[ad_1]

CNBC’s Jim Cramer joins the ‘Halftime Report’ with Jamie Dimon, JPMorgan CEO, to discuss artificial intelligence and inflation’s impact on the economy.

02:04

Thu, Feb 23 202312:42 PM EST

[ad_2]

[ad_1]

CNBC’s Jim Cramer joins the ‘Halftime Report’ with Jamie Dimon, JPMorgan CEO, to discuss artificial intelligence and inflation’s impact on the economy.

02:04

Thu, Feb 23 202312:42 PM EST

[ad_2]

[ad_1]

CNBC’s Jim Cramer joins the ‘Halftime Report’ with Jamie Dimon, JPMorgan CEO, to discuss the company’s investment in underserved areas in the country and the state of the economy.

02:35

Thu, Feb 23 202312:40 PM EST

[ad_2]

[ad_1]

Medicare will not provide broader coverage of the Alzheimer’s drug Leqembi until it receives more evidence that the treatment is reasonable and necessary, according to the federal agency that runs the program for seniors.

The Centers for Medicare and Medicaid Services rejected a request from the Alzheimer’s Association for unrestricted coverage of antibody treatments approved by the Food and Drug Administration that target brain plaque associated with the devastating disease.

“After careful review of the request and supporting documentation, we are making this decision because, as of the date of this letter, there is not yet evidence meeting the criteria for reconsideration,” CMS said in a statement on Wednesday.

The FDA cleared Leqembi on an expedited basis in January after clinical trial results showed that the treatment slowed cognitive decline by 27% in patients with early Alzheimer’s disease. The drug also carries risks of brain swelling and bleeding.

Leqembi was developed by the Japanese pharmaceutical company Eisai and its partner Biogen. When drugs like Leqembi are approved on expedited basis, Medicare will only cover them for patients who are participating in clinical trials.

“As defined in statute, to provide coverage nationally, CMS is required to examine whether a medication is reasonable and necessary,” the agency said in its statement. “This standard differs from the criteria used by the FDA to assess whether medications are safe and effective.”

Eisai, which completed its phase three trial, has priced Leqembi at $26,500 per year. Due to the drug’s high price and Medicare’s coverage restrictions, seniors are unable to access the treatment.

The Alzheimer’s Association, in a statement Wednesday, said it was “appalled” by CMS’ decision.

“CMS’ role is to provide health care coverage. Their role is not to stand between a patient and a doctor when deciding what FDA-approved treatments are appropriate. Their role is not to single out people living with Alzheimer’s and decide that their lives, their independence and their memories are not necessary,” said the association’s president Joanne Pike.

The letter the Alzheimer’s Association sent to CMS in December calling for unrestricted coverage was signed by more than 200 researchers and experts. The American Academy of Neurology has also told CMS that its experts reviewed Eisai’s clinical trial and concluded that the study was well designed and Leqembi provides a clinical benefit.

The Alzheimer’s Association estimates that 2,000 people ages 65 and older progress from mild dementia to a more advanced stage of the disease per day, which would make them ineligible for Leqembi.

CMS said it would provide broader coverage of Leqembi on the same day should the FDA fully approve the treatment. Eisai U.S. CEO Ivan Cheung told CNBC last week that the company expects to receive full FDA approval this summer.

But even with full approval, Medicare’s policy is to cover Alzheimer’s treatments for patients who agree to participate in research studies that collect real-world data. While coverage would be broader, such studies need to be set up and health-care providers have to agree to participate. This would likely still limit the number of people who can access the drug.

But Cheung told CNBC that Medicare could agree to even broader coverage, possibly with no restrictions, if CMS determines that there’s a high level of evidence supporting the treatment.

“With a high level of evidence … the restrictions should be very limited, or maybe even no restrictions and that is Eisai’s position,” Cheung said. “We believe Medicare beneficiaries should have unimpeded access, broad and simple access to Leqembi because the data fulfill those criteria.”

Members of Congress, including 20 senators and more than 70 House members, have called on CMS to change its policy and offer broader coverage of Alzheimer’s antibody treatments. People living in rural and underserved communities face a disadvantage because the institutions that host clinical trials are usually in bigger cities.

“Patients, families, and caregivers living in rural and underserved areas should have the same opportunity for access to treatment,” the House lawmakers told Health and Human Services Secretary Xavier Becerra and CMS Administrator Chiquita Brooks-LaSure. “It is an enormous physical and financial burden for Medicare beneficiaries to spend countless hours traveling to limited research institutions that host the trials.”

Medicare adopted the coverage restrictions after controversy over the Alzheimer’s antibody treatment Aduhelm, which was also developed by Eisai and Biogen. The FDA approved that treatment over the objections of its independent advisors, who said the data did not demonstrate a benefit for patients. Three advisors resigned over the FDA decision, and a congressional investigation found irregularities in the approval process.

Join CNBC’s Healthy Returns on March 29th, where we’ll convene a virtual gathering of CEOs, scientists, investors and innovators in the health care space to reflect on the progress made today to reinvent the future of medicine. Plus, we’ll have an exclusive rundown of the best investment opportunities in biopharma, health-tech and managed care. Learn more and register today: http://bit.ly/3DUNbRo

[ad_2]

[ad_1]

A sign for hire is posted on the window of a Chipotle restaurant in New York, April 29, 2022.

Shannon Stapleton | Reuters

Job cuts are rising at some of the biggest U.S. companies, but others are still scrambling to hire workers, the result of wild swings in consumer priorities since the Covid pandemic began three years ago.

Tech giants Meta, Amazon and Microsoft, along with companies ranging from Disney to Zoom, have announced job cuts over the past few weeks. In total, U.S.-based employers cut nearly 103,000 jobs in January, the most since September 2020, according to a report released earlier this month from outplacement firm Challenger, Gray & Christmas.

Meanwhile, employers added 517,000 jobs last month, nearly three times the number analysts expected. This points to a labor market that’s still tight, particularly in service sectors that were hit hard earlier in the pandemic, such as restaurants and hotels.

The dynamic is making it even harder to predict the path of the U.S. economy. Consumer spending has remained robust and surprised some economists, despite headwinds such as higher interest rates and persistent inflation.

All of it is part of the Covid pandemic’s “legacy of weirdness,” said David Kelly, global chief strategist at J.P. Morgan Asset Management.

The Bureau of Labor Statistics is scheduled to release its next nonfarm payroll on March 3.

Some analysts and economists warn that weakness in some sectors, strains on household budgets, a drawdown on savings and high interest rates could further fan out job weakness in other sectors, especially if wages don’t keep pace with inflation.

Wages for workers in the leisure and hospitality industry rose to $20.78 per hour in January from $19.42 a year earlier, according to the most recent data from the Bureau of Labor Statistics.

“There’s a difference between saying the labor market is tight and the labor market is strong,” Kelly said.

Many employers have faced challenges in attracting and retaining staff over the past few years, with challenges including workers’ child care needs and competing workplaces that might have better schedules and pay.

With interest rates rising and inflation staying elevated, consumers could pull back spending and spark job losses or reduce hiring needs in otherwise thriving sectors.

“When you lose a job you don’t just lose a job — there’s a multiplier effect,” said Aneta Markowska, chief economist at Jefferies.

That means while there might be trouble in some tech companies, that could translate to lower spending on business travel, or if job loss rises significantly, it could prompt households to pull back sharply on spending on services and other goods.

