(Bloomberg) — A selloff in the world’s largest tech companies weighed heavily on stocks, while Treasury yields climbed amid bets the Federal Reserve will take a more measured approach on rate cuts.

Most Read from Bloomberg

Equities extended losses into a third straight day, with the S&P 500 breaking below 5,800. Nvidia Corp. tumbled 4%, leading megacaps lower. Apple Inc. slid 3% after a closely followed analyst said iPhone 16 orders were cut by about 10 million units from the fourth quarter through the first half of 2025. As Tesla Inc. gets ready to report its results, Wall Street will be watching for signs that slowing sales are close to a trough.

FED: ECONOMIC ACTIVITY LITTLE CHANGED IN NEARLY ALL DISTRICTS

Investors face a number of risks that could be making them less willing to jump into the market: The next three weeks capture big tech earnings, October’s payrolls report, and the US election, followed by the Fed meeting. In another sign of Wall Street’s perception of future risk, the term premium on 10-year Treasury notes — an expression of the extra yield investors demand for owning the debt rather than rolling over shorter-term securities — hit the highest since November.

“This is about price exhaustion, this is about election exhaustion, it’s about campaign exhaustion, it’s about Fed exhaustion, it’s about policy exhaustion, it’s about geopolitical exhaustion,” said Kenny Polcari at SlateStone Wealth. “It’s about how stocks are stretched and it’s about the need for stocks to retreat, test lower, shake the branches, see who falls out and then move on.”

The S&P 500 fell 1.4%. The Nasdaq 100 dropped 2.1%. The Dow Jones Industrial Average slipped 1.3%. Boeing Co. dropped after signaling the company’s woes will take time to fix. Qualcomm Inc. got hit as Arm Holdings Plc canceled a license that allowed the company to use Arm’s intellectual property to design chips. Texas Instruments Inc. climbed after its results.

Treasury 10-year yields rose four basis points to 4.25%. A $13 billion sale of 20-year bonds tailed at the highest yield since May. The dollar rose against all of its Group-of-10 peers, on pace for its best month since 2022. The yen hit the lowest in almost three months, reviving concern that Japan may intervene. The loonie slid after the Bank of Canada stepped up the pace of easing.

Oil dropped as US crude inventories rose and the Biden administration renewed efforts to secure a cease-fire in the Middle East. Gold declined from a record.

To Jonathan Krinsky at BTIG, equities are finally noticing the moves in bonds and the dollar. That’s a stark contrast to the moves in the last couple of weeks. The bullish narrative was that bonds were re-pricing to where they should be based on the stronger-than-anticipated economy, he noted.

“While that might be fair in the big picture, markets are always concerned with the velocity of the move rather than the overall level, and the fact that stocks didn’t flinch in the face of those moves suggested complacency,” Krinsky said. Whether this is the start of the pre-election jitters or not, we continue to see downside risk for equities broadly over the coming weeks, with an SPX pullback into the 5,500-5,650 zone a decent probability.”

Swap prices reflect less than a 100% certainty that the central bank reduces rates at each of its two remaining policy meetings this year. The bond market is also trimming bets on the degree of Fed rate reductions over the next year. Traders will get more clarity next week on how much officials are likely to ease, with the release of a key labor-market reading for October.

“The price of options to hedge against Treasury losses is soaring,” said Andrew Brenner at NatAlliance Securities. “In the US, it is about the election and potential sweep. That is what is being built into the rate structure, which is giving the vigilantes the green light. It will reverse, but it might take a severe employment number or a surprise in the election.”

“We would caution investors from reading too much into the recent rise in bond yields,” said Tiffany Wilding at Pacific Investment Management Co. “Over the past six major Fed rate-cutting cycles, the change in the 10-year Treasury yield a month after the first cut has not provided a consistent signal about the magnitude of further cuts or whether the Us economy falls into recession.”

In fact, yields rose in the month after the first cut more often than not, she noted.

“Equity market performance in the first month after the Fed starts cutting has been a similarly bad predictor of future economic performance (and market returns),” Wilding said. “Equities, more often than not, have tended to rise in the month after a cutting cycle begins, despite more significant divergence as time goes on.”

Looking at the same starkly different cycles of 1995 and 2007, equity returns (proxied by the rate-sensitive Russell 2000 of small caps) in the month after the first cut were positive in both cycles (at 4.6% and 6.9%, respectively), Wilding said. However, equity market performance was down 4.4% in the year after the 2007 cut, while it was up 21% in the year following the 1995 adjustment.

“Even with the recent move in 10-year Treasury yields, we remain bullish on US large caps,” said Nicholas Colas at DataTrek Research. “History says to discount the idea that rates will blow out because of deficit worries, at least over the near term. Instead, we see higher yields as a sign that economic growth remains robust and corporate earnings growth should continue over the coming quarters.”

“All else equal, the more rate cuts that are removed for next year the less of an outlier reading it becomes for the market to achieve 15% earnings growth,” said Ryan Grabinski at Strategas. “However, additional rates cuts do not change the challenges the S&P faces with achieving that growth rate.”

