The anti-Israel encampments on the quad are mostly gone, but we’re starting to learn what happened behind the scenes when universities let antisemitism run rampant on campus. Records recently obtained from the University of Arizona show the school’s faculty threw in with pro-Palestinian protesters in the months after Oct. 7, 2023.

Arizona-based researcher Brian Anderson issued the Freedom of Information Act request in May 2024 for university communications on such keywords as “Israel,” “Palestine,” “Gaza,” “Hamas,” “Anti-Semitism” and “Jewish.” Mr. Anderson says the school refused the request until his lawyer sent a demand letter. It later produced nearly 1,000 documents with many names redacted. The university didn’t respond to our request for comment.

The emails reveal that on Oct. 11, 2023, then-Arizona President Robert Robbins issued an unequivocal statement addressing “the horrendous acts of terrorism by Hamas in Israel.” Mr. Robbins called the massacre “antisemitic hatred, murder, and a complete atrocity” and called out Students for Justice in Palestine (SJP) for “endorsing the actions of Hamas.”

For that moment of principled clarity, Mr. Robbins was criticized by the faculty. On Oct. 12, faculty chair Leila Hudson received an email from a professor (name redacted) who expressed “concern” that “President Robbins email and others’ smears are chilling SJP dissent.” (Mr. Robbins had noted that while SJP didn’t speak for the university, the group has “the constitutional right to hold their views and to express them in a safe environment.”)

LONDON—After last week’s terrorist attack on a synagogue in Manchester, the U.K. government is struggling over how to manage near daily pro-Palestinian protests that officials say have fueled a rise in antisemitism and left many British Jews feeling alienated in their own country.

On Tuesday—the second anniversary of the Oct. 7, 2023, attacks that marked the largest loss of Jewish life since the Holocaust—pro-Palestinian protests were held in university campuses across the country, despite an unusual request from Prime Minister Keir Starmer for the protests to be called off given it was the anniversary of the attack.

After winning nearly $500,000 on a $5 sports bet, a New Jersey financial adviser said he is planning to follow some of the advice he gives to clients and put the money to good use.

Travis Dufner, a 32-year-old adviser with Millstone Financial Group in Millstone, N.J., is the bettor who has stepped forward to say he won the $489,378.01 parlay payoff. The wager involved picking 14 players who would score a touchdown over the holiday weekend’s NFL games.

In my day, applying to college meant thumbing through a big paperback encyclopedia of college listings and then pulling out the typewriter and filling in applications. Thirty-some years later as my kid prepares to apply, I need a spreadsheet and access to reams of data that I’m not sure how to process.

I’ve tried doing it the old-fashioned way, by searching through the websites of all the schools my high-school senior is interested in applying to. For each school, you need to find the common data set, a multipage PDF that lists seemingly unrelated stats. Then you need to run the net-price calculator, which attempts to give you a price tag based on the financial information you input. Then you put everything together to try to get some sense of your kid’s chances of getting in and what it might cost you so you can compare the schools to each other.

Of course, there’s an app for that. Well, not so much one app, but several different programs that purport to sort college data in a useful way — some of them free, some by subscription and some through the school. All of it is still confusing and overwhelming for the average family.

Big J Education Consulting is attempting to make it easier with interactive charts, available on its website for free, that allow you to easily sort through data from the common data sets of hundreds of schools, plus some of the company’s own fact-checked and reported updates. Co-owners Jennie Kent and Jeff Levy have been making these charts for years for their own business, and they went high-tech with a new format this year that makes sorting and crunching the data easy enough for a layperson to do.

“People think about that common data set as a snapshot, but it’s really more of a collage,” says Kent. “Admissions fills out part, financial aid fills out part. Sometimes numbers are off, and we reach out to institutions. The best that any of us can do with this is to use the common data set.”

Take, for instance, the sometimes outrageous cost-of-attendance number, a sticker price that includes tuition, room and board, books and fees for one year. At the top of their list is Northwestern University in Evanston, Ill., at a whopping $89,394. Levy and Kent say they are hearing from a number of schools that the price for the upcoming year will be over $90,000, at least for international students.

Need-based and merit aid for the class of 2026, sorted by total cost of attendance for out-of-state students.

Credit: Jennie Kent, Jeff Levy, and Big J Educational Consulting, 2023

You can learn a lot from looking at a chart like this and playing with it according to the choices pertinent to your family. For instance, one thing to note is that if you sort by price, you don’t see prices below $80,000 until you get four pages in. Those are the most expensive 78 out of 427 schools.

To get to the least expensive schools, you have to sort by in-state prices, because most of these will be public institutions that offer special pricing to state residents.

Need-based and merit aid for the class of 2026, sorted by total cost of attendance for in-state students.

Credit: Jennie Kent, Jeff Levy, and Big J Educational Consulting, 2023

Of course, a school’s list price does not tell you how much it will cost your family to send a student there. The price you pay will depend on your own family’s financial situation, and that’s where all the strategizing comes in — and why families sometimes turn to professionals to crunch this data for them.

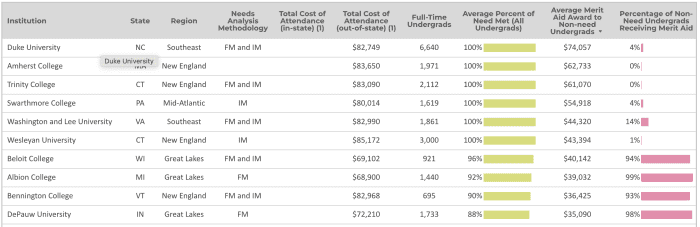

To get any kind of handle on that, you have to look at the other columns detailed on the chart below that analyze how much need-based aid a school gives and how much it gives out in so-called merit aid, which college finance experts have taken to calling “tuition discounting,” because it really just represents a coupon value off the sticker price.

If your family falls under the threshold of “need,” which varies by school, you can get a decent picture of what your price may be from the net-price calculator. But if you fall outside of those parameters, you’ll want to know how generous a school is with that tuition discounting. You really have to look at two numbers to figure this out, because the average amount of merit aid can be inflated by the small number of students it goes to.

Need-based and merit aid for the class of 2026, average merit aid awarded to non-need undergrads.

Credit: Jennie Kent, Jeff Levy, and Big J Educational Consulting, 2023

For instance, according to common-data-set data compiled by Big J, Duke meets all needs of undergraduates and gives out an average of $74,057 in merit awards to non-need undergrads, but it only gives that out to 4% of its full-pay applicants. Whereas Beloit College meets 96% of need but gives out an average of $40,142 in merit awards to 94% of non-need undergrads. Which sounds like the better chance of getting a discount?

You can input your own selection of colleges into this list and do a comparison that way. I input the top colleges on my child’s list and was able to see how they stacked up against each other in terms of merit aid and tuition price. I found that useful for weeding some out.

Playing the early game

None of the price modeling matters if your child doesn’t get into a school in the first place. That’s where strategizing over what type of application to submit matters. A little data visualization on early admission might help you if you want to play that game. And if you pair it with the financial data, you can get a sense of whether it matters at a particular school to apply early, and what it might cost you — since the decision is supposed to be binding.

The choice of whether to apply for early decision is complicated this year because the federal financial-aid form, FAFSA, is not opening until December, and schools cannot typically finalize their aid packages without it. Plus, more colleges across the spectrum are filling their classes with early admits because it maximizes their yield statistics — that is, the number of students who accept their offers. So competition is fierce.

Early-decision and regular-decision acceptance rates for the class of 2026, sorted by early admits as percent of freshman class.

Credit: Jennie Kent, Jeff Levy, and Big J Educational Consulting, 2023

On the Big J chart for early-decision and regular-decision acceptance rates, the schools making the most of this are filling more two-thirds of their classes with early admits. They are also typically accepting students at a far greater rate from the early-decision pool than they are from the regular-decision pool. At Tulane, for instance, the early-decision acceptance rate is 8.6 times greater than that for regular decisions.