Some of the recent layoffs have come from companies that beefed up staffing over the course of the pandemic, when remote work and e-commerce were more central to consumer and company spending.

Amazon last month announced 18,000 job cuts across the company. The Seattle-based company employed 1.54 million people at the end of last year, nearly double the number at the end of 2019, just before the pandemic, according to company filings.

Microsoft said it’s cutting 10,000 jobs, about 5% of its workforce. The software giant had 221,000 employees as of the end of June last year, up from 144,000 before the pandemic.

Tech “used to be a grow-at-all-costs sector, and it’s maturing a little bit,” said Michael Gapen, head of U.S. economic research at Bank of America Global Research.

Other companies are still adding employees. Boeing, for example, is planning to hire 10,000 people this year, many of them in manufacturing and engineering. It will also cut around 2,000 corporate jobs, mostly in human resources and finance departments, through layoffs and attrition. The growth aims to help the aerospace giant ramp up output of new aircraft for a rebound in orders with large sales to airlines like United and Air India.

Airlines and aerospace companies were devastated early in the pandemic when travel dried up and are now playing catch-up. Airlines are still scrambling for pilots, a shortage that has limited capacity, while demand for experiences such as travel and dining has surged.

Chipotle is planning to hire 15,000 workers as it gears up for a busier spring season and to support its expansion.

Businesses large and small are also finding they have to raise wages to attract and retain workers. Industries that fell out of favor with consumers and other businesses, such as restaurants and aerospace, are rebuilding workforces after shedding workers. Walmart said it would raise minimum pay for store employees to $14 an hour to attract and retain workers.

The Miner’s Hotel in Butte, Montana, raised hourly pay for housekeepers by $1.50 to $12.50 for that position in the last six weeks because of a high turnover rate, Cassidy Smith, its general manager.

Airports and concessionaires have also been racing to hire workers in the travel rebound. Phoenix Sky Harbor International Airport has been holding monthly job fairs and offers some staff child-care scholarships to help hiring.

Austin-Bergstrom International Airport, where schedules by seats this quarter has grown 48% from the same period of 2019, has launched a number of initiatives, such as $1,000 referral bonuses, and signing and retention incentives for referred staff.

The airport also raised hourly wages for airport facilities representatives from $16.47 in 2022 to $20.68 in 2023.

“Austin has a high cost of living,” said Kevin Russell, the airport’s deputy chief of talent.

He said employee retention has improved.

Electricians, plumbers and heating-and-air conditioning technicians in particular, however, have been difficult to retain because they can work at other places that aren’t 24/7 and at at higher pay, he said.

Many companies’ new workers need to be trained, a time-consuming element for some industries to ramp back up, even if it’s gotten easier to attract new employees.

“Hiring is not a constraint anymore,” Boeing CEO Dave Calhoun said on an earnings call in January. “People are able to hire the people they need. It’s all about the training and ultimately getting them ready to do the sophisticated work that we demand.”

— CNBC’s Amelia Lucas contributed to this article.

[ad_2]

[ad_1]

New homes at the Cielo at Sand Creek by Century Communities housing development in Antioch, California, U.S., on Thursday, March 31, 2022.

David Paul Morris | Bloomberg | Getty Images

Chicago realtor Jeremy Fisher headed to Florida after Christmas counting on five mostly-relaxed weeks, after a slow second half of 2022 left him with a bunch of unsold listings exiting the year.

Instead, the Compass broker ended up flying back to the Windy City three times during his low season, as seven homes went into contract and his husband ended up driving their baby home from Florida alone. The great real estate bust, it seems, has found something like a floor.

“For somebody, it’s always the right time to buy a house,” Fisher said. “People for the most part have come to terms with interest rates.”

After only a few months in the tank, is the U.S. housing market close enough to a bottom that it’s time for those on the sidelines to at least start thinking about buying as spring shopping season nears?

Signs are accumulating that the big price bust — and mortgage-rate relief — that buyers wanted isn’t materializing, at least not soon.

Goldman Sachs trimmed its estimate of peak-to-trough declines in nationwide home prices to 6 percent from 10 percent in late January. Online housing marketplace Zillow now expects prices to rise slightly in 2023. Existing home sales, which were running at a 6.5 million annual pace in early 2021, have begun to stabilize around 4 million, with the National Association of Realtors forecasting 4.8 million for the year. Meanwhile, mortgage rates, which dipped under a 6 percent national average on Feb. 2 after more than doubling since mid-2021 to almost 7.4 percent, have jumped back to 6.75 percent, driven by a scorching January jobs report.

Instead of a price bust a la the one after the mid-2000s housing bubble, what’s developing is a standoff, says Logan Mohtashami, lead analyst for HousingWire in Irvine, Calif. On the one hand are buyers who would like homes to be as affordable as in 2019. But a big share of them either have to move or can afford to despite higher prices and rates. On the other are sellers, under no pressure to move since they have cheap mortgages and plenty of equity for now. So far, sellers are hanging tough in most cities. Even small increases in demand can keep prices firm, or move them higher, because inventory is so tight, Mohtashami said.

The recipe for 2023’s housing market is shaping up as prices that are roughly stable nationally, but with ongoing drops in some regional markets, interest rates that decline but not hugely, and buyers’ incomes that rise. Experts think they will combine to make affordability improve, maybe to near-normal historical levels, but still fall well short of where home buyers stood when mortgage rates were 3 percent or even lower.

“Households have two incomes, and you have to earn about $100,000 to buy a house,” Mohtashami said. “There are lots of dual-income couples that can do that. It gives you more buying power than people know about.”

The biggest reason why housing prices aren’t plunging like they did after 2008? Because the market isn’t being flooded with homes that drive down prices, as happened then.

Capital-rich banks aren’t under pressure as they were then, with foreclosure rates less than a tenth of those from the housing bust. Neither are households, with debt payment burdens near historic lows and few homeowners owing more on their mortgage than the house is worth. Serious delinquency rates, which skyrocketed after 2006 and led to 6 million foreclosures, have fallen by nearly half in the last year, to less than 0.7% of mortgages, according to Fannie Mae. Unemployment is the lowest in 54 years, letting homeowners either trade up or hang on to their current homes easily – and if they are among the 85 percent of owners whose mortgages carry interest rates below 5 percent, many will stay put rather than buy a more expensive house with a costlier loan.

All that means the supply of homes for sale is likely to stay tight, which limits price declines.

Affordability is bad now, after rate hikes and Covid-driven price increases, but it has been worse. And we’ve all been spoiled by recent history: After the financial crisis, housing affordability nationally literally doubled as interest rates collapsed and prices fell, reaching all-time highs. It had retained most of those gains up until the Covid price surge, even as home values recovered.

“Rates will be dropping in the second quarter, but we don’t see a drastic drop that should make people wait,” said Nadia Evangelou, director of real estate research at the NAR. She predicted that 30-year mortgages will decline to around 5.75 percent. “Buyers realize 3 percent rates are not coming back.”

The NAR’s closely-watched affordability index, which considers prices, rates and buyers’ incomes, is much lower than in 2019, but is still in line with the late 1980s and early 1990s. At current levels, the Housing Affordability Index says the median buyer can afford the median U.S. home — but barely. In 2020, the median buyer could afford the median home with a 70 percent cushion, which was the product of 3% loans, Covid-driven income support and the residual impact of big home price drops between 2006 and 2011. Since 1980, the average is that median home buyers have about 20% more income than they need for the median home, Evangelou said.

So why is anyone buying homes that are suddenly less affordable?

