In one week in April, Metro Credit Union received more than 450 fraudulent account opening applications.

Using manual processes, fraud and digital teams at the Boston-based, $3 billion credit union worked overtime to fend off a series of attacks that Chief Operating Officer Traci Michel believed was enabled by generative AI tools.

Photo by CanStock

“We’re getting it from all sides,” Michel told Bank Automation News. “When you see that type of volume coming into a platform, you have to imagine that there’s some type of computer-generated frequency that’s happening behind the scenes.”

Through informal conversations with colleagues at other financial institutions, Michel discovered that her peers were falling victim to the same attacks.Seventy percent of financial institutions reported losses of over $500,000 to fraud in 2022, according toAlloy’s State of Fraud Benchmark Report.

“The pattern was extremely similar,” she said. “[But] we didn’t have a tool that would help us try to interface and understand whether we were the only financial institution.”

Solutions for smaller FIs

Facing scaling fraud operations, Metro Credit Union turned to anti-fraud platform FiVerity, one of several companies using data collected from a group of member institutions to build records of blacklisted accounts and concerning patterns.

FiVerity opened its Digital Fraud Network in June to more than 100 small and medium-sized businesses for free, according to a release. Other clients include Grasshopper Bank, BHG Financial, and Digital Federal Credit Union.

“Some of the other vendors are going after the larger institutions,” FiVerity Chief Executive Greg Woolf told BAN. “Our focus has really been on the community banks and credit unions, and some of the smaller fintechs… who typically don’t get access to this level of technology.”

FiVerity also launched its Anti-Fraud Collaboration Platform in June, building on its existing network to offer new features to members, according to a release.

The Boston-based company, which raised $4 million in seed funding in April, uses machine learning and data from its members to draw insights and identify fraudulent users in real time, according to its website. Features of its Anti-Fraud Collaboration Platform include an explanation of its risk scoring system that enables customers to see why specific accounts were flagged, Woolf said.

It’s “providing a fraud score, but also providing transparency,” he said. It could be that “the Social [Security number] was used by somebody else, or another institution reported this address was linked to a crime rate… or other elements that could come off the dark web.”

FiVerity has worked with federal regulators, including the Federal Reserve and the Financial Crimes Enforcement Network, that have supported collaboration and promoted equity by encouraging service offerings to smaller FIs, Woolf said.

But bringing together FIs of a similar size and in the same region is also practical, as these institutions often face similar fraud threats, according to Woolf, who referenced an incident in which fraudsters in Maine targeted every financial institution with a branch on the main street of a single town.

“There’s a natural clustering, and that actually helps our models be more effective,” Woolf said, noting a 45% improvement over previous models by focusing on a specific demographic of FIs.

Metro Credit Union hopes that as more FIs join FiVerity’s consortium, the collaboration will help every member fight fraud.

“We’re very excited about the expansion on the client side, because it’s strength in numbers for us,” Metro’s Michel said. “The more financial institutions that are participating into the network and feeding their fraudulent application information, the more we can all benefit.”

A crowded market

Meanwhile, other fintechs have recently announced their own consortiums catering to larger clients.

Anti-fraud fintech Sardine announced its coalition, SardineX, in June to bring together major players from multiple verticals in a similar data-sharing arrangement.

“The way we are going to solve fraud in financial services is to share it across financial services,” SardineX President RaviLoganathan told BAN,adding that the company believes the industry should“not have the silos for fraud data sharing only for banks, and fraud data sharing only for fintechs.”

SardineX’s founding members include card issuer Visa, Williamsburg, Va.-based Chesapeake Bank and cryptocurrency platform Blockchain.com, according to its website.

The week before the Sardine announcement, data transfer fintech Plaid announced its consortium, Plaid Beacon, which focuses on building an after-the-fact fraud database rather than providing real-time insights. Founding members include credit card payment company Tally, buy-now, pay-later provider Uplift and Veridian Credit Union.

With more players entering the market, Metro’s Michel believes competing consortiums may need to work together to offer the best results for members.

“Competition just bears out that there will be multiple providers in the market,” she said, adding that she hopes to see “common data frameworks” used by Fis in the future.