Sales growth continues to show signs of slowing, and if analysts were suggesting rate cuts would reduce interest expense, that argument is beginning to recede, Grabinski said.

“Nearly 14% EPS margins continue to look more and more difficult to achieve,” he added. “The question is when does something give.”

“The equity market is extremely fragile considering the headwinds that are lurking right around the corner,” said Jose Torres at Interactive Brokers. “Earnings expectations are buoyant for next year, which increases the importance of forward guidance rather than past results.”

When considering that valuations are around 22 times next year’s profits, any disappointment in the outlook for the bottom line can significantly impact stock market performance, he added.

Corporate Highlights:

AT&T Inc. gained more mobile subscribers in the third quarter than analysts expected, continuing the winning streak from the previous period.

Hilton Worldwide Holdings Inc. lowered its profit outlook, as the addition of new hotels to its global system failed to offset slower travel demand.

Coca-Cola Co. dropped as investors weighed how much longer the soft-drink purveyor could raise prices without getting customers to buy more of its beverages.

Spirit Airlines Inc. jumped after the Wall Street Journal reported Frontier Group Holdings is exploring a renewed bid for the embattled carrier.

Capital One Financial Corp.’s proposed $35 billion acquisition of Discover Financial Services is being investigated by New York Attorney General Letitia James, who said the deal would have “significant impact” on consumers in the state.

Starbucks Corp. pulled its guidance for 2025, calling attention to the scope of the problems facing new Chief Executive Officer Brian Niccol.

McDonald’s Corp. is trying to contain the fallout from a severe E. coli outbreak that appears to be linked to onions in its Quarter Pounder sandwiches, which has killed one person and sickened dozens of people across the US.

Deutsche Bank AG said it will have to set aside more money than expected for souring debt, the second time this year it had to adjust its guidance.

Kering SA warned that its annual profit will fall to the lowest level since 2016 as a slump in Chinese demand for luxury goods hampers a turnaround of the French fashion group’s biggest label, Gucci.

Key events this week:

US new home sales, jobless claims, S&P Global Manufacturing and Services PMI, Thursday

UPS, Barclays earnings, Thursday

Fed’s Beth Hammack speaks, Thursday

US durable goods, University of Michigan consumer sentiment, Friday

Some of the main moves in markets:

Stocks

The S&P 500 fell 1.4% as of 2:06 p.m. New York time

The Nasdaq 100 fell 2.1%

The Dow Jones Industrial Average fell 1.3%

The MSCI World Index fell 1.2%

Currencies

The Bloomberg Dollar Spot Index rose 0.3%

The euro fell 0.3% to $1.0771

The British pound fell 0.5% to $1.2913

The Japanese yen fell 1% to 152.65 per dollar

Cryptocurrencies

Bitcoin fell 3.2% to $65,331.83

Ether fell 6.4% to $2,464.88

Bonds

The yield on 10-year Treasuries advanced four basis points to 4.25%

Germany’s 10-year yield declined one basis point to 2.30%

Britain’s 10-year yield advanced three basis points to 4.20%

Commodities

West Texas Intermediate crude fell 1.2% to $70.85 a barrel

Spot gold fell 1.2% to $2,714.99 an ounce

This story was produced with the assistance of Bloomberg Automation.

HONG KONG (AP) — Asian stocks were mixed Tuesday after stocks advanced on Wall Street and yields jumped in the U.S. bond market as election-related issues swayed markets worldwide.

U.S. futures fell and oil prices rose. The Japanese yen fell to near a fresh 38-year low, reaching 161.67 yen to the dollar early Tuesday.

Tokyo’s benchmark Nikkei 225 added 1.1% to 40,074.69, as the weaker yen spurred buying of export-oriented shares.

Australia’s S&P/ASX 200 shed 0.4% to 7,718.20. South Korea’s Kospi dropped 0.8% to 2,781.92 despite data from Statistics Korea showing the country’s consumer inflation slowed to an 11-month low in June.

Hong Kong’s market was higher after a holiday break on Monday. The Hang Seng climbed 0.3% to 17,775.84 and the Shanghai Composite index edged up 0.1% to 2,995.78.

Elsewhere, Taiwan’s Taiex gained 0.6%, while the SET in Bangkok slipped 0.4%.

On Monday, the S&P 500 rose 0.3% to 5,475.09. The Dow Jones Industrial Average edged up 0.1% to 39,169.52, and the Nasdaq composite gained 0.8% to 17,879.30.

Some of the world’s strongest action was across the Atlantic, where the CAC 40 index in Paris jumped as much as 2.8% before settling to a gain of 1.1%. Results from France suggested a far-right political party may not win a decisive majority in the country’s legislative elections. That bolstered hopes for potential gridlock in the French government, which would prevent a worst-case scenario where a far-right with a clear majority could push policies that would greatly increase the French government’s debt.

This is a big year for elections worldwide, with voters heading to the polls in the United Kingdom later this week and soon elsewhere. In the United States, pollsters are measuring the fallout from last week’s debate between President Joe Biden and former President Donald Trump.

