food pantries. Why? Because people at the lower end are struggling.”

He also cites the popularity of buy now, pay later.

“I can assure you that the top 1% — the top 10% of the people — are not interested in buy now and pay later. They buy it and they just pay for it and they don’t even think about it. But you’re actually seeing some of the lower-income people buying supermarket groceries with buy now and pay later.”

Chan is not quick to predict a recession. He noted that the Atlanta Fed is projecting 4% growth in the third quarter, following the 3.8% gain in the second quarter.

“I’ve never seen a recession in my entire life where you have 3.8% growth one quarter and 4% in the other quarter,” Chan added. “Potential growth is about 2%, maybe a little bit less than that. So, if you’re growth is twice as fast as potential economic growth, I really think it’s almost economic malpractice to say that we’re entering or close to being in a recession.”

Yet, Chan and deRitis both noted there are wild cards in the economic forecast, and deRitis called out one in particular.

“I suspect that the investments in artificial intelligence are perhaps getting ahead of themselves, and they may not live up to the extreme expectations that we have,” deRitis said. “There’s likely to be some type of correction in the stock market going forward as investors come to grips with the reality.”

In an extended bear market scenario, the top tier of wealthy households might cut back on spending, and the handful of big tech firms that have been leading stock gains would suffer.

“If we have an AI setback, absolutely, it could be a recession,” he added.

The Student Freedom Initiative (SFI) and Atlanta Mayor Andre Dickens teamed up to host a fireside chat on investing in Atlanta’s next generation on Thursday. Hosted at the flagship location of the Gathering Spot, the evening was filled with discussions on how to close the wealth gap created by excessive college loan debt.

The fireside chat featured Dickens, Nancy Flake Johnson, the president and CEO of The Urban League Greater Atlanta, and Keith Shoates, president and CEO of the Student Freedom Initiative. They dived into the mayor’s Neighborhood Reinvestment Initiative, a sweeping initiative to make significant investments in historically underserved communities. According to the mayor, this initiative has resulted in a 44% reduction in homicides and the construction of nearly 12,000 units of affordable housing, with many more units currently under construction.

The event follows the 2024 Year of the Youth, a program launched in 2023 to provide resources and support to the city’s youth. Since the program’s launch, the city has seen a 56% reduction in youth crime, attributed mainly to initiatives such as the Summer Youth Employment program.

Photo by Laura Nwogu/The Atlanta Voice

“That’s what the Neighborhood Reinvestment Initiative is all about. It’s taking the whole of government, taking our non profit partners and civic partners, as well as our business partners, and saying in these areas, we’re going to have investments in people and places in a meaningful way that’s going to drive economic enhancements, affordability, as well as youth development, childcare centers, and grocery stores,” Dickens said. “All of the above is how we’re going to invest in and we’re going to bring energy to these spaces, and we’re going to do this development without displacing the current residents. They’re going to see the benefit of these new amenities and activities.”

Two of those partners are the SFI and the Urban League Greater Atlanta. The mission of the SFI is to empower students at participating Historically Black Colleges and Universities (HBCUs) and MSis with programs that drive persistence toward graduation, creating pathways to economic opportunity without the burden of excessive debt. That mission began with a speech from philanthropist Robert F. Smith at Morehouse College’s 2019 graduation, where he paid off the student loan debt for the entire class.

The change that moment sparked is the core principle of what both organizations hope to accomplish for today’s youth: creating resources and a plan to invest in the youth and the communities they live in.

“Yes, there is $1.7 trillion worth of student loan debt. Yes, there are 43 million borrowers. Yes, they even average around $39,000 each, but the problem is that it delays fully funding retirement plans by 71% of those people. 45% of those people also delay buying their first home, starting a family, and having children. It’s the wealth problem. It’s not the student debt problem,” Shoates said. “So our approach was, how do we address this thing we call the wealth gap, and do it from what we call the lens of education?”

Essentially, the three keynote speakers referred to the mission as a “group project,” emphasizing that they couldn’t sustain transformational change without the help of one another. The event concluded with a call to action by Courtney English, the newly appointed chief of staff for the City of Atlanta, making the case for continued investment into communities and specific zip codes, such as the 30318, to decrease the wealth gap and life expectancy gap.

On Sept. 29, 1916, it was front page news that a surge in Standard Oil’s stock price likely made oil tycoon John D. Rockefeller America’s first billionaire.