Square has teamed up with American Express to launch business credit cards to its customers. The launch is in beta phase with an unknown number of Square’s merchants using the card. The credit card takes additional data points into account, like a business sales processed through Square’s platforms or a business’s credit score, to determine credit […]

London-based open banking startup Volt is looking to expand global operations with a $60 million series B round. The additional funds were announced by the company this month. Founded in 2019, Volt is seeking to create a global real-time payments system by uniting various open payments networks onto one platform, according to its website. “[With […]

Visa is launching cross-wallet transactions platform Visa+ this summer, and PayPal, Venmo and TabaPay will be among person-to-person payment apps integrated into the platform. Visa+ aims to improve interoperability across payment apps and introduces a new payment credential to send funds from one wallet to another, Yuwa Ikhinmwin, director of global partner solutions at Visa, […]

Payments giant Visa and open-banking platform Tarabut Gateway are coming together to develop products and solutions through open-banking technology. “Together with Visa, we will leverage our data infrastructure to bring new and improved products to customers,” Abdulla Almoayed, chief executive of Tarabut Gateway, said in a release. The pair will focus on delivering solutions for […]

Santander Bank tapped earned wage access fintech DailyPay to offer its commercial banking clients an on-demand payment method. Earned wage access (EWA) is a benefit that Santander commercial clients can offer their employees, specifically in the state of today’s economy and inflation, Rob Nardelli, director of commercial banking and business development at DailyPay, told Bank […]

Visa is teaming up with PayPal and Venmo for its new Visa+ service to allow customers to move money between more person-to-person digital payment apps. The Visa+ pilot uses personalized payment addresses linked to PayPal and Venmo accounts to allow users to send payments without using a card, according to a Visa release. “Consumers continue […]

E-commerce and embedded payments continue to gain popularity as millennials and Gen Z consumers look to social media for shopping experiences — and banks must meet their customers where they are shopping online. “Facebook, Instagram, TikTok users — 50% of them say they will make a social media purchase in 2023,” Allie Chafey, innovation senior […]

The collapse of Silicon Valley Bank is having a trickle-down effect on fintechs and banks within the financial services industry, but Cross River Bank is not one— in fact, the bank is swooping in to capture business amid the fall of its competitors. For example, the $9.2 billion Ft. Lee, N.J.-based bank was selected by […]

Oklahoma City-based First Fidelity Bank launched a banking as a service solution (BaaS) Tuesday in development with global payments and banking infrastructure fintech Episode Six. The solution supports embedded finance with low cost, quick to deploy architecture and real-time payment offerings, according to an Episode Six release. “Through a common ledger, we are able to […]

Digital wallet company Wedge is teaming with Visa to launch a debit card within Visa’s network in the U.S. using Wedge’s card technology. Austin, Texas-based Wedge’s card allows users to liquidate their assets — including stocks, ETFs and crypto — to pay for goods and services, according to the company. “We are always looking for […]

London-based fraud prevention fintech SEON has acquired anti-money laundering software company Complytron for an undisclosed amount. The deal has been in the works since April 2022, as SEON aims to improve its compliance and screening capabilities, SEON Chief Executive Tamas Kadar told Bank Automation News. “A lot of companies, especially given the current [macroeconomic conditions], […]

Financial institutions looking to modernize their internal systems in 2022 have often turned to fintech acquisitions or partnerships for cloud computing, digital banking, robotic process automation, payments capabilities and more. Here are Bank Automation News’ five most-read transaction stories of 2022: 1. Envestnet acquires business intelligence firm Truelytics Wealth management giant Envestnet acquired business intelligence […]

Ryan McInerney will become chief executive of Visa effective Feb. 1, 2023, replacing current CEO Alfred Kelly, who is stepping down from the role he has held since 2016. McInerney has served as president of the credit card giant since 2013. “Ryan has boundless energy and passion for this business and in his role as […]

This is an opinion editorial by Stanislav Kozlovski, a software engineer and macroeconomic researcher.

Many Bitcoiners have heard of Bitcoin’s “lack of scalability” — it is one of the most common critiques waged against the project by both gluttonous cryptocurrency competitors and incumbent establishment actors.

Some oldtimers may remember the heated, bathed-in-controversy Blocksize Wars of 2015 to 2017 which, aided by industry insiders, most shallowly aimed to make Bitcoin scale to more transactions by increasing the maximum block size and by doing so, almost set precedent and changed Bitcoin’s future course forever.