Looking at that data might make you feel a little pressure, but remember, at the end of the day, the only school your child should pick for early decision is one that you can afford and that is a good fit for them.

The NCAA started allowing college athletes to make money from their name, image and likeness in 2021, after decades of student-athletes saying it wasn’t fair that they didn’t receive any money while the games they played in generated millions of dollars — especially football and basketball contests. And today, many of these athletes are not just making some extra cash on the side — they’re making millions.

These NIL deals are negotiated by college athletes and their representation, and typically involve leveraging an athlete’s brand and influence through promotional means. For example, a car dealership near a university campus may ask the college’s high-profile quarterback to do a commercial for them in exchange for a monetary payment or a car. Similarly, an athlete can make money from social media, depending on how big their following is.

Football players are among the college athletes who make the most money from NIL deals, followed by men’s basketball, women’s volleyball and women’s basketball. That’s because college football and basketball have multibillion-dollar TV contracts to broadcast games, while most other sports generally have lower visibility.

With that in mind, here are the college athletes who make the most money from NIL deals according to On3’s proprietary NIL algorithm, which is based on NIL-deal data, performance, influence and exposure

10. J.J. McCarthy, $1.3 million

J.J. McCarthy of the Michigan Wolverines in action against the Georgia Bulldogs.

Getty Images

As the junior quarterback for the Michigan Wolverines football team, McCarthy is one of the six college football QBs in the top 10 of NIL earners.

McCarthy sports 276,000 followers across his social-media platforms, and has deals with Alo, Bose and Bowman.

Tie-8. Bo Nix, $1.4 million

Bo Nix of the Oregon Ducks throws a pass against the Stanford Cardinals.

Getty Images

The senior QB for the Oregon Ducks has led his team to a perfect 5-0 start this season.

Nix has 219,000 followers on social media and NIL deals with 7-Eleven, Bojangles and Celsius. Nix is considered one of the top players in the nation and has the third-best betting odds to win college football’s Heisman Trophy on DraftKings DKNG, -2.52%

sportsbook.

Tie-8. Spencer Rattler, $1.4 million

Spencer Rattler of the South Carolina Gamecocks warms up before a game against the Tennessee Volunteers.

Getty Images

The South Carolina Gamecocks senior QB has one of the more robust NIL profiles in the nation. He has deals with Mercedes-Benz MBG, -1.23%,

Leaf trading cards and Raising Canes.

Rattler also has 578,000 followers across TikTok, Instagram META, -0.71%

and X, the platform formerly known as Twitter.

7. Angel Reese, $1.7 million

Angel Reese of the LSU Lady Tigers during the 2023 NCAA Women’s Basketball Tournament championship game.

Getty Images

Reese was one of the breakout stars of the women’s March Madness basketball tournament this year. The Louisiana State University hooper led her team to the 2023 title and famously flashed a “you can’t see me” gesture in the title game.

Reese has brand deals with Airbnb, PlayStation and Intuit TurboTax INTU, -0.50%

and has appeared in ads for Amazon AMZN, +0.01%

and Pepsi Co.’s PEP, +0.59%

Starry. She also has 5.2 million followers across her social-media platforms.

During LSU’s magical title run last season, Reese set an NCAA single-season record with her 34th double-double against the Iowa Hawkeyes and was named the most outstanding player of the Final Four.

Reese is one of just two female athletes inside the top 10 in On3’s NIL valuation tracker, and the top college basketball player on the list.

6. Travis Hunter, $2.3 million

Travis Hunter of the Colorado Buffaloes signals first down after a catch against the TCU Horned Frogs.

Getty Images

Hunter was one of the college football players who transferred to the University of Colorado from Jackson State last season to follow coach Deion Sanders.

Hunter, a five-star sophomore prospect, plays on both offense and defense — as a wide receiver and a cornerback — a rarity in a high-level college program. He has 1.9 million followers on social media, a successful YouTube GOOG, -0.08%

channel, and endorsements with Celsius Energy Drink and 7-Eleven.

Hunter entered the 2023 college season as the most highly touted NFL prospect at Colorado, and Deion Sanders contends rival schools have attempted to poach him via lucrative NIL deals.

“People offered Travis Hunter a bag — about $1.5 million to try to lure him and buy him out of the transfer portal,” coach Sanders told 247Sports over the summer. “But Travis is not the kind of guy that can be bought. He isn’t built like that. Travis is a relational young man that is built on relationships and stability. And that’s what he wanted and desired. That is why he decided to ride and stay with us.”

If and when Hunter decides to declare for the NFL draft, he will likely have a multimillion-dollar contract as a rookie that could dwarf his collegiate NIL earnings.

5. Caleb Williams, $2.7 million

Caleb Williams of the USC Trojans warms up before a game against the Arizona State Sun Devils.

Getty Images

The University of Southern California QB is seen as a generational NFL prospect and the presumptive No. 1 overall pick in the 2024 NFL draft, but he isn’t the top NIL earner.

Williams has 347,000 followers on social media, and brand deals with United Airlines UAL, -1.24%,

Alo and Beats by Dre.

Once the USC junior QB declares for the draft, his rookie contract will likely be set above $37 million, per Spotrac’s estimates.

4. Arch Manning, $2.8 million

Arch Manning of the Texas Longhorns warms up prior to a game against the Alabama Crimson Tide.

Getty Images

The Texas Longhorns freshman QB is one of several top NIL earners whose family plays a role in their fame. Arch Manning is the nephew of Super Bowl champion QBs Peyton and Eli Manning, and the grandson of former NFL QB Archie Manning.

Despite being a backup quarterback with no recorded statistics, the younger Manning has 277,000 followers on social media and has a brand deal with Panini. That deal involved him autographing an extremely rare one-of-one Prizm Black card that was auctioned off for $102,500, which was later donated to charity.

Manning was a standout high school recruit, ranked No. 5 in the nation in the 2023 class, and could have an NFL future.

3. Livvy Dunne, $3.2 million

Olivia Dunne of LSU looks on during a PAC-12 meet against Utah.

Getty Images

Dunne is the only college athlete in the top 10 of NIL earners who doesn’t play basketball or football. The junior LSU gymnast is the top female NIL earner in the nation and has brand deals with Vuori clothing, Body Armor KO, +0.62%

and American Eagle Outfitters.

Dunne is the second most-followed college athlete on social media with 12.1 million followers on Instagram, TikTok and X combined.

For many years Dunne was seen as the poster child for NIL deals, and she said earlier this year that she could make as much as $500,000 from a single post.

“What I love with certain brands is getting long-term brand deals,” Dunne said on the Full Send podcast in June. “Those are probably the best because you build a relationship with the brand and they want you year after year.”

2. Shedeur Sanders, $4.8 million

Shedeur Sanders of the Colorado Buffaloes celebrates as he walks off the field following an NCAAF game against the Arizona State Sun Devils.

Getty Images

University of Colorado’s Shedeur Sanders has become a phenomenon in the sports world. The 21-year-old junior made headlines after throwing for 510 yards and four touchdowns in Colorado’s season-opening shocker against No. 17–ranked Texas Christian.

Colorado has become the center of the football world since Shedeur’s father Deion took over as coach. Coach Prime’s team is currently 4-2 — the team was 1-11 last season, good for last place in its conference.

The quarterback has more than 2.3 million followers on social media, and has already inked several deals with big brands, including with yogurt producer Oikos 0KFX, -1.13%,

Gatorade and Mercedes-Benz. He has shown fans some of his new Mercedes cars on social media, too.

Overall, Shedeur Sanders’s NIL value currently sits at $4.8 million, according to On3, up from $1.5 million at the beginning of the year — that’s the highest value in all of college football. For context, that’s nearly twice the average NFL player’s salary.

1. Bronny James, $5.9 million

Bronny James playing at his high school, Sierra Canyon.

