[ad_1]

U.S. stocks ended lower Friday, booking their worst annual losses since 2008, as tax-loss harvesting along with anxieties about the outlook for corporate profits and the U.S. consumer took their toll.

How stock indexes traded

-

The Dow Jones Industrial Average

DJIA,

-0.22%

slipped 73.55 points, or 0.2%, to 33,147.25. -

The S&P 500

SPX,

-0.25%

shed 9.78 points, or 0.3%, to 3,839.50. - The Nasdaq Composite dipped 11.61 points, or 0.1%, to 10,466.48.

For the week, the Dow fell 0.2%, the S&P 500 slipped 0.1% and the Nasdaq slid 0.3%. The S&P 500 dropped for a fourth straight week, its longest losing streak since May, according to Dow Jones Market Data.

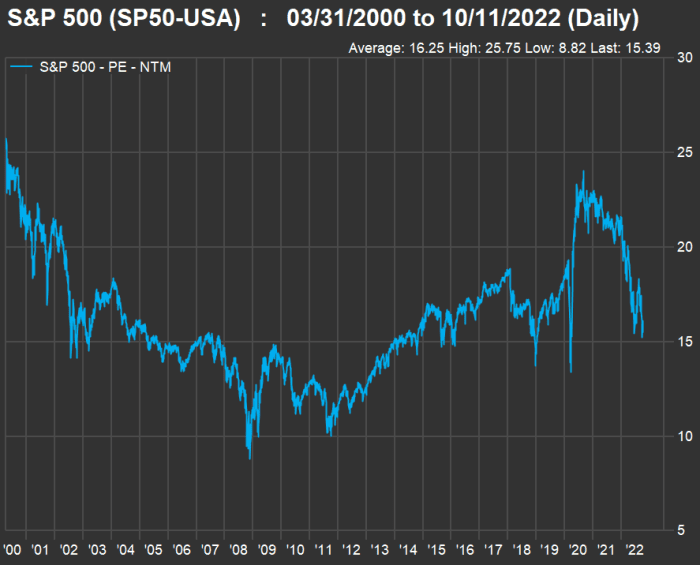

All three major benchmarks suffered their worst year since 2008 based on percentage declines. The Dow dropped 8.8% in 2022, while the S&P 500 tumbled 19.4% and the technology-heavy Nasdaq plunged 33.1%.

What drove markets

U.S. stocks fell Friday, closing out the last trading session of 2022 with weekly and monthly losses.

Stocks and bonds have been crushed this year as the Federal Reserve raised its benchmark interest rate more aggressively than many had expected as it sought to crush the worst inflation in four decades. The S&P 500 ended 2022 with a loss of 19.4%, its worst annual performance since 2008 as the index snapped a three-year win streak, according to Dow Jones Market Data.

“Investors have been on edge,” said Mark Heppenstall, chief investment officer at Penn Mutual Asset Management, in a phone interview Friday. “It seems as though the ability to drive down prices is probably a bit easier given just how crummy the year’s been.”

Stock indexes have slumped in recent weeks as hopes for a Fed policy pivot faded after the central bank in December signaled that it would likely wait until 2024 to cut interest rates.

On the final day of the trading year, markets were also being hit by selling to lock in losses that can be written off of tax bills, a practice known as tax-loss harvesting, according to Kim Forrest, chief investment officer at Bokeh Capital Partners.

An uncertain outlook for 2023 was also taking its toll, as investors fretted about the strength of corporate profits, the economy and the U.S. consumer with fourth-quarter earnings season looming early next year, Forrest said.

“I think the Fed, and then earnings in the middle of January — those are going to set the tone for the next six months. Until then, it’s anybody’s guess,” she added.

The U.S. central bank has raised its benchmark rate by more than four percentage points since the beginning of the year, driving borrowing costs to their highest levels since 2007.

The timing of the Fed’s first interest rate cut will likely have a major impact on markets, according to Forrest, but the outlook remains uncertain, even as the Fed has tried to signal that it plans to keep rates higher for longer.

On the economic data front, the Chicago PMI for December, the last major data release of the year, came in stronger than expected, climbing to 44.9 from 37.2 a month prior. Readings below 50 indicate contraction territory.

Next year, “we’re more likely to shift towards fears around economic growth as opposed to inflation,” said Heppenstall. “I think the decline in growth will eventually lead to a more meaningful decline in inflation.”

Read: Stock-market investors face 3 recession scenarios in 2023

Eric Sterner, CIO of Apollon Wealth Management, said in a phone interview Friday that he’s expecting the U.S. could fall into a recession next year and that the stock market could see a new bottom as companies potentially revise their earnings lower. “I think earnings expectations for 2023 are still too high,” he said.

The Dow Jones Industrial Average, S&P 500 and Nasdaq Composite booked modest weekly declines, adding to their December losses. For the month, the Dow fell 4.2%, while the S&P 500 dropped 5.9% and the Nasdaq sank 8.7%, FactSet data show.

Read: Value stocks trounce growth equities in 2022 by historically wide margin

As for bonds, the U.S. Treasury market was set to record its worst year since at least the 1970s.

The yield on the 10-year Treasury note

TMUBMUSD10Y,

has jumped 2.330 percentage points this year to 3.826%, its largest annual gain on record based on data going back to 1977, according to Dow Jones Market Data.

Two-year Treasury yields

TMUBMUSD02Y,

soared 3.669 percentage points in 2022 to 4.399%, while the 30-year yield

TMUBMUSD30Y,

jumped 2.046 percentage points to end the year at 3.934%. That marked the largest calendar-year increases ever for each based on data going back to 1973, according to Dow Jones Market Data.

Outside the U.S., European stocks capped off their biggest percentage drop for a calendar year since 2018, with the Stoxx Europe 600

SXXP,

an index of euro-denominated shares, falling 12.9%, according to Dow Jones Market Data.

Read: Slumping U.S. stock market lags these international ETFs as 2022 comes to an end

Companies in focus

-

Tesla Inc.

TSLA,

+1.12%

shares rose 1.1% after their worst run of losses in more than four years. -

Southwest Airlines

LUV,

+0.87%

shares gained 0.9% as the company said it expected its holiday travel fiasco to impact fourth-quarter profits. -

Las Vegas Sands Corp.

LVS,

+2.10%

was among the best performers in the S&P 500 index on Friday, with its shares ending 2.1% higher, as it confirmed renewed gaming concessions in Macau.

—Steve Goldstein contributed to this article.

[ad_2]