Both of these issues will ultimately prove to be left on the wrong side of history. In this piece, we are going to show how the Lightning Network addresses Bitcoin’s scalability problems and undoubtedly proves that the small-block decision was ultimately the right one.

Base Layer Limitations And Choices

Before we understand what the Lightning Network is solving, we should first understand what the inherent problem is. Simply put: You cannot scale a blockchain to validate the entire world’s transactions in a decentralized way.

Source: Author

Blockchains suffer from an inherent limitation which forces them to trade off between three qualities — one quality of their system has to go for the other two. As pictured above, a blockchain can only reliably have two of these three qualities:

Decentralized: not controlled by any single party or a small number of elites

Scalable: scale to a sufficient number of transactions

Secure: not be easy to attack and break its invariants

It is worth noting that all of these characteristics sit on separate, complex spectrums. For example, you don’t become “secure” over a certain threshold, it is very dependent on the use case and many different characteristics.

Bitcoin is slow for a reason. It explicitly picked to optimize the “security” and “decentralization” sections of the trilemma, leaving “scalability” (transactions per second) on the sideline.

The key realization is that, much like today’s internet and financial system, it is more optimal to comprise the whole system of separate layers, where each layer optimizes for and is used for different things.

Bitcoin, the base layer, is a globally-replicated public ledger — every transaction is broadcast to every participant in the network. It is evident that one cannot practically scale such a ledger to accommodate the entire world’s growing transaction rate. Apart from being impractical and privacy damaging, its drawbacks vastly outweigh its insignificant benefits.

Back in the day, there was a major civil war between the online community in what Bitcoin should do to increase its transaction throughput capacity. There is major, infuriating controversy in this story and is in large part what shaped Bitcoin to remain what it is today — a grassroots, bottom-up movement where the average people (plebs), in aggregate with one another, dictate the rules of the network.

“The Blocksize War” by Jonathan Bier illustrates the battle between the decentralized network supporters wanting what’s best for the long-term viability of the network and the greed and propaganda perpetuated by major players and corporations to further their own power-gaining and profit-seeking agendas.

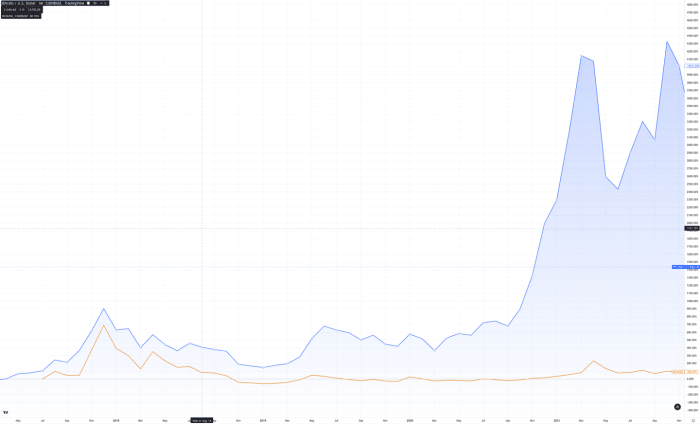

Long story short, Bitcoin was forked into a failed fork named “Bitcoin Cash.”

Bitcoin (blue) price compared to Bitcoin Cash (orange). The fork can be seen at the start of the chart. Source: tradingview.com.

The little guy eventually won — Bitcoin did not rush any bad design choices that would come to compromise its decentralization, security or censorship resistance. The decision was effectively made to scale Bitcoin through layers, introducing second layers that work separately from Bitcoin and checkpoint their state to the main, slower-but-more-secure network.

In stark contrast, the evidently-unsuccessful fork Bitcoin Cash sacrificed all hopes of decentralization by increasing its block size to 32 megabytes, 32 times more than Bitcoin, for a mere maximum of 50 payments per second on the base chain.

Block Size

Each Bitcoin block has a cap on its size and this denotes the upper bound on how many transactions can exist inside of a block. If demand grows to outpace the amount of transactions a block can have, the block becomes full and transactions get left unconfirmed in the mempool. Users begin to outbid each other via the adjustable transaction fee in order to have their transaction be included by the miners, who are incentivized to choose the highest-paying transactions.