Getty Images

James has perhaps the most famous family member of any person on this list. He is the son of NBA legend LeBron James, and is currently set to begin his freshman basketball season at USC.

The younger James has yet to play a game at his new school, but will immediately be one of the most well-known players in college athletics. James has 13.5 million social media followers, the most of any college athlete, and has brand deals with Nike NKE, +1.10%

and Beats by Dre AAPL, -0.06%,

two brands his dad is also repped by.

Bronny James suffered cardiac arrest in July during a basketball practice and had to be taken to the hospital. But he’s on the road to recovery, and hopes to play basketball this season.

“Bronny is doing extremely well,” the older James said last week. “He has begun his rehab process to get back on the floor this season with his teammates at USC. (With) the successful surgery that he had, he’s on the up-and-up. It’s definitely a whirlwind, a lot of emotions for our family this summer. But the best thing we have is each other.”

Roughly 125,000 borrowers will have $9 billion in student debt cancelled, the Biden administration announced Wednesday.

The cohort receiving the relief includes three groups of borrowers who have been eligible to have their debt forgiven for years but struggled to access that benefit. They are public servants who have been working for the government or certain nonprofits for more than 10 years and paying on their student loans during that time; borrowers who have been in repayment on their loans for more than 20 years; and borrowers who are severely disabled.

The announcement comes as payments are resuming this month for 28 million student-loan borrowers for the first time in three years, now that the pandemic-era payment pause has ended. Some have reported challenges enrolling in repayment plans and getting correct information from their servicers about their payment amounts.

Student-loan borrower advocates had called on the Biden administration to wipe debt off the books for borrowers who are already eligible for cancellation under the law before resuming repayment. They’ve said that would help alleviate some of the strain the return to repayment is putting on the student-loan system. It wasn’t immediately clear whether borrowers who are part of Wednesday’s announcement will have their debt cancelled right away or need to wait for a period for the discharge to be processed.

Wednesday’s announcement is distinct from the broad-based debt cancellation that’s grabbed headlines in recent months. Earlier this year, the Supreme Court struck down the Biden administration’s plan to cancel up to $20,000 in debt for borrowers earning less than $125,000.

Last week, officials provided more detail on President Joe Biden’s plan to take another stab at mass debt forgiveness. The process to determine the contours of that relief continues, with a set of meetings next week, and likely won’t be resolved for several months.

Part of groups already eligible for relief under the law

The borrowers covered by Wednesday’s announcement are part of groups that were already entitled to debt cancellation under the law, but for years have struggled to access it due to paperwork and technicalities. Officials have faced pressure from advocates for years to smooth the path to relief for these borrowers.

The group includes 53,000 borrowers who are receiving $5.2 billion in cancellations under the Public Service Loan Forgiveness program. That initiative allows borrowers who work for the government and certain nonprofits to have their student debt forgiven after at least 10 years of payments.

But it was notoriously challenging to access. Roughly 1% of borrowers who applied for relief in the first years of the program actually had their debt cancelled. The Biden administration has taken steps to make it easier for borrowers who meet the spirit of the law to overcome technicalities that in the past had stymied their path to forgiveness.

In addition, the Department of Education has approved debt discharges totaling $2.8 billion for nearly 51,000 borrowers who made more than 20 years of payments on their loans, officials announced Wednesday.

For decades, the government has offered federal student-loan borrowers the ability to pay their debt as a percentage of their income and have the remainder cancelled after at least 20 years. The idea was to provide an alternative to borrowers who couldn’t afford to pay off their debt in 10 years through a mortgage-style plan.

But in the first years, borrowers would have been eligible to have their debt forgiven under these income-driven repayment plans, more than 2 million borrowers who were in repayment for more than 20 years were still paying.

Consumer advocates and regulators said that was largely because servicers were steering borrowers towards forbearance — a status that pauses payments, but where the debt still accrues interest and borrowers don’t build credit toward forgiveness — instead of helping them sign up for these plans.

Last year, the Department of Education said it would review borrowers’ payment history to see whether there were periods when they should have been building credit toward forgiveness, but those months weren’t accurately counted. The agency said it would adjust their payment history accordingly. The 51,000 borrowers are part of this group. Already the Biden administration has cancelled the debt of more than 800,000 borrowers through this initiative.

Finally, officials said that nearly 22,000 borrowers who have a total or permanent disability will have about $1.2 billion in student loans cancelled. Borrowers with a disability that is so severe they’ll never work again qualify to have their federal student loans wiped out. But for years, many eligible borrowers found the application process, which historically required them to provide proof of their disability, challenging to navigate.

In 2021, the Biden administration announced it would match borrowers’ data with data at the Social Security Administration, which through its work administering disability benefits has the information that would indicate whether a borrower is eligible for a total and permanent disability discharge. The roughly 22,000 had their debt discharged approved through this data match, the agency said.

“For years, millions of eligible borrowers were unable to access the student-debt relief they qualified for, but that’s all changed thanks to President Biden and this administration’s relentless efforts to fix the broken student-loan system,” Miguel Cardona, the secretary of education, said in a statement announcing the relief.

“Today’s announcement builds on everything our administration has already done to protect students from unaffordable debt, make repayment more affordable and ensure that investments in higher education pay off for students and working families,” he added.

With his confidence and his aphorisms, to say nothing of his coaching skills, Deion Sanders has led the University of Colorado football program to a 3-0 record and a top 20 ranking.

Just weeks into his first season at the helm in Boulder, Sanders, known as “Prime Time” when he played in the NFL — and MLB — and now called “Coach Prime,” has already made his Buffaloes the most talked-about team in college football.

Colorado was 1-11 last season, good for last place in its conference.

Last weekend’s game in Boulder, against in-state rival Colorado State, drew 9.3 million viewers, making it the most-watched late-night college football game ever on ESPN DIS, -1.55%.

It also attracted star power to Boulder, with rappers Lil Wayne and Offset, Dwayne “The Rock” Johnson, and NBA players Kyle Lowry and Kawhi Leonard on hand.

The success and the publicity are making many people in Sanders’s orbit wealthy.

Colorado’s top three NIL — or name, image and likeness — earners this season are coach Sanders’s sons Shedeur and Shilo, and Travis Hunter. All three players transferred to Colorado from Jackson State last season, an HBCU.

His top players have cashed in on newfound fame with NIL deals to the tune of millions of dollars.

Perhaps most notable among them is his son, junior quarterback Shedeur Sanders. The 21-year old made headlines after throwing for 510 yards and four touchdowns in Colorado’s season-opening shocker against No. 17–ranked Texas Christian. Since then, he’s thrown six more touchdown passes in two further victories.

The quarterback has more than 2 million followers on social media and has already inked several deals with big brands, including with yogurt producer Oikos DANOY, -0.84%,

Gatorade PEP, +0.21%

and Mercedes-Benz MBG, -0.15%

Through his stellar play, Shedeur attracted the attention of another noted quarterback, Tom Brady, who inked the dynamic collegian to an endorsement deal with his clothing company, Brandy Brand, last October.

“I think he needs to get his a— in the film room and spend as much time in there as possible,” Brady joked with the young quarterback during a recent recording of his podcast, “Let’s Go.”

Overall, Shedeur Sanders has an NIL value of approximately $5.1 million, according to On3’s proprietary NIL algorithm, up from $1.5 million at the beginning of the year — that’s the highest value in all of college football. On3’s algorithm considers NIL-deal data, performance, influence and exposure.

While Shedeur Sanders is the headliner at Colorado, he’s not alone in mining the NIL vein. Travis Hunter, a five-star sophomore prospect, has an On3 NIL valuation of $2.2 million, the fourth highest among all college football players. Hunter’s NIL value was $1.7 million at the beginning of the year.

Hunter plays wide receiver on offense and cornerback on defense, a rarity in a high-level college program. He has 1.8 million followers on social media, a successful YouTube GOOG, +0.23%

GOOGL, +0.18%

channel, and endorsements with Celsius Energy Drink and 7-Eleven.

