With the Bank of Japan maintaining its ultra dovish stance of negative interest rates, the rate differentials between the U.S. and Japan’s central bank will persist, said Goldman Sachs economists.

Bloomberg | Bloomberg | Getty Images

The U.S. Federal Reserve, Bank of Japan and European Central Bank will all announce key interest rate decisions this week, with each potentially nearing a pivotal moment in their monetary policy trajectory.

As Goldman Sachs strategist Michael Cahill put it in an email Sunday: “This should be a momentous week.”

“The Fed is expected to deliver what could be the last hike of a cycle that has been one for the books. The ECB will likely signal that it is coming close to the end of its own cycle out of negative rates, which is a big ‘mission accomplished’ in its own right,” G10 FX Strategist Cahill said.

“But as they are coming to a close, the BoJ could out-do them all by finally getting out of the starting blocks.”

The Fed

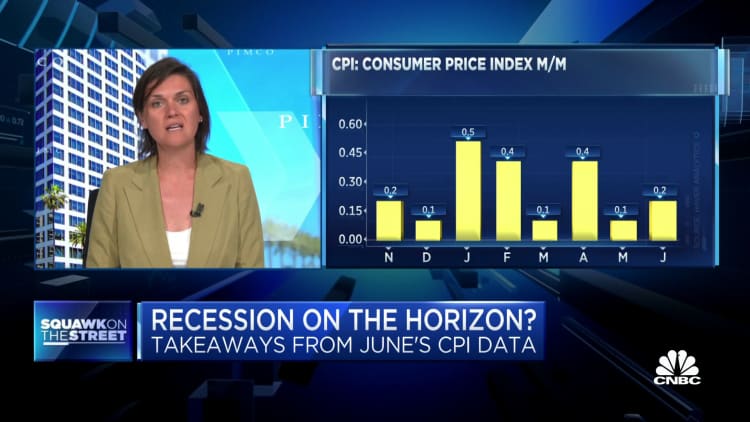

Each central bank faces a very different challenge. The Fed, which concludes its monetary policy meeting on Wednesday, last month paused its run of 10 consecutive interest rate hikes as June consumer price inflation stateside fell to its lowest annual rate in more than two years.

But the core CPI rate, which strips out volatile food and energy prices, was still up 4.8% year-on-year and 0.2% on the month.

Policymakers reiterated their commitment to bringing inflation down to the central bank’s 2% target, and the latest data flow has reinforced the impression that the U.S. economy is proving resilient.

The market is all but certain that the Federal Open Market Committee will opt for a 25 basis point hike on Wednesday, taking the target Fed funds rate to between 5.25% and 5.5%, according to the CME Group FedWatch tool.

Yet with inflation and the labor market now cooling consistently, Wednesday’s expected hike could mark the end of a 16-month run of almost constant monetary policy tightening.

“The Fed has communicated its willingness to raise rates again if necessary, but the July rate hike could be the last — as markets currently expect — if labor market and inflation data for July and August provide additional evidence that wage and inflationary pressures have now subsided to levels consistent with the Fed’s target,” economists at Moody’s Investors Service said in a research note last week.

“The FOMC will, however, maintain a tight monetary policy stance to aid continued softening in demand and consequently, inflation.”

This was echoed by Steve Englander, head of global G10 FX research and North America macro strategy at Standard Chartered, who said the debate going forward will be over the guidance that the Fed issues. Several analysts over the past week have suggested that policymakers will remain “data dependent,” but push back against any talk of interest rate cuts in the near future.

“There is a good case to be made that September should be a skip unless there is a significant upside inflation surprise, but the FOMC may be wary of giving even mildly dovish guidance,” Englander said.

“In our view the FOMC is like a weather forecaster who sees a 30% chance of rain, but skews the forecast to rain because the fallout from an incorrect sunny forecast is seen as greater than from an incorrect rain forecast.”