A naive solution to this would be to simply increase the block size limit — that is, allow more transactions to be included in a block. The negative side effects of this are subtle enough that even intellectuals like Elon Musk make the mistake of suggesting it.

Increasing the block size has second-order effects which decrease the decentralization of the network. As the block size grows, the cost to run a node in the network increases.

In Bitcoin, each node has to store and validate each transaction. Further, said transaction has to be propagated to the node’s peers, which multiplies the network’s bandwidth requirements for supporting more transactions. The more transactions, the more the network’s processing (CPU) and storage (disk) requirements grow for each node. Because running a node yields no financial benefits, the incentive to run one disproportionately decreases the more costly it is.

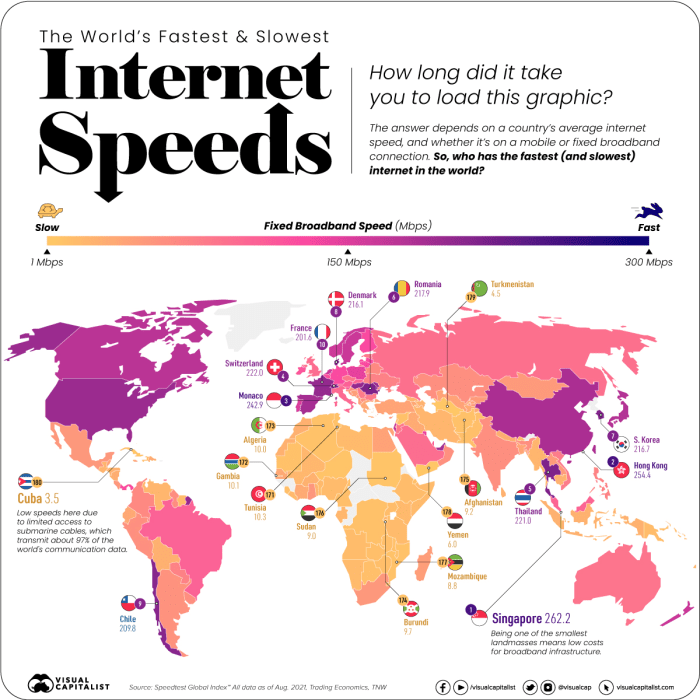

To put it into numbers, if Bitcoin is to ever scale to Visa’s purported peak capacity levels (24,000 transactions per second) a node would need 48 megabytes per second just to receive the transactions over the network. The following is a map showing the average internet speed in the world:

As you can see, a massive part of the world’s average speed would exclude them from the ability to run a node under these conditions. Note that average speed implies that many are even lower than said threshold. Additionally, it doesn’t account for the fact that a user would have other uses for their bandwidth — few selfless people would dedicate 50% of their internet bandwidth for a Bitcoin node.

More importantly, the amount of data this would generate would make it impossible for anybody to practically store it — it would result in 518 gigabytes of data per day, or 190 terabytes of data a year.

Further, spinning up a new node would require one to download all of these petabytes of data and verify each signature — both of which would make it so that a new node would take a long time (years) to spin up.

And to make matters worse, 24,000 transactions per second doesn’t make for a truly unique global payments network in and of itself. Visa isn’t the only payments network in the world, and the world is growing more interconnected every day.

Lightning Network 101

The Lightning Network is a separate, second-layer network that works on top of the main Bitcoin network. Simply said, it batches Bitcoin transactions.

To access it, you need to run your own node or use somebody else’s. The network has two concepts worth understanding for the purposes here:

A Lightning node: separate software that communicates with each other and constitutes a new peer-to-peer network.

Channels: a connection opened between two Lightning nodes, allowing for payments to flow between them.

A channel is literally a Bitcoin base layer transaction, anchoring the channel to the secure chain.

Once two nodes open a channel between one another, payments start flowing between them. Each subsequent payment modifies the channel’s state, cryptographically revoking the old one and checkpointing the new one in memory and on disk of both nodes, but critically, not to the base chain.

Channels can and in my opinion ideally should stay open for a long time (e.g., a year or more). If the nodes ever decide to close down their channel, their latest balance after all the off-chain payments is restored to their original wallets. This is cryptographically-secured by hashed timelocked contracts (HTLC) and digital signatures, which we won’t get into detail for the purposes of this article.