For Maggie Neuder, a client of Fisher’s in Chicago, the answer boiled down to wanting a new place and being able to afford one. Having seen 6 percent interest rates when she bought her first place in 2007, she’s not daunted by today’s rates, she said. The 41-year old finance executive bought a bigger home than she needed during Covid to ride out quarantines, and now wants a smaller place in the city’s Lincoln Park neighborhood, so she executed a flip.

To calm her buyer’s interest rate fears, she is giving a closing credit big enough to buy down the mortgage rate on the buyer’s loan for the first two years, by two percentage points in year one and one percentage point in year two – a move many builders are also using to sell new homes. To make back the money, she extracted a similar concession from the seller of the home she expects to buy in April.

“People look at refinancing like it’s a bad thing,” she said, figuring she can likely lower her payment within a couple of years. “I don’t think we’re going back to the sub-threes, but somewhere in the fours. Even if rates don’t fall below 6, I’m in a comfortable place with my mortgage.”

Fisher says his recent buyers fall into three camps. At either end are first-time buyers who have never had a 3 percent loan, and older buyers who are paying cash. Neither is much bothered by rates around 6 percent, he said. In the middle are move-up buyers who initially worried about rates more. But they are making work-arounds like Neuder’s to get what they want, Fisher said. These buyers likely drove the increase in applications for new mortgages that happened as rates fell earlier this winter.

“People have wrapped their heads around where interest rates are, and they have adapted,” Fisher said.

Indeed, combining the wage gains of the last few years with the deflation that has begun to show in market-based housing data in the last six months, and the most flagrant cases of distorted regional markets have begun to correct already. Another boost comes from solid rates of new household formation, said Daryl Fairweather, chief economist at Redfin.

The average house price is down 6 percent since the June peak, according to the S&P Case-Shiller index of prices in 20 major metro areas, and 3.5% in the index for the whole country.

Recently-hot markets have taken bigger hits, as expected. In San Francisco, the Case-Shiller index is down 12 percent, in Phoenix 8 percent. In Sacramento, home prices have given back almost half of their Covid-era gains, said Ryan Lundquist, a local appraiser who blogs about the market in California’s capital. In metro Tampa, where prices rose 69 percent during Covid, according to Case-Shiller, prices are down only 3 percent.

Add in wage growth — wages rose about 5 percent last year, according to data from Zillow — and the effective price of housing has come down sharply in some places, while remaining well above pre-Covid levels, Zillow chief economist Skylar Olsen said.

“Even with values down a bit since August, if you bought the average house in February 2020 you have annual gains of 11 percent,” Olsen said.

Wage growth is one reason why even in some recently-hot markets, buyers are still out there, said St. Petersburg, Fla. broker Jeffrey Clarke. Indeed, he recently talked one client with a home in another city out of selling their place in St. Petersburg, convincing them that the crash they feared was not coming.

By the NAR’s numbers, affordability is now poor in metro Tampa, with the median buyer only earning 80 percent of what’s needed to buy the median home. But Tampa is close enough to equilibrium that Clarke doesn’t see anything coming like 2008-2011, when the average Tampa house lost half of its value.

“With nothing falling yet, no one is freaking out,” he said.

The big flaw in the thesis that only minor price drops are coming is that so many large regional markets like Tampa remain out of line with local incomes, and many of them were in much better balance as recently as two years ago. Another is that San Francisco, Phoenix and Las Vegas all saw more than a 1% price drop in January alone, according to Zillow, making forecasts for relatively-stable prices look shakier.

Much of Florida and Texas, and markets like Asheville N.C. and Denver, had relatively-affordable housing until 2020 but median homes are now 20 percent to 30 percent too expensive for median local incomes, according to NAR data released in October. In much of California, NAR affordability indexes are at 50 or below, indicating homes cost twice as much as local incomes can support. But much of California has always been less affordable.

Nationally, to get back to the average affordability since 1980, meaning median houses are about 20 percent cheaper than the median family can afford, mortgage rates would have to come down to about 4.6 percent, while wages would need to rise 4% and prices stay stable, the NAR’s Evangelou said. Wage growth has recently cooled a little, but remains above 4% — in the recent nonfarm payrolls report, wages were up 4.4% from a year ago, though a bit below the December gain of 4.6%.

Mortgage rates remain volatile, and the market hopes that began 2023 — that the Fed would be cutting its benchmark interest rates before year-end — have recently dimmed as the labor market and consumer remain too strong to provide confidence that the current rates hikes are doing enough to slow inflation. After falling for five weeks, the average contract interest rate for 30-year fixed-rate mortgages increased to 6.39% from 6.18% last week, and was as high as 6.8% on Friday. The rate was 4.05% one year ago.

How fast could affordability get better? On a $300,000 loan, a drop in fixed rates to 4.5 percent from today’s 6.75 percent, with no change in prices, would change the monthly payment by about $425 on a 30-year loan, about a 23 percent drop. Going to 6 percent cuts a payment by about $150, or 8 percent. A 5 percent income gain this year for the median buyer would add about another $400 a month.

“If rates come down to 5 percent, it gets radically better very fast,” Olsen said.

In a place like Tampa where prices grew rapidly during Covid, the affordability fix will probably blend near-stagnant prices for a year or two, pay raises and lower interest rates, Clarke said. But hotter markets like Tampa may need more price cuts to get affordability all the way back to historical averages, Evangelou said.

The market’s standstill is likely to last for months, at least, because its main underpinnings aren’t going anywhere. Sellers will continue to have the advantage of being equity-rich and sitting on a low interest rate from 2021 or before, Mohtashami says. Some buyers will remain priced out of the market, or able to afford less house than they want. And some will use work-arounds like mortgage buydowns or parental support to buy houses until affordability recovers. Sellers of new homes will do buydowns and have been using incentives since last summer to limit cuts to list prices.

“It has become kind of the norm,” Neuder said.

In some markets, affordability is likely to remain a problem for long enough that policy solutions will be needed, Olsen said. She mentioned solutions like building more dense housing, or letting more homeowners add additional dwelling units such as basement or attic apartments to let families share costs.

In most places, the likely outcome is affordability that falls somewhere between today’s market, where many prospective buyers are stretched and demand is light, and the buyer’s delight that prevailed for close to a decade. The path to that is rising wages, declining inflation that lets interest rates fall, and home prices that give back a still-to-be-determined chunk of the 2021-22 gains – a share that so far is small in most places.

“I want it to be flat the next two years,” said Clarke, the Florida broker. “You can’t rise 20 percent a year for a decade. You end up with a $5 million dollar two-bedroom, two-bath.”

[ad_2]

[ad_1]

Don Peebles, founder of the Peebles Corporation, joins ‘Power Lunch’ to discuss the health of the housing market.

03:36

Thu, Feb 16 20232:49 PM EST

[ad_2]

[ad_1]

The Food and Drug Administration’s independent advisors on Wednesday unanimously recommended over-the-counter use of the nasal spray Narcan to reverse opioid overdoses, which would significantly expand access to the life-saving treatment.

Emergent BioSolutions‘ Narcan is the most commonly sold treatment for opioid overdoses. The FDA is expected to make a decision by March 29 on whether to allow people to buy the four milligram nasal spray without a prescription. The agency is not required to accept its advisors recommendation, though it typically does so.

Emergent BioSolutions said Narcan would be available for the over-the-counter market by late summer if the FDA approves it next month. The company has not yet disclosed how much it would cost.