More than a century later, the United States is home to hundreds of billionaires whose fortunes increasingly come from technology and financial markets. Together, they control a growing share of the country’s wealth — approaching the percentage held by Gilded Age industrialists who built monopolies in railroads, oil and steel.

Here’s what research tells us about America’s billionaire class today.

American billionaires number over 900, according to researchers

There are a few different estimates of the number of American billionaires, but researchers tend to agree that the billionaire class exceeds 900 and is growing.

Forbes, which has produced a list of billionaires since the 1980s, counted roughly 900 in early 2025 — up from 813 in 2024.

Meanwhile, the wealth-data firm Altrata pinned the number of U.S. billionaires at 1,135 in 2024, an uptick from 1,050 in 2023 and up more than 80% from levels in 2016, when they began releasing yearly reports.

And JP Morgan Chase Private Bank estimated the number at roughly 1,990 in 2024 — about 15% more than its 2023 estimate.

Part of the reason estimates vary is that the ultra-wealthy are not required or incentivized to disclose their net worth. The SEC requires investors to report ownership of more than 5% of a company’s shares, but valuations fluctuate with the market, complicating wealth estimates.

Adjusted for inflation, the number of billionaires with a Rockefeller-sized fortune is a much smaller set.

His $1 billion in 1916 would be worth roughly $30 billion today. By that measure, only about 30 American billionaires have a similar fortune, according to Forbes and Bloomberg. Among them are Oracle founder Larry Ellison and Tesla founder Elon Musk, with net worths above $300 billion. Other tech titans also top the list, including Meta CEO Mark Zuckerberg and Amazon founder Jeff Bezos — both with fortunes of over $200 billion each, as of Sept. 29.

Christopher Nichols, a professor of history at Ohio State University said, “The billionaires of the Gilded Age and the multimillionaires were involved in what we think of as blue chip industries, where there are lots of jobs and stuff produced. The billionaires of today’s world are mostly working in tech sectors and places that very often don’t employ many people.”

Billionaires have roughly $6.8 trillion in wealth in 2025

Together, America’s billionaires had an approximate total net worth of $6.8 trillion in the spring of 2025, Forbes estimates, which is a jump of more than a trillion compared to last year after a strong year of growth for U.S. stocks in 2024.

In the 20th century, Scottish journalist B.C. Forbes, who founded the eponymous magazine, wrote that if Rockefeller’s wealth “could be turned into cash and distributed equally—which it couldn’t—[it] would give every man, woman and child in the United States $10 each.”

Today, if that estimated $6.8 trillion held by U.S. billionaires could be turned into cash and divided equally among roughly 340 million Americans, it would amount to about $20,000 per person.

Another way to think about that sum is that it could theoretically be used to buy every NFL team, pay off Americans’ student loan and medical debt and purchase 9 million homes at the current median sales price, with hundreds of billions left over.