This allows one to batch billions of payments into two on-chain transactions — one for opening the channel and one for closing it. Once a payment is complete, it is indisputable what the latest balance is between all parties (assuming nodes redundantly store their channel checkpoints).

Critically, one need not be directly connected to another party in order to pay them — channels can be used by other nodes in the network in order to increase their reachability. In other words, if Alice is connected to Bob and Bob is connected to Caroline, Alice and Caroline can seamlessly pay each other through Bob.

Lightning Scalability

As we will now prove, the Lightning Network already scales to support 16,264 transactions a second today and therefore solves the scalability problem while preserving all the benefits Bitcoin has to offer — permissionlessness, scarcity, user sovereignty, portability, verifiability, decentralization and censorship resistance.

For a payment to make its way through the network, it typically has to go through multiple payment channels. To answer how many payments the network can do in a second, we need to understand how many an average channel supports.

Statistics show that the average payment goes through around three channels.

The benchmark numbers we will use for this analysis have per-node throughput capacity, not per-channel. Therefore, we will inaccurately assume that each node has just one channel. The default LND node is said to be able to do 33 payments per second with a decent machine (8 vCPUs, 32 GB memory) according to the benchmark.

With 16,266 nodes in the network (as of November 2022), assuming each payment has to go through three channels (four nodes), the network should be able to achieve around 134,194 payments per second.

That is, each payment has to go through a group of four nodes, and there are 4,066 such unique groups in the network. Assuming each node can do 33 payments a second, we multiply 4,066 by 33 to reach 134,194.

Now, to be realistic: Not every node is running a machine like the one in the benchmark — many are simply running on a Raspberry Pi. Thankfully, it doesn’t take much to be able to beat the current payment systems.

Lightning Vs. Traditional Payments

Finding authentic numbers about the peak capacity of traditional payment systems is hard, so we will rely on their average payment rate throughout the 2021 financial year. We will compare that to the theoretical capacity of Lightning, because conversely, getting the average rate of payments in Lightning is impossible due to its private nature, and is also not revealing of capability because the demand for Lightning payments is still relatively low. This comparison will give us an idea of how many payments a Lighting node needs to be capable of routing in order to out-compete traditional finance.

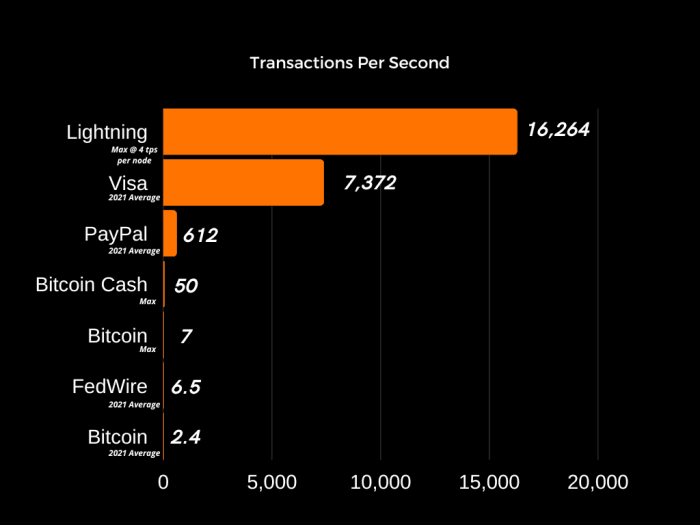

The numbers are promising — it takes each Lightning node to be capable of doing just four payments a second in order to beat the current payment networks by at least two times. At that rate, 4,066 unique four-node groups can achieve 16,264 payments per second — 2.2 times that of the largest competitor, Visa.

Source: Author

To make matters worse for traditional payment networks, the average Lightning transaction fee is 13 times less that of Visa — 0.1% compared to 1.29%.

It’s worth remembering that one could always continue to scale the Lightning Network by creating new nodes. Since it is peer to peer, its scalability is theoretically unlimited as long as nodes in the network grow.

Further, the aforementioned benchmark by Bottlepay makes the case that there are no real technical blockers for Lightning node implementations to eventually reach 1,000 payments per second. At such a number, the network’s current throughput would be closer to four million per second, not to mention what it would be with an increase in the number of nodes.

And lastly, it is worth remembering that the Lightning Network is still very much immature software and has a fair amount of future optimizations to be done, both in the protocol and its implementations. Resources in terms of developers are the only short-term constraint to increasing scalability, which has rightfully come second to more important matters like reliability.