“We have been working on distribution plans with key stakeholders like retailers and government leaders,” said Matt Hartwig, a spokesperson for the company.

Most states have already issued blanket prescriptions that allow pharmacies to distribute Narcan, generically known as naloxone, without the patient having to present a script. But FDA approval of Narcan for over-the-counter use would allow more people to acquire the treatment more easily in more places.

“If naloxone becomes a nonprescription product, it may be sold in many venues previously unavailable to consumers, including vending machines, convenience stores, supermarkets and big box stores, just like other nonprescription products,” Jody Green, an official at the FDA’s nonprescription drug division, told the advisory committee Wednesday.

Since 1999, more than 564,000 people have died from opioids in the U.S. in three waves — first from prescription opioids, then from heroin and most recently from fentanyl, according to the Centers for Disease Control and Prevention. Opioid overdose deaths spiked 17% during the pandemic from about 69,000 in 2020 to nearly 81,000 in 2021.

The Trump administration first declared the opioid epidemic a public health emergency in 2017. The Biden administration has renewed the emergency declaration every 90 days since the president took office.

“Each day 187 people will die — this is absolutely tragic as we think of not only the individuals themselves, but the families, the communities, the workplaces. This has profound human impact and we are all impacted from this,” Manish Vyas, senior vice president of regulatory affairs at Narcan maker Emergent BioSolutions, told the committee.

Scott Hadland, head of adolescent medicine at Massachusetts General Hospital, said the widespread infiltration of fentanyl into the nation’s drug supply has increased the risk of overdoses. Many people who are exposed to fentanyl take counterfeit pills that they thought were prescribed but actually contain the highly potent and often deadly opioid, Hadland said.

“And increasingly there are secondhand exposures that are also rising,” Hadland, who participated in Emergent BioSolutions’ presentation, told the committee. “We’re seeing rising overdose deaths among toddlers who are coming across fentanyl in public settings or fentanyl that may be elsewhere in the home.”

Hadland said he tells parents to to keep Narcan at their home in case of an emergency. He compared it to a fire extinguisher that families should have for safety reasons but hopefully will never have to use.

“Unfortunately for most young people, families and community members all across this country, current avenues of access are challenging,” Hadland said.

Dr. Bobby Mukkamala of the American Medical Association said Narcan should be as easy to obtain as Tylenol to treat a headache or a decongestant for a stuffy nose. The life-saving nasal spray should be just as common in public places as AED devices that are used to treat people suffering from heart attacks.

Jessica Hulsey, executive director of the Addiction Policy Forum, told the committee during a public comment section that Narcan needs to be priced affordably at no more than $20 per dose if it’s sold over the counter. Narcan is packaged as single doses and it can take multiple doses to reverse an overdose from highly potent fentanyl.

Narcan displaces opioids that bind to receptor sites in a person’s nervous system. By displacing and blocking opioids, the nasal spray prevents fatal overdoses by reversing respiratory depression, said Gay Owens, head of global medical affairs at Emergent BioSolutions.

But Narcan has to be administered as soon as an overdose is suspected, which is why it’s crucial to make sure the instructions for using the nasal spray are simple, the FDA’s Green said.

In a study sponsored by Emergent BioSolutions, more than 90% of 71 participants understood over-the-counter label directions and used the Narcan device correctly during a simulated overdose emergency using mannequins. The participants included people with varying levels of literacy, and both adults and adolescents.

But some participants were confused by the five-step instructions because they were split across the side and back panels of the carton, said said , senior pharmacist at the FDA division that monitors errors in administering medicine. This confusion could result in delayed administration or errors in using the Narcan device correctly when time is of the essence, according to Shah.

These instances occurred despite the fact that the participants were allowed as much time as needed to familiarize themselves with the Narcan instructions, which may not be the case in a real-world overdose emergency, according to Shah.

“Therefore, the data collected does not capture this highest-risk use scenario,” said Shah.

The FDA has proposed that Emergent BioSolutions place all five instructions in sequential order on the back panel of the carton and also include instructions in the device blister pack. The company presented a mockup at the advisory meeting, but the FDA said it has not evaluated it yet.

[ad_2]

[ad_1]

Bill Smead of Smead Capital Management joins ‘The Exchange’ to discuss the economy and the homebuilder trade. He’s been bullish on the homebuilders for nearly a decade.

06:18

Wed, Feb 15 20231:48 PM EST

[ad_2]

[ad_1]

A ‘for sale’ sign hangs in front of a home on June 21, 2022 in Miami, Florida.

Joe Raedle | Getty Images

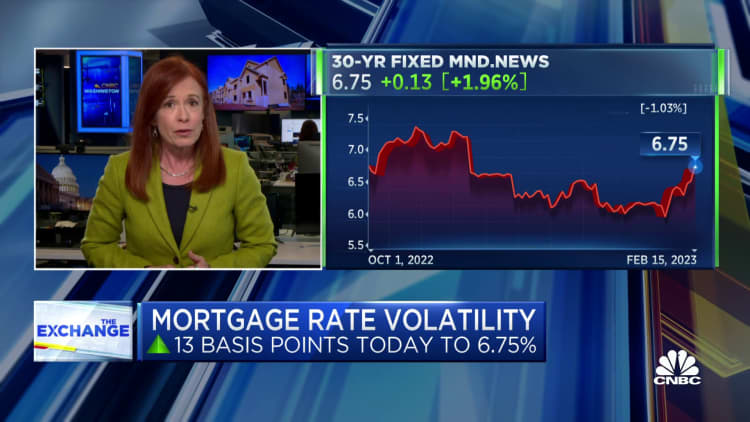

After falling for five straight weeks, mortgage rates jumped last week, triggering a decline in mortgage demand.

Total mortgage application volume fell 7.7% last week, compared with the previous week, according to the Mortgage Bankers Association’s seasonally adjusted index.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($726,200 or less) increased to 6.39% from 6.18%, with points rising to 0.70 from 0.64 (including the origination fee) for loans with a 20% down payment. The rate was 4.05% one year ago.

“Mortgage rates increased across the board last week, pushed higher by market expectations that inflation will persist, thus requiring the Federal Reserve to keep monetary policy restrictive for a longer time,” said Joel Kan, MBA’s vice president and deputy chief economist.

Applications to refinance a home loan dropped 13% for the week and were 76% lower than the same week one year ago. At the current rate, 100,000 fewer borrowers can benefit from a refinance compared with just one week ago, according to data from Black Knight. A year ago, with mortgage rates at 4.05%, there were just under 4 million refinance candidates.

Mortgage applications to purchase a home fell 6% for the week and were 43% lower than the same week a year ago. Real estate agents across the country are reporting a jump in buyer demand in the past few weeks, perhaps indicating an early start to the historically busy spring market.

“I actually thought, my God, this is amazing. Look at how fast it turned on a dime,” said Dana Rice, a real estate agent with Compass, who was running a busy open house in Bethesda, Maryland Saturday. “We went from no showings and nobody coming to open houses, that every single thing that I’ve launched in the last couple of weeks has had multiple offers.”

There is, however, an abnormally high level of all-cash buyers in the market. Peter Fang is one of them. He was at the open house.

“I’m very surprised to see so many cash offers in the market. I thought I would be at a much better position but the competition is still there,” Fang said.

Mortgage rates continued to move higher this week after a government report on inflation showed it was higher than expected in January.