The ultra rich own an increasingly large share of the nation’s wealth

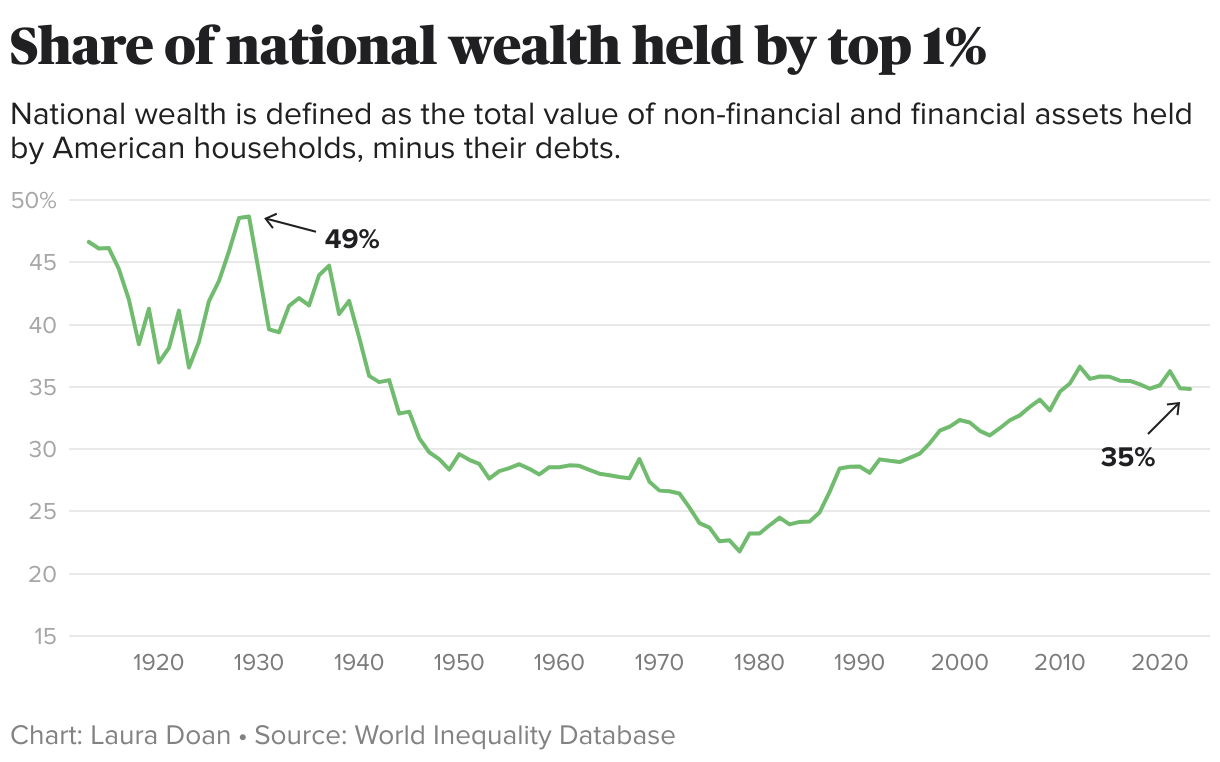

Data from the World Inequality Database shows that the share of wealth held by the top 1% and the ultra-rich top 0.001% has been rising for decades — toward the record levels observed in the Gilded Age.

The share of the national wealth held by the top 1% peaked at nearly 50% in 1929 before tumbling during the Great Depression, according to the data.

“What happened with the Great Depression was that large fortunes were lost in the stock market. And then the New Deal rebuilt the economy around workers and around small businesses,” said Jeremi Suri, a professor of history and public affairs at University of Texas.

But in the early 1980s, the top 1% began regaining ground, as union jobs declined and traditional industries like manufacturing shrunk, according to Suri.

By 2023 the top 1%, or those with over $4.6 million in assets, controlled more than a third of the nation’s wealth — up over 10 percentage points from 1980.

