[ad_1]

- Although there is no notification regarding the daily limit, it is expected to be the standard ₹1 Lakh, with a maximum of 20 transactions.

- But if you are an Amazon Pay user, you can register on the application to use this feature.

- Also, if you reset your UPI PIN, the feature will be automatically disabled, and you will have to re-verify to use it.

UPI is one innovation from India that has been proven to be of extensive utility. Since its inception in 2016, the National Payments Corporation of India (NPCI) has developed it to make it more accessible and safe. They, on October 7th, 2025, announced a mandate directed towards UPI applications, banks, and other stakeholders. Part of this mandate was that all UPI apps should now roll out optional biometric verification for payment authentication. Amazon Pay has rolled out this feature in a new update. Let’s see how you can take advantage of this feature.

UPI Payments Through Fingerprint

Biometric verification means that now you can verify your UPI payments through your fingerprint or face ID (for iOS). Apps like Google Pay, PhonePe, and Paytm are still rolling out the update in phases. But if you are an Amazon Pay user, you can register on the application to use this feature. Make sure your Amazon App is updated and follow the simple steps.

How to Use Fingerprint for Making Payments on Amazon Pay

1. Open the Amazon app and go to the ‘pay’ section.

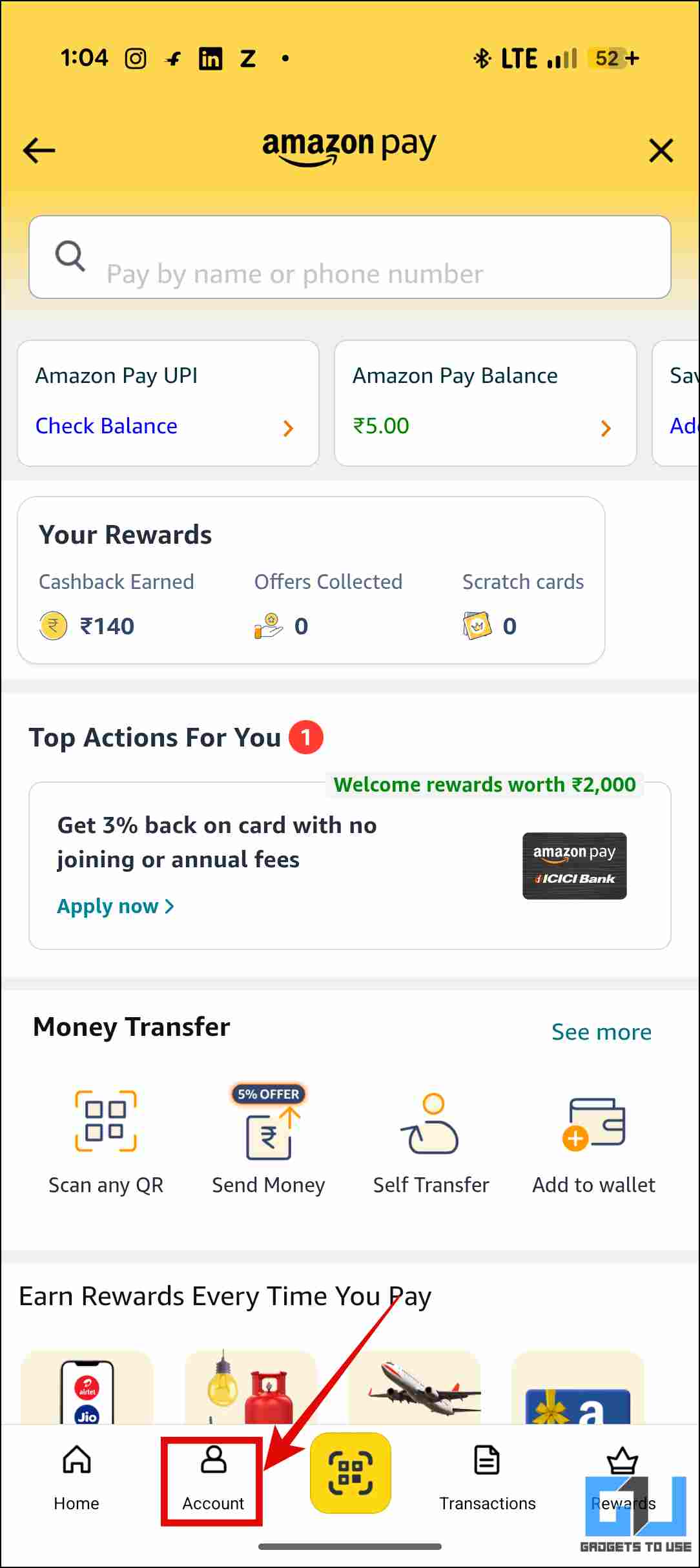

2. Tap on the Account tab at the bottom.

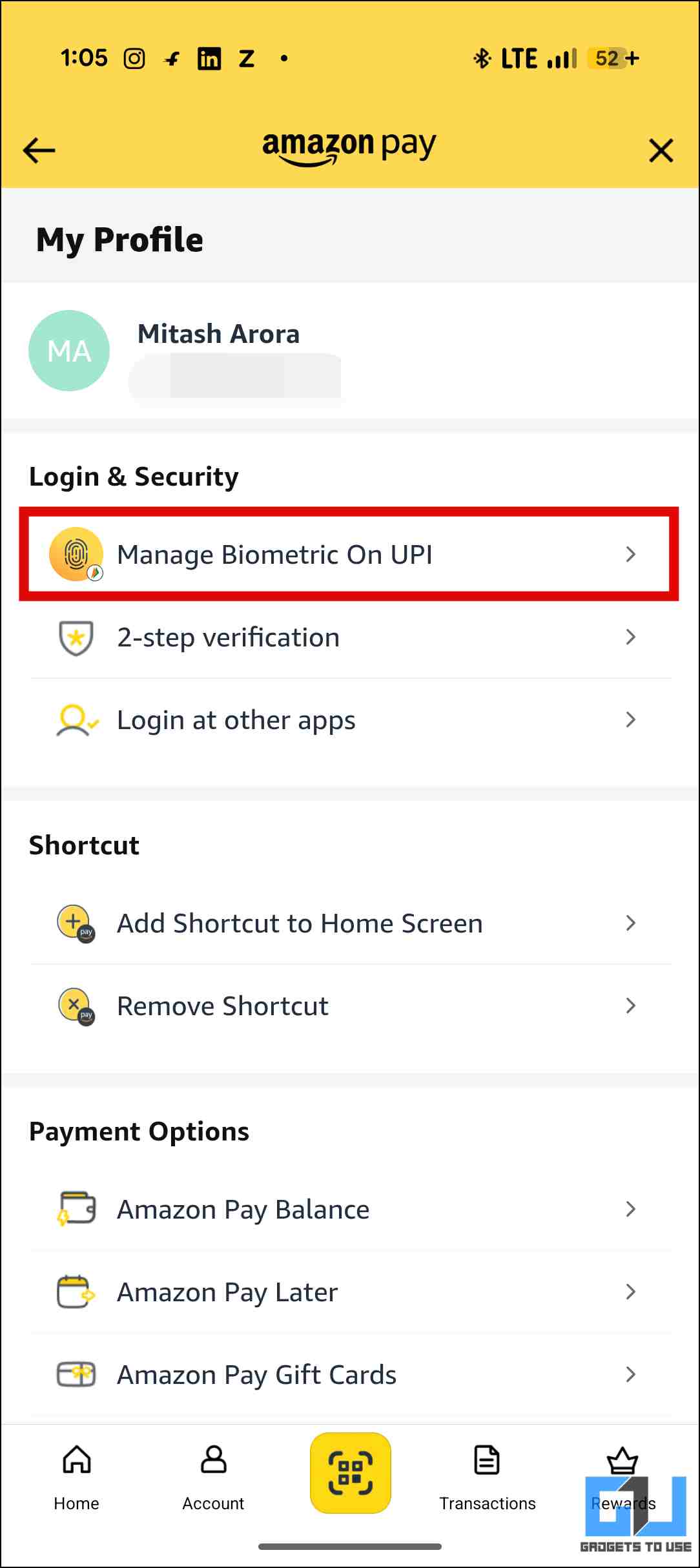

3. In ‘Login & Security’, tap on ‘Manage Biometric on UPI’.

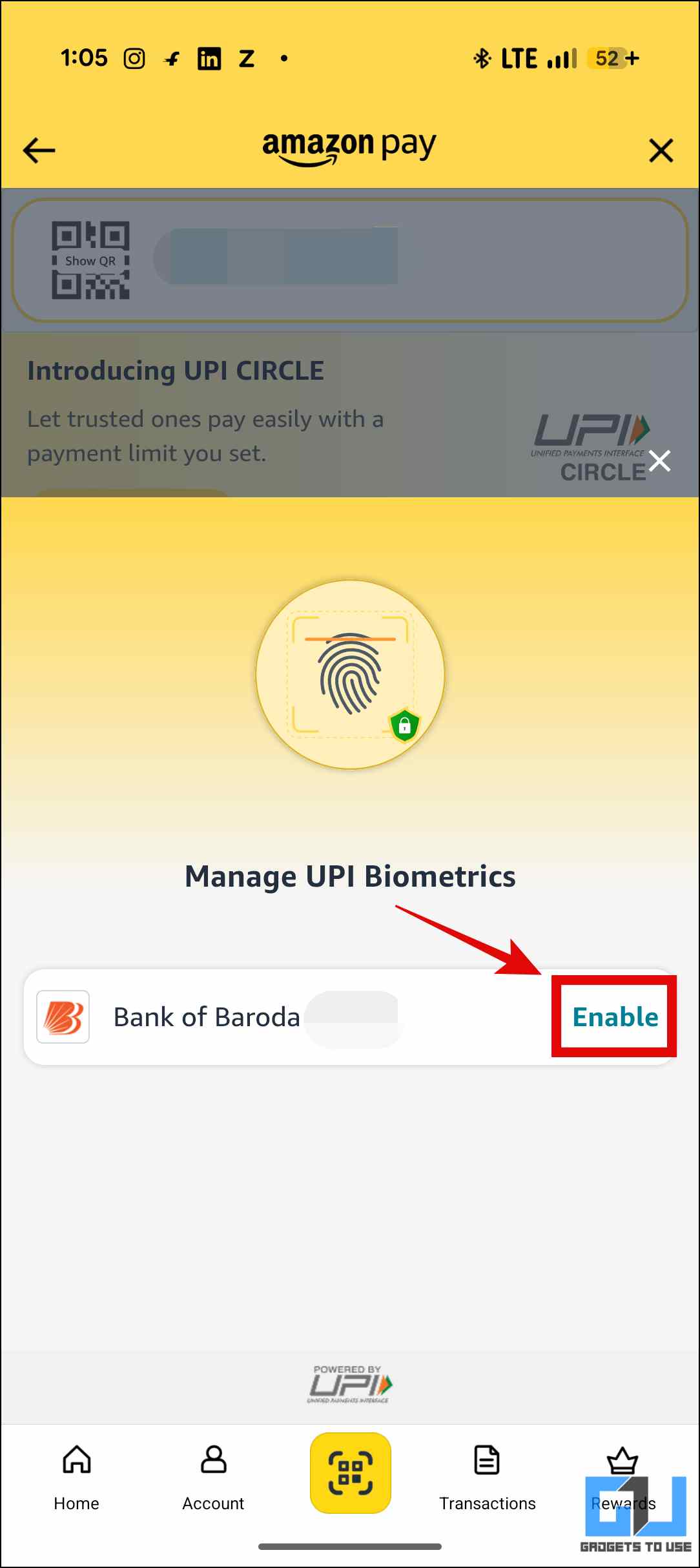

4. A pop-up will open where you can select the bank account you want to register. Tap ‘Enable’.

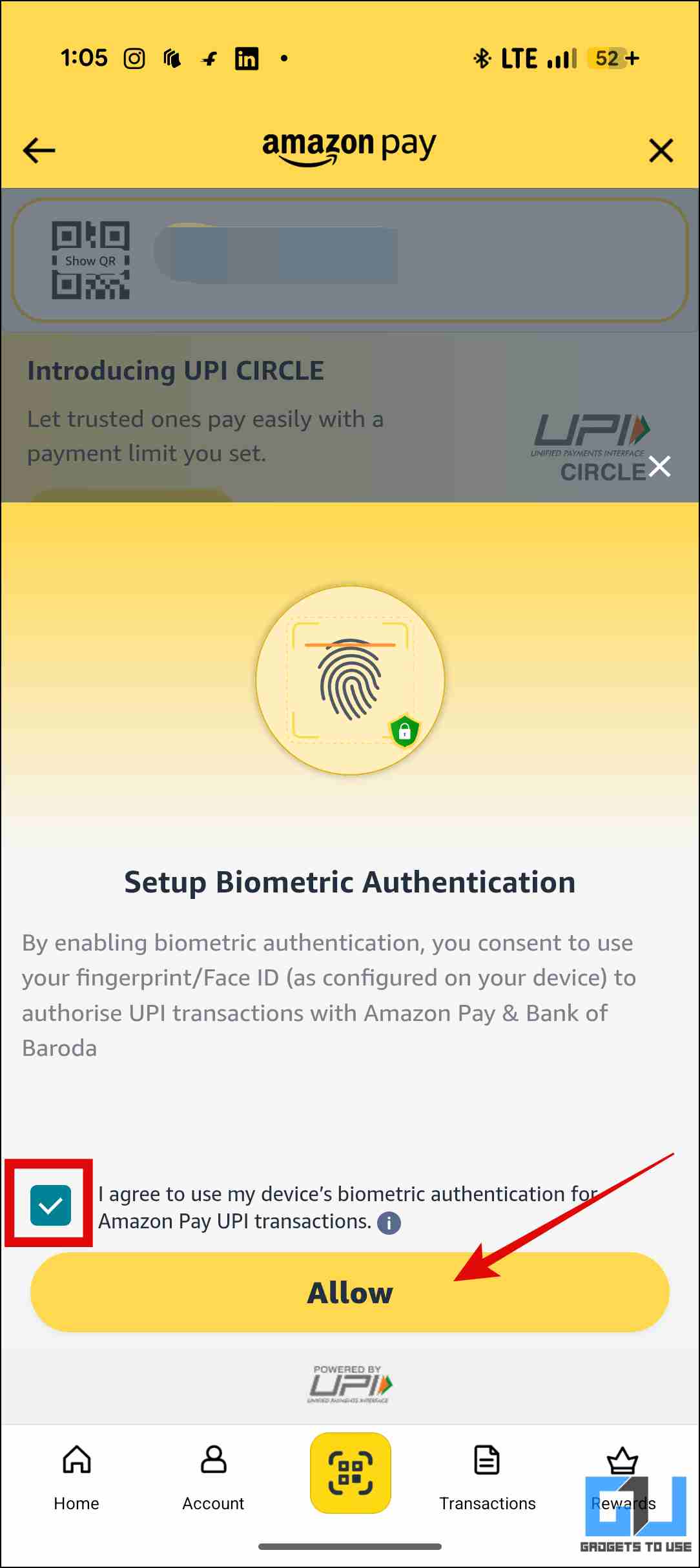

5. Tap on the checkbox and then ‘Allow’ to give your consent.

6. After this, you will have to enter your UPI PIN, which you use for making payments, and then submit your fingerprint. Once this is done, you will be able to make payments through your fingerprint instead of entering the PIN for authentication.

Things to Keep in Mind While Using Fingerprint Authentication