[ad_2]

[ad_1]

CNBC’s Sara Eisen sits down with Brian Moynihan, Bank of America CEO, to get his thoughts on consumer spending, 2023 expectations and mortgages.

05:21

an hour ago

[ad_2]

[ad_1]

Andy Walden, Black Knight, joins ‘The Exchange’ to discuss rising rates and their impact on the housing market heading into the spring.

02:59

Mon, Feb 13 20231:44 PM EST

[ad_2]

[ad_1]

An Optoro warehouse in Tennessee that handles returns for retailers.

Source: Matt Adams | Optoro

As the markets prepare for the latest consumer price index data to be released on Tuesday, logistics managers are warning of a persistent source of inflation in the supply chain and saying consumers should be ready for the effect it will have on their wallets.

While many sources of supply chain inflation that stoked higher goods prices have come down sharply — including ocean freight rates and transportation fuels — bloated inventories due to a lack of consumer demand are sustaining upward pressure on warehouse rates.

“In 2022, we saw rate levels for international air and ocean and domestic trucking fall back down to earth,” said Brian Bourke, global chief commercial officer at SEKO Logistics. “But inflationary pressures remain where demand outpaces supply in 2023, including in warehousing through most of the United States, domestic parcel and labor.”

One reason for the imbalance between warehouse supply and demand is the lack of new facilities coming into the market.

“National warehousing capacity remains low and will remain tight for the foreseeable future as U.S. industrial construction starts have fallen considerably year-over-year due to rising interest rates,” said Chris Huwaldt, vice president of solutions at WarehouseQuote.

Consumer prices have come down sharply as goods inflation that surged during the pandemic has cooled. And Federal Reserve Chairman Jerome Powell expressed confidence after the most recent Fed meeting that disinflation “has begun.” December’s CPI was the smallest year-over-year increase since October 2021, at 6.5% on an annual basis, down from a 9.1% peak in June 2022.

The Fed is now more focused on services inflation, in particular labor prices, as it expects the pressure in goods inflation to continue a downward trend. But the logistics issues suggest there will be some elements of sticky inflation on the goods side of the equation.

“The market is starting to sense that the very comforting disinflation story is more complex than we would like it to be,” Mohamed El-Erian, Allianz chief economic advisor, told CNBC’s “Squawk Box” on Monday morning. “The comforting story was simple: Goods disinflation continues and service inflation comes down, that wonderful concept that Chair Powell calls core services, ex-housing, comes down and, lo and behold, we don’t have an inflation problem. Now we’re starting to see certain goods reverse this inflationary process so there’s more uncertainty about inflation.”

Some shippers are holding their products in containers on chassis because of full warehouses and distribution centers, but this means they’re incurring charges which are passed on to the consumer. Shippers are given an allotted amount of free time during which they are not charged for holding a container, but once those days expire, they start to be charged per diem charges (i.e., late container charges that are charged for containers out of port).

Containers left on chassis create two costly problems, said Paul Brashier, vice president of drayage and intermodal for ITS Logistics. It prevents those chassis from being used to move newly arriving containers, putting additional stress on chassis pools throughout the U.S., especially inland rail ramp pools. Shippers will also be charged fees for the dwelling chassis — separate from the per diem charge shippers pay per day once the container is out of use beyond its free time. “This can lead to tens of millions of dollars in penalties,” Brashier said.

He predicts that per diem charges are going to surge in the second and third quarters of this year.

“These are on top of charges for warehousing, which are still at historic highs,” Brashier said. “Late fees and warehouse fees are passed onto the consumer, which is why we are not seeing products fall as much as they should.”

Shipping containers at a container terminal at the Port of Long Beach-Port of Los Angeles complex, in Los Angeles, California, April 7, 2021.

Lucy Nicholson | Reuters

National storage pricing is up 1.4% month-over-month and 10.6% year-over-year, according to WarehouseQuote.

Many small businesses, which represent the largest share of the U.S. economy in number but are often the last to benefit from a decline in supply chain pricing, tell CNBC they do not believe inflation has peaked.

For shippers with inventory imbalances, Brashier says these charges could cost tens of millions of dollars per quarter. Brashier warns these charges, on top of weaker consumer demand, will ripple through earnings.

ITS Logistics is advising clients to avoid a hit to their bottom line by considering short-term, pop-up storage offered by third-party logistics providers, or 3PL, and grounding operations. “This will reduce reliance on storing freight in ocean containers,” Brashier said.

3PL providers include C.H. Robinson, Expeditors, UPS Supply Chain Solutions, Kuehne + Nagel (Americas), J.B. Hunt, XPO Logistics, GXO Logistics, Uber Freight, and DHL Supply Chain (North America).

Mark Baxa, president and CEO of the Council of Supply Chain Management Professionals, tells CNBC that inflation and higher interest rates are driving supply chain leaders to critically examine working capital investments in inventory and operations in relation to consumer demand forecasts.

“In the short run, supply chains have moved closer to finance teams to manage cash flow, coupled with greater efforts to manage costs across operations. Considerations have moved to close-in review and total cost management across the business, including people, technology, warehousing and transportation investments,” Baxa said.

One industry facing supply chain inflationary headwinds is construction.

Phillip Ross, accounting and audit practice leader of Anchin’s architecture and engineering group, said supply chain inflation has made it more difficult for companies to manage completion times for projects.

“In some cases, we are looking at six to eight months before materials will be available,” Ross said. “Construction, as one of the largest industries in the U.S., is uniquely impacted by the supply chain, which led to construction companies experiencing not only delays in their work but also increased prices for materials.”

Some inflationary elements stemming from Covid-related supply chain disruptions remain, according to Jim Monkmeyer, president of transportation at DHL Supply Chain. These include higher costs related to diversion of containers to East Coast ports, production disruptions and shortages in China and elsewhere, and intermodal constraints forcing higher cost alternatives, such as air freight and expedited truck.

Even with the rate of inflation slowing, higher consumer prices are expected to remain for a variety of other reasons, from contract terms set with suppliers before recent disinflation and company desire to maintain profit margins.

Steve Lamar, CEO of the American Apparel and Footwear Association, tells CNBC that shippers are also finding it harder to absorb extra costs as a result of the Trump-Biden tariffs on China. “These tariffs are now hitting $170 billion and are baked into the cost of goods and, hence, higher prices at the register,” Lamar said. “The tariffs make it harder for companies to absorb other inflationary costs.”

[ad_2]

[ad_1]

An aerial view from a drone shows homes in a neighborhood on January 26, 2021 in Miramar, Florida. According to two separate indices existing home prices rose to the highest level in 6 years.

Joe Raedle | Getty Images

The U.S. housing market cooled off pretty dramatically last year, after mortgage rates more than doubled from historic lows. Home prices, however, have been stickier.

Prices began falling last June, but are still higher than they were a year ago. Now, as demand appears to be coming back into the market, due to a slight drop in mortgage rates, prices are pushing back.

In December, the latest read, U.S. home prices were 6.9% higher year over year, according to CoreLogic. That was the lowest annual appreciation rate since the late summer of 2020. Last April, annual price appreciation hit a high of 20%.

Falling home prices were reflecting weaker housing demand, as inflation, job cuts and uncertainty in the economy piled onto the barrier put up by higher mortgage rates. But mortgage rates began to fall in December, and prices reacted immediately. The cooling continued, but not as much as in the months before.

“While prices continued to fall from November, the rate of decline was lower than that seen in the summer and still adds up to only a 3% cumulative drop in prices since last spring’s peak,” said Selma Hepp, chief economist at CoreLogic.