In this piece, we exposed all of the negative drawbacks of scaling the Bitcoin blockchain through increasing the base layer’s block size, most notably severely compromising its decentralization and ultimately failing to achieve its aim of reaching the immense scalability needed for the demands a global payments network has and will continue to increasingly have in the future.

We showed that the Lightning Network, as a second-layer solution, most elegantly solves the scalability problem by both preserving all of Bitcoin’s benefits while at the same time scaling it way beyond what any base-layer solutions promise.

This is a guest post by Stanislav Kozlovski. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

Recently, PayPal released an update to its terms of service that said it would fine people using its service for spreading disinformation. It faced an immediate free speech backlash on social media. Former PayPal President David Marcus tweeted this policy was against everything the company believed. He seemed to think it was “insanity” for payment companies to refuse service “if you say something they disagree with.” Elon Musk tweeted his agreement.

The company quickly reversed itself, saying the release was a mistake.

But the controversy led libertarian lawyer Eugene Volokh to look more carefully at PayPal’s terms of service and he was horrified to discover that PayPal has a long-standing acceptable use policy that forbids “the promotion of racial intolerance or other forms of discriminatory intolerance.” As a good First Amendment lawyer he pointed out that “sharply criticizing a religion or government officials could be construed as the promotion of hate—and could theoretically violate that policy.” To protect himself from this danger and to protest this form of censorship he closed his PayPal account and urged others to do the same.

Good luck finding an alternative. The reality is that payment companies have always had acceptable use policies, and for good reason.

For one thing, they have legal responsibilities to stop money laundering and terrorist financing. So, they have to know who their customers are and what they are spending their money on. They also have a specific legal obligation to block unlawful internet gambling transactions. Payment companies also have policies against the use of their systems for illegal transactions and most of them take special precautions against copyright violations and child porn.

Beyond these legal issues, payments systems restrict who they do business with for ethical and brand reasons. Amex doesn’t allow its services to be used by pornographers, even though pornography is protected by the First Amendment. Neither do Stripe, Amazon Pay, or Square.

Visa and Mastercard allow their member banks to provide service to legal pornography merchants, but they also allow the banks to refuse this business and many of them do. This tolerance has its limits, however. The payment networks recently cut ties with Pornhub after revelations that it didn’t do much to control depictions of rape on its site.

Both payment systems have broad brand protection clauses in their contracts with merchants and banks. They can withdraw service from “brand-damaging” transactions and reserve the right to unilaterally define what those transactions are.

Some of these payment company restrictions seem idiosyncratic, to say the least. Amazon Pay, for instance, won’t pay for “occult services.” So, witches and warlocks stay away!

But many of them seem right. In particular, the bans on hate speech that mimic PayPal’s. Amazon Pay prohibits “hate literature.” Square rejects “hate or harmful products.” Swipe bans a company or individual “that engages in, encourages, promotes or celebrates unlawful violence toward any group based on race, religion, disability, gender, sexual orientation, national origin, or any other immutable characteristic.”

Visa and MasterCard could ban such merchants under their brand-protection programs, even without an explicit prohibition. What reputable business would want to be associated with companies or groups promoting hate speech? Responsible payment card companies flee contact with such people and they are right to do so.

Of course, enforcement can often be controversial. In 2019 PayPal applied its policy against hate speech to Gab and Infowars, which brought cries of censorship from conservative activists. But displeasing some critics comes with the territory. Controversies over standards enforcement are an inevitable part of being in the payment business.

I talked about these issues with former general counsel for the National Security Agency and current partner at Steptoe & Johnson LLP Stewart Baker on his October 17 Cyberlaw podcast (around 32:40). He’s more suspicious of payment card hate speech standards than I am but we agree that a good step forward would be transparency. Payment card companies should be required to disclose their standards, explain their disconnection decisions, and provide adequate opportunities for challenging them.

Laws providing for this kind of transparency for social media companies are already on the books in some U.S. states and in Europe. Existing financial regulations should be supplemented to require similar transparency rules for payment card companies, to be enforced by the powerful regulators that already supervise financial institutions.