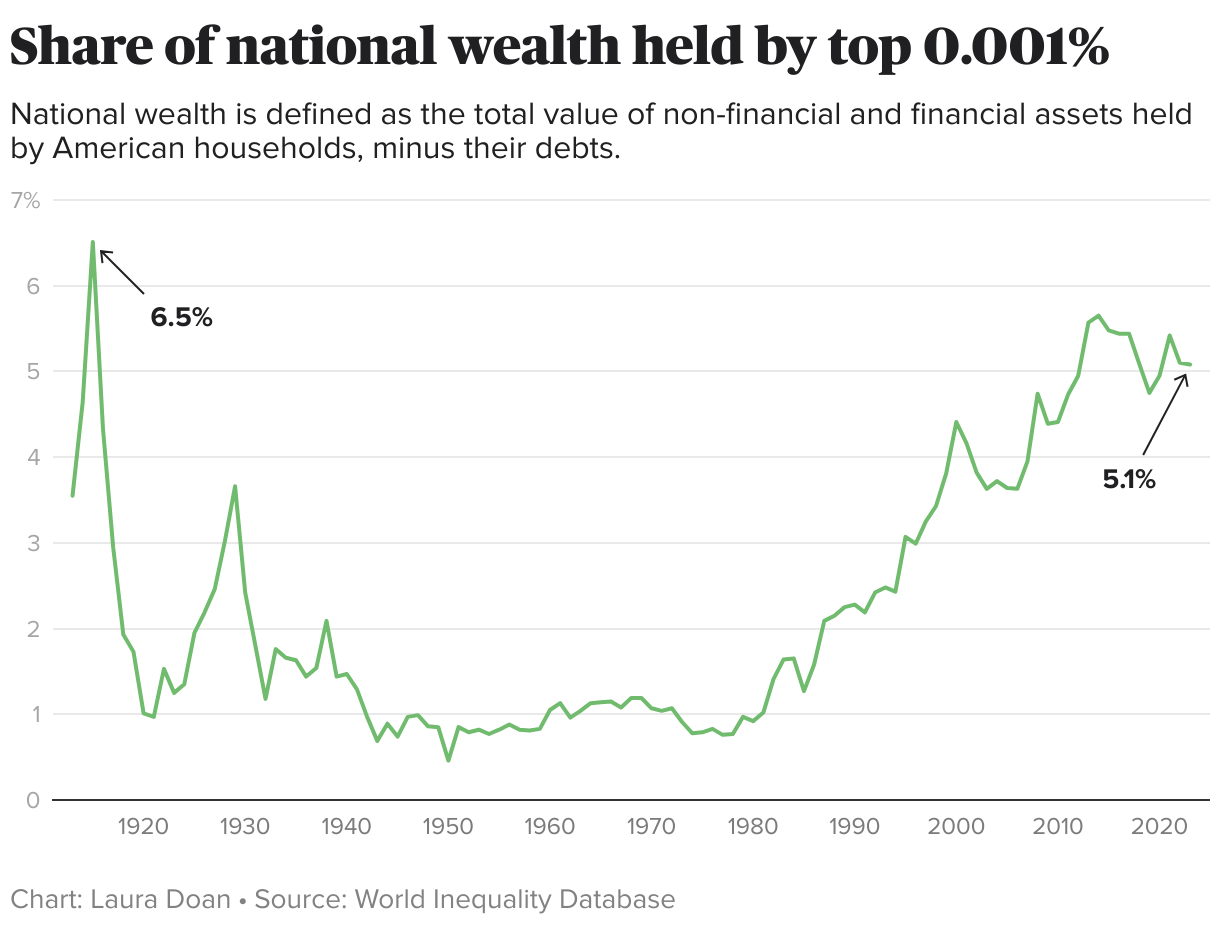

Data collected by the same researchers shows that the trendline looks similar for those in the top 0.001% of people in the country — or those who owned more than $1.5 billion in 2023.

The hundreds of billionaires in this category owned about 1% of the nation’s net wealth in 1980 and 5% in 2023.

Most billionaires are males with self-made fortunes, but a significant number inherited their money

Demographically, the billionaire class still resembles J.D. Rockefeller in many ways.

The vast majority of the world’s billionaires are men — about 86.5% in 2025, according to Forbes — and most make rather than inherit their wealth.

Rockefeller himself was the son of a traveling salesman and a housewife. While his family helped him launch his career, Rockefeller built the majority of his fortune on his own, according to Nichols, an editor of “A Companion to the Gilded Age and Progressive Era.”

“He came from enough middle class wealth that he could get a loan from his dad to start that business, which so often is the story for business folks,” Nichols said. “But he made his billions through his business acumen and hard work, and then also his ruthless competitiveness in an under-regulated time.”

Research suggests inheritance plays a significant role for many wealthy people today. Roughly 30% of the world’s billionaires have inherited their fortunes, according to a 2024 report by UBS, a wealth management company in Sweden. And the share in the U.S. is about a third, according to a Wall Street Journal analysis of Altrata data.

Some of America’s wealthiest heirs include Walmart’s Alice, Rob and Jim Walton, and Jacqueline Mars, who owns roughly one third of the candy giant Mars founded by her grandfather.

Rockefeller and his son gave away a significant amount of their money to charity but it continues to live on. And descendants of the family share a fortune valued around $10.3 billion in 2024.

The rich are different from other people — and that also applies to the share of their income they pay in taxes, according to a new study from University of California, Berkeley, economists.

The individuals who make up the Forbes 400 list, topped by Tesla CEO Elon Musk with a fortune of $244 billion, paid an average effective tax rate of 24% from 2018 to 2020, compared with a 30% rate for all other U.S. taxpayers, the researchers said in a new paper published in the National Bureau of Economic Research.

The research comes as President Trump’s “big, beautiful bill,” signed into law on July 4, delivers its largest benefits to the highest-earning Americans through a mix of new and extended tax breaks. Those include raising the estate-tax exemption to $15 million per person, up from about $14 million.

The changes build on an earlier tax cut — the Tax Cuts and Jobs Act, Mr. Trump’s signature first-term legislation. That 2017 law reduced the effective tax rate for the richest Americans from 30% to 24%, the researchers found.