Hepp notes that some of the exurban areas that became popular during the first years of the pandemic and saw prices rise sharply are now seeing larger corrections. But she doesn’t expect that will last long.

“While price deceleration will likely persist into the spring of 2023, when the market will probably see some year-over-year declines, the recent decrease in mortgage rates has stimulated buyer demand and could result in a more optimistic homebuying season than many expected,” Hepp said.

A monthly survey of homebuying sentiment from Fannie Mae showed an increase in January for the third straight month. Consumers surveyed said they still expected to see prices either fall or flatten over the next year, but the share of those who think it’s a good time to sell a home increased to 59% from 51%.

More inventory on the market would help bring more buyers back into the market. Anecdotally, real estate agents are reporting an earlier-than-usual surge in the spring market, with open houses seeing more foot traffic in the last few weeks. Some also reported the return of bidding wars.

The nation’s homebuilders are also reporting increased demand. Homebuilder sentiment in January rose for the first time in 12 months, the National Association of Home Builders said. Builders reported increases in current sales, buyer traffic and sales expectations over the next six months. Lower mortgage rates are driving the new demand.

“With mortgage rates anticipated to continue to trend lower later this year, affordability conditions are expected to improve, and this will increase demand and bring more buyers back into the market,” said NAHB chief economist Robert Dietz.

The NAHB’s home affordability index started this year at the lowest level since it began tracking the metric a decade ago. But lower rates are starting to turn that around.

If home prices continue to decline at the average rate they have over the past six months, annual home price growth could finally go negative sometime within the next three months, according to a new report from Black Knight. It now takes nearly $600 (+41%) more to make the monthly mortgage payment on the average priced home using a 20% down 30-year rate mortgage than at the same time last year.

Mortgage applications to purchase a home, the most current indicator of demand, rose throughout January and the first week of February, although it is still lower than the same period a year ago, when rates were nearly half what they are now.

“We can see definite signs of a January uptick in purchase lending on lower rates and somewhat lower home prices,” said Ben Graboske, president of Black Knight Data and Analytics. “But affordability still has a stranglehold on much of the market.”

[ad_2]

[ad_1]

Median rents in Manhattan hit a new record in January as a strong job market and limited supply of apartments lifted prices.

The median rental price rose 15% to $4,097 from the year-earlier month — the highest ever in January, according to a report from Douglas Elliman and Miller Samuel. The average rent in Manhattan was $5,142, up 13% over January 2022.

Analysts and real estate experts had expected rents to start falling in January after record surges late last year. But despite a cooling economy and high-profile layoffs in finance and tech, rental demand in Manhattan remains strong.

“We’re not seeing rents fall in any meaningful way” said Jonathan Miller, CEO of Miller Samuel, a real estate appraisal and research company. “They’re really just moving sideways.”

Analysts say the main driver for Manhattan’s rental market is a strong job market. While layoffs at large tech companies and Wall Street banks have made headlines, the overall job market and wage growth remains strong in New York. As more workers return to the office, more employees may also be moving back to the city.

New leases in January surged 8% over December and rose 9% over January 2022 suggesting that while prices are high, renters are still willing to pay them.

At the same time, the inventory of available apartments, while rising, remains low. The vacancy rate — or share of apartments available for rent — was 2.5% last month, below the 3% rate that’s more typical for Manhattan, Miller said.

Joshua Young, executive vice president and managing director of sales and leasing at Brown Harris Stevens, said the rental strength is “a tale of two cities.”

He said there is strong demand for new high-quality rentals coming on the market in prime locations, creating limited supply of top apartments. At the same time, more and more potential apartment buyers are choosing to rent while they wait for sales prices to fall.

“They’re sitting and waiting in rentals until prices come down,” he said. “They don’t want to be the one who buys and overpays for a property that will be worth less in six months.”

Rental demand is especially high in luxury rentals, since many of the potential luxury buyers are choosing to rent. Nearly one in five luxury rentals in January led to a bidding war, Miller said.

Analysts say rents aren’t likely to come down much, if at all, in the coming months, unless the economy and job market loses steam.

“I believe 2023 will be just as strong as 2022 as far as the rental market [goes],” Young said.

[ad_2]

[ad_1]

More than half of smartphone users in the U.S. are sending money via some sort of peer-to-peer payment service to send money to friends, family and businesses.

Stocks of payment services like PayPal, which owns Venmo, and Block, which owns Cash App, boomed in 2020 as more people began sending money digitally.

Zelle, which launched in 2017, stands out from the pack in a few ways. It’s owned and operated by Early Warning Services, LLC, which is co-owned by seven of the big banks and it’s not publicly traded. The platform serves the banks beyond generating an independent revenue stream.

“Zelle is not really a revenue-generating enterprise on a stand-alone basis,” said Mike Cashman, a partner at Bain & Co. “You should think of this really as a little bit of an accommodation, but also as an engagement tool versus a revenue-generating machine.”

“If you’re already transacting with your bank and you trust your bank, then the fact that your bank offers Zelle as a means of payment is attractive to you,” said Terri Bradford, a payment specialist at the Federal Reserve Bank of Kansas City.

One limitation of PayPal, Venmo and Cash App is that users must all be using the same service. Zelle, on the other hand, appeals to users because anyone with a bank account at one of the seven participating firms can make payments.

“For banks, it’s a no-brainer to try to compete in that space,” said Jaime Toplin, senior analyst at Insider Intelligence. “Customers use their mobile-banking apps all the time, and no one wants to cede the opportunity from a space that people are already really active in to third-party competitors.”

Watch the video above to learn more about why the banks created Zelle and where the service may be headed.

[ad_2]

[ad_1]

Prospective buyers at an open house in Florida.

Mike Stocker | South Florida Sun Sentinel | Tribune News Service | Getty Images

The average rate on the 30-year fixed rate mortgage has fallen to 5.99%, according to Mortgage News Daily.

The housing market hasn’t seen the rate with a five handle since a brief blip in early September. Before that, it was in early August.

The rate started this week at 6.21% and fell sharply Wednesday after Federal Reserve Chairman Jerome Powell said inflation “has eased somewhat but remains elevated,” which was a shift from previous language.

That sent bond yields lower, and mortgage rates loosely follow the yield on the 10-year Treasury.

“Measured steps can continue as long as the economic and inflation data is there to support them. This means rates can make progress down into the 5’s but are unlikely to stampede quickly into the 4’s,” said Matthew Graham, chief operating officer at Mortgage News Daily. “I’m not saying that won’t happen–just that it would take a bit more time than some of the rate rallies we remember from the past.”

Mortgage rates peaked in October with the 30-year fixed at 7.37% and have been sliding since then. For potential homebuyers that means savings. For a consumer purchasing a $400,000 home today with a 20% down payment, the monthly payment is $293 less than it would have been in October.

Lower rates already appear to be juicing buyer interest.

Pending home sales, which measure signed contracts on existing homes, rose in December for the first time in six months. They gained 2% compared with November, according to the National Association of Realtors.

Stocks of the nation’s homebuilders have been on a tear since rates started to fall back and several are seeing 52-week highs Thursday. The U.S. Home Construction ETF is hitting a new one-year high, up over 3% on the day.

Homebuilder stocks are also reacting positively to earnings beats reported this week from PulteGroup and last week from the nation’s largest homebuilder, D.R. Horton. Both builders reported seeing renewed buyer interest in December, attributing that to lower mortgage rates.