Hunter entered this season as the most highly touted NFL prospect at Colorado, and Deion Sanders contends rival schools have attempted to poach him via lucrative NIL deals.

“People offered Travis Hunter a bag — about $1.5 million to try to lure him and buy him out of the transfer portal,” coach Sanders told 247Sports over the summer. “But Travis is not the kind of guy that can be bought. He isn’t built like that. Travis is a relational young man that is built on relationships and stability. And that’s what he wanted and desired. That is why he decided to ride and stay with us.”

Sanders’s other son on the team, Shilo, is also a top NIL earner. A senior defensive back who took an interception 80 yards and into the end zone during the Buffaloes’ win over Colorado State, Shilo’s NIL value, per On3, sits at $719,000. He has NIL deals with Porsche DRPRY, +0.10%

The NCAA started allowing college athletes to profit from their names, images and likenesses in 2021, ending a years-long crusade by student athletes. Football has been the college sport attracting the most NIL deals, followed by men’s basketball, women’s volleyball and women’s basketball, according to NIL platform Opendorse.

“NIL money, that’s a real part of college football now,” former University of Colorado and NFL football player Tyler Polumbus told CBS shortly after Sanders took the coaching job at Colorado. “I never thought that Colorado would be able to live in that world and compete in that world, but with Deion Sanders it becomes a whole new land of opportunity.”

Sanders, the coach, is getting paid, too, of course.

In addition to the $33.5 million he made while playing in the NFL (to say nothing of the nine big-league baseball seasons in which he was an active player), coach Sanders is on a five-year contract with the University of Colorado worth $29.5 million, as reported by the Mississippi Clarion Ledger, with various escalators tied to performance.

If Sanders continues to have success at Colorado, he’s likely to field even richer offers from bigger-time football schools. At Jackson State, his salary reportedly was just $300,000.

The wealth coming to Sanders and his top players, including his own offspring, is also accruing to the school and brands attached to “Coach Prime.”

The university has sold out all home games on the current schedule — a first in program history — and he’s selling tens of thousands of $67 “Prime 21” sunglasses, which won’t ship until December. He’s also helping sell merchandise at Colorado’s bookstore — it’s up 819% this fall vs. 2022 — and several varieties of Colorado-themed Prime gear are sold out at Nike’s NKE, -0.86%

online store.

Also on Sanders’s radar: trademarks. The six-time NFL All-Pro, two-time Super Bowl champion and Hall of Famer has filed for trademarks on “Coach Prime,” “Prime Effect,” “Daddy Buck” and “It’s Personal,” according to attorney Josh Gerben of Gerben Intellectual Property.

Colorado plays at the University of Oregon on Saturday afternoon. The Ducks are ranked No. 10, while Sanders’s Buffaloes, unranked in the preseason, have climbed to No. 19.

Oregon is a 21-point favorite, according to DraftKings oddsmakers, but 81% of all bets have been placed on Colorado.

Texas is home to the largest number of borrowers who will benefit from the reform — and debt cancellation, data from the Education Department released Tuesday morning revealed.

The three states with the largest number of borrowers who will see their student debt erased under the fix to the program, known as Income-Driven Repayment, are Texas, California and Florida, according to data from Education Department.

Nearly 64,000 Texans are expected to see around $3.1 billion in student loans canceled as a result of having paid their outstanding balance through the IDR program over the past two decades.

“Republican lawmakers — who had no problem with the government forgiving millions of dollars of their own business loans — have tried everything they can to stop me from providing relief to hardworking Americans,” President Joe Biden said Friday, announcing the plan. “Some are even objecting to the actions we announced today, which follows through on relief borrowers were promised, but never given, even when they had been making payments for decades.”

“The hypocrisy is stunning,” Biden added, “and the disregard for working- and middle-class families is outrageous.”

State

Borrower Count

Debt Eligible for Discharge (in millions)

Texas

63,730

$3,091.80

California

61,890

$2,958.80

Florida

56,930

$3,036.80

New York

42,070

$1,924.10

Georgia

38,590

$2,130.40

At the lower end, loan forgiveness through the IDR fix is least likely to help borrowers in Alaska, Wyoming and Hawaii. In Alaska, only 970 student debtors will see their debt erased through the IDR fix, the federal data revealed.

Last year, the Biden administration and Education Department announced that they would be reviewing borrowers’ accounts to make sure all student-loan borrowers’ monthly payments toward their debt have been accurately counted.

The count is an important part of the Income Driven Repayment program, which allows debtors to pay 20 or 25 years of debt as a percentage of their income and have the remainder forgiven.

Until the fix was announced, few had received loan forgiveness in exchange for paying their debt for 20 to 25 years.

The forgiveness comes as a result of a government program that promised loan forgiveness in exchange for debtors paying back their debt over two decades.

Student-loan payments are poised to resume this fall without smaller balances now that the U.S. Supreme Court has blocked President Joe Biden’s loan cancellation plan.

The Biden administration’s loan forgiveness initiative would have canceled up to $10,000 of debt for eligible borrowers, and in some cases up to $20,000.

But the Supreme Court’s conservative majority ruled on Friday that the executive branch overstepped its authority by trying to wipe out billions in student loan debt on its own.

“Six States sued, arguing that the HEROES Act does not authorize the loan cancellation plan. We agree,” Chief Judge John Roberts said, writing for the 6-3 majority.

Now it’s time for more than 40 million borrowers with federal student loans to figure out their next move. They are staring at more than $1.6 trillion in student loan debt. Add on private student loans, and the number climbs to $1.7 trillion.

Federal student loan payments have been on hold since March 2020.

On Friday, the Department of Education filed notice saying it would embark on a regulatory process that would seek an alternative pathway to student-debt relief. Activists have focused on a provision in the Higher Education Act, allowing the Department of Education to “compromise, waive, or release,” any right to collect on student loans.

Approximately 26 million people had either applied for loan forgiveness or were already eligible for the relief as of late last year, the White House said.

Here’s what to know.

When do student-loan payments restart?

In October, according to the Department of Education. Expect more specifics soon on those payments. “We will notify borrowers well before payments restart,” the department said.

While payments start coming in October, interest starts accumulating on the loans in September. Loan balances have not been accumulating interest since the payment pause started in March 2020, during the pandemic’s early days.

“We will also be in direct touch with borrowers and ramping up our communications with servicers well before repayment resumes to ensure borrowers and their families are receiving accurate and timely information about the return to repayment,” an Education Department spokesperson said.

There’s a range of estimates on how much student-loan borrowers typically pay each month on their loans.

According to Bank of America data, $180 was the median monthly student-loan payment as of January 2020. Federal Reserve research before the pause said the average monthly payment was $393, while the median payment was $222.

Can I lower my payments?

Possibly yes, with a range of income-driven repayment plans through the Education Department. These plans are supposed to make repaying loans more affordable by letting borrowers modify their monthly payments based on their income.

While these plans already exist, the department is reworking them. As a result, more monthly income will be shielded from the calculations on what a person could repay for student loans each month, meaning payments will become more affordable. While the revised plans are not in effect yet, the existing plans are up and running.

Many people will likely struggle to fit a student-loan bill back into their budget — the question is how far that financial hardship will go. Student-loan payments would be hitting at a time when car loan and credit-card delinquencies are already rising from their pandemic lows, according to the Federal Reserve Bank of New York.

Part of the Biden administration’s Supreme Court arguments pointed to the possible economic consequences of resuming student-loan payments without canceling some of the debt.

Without cancellation, there will be a “surge” of loan defaults and delinquencies once payments resume, Solicitor General Elizabeth Prelogar told the justices during oral arguments earlier this year.

When deciding which debts have to get paid first, a student-loan bill might fall behind other monthly debts like a mortgage or a credit-card bill.