The ECB

Downside inflation surprises have also emerged in the euro zone of late, with June consumer price inflation across the bloc hitting 5.5%, its lowest point since January 2022. Yet core inflation remained stubbornly high at 5.4%, up slightly on the month, and both figures still vastly exceed the central bank’s 2% target.

The ECB raised its main interest rate by 25 basis points in June to 3.5%, diverging from the Fed’s pause and continuing a run of hikes that began in July 2022.

The market is pricing in a more-than 99% chance of a further 25 basis point hike upon the conclusion of the ECB’s policy meeting on Thursday, according to Refinitiv data, and key central bank figures have mirrored transatlantic peers in maintaining a hawkish tone.

ECB Chief Economist Philip Lane last month warned markets against pricing in cuts to interest rates within the next two years.

With a quarter-point hike all but predetermined, as with the Fed, the key focus of Thursday’s ECB announcement will be what the Governing Council indicates about the future path of policy rates, said BNP Paribas Chief European Economist Paul Hollingsworth.

“In contrast to June, when President Christine Lagarde said that ‘it is very likely the case that we will continue to increase rates in July’, we do not expect her to pre-commit the Council to another hike at September’s meeting,” Hollingsworth said in a note last week.

“After all, recent comments suggest no strong conviction even among the hawks for a September hike, let alone a broad consensus to signal its likelihood already this month.”

Given this lack of an explicit direction, Hollingsworth said traders will be reading between the lines of the ECB’s communication to try to establish a bias toward tightening, neutrality or a pause.

At its last meeting, the Governing Council said its “future decisions will ensure that the key ECB interest rates will be brought to levels sufficiently restrictive to achieve a timely return of inflation to the 2% medium-term target and will be kept at those levels for as long as necessary.”

BNP Paribas expects this to remain unchanged, which Hollingsworth suggested represents an “implicit bias for more tightening” with “wiggle room” in case incoming inflation data disappoints.

“The message in the press conference could be more nuanced, however, suggesting that more might be needed, rather than that more is needed,” he added.

“Lagarde could also choose to reduce the focus on September by pointing towards a possible Fed-style ‘skip’, which would leave open the possibility of hikes at subsequent meetings.”

The Bank of Japan

Far from the discussion in the West about the last of the monetary tightening, the question in Japan is when its central bank will become the last of the monetary tighteners.

The Bank of Japan held its short-term interest rate target at -0.1% in June, having first adopted negative rates in 2016 in the hope of stimulating the world’s third-largest economy out of a prolonged “stagflation,” characterized by low inflation and sluggish growth. Policymakers also kept the central bank’s yield curve control (YCC) policy unchanged.

Yet first-quarter growth in Japan was revised sharply higher to 2.7% last month while inflation has remained above the BOJ’s 2% target for 15 straight months, coming in at 3.3% year-on-year in June. This has prompted some early speculation that the BOJ may be forced to finally begin reversing its ultra-loose monetary policy, but the market is still pricing no revisions to either rates or YCC in Friday’s announcement.

Yield curve control is usually a temporary measure in which a central bank targets a longer-term interest rate, then buys or sells government bonds at a level necessary to hit that rate.

Under Japan’s YCC policy, the central bank targets short-term interest rates at -0.1% and the 10-year government bond yield at 0.5% above or below zero, with the aim of maintaining the inflation target at 2%.

Barclays noted Friday that Japan’s output gap — the difference between actual and potential economic output — was still negative in the first quarter, while real wage growth remains in negative territory and the inflation outlook is uncertain. The British bank’s economists expect a shift away from YCC at the central bank’s October meeting, but said the vote split this week could be important.

“We think the Policy Board will reach a majority decision, with the vote split between relatively hawkish members emphasizing the need for YCC revision (Tamura, Takata) and more neutral members, including Governor Ueda, and dovish members (Adachi, Noguchi) in the reflationist camp,” said Barclays Head of Economics Research Christian Keller.

“We think this departure from a unanimous decision to maintain YCC could fuel market expectations for future policy revisions. In this context, the July post-MPM press conference and the summary of opinions released on 7 August will be particularly important.”