[ad_2]

[ad_1]

The Federal Reserve raised the target federal funds rate for the eighth time in a row on Wednesday, in its continued effort to tame persistent inflation.

At its latest meeting, the central bank approved a more modest 0.25 percentage point increase after recent signs that inflationary pressures have started to cool.

“The easing of inflation pressures is evident, but this doesn’t mean the Federal Reserve’s job is done,” said Greg McBride, chief financial analyst at Bankrate.com. “There is still a long way to go to get to 2% inflation.”

The federal funds rate, which is set by the U.S. central bank, is the interest rate at which banks borrow and lend to one another overnight. Although that’s not the rate consumers pay, the Fed’s moves do affect the borrowing and saving rates consumers see every day.

This rate hike will correspond with a rise in the prime rate and immediately send financing costs higher for many forms of consumer borrowing — putting more pressure on households already under financial strain.

“Inflation has shredded household budgets and, in many cases, households have had to lean against credit cards to bridge the gap,” McBride said.

On the flip side, “with rates still rising and inflation now declining, it is the best of both worlds for savers,” he added.

Since most credit cards have a variable rate, there’s a direct connection to the Fed’s benchmark. As the federal funds rate rises, the prime rate does, as well, and your credit card rate follows suit within one or two billing cycles.

“Credit card interest rates are already as high as they’ve been in decades,” said Matt Schulz, chief credit analyst at LendingTree. “While the Fed is taking its foot off the gas a bit when it comes to raising rates, credit card APRs almost certainly will keep climbing for at least the next few months, so it is important that cardholders continue to focus on knocking down their debt.”

Credit card annual percentage rates are now near 20%, on average, up from 16.3% a year ago, according to Bankrate. At the same time, more cardholders carry debt from month to month while paying sky-high interest charges — “that’s a bad combination,” McBride said.

At more than 19%, if you made minimum payments toward the average credit card balance — which is $5,474, according to TransUnion — it would take you almost 17 years to pay off the debt and cost you more than $7,528 in interest, Bankrate calculated.

Altogether, this rate hike will cost credit card users at least an additional $1.6 billion in interest charges in 2023, according to a separate analysis by WalletHub.

“A 0% balance transfer credit card remains one of the best weapons Americans have in the battle against credit card debt,” Schulz advised.

Otherwise, consumers should consolidate and pay off high-interest credit cards with a lower-interest personal loan, he said. “The rates on new personal loan offers have climbed recently as well, but if you have good credit, you may be able to find options that feature lower rates that what you currently have on your credit card.”

Rates on 15-year and 30-year mortgages are fixed and tied to Treasury yields and the economy. As economic growth has slowed, these rates have started to come down but are still at a 10-year high, according to Jacob Channel, senior economist at LendingTree.

The average interest rate for a 30-year fixed-rate mortgage is now around 6.4% — up almost 3 full percentage points from 3.55% a year ago.

“Relatively high rates, combined with persistently high home prices, mean that buying a home is still a challenge for many,” Channel said.

This rate hike has increased the cost of new mortgages by around 10 basis points, which translates to roughly $9,360 over the lifetime of a 30-year loan, assuming the average home loan of $401,300, WalletHub found. A basis point is equal to 0.01 of a percentage point.

“We’re still a ways away from the housing market being truly affordable, even if it has recently become a bit less expensive,” Channel said.

Other home loans are more closely tied to the Fed’s actions. Adjustable-rate mortgages, or ARMs, and home equity lines of credit, or HELOCs, are pegged to the prime rate. Most ARMs adjust once a year, but a HELOC adjusts right away. Already, the average rate for a HELOC is up to 7.65% from 4.11% a year ago.

More from Personal Finance:

64% of Americans are living paycheck to paycheck

What is a ‘rolling recession’ and how does it impact you?

Almost half of Americans think we’re already in a recession

Even though auto loans are fixed, payments are getting bigger because the price for all cars is rising along with the interest rates on new loans, so if you are planning to buy a car, you’ll shell out more in the months ahead.

The average interest rate on a five-year new car loan is currently 6.18%, up from 3.96% last year.

The Fed’s latest move could push up the average interest rate even higher, although consumers with higher credit scores may be able to secure better loan terms or look to some used car models for better deals.

Paying an annual percentage rate of 6% instead of 4% would cost consumers $2,672 more in interest over the course of a $40,000, 72-month car loan, according to data from Edmunds.

“The ever-increasing costs of financing remain a challenge,” said Ivan Drury, Edmunds’ director of insights.

Federal student loan rates are also fixed, so most borrowers won’t be affected immediately. But if you are about to borrow money for college, the interest rate on federal student loans taken out for the 2022-23 academic year already rose to 4.99%, up from 3.73% last year and any loans disbursed after July 1 will likely be even higher.

If you have a private loan, those loans may be fixed or have a variable rate tied to the Libor, prime or T-bill rates, which means that as the central bank raises rates, borrowers will likely pay more in interest, although how much more will vary by the benchmark.

Currently, average private student loan fixed rates can range from just under 4% to almost 15%, according to Bankrate. As with auto loans, they also vary widely based on your credit score.

For now, anyone with existing federal education debt will benefit from rates at 0% until the payment pause ends, which the Education Department expects to happen sometime this year.

The good news is that interest rates on savings accounts are finally higher after the recent run of rate hikes.

While the Fed has no direct influence on deposit rates, they tend to be correlated to changes in the target federal funds rate, and the savings account rates at some of the largest retail banks, which have been near rock bottom during most of the Covid pandemic, are currently up to 0.33%, on average.

Also, thanks, in part, to lower overhead expenses, top-yielding online savings account rates are as high as 4.35%, much higher than the average rate from a traditional, brick-and-mortar bank.

Rates on one-year certificates of deposit at online banks are even higher, now around 4.75%, according to DepositAccounts.com.

As the Fed continues its rate-hiking cycle, these yields will continue to rise, as well. However, you have to shop around to take advantage of them, according to Yiming Ma, an assistant finance professor at Columbia University Business School.

“If you haven’t already, it’s really important to benefit from the high interest environment by getting a higher return,” she said.

Still, because the inflation rate is now higher than all of these rates, any money in savings loses purchasing power over time.

[ad_2]

[ad_1]

Vials and a medical syringe seen displayed in front of the Food and Drug Administration (FDA) of the United States logo. FDA finds the COVID-19 vaccine.

Pavlo Gonchar | LightRocket | Getty Images

The Food and Drug Administration on Tuesday said its emergency authorizations of Covid vaccines, tests and treatments will not be impacted by the end of the public health emergency this spring.

President Joe Biden is planning to terminate in May the public health and national emergencies declared in response to the Covid pandemic three years ago, the White House said Monday. The public health emergency gave U.S. health regulators expanded powers to respond faster to the pandemic.

The FDA’s emergency powers, however, aren’t directly tied to public health declaration, according to the agency.

Former Health Secretary Alex Azar made separate determinations in February and March of 2020 under the Food, Drug and Cosmetics Act that the circumstances of the pandemic justified the authorization of vaccines, treatments and tests for emergency use.

The FDA used its emergency powers to authorize the Pfizer, Moderna, Johnson & Johnson and Novavax vaccines. The agency also authorized the oral antivirals Paxlovid and molnupiravir, several antibody treatments as well as numerous tests and other medical devices on an emergency basis.

“Existing emergency use authorizations (EUAs) for products will remain in effect and the agency may continue to issue new EUAs going forward when criteria for issuance are met,” The FDA wrote in post on Twitter Monday.