The new findings — from Berkeley economists and noted inequality experts Emmanuel Saez and Gabriel Zucman — calculates the tax rate by tallying all income taxes, as well as corporate taxes that are paid by the companies owned by the richest Americans. In other words, it assigns a share of Amazon’s corporate taxes to that of Amazon founder Jeff Bezos when calculating his total tax burden.

“The economic income of the wealthiest are essentially the profits of the businesses they own,” Saez told CBS MoneyWatch in an email. “Jeff Bezos owns about 10% of Amazon, and hence his true economic income is 10% of Amazon’s profits.”

Corporate taxes are levies on the profits generated for Bezos, similar to how an employer withholds federal income and Social Security contributions from a worker’s paycheck, he added.

Saez and Zucman are leading proponents of instituting a U.S. wealth tax to help address widening inequality between the haves and have-nots. That idea has been embraced by some lawmakers, such as Senators Elizabeth Warren, a Democrat from Massachusetts, and Bernie Sanders, an independent from Vermont.

Some conservative critics have argued that wealth taxes could be self-defeating, with the Hoover Institute noting in a 2023 blog post that the levy could discourage entrepreneurship and investment.

Research shows that the Tax Cuts and Jobs Act, while cutting taxes for many individuals and businesses, hasn’t had a significant impact on the economy, the Congressional Research Service found in an April report. Republican proponents of the “big, beautiful bill,” such as House Speaker Mike Johnson, also say that it will boost the economy and provide tax relief to workers and families.

How billionaires pay a smaller share

U.S. income taxes are designed to be progressive, meaning that higher-earning workers pay a bigger share of their income to the IRS than people lower down the ladder. But because capital gains — the profits earned from selling stocks, bonds, real estate and other assets —and business income are taxed at a lower rate than the top rate for income that people earn through their jobs, the richest Americans reap a massive tax break.

For instance, the highest tax rate on earned income stands at 37%, which is assessed on every dollar earned above $609,351 for individual taxpayers. Yet that same person will pay only a 20% tax rate on long-term capital gains, such as profits from a stock sale, and a 21% corporate tax rate on income earned through a partnership or other business.

And if the rich don’t sell their shares, they don’t have to pay any taxes on that wealth because they haven’t realized a capital gain, Saez noted.

“The individual income tax is designed to be progressive thanks to its increasing tax rates by brackets, and it does a pretty good job except among the billionaire class,” he said. “As I said, the billionaire class can avoid realizing individual income and hence can escape the individual income tax.”

To be sure, the rich are shouldering the largest share of the nation’s taxes, IRS data also shows. The top 1% of earners – people who make over roughly $663,000 per year — account for roughly 40% of all federal individual income tax, while the top 50% contribute 97%, a Tax Foundation analysis of IRS data shows. The bottom half of income earners account for about 3% of those taxes.

Some wealthy Americans pay a tax rate exceeding the 30% average, the new paper also found. The top labor earners — people who depend on high wages for their incomes rather than capital gains or corporate profits — have a 45% effective tax rate, according to Berkeley analysis.

The findings about the richest 400 Americans suggest that a wealth tax is still needed to curb inequality in the U.S., Saez said.

“The wealth tax is the most direct and powerful way to specifically target the ultra-rich and increase tax progressivity at the very top,” he said. “The wealth tax on the ultra-rich is also popular but will obviously be fought by billionaires, and they have disproportionate influence.”

Aimee Picchi is the associate managing editor for CBS MoneyWatch, where she covers business and personal finance. She previously worked at Bloomberg News and has written for national news outlets including USA Today and Consumer Reports.

Jeff Bezos’ $80M Gulfstream G700: What Does This Purchase Say About Billionaire Spending?

Amazon founder Jeff Bezos recently purchased a new $80 million ride: a Gulfstream G700. This advanced private jet – boasting cutting-edge tech, a spacious cabin, and exceptional range – adds yet another item to the billionaire’s list of millions-worth purchases.

Don’t Miss:

Among this collection are a megayacht worth around $500 million, a $42 million clock in the mountains of West Texas, a $65 million Gulfstream G-650ER (that’s another private jet), and a $23 million mansion – just some of the extravagant purchases Bezos can afford.

Billionaires like Bezos have long been associated with lavish lifestyles – with private jets, superyachts, and sprawling real estate portfolios. According to Business Insider, billionaires can typically afford to spend around $80 million per year.

With a net worth of around $194 billion, the Gulfstream purchase is only 0.04% of Bezos’ wealth. For many, these purchases demonstrate how wide the economic divide is.