Investors are also eyeing the potential impact from a Supreme Court ruling Monday that former presidents have broad immunity from prosecution, likely extending the delay in a criminal case against Donald Trump to after the November election.

Trump Media & Technology Group, whose stock has been rising and falling with Trump’s White House chances, climbed 1% to $33.08. Shares of the company behind Trump’s Truth Social platform, though, are still well below their perch of roughly $70 reached earlier this year.

Treasury yields jumped, as they did Friday immediately following the Biden-Trump debate. Increased prospects for a Republican sweep in November sent traders back to moves from 2016, according to strategists at Morgan Stanley. Besides pushing rates higher, traders also piled into stocks of energy and financial companies.

The yield on the 10-year Treasury climbed to 4.46% from 4.39% late Friday and from 4.29% late Thursday. It’s a reversal of the general trend since the spring, when the 10-year Treasury yield had topped 4.70% in late April.

Yields had been largely easing on hopes inflation will slow enough to convince the Federal Reserve to cut its main interest rate later this year, down from the highest level in more than two decades. High rates have been grinding on the U.S. economy by making it more expensive to borrow money for a house, car or anything else.

Hopes for rate cuts held after a report on Monday showed U.S. manufacturing weakened last month by more than economists expected. Perhaps even more importantly for Wall Street, the report from the Institute for Supply Management also said price increases are decelerating. Taken together, the data could offer more of the evidence that the Federal Reserve wants to see of lessening pressure on inflation before it will cut rates.

This week’s economic highlight will likely arrive Friday, when the U.S. government will say how many workers employers hired during June. Economists predict overall hiring slowed to 190,000 from May’s 272,000. That would get the number closer to what Bank of America calls the “Goldilocks” figure of roughly 150,000, give or take 25,000.

At that level, the U.S. economy could continue to grow and avoid a recession without being so strong that it puts too much upward pressure on inflation.

In other dealings, benchmark U.S. crude rose 15 cents to $83.53 a barrel in electronic trading on the New York Mercantile Exchange. Brent crude, the international standard, added 23 cents to $86.83 per barrel.