Transparency has another advantage. It can reveal behind-the-scenes government pressure on card companies to withhold service. This apparently happened in December 2010 when Wikileaks began to release the contents of confidential diplomatic cables. Senator Joe Lieberman, then-Chair of the Senate Homeland Security Committee, publicly called for card companies to disconnect Wikileaks. But PayPal said that it received secret pressure from the State Department. Visa, MasterCard, and PayPal soon suspended Wikileaks’ accounts.

Government agencies should not exert shadowy pressure on payment companies to disconnect disfavored companies and groups. A little sunlight on such hidden agency nudges would be a good disinfectant and transparency requirements would provide it.

NEW YORK, February 17, 2021 (Newswire.com)

– During the coronavirus pandemic, everyone felt helpless. There was no basic information regarding safety and security, no clear rules to follow, and significant uncertainty about the future. But as successful New York City immigration attorneys, Min Chan and Sumaiya Khalique also know that immigrants feel that same helplessness every day. That’s why they created Immigration Map (IM), a simple way for immigrants and employers to navigate the dense bureaucracy that is the United States Citizenship and Immigration Services (USCIS). IM assists and empowers its members to navigate the complex immigration process with confidence.

IM knows where its members want to go and how to get them there.

IM’s founders are both immigrants, and children of Asian immigrants, who remember their own parents being frightened of a system they didn’t understand. While moving to America remains a powerful draw for many seeking legal and economic stability, one false move and immigrants can lose everything. “The best advice we can give immigrants is to carefully analyze, build and complete your visa or Green Card application before you file with USCIS,” says Min Chan. And IM can help.

Analyze, Build, and Complete an Immigration Petition

IM takes an individual from start to finish and turns their American Dream into reality. The three-step Analyze, Build, and Complete process is as simple as ABC. Immigrants can analyze their situation, build their case, and then complete and submit their petition to USCIS confidently.

How is IM different from LegalZoom or Rocket Lawyer? With 30 years of combined experience, two attorneys provide more than downloadable forms members can struggle through; IM gives its members complete control over their immigration journey. IM is transparent with its services, where its information comes from, and what it offers in the monthly subscription and its legal help with attorneys. The DIY technology and three-step Analyze, Build, and Complete process with IM will clearly outline what its members need, what its member should prepare for, and what its members never even considered.

A veteran immigration consultant noted that there has been a sharp increase in interested entrepreneurs and professionals who are looking to move to Singapore as Hong Kong’s political future remains uncertain.

Press Release –

updated: Sep 12, 2019

SINGAPORE, September 12, 2019 (Newswire.com)

– Amid a volatile political climate, Hong Kong-based entrepreneurs and professionals are looking to migrate their businesses and careers to another Asian powerhouse.

According to One Visa Immigration Consultant Cheng King Heng, there has been “200% increase” in inquiries about migrating to Singapore, mostly from workers and business owners who are currently based in Hong Kong. The heightened interest is driven by the uncertainty of Hong Kong’s current political situation, following months of pro-democracy protests that began over a proposed and now-withdrawn bill that would have allowed extradition to mainland China.

“As Asia’s Lion City, Singapore is a known business hub. This shift in interest is not at all unusual,” he said. “Both Hong Kong and Singapore are top destinations for entrepreneurs and professionals who want access to a global market from a strategic regional headquarters.”

Earlier this year, Singapore was named as the world’s most competitive economy because of its business-friendly landscape, favourable immigration policies, competitive labour market and advanced IT infrastructure. Hong Kong was ranked second in the report and former number one U.S. moved down two spots to third.

A World Bank list released last year also cited Singapore as the top country when it comes to “success in developing human capital.” The ranking was based on factors such as health, education, earning potential, future productivity as well as mortality and survivability rates.

And in another survey among expatriates, it was found that, even though expats earned more in Hong Kong, Singapore was still considered the “best place to live.”

For global companies and entrepreneurs, Singapore has always been a top choice because of tax benefits including tax-free dividends, world-class transport hubs particularly the Changi Airport which has been ranked as the World’s Best Airport since 2013, and a generally accommodating business environment.

Heng added, “As it is, employment and business applications to Singapore are competitive. With the current developments in Hong Kong and the influx of interested parties, it is best to stay ahead of the curve and get professional help when it comes to relocation plans. There are many ins and outs that must be navigated, and the insights of an immigration expert are invaluable to a successful outcome.”