Billionaire spending habits frequently gain public attention because they show how significant the disparity between the top 1% and average citizens is. While many Americans struggle to afford basic amenities, don’t have enough saved for retirement, and face increasing financial uncertainty, billionaires like Bezos can afford to spend millions on luxury items.

Critics argue that billionaire spending highlights the wealth gap in the U.S., where the top 1% hold nearly as much wealth as the bottom 90%. Others defend billionaire spending, claiming it stimulates economic growth and job creation.

Bezos’s jet purchase may seem extreme, but it’s part of a larger pattern of wealth distribution. Billionaires invest heavily in purchases like yachts, islands, and art. In 2021, yacht sales increased as billionaires sought privacy and security during the pandemic. The art market also surged, with global sales reaching $64.1 billion in 2019.

Luxury goods industries thrive when high-net-worth individuals seek out these items and make continual purchases. The G700 purchase alone supports jobs, from engineers and manufacturers to pilots and crew.

That’s not to say that billionaires only spend their money on lavish lifestyles, though. Many billionaires are known for their philanthropic efforts. Warren Buffett, George Soros, and Lynn Schusterman give away 20% or more of their wealth, while others, like Bezos and Elon Musk, have given away less than 1% of their wealth.

Despite contributing less than others, Bezos has still made significant charitable contributions. He has pledged $10 billion to fight climate change. However, extravagant purchases like jets and yachts often overshadow these charitable efforts.

For those nearing retirement, the spectacle of billionaire spending can feel distant from your financial reality. However, it highlights important economic trends and questions about wealth distribution that may impact policies affecting retirement, taxation, and financial security.

That being said, talking with a financial advisor can help you navigate your important financial decisions, focusing on the purchases and choices within your grasp and helping you secure your financial future.

Read Next:

“ACTIVE INVESTORS’ SECRET WEAPON” Supercharge Your Stock Market Game with the #1 “news & everything else” trading tool: Benzinga Pro – Click here to start Your 14-Day Trial Now!

LOS ANGELES, December 14, 2023 (Newswire.com)

– Snowball Wealth is proud to announce the launch of a bilingual financial education program with Lynwood Unified School District in Los Angeles. This initiative marks a significant step towards equipping high school students with vital financial knowledge and skills in both English and Spanish.

“As first-generation college graduates, my co-founder Pamela Martinez and I understand the challenges these students face,” said Tanya Menendez, CEO of Snowball Wealth. “Our program is designed to provide them with the financial skills that we wish we had learned at their age.”

The program covers essential topics such as banking, credit, investing, and comprehensive college readiness. A special emphasis is placed on guiding students through the Free Application for Federal Student Aid (FAFSA) and providing crucial information about the Deferred Action for Childhood Arrivals (DACA) program.

“Our students, a significant number of whom are first-generation and 96% who would be the first in their families to go to college, face unique financial challenges,” stated Patrick Gittisriboongul, Assistant Superintendent of Lynwood School District. “This program is an essential tool in helping them navigate their financial futures confidently.”

A key component of the curriculum is the college readiness course, which includes strategies on selecting a college, financing higher education, and opportunities to attend college for free. This course aims to demystify the college experience for students and their families.

Miram Casuso, a teacher working closely with Snowball Wealth, is deeply invested in the students’ well-being. “Our goal is to empower students with the financial knowledge that can transform their lives,” shared Miriam Casuco. “Financial literacy is more than just numbers; it’s about shaping futures.”

Snowball Wealth is complementing digital resources with in-person workshops, ensuring an engaging and comprehensive learning experience. These workshops are designed to actively involve students in their financial education journey.

Pamela Martinez, CTO at Snowball Wealth, emphasized the program’s significance. “We’re committed to bridging the financial literacy gap. This initiative is a crucial step in preparing students for a successful future, both in college and beyond.”

Recognizing the widespread need for financial literacy education, Martinez invites educators to join the program. “We are opening a waitlist for educators interested in bringing this transformative program to their schools. Teachers who wish to participate in our bilingual financial education initiative can sign up via our website. By signing up, educators can stay informed about the program’s development and receive early notifications about when it becomes available in their district.”

As Snowball Wealth’s bilingual financial education program continues to grow and make an impactful difference in the lives of students, it is seeking to expand its network of partners and sponsors in 2024. Banks, financial institutions, and other organizations interested in collaborating can find more information by visiting snowballwealth.com/partnerships.