Anywhere from roughly one-third to three-quarters of borrowers could miss their first student-loan bill when payments resume, according to projections from the credit score company VantageScore.

A missed first payment — in theory — could eventually lead to an average 49- to 82-point reduction in a credit score ranging from 350 to 850, VantageScore researchers said.

However, President Biden on Friday announced a temporary “ramp-up” — a 12-month grace period for borrowers who miss student-loan payments. If borrowers miss payments during this time, they won’t be reported to any of three main credit bureaus — Equifax EFX, +0.37%,

TransUnion TRU, +1.06%

and Experian EXPGF, +0.80%

— and they won’t go into default.

The ramp-up will run from Oct. 1, 2023 through Sept. 30, 2024.

“This is not the same as the student-loan pause, but during this period — if you miss payments — this ‘on ramp’ will temporarily remove the threat of default or having your credit harmed,” Biden wrote in a tweet Friday.

Prior to the payment pause and Biden’s ramp-up announcement, loan servicers waited for a borrower to miss three straight payments before they reported it to the credit reporting bureaus, according to Scott Buchanan, executive director of the Student Loan Servicing Alliance.

In the meantime, brace for potentially long call hold times, curtailed hours and loan servicer glitches, borrower advocates say. It stems back to Congressional cuts on the funding for vendor contracts that handle the day-to-day details of student-loan repayments.

The Supreme Court knocked down the Biden administration’s plan to cancel up to $20,000 in student debt for a wide swath of borrowers, the court announced Friday.

The decision means that the White House won’t move forward with the plan for now, though it’s possible officials could try to launch a new version of the debt-forgiveness initiative using a different legal authority. Roughly 26 million borrowers applied for or were automatically eligible for debt relief under the Biden administration’s plan, which canceled up to $10,000 in student debt for borrowers earning less than $125,000 and up to $20,000 in federal loans for borrowers who met that criteria and also used a Pell grant in college.

Americans owe $1.7 trillion of student loans and the White House had estimated that more than 40 million borrowers would benefit from the initiative. But almost as soon as the Biden administration announced the debt-forgiveness plan last year, opponents looked for ways to challenge it legally. Ultimately, two cases made it to the high court.

In one case, two student-loan borrowers sued over the debt-relief plan in part because the Department of Education didn’t submit it for public comment. That, they said, resulted in an initiative that arbitrarily left out or limited the amount of relief available to some student loan borrowers, like themselves. The suit filed by the borrowers was backed by the Job Creators Network, a conservative advocacy organization co-founded by Bernard Marcus, the co-founder of Home Depot, who also supported former President Donald Trump.

Six Republican-led states brought the other case on the basis that canceling debt could harm their state coffers.

The court considered two issues in these cases. The first is whether the plaintiffs had standing, or the ability to bring a lawsuit because they’ve been directly harmed by the policy. The second is whether the Biden administration overstepped in its executive authority when issuing the policy. In order for the justices to reach the second issue, or the merits of the case, they had to find that the plaintiffs had standing to sue.

Legal experts, including some who believed the Biden administration didn’t have the authority to authorize the debt-relief plan, were skeptical of the notion that the parties bringing the cases had standing to sue. During oral arguments in February, the court’s three liberal justices also questioned whether the parties who challenged debt forgiveness were actually injured by the policy.

In addition, one of the members of the court’s conservative wing, Justice Amy Coney Barrett, asked pointed questions about the six states’ argument that they had standing to sue in part because the debt-relief plan would injure the state of Missouri. That claim surrounded the Missouri Higher Education Loan Authority, or MOHELA, a state-affiliated organization that services federal student loans. The states had argued if MOHELA lost accounts due to the debt-relief plan, its revenue would decline and that loss would hurt Missouri because of MOHELA’s ties to the state.

Despite these questions, Barrett agreed with the court’s five other conservative judges and found that the states have standing to sue. The three liberal justices dissented.

“MOHELA is, by law and function, an instrumentality of Missouri,” Chief Justice John Roberts wrote in the majority opinion. “It was created by the State, is supervised by the State, and serves a public function. The harm to MOHELA in the performance of its public function is necessarily a direct injury to Missouri itself.”

The court’s decision in the states’ suit allowed the justices to get to the merits of the case. The parties challenging the debt-relief plan argued that the Department of Education went beyond the authority Congress delegated it in discharging student debt. Solicitor General Elizabeth Prelogar argued to the justices that in canceling student debt, the Secretary of Education acted “within the heartland” of the authority Congress provided to him under the HEROES Act, a 2003 law that aims to ensure student-loan borrowers aren’t left worse off by a national emergency.

The court’s conservative majority sided with the states, with a 6-3 decision, striking down the debt-relief plan in its current form.

“The HEROES Act allows the Secretary to ‘waive or modify’ existing statutory or regulatory provisions applicable to financial assistance programs under the Education Act, but does not allow the Secretary to rewrite that statute to the extent of canceling $430 billion of student loan principal,” Roberts wrote.

In the months leading up to the court’s decision, White House officials said there was no backup plan for if the Supreme Court knocked down the debt-forgiveness initiative. Advocates and activists have said that student-loan repayments shouldn’t resume until the Biden administration fulfills its promise to cancel some student debt.

The bill President Joe Biden signed in June to raise the nation’s debt limit requires that the Department of Education end the pause on federal student loan, interest payments and collections 60 days after June 30, 2023. Interest on federal student loans will resume starting September 1 and payments will start to come due in October, according to the Department’s website.

Advocates and activists have said for years that the Higher Education Act provides the Secretary of Education with the authority to discharge student loans. In ruling that the HEROES Act didn’t authorize the Biden administration’s debt-relief plan, the court left the option open for the Biden administration to create a loan-forgiveness program authorized under the HEA.

The court’s decision marks the latest development in a more-than-decade-long push to get the government to cancel student debt en masse. The idea, which has its origins in the Occupy Wall Street movement, made it to the presidential campaign stage during the 2020 cycle and was adopted by the White House last year.

Proponents of student debt cancellation and the Biden administration, have expressed concern that without some kind of relief a large swath of borrowers could slip into delinquency and default with the return of student loan payments later this year.

Student loan borrowers aren’t just the freshly graduated and mid-30s working generations — millions of Americans in their retirement years have student debt to pay back, too.

There are six times as many borrowers ages 60 and older now than there were in 2004, but their debt has increased “19-fold,” according to a report from New America, a public policy think tank. About 3.5 million Americans in this age bracket carry $125 billion in student debt, the report found.

Overall, Americans hold $1.75 trillion in student debt, the World Economic Forum found. The president’s student loan forgiveness plan, which was announced last August and is now in the midst of legal battles in the Supreme Court, would alleviate $10,000 for qualifying borrowers, or $20,000 for those with Pell Grants. At the time of the announcement, the White House said 20 million borrowers would see their debt washed away, and a total of 40 million would find benefit from cancellation.

Student debt has been especially problematic because of “stagnant wages and soaring tuition prices,” AARP said in another report highlighting older borrowers. Around 3% of families headed by someone who was 50 or older had student debt in 1989, with an average balance of $10,000, but by 2016, that figure rose to 9.6%, with an average of $33,000, AARP said.

Whether student debt forgiveness will happen or not is still to be determined. Borrowers have been anxiously awaiting an answer from the Supreme Court over two cases linked to the plan — one that argues whether or not the president had the legal authority to forgive loans, and another case about whether the program has standing. The Supreme Court is expected to release its decision on Friday, the last day of the court’s term before summer break.

Older borrowers have various reasons to carry debt. Some are paying off their own education, while others have taken on student debt for their loved ones. Federal PLUS loans, for example, allow parents to take loans out for their children’s education. Older Americans may have also taken on debt to refine their skills for a promotion, AARP noted in its report.