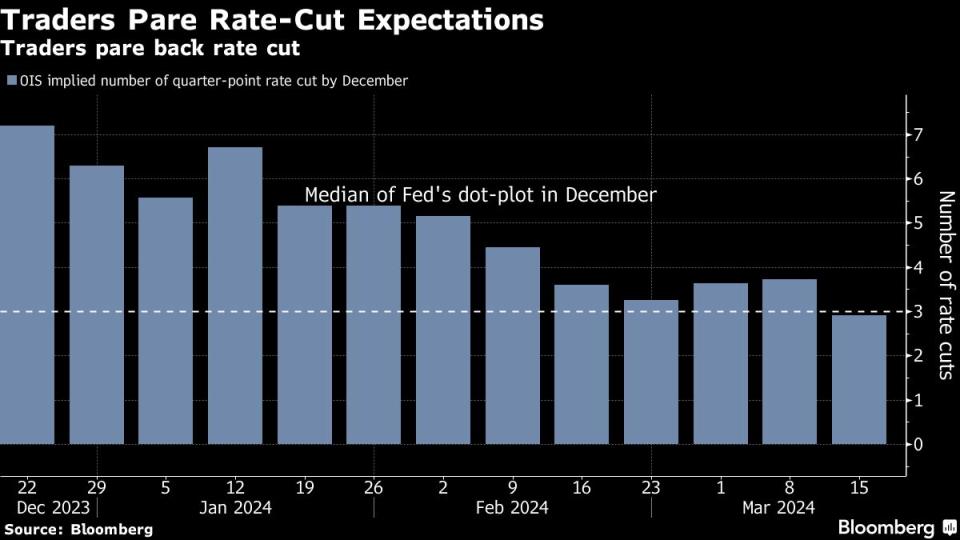

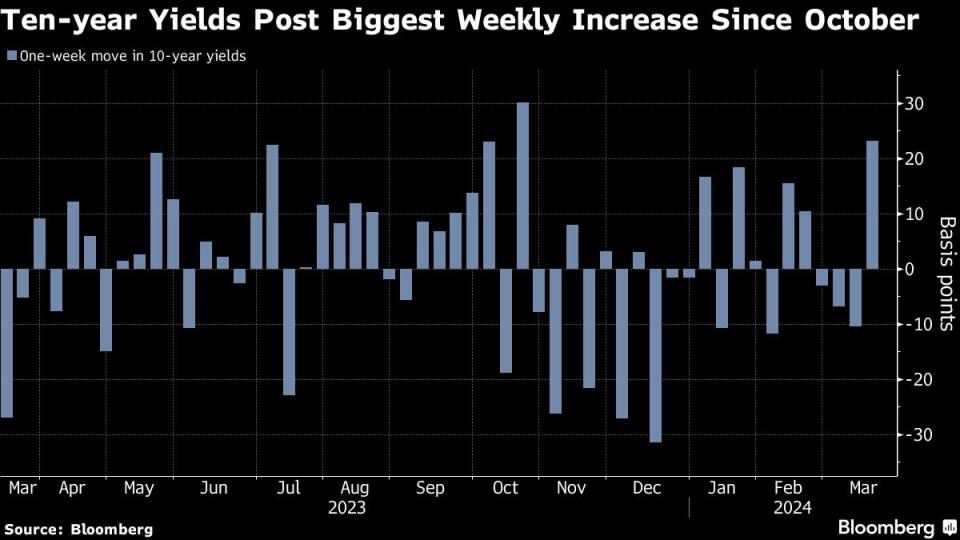

(Bloomberg) — Bond investors who were once convinced that the Federal Reserve would start cutting interest rates this week are painfully surrendering to a higher-for-longer reality and a murky path forward for the market.

Most Read from Bloomberg

Treasury yields spiked in recent days and are on the cusp of setting new highs for the year as data continues to point to persistent inflation, which is causing traders to push back their timetable for US monetary easing.

Interest-rate swaps now reflect market expectations for fewer than three quarter-point rate cuts this year. That’s less than the Fed’s median projection in December and a shade of the six reductions that were priced in at the end of 2023. And the first move lower? Investors are no longer confident that it’ll even happen in the first half of the year.

The shift underscores mounting worries that US central bankers led by Fed Chair Jerome Powell may signal an even shallower easing cycle at this week’s two-day gathering, which begins on Tuesday. Already, economists at Nomura Holdings Inc. scaled back their estimate for Fed rate reductions this year to two cuts from three. And recent trading flows in options markets show investors are seeking protection against the risk of higher long-term yields and fewer rate cuts — even if their longer-term view is for rates to eventually come down.

“The Fed wants to ease but the data isn’t allowing them,” said Earl Davis, head of fixed income and money markets at BMO Global Asset Management. “They want to maintain optionality to ease in summer. But they will start to change, if the labor market is tight and inflation remains high.”

US 10-year yields jumped 24 basis points last week, the most since October, to 4.31% — nearing their year-to-date high of 4.35%. Davis sees 10-year yields rising toward 4.5% a move that would eventually offer an entry point for him to buy bonds. The benchmark rose above 5% last year for the first time since 2007.

Both two- and five-year US yields surged more than 20 basis points, for their biggest rise since May. The selloff extended Treasuries’ losses for the year to 1.84%.

As recently as December, bond traders were all but certain the Fed would start to ease at this week’s meeting. But after a raft of surprisingly strong data on growth and inflation, they see zero chance of action this week, slim odds of a move in May and only a 60% possibility of a cut in June. For the year, traders have penciled in expectations for a total reduction of 71 basis points, meaning a three full-quarter-point cut is no longer seen as guaranteed.

For its part, Nomura now sees the Fed easing in July and December, instead of in June, September and December. “With little urgency to ease, we expect the Fed will wait to see whether inflation is slowing before beginning a rate-cut cycle,” economists including Aichi Amemiya wrote in a note.

The margin to shift the Fed’s median rate projections on its so-called dot-plot is thin. It would take only two policymakers switching to two cuts this year from three for the central bank’s median forecast to move higher.

Read more: Bond Traders Prep for Dot Plot, With Three Cuts in Question

“It’s not going to take a lot” for the median dots to move higher, said Ed Al-Hussainy, a rates strategist at Columbia Threadneedle Investment. “What I am nervous about is the front end of the curve. It’s super-sensitive to the near-term policy path.”

Even if 2024 median rate projections remain intact, the dots in 2025 and 2026 as well as the long-term “neutral” rate — the level seen as neither stoking growth or holding it back — may move higher, a scenario will prompt traders to price in less rate reductions, according to Tim Duy, chief US economist at SGH Macro Advisors LLC.

“We don’t think market participants need to wait for the Fed’s permission” to price in less cuts, wrote Duy. If the two-cut scenario doesn’t materialize this week, it may come by the June meeting, “or at least that market participants will price it as coming by June,” he added. “The risks at this moment are decidedly asymmetric.”

What Bloomberg Intelligence Says …

“Changes are likely to be incremental, though the knee-jerk reaction to a move higher in the 2024 dot may be quickly discounted if the 2025 dots are largely unchanged. …the market is sensitive to the end of next year dots, meaning rate markets may focus on 2025.”

— Ira Jersey, chief US interest-rate strategist

Instead of sweating over two or three reductions, investors shouldn’t lose the big picture that the Fed’s next move is a cut, not a hike, said Baylor Lancaster-Samuel, chief investment officer at Amerant Investments Inc. That means it’s time to buy bonds and take the interest-rate, or “duration” risk, in Wall Street parlance.

“You can debate the timing, but in our opinion, the Fed is still likely to cut sometime this year,” said Lancaster-Samuel. “In that environment, we think the level of rates does not have too much risk of ratcheting higher from here. So we believe the opportunity cost of not taking duration is higher than the risk of taking it.”