America has failed its least wealthy citizens—and “insulting” those with opposing political views isn’t going to make things better, according to JPMorgan CEO Jamie Dimon.

Speaking at the New York Times DealBook Summit on Wednesday, the Wall Street veteran called on people of all ideological views to do what they can to prevent another Donald Trump presidency.

“If you’re a very liberal Democrat, I urge you: help Nikki Haley,” he said. “Get a choice on the Republican side that might be better than Trump.”

Asked whether he believed the best outcome for the election was “anyone but Trump,” Dimon responded: “I would never say that.”

“He might be the president, I have to deal with that too,” he joked—but he noted that he didn’t mind criticizing whoever ends up in the Oval Office.

Stop slamming MAGA movement, Dimon says

While he made it clear he wasn’t the biggest fan of Trump returning to office, Dimon urged Americans on Wednesday to put aside some of their ideological differences and look for the nuance in others’ political beliefs.

“We should stop talking about ultra-MAGA,” he insisted. “I think you’re insulting a large group of people, and making this assumption, scapegoating—which the press is pretty good at too—that these people believe in Trump’s family values and are supporting the personal person. I don’t think that’s true.”

A lot of the support for Trump’s so-called MAGA (“Make America Great Again”) campaign, Dimon argued, came from specific things he had called out or achieved during his presidency.

“I think what [supporters are] looking at is the economy was pretty good—the Black community had the lowest unemployment rate ever in his last year,” he said. “He wasn’t wrong about China. He wasn’t wrong about NATO. He was wrong about the misuse of the military. So that’s why—they’re looking at that.”

He called on people to do what they can to consider why people take opposing views. For Democrats, he suggested reading the work of conservative columnist George Will, while he said Republicans ought to look up the work of Pulitzer winning columnist Thomas Friedman.

“We should get out of this [idea that] it’s one way or the other,” he said. “I’m not mad at people who are anti-abortion. If you believe in God and that conception starts at the moment of birth, you are not a bad person. I think people need to stop denigrating each other all the time because people take a point of view that is slightly different than yours. We’re a democracy—people should vote and solve some of these issues, and they won’t always be what you want.”

However, he made it clear on Wednesday what he would have done differently to former president Trump or incumbent candidate Joe Biden.

“We’ve done a terrible job taking care of our bottom 30% of earners,” he said, telling the audience: “You all are wealthy and have money, but their average, their average wages are [low].”

“They’re the ones who lost their job in COVID,” he added. “They’re the ones who are dying five or six years younger than the rest of us. They’re the ones who don’t have medical insurance. They’re the ones whose schools don’t work, and they’re the ones dealing with crime. What the hell have we done as a nation?”

Insisting that “we need to fix it,” the JPMorgan chief said the U.S. needed better immigration, education and infrastructure policies—and he pledged to do what he could to help make that a reality.

“Whoever’s president, I’m going to try to help do the best job possible,” he said, before sharing an anecdote about his wife and daughters criticizing him for going to the White House years ago to meet with then-president Trump.

“I will walk into that oval office trying to help whoever is the president of the United States to do a better job for our people,” he added. “I don’t agree with a lot of things [Trump] does… [but] I couldn’t imagine saying ‘I’m not going to go into the White House because of who’s there.’”

Tax the rich, help the poor

During the DealBook Summit talks, Business Insider reported that Dimon was also asked by audience member and billionaire hedge funder Bill Ackman—who once urged the JPMorgan CEO to run for president—what he would hypothetically do if he were to be elected president of the United States.

He said he would start by building a cabinet of “really smart, talented brainy people” that included both Republicans and Democrats, before tackling education, immigration and “doubling down on diplomacy.”

Dimon—who has a personal net worth of $1.8 billion, according to Forbes—also said presidents should have an economic growth strategy that included “proper taxation” policies, adding that he would double the earned income tax credit for low earners “tomorrow.”

“I’d make people like you pay a little bit more,” he also told Ackman. “This carried interest stuff would be gone the day I got in office because it is unfair.”

The carried interest loophole—which Ackman has previously slammed as a “stain on the tax code”—allows private equity and hedge fund managers to lower their tax bill on profits from fund investments.

Get the business news that matters most to you with our customizable digest, Fortune Daily. Register to get it delivered free to your inbox.

Opinions expressed by Entrepreneur contributors are their own.