Emergency authorizations allow the FDA to roll out medical products before they receive the agency’s full approval. This allows the agency to respond more swiftly to public health crises.

[ad_2]

[ad_1]

The Federal Reserve is widely expected to announce its eighth consecutive rate hike at this week’s policy meeting.

This time, Fed officials likely will approve a 0.25 percentage point increase as inflation starts to ease, a more modest pace compared with earlier super-size moves in 2022.

Still, any boost in the benchmark rate means borrowers will pay even more interest on credit cards, student loans and other types of debt. On the flip side, savers could benefit from higher yields.

More from Personal Finance:

What is a ‘rolling recession’ and how does it impact you?

Almost half of Americans think we’re already in a recession

If you want higher pay, your chances may be better now

“The good news is that the worst is over,” said Yiming Ma, an assistant finance professor at Columbia University Business School.

The U.S. central bank is now knee-deep in a rate hike cycle that has raised its benchmark rate by 4.25 percentage points in less than a year.

Although inflation is still above the Fed’s 2% long-term target, pricing pressures have “come down substantially and the pace of rate hikes is going to slow,” Ma said.

The good news is that the worst is over.

Yiming Ma

assistant finance professor at Columbia University Business School

The goal remains to tame runaway inflation by increasing the cost of borrowing and effectively pump the brakes on the economy.

The federal funds rate, which is set by the central bank, is the interest rate at which banks borrow and lend to one another overnight. Whether directly or indirectly, higher Fed rates influence borrowing costs for consumers and, to a lesser extent, the rates they earn on savings accounts.

Here’s a breakdown of how it works:

Since most credit cards have a variable interest rate, there’s a direct connection to the Fed’s benchmark. As the federal funds rate rises, the prime rate does, too, and credit card rates follow suit. Cardholders usually see the impact within a billing cycle or two.

After rising at the steepest annual pace ever, the average credit card rate is now 19.9%, on average — an all-time high. Along with the Fed’s commitment to keep raising its benchmark to combat inflation, credit card annual percentage rates will keep climbing, as well.

Households are also increasingly leaning on credit to afford basic necessities, since incomes have not kept pace with inflation. This makes it even harder for the growing number of borrowers who carry a balance from month to month.

“Credit card balances are rising at the same time credit card rates are at record highs; that’s a bad combination,” said Greg McBride, chief financial analyst at Bankrate.com.

If you currently have credit card debt, tap a lower-interest personal loan or 0% balance transfer card and refrain from putting additional purchases on credit unless you can pay the balance in full at the end of the month and even set some money aside, McBride advised.

Although 15-year and 30-year mortgage rates are fixed and tied to Treasury yields and the economy, anyone shopping for a new home has lost considerable purchasing power, partly because of inflation and the Fed’s policy moves.

“Despite what will likely be another rate hike from the Fed, mortgage rates could actually remain near where they are over the coming weeks, or even continue to trend down slightly,” said Jacob Channel, senior economist for LendingTree.

The average rate for a 30-year, fixed-rate mortgage currently sits at 6.4%, down from mid-November, when it peaked at 7.08%.

Still, “these relatively high rates, combined with persistently high home prices, mean that buying a home is still a challenge for many,” Channel added.

Adjustable-rate mortgages, or ARMs, and home equity lines of credit, or HELOCs, are pegged to the prime rate. As the federal funds rate rises, the prime rate does, as well, and these rates follow suit. Most ARMs adjust once a year, but a HELOC adjusts right away. Already, the average rate for a HELOC is up to 7.65% from 4.11% a year ago.

Even though auto loans are fixed, payments are getting bigger because the price for all cars is rising along with the interest rates on new loans. So if you are planning to buy a car, you’ll shell out more in the months ahead.

The average interest rate on a five-year new car loan is currently 6.18%, up from 3.96% at the beginning of 2022.

Boonchai Wedmakawand | Moment | Getty Images

“Elevated pricing coupled with repeated interest rate increases continue to inflate monthly loan payments,” Thomas King, president of the data and analytics division at J.D. Power, said in a statement.

Car shoppers with higher credit scores may be able to secure better loan terms or look to some used car models for better pricing.

Federal student loan rates are also fixed, so most borrowers won’t be affected immediately by a rate hike. The interest rate on federal student loans taken out for the 2022-23 academic year already rose to 4.99%, up from 3.73% last year and 2.75% in 2020-21. Any loans disbursed after July 1 will likely be even higher.

Private student loans tend to have a variable rate tied to the Libor, prime or Treasury bill rates — and that means that, as the Fed raises rates, those borrowers will also pay more in interest. How much more, however, will vary with the benchmark.

For now, anyone with existing federal education debt will benefit from rates at 0% until the payment pause ends, which the Education Department expects to happen sometime this year.

On the upside, the interest rates on some savings accounts are higher after a run of rate hikes.

While the Fed has no direct influence on deposit rates, the rates tend to be correlated to changes in the target federal funds rate. The savings account rates at some of the largest retail banks, which were near rock bottom during most of the Covid pandemic, are currently up to 0.33%, on average.

Guido Mieth | DigitalVision | Getty Images

Thanks, in part, to lower overhead expenses, top-yielding online savings account rates are as high as 4.35%, much higher than the average rate from a traditional, brick-and-mortar bank, according to Bankrate.

“If you are shopping around, you are finding the best returns since the great financial crisis. If you are not shopping around, you are still earning next to nothing,” McBride said.

Still, any money earning less than the rate of inflation loses purchasing power over time, and more households have less set aside, in general.

“The best advice is pick up a side hustle to bring in some additional income, even if it’s just temporary, and pay yourself first with a direct deposit into your savings account,” McBride advised. “That’s how you are going to create the pathway to be able to save.”

[ad_2]

[ad_1]

The Centers for Disease Control and Prevention on Friday urged people with weak immune systems to take extra precautions to avoid Covid after the dominant omicron subvariants knocked out a key antibody treatment.

These precautions include wearing a high quality mask and social distancing when it’s not possible to avoid crowded indoor spaces, according to the CDC.

The guidance comes after the Food and Drug Administration on Thursday pulled its authorization of Evusheld, a combination antibody injection that people with weak immune systems took as an additional layer of protection to prevent Covid infection.

The FDA pulled Evusheld because it is not effective against 95% of the omicron subvariants circulating in the U.S. This includes the XBB subvariants which are now causing 64% of new cases, as well as the BQ family that is responsible for 31% of reported infections.

Although most Americans have largely returned to normal life as the Covid pandemic has ebbed, people with weak immune systems remain at higher risk of severe disease because they do not mount as strong of an immune response to the vaccines.

Still, it is important for people with weak immune systems to stay up to date on their Covid vaccines by receiving the omicron booster because the shots can slash the risk of severe disease, according to the CDC.

If you have a weak immune system and develop Covid symptoms, you should get tested as soon as possible and receive treatment with an antiviral within five to seven days, according to CDC.

Available antivirals include Paxlovid, remdesivir or molnupiravir, but patients should talk to their doctor to find out which treatment is best. Some people cannot take Paxlovid due to how it interacts with other drugs they are taking.

People with weak immune systems include cancer patients who are on chemotherapy, organ transplant patients who are taking medication for their transplant, people with advanced HIV infection, and those born with immune deficiencies.

Some 7 million adults in the U.S. have a condition, like cancer, that compromises their immune system, according to the CDC.

[ad_2]