Options traders are less sanguine. On the heels of last week’s stronger-than-expected data on producer prices, traders rushed to buy hawkish protection for this year and next in options linked to the Secured Overnight Financing Rate, a measure which closely tracks the central bank policy rate.

“Higher inflation readings, coupled with outsize deficits, the potential for the Fed to remain on hold longer, lends itself to another move toward the 2023 yield highs,” said Gregory Faranello, head of US rates trading and strategy for AmeriVet Securities.

What to Watch

Economic data:

March 18: New York Fed services business activity; NFIB housing market index

March 19: Building permits; housing starts; TIC flows

March 20: MBA mortgage applications; FOMC meeting

March 21: Current account balance

March 21: Philadelphia Fed business outlook; initial jobless claims; S&P Global US manufacturing PMI; leading index; existing home sales

Fed calendar:

March 21: Vice Chair for Supervision Michael Barr

March 22: Chair Jerome Powell, Vice Chair Philip Jefferson and Governor Michelle Bowman at Fed Listens event; Barr; Atlanta Fed President Raphael Bostic

Bank of America shares have fallen 14% this year.Spencer Platt/Getty Images

Big banks are sitting on $650 billion of unrealized losses, Moody’s has estimated.

It’s a sign even Wall Street’s best-known names are feeling the heat from the Treasury-market rout.

Crashing bond prices sank Silicon Valley Bank earlier this year, and there may be more chaos to come.

Crashing bond prices sank Silicon Valley Bank in March — and there’s reason to believe that what triggered the California lender’s collapse may be haunting Wall Street again.

The brutal Treasury-market meltdown has hit some of the largest financial institutions hard, dragging down the share prices of big names such as Bank of America and fueling fears that the turmoil triggered by SVB’s bankruptcy may not be over just yet.

Here’s everything you need to know about unrealized losses, including why they’re dragging on bank stocks and whether they could trigger another financial crisis.

Unrealized losses

Treasury bonds — debt instruments the government issues to fund its spending — have been on a nightmarish run since the onset of the pandemic, with investors fretting about rising interest rates and the long-term viability of the US’s massive deficit.

As a result of that sell-off, some of the US’s biggest banks are now sitting on unrealized, or “paper,” losses worth hundreds of billions of dollars. That means the value of their bond holdings has plunged, but they’ve chosen to hold on rather than offload their investments.

Moody’s estimated last month that US financial institutions had racked up $650 billion worth of paper losses on their portfolios by September 30 — up 15% from June 30. The ratings agency’s data still doesn’t account for a hellish October where the longer-term collapse in bond prices spiraled into one of the worst routs in market history.

These “losses” are not the same as debt, however, which describes actual borrowings that need to be repaid.

Bank of America is the big lender worst affected by the crash in bond prices, having disclosed a potential $130 billion hole in its balance sheet last month.

The other “Big Four” banks — Citigroup, JPMorgan Chase, and Wells Fargo — have also racked up unrealized losses in the tens of billions, according to their second- and third-quarter earnings reports.

Another SVB-style crisis?

Silicon Valley Bank failed in March after disclosing a $1.8 billion loss on its own bond portfolio, triggering a run on deposits. Similarly, big banks’ huge unrealized losses are also sparking concern among Wall Street doom-mongers.

“‘Higher for longer’ is absurd baloney,” the market vet Larry McDonald said in a post on X Sunday, referring to the Fed signaling it would hold interest rates at about their current level well into 2024 in a bid to kill off inflation. “A 6% + Fed funds and Bank of America is near insolvency.”

It’s important to remember that BofA’s $130 billion losses are still unrealized. Unlike SVB, it isn’t officially in the red yet because it has not sold its bond holdings.

The bank’s chief financial officer, Alastair Borthwick, shrugged off the market’s worries on last month’s earnings call, pointing out that most of the bank’s fixed-income portfolio was low-risk government bonds it planned to hold until the debt expires.

“All of these are unrealized losses are on government-guaranteed securities,” he told reporters. “Because we’re holding them to maturity, we will anticipate that we’ll have zero losses over time.”

There’s still a possibility that spooked BofA customers will pull their money en masse, as they did with SVB — but that hasn’t happened. In fact, deposits are up after registering about 200,000 new accounts in the third quarter.

Some analysts also believe the worst of the Treasury-market rout is now over, with the Federal Reserve starting to signal that its tightening campaign is nearly done. Ten-year yields have softened in recent weeks, falling from 5% to 4.6% as of Tuesday.

Banks under pressure

That doesn’t mean the Big Four banks can afford to just dismiss the bond rout.

In a paper published earlier this year, researchers for the Kansas City Fed concluded that paper losses could still drag down a bank’s share price: “Unrealized losses can increase equity costs as investors’ perceptions of financial health deteriorate.”

That’s been happening this year, with three of the big four banks’ stocks sliding. Predictably, Bank of America has been worst affected, with its stock down 24% over the past year and 14% year-to-date.