Philanthropy and government programs have been trying to close the racial wealth gap for a long time, but they’ve been focused on band-aids when we need ladders. While the wealth gap is fueled by several contributing factors, including disparity in home ownership, accumulation of financial assets and strong growing wages, as small business investors, we can draw our attention to a core piece of the problem: the wage gap.

Let’s take a moment to clarify what we mean when we talk about the wage gap as it relates to the racial wealth gap. We are not just talking about good-paying jobs for people of color. We really need good-paying jobs that provide a clear pathway for Black and Brown employees to build a stronger, sustaining financial future.

The typical white U.S. household has nearly eight times the wealth of the typical Black household. To address the systemic issue of racial wealth inequity, the private sector must do what it does best – invest in great companies and entrepreneurs that create quality jobs –and ensure all workers, especially Black and Brown workers, have an equal opportunity to build a lasting, positive economic reality for themselves and their families.

Media reported widely that recent pandemic aid cut U.S. poverty to a new low, but that was a short-term solution to a global crisis — it wasn’t aimed at driving wages higher in perpetuity. As that funding source dries up, those in a lower economic bracket return to the same or even worse circumstances than they were at the start. To truly attack the racial wealth gap, we need the private sector to make the change that the government and non-profits simply cannot do independently.

Private sector employers and investors often can’t see how they can drive the change needed to give Black and Brown Americans access to wealth-creation opportunities while growing businesses and pleasing investment partners. But it is not as hard as they may think, and the benefits to their business and community deliver a long-lasting ROI for companies, workers and families.

Building a path to financial security starts with strategic wages

For decades, wages for Black and Brown workers have lagged behind those of white workers with the same experience and education, even in the same geography Even when people of color climb the corporate ladder, they make less — 97 cents on the dollar.

These communities need more than just a living wage; they also need opportunities for long-term career development, pay parity and wage progression. A rising wage promotes economic stability, helps workers provide for their families and facilitates wealth accumulation for future generations.

Wage progression — whether linked to individual performance, company performance, tenure, skills development, or promotion — is also good for business. It helps attract the best employees, improves retention, and sustains and incentivizes business growth.

The role of benefits in building generational wealth

Meaningful benefits are a major piece of increasing sustainable employee wealth. Most employee wealth is derived from workplace benefits packages: health insurance, 401ks, stock options, etc. Low-wage workers typically don’t have those options, which are key to building generational wealth.

Business leaders and investors can change this situation by learning from employees what benefits and opportunities would make the greatest difference in their lives and free up income for saving and investing– be that affordable healthcare, child/eldercare support, or direct wealth creation through incentivized savings opportunities like 401k plans, IRAs, and employer matching savings programs.

Offering these types of household-stabilizing benefits could largely pay for themselves in terms of lower absenteeism, greater productivity, increased retention and worker-driven competitive advantage.

Help employees continually grow their skills

Too often, the leadership potential and training of Black and Brown Americans is overlooked. According to McKinsey, Black workers are disproportionately concentrated in entry-level jobs with low pay and underrepresented in leadership and executive positions.

Correcting this divide means providing entry-level workers with access to training and development opportunities from the moment they are hired. Programs that teach employees valuable skills for remaining relevant in their careers to prepare them for higher responsibilities while reducing turnover, improving engagement and accelerating business growth.

Making it happen

Investors typically provide small businesses with growth capital, but they can also provide operational capital that is invested directly in employees. Business leaders, their investors and advisors can collaborate to devise a feasible and ambitious plan that establishes measurable goals for the company and the impact company leaders aim to achieve by driving an innovative wage strategy.

Furthermore, it is crucial to monitor and evaluate outcomes using meaningful metrics. Failing to measure outcomes from these changes means businesses will not know what they’ve really achieved, which keeps them from continuous improvement.

I believe that every employer and their investors have a moral imperative to make closing the racial wealth gap a focal point of their business model, even if it means taking a little less for themselves and other executives off the bottom line. There is a tremendous opportunity to hire workers from disadvantaged communities and grow and sustain a strong workforce that helps grow all businesses. In return, employees would benefit from quality jobs and greater economic vitality now and in the future, setting up the next generation for even greater progress.

It’s about doing something incredible and making work “work” for businesses and employees alike. This type of investment is the catalyst for the change we need in our business world and our society —but it can’t happen without the private sector and its leaders driving the charge.