Student loans can have a rippling impact on retirement savings — not just in allocating a portion of retirement income toward this debt, but also in accruing enough wealth for old age. Graduates with student loans had 50% less in retirement wealth by age 30 than the graduates without this debt, a Boston College Center for Retirement Research study found.

She doesn’t know how much her student-loan bill will be when the years-long pandemic-era freeze on payments ends. Eminger’s loans were transferred during the pandemic to a new servicer, but she’s struggled to communicate with the organization, which could help her learn her monthly payment amount. She’s also rushing to take steps that could provide her access to a loan-forgiveness program for public servants.

“I am very nervous about them starting again,” Eminger, 37, who has about $175,000 in student debt, said of the loan payments. “There’s just a lot of uncertainty and murkiness around it, which for a loan amount of my size is pretty scary.”

After a more than three-year freeze, payments, collections and interest are scheduled to resume on federal student loans later this year. This is the ninth time — spanning two administrations — that the government has threatened to turn payments back on. Once again, borrowers, advocates and servicers are gearing up for a financial and operational headache.

“It’s going to be frustrating for everybody involved — borrowers, servicers, the Department of Education, advocacy organizations like ours,” said Betsy Mayotte, the president of the Institute of Student Loan Advisors, a nonprofit that helps borrowers manage their student loans.

To advocates who pushed officials to delay restarting payments in the past, this moment in many ways looks similar to the months before the freeze was scheduled to end those eight other times. A challenging economy means borrowers’ budgets are still tight and promised fixes to the student-loan system that could help ensure a smooth transition to repayment and make borrowers’ bills more manageable still haven’t materialized.

But a few key factors are different, some of which are upping the pressure on the Biden administration to turn the student-loan system back on: the official end to the pandemic emergency, congressional Republicans taking aim at the payment pause in two pieces of legislation and multiplelawsuits challenging the freeze. Other elements unique to this moment are exacerbating the uncertainty and challenges related to restarting payments. Servicers will have fewer resources than in the past to handle a likely crush of calls.

“The Department remains focused on doing everything in its power to better serve students and borrowers, and we are fully committed to supporting student loan borrowers as they successfully navigate returning to repayment,” a Department of Education spokesperson wrote in an email. “The Department is deeply concerned about the lack of adequate annual funding made available to Federal Student Aid this year,” the spokesperson said, referring to Congress’s decision not to increase funding for FSA, despite the agency’s request. “As the Department has repeatedly made clear, restarting repayment requires significant resources to avoid unnecessary harm to borrowers.”

For Eminger, and other borrowers, part of the anxiety surrounding the restart to payments stems from major upheaval to the student-loan system that’s been announced during the pause that will make her loans more manageable. But accessing these benefits requires both diligence — staying on top of announcements and paperwork — and patience while she and others wait for the full implementation of these initiatives.

“The rules have been changing so much,” Eminger said. “Before the pandemic I felt like I very much understood what I was required to do. I always felt very on top of it. Now it just feels like a completely moving target.”

Kate Eminger says she’s nervous about the looming resumption of student-loan payments.

Courtesy of Kate Eminger

Compounding her uncertainty is a lack of clarity surrounding exactly when payments will resume. In November, President Joe Biden told borrowers they could expect the pause to end in the late summer, but he didn’t give an exact date. In addition, it’s hard for Eminger to see how this deadline for payments to restart is different from all the others, where student-loan bills never materialized. All of that has made it difficult for Eminger to figure out exactly when to take steps to make sure her student-loan payment can fit in with the rest of her budget such as the sale of her car.

“It does not feel real at all,” she said of the restart of student-loan payments. “It would be great to name a date. If they could name a date and if that date felt certain then you could plan.”

Tied up in court

The Biden administration has said that the freeze will end 60 days after litigation surrounding its plan to cancel up to $20,000 in debt for a wide swath of borrowers is resolved or 60 days after June 30, 2023, whichever comes first.

“When payments turn back on, it’s going to be a big problem,” said Eleni Schirmer, a researcher and organizer with the Debt Collective, a debtor activist group, “but to not even be granted the dignity of a clear date of when that happens just makes it even more of a problem.” She described providing a ballpark estimate for the restart of payments instead of an exact date as signaling an “almost cruel indifference” to how resumed monthly student-loan bills will impact borrowers.

That uncertainty could exacerbate the stress that student debt already places on borrowers, according to Daniel A. Collier, an assistant professor of higher education at the University of Memphis, who is studying the impact of student debt on mental health. What he’s found is that people who are the most uncertain about what’s going on with their student loan have the highest rates of psychological distress and suicidal ideation. For example, these borrowers worry they’re not getting an accurate sense of their balance or the number of payments they need to make before qualifying for a forgiveness plan.

“People are concerned about the pause because they don’t know what a restart looks like, this has never been done before,” he said. In the past, when payments have resumed after more limited pauses, delinquencies and defaults spiked — part of the Biden administration’s legal rationale for tying mass debt cancellation to the restart of payments. Borrowers don’t know “when it’s going to start, what their repayments are actually going to be,” Collier added.

Kevin Noonan, who together with his wife has about $100,000 in student debt, said he’s benefited from the pause. The couple has used the extra room in their budget to pay down private student loans. Still, Noonan is “frustrated” with the lack of clarity surrounding the resumed payments and the status of the Biden administration’s loan-forgiveness plan.

“Not knowing is the hardest part,” he said. “I have a Google alert set up, every time student loans come up I check everything. You kind of just have to plan for the worst-case scenario.”

Megan and Kevin Noonan have about $100,000 in student debt.

Courtesy of Kevin Noonan

The decision to tie the resumption of payments to the court’s decision “added an element of unpredictability,” said Persis Yu, managing counsel and deputy executive director at the Student Borrower Protection Center, an advocacy group.

“There’s the choice to not land on a certain date, but there’s also the choice of 60 days,” Yu said, referring to the 60-day delay between the court’s decision and payments resuming.

“I really wonder whether or not 60 days is enough time for borrowers,” she said. “When we think about the amount of work that is really going to have to happen to effectively turn on this system, 60 days does not seem like a lot of lead time.”

Secretary of Education Miguel Cardona said in a congressional hearing this month that the agency is “preparing to restart repayment because the emergency period is over.” He told another congressional panel that the agency is “geared up and ready to go,” to resume payments.

Scott Buchanan, the executive director of the Student Loan Servicing Alliance, a trade group, said that 60 days should be enough time for student-loan servicers to implement the restart. In order to accomplish that, they’ll need to be able to communicate with borrowers in the coming weeks about the end of the payment pause and be allowed to offer flexibilities like forbearance and allowing borrowers to verbally recertify their income for payment plans.

When the end of the payment freeze loomed in the past, servicers didn’t have the go-ahead from the Department of Education to communicate with borrowers, Buchanan said. They still don’t, but servicers have been working closely with officials to discuss the “communication playbook” in recent weeks and hope to roll it out shortly.

The Department of Education “remains in constant contact with servicers,” the department spokesperson wrote in an email, and will be in “direct contact” with borrowers before the end of the payment freeze. “Engaging with servicers to ensure they are communicating directly with borrowers about successfully returning to repayment is an important part of the Department’s efforts to smoothly transition borrowers back into repayment,” the spokesperson wrote.

Still, the uncertainty surrounding exactly when payments will start could create an obstacle to a seamless return to repayment, Buchanan said.

“If you’re a family and you’re planning a budget you need to know what is the date that I need to be prepared to make this payment,” he said. “Having a fuzzy date doesn’t do anyone any good including servicers, but especially for borrowers.”

Borrowers will receive a bill at least 21 days before their payments are scheduled to resume and likely won’t end up having to make a payment until October, Politico reported last month. Officials are also considering offering borrowers a grace period when the freeze ends, according to the report.

Servicers will be implementing plans the department previously developed to restart payments, Buchanan said. But they’ll be working with fewer resources than previously anticipated. The Department of Education cut the amount it’s paying servicers to manage each account. The agency has said the cuts are due to lawmakers’ decision not to increase funding for the Office of Federal Student Aid for the 2023 fiscal year. The lack of funds will mean fewer customer-service representatives and reduced call-center hours, including none on weekends.