“Worries over unrealized losses on sovereign bond holdings are also weighing on the US lenders, to again reflect concerns over rising interest rates and whether the US Federal Reserve will ultimately tighten policy by too much for too long,” AJ Bell’s Russ Mould said in a note last week.

Unrealized losses may not be about to trigger another financial crisis — but as long as bank stocks are down, they’ll remain a concern for Wall Street’s biggest names.

(Bloomberg) — Stocks rallied as investors reacted to the possible peak of the Federal Reserve’s historic tightening campaign and processed the latest major company earnings.

Most Read from Bloomberg

Rates-sensitive real estate stocks led the advance in Europe’s Stoxx 600 index, which is set for its longest winning streak since July. US equity futures pointed to an extension of Wednesday’s gains on Wall Street as Asian stocks headed for their biggest gain in almost four months.

Novo Nordisk A/S rose after reporting that third-quarter sales surged amid the frenzy for its blockbuster obesity and diabetes drugs. Shell Plc gained after accelerating the pace of share buybacks as its third-quarter profit rose. Apple Inc. headlines the roster of US earnings due later.

While the Fed left the door open to another increase after pausing Wednesday, officials hinted that a run-up in long-term Treasury yields reduces the impetus to tighten policy further. The Bank of England is likely to keep interest rates at the highest level since 2008 later Thursday, amid evidence that the UK economy, labor market and inflation are weakening.

“The Fed did not throw in the towel yesterday, but the changes in the speech are in line with a more moderate growth situation,” said Florian Ielpo, head of macro research at Lombard Odier Asset Management. “What transpires from the speech is essentially a first eyebrow raised at the real growth situation, which markets decided to take for a ‘bad news is good news’ message.”

The dollar weakened and Treasuries steadied after Wednesday’s sharp gains.

US yields were already heading lower prior to the Fed decision after the government announced plans to borrow slightly less than expected over the next three months, reassuring investors worried about a deluge of debt issuance. A gauge of US factory activity also came in below expectations, adding to concerns of an economic downturn.

In Asia, the yen extended its gains from Wednesday, while the South Korean won led emerging-market currencies higher.

Meanwhile, the rebound in the region’s stocks signaled relief among investors fretting over the expectation of higher-for-longer US rates and hikes continuing into 2024. Asian stocks lost more than 12% from the end of July through October.

Fed Chair Jerome Powell on Wednesday noted that financial conditions have “tightened significantly in recent months driven by higher, longer—term bond yields, among other factors.” He repeatedly said the committee was moving “carefully,” a wording that often has signaled a low likelihood of any immediate change in policy, while adding that risks to the outlook have become more two-sided as the tightening campaign nears its end.

US jobs data painted a mixed picture. There were more job openings than forecast, according to the latest JOLTS data, while ADP’s private payrolls figures showed fewer new roles than anticipated. Initial jobless claims figures will be released later Thursday.

In commodities, global benchmark Brent crude oil rose past $85 a barrel, after sliding around 5% over the previous three sessions.

Key events this week:

Eurozone S&P Global Eurozone Manufacturing PMI, Thursday

Bank of England interest rate decision. Governor Andrew Bailey holds news conference, Thursday

US factory orders, initial jobless claims, productivity, Thursday

Apple earnings, Thursday

China Caixin services PMI, Friday

Eurozone unemployment, Friday

US unemployment, nonfarm payrolls, Friday

Canada employment report, Friday

Here are some of the major moves in markets:

Stocks

The Stoxx Europe 600 rose 1.4% as of 8:52 a.m. London time

S&P 500 futures rose 0.5%

Nasdaq 100 futures rose 0.6%

Futures on the Dow Jones Industrial Average rose 0.3%

The MSCI Asia Pacific Index rose 1.4%

The MSCI Emerging Markets Index rose 1.6%

Currencies

The Bloomberg Dollar Spot Index fell 0.3%

The euro rose 0.3% to $1.0604

The Japanese yen rose 0.4% to 150.42 per dollar

The offshore yuan was little changed at 7.3321 per dollar

The British pound rose 0.1% to $1.2166

Cryptocurrencies

Bitcoin fell 0.4% to $35,306.23

Ether fell 1.3% to $1,831.95

Bonds

The yield on 10-year Treasuries declined one basis point to 4.72%

Germany’s 10-year yield declined five basis points to 2.72%

Britain’s 10-year yield declined eight basis points to 4.42%

Commodities

Brent crude rose 1.4% to $85.79 a barrel

Spot gold rose 0.2% to $1,987.46 an ounce

This story was produced with the assistance of Bloomberg Automation.

–With assistance from Winnie Hsu and Sagarika Jaisinghani.

(Bloomberg) — The interest rate that neither spurs nor slows the US economy has at least doubled in the aftermath of the pandemic, handing investors a reason to be nervous about buying bonds or stocks, according to the latest Bloomberg Markets Live Pulse survey.

Most Read from Bloomberg

Some 85% of 528 respondents reckon the so-called real neutral rate — which strips out the effect of inflation — has risen to around 100 basis points or higher, from estimates of about 50 basis points before Covid struck.