- Transaction Limit: The amount that you can send per transaction is capped at ₹5000. For any transaction involving more than that, you would have to enter your default 4 or 6 digit UPI PIN. Although there is no notification regarding the daily limit, it is expected to be the standard ₹1 Lakh, with a maximum of 20 transactions.

- Inactivity: If you don’t use the biometrics feature for more than 90 days, it will be disabled for security reasons. You will have to enable it again to use the feature.

- PIN Reset: Also, if you reset your UPI PIN, the feature will be automatically disabled, and you will have to re-verify to use it.

- Device Compatibility: This feature would work on most devices with an in-built fingerprint sensor. Although NPCI hasn’t set any minimum requirement for Android version, UPI apps require at least Android 10 or higher to offer advanced biometric features. For iOS devices, Face ID is utilised to offer a similar PIN-less payment experience.

FAQs

Q. Can Android users also use the face verification feature for payments?

Most Android phones use 2D face scanning, which isn’t considered secure enough like the Face ID in iPhones. This is the reason why UPI apps don’t allow using face verification for payment authentication.

Q. Are there any other apps supporting this feature?

Yes, apart from Amazon Pay, apps such as Navi and Samsung Wallet are also providing this feature. Other apps like Google Pay, PhonePe, and Paytm are expected to roll out this update soon in all compatible devices

Wrapping Up

The feature could prove to be a welcome update. It would allow for a secure and fast payment experience. Moreover, it would prevent cases of PIN theft. It is also expected to benefit senior citizens or people using digital payment for the first time, who might find PIN-based authentication systems challenging.

You may also like to read:

Have any questions related to our how-to guides, or anything in the world of technology? Check out our new GadgetsToUse AI Chatbot for free, powered by ChatGPT.

You can also follow us for instant tech news at Google News or for tips and tricks, smartphones & gadgets reviews, join the GadgetsToUse Telegram Group, or subscribe to the GadgetsToUse Youtube Channel for the latest review videos.

Was this article helpful?

YesNo

[ad_2]

Mitash Arora

Source link