“What is the right level of resources? How many staff should you have? It’s not a definable thing,” Buchanan said. “What I can say is having fewer than we had before does not make it better.”

The department spokesperson said the agency will keep working with Congress to fully fund President Biden’s fiscal 2024 budget request. The department asked for a $620 million increase in funding for FSA.

“Restarting repayment requires significant resources to avoid unnecessary harm to borrowers,” the spokesperson wrote in the email.

Members of the Class of 2022 at the University of Delaware.

Mandel Ngan/Agence France-Presse/Getty Images

In addition, the Department of Education recently announced an overhaul of the student-loan servicing system aimed at increasing accountability for servicers. For years, borrowers and advocates have complained that the firms don’t provide borrowers with enough information or the right information. Without that in place, Yu worries that ensuring borrowers have a truly affordable payment will be “a nightmare.”

“At this inflection point where you need the best servicing possible, we don’t have it,” she said. “It seems irresponsible to turn on the payment system into a broken servicing system and into a broken system overall.”

Though the new servicing system won’t go live until 2024, “our servicer contracts continue to include the same requirements that all vendors effectively serve our customers and still provide that servicers compete against each other to maintain low call-abandonment rates,” the department spokesperson wrote.

Fixing servicing is just one of many initiatives from the Biden administration aimed at overhauling the student-loan system in the process of being implemented and won’t be fully realized before the end of the summer.

For example, some borrowers have debts that should be wiped off the books, Yu said. The Biden administration has launched several initiatives over the past few years aimed at making it easier for borrowers to access the forgiveness already available to them under the law. So far, the department has announced more than $66 billion in discharges for nearly 2.2 million borrowers, including public servants, borrowers with severe disabilities and borrowers who were scammed by schools.

Still, there are more borrowers eligible to have their debt canceled under these programs who haven’t received relief, Yu said. “These borrowers are going to be thrown into a system to make payments on loans they shouldn’t be making payments on anymore,” she said.

In addition, a promise to make repaying student loans more manageable hasn’t fully materialized. At the same time that President Biden announced the mass debt-cancellation plan, he also unveiled sweeping changes to the repayment system aimed at making student-loan bills more affordable. But the program, which Biden called “a game changer” when he announced it in August, likely won’t be ready by the end of the summer. It’s also been a target for criticism by conservative advocacy groups and Republican members of Congress.

“The only way that that could be available to borrowers when payments resume is with another extension,” Yu said.

The proposed plan, which the department spokesperson described as “the most affordable student loan plan in history,” builds on an existing income-driven repayment plan called REPAYE. Eligible borrowers who enroll in REPAYE now will have their monthly payments automatically updated as the terms of the new plan are “finalized and implemented, starting later this year,” the spokesperson wrote.

‘Almost like a tax increase’

For many borrowers, the financial burden of resuming student-loan payments will be significant. Thomas Simons, a senior economist at Jefferies, estimates the return to repayment will cost borrowers about $18 billion per month.

“It’s almost like a tax increase for these people,” Simons said. “They have to pay it, [and] it doesn’t get them anything tangible right now.”

The amount borrowers are saving by not making student-loan payments accounts for about 2% of discretionary spending, Simons said. He sees the hit to borrowers’ wallets as analogous to the impact of a payroll-tax increase in 2013, which impacted a smaller share of discretionary spending for a larger number of Americans.

“‘It’s almost like a tax increase for these people. They have to pay it, [and] it doesn’t get them anything tangible right now.’”

— Thomas Simons, senior economist, Jefferies

“If you look at what happened in the economy in 2013 after those tax increases were announced, the first half of the year spending decelerated quite significantly,” he said. “It really didn’t recover until the latter part of the year.”

“I would be very surprised if we don’t see a similar slowdown in spending coming out of this,” Simons added.

And if payments resume in late summer or early fall, as planned, the hits to borrowers’ bank accounts will be arriving at “the worst possible time,” Simons said, when the labor market will likely start to feel the effects of the Federal Reserve’s battle against inflation.

“That could be a double whammy where people are starting to have significant questions about their income and then having a pretty significant expense,” Simons said.

Many borrowers will likely be juggling other bills, too. For one, the costs of rent, groceries and other basic needs have risen since the advent of the coronavirus pandemic. And borrowers’ other debt payments have actually become less manageable in the three years since the freeze was first implemented.

As of September of last year, about 7% of student-loan borrowers who were not in default on their student loans at the start of the pandemic were more than 60 days delinquent on other debt, compared with 6.2% at the beginning of the pandemic, according to the Consumer Financial Protection Bureau. Their monthly payments on other credit products have also increased during the pause period — 46% of borrowers saw their monthly payments on credit cards and car loans increase by at least 10% since the start of the pandemic, the agency found.

For Kelly, a Charleston, W. Va., student-loan borrower and her husband, the freeze on student-loan payments created financial space to take care of emergency expenses, like a leaking roof. Kelly, who declined to use her last name in order to more freely discuss her financial circumstances, owes about $23,000 in student debt from studying to become a paralegal. Her husband owes about $20,000 from his nursing-school studies.

Kelly, 45, found a job in her field after graduating, but was laid off during the pandemic. She started working some side gigs and eventually launched a dog-grooming business. Despite the business’s success and her passion for it, it likely won’t be enough to cover her bills once she has to start paying on her student loan again. She’s considering getting a second job when the payment freeze ends.

“We’re dual-income, no kids. One car is paid off, the other one is modest — a Volkswagen VOW, -0.43%

VWAGY, +0.22%,

” she added. “We don’t finance things, we don’t live a high and mighty life, but it seems like every month we’re budgeting to the penny.”

“I don’t know how much we can cut back,” she added. “Our entertainment as it is, is Netflix NFLX, -1.60%,

or we go out to eat once a month or so. I guess we can cut back on that.

I’m the first of my generation to own a home and the first to earn this much annually and don’t want to mess this up. How, specifically, can a financial adviser help me?

Getty Images

Question: By the end of 2022, I will have made $350,000 before taxes as the sole breadwinner and head of household. This is a great starting point and I’m very aware how blessed we are to be in this position, but I’m always looking ahead on how to improve. I currently have $88K left in student loans (originally close to $150K) and very little credit card debt (less than $2K with more than $25K available). I have two auto loans totaling $170K for two electric vehicles at 5% interest.

I’ve recently been offered a $200K HELOC at 9%, which would help me bring down some of my monthly payments and do some small home repairs and improvements, but I want to make the right moves. And I’ve also been presented with a few long-term real estate investment opportunities that are rental properties out of state and are currently bringing it 10-12% ROI. But my biggest concern is that after taxes, 401(k) contributions, bills, savings and mortgage ($4,500), on paper I’m paycheck to paycheck. I’d like to use this HELOC to consolidate debt while also participating in some of these investment opportunities. I’m the first of my generation to own a home and the first to earn this much annually and don’t want to mess this up. How, specifically, can a financial adviser help me? (Looking for a new financial adviser too? This tool can help match you with an adviser who might meet your needs.)

Answer: You have a few questions to tackle here, so let’s go one by one. The first being the HELOC. Yes, HELOCs can be a good way to consolidate debt, but the rate you’re being offered isn’t favorable, as average HELOC rates are a little over 6%. “I would ask if 9% is the best rate you can get, because it appears a bit high,” says Chris Chen, certified financial planner at Insight Financial Strategists. What’s more, “I would like you to consider the potential impact that our Fed policy and inflation are having on interest rates, as HELOCs usually have variable interest rates and we’re in an environment with rising rates. You may start at 9% and end up significantly higher,” says Chen.