Federal Reserve Chair Jerome Powell said in March that “honestly, we don’t know” where the neutral rate lies. But if the resilient US economy has pushed it above what has prevailed historically, that adds to the case for the central bank to keep monetary policy tighter for longer — crimping the value of stocks and bonds.

Both asset classes have been getting battered of late as investors have absorbed the prospect of an extended period of higher interest rates. Ten-year Treasury yields briefly eclipsed 5% last week for the first time since 2007, fueling concern over technology-stock valuations in particular. Meanwhile, both the S&P 500 Index and the tech-heavy Nasdaq 100 entered a correction.

For 10-year Treasuries, survey participants have little expectation the pressure will ease. The maturity will likely end the year yielding 5%, according to the median forecast of respondents. More than 60% of poll participants say that both the S&P 500 and the Nasdaq 100 are overvalued, while some 15% estimate that valuations are stretched only for technology stocks.

The Nasdaq 100 will decline by as much as 10% this quarter, according to 45% of respondents. A fifth say it will slump more than that. Earlier in the year, enthusiasm surrounding artificial intelligence spurred investors to overlook rising interest rates, propelling the Nasdaq 100 about 35% higher in the first three quarters of the year. It’s now on track for its third straight monthly decline, something it hasn’t done in more than a year. And by one calculation, the technology complex is still overvalued by 10% as of the close on Friday.

The poll’s findings gel with a report from Bloomberg Economics that concluded the real neutral rate will climb to as much as 2.7% in the 2030s. In turn, according to the study, 10-year Treasury yields could settle somewhere between 4.5% and 5%.

As they did in December 2019, Fed officials estimate a long-run funds rate of 2.5% while assuming inflation of 2%, implicitly projecting a neutral real rate of 50 basis points. The neutral rate may have risen because of a host of factors, on top of the economy’s strength: Baby boomers are retiring and spending down their nest eggs, diminishing the supply of savings; China’s appetite for Treasuries is waning; and widening government deficits are increasing competition for investment capital.

What’s more, uncertainty about the future in the wake of the pandemic has spurred consumers to spend now and save later — a phenomenon known as high time preference. Essentially, that means consumers will seek higher interest rates to invest and forgo current spending, pushing the neutral rate higher.

A narrow majority of survey respondents are pessimistic about the implications of higher Treasury yields. This group projects that if yields stay above 5% for a quarter or longer, they would cause a hard landing, a scenario where the Fed’s actions to tame inflation trigger a recession. Some 47% say the economy would take it in stride.

The topic of elevated yields is likely to come up during Powell’s press conference after the central bank’s Nov. 1 policy decision, when officials are widely expected to hold rates steady at the highest in more than two decades. Investors will watch to see whether Powell comments on the Fed’s comfort level with the recent surge in yields and what that implies for the prospect of a soft landing.

Against the backdrop of elevated Treasury yields and the Fed’s message of higher for longer, almost 60% of survey respondents said they anticipate the dollar will be a stronger a month from now.

The MLIV Pulse survey of Bloomberg News readers on the terminal and online is conducted weekly by Bloomberg’s Markets Live team, which also runs the MLIV blog. Ven Ram is a cross-asset strategist for Bloomberg’s Markets Live. The observations are his own and not intended as investment advice. To subscribe for more MLIV Pulse surveys, click here.

Meanwhile, S&P 500 (^GSPC) futures were down 0.3% in the wake of the benchmark’s lowest close since May. Dow Jones Industrial Average (^DJI) futures traded flat.

Earnings are in the drivers seat for stocks, as investors punish megacaps whose third-quarter reports turned out more downbeat than hoped. Concerns are growing that valuations are too high in a world of surging Treasury yields, as the benchmark 10-year yield (^TNX) climbed back near 5% on Thursday.

While Meta’s (META) earnings beat on the top and bottom lines, its shares reversed initial gains after the Facebook parent warned geopolitical unrest could drag on its ad business. The flow of earnings resumes Thursday, with Amazon (AMZN), Intel (INTC), Ford (F) and Chipotle (CMG) the highlights on the docket.

“There’s real dispersion,” BlackRock’s Global CIO Rick Rieder said, noting Microsoft and Alphabet earnings. “We’re getting a series of conflicting signs around market. That’s why markets are so jumpy, so uncertain.”

In one positive development, Thursday’s third-quarter GDP reading came in hot with the US economy growing at its fastest pace in nearly two years.

The strong data comes despite the Federal Reserve’s higher for longer interest rate mantra, which has failed to constrain the American consumer. The Fed’s next interest rate decision is scheduled for Nov. 1

Other central banks are beginning to shift their monetary policy. On Thursday, the European Central Bank held interest rates steady for the first time in over a year following ten consecutive rate increases.

The ECB said it would hold its deposit rate at a record high 4%. The bank maintained its previous guidance of steady policy moving forward.

A

GDP: US economy grows 4.9% amid strong consumer spending

The US economy grew at its fastest pace in nearly two years during the past three months as consumers stepped up their spending despite a high interest rate environment.