NEW YORK, September 27, 2017 (Newswire.com)

– The New York law firm Cea Badoeva P.C. is providing free legal advice throughout the month of October, helping business owners and employees who have questions regarding their extraordinary ability visa and investor visa.

A recent Harris Poll shows 63 percent of U.S. employers say hiring international talent is crucial to their company’s business. That’s up 42 percent from last year’s report, showing U.S. employers continue to seek workers from other countries.

As a boutique law firm, we work directly with business owners and employees who need help with their investor visa or extraordinary ability visa. This free consultation makes it easy for entrepreneurs, employers, and employees to get guidance over the phone — and for free.

Michele Cea, Cea Badoeva

The partners at Cea Badoeva — Michele Cea and Viktoriya Badoeva — say they continually hear from start-ups, entrepreneurs, small and medium-sized business owners that they don’t know their options for starting a new business in the USA, or for expanding their business into the USA.

Mr. Cea says many people don’t know their professional achievements can qualify them for an extraordinary visa and potentially help them obtain a green card.

“There are several types of visas in the USA — E1, E2, EB5, EB1, O1, J1, H1B — and all of these applications have different requirements and restrictions,” says Mr. Cea.

“As a boutique law firm, we work directly with business owners and employees who need help with their investor visa or extraordinary ability visa,” said Mr. Cea. “Many of these potential clients have similar questions. This free consultation makes it easy for entrepreneurs, employers, and employees to get guidance over the phone — and for free. This is our way of helping our community.”

“We are trying to bring talented people to our community and in many cases, those are artists who may not realize they can benefit from the extraordinary ability visa based on their creative background,” said Ms. Badoeva.

Mr. Cea and Ms. Badoeva both worked at big international law firms in New York and abroad, focusing their work on corporate law and business immigration law.

Ms. Badoeva graduated from Fordham University School of Law in 2011 and Moscow State University of International Affairs School of Law in 2007. She has experience in both corporate and health care law, and has represented many international clients. She is fluent in Russian.

Mr. Cea graduated from Fordham University School of Law in 2011 and Catholic University School of Law in Milan, Italy in 2009. He has experience with corporate law and business immigration. Prior to partnering with Ms. Badoeva, Mr. Cea founded his own practice focused on business immigration. He is fluent in Italian and conversational Spanish.

Frequently Asked Extraordinary Ability Visa and Investor Visa Related Questions

Mr. Cea and Ms. Badoeva will be answering all extraordinary ability visa and investor visa-related questions over the phone, every Tuesday – from noon to 1 p.m. EST — throughout the month of October.

Anyone with questions related to the investor visa or extraordinary ability visa can call their conference line and ask either of them such questions for no charge.

Callers will not be speaking with a lower-level paralegal, but someone with years of legal experience in business immigration law.

“This is also an opportunity to listen to questions that others in similar situations may have,” says Ms. Badoeva. “It’s also an easy and timeless way to get some quick guidance with your investor or extraordinary ability visa. You don’t need to travel to our Midtown offices. Anyone with a phone can call us from literally anywhere in the world.”

With larger law firms, this service would cost upwards of $500 an hour. In many of these situations, the law firm may not even be able to help visa applicants or businesses.

“We will also offer guidance and help applicants find the correct visa,” said Mr. Cea. “For instance, an entrepreneur investing in an American business will want to know the differences between EB-5 and E2 investment visas. We will explain different requirements and restrictions for visas to help secure visa application approval.”

Cea Badoeva P.C. will not be answering any visa questions concerning refugee, asylum, family immigration or travel visas.

About Cea Badoeva P.C.

The law firm of Cea Badoeva counsels business owners and entrepreneurs on a broad range of transaction and business matters including, but not limited to:

– Business start-up

– Corporate formation and organization

– Corporate governance

– Contracts and commercial transactions

– Business immigration.

Their experience in a variety of legal practices, combined with international reach, allows them to address most of the legal needs of small to mid-sized businesses.

Details of the Free Consultation for Work Visa-Related Questions

When: October 3rd, 10th, 17th, 24th, and 31st — Every Tuesday throughout the month of October 2017.

Time: Noon to 1 p.m. EST

Dial-In Number: (641) 715-0654 Access Pin: 309249

For more information, go to www.Cebalaw.com or call (917) 728-1455