What’s more, your student loans, car loans and mortgage are all likely less than 9%, so it’s not likely that consolidation via a HELOC would save you money. “You may want to start somewhere different, like the snowball method, where you focus on one loan, usually the smallest one, and direct all of your resources to pay off that loan while maintaining payments on the others,” says Chen. This method could work to finish off your student loans and maybe one of your car loans, to start with.

Have an issue with your financial adviser or have questions about hiring a new one? Email picks@marketwatch.com.

As for those real estate investments, what do you really know about those returns? “With regards to real estate investments, I assume that the 10% to 12% ROI you speak of is the income that you would be getting from the investment. If so, that’s very high and often when you get a return that is significantly higher than the norm, there’s something else that makes the investment less desirable. Be careful,” says Chen. (Looking for a new financial adviser too? This tool can help match you with an adviser who might meet your needs.)

Certified financial planner Kaleb Paddock says you may actually want to work with a money coach before you work with a financial adviser. Whereas a financial adviser assists with developing investment strategies and long-term financial plans, a money coach offers a more educational experience and focuses on shorter term goals for money management. “A money coach will help you with paying off all of your debts, maximize your cash flow and help you create systems and processes to direct your money proactively,” says Paddock.

While having a high income is great, there’s a concept called Parkinson’s Law, which essentially states that your spending will always rise to meet your income no matter how high that income rises, explains Paddock. “Working with a money coach will help you defeat Parkinson’s Law, eliminate your debt and then enable you to supercharge your investing and life planning with a financial adviser,” says Paddock.

A financial adviser could help too, and Danielle Harrison, certified financial planner at Harrison Financial Planning, says to look for one who does comprehensive financial planning and can help you create a more holistic plan for your money. “They can assist you in the creation of both short and long-term goals and then help you by giving guidance on the financial decisions and opportunities you are presented with,” says Harrison.

A financial adviser would also help you take a long-term approach to your money and help you create a spending plan where you don’t feel like you’re living paycheck to paycheck on a $350,000 salary. “Everyone has blind spots when it comes to their finances, so finding a competent financial partner can be invaluable,” says Harrison. (Looking for a new financial adviser too? This tool can help match you with an adviser who might meet your needs.)

Have an issue with your financial adviser or have questions about hiring a new one? Email picks@marketwatch.com.

*Questions edited for brevity and clarity.

The advice, recommendations or rankings expressed in this article are those of MarketWatch Picks, and have not been reviewed or endorsed by our commercial partners.

Student-loan borrowers got a break this week, but that doesn’t mean they can spend more for the holidays.

The Biden administration on Wednesday extended a pause on student loan payments, yet borrowers should prepare for the eventual resumption of payments by saving the amount they would otherwise owe, experts advise.

Chinese authorities have locked down Peking University after finding a single COVID case, evidence of their continued commitment to the country’s zero-COVID policy.

Beijing reported more than 350 new cases in the latest 24-hour period, representing a small fraction of its population of 21 million but still enough to trigger localized lockdowns and quarantines under China’s zero-COVID strategy, as the Associated Press reported. Nationwide, China reported about 20,000 cases, up from about 8,000 a week ago.

Authorities are trying to move away from the lockdowns, such as those seen earlier this year in Shanghai, that have frustrated locals and prompted protests. And revised national guidelines issued last week instructed local governments to follow a targeted and scientific approach that avoids unnecessary measures. But that doesn’t mean an end to zero-COVID, a policy that has hurt the country’s economy.

Peking University has more than 40,000 students on multiple campuses, most of them in Beijing. It was unclear how many were affected by the new lockdown. The 124-year-old institution is one of China’s top universities and was a center of student protest in earlier decades. Its graduates include leading intellectuals, writers, politicians and businesspeople.

The news comes as known U.S. cases of COVID are climbing again for the first time in a few months. The daily average for new cases stood at 39,414 on Tuesday, according to a New York Times tracker, up 2% versus two weeks ago.

Cases are climbing in 29 states, as well as Washington, D.C., Guam and Puerto Rico. They are up a staggering 868% in Nebraska from two weeks ago, with an average of 16 cases per 100,000 residents. Cases are up 77% in Utah, 54% in Oklahoma and 53% in Arizona.

The U.S. daily average for hospitalizations is up 2% to 27,807, but it is up by higher rates in Western states, led by Colorado at 67%, Arizona at 60% and Nevada at 45%.

On a brighter note, the daily death toll continues to decline and is now down 15%, to 292, from two weeks ago.

Physicians are reporting high numbers of respiratory illnesses like RSV and the flu earlier than the typical winter peak. WSJ’s Brianna Abbott explains what the early surge means for the winter months. Photo illustration: Kaitlyn Wang

• A federal judge has approved a nearly $58 million settlement in a class-action lawsuit filed in response to the deaths of dozens of veterans who contracted COVID-19 at a Massachusetts veterans home, the AP reported. “It was with heavy hearts that we got to the finish line on this case,” Michael Aleo, an attorney for the plaintiffs, said Tuesday, the day after the settlement was approved by a U.S. district court judge in Springfield. The coronavirus outbreak at the Soldiers’ Home in Holyoke in the spring of 2020 was one of the deadliest outbreaks at a long-term care facility in the U.S.

• Australian health authorities have recommended against getting a fifth COVID vaccine shot, even as they urged those who are eligible to sign up for their remaining booster doses as the country’s latest COVID wave grows rapidly, Reuters reported. Average daily cases were 47% higher last week than the week before, said Health Minister Mark Butler at a press conference on Tuesday, announcing the new vaccination recommendations. But cases remain 85% below the previous late July peak.

• A federal judge on Tuesday ordered the Biden administration to lift Trump-era asylum restrictions that have been a cornerstone of border enforcement since the beginning of the pandemic, the AP reported separately. U.S. District Judge Emmet Sullivan ruled in Washington that enforcement must end immediately for families and single adults, calling the ban “arbitrary and capricious.” The administration has not applied it to children traveling alone. Within hours, the Justice Department asked the judge to let the order take effect Dec. 21, giving it five weeks to prepare. Plaintiffs including the American Civil Liberties Union didn’t oppose the delay.

The U.S. leads the world with 98 million cases and 1,075,112 fatalities.

The Centers for Disease Control and Prevention’s tracker shows that 227.8 million people living in the U.S., equal to 68.6% of the total population, are fully vaccinated, meaning they have had their primary shots.

So far, just 31.4 million Americans have had the updated COVID booster that targets the original virus and the omicron variants, equal to 10.1% of the overall population.

CHARLOTTESVILLE, Va. (AP) — The three students killed in a shooting at the University of Virginia were all members of the school’s football team, the school’s president said.

President Jim Ryan told a Monday morning news conference the shooting happened Sunday night on a school bus of students returning from an off-campus trip.

The suspect has been identified as Christopher Darnell Jones Jr., who is also student.

The incident occurred Sunday near a university parking garage. In addition to the three football players killed, two others were reported to have been wounded.

Police went on a manhunt Monday in search of the student suspected in the attack, officials said.

During a press conference in the 11 o’clock hour local time, the university police chief, Tim Longo, was given word that the suspect was in custody. He immediately returned to the microphone and reported that update to the assembled reporters.

Classes at the university were canceled Monday, following the violence Sunday night, and the Charlottesville campus was unusually quiet as authorities searched for the suspect, whom university President Ryan identified as Christopher Darnell Jones Jr.

A shelter-in-place order to the university community had been lifted less than an hour earlier after a law-enforcement search of the campus.

In a letter to the university posted on social media, Ryan said the shooting happened around 10:30 p.m. Sunday.

The university’s emergency management issued an alert Sunday night notifying the campus community of an “active attacker firearm.” The message warned students to shelter in place following a report of shots fired on Culbreth Road on the northern outskirts of campus.

Access to the shooting scene was blocked by police vehicles Monday morning.

Officials urged students to shelter in place and helicopters could be heard overhead as a smattering of traffic and dog-walkers made their way around campus.