The Bureau of Economic Analysis’s advance estimate of third quarter US gross domestic product (GDP) showed the economy grew at an annualized pace of 4.9% during the period, faster than consensus forecasts. Economists surveyed by Bloomberg estimated the US economy grew at an annualized pace of 4.5% during the period.

The reading came in higher than second quarter GDP, which was revised down to 2.1%.

The GDP release highlights the resilience of the US consumer despite ongoing concerns of a slowdown. But many economists see this as the high water mark for economic growth before the credit tightening induced by the Federal Reserve’s interest rate hikes and the recent rise in bond yields grabs hold of business development and consumer spending.

Wall Street stocks were on track Thursday to add to the previous day’s sharp losses, as investors looked ahead to fresh earnings releases.

Futures on the Dow Jones Industrial Average (^DJI) were down 0.41%, or 136 points, while S&P 500 (^GSPC) futures shed 0.67%. Contracts on the tech-heavy Nasdaq 100 (^NDX) were 0.95% lower.

NEW YORK (Reuters) – Relentless selling of U.S. government bonds has brought Treasury yields to their highest level in more than a decade and a half, roiling everything from stocks to the real estate market.

The yield on the benchmark 10 year Treasury – which moves inversely to prices – briefly hit 5% late Thursday, a level last seen in 2007. Expectations that the Federal Reserve will keep interest rates elevated and mounting U.S. fiscal concerns are among the factors driving the move.

Because the $25-trillion Treasury market is considered the bedrock of the global financial system, soaring yields on U.S. government bonds have had wide-ranging effects. The S&P 500 is down about 7% from its highs of the year, as the promise of guaranteed yields on U.S. government debt draws investors away from equities. Mortgage rates, meanwhile, stand at more than 20-year highs, weighing on real estate prices.

“Investors have to take a very hard look at risky assets,” said Gennadiy Goldberg, head of U.S. rates strategy at TD Securities in New York. “The longer we remain at higher interest rates, the more likely something is to break.”

Fed Chairman Jerome Powell on Thursday said monetary policy does not feel “too tight,” bolstering the case for those who believe interest rates are likely to stay elevated.

Powell also nodded to the “term premium” as a driver for yields. The term premium is the added compensation investors expect for owning longer-term debt and is measured using financial models. Its rise was recently cited by one Fed president as a reason why the Fed may have less need to raise rates.

Here is a look at some of the ways rising yields have reverberated throughout markets.

Higher Treasury yields can curb investors’ appetite for stocks and other risky assets by tightening financial conditions as they raise the cost of credit for companies and individuals.

Elon Musk warned that high interest rates could sap electric-vehicle demand, which knocked shares of the sector on Thursday. Tesla’s shares closed the day down 9.3%, as some analysts questioned whether the company can maintain the runaway growth that has for years set it apart from other automakers.

With investors gravitating to Treasuries, where some maturities currently offer far above 5% to investors holding the bonds to term, high-dividend paying stocks in sectors such as utilities and real estate have been among the worst hit.

The U.S. dollar has advanced an average of about 6.4% against its G10 peers since the rise in Treasury yields accelerated in mid-July. The dollar index, which measures the buck’s strength against six major currencies, stands near an 11-month high. A stronger dollar helps tighten financial conditions and can hurt the balance sheets of U.S. exporters and multinationals. Globally, it complicates the efforts of other central banks to tamp down inflation by pushing down their currencies. For weeks, traders have been watching for a possible intervention by Japanese officials to combat a sustained depreciation in the yen, down 12.5% against the dollar this year.

“The correlation of the USD with rates has been positive and strong during the current policy tightening cycle,” BofA Global Research strategist Athanasios Vamvakidis said in a note on Thursday.

The interest rate on the 30-year fixed-rate mortgage – the most popular U.S. home loan – has shot to the highest since 2000, hurting homebuilder confidence and pressuring mortgage applications. In an otherwise resilient economy featuring a strong job market and robust consumer spending, the housing market has stood out as the sector most afflicted by the Fed’s aggressive actions to cool demand and undercut inflation.

U.S. existing home sales dropped to a 13-year low in September.

As Treasury yields surge, credit market spreads have widened with investors demanding a higher yield on riskier assets such as corporate bonds. Credit spreads blew out after a banking crisis this year, then they narrowed in subsequent months.

The rise in yields, however, has taken the ICE BofA High Yield Index near a four-month high, adding to funding costs for prospective borrowers.

Volatility in U.S. stocks and bonds has bubbled up in recent weeks as expectations have shifted for Fed policy. Anticipation of a surge in U.S. government deficit spending and debt issuance to cover those expenditures has also unnerved investors.

The MOVE index, measuring expected volatility in U.S. Treasuries, is near its highest in more than four months. Volatility in equities has also picked up, taking the Cboe Volatility Index to a five-month peak.

(This story has been refiled to add the dropped word ‘briefly’ in paragraph 2)

(Reporting by Saqib Iqbal Ahmed; Writing by Ira Iosebashvili; Editing by Stephen Coates)